Information Flow between Composite Stock Index and Individual Stocks

Abstract

We investigate the strength and the direction of information transfer in the U.S. stock market between the composite stock price index of stock market and prices of individual stocks using the transfer entropy. Through the directionality of the information transfer, we find that individual stocks are influenced by the index of the market.

keywords:

transfer entropy , information flow , econophysics , stock marketPACS:

05.45.Tp , 89.65.Gh , 89.70.+c,

1 Introduction

Recently, economy has become an active research area for physicists. Physicists have attempted to apply the concepts and methods of statistical physics, such as the correlation function, multifractal, spin models, complex networks, and information theory to study economic problems [1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17, 18].

From the economic system, many empirical data reflecting the economic conditions can be obtained. Among them the time series of composite stock price index is one of the best data reflecting economics conditions well. The index data is used to analyze and predict the perspective of markets. The scientific interest in studying financial markets stems from the fact that there is a large amount of reasonably well defined data.

Information is an important keyword in analyzing the market or in estimating the stock price of a given company. It is quantified in rigorous mathematical terms [19], and the mutual information, for example, appears as meaningful choice replacing a simple linear correlation even though it still does not specify the direction. The directionality, however, is required to discriminate the more influential one between correlated participants, and can be detected by the transfer entropy [20].

In many case, traders in the stock market refer to the index to invest in stocks. Therefore, we can guess that prices of stocks is affected by the composite stock index of the market. However, No attempt to measure the influence of index quantitatively has been accomplished, while it is found evident that the interaction therein is highly nonlinear, unstable, and long-ranged from many previous research on econophysics using financial time series. Schreiber [20] introduced the transfer entropy which measures dependency in time between two variables. We focus quantitatively on the direction of information flow between the index data and the price of individual companies using the method of the transfer entropy. This concept of the transfer entropy has been already applied to the analysis of financial time series by Marschinski and Kantz [21]. They calculated the information flow between the Dow Jones and DAX stock indexes and obtained conclusions consistent with empirical observations. While they examined interactions between two huge markets, we construct its internal structure between stock index and individual stocks.

2 Transfer entropy

The transfer entropy which measures directionality of variable with respect to time has been recently introduced by Schreiber [20] based on the probability density function (PDF). Let us consider two discrete and stationary process, and . The transfer entropy relates previous samples of process and previous samples of process is defined as follows:

| (1) |

where and represent the discrete states at time of and , respectively. and denotes and dimensional delay vectors of two time consequences and , respectively. The joint PDF is the probability that the combination of , and have particular values. The conditional PDF and are the probability that has a particular value when the value of previous samples and are known and are known, respectively.

The transfer entropy with index measures how much the dynamics of process influences the transition probabilities of another process . The reverse dependency is calculated by exchanging and of the joint and conditional PDFs. The transfer entropy is explicitly asymmetric under the exchange of and . It can thus give the information about the direction of interaction between two time series.

The transfer entropy is quantified by information flow from to . The transfer entropy can be calculated by subtracting the information obtained from the last observation of only from the information about the latest observation obtained from the last joint observation of and . This is the main concept of the transfer entropy. Therefore, the transfer entropy can be rephrased as

| (2) |

where

| (3) | |||||

| (4) |

3 Empirical data analysis

We analyze daily records of the S&P 500 index (GSPC), Dow Jones index (DJI) and stock price of selected 125 individual companies. The dataset consists of about 4,000 simultaneously recorded data points during the period June 1, 1983 to May 31, 2007. We use logarithmic price difference as follows:

| (5) |

where means index or stock price of n-th trading day. The first step in analysis for the transfer entropy is to discretize the time series by some coarse graining. Quite often, statistical studies which use the entropy assume that the variables of interest are discrete, or may be discretized in some straightforward manner. We partitioned the real value into discretized price change . In the concrete, for (decrease), for (intermediate), for (increase) are chosen.

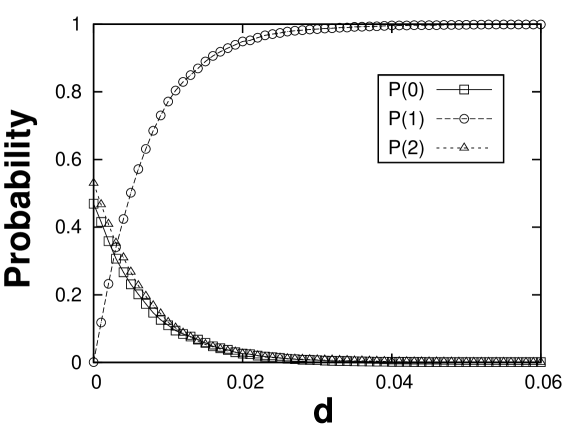

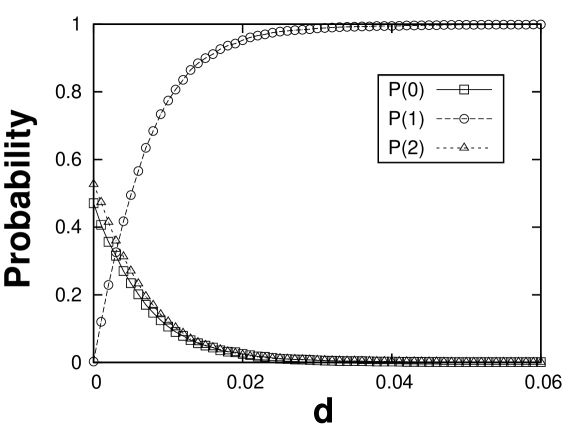

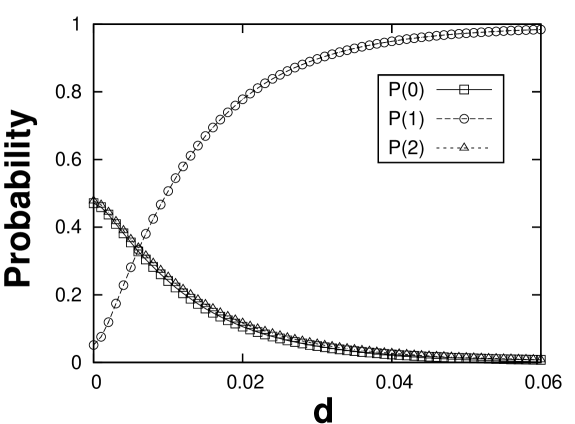

When data is discretized, it is important to determine the size of because probability of each state is varied by . In case of very small , most of return value is belonged not to the intermediate state but to the increase or decrease states. Therefore, the data can be regarded as two-states practically. Also, when is very high, the greater part of return is fallen under intermediate state. So data is able to be considered in one-state system. As the value of , the range of intermediate state, is changed, the probability of each state is varied. Fig. 1 represents the probability of each state. The probabilities of increase and decrease states are almost same. Therefore, the probability of intermediate state increases as is increasing, while those of increase and decrease are reduced. Around , the probabilities of three states are approximately same for both of composite stock index. On the other hand, individual stocks represent the same probability at . The reason, why the value of which makes the same probability for composite stock index is not same to that for individual stock prices, is that index usually does not change its value abruptly in a day compare with individual stocks, because composite stock index is average or weighted average of individual stock prices.

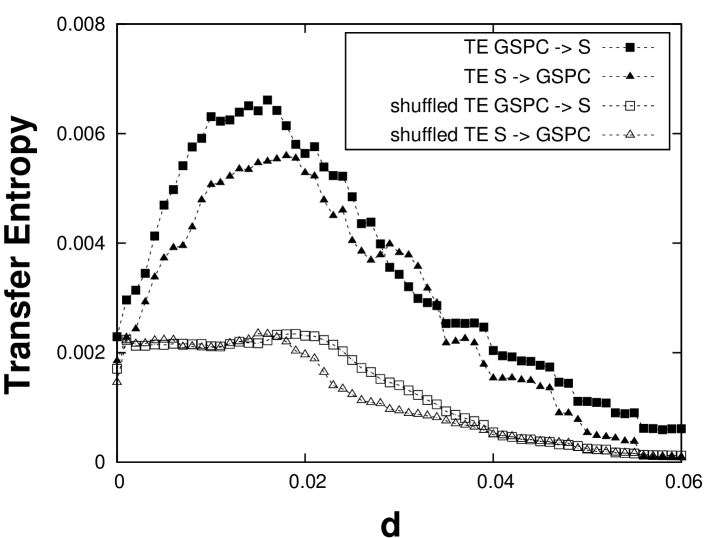

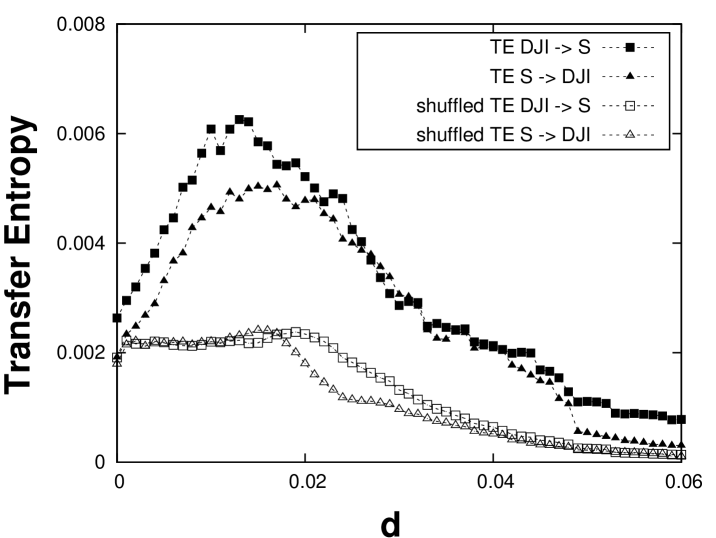

Fig. 2 shows the mean value of the transfer entropy between composite stock index () and price of individual stocks () for the GSPC and the DJI as a function of with and . The transfer entropy from the stock index to the stock prices, , is almost higher than that from the stock prices to the stock index, . At , discretized data is fallen into two-states because the intermediate state is disappeared. Therefore, it has smaller value of the transfer entropy compared with that for three states. As is increasing, the number of state turns to three, and the transfer entropy is maximized around . Above which makes maximized the transfer entropy, the larger , the larger probability of the intermediate state. Moreover, above about 0.02, for the index goes close to 1. Therefore, the transfer entropy is deceasing and finally goes to 0 because all data is fallen into the intermediate state at very large .

Open squares () and triangles () of Fig. 2 represent the transfer entropy from shuffled data. As expected, the transfer entropy from shuffled data is smaller than that from the original data, and also the difference between and is disappeared below and above in both indices. In the range from around 0.02 to around 0.04, number of states for the indices is 1, while it is still 3 for individual stocks. Therefore, this difference between them triggers discrepancy of the transfer entropy between the indices and stocks.

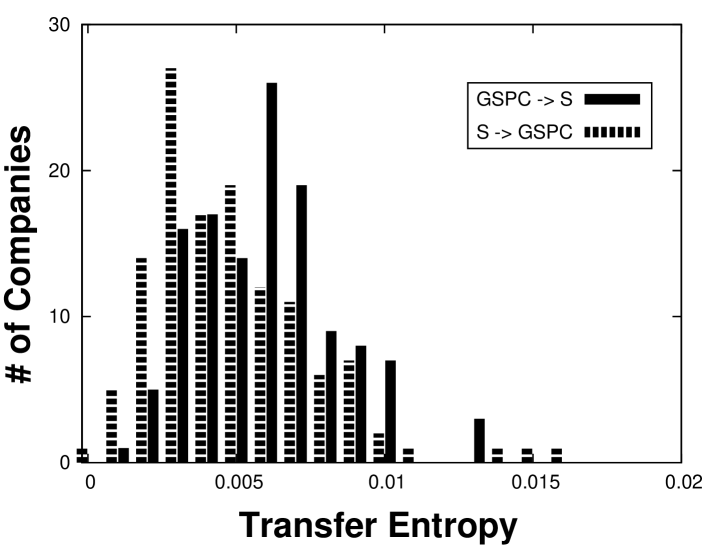

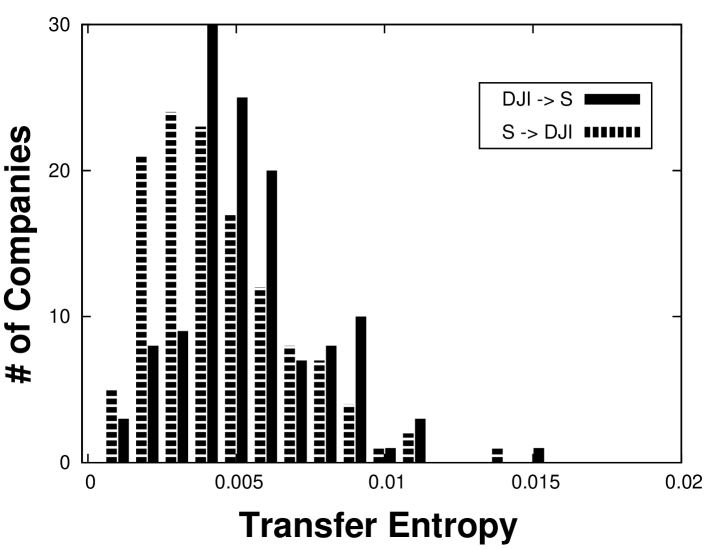

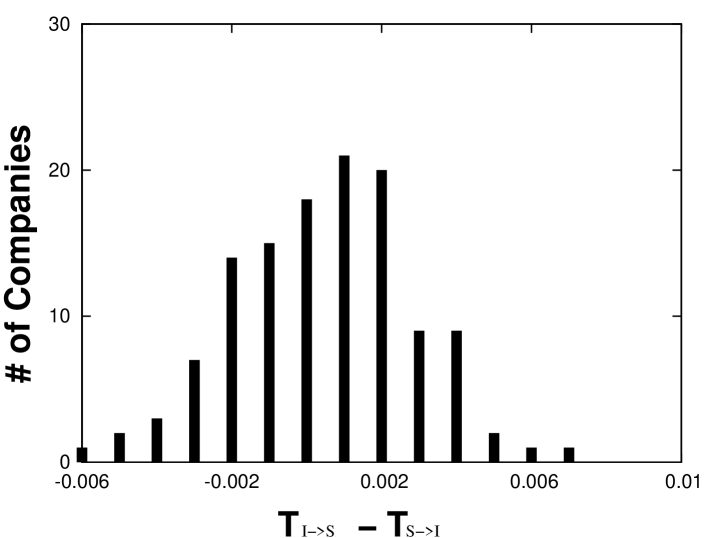

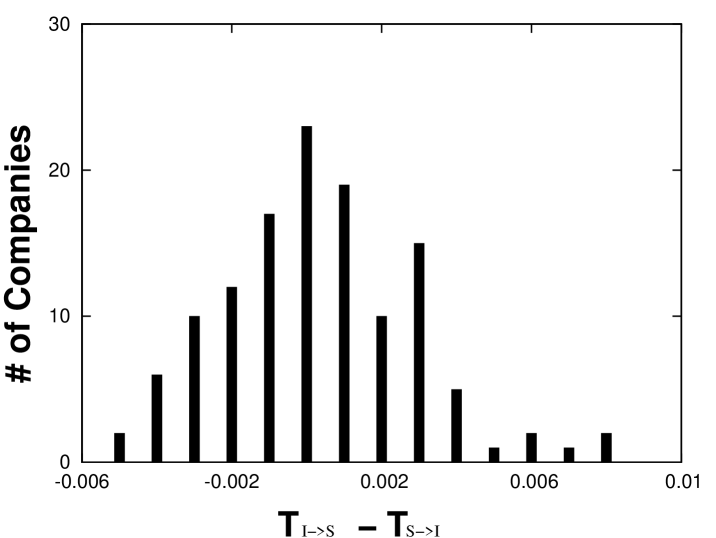

Figs. 3(a) and 3(b) show the frequency of the transfer entropy between composite stock index and stock prices at . Frequency distribution of the transfer entropy from index to stocks is more skewed to right than that from stocks to index. Figs. 3(c) and 3(d) show the difference between and . For the majority of companies, the transfer entropy from index to stocks are larger than the transfer entropy for the reverse. However, about 35% companies gives information to index of the next day.

| GSPC stock | stock GSPC | |

|---|---|---|

| 1 | Pepsico Inc. | Centerpoint Energy Inc. |

| 2 | FPL Group Inc. | Duke Energy Corp. |

| 3 | Xerox Corp. | Xerox Corp. |

| 4 | Entergy Corp. | Bristol-Myers Squibb Co. |

| 5 | Consolidated Edison Inc. | International Business Machines Corp. |

| 6 | Walt Disney co. | American Electric Power Co. Inc. |

| 7 | Union Pacific Corp. | PG & E Corp. |

| 8 | United Technologies Corp. | TXU Corp. |

| 9 | Clorox Co. | Wyeth |

| 10 | Centerpoint Energy Inc. | Consolidated Edison Inc. |

| DJI stock | stock DJI | |

| 1 | Walt Disney Co. | Xerox Corp. |

| 2 | Consolidated Edison Inc. | Centerpoint Energy Inc. |

| 3 | Xerox Corp. | Willams Companies Inc. |

| 4 | Whirlpool Corp. | Duke Energy Corp. |

| 5 | Pepsico Inc. | Southern Co. |

| 6 | FPL Group Inc. | PG & E Corp. |

| 7 | Coca-Cola Co. | American Electric Power Co. Inc. |

| 8 | United Technologies Corp. | Honeywell International Inc. |

| 9 | Corning Inc. | Entergy Corp. |

| 10 | PG & E Corp. | Bristol-Myers Squibb Co. |

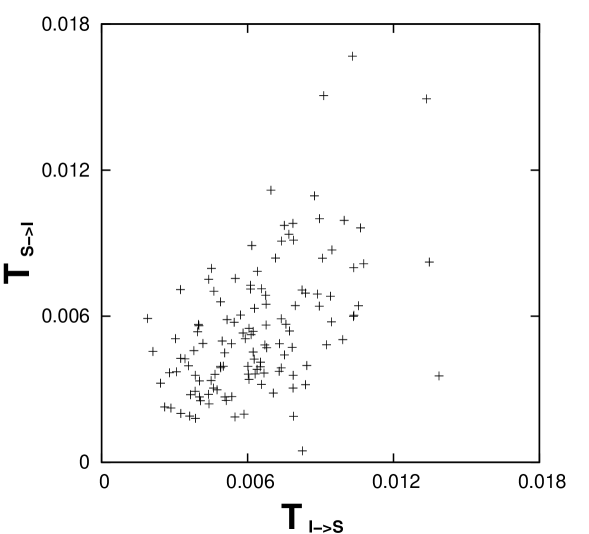

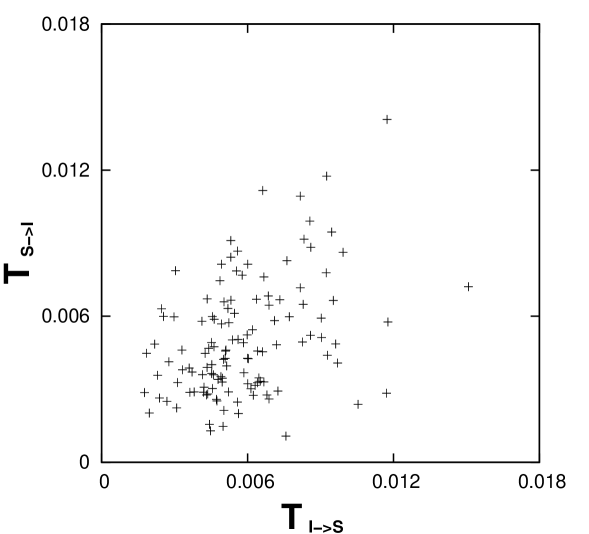

Fig. 4 shows the positive relation between and . The value of correlation between them is 0.51(9) for the GSPC and 0.40(9) for the DJI. In Table 1, the top 10 companies of the transfer entropy is listed. Among the top 10 companies, Xerox Corp., Entergy Corp., Consolidated Edison Inc., Centerpoint Energy Inc., and PG & E belong to the top 10 companies for both and . Both Fig. 4 and Table 1 show that the higher , the higher , though the average value of is higher than one of . Consequently, individual stocks are able to be divided into highly connected stocks and lowly connected stocks to the market.

4 Conclusion

The concept of the transfer entropy has been proposed for finding direction of casuality. Using the measure, we are able to investigate the information flow between stock index and individual stocks. Our results indicate that there is a stronger flow of information from the stock index to the individual stocks than vice versa, and the transfer entropy for both direction has positive correlation. Moreover, we expect similar result to the U.S. market for other stock markets. As a matter of fact, the result of the information flow in Japan stock market also produces the same directional casuality although it is not shown in this paper.

We have desire to find the correlations between the direction of information flow and company profile. However, we could not find it yet. The division of individual stocks due to the direction of casuality between composite stock index and companies may be useful for the stock investment strategies.

References

- [1] W. B. Arthur, S. N. Durlauf, D. A. Lane, The Economy as an Evolving Complex System II (Perseus Books, 1997).

- [2] R. N. Mantegna, H. E. Stanley, An Introduction to Econophysics (Cambridge University Press, 2000).

- [3] J.-P. Bouchaud, M. Potters, Theory of Financial Risks (Cambridge University Press, 2000).

- [4] B. B. Mandelbrot, Quant. Finance 1 (2001) 124.

- [5] L. Kullmann, J. Kertész, R. N. Mantegna, Physica A 287 (2000) 412.

- [6] L. Giada, M. Marsili, Physica A 315 (2002) 650.

- [7] V. M. Eguiluz, M. Zimmermann, Phys. Rev. Lett. 85 (2000) 5659.

- [8] A. Krawiecki, J. A. Hołyst, D. Helbing, Phys. Rev. Lett. 89 (2002) 158701.

- [9] T. Takaishi, Int. J. Mod. Phys. C 16 (2005) 1311.

- [10] T. Kaizoji, Physica A 287 (2000) 493.

- [11] J. B. Park, J. W. Lee, J.-S. Yang, H.-H. Jo, H.-T. Moon, Physica A 379 (2007) 179.

- [12] J. W. Lee, J. B. Park, H.-H. Jo, J.-S. Yang, H.-T. Moon, physics/0607282, 2006.

- [13] W.-S. Jung, S. Chae, J.-S. Yang, H.-T. Moon, Physica A 361 (2006) 263.

- [14] W.-S. Jung, O. Kwon, J.-S. Yang, H.-T. Moon, J. Korean Phys. Soc. 48 (2006) S135.

- [15] K. Matal, M. Pal, H. Salunkay, H. E. Stanley, Europhys. Lett. 66 (2004) 909.

- [16] J.-S. Yang, S. Chae, W.-S. Jung, H.-T. Moon, Physica A 363 (2006) 377.

- [17] S. Chae, W.-S. Jung, J.-S. Yang, H.-T. Moon, J. Korean Phys. Soc. 48 (2006) 313.

- [18] J.-S. Yang, W. Kwak, T. Kaizoji, I.-m. Kim, physics/0701179, 2007.

- [19] C. E. Shannon, W. Weaver, The Mathematical Theory of Information (University of Illinois Press, 1994).

- [20] T. Schreiber, Phys. Rev. Lett. 85 (2000) 461.

- [21] R. Marschinski, H. Kantz, Eur. Phys. J. B. 30 (2002) 275.