Correlated multi-asset portfolio

optimisation

with transaction

cost

Abstract

We employ perturbation analysis technique to study multi-asset portfolio optimisation with transaction cost. We allow for correlations in risky assets and obtain optimal trading methods for general utility functions. Our analytical results are supported by numerical simulations in the context of the Long Term Growth Model.

1 Introduction

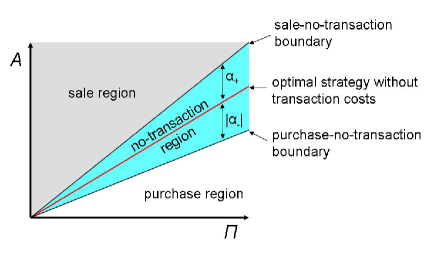

In recent years, the study of portfolio optimisation under non-zero transaction cost has received its due attention (Davis & Norman 1990; Atkinson & Wilmott 1995; Morton & Pliska 1995; Akian et al. 1996; Atkins & Dyl 1997; Atkinson & Al-Ali 1997; Atkinson et al. 1997; Atkinson & Mokkhavesa 2001, 2003, 2004; Mokkhavesa & Atkinson 2002; Chellathurai & Draviam 2005). In the literature, it is found that the incorporation of transaction fees into the model introduces a no-transaction region around the original optimal curve, surrounded by purchase and sale regions (cf. figure 1). Most of previous work focused on having only one risky asset (stock) and one risk-free asset (bond), except the study by Atkinson and Mokkhavesa (2004) in which portfolio with multiple risky assets is analysed. In this work, the authors are able to obtain the optimal investment strategy with the assumption that the risky assets are uncorrelated. Here, we go beyond this restriction and consider correlated risky assets. By assuming that the purchase and sale boundaries are of an equal distance away from the optimal curve, we obtain analytical expressions for the optimal trading strategy for general utility functions. We further support our analytical results with numerical simulations in the context of the Long Term Growth Model.

The plan of the paper is as follows: In §2, we will consider portfolio optimisation without transaction costs, thereby introduce the dynamic programming method employed. We will then consider trading with transaction cost in §3. The details of our simulation method in support of our analytical results are given in 4. For reference, the expressions for the derivatives of the value function in terms of the expansion parameter are given in 4.

2 Trading without transaction costs

We consider a market with investment opportunities on stocks and a risk free bond, and we let , and be the values held in stock , the value held in risk free bond and the total wealth at time respectively. We assume that follows a geometric Brownian motion with growth rate and volatility , and the risk free bonds, , compounds continuously with risk free rate . The volatilities , growth rates and interest rate are assumed to be constant. Cash generated or needed from the purchase or sale of stocks is immediately invested or withdrawn from the risk free bonds. In the absence of transaction costs, the problem is easily solved without recourse to perturbation analysis and this section will serve to familiarise the readers with the use of dynamic programming method in this optimisation problem.

The market model equations are represented by the followings:

| (1) |

where , , are Weiner processes whose correlations, , are assumed constant. At time , an investor has an amount of resources and the problem is to allocate investments over the time horizon , so as to maximise the following expectation value:

The functions and can represent anything from utility to the year end bonus of the trader. For example, if we assume that and , then the opimisation problem constitutes the Long Term Growth Model and the goal would then be to optimise the logarithm of the final wealth. To make financial sense, we will assume that the utility functions are increasing and concave down, i.e.,

| , | (2) | ||||

| , | (3) |

We restate the optimisation problem in dynamic programming form by first defining the optimal expected value function, :

| (4) |

We now apply the Bellman Principle and Itô’s Lemma to the above value function to obtain the following Hamilton-Bellman-Jacobi equation (Kamien 1991):

| (5) | |||||

with the boundary condition . In the above equation, is the standard covariance matrix, and act as the control parameters in the context of dynamic programming.

In matrix notation, we can rewrite equation (5) as

| (6) |

where symbols without an index denote the corresponding vectors (e.g. ). We have also introduced a new vector , which is defined to be .

By differentiating equation (6) with respect to , one obtains as the solution to the HBJ Equation:

| (7) |

Therefore, the optimal portfolio corresponds to:

| (8) |

2.1 Example: the Long Term Growth Model

In this model, our aim is to maximize . The value function is thus

| (9) |

such that . This boundary condition together with the differential equation obtained by substituting equation (8) into equation (6) implies that

| (10) |

The optimal portfolio from equation (8) is therefore given by:

| (11) |

For the case of having two-risky assets, the optimal portfolio corresponds to having with , and with . By the Itô’s lemma, we have

| (12) |

where

| (13) |

The optimal expected payoff in this model is therefore:

| (14) |

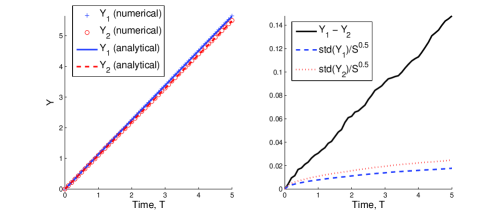

We now consider a two-risky-asset market model. With the model parameters given in 4, the optimal stock holdings in this case are and (cf. equation (11)). The performances of this optimal trading strategy based on our analytical expression in equation (14) and our numerical simulations (cf. 4 for details of simulation method) are given in figure 2. If the correlation in the risky assets is ignored, the optimal portfolio becomes: and . The corresponding performance is shown to be sub-optimal in figure 2.

3 Trading with transaction cost

We will now include transaction cost into our discussion. As the transaction cost usually amounts to a small percentage () of the total transaction, we employ perturbation method to analyse this optimisation problem with the transaction cost as the expansion parameter. By keeping track of the first few lowest order terms, we will derive the first order correction to the optimal trading strategy determined under no transaction cost.

We assume that the transaction fee is proportional to the asset under transaction and the proportionality constant is denoted by . Note that we again define the total wealth, , as

| (15) |

The market model equations in this case are:

| (16) | |||||

where and represent the cumulative purchase and cumulative sale of assets during the time interval . The optimal expected value function is as before:

| (17) |

and the corresponding HBJ equation is (Kamien 1991):

| (18) | |||||

Here, and are the control parameters from the dynamics programming perspective.

3.1 Three regions

By isolating terms involving or separately in equation (18), we arrive at three separate cases:

Case 1:

and .

In this case, the maximum in equation (18) is achieved by choosing and , which is equivalent to selling at maximum rate.

Case 2:

and .

In this case, the maximum is achieved by choosing and , which is equivalent to buying at maximum rate.

Case 3:

and .

In this case, the maximum is achieved by choosing and , which indicates that no transactions are needed.

We note that it is not possible to have and be both greater than zero as we assume that is an increasing function of .

This can be broadly interpreted as more wealth cannot decrease the value function from the trader’s point of view.

With the above consideration, the optimal trading strategy can be seen to be partitioned into three separate regions: sale, purchase and no-transaction regions (cf. figure 1). In other words, if the portfolio is in the sale (purchase) region, the optimal strategy is to sell (buy) stocks until the portfolio is at the no-transaction region boundary, and thus bring the portfolio back into the no-transaction region. Inside the no-transaction region, and are identically zero and hence satisfies the HBJ equation with .

3.2 Continuity and optimality assumptions

To make progress with our analysis, we will assume that the optimal value function, , is everywhere continuous and that its derivatives are also continuous. We call the latter the optimality assumption. The validities of these assumptions are discussed in Morton & Pliska (1996) and Whalley & Wilmott (1997).

We now restrict ourselves to one risky asset for notational convenience. Suppose that the point is inside the sale region, when a very small quantity of assets, is sold, the risk-free bond increases by the amount , while the whole portfolio value is reduced by . As , the value function must be the same after the sale (the continuity assumption), we therefore have

| (19) | |||||

| (20) | |||||

| (21) |

By a similar argument, we can conclude that inside the purchase region, we have

| (22) |

By applying again the same argument to equations (21) and (22) with the use of the optimality assumption, we have that in the sale region and at the sale-no-transaction boundary:

| (23) |

and in the purchase region and at the purchase-no-transaction boundary:

| (24) |

Inside the no-transaction region, the value function, , must satisfy equation (18) with , i.e.,

| (25) | |||||

These equalities are to be supplemented by the boundary condition at : .

3.3 Perturbative expansion and order matching

We now redefine the coordinate as , where is the optimal value of stock held when tends to zero, and introduce the modified value function, , such that . In 4, we display the various derivatives of in terms of and .

We further expand in powers of as:

| (26) | |||||

The reason for expanding and in powers of is out of necessity and has previously been studied in the literature (Atkinson & Wilmott 1995, Rogers 2004).

We will from now on keep track of the expression up to the first non-trivial correction: . By matching the orders of , equations (21) and (22) at the sale-no-transaction boundary (corresponds to the + sign in ) and at the purchase-no-transaction boundary (corresponds to the sign in ) become:

| (27) | |||||

| (28) | |||||

| (29) |

and equations (23) and (24) become:

| (30) | |||||

| (31) | |||||

| (32) |

Inside the no-transaction region, after expanding according to equation (26) and collecting terms of the same order in , we arrive at the following conditions:

-

1.

Equation: , where is an operator defined as with

(33) -

2.

Equation: .

-

3.

Equation: , where is an operator defined as

(34) -

4.

Equation: .

-

5.

Equation: .

Combining the equation with equations (27) and (30) when , one finds that is independent of . Combining the with equations (27) and (30) when shows that is independent of . Combining the equation with equations (27) and (30) when shows that is independent of . The equation together with equations (28) and (31) imply that is independent of . In summary, by matching the coefficients of the various orders in , we determine that are independent of .

Without loss of generality, we focus on the first asset and let denotes the width of the purchase-no-transaction boundary, and the width of the sale-no-transaction boundary (cf. figure 1). From equations (29) and (30), we find that at the boundary :

| (35) | |||||

| (36) |

and at boundary , we have:

| (37) | |||||

| (38) |

As we have established that and are independent of , with the equation, we can conclude that has the following general form:

| (39) |

where denotes the set . In other words, is a polynomial in with a degree of at most four. We now make the simplifying assumption that . This is equivalent to saying that the transaction (buy or sell) boundaries are of the same distance away from the unperturbed optimal curve. We note that this assumption is proved to be true in the case of having uncorrelated risky assets (Atkinson and Mokkhavesa 2004). With the assumption of equal magnitude, we can conclude that at the boundaries by subtracting equation (36) from equation (38). In particular, we have

| (40) |

By summing equations (35) and (37), we can further determine that at the boundaries. By subtracting equation (35) from equation (37), we conclude that satisfies:

| (41) |

Substituting equation (40) into equation (41), we obtain

| (42) |

To calculate , we invoke the equation: By comparing the coefficient of the term on both sides, we find that:

| (43) |

So finally, can be expressed as:

| (44) |

where is the optimal value function when transaction cost is absent.

In general, denoting the trading boundary for stock by , we have the following general expression for the widths of the trading boundaries:

| (45) |

For any financial model where is known, the above equation together with equation (8) provides an analytical description of the optimal trading strategy. This is the main result of this paper.

3.4 Example: the Long Term Growth Model

According to equations 10 and 11:

| (46) | |||||

| (47) |

Combining these with equation (33), we have

| (48) | |||||

| (49) |

The width of the boundary for stock is therefore (cf. equation (45)):

| (50) |

If the risky assets are uncorrelated, the expression above coincides with the result of Atkinson & Mokkkhavesa (2004).

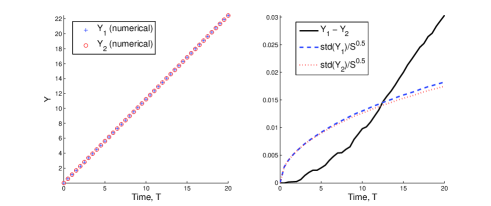

We now employ this optimal trading strategy to the two-risky-asset market considered before. The optimal curve corresponds to: and (cf. equation (11)), and according to equation (50), the boundaries widths are: and . The performance of this strategy is shown in figure 3. If we ignore the correlation between the risky assets in calculating the boundary widths, and become and respectively. The trading strategy employing these boundaries together with the same optimal curve as before is shown in figure 3 and can be seen to be sub-optimal, albeit the difference is small.

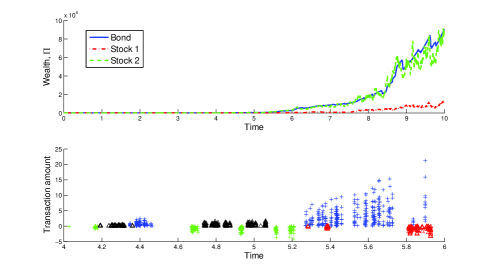

In figure 4, the portfolio’s temporal evolution of a particular simulation is shown together with the transaction amounts displayed.

4 Conclusion

In conclusion, we have employed perturbation method to study multi-asset optimisation for arbitrary utility functions. By making the assumption that the sale and purchase boundaries are of the same distance away from the optimal curve, we arrived at an analytical expression for the optimal trading strategy. We have also supported our analytical results with numerical simulations in the context of the long term growth model.

Details of numerical simulation method

We consider a portfolio consisting of two risky assets and one risk-free asset. The values in the bond and risky assets are updated as follows:

| (51) | |||||

| (52) | |||||

| (53) |

where and are random numbers drawn from the normal distribution with zero mean and a standard deviation of one, such that the correlation coefficient between and is .

In the case of trading without transaction costs, the portfolio is updated after each iteration according to equation (11). When transaction costs are present, trading only occurs when the value of the risky assets are outside of the no-transaction region (cf. figure 1), i.e., if

| (54) |

When such an event occur, the portfolio is adjusted such that is moved back to the nearest boundary and the cost of transaction is subtracted from the wealth. For example, if , then the portfolio is adjusted so that:

| (55) | |||||

| (56) |

The simulations always start with a total wealth of 1 at the optimal portfolio distribution and the set of parameters employed are: and .

Change of variables Letting with , we have the following expressions for the derivative of in terms of and .

| (57) | |||||

| (58) | |||||

| (59) | |||||

| (60) | |||||

| (61) | |||||

| (62) |

Acknowledgements

We would like to thank Colin Atkinson and Michael Giles for valuable comments. SLL thanks the Croucher Foundation, CFL thanks the Glasstone Trust (Oxford) and Jesus College (Oxford), for financial support.

References

- [1]

- [2] Akian, M., et al. 1996 On an investment-consumption model with transaction costs. SIAM Journal on Control and Optimization 34, 329–364.

- [3]

- [4] Atkins, A. B. & Dyl, E. A. 1997 Transactions costs and holding periods for common stocks. The Journal of Finance 52, 309–325.

- [5]

- [6] Atkinson, C. & Al-Ali, B. 1997 On an investment-consumption model with transaction costs: an asymptotic analysis. Applied Mathematical Finance 4, 109–133.

- [7]

- [8] Atkinson, C. & Mokkhavesa, S. 2003 Intertemporal portfolio optimization with small transaction costs and stochastic variance. Applied Mathematical Finance 10, 267–302.

- [9]

- [10] Atkinson, C. & Mokkhavesa, S. 2004 Multi-asset portfolio optimization with transaction cost. Applied Mathematical Finance 11, 95–123.

- [11]

- [12] Atkinson, C. & Wilmott, P. 1995 Portfolio management with transaction costs: An asymptotic analysis of the morton and pliska model. Mathematical Finance 5, 357–367.

- [13]

- [14] Atkinson, C. & Mokkhavesa, S. 2001 Towards the determination of utility preference from optimal portfolio selections. Applied Mathematical Finance 8, 1–26.

- [15]

- [16] Atkinson, C., et al. 1997 Portfolio management with transaction costs. Proc. R. Soc. A 453, 551–562.

- [17]

- [18] Chellathurai, T. & Draviam, T. 2005 Dynamic portfolio selection with nonlinear transaction costs. Proc. R. Soc. A 461, 3183–3212.

- [19]

- [20] Davis, M. H. A. & Norman, A. R. 1990 Portfolio selection with transaction costs. Mathematics of Operations Research 15, 676–713.

- [21]

- [22] Kamien, M. I. & Schwartz, N. L. 1991 Dynamic Optimization: The Calculus of Variations and Optimal Control in Economics and Management, 2nd edn. Amsterdam, The Netherlands: Elsevier Science.

- [23]

- [24] Law, S. L. 2005 Financial Optimization Problems. DPhil thesis, Oxford University.

- [25]

- [26] Merton, R. C. 1992 Continuous-Time Finance. New York, NY: Wiley-Blackwell.

- [27]

- [28] Mokkhavesa, S. & Atkinson, C. 2002 Perturbation solution of optimal portfolio theory with transaction costs for any utility function. IMA J. Management Math. 13, 131–151.

- [29]

- [30] Morton, A. J. & Pliska, S. R. 1995 Optimal portfolio management with fixed transaction costs. Mathematical Finance 5, 337–356.

- [31]

- [32] Rogers, L. C. G. 2004 Why is the effect of proportional transaction costs ?. In Mathematics of Finance (eds Yin, G. & Zhang, Q.), pp. 303–308. Oxford, UK: Oxford University Press.

- [33]

- [34] Whalley, A. E. & Wilmott, P. 1997 An asymptotic analysis of an optimal hedging model for option pricing with transaction costs. Mathematical Finance 7, 307–324.

- [35]