A two-dimensional ruin problem on the positive quadrant.

Florin Avram

111 Dept. de Math., Université de Pau, E-mail:

Florin.Avram@univ-Pau.fr Zbigniew

Palmowski222University of Wroclaw, pl. Grunwaldzki 2/4,

50-384 Wroclaw, Poland and Utrecht University, P.O. Box 80.010,

3500 TA, Utrecht, The Netherlands, E-mail:

zpalma@math.uni.wroc.pl and Martijn

Pistorius333Department of Mathematics, King’s College

London, Strand, London WC2R 2LS, UK, Email:

Martijn.Pistorius@kcl.ac.uk

Abstract

In this paper we study the joint ruin problem for two insurance

companies that divide between them both claims and premia in some

specified proportions (modeling two branches of the same insurance

company or an insurance and re-insurance company). Modeling the risk

processes of the insurance companies by Cramér-Lundberg

processes we obtain the Laplace transform in space of the

probability that either of the insurance companies is ruined in

finite time. Subsequently, for exponentially distributed claims, we

derive an explicit analytical expression for this joint ruin

probability by explicitly inverting this Laplace transform.

We also provide a characterization of the Laplace transform

of the joint ruin time.

1 A two dimensional ruin problem

In this paper

we consider a particular two dimensional risk model in which two

companies split the amount they pay out of each claim in positive

proportions and with ,

and the premiums according to rates and . Thus, the risk

process of the ’th company satisfies

where are the initial reserves. We will work with a spectrally

positive Lévy process , that is Lévy process with only

upward jumps that represents the cumulative amount of claims up to

time . In particular we focus on the classical

Cramér-Lundberg model:

(1)

where is a Poisson process with

intensity and the claims are i.i.d. random

variables independent of , with distribution function

and mean . We shall assume that the second

company, to be called the reinsurer, gets smaller profits per amount

paid, i.e.:

(2)

As usual in risk theory, we assume that

, which implies that in the

absence of ruin, as ().

Ruin happens at the time when at least one

insurance company is ruined:

(3)

i.e. at the first exit time of from the positive

quadrant. In this paper we will analyze the perpetual or ultimate

ruin probability:

(4)

Although ruin theory

under multi-dimensional models rarely admits analytical solutions,

we are able to obtain in our problem a closed form solution for

(4) if are exponentially distributed with

intensity .

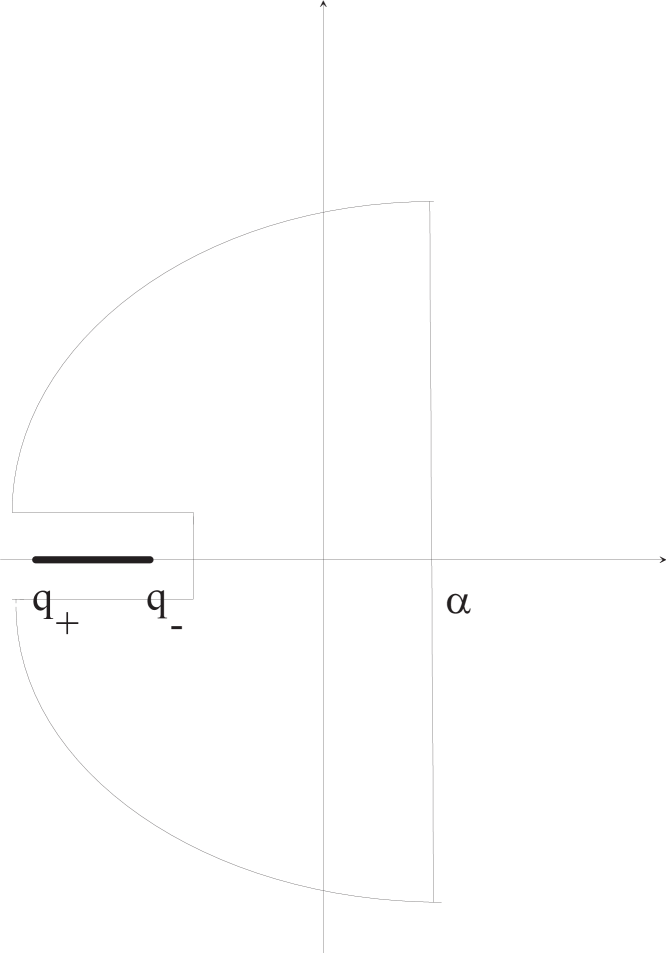

Geometrical considerations. The solution of the

two-dimensional ruin problem (4) strongly depends on the

relative sizes of the proportions and

premium rates – see Figure 1.

Figure 1: Geometrical considerations

If, as assumed throughout, the angle of the vector with

the axis is larger than that of , i.e. we note that starting with initial capital

in the cone situated below the line , the process ends up hitting at time the

axis. Thus, in the domain ruin occurs iff there is

ruin in the one-dimensional problem corresponding to the risk

process .

One dimensional reduction. A key observation is that in

(3) is also equal to

where . The

two dimensional problem (4) may thus be also viewed as

a one dimensional crossing problem over a piecewise linear

barrier.

In the case that the initial reserves and are such

that , that is, , the barrier is linear,

, the ruin happens always for the second

company. Thus, as we already observed, the problem (4)

reduces in fact to the classical one-dimensional ultimate ruin

problem with premium and claims , i.e.

where and is the ruin probability of ,

with . For the model (1) the Pollaczeck-Khinchine

formula, well known from the theory of one-dimensional ruin (see

e.g. [8] or [1]), yields then an explicit series

solution for in the case of a

general claims distribution. For the phase-type claims , i.e. with , the

ruin probability

may be written in a simpler matrix exponential form:

with

(see for example (4) in [2]), and

in the case of exponential claim sizes with intensity , it

reduces to:

(5)

where and

.

The rest of the paper is devoted to the analysis of

the opposite case, and is organised as follows.

Section 2 is devoted to the Laplace transform of

the ruin time in the case is of the form (1)

with exponential jumps. Subsequently, in Sections 3 and 4

we derive the Laplace double transform in

of the ruin probability if is a general

spectrally positive Lévy process.

Finally, in Section 5 this Laplace transform is

explicitly inverted, in the case of exponential claim sizes.

2 The differential system

for the exponential claim sizes case

In this section we provide a system of partial differential equations

for the Laplace transform

(6)

of the ruin time in (3) in the case

that is given by a compound Poisson process (1)

with intensity and with claims sizes that are

exponentially distributed with parameter . The memoryless

property of interarrival times and claim sizes opens up the

possibility of embedding the (discontinuous) Cramér-Lundberg

processes into a continuous Markov-modulated fluid

model. Informally, this is achieved by a transformation that

replaces the jumps of by a linear movement in the

direction of duration equal to the size of the

jump, creating thereby a new continuous semi-Markovian model

called the fluid embedding of

. As the process crosses

boundaries continuously and has exactly the same maxima and minima

as , first passage problems may be easier to handle for

than for the original process .

A formal construction of the fluid-embedding is given in the Appendix.

If we write

for the joint ruin time of , it follows from the definition

of that , where

denotes the time up to time that

was increasing. In particular,

(7)

Setting and writing

and for the partial derivative of

and with respect to we have the following

characterization of and .

Theorem 1

For it holds that

solves the Feynman-Kac system:

with the boundary condition:

(8)

Proof. Conditioning on the first shared claim occurrence

epoch we obtain:

(9)

.

(10)

Both integrals on the LHS of (9)

go to 0 as . This implies that

is a continuous function with respect to and .

Note that since we

live in the upper cone. This gives after simple manipulation:

Note that the last 3 terms on the LHS of above equation have

limits as , since is a continuous function. Thus

is a differentiable function of . Taking we derive

This gives the first equation in the Feynman-Kac system.

To derive the second one, we apply

integration-by-parts formula to (10):

which gives the second equation in the Feynman-Kac formula. The

boundary conditions follow immediately.

The above system may also be reformulated as a second

partial-differential equation in terms of only.

To that end, we define a linear transformation of

by and where are given by

with inverse

transformation:

where . In

the next result a PDE is derived for .

Corollary 1

The function

solves the equation

(11)

with the boundary conditions:

Proof: Note that:

•

during drift periods, is constant and

increases, at rate

•

during jump periods, is constant and

decreases, at rate .

Thus, in these new coordinates, the time is split between moving

into the direction of the axes and moving away from the axes. In

particular, at any time we have , where

are the total times of growing reserves (upward

drifting)/shrinking reserves (jumping). Note that

and hold.

In terms of the variables, the Feynman-Kac system becomes:

(12)

with

(13)

for all . Recall that the upper cone is described be

inequalities and . Following the steps

used in the proof of differentiability of

one can prove that is in class .

Eliminating , we find

(14)

with

(17)

We may remove the linear terms by switching to the

function in terms of which we get the stated result.

3 Probabilistic solution

One way to obtain the Laplace transform of the joint ruin probability

is to solve the above systems numerically. Here, we

pursue a different approach, by establishing first a general analytical

representation of the solution that holds for a general

spectrally positive Lévy process .

Noting that the process has

the same ruin probability as the original two-dimensional process

, we can restrict ourselves without loss of generality

to the process . In the sequel we will write for the

joint ruin probability (3) - (4) corresponding to

the process .

Proposition 1

If , then

(18)

where

(19)

with denoting conditioned on .

Proof: In view of the definition (3)

of we see that

where . Next, we note that,

if , it holds that the minimum

is equal to for and for ,

where was defined in (19). We have also .

Subsequent application of the Markov property of at time

shows that

In Section 4 we obtain the double Laplace transform of

in , which

we invert in Section 5,

in the case of exponentially distributed jumps,

using Bromwich type contours.

4 Double Laplace transform in space

Let now be a general spectrally positive Lévy process and

denote by the Laplace exponent of the spectrally

negative Lévy process ,

(20)

We may obtain directly the double Laplace transform in space of

, by exploiting

for the integral representation

in Proposition 1 and for

the explicit formula of the Laplace

transform in of the one-dimensional ultimate

ruin probability . We will use the following results:

1.

If , the

Laplace transform with respect to the starting point of the

ultimate survival probability (see e.g. Bertoin [4],

Thm. VII.8):

(21)

2.

The resolvent of a spectrally negative Lévy process killed as

it enters the nonpositive half-line, due to Suprun [7]

(see also Bertoin [5, Lem. 1]):

(22)

where largest root of and is a continuous and increasing function (called

the -scale function of ) with the Laplace

transform:

(23)

Now we obtain the double Laplace transform of the non-ruin probability

with respect to the initial reserves:

Note that

The first Laplace transform is given by

Writing and we see from (18)

and (22) that the second Laplace transform is given

by

where for the calculation of quantity we used (21)

and (23). In view of (21) we note that

the quantity is equal to

(24)

Similarly, since ,

we see that can be written as

Putting everything together we find:

Proposition 2

The double Laplace transform is given by

(25)

4.1 Exponential claims

In this section we

specialize the above result to the classical model (1)

where the jumps are exponentially distributed with parameter

() and we write , . In

this case the characteristic exponent of is given by

In particular, in

view of the form of and it can be verified that

(with ) and is equal to

where and and

(26)

with , . For later reference we note that

(27)

with .

Noting that is the largest root of

and is the largest root

of we identify

In this subsection

we invert the Laplace transform (28) of the ruin

probability for exponential claim sizes. To perform the

inversion we shall employ the method of residues. For an overview

of the theory of Laplace transforms and complex analysis see e.g.

Widder [9] or Ahlfors [3]. The method of residues

leads to an explicit analytical representation of the survival

probability given in the following theorem.

Theorem 2

Let and let is given by (1) with

. Then it holds that

where and

(29)

with

and

To prove this result, first observe that

can be recovered from using Mellin’s formula, as folows:

(30)

where .

The next step consists in iteratively evaluating this double

integral (first w.r.t. and then w.r.t. ) using Cauchy’s theorem.

The result of the first inversion is given in the next result:

Lemma 1

For and fixed with it holds that

(31)

where is given by

(32)

The proofs of results that are not developed in the text can be

found in the Appendix.

In view of equations (21) and (5) we

recognize the first term in (31) as the Laplace

transform of . The inversion

of the second term relies on the following properties of

and , that were defined in (32) and (26)

respectively:

Lemma 2

(i) The functions and ,

are analytic in the set

where and remains bounded if .

(ii) Let with and .

If , then

(33)

Figure 2: Bromwich

contour

In order to ensure that we can calculate the inversion

of the second term in (31) using the method of residues

we fix and replace by (note that

in view of Lemma 2 the latter is

as ).

Denote by and the Laplace inverses of

and , that is

Then it follows that can be recovered from by

(34)

To complete the inversion of we are thus led to

evaluate the integral

(35)

Using Lemma 2 we choose a Bromwich contour that encloses the poles of

while the cut of the square root is not enclosed (see

Figure 2 and the proof of Lemma 4 for

formal definition of ). We note that this is a

standard approach to calculate integrals of the form

(35) (e.g. Ahlfors [3] or see Pervozvansky

[6] for a recent application to the calculation of

one-dimensional ruin probabilities).

Recalling from Lemma 2 that has two simple

poles, in and , Cauchy’s theorem implies

that

(36)

The next step consists in evaluating the residues in (36),

which is a matter of straightforward calulations:

Lemma 3

Writing

it holds for that

Next we turn to the left-hand side of the formula (36):

Proof of Theorem 2

In view of (34), (36) and Lemmas

3 and 4, the final result is obtained

by first differentiating the residues in Lemma 3 and

with respect to and subsequently letting subsequently tend to zero.

Taking note of the facts

completes the proof

(where the latter follows using the dominated convergence thoerem).

Appendix A Appendix

A.1 Formal construction of the fluid-embedding

A formal construction of the process is as follows.

Let and denote the subsequent

inter-arrival times and claim sizes. Note that these form

sequences of i.i.d. exponential random variables with parameters

and respectively. Define the switch times by

and, for ,

and construct taking values in by setting

Then is a two-state

Markov chain indicating whether is

increasing (state ) or decreasing (state ); more precisely,

denoting by

the total time up to that

has spent in state , we set

(i) Noting that the argument of the square root in (26) is positive

if is real and or , it follows that

is analytic outside the cut . Since, furthermore,

the denominator of has no roots in , we see that is analytic

in the set . The asymptotics directly follow from the form of .

(ii) Employing the standard

definition of the square root

(with the cut along the negative half-line) and

appealing to the definition of and the continuity of

the argument and modulus

imply that the convergence in (33) holds true.

Consider the contour that is given in Figure

2, i.e. consists of the line segments , , and and two quarter circles in

the left half-plane joining and , and,

and , respectively.

By taking the limits of and subsequently letting

and using that the integrals of the

quarter-circles tend to zero (in view of the fact that

as , cf. Lemma

2(i)) we find that the contour integral

converges to

(38)

where integrals and are

the limits of the line integrals along the segments

and of the

contour , respectively. In view of Lemma

2(ii) it follows that the last two integrals in

(38) are equal to

(39)

where and are defined in (33). Use of

the representation (for

) completes the calculation of the contour

integral of .

Acknowledgements

F. Avram and M. Pistorius gratefully acknowledge support from

the London Mathematical Society, grant # 4416. F. Avram and Z.

Palmowski acknowledge support by POLONIUM no 09158SD. Z. Palmowski

acknowledges support by KBN 1P03A03128 and NWO 613.000.310. M.

Pistorius acknowledges support by the Nuffield Foundation

NUF/NAL/000761/G.

References

[1] Asmussen, S. (2000) Ruin probabilities. World

Scientific,Singapore.

[2]

Asmussen, S, Avram, F, Usabel, M. (2002) Erlangian approximations

for finite-horizon ruin probabilities. Astin Bulletin32, 267–281.

[3] Ahlfors, L. V. (1979) Complex Analysis. 3rd Edition.

McGraw-Hill.

[4]

Bertoin, J. (1996) Lévy processes.

Cambridge University Press.

[5]

Bertoin, J. (1997) Exponential decay and ergodicity of completely

asymmetric Lévy processes in a finite interval. Ann.

Appl. Probab.7(1), 156–169.

[6] Pervozvansky, A.A. (1998) Equation for survival

probability in a finite time interval in case of non-zero real

interest force . Insurance Math. Econom.23, 287-295.

[7]

Suprun, V.N. (1976) Problem of destruction and resolvent of a

terminating process with independent increments. Ukrainian

Math. J.28, 39–45.

[8] Rolski, T., Schmidli, H., Schmidt, V. and Teugels,

J. (1999) Stochastic processes for insurance and finance.

John Wiley and Sons, Inc., New York.

[9] Widder, D.V. (1941) The Laplace Transform.

Princeton, NJ: Princeton University Press.