10cm

Strong confidence intervals for autoregression

Abstract

In this short preliminary note I apply the methodology of game-theoretic probability to calculating non-asymptotic confidence intervals for the coefficient of a simple first order scalar autoregressive model. The most distinctive feature of the proposed procedure is that with high probability it produces confidence intervals that always cover the true parameter value when applied sequentially.

1 Introduction

Game-theoretic probability (see, e.g., [6], with the basic idea going back to Ville [7]) provides a means of testing probabilistic models. In this note the game-theoretic methodology is extended to statistical models; it will be demonstrated on the first-order scalar autoregressive model

| (1) |

without the intercept term, with constant , and with independent innovations .

We will be interested in procedures for computing, for each , a confidence interval for given . Let us fix a confidence level , and let be the true parameter value. The usual procedures are “batch”, in that they only guarantee that with high probability for a fixed . It is usually true that, when they are applied sequentially, the intersection is empty with probability one. Our goal is to guarantee that

| (2) |

with probability at least .

Analogously to the usual classification of the limit theorems of probability theory into “strong” (involving the conjunction over all ) and “weak” (applicable to individual ), let us call such confidence intervals strong. In particular, confidence intervals satisfying (2) with probability at least will be called strong -confidence intervals. Accordingly, confidence intervals produced by the standard procedures will be referred to as weak; weak -confidence intervals satisfy with probability at least for each individual . (This probability is sometimes required to be precisely , but we will only consider the “conservative” definitions.)

To achieve the goal (2), for each possible value of the parameter we construct random variables , , that form a nonnegative martingale under the probability measure corresponding to the probabilistic model (1) with the given . It will also be true that ; such sequences (nonnegative martingales starting from 1) will be called martingale tests. We can then set

(assuming that the set on the right-hand side is an interval, which it will be in our case). The special case

(due to Ville; see, e.g., [7], p. 100, or [6], (2.12)) of Doob’s inequality shows that (2) will indeed be true with probability at least .

2 Derivation of strong confidence intervals

If the true probability density of (conditional on the past) is

and we want to reject the hypothesis

the best, in many respects111Cf., e.g., the nonnegativity of the Kullback–Leibler divergence, Neyman–Pearson lemma, and the optimality property of the probability ratio test in sequential analysis., martingale test is the likelihood ratio sequence with the relative increments

The product over is the martingale test itself:

| (3) |

where

and

To get rid of the parameter , let us integrate (3) over the probability distribution on the s:

(where I made the substitution ). Now the formula

gives

| (4) |

To find the confidence intervals corresponding to (4), fix a confidence level . The -confidence interval corresponding to (4) is defined as the set of s satisfying

Solving this in gives the confidence interval

| (5) |

Notice that, in the stationary case , where has the order of magnitude , the size of the confidence interval (5) is as . This is worse that the usual iterated-logarithm behaviour () but agrees with [4], Theorem 2.5 (although the latter result is just an upper bound). One can speculate that, in the stationary case, the behaviour will be recovered if the is replaced by a probability distribution that is more concentrated around , as in Ville’s [7] proof of the law of the iterated logarithm (see also [6], Chapter 5).

Most of the terms in the confidence interval (5) are familiar from the literature (which, however, mainly covers the case of weak confidence intervals). The centre of the interval is just the least-squares estimate of from the given sample. The statistic

| (6) |

(for a fixed sample size ) has been studied extensively. In describing the known results I will follow [2]. Mann and Wald [3] showed that is asymptotically when . Anderson [1] extended this to the case . White [8] and Rao [5] showed that, in the case , converges in distribution to

| (7) |

where is a standard Brownian motion.

Suppose, for concreteness, that (6) is asymptotically . The central asymptotic weak confidence interval for based on the statistic given after the “” in (6) will be different from (5) in that

| (8) |

will be replaced by the upper -quantile of , essentially by

for a small . This is close to the first addend on the right-hand side of (8), and so the second addend represents the price that we are paying for our confidence intervals being strong.

3 Empirical results

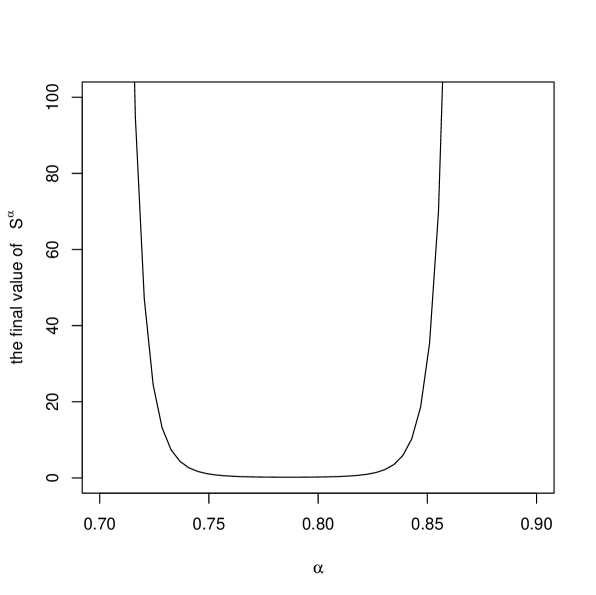

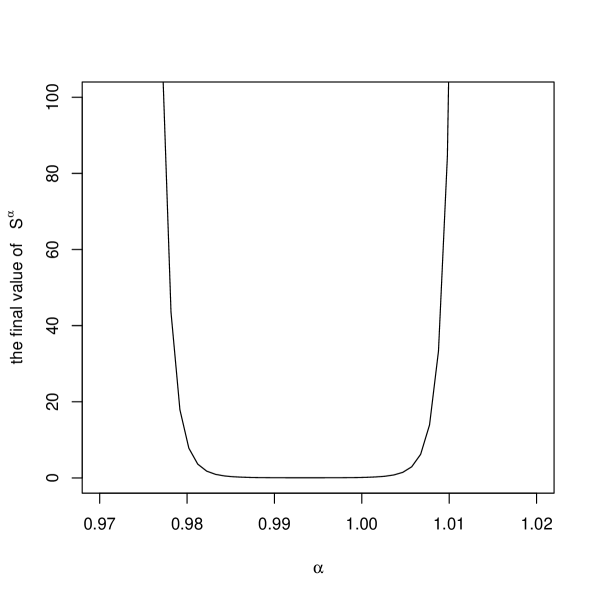

To test the test martingales (4) empirically, I generated from the model (1) with and . The case illustrates the stationary behaviour (), and the “unit-root” case is intermediate between the stationary and “explosive” () behaviour. Tables 1 and 2 give the approximate weak central -confidence intervals based on the above approximations for (normal for and (7) for ) and the strong -confidence intervals computed from (5).

| Type of the interval | Confidence interval | Its width |

|---|---|---|

| Weak (approximate) | ||

| Strong |

| Type of the interval | Confidence interval | Its width |

|---|---|---|

| Weak (approximate) | ||

| Strong |

The intuition behind the value of in (5) is that it should be of the same order of magnitude as the expected width of the confidence interval (since represents the order of magnitude of the distance to the bulk of that we are competing with). It is taken as in the tables, but the results will not be drastically different if , which is intuitively more “neutral”, is chosen: e.g., the width in Table 1 would go up to , and the width in Table 2 would go up to .

4 Directions of further research

These are some possible areas in which the methods of martingale testing could be applied:

- Online testing of statistical models.

-

When the strong confidence interval becomes empty, the statistical model can be rejected. Of course, efficient testing of statistical models will require different martingale tests: it will not be sufficient to consider, as in this note, different values of parameters as alternatives.

- Prediction.

-

In the simplest case, the prediction interval at step might be computed as the union of the prediction intervals corresponding to all .

- Alternative assumptions about innovations.

-

For example, the assumption that have zero medians (conditional on the past) might lead to feasible statistical procedures.

Acknowledgments

I am grateful to Bent Nielsen, Clive Bowsher, David Hendry, and Jennifer Castle for useful discussions. This work was partially supported by EPSRC (grant EP/F002998/1), MRC (grant G0301107), and the Cyprus Research Promotion Foundation.

References

- [1] T. W. Anderson. On asymptotic distributions of estimates of parameters of stochastic difference equations. Annals of Mathematical Statistics, 30:676–687, 1959.

- [2] N. H. Chan and Ching Zong Wei. Asymptotic inference for nearly nonstationary AR(1) processes. Annals of Statistics, 15:1050–1063, 1987.

- [3] H. B. Mann and Abraham Wald. On the statistical treatment of linear stochastic difference equations. Econometrica, 11:173–220, 1943.

- [4] Bent Nielsen. Strong consistency results for least squares estimators in general vector autoregressions with deterministic terms. Econometric Theory, 21:534–561, 2005.

- [5] M. M. Rao. Asymptotic distribution of an estimator of the boundary parameter of an unstable process. Annals of Statistics, 6:185–190, 1978. Correction: 8:1403, 1980.

- [6] Glenn Shafer and Vladimir Vovk. Probability and Finance: It’s Only a Game! Wiley, New York, 2001.

- [7] Jean Ville. Etude critique de la notion de collectif. Gauthier-Villars, Paris, 1939.

- [8] J. S. White. The limiting distribution of the serial correlation coefficient in the explosive case. Annals of Mathematical Statistics, 29:1188–1197, 1958.