Unconstrained Recursive Importance Sampling

Abstract

We propose an unconstrained stochastic approximation method of finding the optimal measure change (in an a priori parametric family) for Monte Carlo simulations. We consider different parametric families based on the Girsanov theorem and the Esscher transform (or exponential-tilting). In a multidimensional Gaussian framework, Arouna uses a projected Robbins-Monro procedure to select the parameter minimizing the variance (see [2]). In our approach, the parameter (scalar or process) is selected by a classical Robbins-Monro procedure without projection or truncation. To obtain this unconstrained algorithm we intensively use the regularity of the density of the law without assume smoothness of the payoff. We prove the convergence for a large class of multidimensional distributions and diffusion processes.

We illustrate the effectiveness of our algorithm via pricing a Basket payoff under a multidimensional NIG distribution, and pricing a barrier options in different markets.

Key words: Stochastic algorithm, Robbins-Monro, Importance sampling, Esscher transform, Girsanov, NIG distribution, Barrier options.

2000 Mathematics Subject Classification: 65C05, 65B99, 60H35.

1 Introduction

The basic problem in Numerical Probability is to optimize some way or another the computation by a Monte Carlo simulation of a real quantity known by a probabilistic representation

where is a random vector having values in a Banach space and is a Borel function (and is square integrable). The space is but can also be a functional space of paths of a process . However, in this introduction section, we will first focus on the finite dimensional case .

Assume that has an absolutely continuous distribution ( denotes the Lebesgue measure on ) and that with (otherwise the expectation is clearly and the problem is meaningless). Furthermore we assume that the probability density is everywhere positive on .

The paradigm of importance sampling applied to a parametrized family of distributions is the following: consider the family of absolutely continuous probability distributions , , such that , - . One may assume without loss of generality that is an open non empty connected subset of containing so that . In fact we will assume throughout the paper that . Then for any -valued random variable with distribution , we have

| (1.1) |

Among all these random variables having the same expectation , the one with the lowest variance is the one with the lowest quadratic norm: minimizing the variance amounts to finding the parameter solution (if any) to the following minimization problem

where, for every ,

| (1.2) |

A typical situation is importance sampling by mean translation in a finite dimensional Gaussian framework i.e.

Then the second equality in (1.2) is simply the Cameron-Martin formula. This specific framework is very important for applications, especially in Finance, and was the starting point of the new interest for recursive importance sampling procedures, mainly initiated by Arouna in [2] (see further on). In fact, as long as variance reduction is concerned, one can consider a more general framework without extra effort. As a matter of fact, if the distributions satisfy

| () |

and satisfies for every , then (see Proposition 1 below), the function is finite, convex, goes to infinity at infinity. As a consequence is non empty. Assumption can be localized by by considering that one the two conditions holds only on a Borel set of such that . If is strictly -concave for every in a Borel set such that , then is strictly convex and is reduced to a single . These results follow from the second representation of as an expectation in (1.2) which is obtained by a second change of probability (the reverse one). For notational convenience we will temporarily assume that in this introduction section, although our main result needs no such restriction.

A classical procedure to approximate is the so-called Robbins-Monro algorithm. This is a recursive stochastic algorithm (see (AlgoRM) below) which can be seen as a stochastic counterpart of deterministic recursive zero search procedures like the Newton-Raphson one. It can be formally implemented provided the gradient of the (convex) target function admits a representation as an expectation. Since we have no a priori knowledge about the regularity of (111When is smooth enough alternative approaches have been developed based on some large deviation estimates which provide a good approximation of by deterministic optimization methods (see [10]).) and do not wish to have any, we are naturally lead to formally differentiate the second representation of in (1.2) to obtain a representation of as

| (1.3) |

Then, if we consider the function such that naturally defined by (1.3), the derived Robbins-Monro procedure writes

| (AlgoRM) |

with a step sequence decreasing to 0 (at an appropriate rate), a sequence of i.i.d. random variables with distribution . To establish the convergence of a Robbins-Monro procedure to requires seemingly not so stringent assumptions. We mean by that: not so different from those needed in a deterministic framework. However, one of them turns out to be quite restrictive for our purpose: the sub-linear growth assumption in quadratic mean

| (NEC) |

which is the stochastic counterpart of the classical non-explosion condition needed in a deterministic framework. In practice, this condition is almost never satisfied in our framework due to the behaviour of the term as goes to infinity.

The origin of recursive importance sampling as briefly described above goes back to Kushner and has recently been brought back to light in a Gaussian framework by Arouna in [2]. However, as confirmed by the numerical experiments carried out by several authors ([2, 12, 14]), the regular Robbins-Monro procedure (AlgoRM) does suffer from a structural instability coming from the violation of (NEC). This phenomenon is quite similar to the behaviour of the explicit discretization schemes of an when has a super-linear growth at infinity. Furthermore, in a probabilistic framework no “implicit scheme” can be devised in general. Then the only way out mutatis mutandis is to kill the procedure when it comes close to explosion and to restart it with a smaller step sequence. Formally, this can be described as some repeated projections or truncations when the algorithm leaves a slowly growing compact set waiting for stabilization which is shown to occur . Then, the algorithm behaves like a regular Robbins-Monro procedure. This is the so-called “Projection à la Chen” avatar of the Robbins-Monro algorithm, introduced by Chen in [6, 7] and then investigated by several authors (see [1, 14]) Formally, repeated projections “à la Chen” can be written as follows:

| (AlgoP) |

where denotes the projection on the convex compact ( is increasing to as ). In [14] is established a a Central Limit Theorem for this version of the recursive variance reduction procedure. Some extensions to non Gaussian framework have been carried out by Arouna in his PhD thesis (with some applications to reliability) and more recently to the marginal distributions of a Lévy processes by Kawai in [12].

However, convergence occurs for this procedure after a long “stabilization phase” …provided that the sequence of compact sets have been specified in an appropriate way. This specification turns out to be a rather sensitive phase of the “tuning” of the algorithm to be combined with that of the step sequence.

In this paper, we show that as soon as the growth of at infinity can be explicitly controlled, it is always possible to design a regular Robbins-Monro algorithm which converges to a variance minimizer with no risk of explosion (and subsequently no need of repeated projections).

To this end the key is to introduce a third change of probability in order to control the term . In a Gaussian framework this amounts to switching the parameter from the density to the function by a third mean translation. This of course corresponds to a new function but can also be interpreted a posteriori as a way to introduce an adaptive step sequence (in the spirit of [15]).

In terms of formal importance sampling, we introduce a new positive density (everywhere positive on ) so that the gradient writes

| (1.4) |

where . The “weight” may seem complicated but the rôle of the density is to control the critical term by a (deterministic) quantity only depending on . Then we can replace by a function in the above Robbins-Monro procedure (AlgoRM) where is a positive function used to control the behaviour of for large values of (note that ).

We will first illustrate this paradigm in a finite dimensional setting with parametrized importance sampling procedures: the mean translation and the Esscher transform which coincide for Gaussian vectors on which a special emphasis will be put. Both cases correspond to a specific choice of which significantly simplifies the expression of the weight.

As a second step, we will deal with an infinite dimensional setting (path-dependent diffusion like processes) where we will rely on the Girsanov transform to play the role of mean translator. To be more precise, we want now to compute where is a path-dependent diffusion process and is a functional defined on the space of continuous functions defined on . We consider a -dimensional Itô process solution of the path-dependent SDE

| () |

where is a -dimensional standard Brownian motion, is the stopped process at time , and are Lipschitz with respect to the on the space and continuous in (see [18] for more details about these path-dependent SDE’s).

Let be a fixed borel bounded functional on with values in (where is a free integral parameter). Then a Girsanov transform yields that for every ,

where is the solution to . The functional to be minimized is now

In practice we will only minimize over a finite dimensional subspace of .

The paper is organized as follows. Section 2 is devoted to the finite dimensional setting where we recall the main tool including a slight extension of the Robbins-Monro theorem in the Subsection 2.1 and the gaussian case investigated in [2] is revisited to emphasize the new aspects of our algorithm in the Subsection 2.2.

In Section 2 we successively investigate the translation for log-concave distributions probability and the Esscher transform. In Section 3 we introduce a functional version of our algorithm based on the Girsanov theorem to deal the SDE. In Section 4 we provide some comments on the practical implementation and in Section 5 some numerical experiments are carried out on some option pricing problems.

Notations: We will denote by the fact that a symmetric matrix is positive definite. will denote the canonical Euclidean norm on and will denote the canonical inner product.

The real constant denotes a positive real constant that may vary from line to line.

if is an -valued (class of) Borel function(s).

2 The finite-dimensional setting

2.1 as a target

Proposition 1

Suppose () holds.

Then the function defined by (1.2) is convex and . As a consequence

Proof. By the change of probability we have . Let fixed in . The function is concave, hence is convex so that, owing to the Young Inequality, the function is convex since it is non-negative.

To prove that tends to infinity as goes to infinity, we consider two cases:

-

–

If for every , the result is trivial by Fatou’s Lemma.

-

–

If for every , we apply the reverse Hölder inequality with conjugate exponents to obtain

( and are probability density functions). One concludes again by Fatou’s Lemma.

The set , or to be precise, the random vectors taking values in will the target(s) of our new algorithm. If is strictly convex, if

then . Nevertheless this will not be necessary owing to the combination of the two results that follow.

Lemma 1

Let be a convex differentiable function, then

Furthermore, if is nonempty, it is a convex closed set (which coincide with ) and

A sufficient (but in no case necessary) condition for a nonnegative convex function to attain a minimum is that .

Now we pass to the statement of the convergence theorem on which we will rely throughout the paper. It is a slight variant of the regular Robbins-Monro procedure whose proof is rejected in an annex.

Theorem 1

(Extended Robbins-Monro Theorem) Let a Borel function and an -valued random vector such that for every . Then set

Suppose that the function is continuous and that satisfies

| (2.5) |

Let be a sequence of gain parameters satisfying

| (2.6) |

Suppose that

| (NEC) |

(which implies ).

Let be an i.i.d. sequence of random vectors having the distribution of , a random vector , independent of satisfying , all defined on the same probability space . Then, the recursive procedure defined by

| (2.7) |

satisfies:

| (2.8) |

The convergence also holds in , .

The proof is postponed to the Appendix at the end of the paper. The natural way to apply this theorem for our purpose is the following:

-

–

Step 1: we will show that the convex function in (1.2) is differentiable with a gradient having a representation as an expectation formally given .

- –

-

–

Step 3: Specify in an appropriate way the function so that the linear quadratic growth assumption is satisfied. This is the sensitive point that will lead us to modify the structure more deeply by finding a new representation of as an expectation not directly based on the local gradient .

2.2 A first illustration: the Gaussian case revisited

The Gaussian is the framework of [2]. It is also a kind of introduction to the infinite dimensional diffusion setting investigated in Section 3. In the Gaussian case, the natural importance sampling density is the translation of the gaussian density: for ( ). We have

The assumption () is clearly satisfied by the Gaussian density, and we assume that satisfies so that is well defined.

In [2], Arouna considers the function defined by

It is clear that the condition (NEC) is not satisfied even if we simplify this function by (which does not modify the problem).

A first approach: When have finite moments of any order, a naive way to control directly by an explicit deterministic function of (in order to rescale it) is to proceed as follows: one derives from Hölder Inequality that for every couple , of conjugate exponents

Setting and , yields

Then, satisfies the condition (NEC) and theoretically the standard Robbins-Monro algorithm implemented with converges and no projection nor truncation is needed. Numerically, the solution is not satisfactory because the correcting factor goes to zero much too fast as goes to infinity: if at any iteration at the beginning of the procedure is sent “too far”, then it is frozen instantly. If is too small it will simply not prevent explosion. The tuning of becomes quite demanding and payoff dependent. This is in complete contradiction with our aim of a self-controlled variance reducer. A more robust approach needs to be developed. On the other hand this kind of behaviour suggests that we are not in the right asymptotics to control .

Note however that when is bounded with a compact support, then one can set and the above approach provides an efficient answer to our problem.

A general approach: We consider the density

By (1.4), we have

with , i.e. . Since is the Gaussian density, we have . As a consequence, the function defined by

provides a representation of the gradient . As soon as is bounded, this function satisfies the condition (NEC). Otherwise, we note that thanks to this new change of variable the parameter lies now inside the payoff function and that the exponential term has disappeared from the expectation. If we have an a priori control on the function as goes to infinity, say

then we can consider the function which satisfies

The resulting Robbins-Monro algorithm reads

We no longer to tune the correcting factor and one verifies on simulations that it does not suffer from freezing in general. In case of a too dissymmetric function this may still happen but a self-controlled variant is proposed in Section 2.3 below to completely get rid of this effect (which cannot be compared to an explosion).

2.3 Translation of the mean: the general strongly unimodal case

We consider importance sampling by mean translation, namely we set

for .

In this section we assume that

so that () holds. Moreover, we make the following additional assumption on the probability density

| () |

First we will use (1.2) to differentiate since

Proposition 2

Proof. The formal differentiation to get (2.10) from (1.2) is obvious. So it remains to check the domination property for lying inside a compact set. Let and . The -concavity of implies that

so that

Using the assumption () yields, for every ,

To derive the second expression (2.11) for the gradient, we proceed as follows: an elementary change of variable shows that

Remark. The second change of variable (in (1.2)) has been processed to withdraw the parameter from the possible non smooth function to make possible the differentiation of (since is smooth). The second expression (2.11) results form a third translation of the variable in order to plug back the parameter into the function which in common applications has a known controlled growth rate at infinity.

This last statement may look strange at a first glance since appears in the “weight” term of the expectation that involves the probability density . However, when , this term can be controlled easily since it reduces to

The following lemma shows that, more generally in our strongly unimodal setting, if () and () are satisfied, this “weight” can always be controlled by a deterministic function of .

Proof. Let be the convex function defined on by . Then, for every ,

Note that . Then, using the -convexity of and the elementary inequality

(valid if ) yields

| (2.13) |

Remark. Thus the normal distribution satisfies () with and . Moreover, note that the last inequality in the above proof holds as an equality.

Now we are in position to derive an unconstraint (extended) Robbins-Monro algorithm to minimize the function , provided the function satisfies a sub-multiplicative control property, in which is a real parameter and a function from to , such that, namely

| () |

Remark. Assumption () seems almost non-parametric. However, its field of application is somewhat limited by () for the following reason: if there exists a positive real number such that is concave, then for some real constant ; which in turn implies that the function in () needs to satisfy for some and some . (Then with if and if , when ).

Theorem 2

Suppose and satisfy (), (), (2.9) and () for some parameters , and , and that the step sequence satisfies the usual decreasing step assumption

Then the recursive procedure defined by

| (2.14) |

where is an i.i.d. sequence with the same distribution as and

| (2.15) |

converges toward an -valued (square integrable) random variable .

Proof. In order to apply Theorem 1, we have to check the following fact:

– Mean reversion: The mean function of the procedure defined by (2.14) reads

so that and if and ,

for every .

– Linear growth of : All our efforts in the design of the procedure are motivated by this Assumption (NEC) which prevents explosion. This condition is clearly fulfilled by since

where we used Assumption () in the first line and Inequality (2.12) from Lemma 2 in the second line. One derives that there exists a real constant such that

Examples of distributions

- •

-

•

The hyper-exponential distributions

where is polynomial function. This wide family includes the normal distributions, the Laplace distribution, the symmetric gamma distributions, etc.

- •

2.4 Exponential change of measure: the Esscher transform

A second classical approach is to consider an exponential change of measure (or Esscher transform). This transformation has already been consider for that purpose in [12] to extend the procedure with repeated projections introduced in [2]. We denote by the cumulant generating function (or log–Laplace) of i.e. . We assume that for every (which implies that is an infinitely differentiable convex function) and define

Let denote any random variable with distribution .

We assume that satisfies

| () |

One must be aware that what follows makes sense as a variance reduction procedure only if the distribution of can be simulated at the same cost as or at least at a reasonable cost

| (2.16) |

where is a Borel subset of a metric space and is an explicit Borel function. By (1.2), the potential to be minimized is

Proposition 3

Proof. The function is clearly log-convex so that is -concave for every . On the other hand, by () we have for every , and () is fulfilled.

The formal differentiation to get (2.18) is obvious and is made rigorous by applying the assumption on . The second expression (2.19) of the gradient uses a third change of variable

Theorem 3

Proof. We have to check the linear growth of the function (condition (NEC)). We have

| (2.20) |

First, by the following inequality

we have where if or if . With this notation, we have

By the concavity of , we have

so that

| (2.21) |

In the same way, we have

| (2.22) |

Now, by differentiation of it is easy to check that

which implies

The assumption () implies that (for the partial order on symmetric matrices induced by nonnegative symmetric matrices) then is a bounded function of and in turn has a linear growth by the fundamental formula of calculus. Consequently, for every ,

Plugging this into (2.22) and using (2.21) and (2.20) we obtain .

3 Adaptive variance reduction for diffusions

3.1 Framework and preliminaries

We consider a -dimensional Itô process solution to the stochastic differential equation (SDE)

| () |

where is a -dimensional standard Brownian motion, is the stopped process at time , and are measurable with respect to the canonical predictable -field on . For further details we refer to [18], p. 124-130.

Thus, if and for every , is a usual diffusion process with drift and diffusion coefficient .

If and for every where , then is the continuous Euler scheme with step of the above diffusion with drift and diffusion coefficient .

An easy adaptation of standard proofs for regular SDE’s show (see [18]) that strong existence and uniqueness of solutions for () follows from the following assumption

| () |

Our aim is to devise an adaptive variance reduction method inspired from Section 2 for the computation of

where is an Borel functional defined on such that

| (3.23) |

In this functional setting, Girsanov Theorem will play the role of the invariance of Lebesgue measure by translation. The translation process that we consider in this section is of the form where is defined for every and by

a bounded Borel function and (represented by a Borel function) for . In the sequel, we use the following notations ,

where denotes the solution to .

First we need the following standard abstract lemma.

Lemma 3

Suppose holds.

The SDE satisfies the weak existence and uniqueness assumptions and for every non negative Borel functional and we have, with the above notations,

and

Proof. This is a straightforward application of Theorem 1.11, p.372 (and the remark that immediately follows) in [16] once noticed that , and are predictable processes with respect to the completed filtration of .

Remarks. The Doléans exponential is a true martingale for any .

In fact, still following the above cited remark form [16], the above lemma holds true if we replace by any progressively measurable process such that .

It follows from the first identity in Lemma 3 that for every bounded Borel function and for every

(set ). So, finding the estimator with the lowest variance amounts to solving the minimization problem

Using Lemma 3 with and yields

| (3.24) |

Proposition 4

Assume for some as well as Assumptions (3.23) and . Then function is finite on and -convex.

-

Assume that the bounded matrix-valued Borel function satisfies that has a non-atomic kernel on the event

(3.25) then for every finite dimensional subspace , . If furthermore

(3.26) then .

-

The function is differentiable at every and the differential is characterized on every by

(3.27)

Remarks. For practical implementation, the “finite dimensional” statement is the only result of interest since it ensures that .

If and , the “infinite-dimensional” assumption is always satisfied.

Proof. As concerns the function , we rely on Equality (3.24). Set . Owing to the Hölder Inequality, showing that this function is finite on the whole space amounts to proving that

To show that goes to infinity at infinity, one proceeds as follows. Using the trivial equality

and the reverse Hölder inequality with conjugate exponents we obtain

by the martingale property of the Doléans exponential. Let such that . We have then , and by the conditional Jensen inequality

Now

The assumption (3.25) implies that, for every ,

so that if runs over the compact sphere of a finite dimensional subspace of

so that

and one concludes by Fatou’s Lemma using that . The second claim easily follows from Assumption (3.26).

As a first step, we show that the random functional from into (), is differentiable. Indeed, it from the below inequality,

| (3.28) |

where is clearly a bounded random functional from into , with an operator norm ( (this follows from Hölder and B.D.G. inequalities).

Then, we derive that is differentiable form into every with differential . This follows from standard computation based on (3.28), the elementary inequality and the fact that

where we used both Hölder and B.D.G. inequality.

One concludes that is differentiable by using the –differentiability of with .

The second form of the gradient is obtained by a Girsanov transform using Lemma 3.

3.2 Design of the algorithm

In view of a practical implementation of the procedure we are lead to consider some non trivial finite dimensional subspaces of . The function being strictly -convex on and going to infinity as goes to infinity, , the restriction of on attains a minimum which de facto becomes the target of the procedure. Furthermore, for every , and the quadratic function is a Lyapunov function for the problem.

Like for the static framework investigated in Section 2.3, our algorithm will be based on the representation (3.27) for the differential of : in this representation the variance reducer appears inside the functional which makes easier a control at infinity in order to prevent from any early explosion of the procedure. However, to this end we need to control the discrepancy between and . This is the purpose of the following Lemma.

Lemma 4

Assume holds. Let be a bounded Borel -valued function defined on , let and let and denote a strong solutions of and driven by the same Brownian motion. Then, for every , there exists a real constant such that

| (3.29) |

Proof. The proof follows the lines of the proof of the strong rate of convergence of the Euler scheme (see [3]).

The main result of this section is the following theorem.

Theorem 4

Suppose that Assumption (3.23) and hold.

Let be a bounded Borel -valued function (with ) defined on , and let be a functional satisfying

| () |

for some positive exponent (then for every ). Let be a finite dimensional subspace of spanned by an orthonormal basis .

Let . We define the algorithm by

where satisfies (2.6), is a sequence of independent Brownian motions for which is a strong solution to and for every standard Brownian motion , every -adapted -valued process ,

where for

Then the recursive sequence a.s. converges toward an -valued (squared integrable) random variable .

Remark. For a practical implementation of this algorithm, we must have for all Brownian motions a strong solution of . In particular, this is the case if the driver is locally Lipshitz (in space) or if is the continuous Euler scheme of a diffusion with step (using the driver ).

Note that if is continuous (in space) but not necessarily locally Lipshitz, the Euler scheme converges in law to the solution of the SDE.

First note that for every , the mean function of the algorithm reads

so that, for every ,

It remains to check that for every , to apply the Robbins-Zygmund Lemma which ensures the convergence of the procedure (see Section 2.1). We first deal with the term . Let .

Now

One shows likewise that

Combining theses estimates shows that satisfies the linear growth assumption in .

If is unbounded it follows from Assumption () that, for every ,

Elementary computation based on (3.29) and Lemma 3 yield

for every (Assumption () implies that for every ). Following the same proof to the bounded case, we obtain easily the results with . We conclude by noting that is an arbitrary parameter to cancel the denominator.

Remark. If the functional is bounded (), we prove in the same way that the algorithm without correction, i.e. build with , a.s. converges.

4 Additional remarks

For the sake of simplicity we focus in this section on importance sampling by mean translation in a finite dimensional setting (Section 2.3) although most of the comments below can also be applied at least in the path-dependent diffusions setting.

4.1 Purely adaptive approach

As proved by Arouna (see [2]), we can consider a purely adaptive approach to reduce the variance. It consists to perform the Robbins-Monro algorithm simultaneously with the Monte Carlo approximation. More precisely, estimate by

where is the same innovation as that used in the Robbins-Monro procedure . This adaptive Monte Carlo procedure satisfies a Central Limit Theorem with the optimal asymptotic variance

This approach can be extended to the Esscher transform when we use the same innovation (see (2.16)) for the Monte Carlo procedure (computing ) and the Robbins-Monro algorithm (computing ). Likewise in the functional setting we can combine the variance reduction procedure and the Monte Carlo simulations using the same Brownian motion.

In practice, it is not clear that this adaptive Monte Carlo is better than the naive two stage procedure: performing first Robbins-Monro with a small number of iterations (to get a rough estimate ), then performing the Monte Carlo simulations with this optimized parameter.

4.2 Weak rate of convergence: Central Limit Theorem (CLT)

As concerns the rate of convergence, once again this a regular stochastic algorithm behaves as described in usual Stochastic Approximation Theory textbooks like [13], [5], [8]. So, as soon as the optimal variance reducer set is reduced to a single point , the procedure satisfies under quite standard assumptions a . We will not enter into technicalities at this stage but only try to emphasize the impact of a renormalization factor like or induced by the function on the “final” rate of convergence of the algorithm toward . We will assume that and that for the sake of simplicity. One can write

The function corresponds to the case of a bounded function (then ). Under simple integration assumptions, one shows that is twice differentiable and that

Consequently the mean functions and related to and which read respectively

are differentiable at and

Now, general results about CLT say that if , with

| (4.30) |

then

where

| (4.31) |

The mapping reaches its minimum at leading to the minimal asymptotic variance

by homogeneity.

So the optimal rate of convergence of the procedure is not impacted by the use of the normalizing function . However, coming back to condition (4.30), we see that this assumption on the coefficient is more stringent since (in practice this factor can be rather large). Consequently, given the fact that is unknown to the user, this will induce a blind choice of biased to higher values. With the well-known consequence in practice that if is too large the “CLT regime” will take place later than it would with smaller values. One solution to overcome this contradiction can be to make depend on and slowly decrease.

As a conclusion, the algorithm never explodes (and converges) even for strongly unbounded functions which is a major asset compared to the version of the algorithm based on repeated projections. Nevertheless, the normalizing factor which ensures the non-explosion of the procedure may impact the rate of convergence since it has an influence on the tuning of the step sequence (which is always more or less “blind” since it depends on the target . In fact, we did not meet such difficulty in our numerical experiments reported below.

One classical way to overcome this problem can be to introduce the empirical mean of the algorithm implemented with a slowly decreasing step “à la Rupert & Poliak” (see [17]): Set , and

where denotes the regular Robbins-Monro algorithm defined by (2.14) starting at . Then converges toward and satisfies a CLT with the optimal asymptotic variance (4.31). See also a variant based on a gliding window developed in [14].

4.3 Extension to more general sets of parameters

In many applications (see below with the Spark spread options with the NIG distribution) the natural set of parameters is not but an open connected subset of . Nevertheless, as illustrated below, our unconstrained approach still works provided one can proceed a diffeomorphic change of parameter by setting

where is a -diffeomorphism with a bounded differential ( ). As an illustration, let us consider the case where the state function of the procedure is designed so that where is the objective function to be minimized over and is a bounded positive Borel function. Then, one replaces by and defines recursively a procedure on by

In order to establish the convergence of to , one relies on a variant of Robbins-Monro algorithm, namely a stochastic gradient approach (see [8, 13] for further details): one defines which turns out to be a Lyapunov function for the new algorithm since

If satisfies (which is a hidden constraint on the choice of ), one shows under the standard “decreasing” assumption on the step sequence that and . If or , one easily derives that as .

5 Numerical illustrations

5.1 Multidimensional setting: the NIG distribution

First we consider a simple case to compare the two algorithms of Section 2. The quantity to compute is

where is the density of a normal inverse gaussian (NIG) random variable of parameters i.e. , , , ,

where is a modified Bessel function of the second kind and .

We can summarize the two algorithms presented in section 2, more precisely the variance reduction based on translation of the density (see Subsection 2.3) and the one based on the Esscher transform (see Subsection 2.4), by the following simplified (no computation of the variance) pseudo-code:

Translation (see 2.3)

-

–

Translation case. We consider the function of the Robbins-Monro procedure of the first algorithm defined by

where an analytic formulation of the derivative is easily obtained using the relation on the modified Bessel function .

The assumption () is satisfied with , and our results of Subsection 2.3 apply.

-

–

Esscher transform. In the Esscher approach we consider the function defined by

Note that is not well defined for every . Indeed, the cumulant generating function of the NIG distribution is defined by

for every . Moreover, we need to be well defined i.e. . To take account of these restrictions, we slightly modify the algorithm parametrization (see Subsection 4.3) , and update in the Robbins-Monro procedure (multiply the function by the derivative ).

The payoff is a Call option of strike , . The parameters of the NIG random variable are , , and . The variance reduction obtained for different value of are summarized in the tabular 1. The number of iterations in the Robbins-Monro variance reduction procedure is and the number of Monte Carlo iterations is . Note that for each strike, the prices are computed using the same pseudo-random number generator initialized with the same seed.

| K | mean | crude var | var. ratio. | var. ratio | ||

|---|---|---|---|---|---|---|

| translation | () | Esscher | () | |||

| 0.6 | 42.19 | 8538 | 5.885 | (0.791) | 56.484 | (1.322) |

| 0.8 | 34.19 | 8388 | 7.525 | (0.903) | 39.797 | (1.309) |

| 1.0 | 27.66 | 8176 | 9.218 | (0.982) | 32.183 | (1.294) |

| 1.2 | 22.60 | 7930 | 10.068 | (1.017) | 29.232 | (1.280) |

| 1.4 | 18.76 | 7677 | 9.956 | (1.026) | 28.496 | (1.268) |

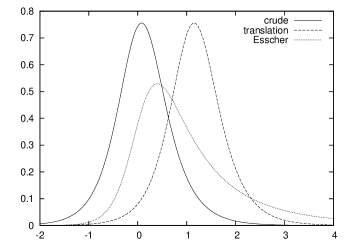

To complete this numerical example, Figure 1 illustrates the densities obtained after the Robbins-Monro procedure. The deformation provided by the Esscher transform is very impressive in this example. We remark that the Esscher transform modifies the parameter which controls the asymmetric shape of the NIG distribution.

Spark spread

We consider now a exchange option between gas and electricity (called spark spread). We choose to model the price of the energy by the exponential of a distribution. A simplified form of the payoff is then

where and are independent.

The results obtained for different strikes after iterations of the Robbins-Monro procedure and iterations of Monte Carlo, are summarized in the Table 2.

| K | c | mean | crude var | var. ratio. | var. ratio |

|---|---|---|---|---|---|

| translation | Esscher | ||||

| 0.4 | 0.2 | 41.021 | 8540.6 | 5.0118 | 25.171 |

| 0.4 | 32.719 | 8356.9 | 5.1338 | 27.006 | |

| 0.6 | 26.337 | 8112.2 | 4.9752 | 28.062 | |

| 0.8 | 21.556 | 7845.3 | 4.7569 | 29.964 | |

| 1 | 17.978 | 7582 | 4.5575 | 32.849 | |

| 0.6 | 0.2 | 33.235 | 8378.4 | 5.2609 | 27.455 |

| 0.4 | 26.534 | 8133.3 | 5.0604 | 28.669 | |

| 0.6 | 21.587 | 7862.7 | 4.8046 | 30.649 | |

| 0.8 | 17.931 | 7595.2 | 4.5839 | 33.656 | |

| 1 | 15.184 | 7344.2 | 4.4064 | 37.489 | |

| 0.8 | 0.2 | 26.908 | 8160.1 | 5.1366 | 28.876 |

| 0.4 | 21.725 | 7884.9 | 4.844 | 31.018 | |

| 0.6 | 17.955 | 7612.5 | 4.6031 | 34.166 | |

| 0.8 | 15.156 | 7357.3 | 4.416 | 38.167 | |

| 1 | 13.027 | 7123.9 | 4.2685 | 42.781 |

5.2 Functional setting: Down & In Call option

We consider a process solution of the following diffusion

A Down & In Call option of strike and barrier is a Call of strike which is activated when the underlying moves down and hits the barrier . The payoff of such a European option is defined by

A naive Monte Carlo approach to price this option is to consider an Euler-Maruyama scheme to discretize and to approximate by . It is well known that this approximation of the functional payoff is poor. More precisely, the weak order of convergence cannot be greater than (see [11]).

A standard approach is to consider the continuous Euler scheme obtained by extrapolation of the Brownian between two instants of discretization. More precisely, for every ,

By preconditioning,

| (5.32) |

with . Now using the Girsanov Theorem and the law of the Brownian bridge (see for example [9]), we have

| (5.33) | ||||

In the following simulations we consider an Euler scheme of step with .

Deterministic case (trivial driver )

We consider three different basis of

-

–

a polynomial basis composed of the shifted Legendre polynomials defined by

(ShLeg) -

–

the Karhunen-Loève basis defined by

(KL) -

–

the Haar basis defined by

(Haar) where

Black&Scholes Model

First, we consider the classical Black&Scholes model. We set the interest rate to and the volatility to (which is a high volatility).

The strike of the payoff is set at and the barrier level at . A crude Monte Carlo (with Brownian bridge interpolation, see (5.32)) give a price of with a variance of after trials. Note that the true price of this product is .

For different basis, the results of our algorithm are summarized in the table 3. In the Robbins-Monro procedure, we define the step sequence by and set the number of iterations at .

| Basis | Dim. | Mean | CI | Variance ratio |

|---|---|---|---|---|

| Constant | 1 | 2.5737 | 0.0230 | 3.4710 |

| ShiftLegendre | 2 | 2.5741 | 0.0197 | 4.7225 |

| (ShLeg) | 4 | 2.5717 | 0.0193 | 4.9478 |

| 8 | 2.5717 | 0.0193 | 4.9494 | |

| Karhunen-Loève | 2 | 2.5678 | 0.0164 | 6.8644 |

| (KL) | 4 | 2.5729 | 0.0160 | 7.1851 |

| 8 | 2.5705 | 0.0156 | 7.5218 | |

| Haar | 2 | 2.5657 | 0.0192 | 4.9710 |

| (Haar) | 4 | 2.5671 | 0.0163 | 6.9459 |

| 8 | 2.5663 | 0.0155 | 7.6574 |

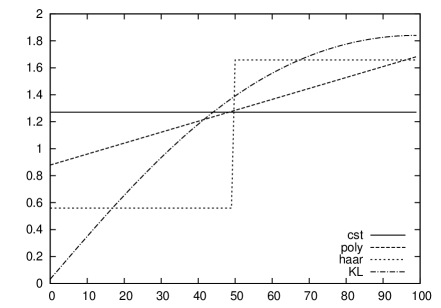

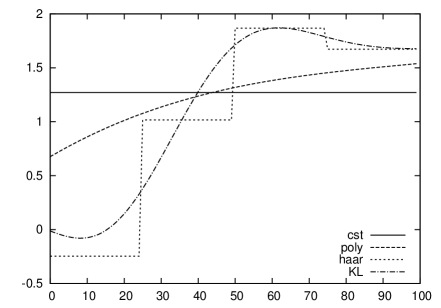

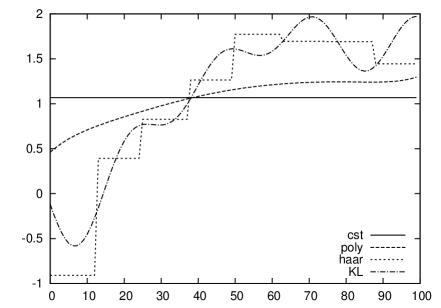

In figure 2 are depicted the optimal variance reducer when the optimization of is carried out on for several values of (2, 4 and 8) in the different basis mentioned above.

A local volatility Model

To emphasize the generic feature of our algorithm we consider the same product in a local volatility model (inspired by the CEV model) defined by

| (5.34) |

with , and .

The price of the Down & In Call (strike 115, barrier 65) given by a crude Monte Carlo with Brownian interpolation after trials is and the variance is .

| Basis | Dim. | Mean | CI | Variance ratio |

|---|---|---|---|---|

| Constant | 1 | 3.1836 | 0.0251 | 2.6297 |

| ShiftLegendre | 2 | 3.1830 | 0.0223 | 3.3258 |

| (ShLeg) | 4 | 3.1815 | 0.0215 | 3.5670 |

| 8 | 3.1813 | 0.0215 | 3.5659 | |

| Karhunen-Loève | 2 | 3.1852 | 0.0187 | 4.7254 |

| (KL) | 4 | 3.1862 | 0.0183 | 4.9385 |

| 8 | 3.1918 | 0.0178 | 5.2183 | |

| Haar | 2 | 3.1834 | 0.0215 | 3.5699 |

| (Haar) | 4 | 3.1871 | 0.0186 | 4.7896 |

| 8 | 3.1864 | 0.0177 | 5.2675 |

Adaptive case (non-trivial driver)

We experiment now our algorithm with a non-trivial driver defined for by

where is defined by (5.33). Note that so that there is no extra-computation compared to the Brownian bridge interpolation.

We set and so that the optimal parameter with . The results for different strikes and barrier levels are reported in Table 5 for the Black&Scholes model and in Table 6 for the local volatility model. The simulation parameters are unchanged.

| Strike | Barrier | Mean | CI 95 | Variance ratio (Crude) | |||

| 85 | 65 | 2.5738 | 0.0115 | 13.49 | (16.56) | -0.1752 | 1.6685 |

| 75 | 6.0489 | 0.0186 | 14.26 | (43.39) | 0.0493 | 1.9191 | |

| 95 | 65 | 2.5704 | 0.0110 | 14.64 | (15.26) | 0.0524 | 1.9987 |

| 75 | 6.0492 | 0.0190 | 13.67 | (45.25) | 0.1557 | 2.0560 | |

| 85 | 11.5970 | 0.0301 | 12.23 | (112.92) | 0.4108 | 2.1226 | |

| 105 | 65 | 2.5687 | 0.0122 | 12.03 | (18.56) | 0.3888 | 2.1423 |

| 75 | 6.0548 | 0.0206 | 11.66 | (53.08) | 0.3895 | 2.1720 | |

| 85 | 11.5953 | 0.0308 | 11.67 | (118.32) | 0.4524 | 2.1608 | |

| 95 | 19.2882 | 0.0348 | 17.17 | (151.04) | 0.6619 | 1.7910 | |

| 115 | 65 | 2.5706 | 0.0135 | 9.75 | (22.90) | 0.5473 | 1.8903 |

| 75 | 6.0530 | 0.0211 | 11.16 | (55.42) | 0.4591 | 1.9371 | |

| 85 | 11.5976 | 0.0297 | 12.55 | (109.98) | 0.4807 | 2.0008 | |

| 95 | 19.2958 | 0.0347 | 17.21 | (150.67) | 0.7217 | 1.6380 | |

| Strike | Barrier | Mean | CI 95 | Variance ratio (Crude) | |||

| 85 | 65 | 3.1827 | 0.0127 | 10.02 | (20.28) | -0.3057 | 1.5522 |

| 75 | 6.4115 | 0.0190 | 9.96 | (45.03) | -0.1428 | 1.7985 | |

| 95 | 65 | 3.1846 | 0.0124 | 10.65 | (19.08) | -0.1141 | 1.9139 |

| 75 | 6.4117 | 0.0199 | 9.07 | (49.42) | -0.0029 | 1.9814 | |

| 85 | 11.4478 | 0.0293 | 8.03 | (106.99) | 0.1898 | 1.8937 | |

| 105 | 65 | 3.1835 | 0.0135 | 8.98 | (22.65) | 0.1487 | 1.9628 |

| 75 | 6.4120 | 0.0209 | 8.21 | (54.59) | 0.1493 | 2.0060 | |

| 85 | 11.4458 | 0.0295 | 7.88 | (108.94) | 0.2503 | 1.8737 | |

| 95 | 18.6060 | 0.0345 | 9.83 | (149.07) | 0.5594 | 1.4343 | |

| 115 | 65 | 3.1817 | 0.0148 | 7.38 | (27.54) | 0.3062 | 1.6884 |

| 75 | 6.4112 | 0.0209 | 8.18 | (54.79) | 0.1928 | 1.8119 | |

| 85 | 11.4470 | 0.0289 | 8.24 | (104.16) | 0.2599 | 1.7430 | |

| 95 | 18.6061 | 0.0346 | 9.79 | (149.76) | 0.5755 | 1.4313 | |

References

- [1] C. Andrieu, É. Moulines, P. Priouret (2005). Stability of stochastic approximation under verifiable conditions. SIAM J. Control Optim., 44(1), no. 1, 283–312 (electronic).

- [2] B. Arouna (2004). Adaptative Monte Carlo method, a variance reduction technique. Monte Carlo Methods and Appl., 10(1), 1–24.

- [3] N. Bouleau, D. Lépingle (1994). Numerical methods for stochastic processes, Wiley Series in Probability and Mathematical Statistics: Applied Probability and Statistics. A Wiley-Interscience Publication. John Wiley & Sons, Inc., New York, 359 pp. ISBN: 0-471-54641-0.

- [4] B. Arouna, O. Bardou (2004). Efficient variance reduction for functionals of diffusions by relative entropy, technical report, CERMICS-ENPC (France).

- [5] M. Benveniste, M. Métivier, P. Priouret (1990). Adaptive algorithms and stochastic approximation, 22, Applications of Mathematics, transl. from French by S. Wilson, Springer-Verlag, Berlin.

- [6] H. Chen, Y. Zhu (1986). Stochastic Approximation Procedure with randomly varying truncations, Scientia Sinica Series.

- [7] H. F. Chen, G. Lei, A.J. Gao (1988). Convergence and robustness of the Robbins-Monro algorithm truncated at randomly varying bounds, Stoch. Proc. Appl., 27(2), 217–231.

- [8] M. Duflo (1997). Iterative random models, transl. from French, Springer-Verlag.

- [9] P. Glasserman (2004). Monte Carlo Methods in Financial Engineering, Springer.

- [10] P. Glasserman, P. Heidelberger, P. Shahabuddin (1999). Asymptotically optimal importance sampling and stratification for pricing path-dependent options. Math. Finance 9(2), no. 2, 117–152.

- [11] E. Gobet (2000). Weak approximation of killed diffusion using Euler schemes, Stoch. Proc. Appl., 87(2), 167–197.

- [12] R. Kawai (2008). Optimal importance sampling parameter search for Lévy Processes via stochastic approximation, pre-print.

- [13] H.J. Kushner, G. Yin (2003). Stochastic Approximation and Recursive Algorithms and Applications, Springer.

- [14] J. Lelong (2007). Algorithmes stochastiques et Options parisiennes, thèse de l’ENPC, 151p.

- [15] V. Lemaire (2007). An adaptive scheme for the approximation of dissipative systems, Stoch. Proc. Appl., 117(10), 1491–1518.

- [16] D. Revuz, M. Yor (1998). Continuous martingales and Brownian motion, edition, Springer, Berlin, 1998 ( edition, 1990).

- [17] M. Pelletier (2000). Asymptotic almost sure efficiency of averaged stochastic algorithms. SIAM J. Control Optim. 39(1), 49–72 (electronic).

- [18] L.C.G. Rogers, D. Williams (1986). Diffusions, Markov Processes and Martingales, edition, Cambridge Mathematical Library.

6 Appendix: proof of Theorem 1

We propose below the proof of the slight extension of the regular Robbins-Monro algorithm when is not reduced to a single equilibrium point. The key is still the convergence theorem for non negative super-martingales.

Proof. Set , . Let . Then

| (6.35) |

where

is an increment of (local) martingale satisfying owing to the assumptions on and Schwarz Inequality which also implies that

for an appropriate real constant . Then, one shows by induction on from (6.35) that is square integrable for every and that is integrable, hence a true martingale increment. Now, one derives from the assumptions (2.6) and (6.35) that

is a (non negative) super-martingale with . This uses the mean-reverting assumption (2.5). Hence is - converging toward an integrable r.v. . Consequently, using that , one gets

| (6.36) |

The super-martingale being -bounded, one derives likewise that is -bounded since

Now, a series with nonnegative terms which is upper bounded by an () converging sequence, converges in so that

It follows from (6.36) that, -, which is integrable since is -bounded and consequently finite.

Let . Set

It follows from the finiteness of that . Now we consider the compact set . It is separable so there exists an everywhere dense sequence in , denoted for convenience . The above proof shows that -, for every , as . Then set

which satisfies . Assume . Up to two successive extractions, there exists a subsequence such that

The function being continuous which implies that . Hence . Then any limiting value of the sequence will satisfy

which in turn implies that by considering a subsequence . So, is the unique limiting value of the sequence as . The fact that the resulting random vector is square integrable follows from Fatou’s Lemma and the -boundedness of the sequence .