Localisable moving average symmetric

stable and multistable processes

Abstract

We study a particular class of moving average processes which possess a property called localisability. This means that, at any given point, they admit a “tangent process”, in a suitable sense. We give general conditions on the kernel defining the moving average which ensures that the process is localisable and we characterize the nature of the associated tangent processes. Examples include the reverse Ornstein-Uhlenbeck process and the multistable reverse Ornstein-Uhlenbeck process. In the latter case, the tangent process is, at each time , a Lévy stable motion with stability index possibly varying with . We also consider the problem of path synthesis, for which we give both theoretical results and numerical simulations.

1 Introduction and background

In this work, we study moving average processes which are localisable. Loosely speaking, this means that they have a well-defined local form: at each point, they are “tangent” to a given stochastic process.

Localisable processes are useful both in theory and in practical applications. Indeed, they provide an easy way to control important local properties such as the local Hölder regularity or the jump intensity. In the first case, one speaks of multifractional processes, and in the second one, of multistable processes. Such processes provide fine models for real world phenomena including natural terrains, TCP traffic, financial data, EEG or highly textured images.

Formally, a process defined on (or a subinterval of ) is -localisable at if exists as a non-trivial process in for some , where the convergence is in finite dimensional distributions, see [3, 4]. When convergence occurs in distribution with respect to the appropriate metric on (the space of continuous functions on ) or on (the space of càdlàg functions on , that is functions which are continuous on the right and have left limits at all ), we say that is strongly localisable. The limit, denoted by , is called the local form or tangent process of at and will in general vary with . A closely related notion is that of locally asymptotically self-similar processes, which are for instance described in [2].

The simplest localisable processes are self-similar processes with stationary increments (sssi processes); it is not hard to show that an sssi process is localisable at all with local form . Furthermore, an sssi process is strongly localisable if it has a version in or .

In [5], processes with prescribed local form are constructed by “gluing together” known localisable processes in the following way: let be an interval with an interior point. Let be a random field and let be the diagonal process . In order for and to have the same local forms at , that is where is the local form of at , we require

| (1.1) |

as .

This approach allows easy construction of localisable processes from “elementary pieces” which are known to be themselves localisable. In particular, it applies in a straightforward way to processes such that is sssi for each .

In this work we shall study a rather different way of obtaining localisable processes. Instead of basing our constructions on existing sssi processes we will consider moving average processes which, as we shall see, provide a new class of localisable -stable processes.

The remainder of this paper is organized as follows: in section 2, we give general conditions on the kernel defining the moving average process to ensure (strong) localisability. Section 3 specializes these conditions to cases where explicit forms for the tangent process may be given, and presents some examples. In section 4, we deal with multistable moving average processes, which generalize moving average stable processes by letting the stability index vary over time. Finally, section 5 considers numerical aspects: for applications, it is desirable to synthesize paths of these processes. Using the approach developed in [12], we first explain how to build traces of arbitrary moving average stable processes. In the case where the processes are localisable, we then give error bounds between the numerical and theoretical paths. Under mild additional assumptions, an ‘optimal’ choice of the parameters defining the synthesis method is derived. Finally, traces obtained from numerical experiments are displayed.

2 Localisability of stable moving average processes

Recall that a process , where is a subinterval of , is called -stable if all its finite-dimensional distributions are -stable, see the encyclopaedic work on stable processes [10]. -stable processes are just Gaussian processes.

Many stable processes admit a stochastic integral representation. Write for the -stable distribution with scale parameter , skewness and shift-parameter ; we will assume throughout that . Let be a sigma-finite measure space ( will be Lebesgue measure in our examples). Taking as the control measure, this defines an -stable random measure on such that for we have that (since , the process is symmetric).

Let

where is the quasinorm (or norm if ) given by

| (2.1) |

The stochastic integral of with respect to then exists [10, Chapter 3] with

| (2.2) |

where .

We will be concerned with a special kind of stable processes that are stationary and may be expressed as moving average stochastic integrals in the following way:

| (2.3) |

where is sometimes called the kernel of .

Such processes are considered in several areas (e.g. linear time-invariant systems) and it is of interest to know under what conditions they are localisable. A sufficient condition is provided by the following proposition.

Proposition 2.1

Let and let be a symmetric -stable measure on with control measure Lebesgue measure . Let and let be the moving average process

Suppose that there exist jointly measurable functions such that

| (2.4) |

for all , where . Then is -localisable with local form at all .

Proof. Using stationarity followed by a change of variable and the self-similarity of ,

where equalities are in finite dimensional distributions. Thus

By [10, proposition 3.5.1] and (2.4), in probability and thus in finite dimensional distributions.

A particular instance of (2.3) is the reverse Ornstein-Uhlenbeck process, see [10, Section 3.6]. This process provides a straightforward application of proposition 2.1.

Proposition 2.2

(Reverse Ornstein-Uhlenbeck process) Let and and let be an -stable measure on with control measure . The stationary process

has a version in that is -localisable at all with , where is -stable Lévy motion.

Proof. The process is a moving average process that may be written in the form (2.3) with . It is easily verified using the dominated convergence theorem that satisfies (2.4) with and for and for , so proposition 2.1 gives the conclusion with for and a similar formula for .

Proposition 2.1 gives a condition on the kernel ensuring localisability. With an additional constraint we can get strong localisability. First we need the following proposition on continuity.

Proposition 2.3

Let , and let be an -stable symmetric random measure on with control measure . Consider the moving average process defined by (2.3). Suppose that satisfies, for all sufficiently small ,

where and . Then has a continuous version which satisfies a -Hölder condition for all .

Proof. By stationarity,

So for

The result then follows from the Kolmogorov criterion by taking arbitrarily close to .

Proposition 2.4

With the same notation and assumptions as in proposition 2.1, suppose that in addition that satisfies, for all sufficiently small ,

| (2.5) |

where and . Then has a version in that is -strongly localisable with at all .

Proof. By proposition 2.3, has a continuous version and so also has a continuous version. Thus, for , by stationarity and setting sufficiently small,

provided is sufficiently small, using (2.5) in the last step. We may choose sufficiently close to so that . By a Corollary to Kolmogorov’s criterion (see e.g. [9, Theorem 85.5]) the measures on underlying the processes are conditionally compact. Thus convergence in finite dimensional distributions of to as implies the convergence in distribution (with necessarily having a continuous version). Together with localisability which follows from proposition 2.1 this gives strong localisability.

Note that the reverse Ornstein-Uhlenbeck process is a stationary Markov process which has a version in see [11, Remark 17.3]. It also satisfies (2.5) for with . However, we cannot deduce that it is strongly localisable since proposition 2.4 is only valid for . The case would be interesting to deal with, but is much harder and would require different techniques.

3 Sufficient conditions for localisability and examples

For the reverse Ornstein-Uhlenbeck process, it was straightforward to check the conditions of proposition 2.1. In general, however, it is not easy to guess which kind of functions in will satisfy (2.4). In this section we will find simple practical conditions ensuring this.

Recall that the following process is called linear fractional -stable motion:

where , , and

| (3.1) |

where is a symmetric -stable random measure with control measure Lebesgue measure. Being sssi, is localisable. In addition, it is strongly localisable when , since its paths then belong to .

Recall also that the process

| (3.2) |

is -stable Lévy motion and the process

| (3.3) |

is called log-fractional stable motion.

We are now ready to describe easy-to-check conditions that ensure that propositions 2.1 and 2.4 apply.

Proposition 3.1

Let , and be an -stable symmetric random measure on with control measure . Let be the moving average process

If there exist with , and such that

as and

| (3.4) |

then is -localisable at all with local form

If, in addition, and then has a version in and is strongly localisable.

Note that condition (3.4) on the increments of may be interpreted as a 2-microlocal condition, namely that belongs to the global 2-microlocal space , see [7]. Remark also that, in order for this condition to be satisfied by non-trivial functions , one needs , which in turns implies that and .

Proof (a) We have

As ,

To get convergence in we use the dominated convergence theorem. Fix and such that for all ,

For fixed write . If ,

thus which belongs to . Assume now . There is a constant such that for all and . From (3.4)

for , so, as and ,

Since also , the dominated convergence theorem implies that in . The conclusion in case (a) follows from proposition 2.1, (3.1), and noting that is a symmetric -stable measure.

(b) In this case the limit (3) is

Dominated convergence follows in the same way as in case (a) so the conclusion follows from proposition 2.1 and (3.2).

Moving to strong localisability, for small enough,

and

We now give an alternative condition for localisability in terms of Fourier transforms. Note that the Fourier transform of is given by

Proposition 3.2

Let , and be defined by (2.3). If there exist , , and with , such that for almost all ,

| (3.6) |

then is -localisable at all with local form

where

Proof (a) First note that, with and as above, we have, for ,

Set . Then and

With such that we have and . We now show that when . Note that (3.6) implies that for

Writing , for almost all

Let . Then and we may write for

| (3.7) |

where .

It is easy to verify that for all . By the conditions on and , there exists such a which also satisfies and in particular, . Consequently we may take the inverse Fourier transform of (3.7) see, for example, [13, Theorem 78] to get:

where denotes convolution. As , the Hausdorff-Young inequality yields

We conclude that in . The result follows from proposition 2.1. The case is dealt with in a similar way.

(b) Let and be defined by

and

A straightforward computation shows that

so that, in the space of distributions we get

where PV denotes the Cauchy principal value. Thus

With , we obtain

As in (a) we conclude that in . proposition 2.1 implies that is -localisable at all with local form , since is symmetric.

Example 3.3

Let and let be an -stable symmetric random measure on with control measure . Let

The stationary process defined by

is -strongly localisable at all with local form .

Proof. We apply proposition 3.1 case (a) with . The function satisfies the assumptions with , , and .

To verify condition (3.6) of proposition 3.2, one needs to check that and also that is the Fourier transform of a function in for some in the admissible ranges. For this purpose, one may for instance apply classical theorems such as in [13, Theorems 82-84]. We give below an example that uses a direct approach.

Example 3.4

For let be an -stable symmetric random measure on with control measure . Let be defined by its Fourier transform

where . Then and the moving average process

is well-defined and -localisable at all , with local form , where .

Proof. Taking with and in (3.6) gives . To check that for all , note that is continuous (in fact ) and that for all . Then will be well-defined if is in . To verify this, one computes the inverse Fourier transform of , to get . By proposition 3.2(a), is -localisable at all with the local form as stated.

The approach of this example may be be used for general classes of functions .

4 Multistable moving average processes

In [5], localisability is used to define multistable processes, that is processes which at each point have an -stable random process as their local form, where is a sufficiently smooth function ranging in . Thus such processes “look locally like” a stable process at each but with differing stability indices as time evolves.

Before we recall how this was done in [5], we note briefly that “stable-like” processes have been defined and studied in [8]. These stable-like processes are Markov jump processes, and are, in a sense, “localisable”, but with localisability defined by the requirement that they are solutions of an order fractional stochastic differential equations. See Theorem 2.1 in [8], which shows that the local form of sample paths is considered rather than of the limiting process. Another essential difference is that stable-like processes are Markov, whereas, in general, multistable ones, as defined below, are not. In fact, formula (4.6), where a Poisson process element Y is independent of t but is raised to a power that involves t means that our processes are “far” from Markov.

We now come back to our multistable processes. One route to defining such processes is to rewrite stable integrals as countable sums over Poisson processes. We recall briefly how this can be done, see [5] for fuller details. Let be a -finite measure space and let be a Poisson process on with mean measure . Thus is a random countable subset of such that, writing for the number of points in a measurable , the random variable has a Poisson distribution of mean with independent for disjoint , see [6]. In the case of constant , with a symmetric -stable random measure on with control measure , one has, for ([10, Section 3.12]),

| (4.1) |

where

| (4.2) |

and .

Now define the random field

| (4.3) |

Under certain conditions the “diagonal” process gives rise to a multistable process with varying of the form

| (4.4) |

Theorem 5.2 of [5] gives conditions on that ensure that is localisable (or strongly localisable) with at a given , provided is itself localisable (resp. strongly localisable) at . These conditions simplify very considerably in the moving average case, taking and with . Our next theorem restates [5, Theorem 5.2] in this specific situation.

We need first to define a quasinorm on certain spaces of measurable functions on . For let

where

| (4.5) |

Theorem 4.1

(Multistable moving average processes) Let be a closed interval with an interior point. Let satisfy

where . Let , and define

| (4.6) |

Assume that satisfies

| (4.7) |

for jointly measurable functions , where . Then is -localisable at with local form , where is the symmetric -stable measure with control measure and skewness .

Suppose further that and for sufficiently small

Then has a continuous version and is strongly -localisable at with local form under either of the following additional conditions:

and is bounded

and is continuously differentiable on with

where .

Proof. Taking

| (4.8) |

this theorem is essentially a restatement of [5, Theorem 5.2] in the special case of and with in (4.3). Since no longer depends on most of the conditions in [5, Theorem 5.2] are trivially satisfied and we conclude that , noting that is -localisable (or strongly localisable) with the local form given by propositions 2.1 or 2.4.

It is curious that neither cases (i) or (ii) address localisability if . This goes back to the proof of [3, Theorem 5.2] where different approaches are used in the two cases. For the proof uses that the sum (4.8) is absolutely convergent almost surely, whereas for we need to find a number such that for near with to enable us to apply Kolmogorov’s criterion to certain increments.

Corollary 4.2

Proof. This follows easily in just the same way as proposition 2.2 of [5].

We may apply this theorem to get a multistable version of the reverse Ornstein-Uhlenbeck process considered in Section 2:

Proposition 4.3

(Multistable reverse Ornstein-Uhlenbeck process) Let and be continuously differentiable. Let

Then is -localisable at all with , where is -stable Lévy motion.

5 Path synthesis and numerical experiments

We address here the issue of path simulation. In the previous sections, we have considered two kinds of stochastic processes: moving average stable ones, that are stationary, and their multistable versions, which typically are not, nor have stationary increments. Our simulation method for the moving average stable processes is based on that presented in [12]. There, the authors propose an efficient algorithm for synthesizing paths of linear fractional stable motion. In fact, this algorithm really builds traces of the increments of linear fractional stable motion. These increments form a stationary process, an essential feature for the algorithm to work. It is straightforward to modify it to synthesize any stationary stable process which possesses an integral representation. In addition, we are able to obtain bounds on the approximation error measured in the -norm, and thus on the moments for , as shown below.

For non (increment) stationary processes, like multistable processes, a possibility would be to use the general method proposed in [1]. It allows to synthesize (fractional) fields defined by integration of a deterministic kernel with respect to a random infinitely divisible measure. When the control measure is finite, the idea is to approximate the integral with a generalized shot noise series. In this situation, a bound on the norm of the error is obtained for appropriate . In the case of infinite control measure, one needs to deal with the points “far from the origin” through a normal approximation. This second approximation maybe controlled through Berry-Esseen bounds which lead to a convergence in law. Thus the overall error when the control measure is infinite may only be assessed in law, and not in the stronger norm.

Although the method of [1] may be used for the synthesis of multistable processes, we will rather take advantage here of the particular structure of our processes: being localisable, they are by definition tangent, at each point, to an increment stationary process. Thus we may simulate them by “gluing” together in a appropriate way paths of their tangent processes, which are themselves synthesized through the simpler procedure of [12]. This approach allows in addition to control the error in the norm, rather than only in law (since we are in an infinite control measure case).

We briefly present in the next subsection the main ingredients of the method. We then give bounds estimating the errors entailed by the numeric approximation, in the case where the process is localisable. Finally, we display graphs of localisable moving average processes obtained with this synthesis scheme.

5.1 Simulation of stable moving averages

Let be the process defined by (2.3). To synthesize a path , of , the usual (Euler) method consists in approximating the integral by a Riemann sum. Two parameters tune the precision of the method: the discretization step and the cut-off value for the integral . The idea in [12] is to use the fast Fourier transform for an efficient computation of the Riemann sum. More precisely, let

Let and

| (5.1) |

where are i.i.d. -stable symmetric random variables. Let denote a sequence of normalised i.i.d -stable symmetric random variables. Then one has the equality in law: . One may thus write:

where

For , let

Then has the same law as . But is the convolution product of the sequences and . As such, it may be be efficiently computed through a fast Fourier transform. See [12] for more details.

5.2 Estimation of the approximation error

When the moving average process is localisable, or more precisely when the conditions of proposition 3.1 are satisfied, it is easy to assess the performances of the above synthesis method.

The following proposition gives a bound on the approximation error in the norm. Recall that the norm (defined in (2.1)) is just the scale factor of the random variable, and is thus independent of the integral representation that is used. In addition, it us, up to a constant depending on and , an upper bound on moments of order .

Proposition 5.1

Proof. By stationarity and independence of the increments of Lévy motion, one gets:

| (5.2) |

By assumption, for almost all , when . Recall that . A change of variables yields

and thus

Rearranging terms:

which is the stated result.

Corollary 5.2

Under the conditions of proposition 5.1, when tends to infinity.

If in addition when for some and , then:

| (5.3) |

where is a constant independent of .

Proof. Since satisfies the assumptions of proposition 3.1, . As a consequence, the sum in the first term of converges when tends to infinity. The first statement then follows from the facts that and . The second part follows by making the obvious estimates.

The significance of (5.3) is that it allows us to tune and to obtain an optimal approximation, provided a bound on the decay of at infinity is known: optimal pairs are those for which the two terms in (5.3) are of the same order of magnitude. More precisely, if the value of is sharp, the order of decay of the error will be maximal when . Note that the exponent is always positive, as expected. Intuitively, is related to the regularity of (irregular requires larger ), while is linked with the rate of decay of at infinity.

For concreteness, let us apply these results to some specific processes:

Example 5.3

However, we may obtain a more precise bound on the approximation error, valid for any , by using (5.2) directly:

When , , which is better than above when .

We note finally that the optimal choice for is here , which is consistent with the fact that the in Corollay 5.2 may be chosen arbitrarily large.

Example 5.4

(linear fractional stable noise) Let and let be an -stable symmetric random measure on with control measure . Let:

and

Applying the analysis above with , ,, one gets, for , ,

When ,

This process is the one considered in [12]. Here we reach a conclusion similar to [12, Theorem 2.1], which yields the same order of magnitude for the error when . Extensive tests are conducted in [12] to choose the best values for . The criterion for optimizing these parameters is to test how an estimation method for performs on synthesized traces. Here we adopt a different approach based on Corollary 5.2: optimal pairs are those for which (5.3) is minimized. Since the value of is sharp here, one gets . It is interesting to note that the exponent depends only on the scaling factor and not on , and that it may be larger or smaller than one depending on the value of . We do not have an explanation for this fact nor for the reason why plays a special rôle.

Example 5.5

As a final illustration, we consider the process of Example 3.3. With , ,,, one gets, for , ,

Again, the value of is sharp, and the optimal choice is to set . Since , is larger than in this case, in contrast to the reverse Ornstein-Uhlenbeck process: it is the decay at infinity of the kernel that dictates the parameters here, while it was the regularity that mattered in the case of the reverse Ornstein-Uhlenbeck process.

5.3 Numerical experiments

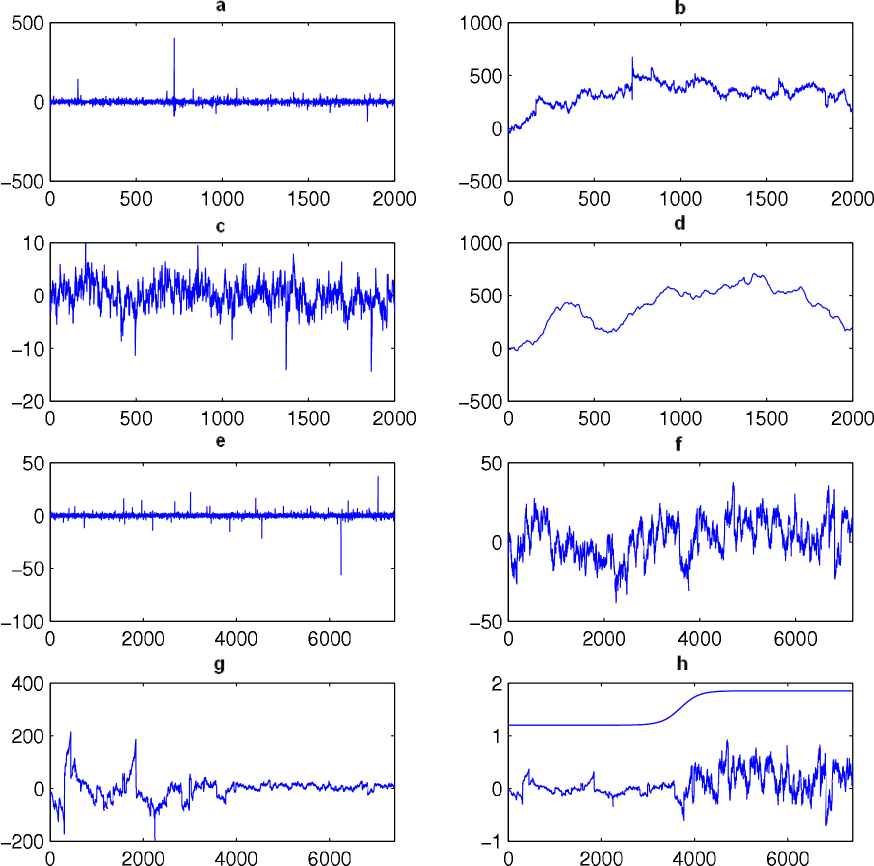

We display in figure 1 traces of:

-

•

moving average stable processes: the reverse Ornstein-Uhlenbeck process (figures 1(e),(f)), and the processes of Examples 3.3 (figure 1(c)) and 3.4 (figure 1(a)). In each case, . Some of the relevant features of the processes of Examples 3.3 and 3.4 seem to appear more clearly when one integrates them. Thus integral versions are displayed in the right-hand part of the corresponding graphs, figures 1(b),(d).

-

•

a multistable version of the reverse Ornstein-Uhlenbeck process, using the theory developed in Section 4 (figures 1(g),(h)). Since these processes are localisable, one may obtain paths by computing first stable versions with all values assumed by , and then “gluing” these tangent processes together as appropriate. More precisely, assume we want to obtain the values of a multistable process at the discrete points . At each , is tangent to a stable process denoted . We first synthesize the stable processes with the method just described, all with the same random seed. The multistable process is then obtained by setting . Two graphs are displayed for the multistable process: in figure 1(g) the graphs are as explained above. In figure 1(h) each “line” of the random field (i.e. the process obtained for a fixed value of ) is renormalized so that it ranges between -1 and 1, prior to building the multistable process by gluing the paths as appropriate. This renormalization may be justified using Corollary 4.2.

The parameters are as follows:

-

•

Process of Example 3.4: , , . The approximation error is bounded by 2.172.

-

•

Process of Example 3.3: , . The term is equal to 0.074.

-

•

Reverse Ornstein-Uhlenbeck process with . The term is equal to 0.0018.

-

•

Reverse Ornstein-Uhlenbeck process with . The term is equal to 0.0032.

-

•

Multistable reverse Ornstein-Uhlenbeck process: . The function is the logistic function starting from 1.2 and ending at 1.85. More precisely, we take: , where is the number of points and ranges from 1 to (the graph of is plotted in figure 1(h). Thus, one expects to see large jumps at the beginning of the paths and smaller ones at the end. Note that we do not have any results concerning the approximation error for these non-stationary processes.

The value of in all cases is adjusted so that the pair is approximately “optimal” as described in the preceding subsection (optimality is not guaranteed for the multistable processes. Nevertheless, since the relation between and does not depend on for the reverse Ornstein-Uhlenbeck process, it holds in this case).

The function of example 3.4 cannot be treated using corollary 5.2 nor proposition 5.1 since does not satisfy the conditions of proposition 3.1. However, it is possible to estimate directly. Since and , one gets:

The asymptotic optimal relation between and is thus . The values in our simulation are slightly different since they are chosen to optimize the actual expression with a finite .

Finally, we stress that the same random seed (i.e. the same underlying stable ) has been used for all simulations, for easy comparison. Thus, for instance, the jumps appear at precisely the same locations in each graph. Notice in particular the ranges assumed by the different processes.

The differences between the graphs of the processes of Examples 3.3, 3.4 and the reverse Ornstein-Uhlenbeck process are easily interpreted by examining the three kernels: the kernel of the process of Example 3.4 diverges at 0, thus putting more emphasis on strong jumps, as seen on the picture, with more jaggy curves and an “antipersistent” behaviour. The kernel of the process of Example 3.3, in contrast, is smooth at the origin. In addition, it has a slow decay. These features result in an overall smoother appearance and allow “trends” to appear in the paths. Finally, the kernel of the reverse Ornstein-Uhlenbeck process has a decay controlled by . For “large” (here, ), little averaging is done, and the resulting path is very irregular. For “small” (here, ), the kernel decays slowly and the paths look smoother (recall that, in the Gaussian case, the Ornstein-Uhlenbeck tends in distribution to white noise when tends to infinity, and to Brownian motion when tends to 0).

References

- [1] Cohen, S. and Lacaux, C. and Ledoux, M. (2008). A general framework for simulation of fractional fields. Stochastic Process. Appl., (118) 9, 1489 1517.

- [2] Cohen, S. (1999) From self-similarity to local self-similarity: the estimation problem, Fractal in Engineering, J. Lévy Véhel, E. Lutton and C. Tricot (eds.), Springer Verlag.

- [3] Falconer, K.J. (2002). Tangent fields and the local structure of random fields. J. Theoret. Probab. 15, 731–750.

- [4] Falconer, K.J. (2003). The local structure of random processes. J. London Math. Soc.(2) 67, 657–672.

- [5] Falconer, K.J. and Lévy Véhel, J. (2008). Multifractional, multistable, and other processes with prescribed local form, J. Theoret. Probab., DOI 10.1007/s10959-008-0147-9.

- [6] Kingman, J.F.C. (1993). Poisson Processes, Oxford University Press, Oxford.

- [7] Lévy Véhel, J. and Seuret, S. (2004). The 2-microlocal Formalism, Fractal Geometry and Applications: A Jubilee of Benoit Mandelbrot, Proc. Sympos. Pure Math., 72 (2), 153-215.

- [8] Negoro, A. (1994). Stable-like processes: construction of the transition density and the behavior of sample paths near t = 0. Osaka J. Math. (31) 1, 189- 214.

- [9] Rogers, L.C.G. and Williams, D. (2000). Diffusions, Markov Processes and Martingales, Volume 1, 2nd edn. Cambridge University Press, Cambridge.

- [10] Samorodnitsky, G. and Taqqu, M.S. (1994) Stable Non-Gaussian Random Processes, Chapman and Hall.

- [11] Sato, K. (1999). Lévy Processes and Infinitely Divisible Distributions, Cambridge University Press, Cambridge.

- [12] Stoev, S. and Taqqu, M.S. (2004). Simulation methods for linear fractional stable motion and FARIMA using the Fast Fourier Transform. Fractals (2) 1,95–121.

- [13] Titchmarsh, E. (1948) Introduction to the Theory of Fourier Integrals, Second Edition, Clarendon Press.