∎

Tel.:+43 1 4277 50757

22email: christa.cuchiero@univie.ac.at 33institutetext: Martin Keller-Ressel 44institutetext: TU Berlin - Fakultät II, Institut für Mathematik, Strasse des 17. Juni 136, D-10623 Berlin, Germany

Tel.:+49 30 314 28619

44email: mkeller@math.TU-Berlin.DE 55institutetext: Josef Teichmann 66institutetext: ETH Zürich, D-MATH, Rämistrasse 101, CH-8092 Zürich, Switzerland

Tel.:+41 44 632 3174

66email: josef.teichmann@math.ethz.ch

Polynomial processes and their applications to mathematical finance

Abstract

We introduce a class of Markov processes, called -polynomial, for which the calculation of (mixed) moments up to order only requires the computation of matrix exponentials. This class contains affine processes, processes with quadratic diffusion coefficients, as well as Lévy-driven SDEs with affine vector fields. Thus, many popular models such as exponential Lévy models or affine models are covered by this setting. The applications range from statistical GMM estimation procedures to new techniques for option pricing and hedging. For instance, the efficient and easy computation of moments can be used for variance reduction techniques in Monte Carlo methods.

Journal of Economic Literature Classification C02, G12

Keywords:

Markov processes diffusions with jumps affine processes analytic tractability pricing hedgingMSC:

60J25 91B701 Introduction

Pricing and hedging of contingent claims are the crucial computations done within every model in mathematical finance. For European type claims this amounts to the computation of the expected value of a functional of the (discounted) price process under some martingale measure. (Partial) Hedging portfolios are then constructed via appropriate derivatives of those expected values with respect to model parameters or to the prices, so called Greeks. Let us denote the (discounted) price process at time , a vector in , by . We can roughly distinguish three cases of complexity for the mentioned computations:

-

1.

The probability distribution of is analytically known.

-

2.

The characteristic function of is analytically known.

-

3.

The local characteristics of are analytically known.

In the first case, a numerical quadrature algorithm is sufficient for the efficient computation of the contingent claim’s price , where denotes some payoff function.

In the second case, variants of Plancherel’s theorem are applied in order to evaluate the price functional , for instance,

where denotes the Fourier transform of the function . Remark that often modifications of the original payoff function are used to make the Fourier methodology applicable. This is numerically efficient, even though its implementation, in particular the complex integration, can take some time (see, e.g., carr ). Also there are different levels of what it means to “know analytically” the characteristic function of . In affine models, for example, one might need to solve a high-dimensional Riccati equation for each to calculate the characteristic function . In this case, “analytic knowledge” involves some precalculations, which also have to be performed efficiently.

The third case is characterized by the use of Monte Carlo methods: one samples from the (unknown) distribution of by generating, for instance through Euler schemes, approximate distributions for . This procedure is very robust, but takes a considerable amount of time. Moreover, for the convergence of the Euler scheme certain regularity assumptions on the characteristics, e.g. (local) Lipschitz continuity, are required.

In this article we would like to add a fourth case which – in the previous order – would correspond to case . We can describe a class of Markov processes, called “polynomial processes”, which have the property that the expected value of any polynomial of the random variables , , is again a polynomial in the initial value of the process. This means in particular that moments of all orders of can be computed in an easy and efficient way, even though neither its probability distribution nor its characteristic function needs to be known. Loosely speaking one could say that the expressions for all finite moments are analytically known (up to a matrix exponential).

We shall analyze this class and show that exponential Lévy processes, affine processes or processes of Pearson diffusion type belong to it. The method is best explained by an example: consider a stochastic volatility model of SVJJ-type gatheral , i.e. both the logarithmic (discounted) price process and the stochastic volatility can jump. Such models can be described by stochastic differential equations of the type

where are possibly correlated Brownian motions and is a bivariate pure-jump Lévy process, independent of , whose second component has positive increments. For such models there is no easy-to-implement (explicit) formula for the characteristic function, even though they are affine models. Assuming now appropriate moment conditions on the jump measures, the Markov process turns out to be a polynomial process, that is, the expected value of any polynomial of is a polynomial in and . The coefficients of this polynomial can be calculated efficiently by exponentiating a matrix, which can be easily deduced from the (extended) generator. In other words, there is a large subset of claims for which the prices and hedge ratios are explicitly known (up to matrix exponentials). Large can be made precise in the following sense: if the law of , say , is characterized by its moments, then “large” means dense, i.e. polynomial claims are dense (with respect to the norm) in the set of “all” claims. If this is not the case, the payoff function can at least be uniformly approximated by polynomials on some interval, which can be chosen according to the support of the probability distribution. The explicit knowledge of prices of polynomial claims then allows to apply variance reduction techniques for Monte-Carlo computations.

The remainder of our article is organized as follows: in Section 2 we formally introduce the class of -polynomial processes, establish a relationship to semimartingales and give conditions on the (extended) generator such that a Markov process is -polynomial. Section 3 deals with examples from the class of -polynomial processes and Section 4 with applications to pricing and hedging in mathematical finance.

2 Polynomial Processes

We define polynomial processes as a particular class of time-homogeneous Markov processes with state space , some closed subset of . To clarify notation, we find it useful to recall the basic ingredients of a time-homogeneous Markov process and the particular assumptions and conventions being made in this article (compare (rogers, , Chapter 3)).

Throughout, is a closed subset of and denotes its Borel -algebra. Since we shall not assume the process to be conservative, we adjoin to the state space a point , called cemetery, and set as well as . We make the convention that for any function on .

We consider a time-homogeneous Markov semigroup given by

and acting on all Borel measurable functions for which the integral is well defined. Here, denotes the transition function, which satisfies beside the standard conditions (see (rogers, , Definition III.1.1)) the following properties:

-

(i)

for all , , where denotes the Dirac measure;

-

(ii)

for all and , and .

Since the theory of polynomial processes always deals with a Markov process having the property that is a special semimartingale for all linear functionals on (extended by on ), we can bona fide assume that the probability space is the space of càdlàg functions such that and implies for all . This follows from the simple conclusion (i) to (iii) of Theorem 2.1, martingale regularity, and from the remarks at the bottom of (rogers, , p. 245). We thus understand as the coordinate process and denote by the filtration generated by and set .

In the sequel we consider some right continuous filtration satisfying and . We finally assume that for each there exists a probability measure on such that is Markovian relative to with semigroup , that is,

for all , and all Borel functions satisfying

for all and .

2.1 Definition and characterization of polynomial processes

For the treatment of polynomial process we have chosen a framework of stochastic analysis leading to easy-to-verify conditions for a process to be -polynomial (see Theorem 2.3 and Theorem 2.4). Before giving the precise definition of polynomial processes, let us introduce some notation.

Let denote the finite dimensional vector space of polynomials up to degree on , i.e. the restriction of polynomials on to , defined by

where we use multi-index notation , and . The dimension of is denoted by and depends on : if is a single point, the dimension is always and if is the whole space , it is maximal.

Moreover, for every multi-index , we define functions by setting

| (3) |

Furthermore, we write when and when , where denotes the canonical basis vector. Then the space clearly corresponds to the linear hull of the functions .

Here is our main definition:

Definition 1

We call an -valued time-homogeneous Markov process

-polynomial if we have for all , all , and ,

Additionally, we assume that is continuous at for all . If is -polynomial for all , then it is called polynomial.

Remark 1

-

(i)

Let us stress that in the above definition it is implicitly assumed that

for every , and , because otherwise the expression would not even be well-defined.

-

(ii)

The subtlety of Definition 1 lies in the fact that we assume for all (compare with Remark 5 (iv)). The assumption that only for , but not for smaller degrees is not sufficient for our proofs of Theorem 2.3 and Theorem 2.4, which we consider as the most important assertions from the point of view of applications.

Let us introduce the following notion of an extended Markov generator, which is due to Dynkin (see, e.g., (cinlar, , Definition 7.1)) and which we shall use to characterize -polynomial processes.

Definition 2

An operator with domain is called extended generator for some Markov process , if consists of those Borel measurable functions for which there exists a function such that the process

| (4) |

is well defined and a -local martingale for every .

Remark 2

We define the lifetime of the process by

| (5) |

where the infimum over the empty set is set to be . Since and as is supposed to be right continuous, is an -stopping time. Due to our convention , the local martingale property of (4) is therefore equivalent to

being a local martingale.

Remark 3

Suppose that lies in the domain of the extended generator and satisfies for all and . Then as defined in (4) is a true martingale if and only if all increments of have vanishing expectation, i.e. for all ,

In particular, by Fubini’s theorem exists on finite time intervals and thus also for almost all with respect to the Lebesgue measure.

The following lemma is well known for Feller processes (but perhaps not in our particular setting) and aims to establish a connection between the Kolmogorov backward equation and the extended generator introduced in (2).

Lemma 1

Let be a time-homogeneous Markov process with semigroup and denote by some function satisfying for all and . If lies in the domain of the extended generator, , and if as defined in (4) is additionally a true martingale, then we have:

-

(i)

For any given , is a true martingale, in particular , and .

-

(ii)

If is continuous at , then solves the Kolmogorov backward equation, that is,

Proof

For the first statement, we show that

is a true -martingale for any fixed . By the definition of the extended generator, this then implies that and . Indeed, we have by the assumption for all and and Remark 3 that and are integrable for every , hence and as well. Therefore the following expectation is well defined and we obtain for

By the Markov property, the conditional expectation on the right is equal to

But for any , we have

where the last equality follows from Remark 3. This completes the proof of (i).

Statement (ii) follows from Remark 3, the continuity of and from assertion (i), since

Let us now state our first theorem which is a consequence of elementary results in semigroup theory:

Theorem 2.1

Let be a time-homogeneous Markov process with state space and semigroup . Then the following assertions are equivalent:

-

(i)

is -polynomial for some .

-

(ii)

For every , there exists a linear map on , such that for all , restricted to can be written as

-

(iii)

For all , and , and

is a true martingale, and the extended generator satisfies

for all .

Proof

Our strategy to prove the above equivalences is to show (i) (ii) (iii) (i).

Throughout the proof, let be fixed. We start by showing (i) (ii). By the definition of an -polynomial process, the Markovian semigroup induces a semigroup of operators on . Since is finite dimensional and continuous at , standard results of semigroup theory (see, e.g., (nagel, , Theorem 2.9)), imply the representation of as matrix exponential, that is, there exists some linear map on such that .

Next, we show (ii) (iii). For every we have by (ii), and

Thus, is a -martingale. Hence lies in and , implying that holds true.

In order to prove (iii) (i), we consider the Kolmogorov backward equation for an initial value

By Lemma 1 (ii), solves the Kolmogorov equation, since is continuous at for any . This follows from the fact that maps to itself and the martingale property of , which implies

thus in particular continuity of for any . By choosing a basis of , we can define a linear map on by setting

Then . On , the Kolmogorov backward equation thus reduces to the following linear ODE

whose unique solution is given by (see, e.g., (nagel, , Theorem 2.8)). Hence on , is equal to and is therefore a polynomial of degree smaller than or equal to . Since this holds true for all , is -polynomial.

Remark 4

There is no need in assertion (ii) to restrict the time parameter to , since for , extends to a group.

The equivalence (iii) (i) of Theorem 2.1 provides a characterization of -polynomial processes in terms of the extended generator, however under the additional assumption that as defined in (4) is a true martingale. If is an even number, this latter condition is no longer needed, since the local martingales turn out to be always true martingales. In other words, for even numbers , Condition (2.2) below is necessary and sufficient for being an -polynomial process.

Condition 2.2

lies in the domain of the extended generator, i.e. for all , and , as defined in (4) is a -local martingale, and for all

Theorem 2.3

Let be a time-homogeneous Markov process with state space and let be an even number. Then is an -polynomial process if and only if Condition 2.2 is satisfied.

Proof

The necessary direction, that is, Condition 2.2 holds, if is an -polynomial process, is an obvious implication of Theorem 2.1 (i) (iii) (of course for all , not only even numbers larger than or equal to ).

For the sufficient direction we prove, for every , and , that and that is a true -martingale. Then Theorem 2.1 (iii) (i) yields the assertion.

First, fix some and some increasing sequence of stopping times with -a.s. such that are martingales for all . Furthermore we set

where , are given by (3). We notice that there is some finite constant such that

for all . Hence we obtain for and

Since the stopping times can be chosen such that is bounded, the right-hand side of the above inequality is finite and Gronwall’s lemma yields

| (6) |

for all , and . Due to the nonnegativity of , we have by Fatou’s lemma

| (7) |

for all . Hence for .

Next we show that for each , and

| (8) |

First, let for be fixed and set . Notice that there is a finite constant such that

for all . We then have

for appropriate positive constants and . Taking expectations and using (6), we see that for each fixed there exists some finite constant such that

for all and . Moreover, by Doob’s maximal -inequality for , we have for all that . Since the left-hand side is increasing in , monotone convergence yields (8) for this , in particular

| (9) |

Finally let us deal with the case . We consider the polynomial for and , which is an integer by hypothesis. For notational convenience, we write and estimate again

Therefore,

| (10) |

Due to (9), and by (7), we have . Hence we conclude that the right-hand side of (10) is integrable. Summing over all yields integrability of , which implies (8) for all .

Remark 5

-

(i)

If is an -polynomial process, then the process is a -polynomial process. If is even, the analysis of -polynomial processes could be reduced to the study of -polynomial processes at the cost of a more complicated state space, due to the construction .

-

(ii)

Let us remark that the condition in Theorem 2.3 is necessary for (4) being a true martingale. Indeed, the inverse -dimensional Bessel process defined by , where denotes a -dimensional Brownian motion started at satisfies

where is a one-dimensional standard Brownian motion. The extended generator is therefore given by

Hence , but

(11) is a strict local martingale, so is not a -polynomial process.

-

(iii)

In Definition 1 we require -polynomial processes to be also -polynomial for all , that is, we implicitly exclude processes whose extended generator maps polynomials of degree to polynomials of degree greater than , while still holds true. Consider for instance

where and is a one-dimensional standard Brownian motion. The state space is the interval and we have

Thus , while . Due to compactness of the state space it follows that is a true martingale for and hence we can conclude that but as in the proof of Theorem 2.1 (iii) (i). On the other hand – even though all moments of exist and – the subspace is not only consisting of polynomials anymore.

2.2 Polynomial processes and semimartingales

The purpose of this section is to characterize polynomial processes as special semimartingales with characteristics of a particular form. Indeed, in Proposition 1 below, we prove the equivalence of Condition 2.2 and the fact that the process is a special semimartingale whose characteristics are essentially polynomials (of a particular degree) in and absolutely continuous with respect to the Lebesgue measure.

Having established the particular form of the semimartingale characteristics, the characterization of the extended generator then simply follows from Itô’s formula and is given by (17). This in turn allows us to state easy-to-verify conditions which guarantee that is an -polynomial process for all . Notice that this fills a gap which is left open in Theorem 2.3, where only the case of even is considered.

In order to formulate the following proposition concisely, we set

and the define as the space of -times continuously differentiable functions , for which there exists some constant such that

Proposition 1

Let be a time-homogeneous Markov process with state space and let . Then the following assertions are equivalent.

-

(i)

Condition 2.2 holds, i.e. and for all .

-

(ii)

is a semimartingale with respect to the stochastic basis . Moreover,

(12) for some constant and the semimartingale characteristics associated with the “truncation function” satisfy 111All statements concerning the characteristics are meant up to an evanescent set.

(13) (14) where and . Furthermore, the characteristics and can be written as

(15) where denotes some Borel measurable functions taking values in the set of positive semidefinite matrices and is a positive kernel from into satisfying and . Finally, we have for all

(16) where denote some finite coefficients.

-

(iii)

lies in the domain of the extended generator of and for all , is given by

(17) where and satisfy the conditions of (ii) and .

All conditions (i), (ii) and (iii) imply that is a special semimartingale.

Remark 6

-

(i)

Concerning the direction (i) (ii), note that the existence of for all , follows from the fact that is a well defined polynomial for every . In particular, it means that for all .

- (ii)

- (iii)

Proof

Let us first prove . Due to Condition 2.2

| (19) |

is a -local martingale for all . As the process is predictable, is a special -valued semimartingale for all . Note here that which is due to the convention . In particular, has càdlàg paths implying that and cannot explode. Choosing for , then implies that is an (-dimensional) special semimartingale.

Consider now (19) for . Since , is a true martingale and there exists some constant such that

Taking expectations thus yields

which in turn implies (12).

Let now denote the characteristics of with respect to the “truncation function” . In order to determine their properties, we apply Itô’s formula to for for

| (20) |

where denotes the random measure associated with the jumps of and

Since is a local martingale and is càglàd, is a local martingale, too, for all . Furthermore, the third and forth term on the right-hand side are predictable processes of finite variation, thus in particular a process of locally integrable variation by (jacod, , Lemma I.3.10). As is a special semimartingale, it follows from (jacod, , Proposition I.4.22) that is also of locally integrable variation, since it is of finite variation and for a special semimartingale the finite variation part is locally integrable. Therefore, we have by (jacod, , Proposition II.1.28) that

is a local martingale. Combining thus (20) with (19) and using the unique decomposition of a special semimartingale into a local martingale and a predictable finite variation process, we find

Therefore

| (21) |

Consider now (21) for , i.e. the polynomials , where . In this case (21) reads as

Setting therefore implies that . Moreover, applying (21) to the quadratic polynomials for yields

| (22) |

for some , since and lie in . Hence we have proved (13) and (14).

In order to show (15), we define . By the same arguments as in the proof of (jacod, , Proposition II.2.9.b), there exists a random measure on such that . Moreover, since

and as , and are non-negative increasing processes (of finite variation), and are absolutely continuous with respect to Lebesgue measure. Hence, (jacod, , Proposition I.3.13) implies the existence of predictable processes and such that and . Then is again a predictable random measure satisfying almost surely. Having constructed this kernel, (22) now becomes

implying that for is also absolutely continuous with respect to Lebesgue measure and can therefore be written as . Finally, by (cinlar, , Theorem 6.27) we can choose homogeneous versions for the processes and such that

It remains to establish property (16). To this end notice that (21) can be written as

Since , and lie in for all , (16) simply follows by induction.

Let us now prove the implication (ii) (iii). For notational simplicity we set

for . Then, since for all , which is a consequence of (14) and (16), we have

where and denote some positive (finite-valued) functions. Hence, the process is of locally integrable variation and Itô’s formula thus implies that

| (23) |

is a local martingale (compare also (jacod, , Theorem II.2.42)). Moreover,

is a martingale, since

Denote now by the right-hand side of (17). We need to prove that

is a local martingale. By the definition of we have

where is given by (23). Since both terms on the right-hand side are local martingales, the same holds true for .

Finally (i) follows from (iii), since and since applied to maps into for , which is due to the assumptions on the characteristics.

Since every -polynomial process satisfies Condition 2.2, the following corollary is an obvious consequence of Proposition 1.

Corollary 1

When is an even number, the converse direction also follows easily from Theorem 2.3 and Proposition 1. The general case is treated in the subsequent theorem, where we provide sufficient conditions in terms of the compensator of the jump measure such that the converse statement holds true. Its proof relies on a maximal inequality which can be established for semimartingales whose characteristics satisfy the conditions (13) - (16). This is subject of Lemma 2 below.

Theorem 2.4

Let be a time-homogeneous Markov process with state space and let . Suppose that is a semimartingale, which satisfies the conditions (12) - (16) (with respect to the “truncation function” ) or equivalently that and that its extended generator is given by (17). If

| (24) |

or if

| (25) |

for some constant , then is an -polynomial process.

Proof

Remark 7

Let us remark that under (16), condition (25) is always satisfied when is an even number (see also Remark 6 (ii)). In this case is always finite, as already shown in the proof of Theorem 2.3. If is an odd number, Condition 2.2 together with (24) or (25) is sufficient for being an -polynomial process.

Using the structure of the semimartingale characteristics derived in Proposition 1, we now state the announced maximal inequality and some associated moment estimates. This result is probably known but the proof is included for convenience. A similar statement for the case of Lévy driven SDEs can be found in jacodkurtz .

Lemma 2

Fix and let . Let be a semimartingale with respect to , whose characteristics associated with the “truncation function” satisfy the conditions (13), (14) and (15) given in Proposition 1. Then there exists a constant such that

| (26) |

In particular, if one of the conditions (24) or (25) is satisfied, then there exist finite constants and such that

| (27) |

Proof

For notational simplicity we only consider the case where is one-dimensional and thus omit all indices. Due to Proposition 1 and the assumptions on the characteristics, is a special semimartingale and its canonical decomposition is given by , where we write for . Denote by the quadratic variation of the purely discontinuous martingale part of , that is,

where is the random measure associated with the jumps of . Define furthermore stopping times

and set . We can estimate

where denotes some constant which may vary from line to line.

Since we have

| (28) |

Concerning , an application of Burkholder-Davis-Gundy’s inequality yields

| (29) |

As satisfies (14), we can estimate it by , where is nonnegative, and we get

Therefore it remains to handle . Following the approach of jacodkurtz , we can write

which is due to the fact that is purely discontinuous, non-decreasing and . Furthermore, since is the predictable compensator of , we have

| (30) |

In the sequel we shall use the following inequalities (see jacodkurtz )

| (31) | ||||

| (32) |

for , and . Applying (31), equation (30) becomes

For the first part, we then have due to the assumption on

where we use the fact that is nonnegative, and (32). Estimating which follows from the fact that is non-decreasing and for , we finally obtain

Choosing leads to

Combining this with the estimates (28) and (29), we find

| (33) |

By monotone convergence we obtain (26).

Remark 8

-

(i)

It is important to note that the characteristics of in the above statements are always specified with respect to the “truncation function” . While and do not depend on this choice, the characteristic does depend on . So, if one chooses another truncation function , then the difference between and is given by . Thus, the requirement that and are as in Theorem 2.4 and

(34) is an equivalent condition guaranteeing that is -polynomial.

-

(ii)

We now give two examples of kernels which satisfy the conditions of Proposition 1 as long as and satisfies (34).

-

(a)

The first one essentially requires to be a quadratic polynomial in , that is,

where all are finite signed measures on such that is a well defined Lévy measure for every . In view of Remark 6, it is necessary to require

where denotes the Jordan decomposition of .

-

(b)

Alternatively, can be specified as the pushforward of a Lévy measure under an affine function. Let and let

be an affine function in . Here, and are assumed to be measurable. We define then by

where for each , denotes the pushforward of the measure under the map . Moreover, is a Lévy measure on integrating

-

(a)

3 Examples

In order to apply Theorem 2.4 to the following examples, we assume .

Example 1 (Affine processes)

Every affine process on is -polynomial if the killing rate is constant and if the Lévy measures for , satisfy

| (35) |

For details on affine processes see, e.g., dfs and kst .222We write here for the constant part of the jump measure in contrast to dfs , where it is denoted by .

Proof

Let us remark that affine processes are defined via their characteristic function, which is of the form

for some function and . This definition then implies affine semimartingale characteristics, from which the polynomial property can easily be seen due to Theorem 2.4. Note also that the explicit knowledge of and is not necessary to compute the moments of an affine process. Simply the knowledge of its characteristics, which determine the linear map as given in Theorem 2.1 (ii), is enough (see Section 4). Moreover, for affine processes, it has not been proved so far that the existence of the moments of the Lévy measures automatically implies the existence of the moments of the process itself. We can conclude this simply from the more general statement of Lemma 2.

Example 2 (Exponential Lévy models)

Exponential Lévy models are of the form , where is a Lévy process on with triplet . Under the integrability assumption , which guarantees the existence of , exponential Lévy models are -polynomial, since we have where denotes the cumulant generating function of the Lévy process.

Example 3 (Lévy driven SDEs)

Let denote a Lévy process on with triplet . Suppose furthermore that are affine functions, i.e. we have where and . A process which solves the stochastic differential equation

and leaves invariant, is -polynomial, if the following moment condition on the Lévy measure

| (36) |

is satisfied.

Proof

For -functions and general Lipschitz continuous functions the extended generator of with respect to some truncation function is given by

Concerning the the compensator of the jump measure , this example corresponds to the situation of Remark (ii) (ii) (b) with . Condition (25), that is,

for some constant , is satisfied due to (36). Hence Theorem 2.4 yields the assertion.

Example 4 (Quadratic term structure models chen )

Consider the following quadratic term structure model , specified as non-negative quadratic function of a one-dimensional Ornstein-Uhlenbeck process

for appropriate . Here, is given by

where is a standard Brownian motion. The joint process then satisfies the dynamics

and is therefore clearly a polynomial process with

Example 5 (Jacobi process)

Another example of a polynomial process is the Jacobi process (see gourieroux ), which is the solution of the stochastic differential equation

on , where and . This example can be extended by adding jumps, where the jump times correspond to those of a Poisson process with intensity and the jump size is a function of the process level. Indeed, if a jump occurs, then the process is reflected at so that it remains in the interval . The extended generator is given by

In terms of Remark (ii) (ii) (b), we have here and .

Example 6 (Pearson diffusions)

The above example 5 (without jumps) as well as Ornstein-Uhlenbeck and Cox-Ingersoll-Ross processes, all of them with mean-reverting drift, can be subsumed under the class of so called Pearson diffusions, which are the solutions to SDEs of the form

where and and are specified such that the square root is well defined. In view of Theorem 2.4 it is thus obvious that these processes are polynomial. Forman and Sørensen forman give a complete classification of the different types of the Pearson diffusion in terms of their invariant distributions.

4 Applications

By Theorem 2.1 we know that there exists a linear map such that moments of -polynomial processes can simply be calculated by computing . Indeed, by choosing a basis of the matrix corresponding to this linear map, which we also denote by , can be obtained through Writing as , we then have

| (37) |

which means that moments of polynomial processes can be evaluated simply by computing matrix exponentials.

By means of the one-dimensional Cox-Ingersoll-Ross process

we exemplify how moments of order can be calculated. Its extended generator is given by

Applying to yields the following matrix

Hence, .

Remark 9

- (i)

-

(ii)

If one has to apply well-known techniques from linear algebra of polynomials, in order to enumerate efficiently a basis of and to exploit sparsity properties of , see for instance reimer .

4.1 Moment estimation - Generalized Method of Moments (GMM)

In view of this easy and fast technique of moment calculation for polynomial processes, the Generalized Method of Moments (GMM) can be applied for parameter estimation. If we are given a stationary polynomial process , then typical functionals applied for parameter estimation are of the form

where is the set of parameters to be estimated. This functional is indeed simple to evaluate, since can also be computed easily. The usual technology of equating time averages to expectations applies for and leads to efficient calibration methods. In the case of one-dimensional jump-diffusions, Zhou zhou already uses this method for GMM estimation.

4.2 Model calibration

In model calibration – in contrast to estimation of parameter values of a stationary process from time series data – parameters are chosen such that derivatives’ prices are best explained. Here also the polynomial structure can be very helpful: assume a polynomial process , where derivatives’ prices are known from the market. Derivatives’ prices are expectations for sufficiently many time points and sufficiently many payoffs , such that we can estimate the curves for today’s initial value and several polynomials . In other words we need as many derivatives’ prices as necessary to calculate (estimate) the prices of some payoffs, which are polynomials in the underlying.

Having now those curves it is often a very easy task to read off the parameter values which explain this curve. This will be worked out in a follow-up paper.

4.3 Pricing - Variance reduction

The fact that moments of polynomial processes are analytically known also gives rise to new and efficient techniques for pricing and hedging.

Let be an -polynomial process and a deterministic bi-measurable map such that the discounted price processes are given through under a martingale measure. Typically if are log-prices. We denote by a bounded measurable European claim for some maturity , whose (discounted) price at is given by the risk neutral valuation formula

Obviously, claims of the form

| (38) |

for are analytically tractable, since we have

for , where is the previously defined linear map on . Although claims are in practice not of form (38), the explicit knowledge of the price of polynomial claims can be used for variance reduction techniques based on control variates. Instead of using the estimator in a Monte-Carlo simulation, where are samples of , we can use

where is an approximation of and serves as control variate. Both estimators are unbiased and the second clearly outperforms the first since , where the ratio of the variances depends on the accuracy of the polynomial approximation.

It is worth mentioning that the previous pricing algorithm has also important consequences for hedging, since the Greeks for “polynomial claims” can also be calculated explicitly and efficiently: The coefficients of the polynomial can be computed using matrix exponentiation, taking derivatives of this polynomial is then a simple algebraic operation. To be more precise, the sensitivities of the price process with respect to the factors can be calculated by

Assuming a complete market situation, the claim , can be replicated by a trading strategy , i.e.

Similarly the polynomial claim can be replicated by the delta-hedging strategy and we conclude that

Therefore, if we assume that has small variance, then also the stochastic integral representing the difference of the cumulative gains and losses of the two hedging portfolios, namely the one built by the unknown strategy and the one built by the known strategy , is small.

Concerning the approximation of by a polynomial, let us consider the case with , meaning that we only have one asset which depends on the first component of the polynomial process as it is usually the case in stochastic volatility models. If the Hamburger moment problem for the law of , say , admits a unique solution, then the set of all polynomials is dense in (see (akhiezer, , Theorem 2.3.3)) and hence also in . A sufficient conditions for the uniqueness of a solution to this moment problem is

| (39) |

for some constants and (see (reed, , Example X.4)). This condition can be assured by the existence of exponential moments of around , that is, the moment generating function is finite for all , which is often satisfied in financial applications.

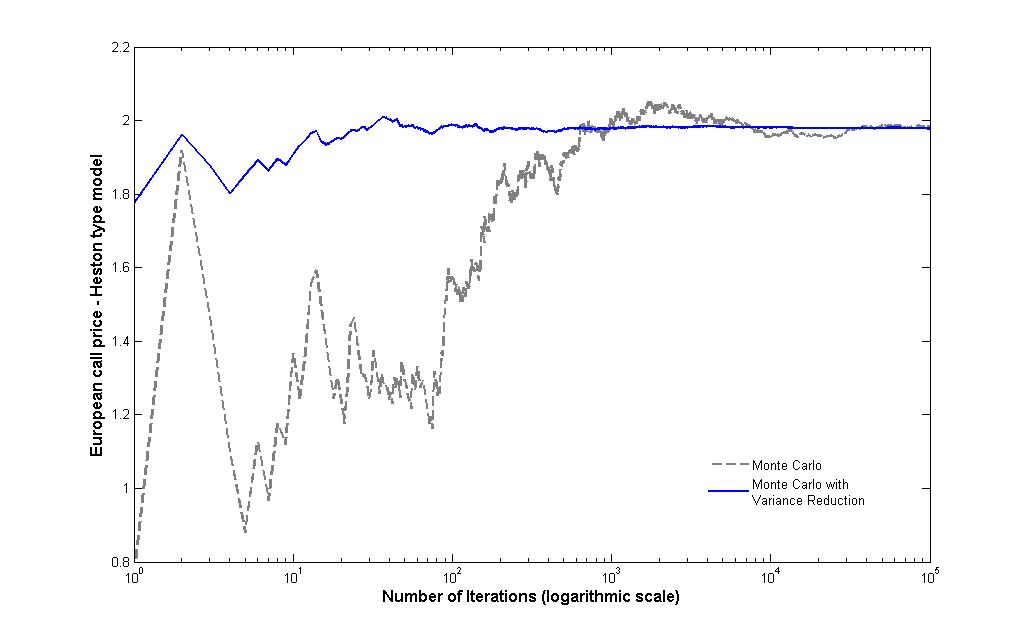

Fur illustratory purposes we have implemented the following affine stochastic volatility model which was initially proposed by Bates bates . The price process is specified as with dynamics

where is a 2-dimensional Brownian motion and a pure jump process in with jump intensity and exponentially distributed jump sizes, i.e. , for some parameter . Figure 1 illustrates the comparison between the Monte Carlo simulation for European call prices with and without variance reduction. In this example we use the following parameters:

| Strike | |||||||||

|---|---|---|---|---|---|---|---|---|---|

The polynomial which we take to approximate the payoff function is of degree and is chosen such as to minimize the approximation error in a certain interval (depending on the support of the probability distribution). Concerning computation time, we remark that beside the one-time calculation of the matrix exponential, the only additional computational effort resulting from the use of the control variates is the evaluation of a polynomial in each loop. In our MATLAB code, this causes an increase of computation time of less than per replication. Observing that one can achieve the same accuracy by using times less replications through the polynomial control variates, the computation time (in our MATLAB implementation) can be decreased by a factor of more than .

Let us finally remark that our variance reduction technique is of particular interest for affine models for which the generalized Riccati ODEs (see dfs ) determining the characteristic function cannot be explicitly solved. Moreover, it can also be applied to derivatives involving several assets, provided that their dynamics are described by a polynomial process. This can simply be done by approximating European payoff functions depending on several variables with multivariate polynomials.

Acknowledgements.

All authors gratefully acknowledge the support from the FWF-grant Y 328 (START prize from the Austrian Science Fund) and from ETH foundation. Furthermore the authors are grateful for many comments and valuable suggestions by Chris Rogers, which improved our paper a lot.References

- (1) N. I. Akhiezer. The classical moment problem and some related questions in analysis. Translated by N. Kemmer. Hafner Publishing Co., New York, 1965.

- (2) D. S. Bates. Post-’87 crash fears in the S&P 500 futures option market. J. Econometrics, 94(1-2):181–238, 2000.

- (3) P. Carr and D. Madan. Option valuation using the fast Fourier transform. Journal of Computational Finance, 2(4):61–73, 1998.

- (4) E. Çinlar, J. Jacod, P. Protter, and M. J. Sharpe. Semimartingales and Markov processes. Z. Wahrsch. Verw. Gebiete, 54(2):161–219, 1980.

- (5) L. Chen, D. Filipović, and H. V. Poor. Quadratic term structure models for risk-free and defaultable rates. Math. Finance, 14(4):515–536, 2004.

- (6) P. Cheridito, D. Filipović, and M. Yor. Equivalent and absolutely continuous measure changes for jump-diffusion processes. Ann. Appl. Probab., 15(3):1713–1732, 2005.

- (7) D. Duffie, D. Filipović, and W. Schachermayer. Affine processes and applications in finance. Ann. Appl. Probab., 13(3):984–1053, 2003.

- (8) C. F. Dunkl. Hankel transforms associated to finite reflection groups. In Hypergeometric functions on domains of positivity, Jack polynomials, and applications (Tampa, FL, 1991), volume 138 of Contemp. Math., pages 123–138. Amer. Math. Soc., Providence, RI, 1992.

- (9) K.-J. Engel and R. Nagel. One-parameter semigroups for linear evolution equations, volume 194 of Graduate Texts in Mathematics. Springer-Verlag, New York, 2000. With contributions by S. Brendle, M. Campiti, T. Hahn, G. Metafune, G. Nickel, D. Pallara, C. Perazzoli, A. Rhandi, S. Romanelli and R. Schnaubelt.

- (10) J. L. Forman and M. Sørensen. The Pearson diffusions: a class of statistically tractable diffusion processes. Scand. J. Statist., 35(3):438–465, 2008.

- (11) L. Gallardo and M. Yor. Some remarkable properties of the Dunkl martingales. In In memoriam Paul-André Meyer: Séminaire de Probabilités XXXIX, volume 1874 of Lecture Notes in Math., pages 337–356. Springer, Berlin, 2006.

- (12) J. Gatheral. The Volatility Surface: A Practitioner’s Guide. Wiley Finance, 2006.

- (13) G. H. Golub and C. F. Van Loan. Matrix computations. Johns Hopkins Studies in the Mathematical Sciences. Johns Hopkins University Press, Baltimore, MD, third edition, 1996.

- (14) C. Gourieroux and J. Jasiak. Multivariate Jacobi process with application to smooth transitions. J. Econometrics, 131(1-2):475–505, 2006.

- (15) J. Jacod, T. G. Kurtz, S. Méléard, and P. Protter. The approximate Euler method for Lévy driven stochastic differential equations. Ann. Inst. H. Poincaré Probab. Statist., 41(3):523–558, 2005.

- (16) J. Jacod and A. N. Shiryaev. Limit theorems for stochastic processes, volume 288 of Grundlehren der Mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences]. Springer-Verlag, Berlin, 1987.

- (17) M. Keller-Ressel, W. Schachermayer, and J. Teichmann. Affine processes are regular. Probab. Theory Relat. Fields, 151:591–611, 2011.

- (18) C. Moler and C. Van Loan. Nineteen dubious ways to compute the exponential of a matrix. SIAM Rev., 20(4):801–836, 1978.

- (19) M. Reed and B. Simon. Methods of modern mathematical physics. II. Fourier analysis, self-adjointness. Academic Press [Harcourt Brace Jovanovich Publishers], New York, 1975.

- (20) M. Reimer. Multivariate polynomial approximation, volume 144 of International Series of Numerical Mathematics. Birkhäuser Verlag, Basel, 2003.

- (21) L. C. G. Rogers and D. Williams. Diffusions, Markov processes, and martingales. Vol. 1. Cambridge Mathematical Library. Cambridge University Press, Cambridge, 2000. Foundations, Reprint of the second (1994) edition.

- (22) H. Zhou. Itô conditional moment generator and the estimation of short rate processes. Journal of Financial Econometrics, pages 250–271, 2003.