A mathematical proof of the existence of

trends in financial time series

Abstract

We are settling a longstanding quarrel in quantitative finance by proving the existence of trends in financial time series thanks to a theorem due to P. Cartier and Y. Perrin, which is expressed in the language of nonstandard analysis (Integration over finite sets, F. & M. Diener (Eds): Nonstandard Analysis in Practice, Springer, 1995, pp. 195–204). Those trends, which might coexist with some altered random walk paradigm and efficient market hypothesis, seem nevertheless difficult to reconcile with the celebrated Black-Scholes model. They are estimated via recent techniques stemming from control and signal theory. Several quite convincing computer simulations on the forecast of various financial quantities are depicted. We conclude by discussing the rôle of probability theory.

Keywords:

Financial time series, mathematical finance, technical analysis, trends, random walks, efficient markets, forecasting, volatility, heteroscedasticity, quickly fluctuating functions, low-pass filters, nonstandard analysis, operational calculus.

1 Introduction

Our aim is to settle a severe and longstanding quarrel between

-

1.

the paradigm of random walks111Random walks in finance go back to the work of Bachelier [4]. They became a mainstay in the academic world sixty years ago (see, e.g., [8, 11, 41] and the references therein) and gave rise to a huge literature (see, e.g., [53] and the references therein). and the related efficient market hypothesis [16] which are the bread and butter of modern financial mathematics,

-

2.

the existence of trends which is the key assumption in technical analysis.222Technical analysis (see, e.g., [5, 30, 31, 44, 45] and the references therein), or charting, is popular among traders and financial professionals. The notion of trends here and in the usual time series literature (see, e.g., [23, 25]) do not coincide.

There are many publications questioning the existence either of

trends (see, e.g., [16, 37, 48]), of random

walks (see, e.g., [32, 56]), or of the market

efficiency (see, e.g.,

[24, 52, 56]).333An excellent book by

Lowenstein [36] is giving flesh and blood to those hot

debates.

A theorem due to Cartier and Perrin [10], which is stated in the language of nonstandard analysis,444See Sect. 2.1. yields the existence of trends for time series under a very weak integrability assumption. The time series may then be decomposed as a sum

| (1) |

where

-

•

is the trend,

-

•

is a “quickly fluctuating” function around .

The very “nature” of those quick fluctuations is left unknown and

nothing prevents us from assuming that is random and/or fractal. It implies the following

conclusion which seems to be rather unexpected

in the existing literature:

The two above alternatives are not necessarily contradictory

and may coexist for a given time series.555One should then

define random

walks and/or market efficiency “around” trends.

We nevertheless show that it might be difficult to reconcile with

our setting the celebrated Black-Scholes model [9], which

is in the heart of the approach to quantitative finance via

stochastic differential equations (see, e.g., [53]

and the references therein).

Consider, as usual in signal, control, and in other engineering sciences, in Eq. (1) as an additive corrupting noise. We attenuate it, i.e., we obtain an estimation of by an appropriate filtering.666Some technical analysts (see, e.g., [5]) are already advocating this standpoint. These filters

- •

- •

A mathematical definition of trends and effective means for estimating them, which were missing until now, bear important consequences on the study of financial time series, which were sketched in [20]:

-

•

The forecast of the trend is possible on a “short” time interval under the assumption of a lack of abrupt changes, whereas the forecast of the “accurate” numerical value at a given time instant is meaningless and should be abandoned.

-

•

The fluctuations of the numerical values around the trend lead to new ways for computing standard deviation, skewness, and kurtosis, which may be forecasted to some extent.

-

•

The position of the numerical values above or under the trend may be forecasted to some extent.

The quite convincing computer simulations reported in Sect. 4 show that we are

- •

-

•

on the verge of producing on-line indicators for short time trading, which are easily implementable on computers.777The very same mathematical tools already provided successful computer programs in control and signal.

Remark 1.

We utilize as in [20] the differences between the actual prices and the trend for computing quantities like standard deviation, skewness, kurtosis. This is a major departure from today’s literature where those quantities are obtained via returns and/or logarithmic returns,888See Sect. 2.4. and where trends do not play any rôle. It might yield a new understanding of “volatility”, and therefore a new model-free risk management.999The existing literature contains of course other attempts for introducing nonparametric risk management (see, e.g., [2]).

2 Existence of trends

2.1 Nonstandard analysis

Nonstandard analysis was discovered in the early 60’s by Robinson [51]. It vindicates Leibniz’s ideas on “infinitely small” and “infinitely large” numbers and is based on deep concepts and results from mathematical logic. There exists another presentation due to Nelson [46], where the logical background is less demanding (see, e.g., [13, 14, 50] for excellent introductions). Nelson’s approach [47] of probability along those lines had a lasting influence.101010The following quotation of D. Laugwitz, which is extracted from [28], summarizes the power of nonstandard analysis: Mit üblicher Mathematik kann man zwar alles gerade so gut beweisen; mit der nicht-standard Mathematik kann man es aber verstehen. As demonstrated by Harthong [26], Lobry [34], and several other authors, nonstandard analysis is also a marvelous tool for clarifying in a most intuitive way questions stemming from some applied sides of science. This work is another step in that direction, like [17, 18].

2.2 Sketch of the Cartier-Perrin theorem111111The reference [35] contains a well written elementary presentation. Note also that the Cartier-Perrin theorem is extending previous considerations in [27, 49].

2.2.1 Discrete Lebesgue measure and -integrability

Let be an interval of , with extremities and . A sequence is called an approximation of , or a near interval, if is infinitesimal for . The Lebesgue measure on is the function defined on by . The measure of any interval , , is its length . The integral over of the function is the sum

The function is said to be -integrable if, and only if, for any interval the integral is limited and, if is infinitesimal, also infinitesimal.

2.2.2 Continuity and Lebesgue integrability

The function is said to be -continuous at if, and only if, when .131313 means that is infinitesimal. The function is said to be almost continuous if, and only if, it is -continuous on , where is a rare subset.141414The set is said to be rare [6] if, for any standard real number , there exists an internal set such that . We say that is Lebesgue integrable if, and only if, it is -integrable and almost continuous.

2.2.3 Quickly fluctuating functions

A function is said to be quickly fluctuating, or oscillating, if, and only if, it is -integrable and is infinitesimal for any quadrable subset.151515A set is quadrable [10] if its boundary is rare.

Theorem 2.1.

and are respectively called the trend and the quick fluctuations of . They are unique up to an infinitesimal.

2.3 The Black-Scholes model

The well known Black-Scholes model [9], which describes the price evolution of some stock options, is the Itô stochastic differential equation

| (2) |

where

-

•

is a standard Wiener process,

-

•

the volatility and the drift, or trend, are assumed to be constant.

This model and its numerous generalizations are playing a major rôle in financial mathematics since more than thirty years although Eq. (2) is often severely criticized (see, e.g., [39, 55] and the references therein).

The solution of Eq. (2) is the geometric Brownian motion which reads

where is the initial condition. It seems most natural to consider the mean of as the trend of . This choice unfortunately does not agree with the following fact: is almost surely not a quickly fluctuating function around , i.e., the probability that , , is not “small”, when

-

•

is “small”,

-

•

is neither “small” nor “large”.

Remark 2.

Remark 3.

Many assumptions concerning Eq. (2) are relaxed in the literature (see, e.g., [53] and the references therein):

-

•

and are no more constant and may be time-dependent and/or -dependent.

-

•

Eq. (2) is no more driven by a Wiener process but by more complex random processes which might exhibit jumps in order to deal with “extreme events”.

The conclusion reached before should not be modified, i.e., the price is not oscillating around its trend.

2.4 Returns

Assume that the function gives the prices of some financial asset. It implies that the values of are positive. What is usually studied in quantitative finance are the return

| (3) |

and the logarithmic return, or log-return,

| (4) |

which are defined for . There is a huge literature investigating the statistical properties of the two above returns, i.e., of the time series (3) and (4).

Remark 4.

Returns and log-returns are less interesting for us since the trends of the original time series are difficult to detect on them. Note moreover that the returns and log-returns which are associated to the Black-Scholes equation (2) via some infinitesimal time-sampling [3, 7] are not -integrable: Theorem 2.1 does not hold for the corresponding time series (3) and (4).

3 Trend estimation

Consider the real-valued polynomial function , , of degree . Rewrite it in the well known notations of operational calculus (see, e.g., [57]):

Introduce , which is sometimes called the algebraic derivative [42, 43], and which corresponds in the time domain to the multiplication by . Multiply both sides by , . The quantities , , which are given by the triangular system of linear equations, are said to be linearly identifiable (see, e.g., [18]):

| (5) |

The time derivatives, i.e., , , , are removed by multiplying both sides of Eq. (5) by , , which are expressed in the time domain by iterated time integrals.

Consider now a real-valued analytic time function defined by the convergent power series , . Approximating by its truncated Taylor expansion yields as above derivatives estimates.

Remark 5.

Remark 6.

See [22] for other studies on filters and estimation in economics and finance.

Remark 7.

See [56] for another viewpoint on a model-based trend estimation.

4 Some illustrative computer simulations

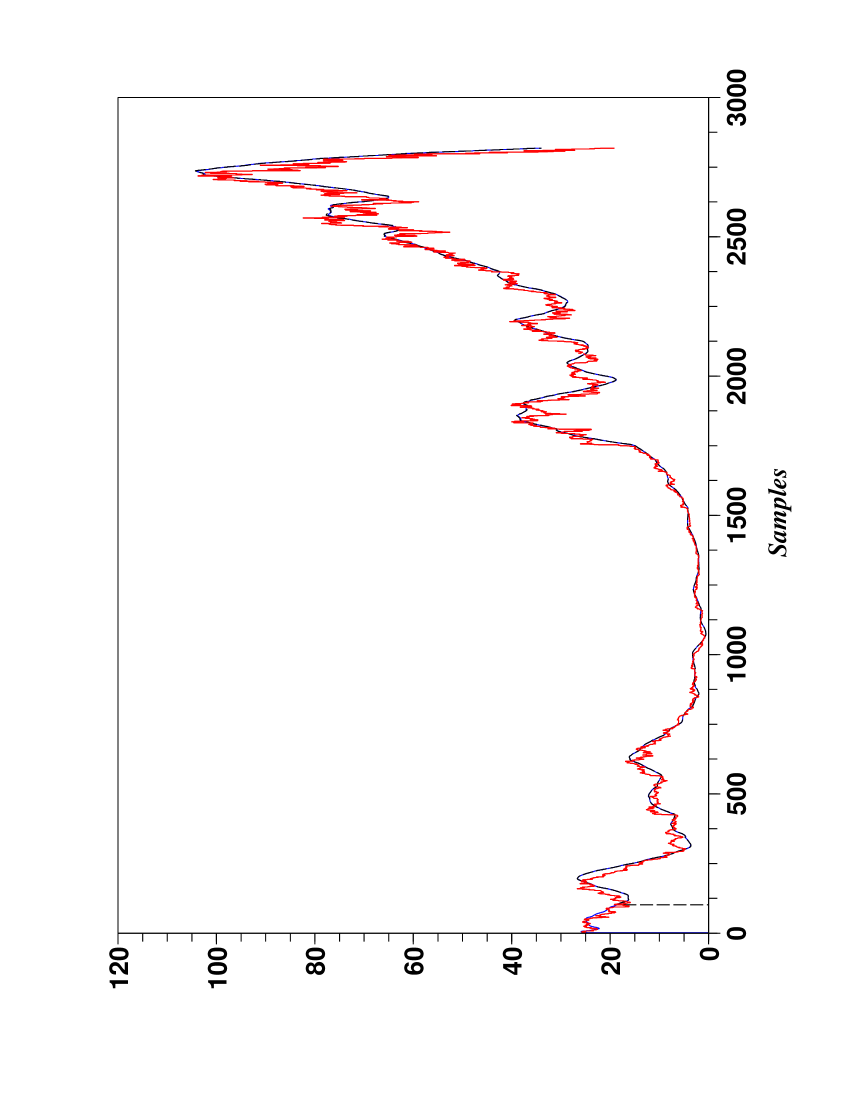

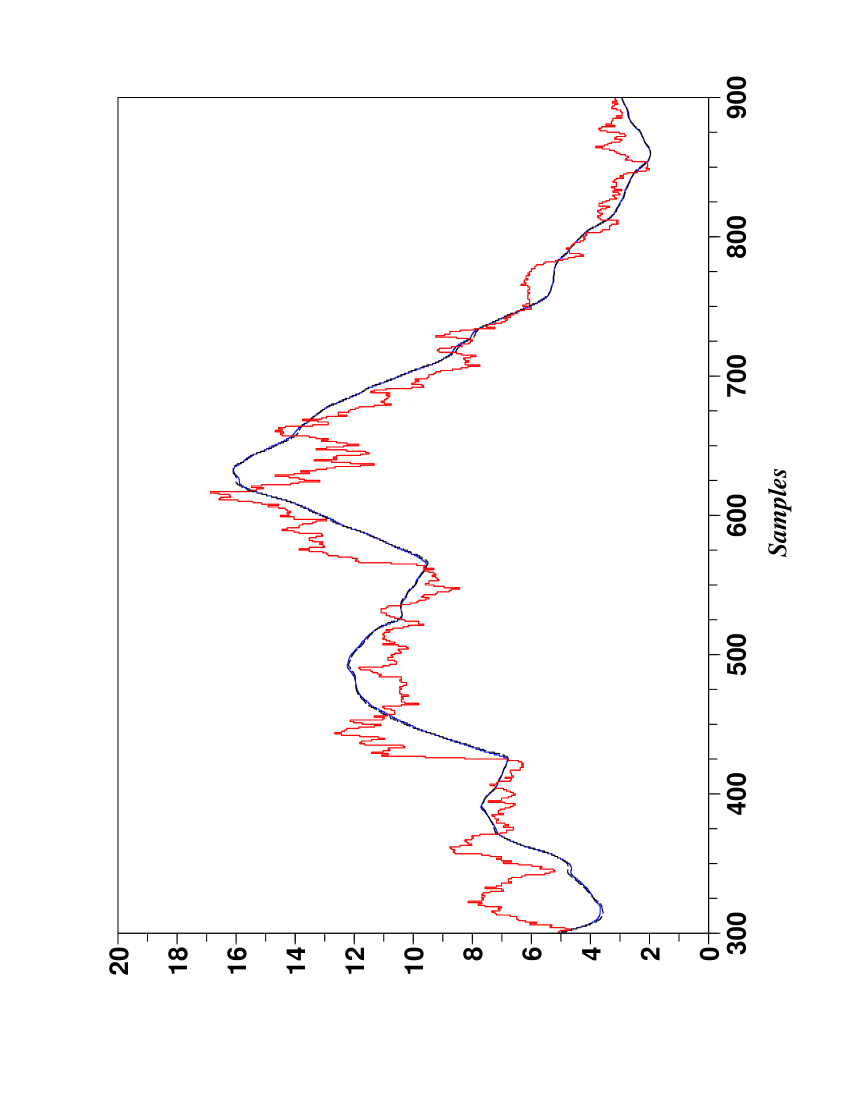

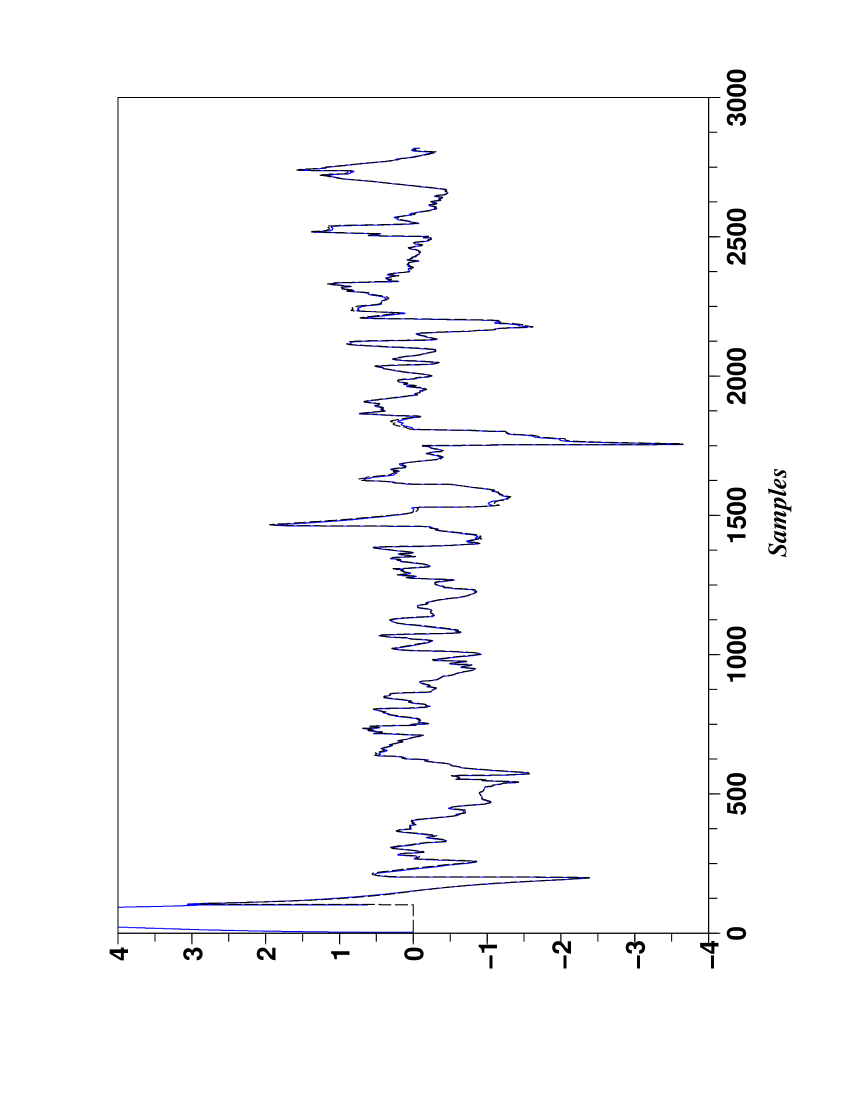

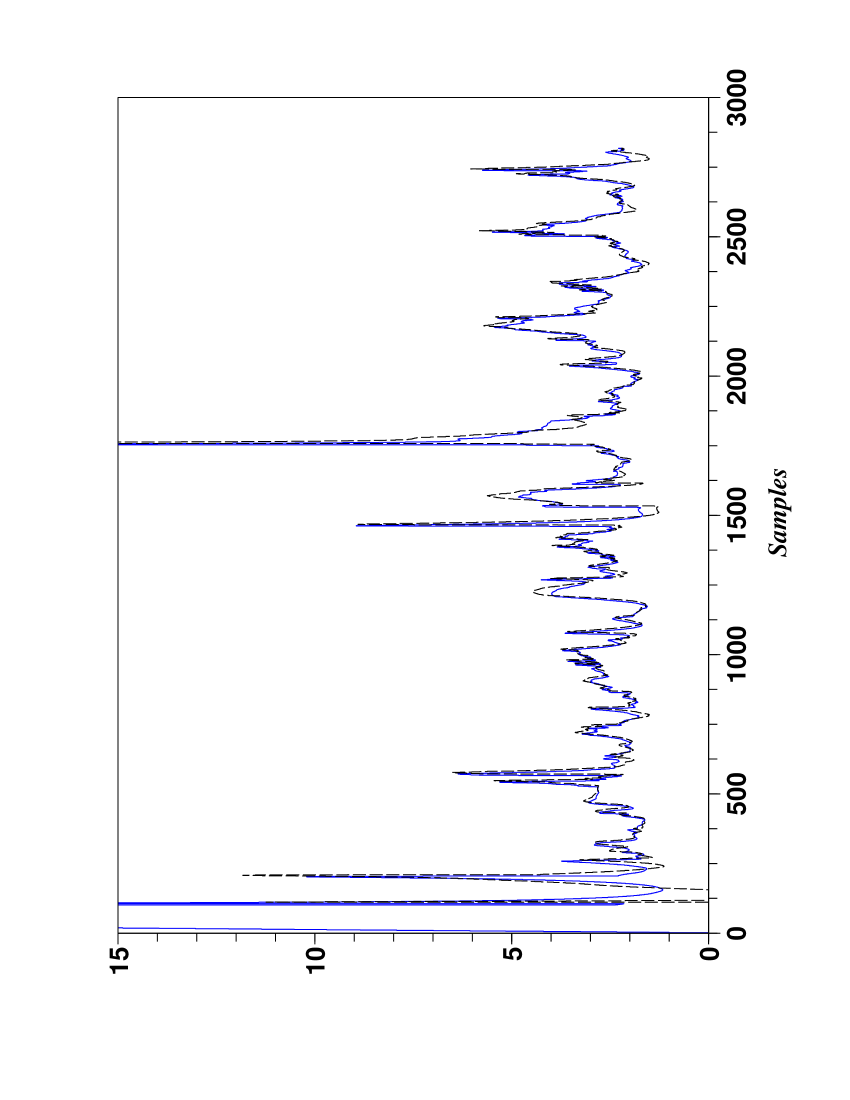

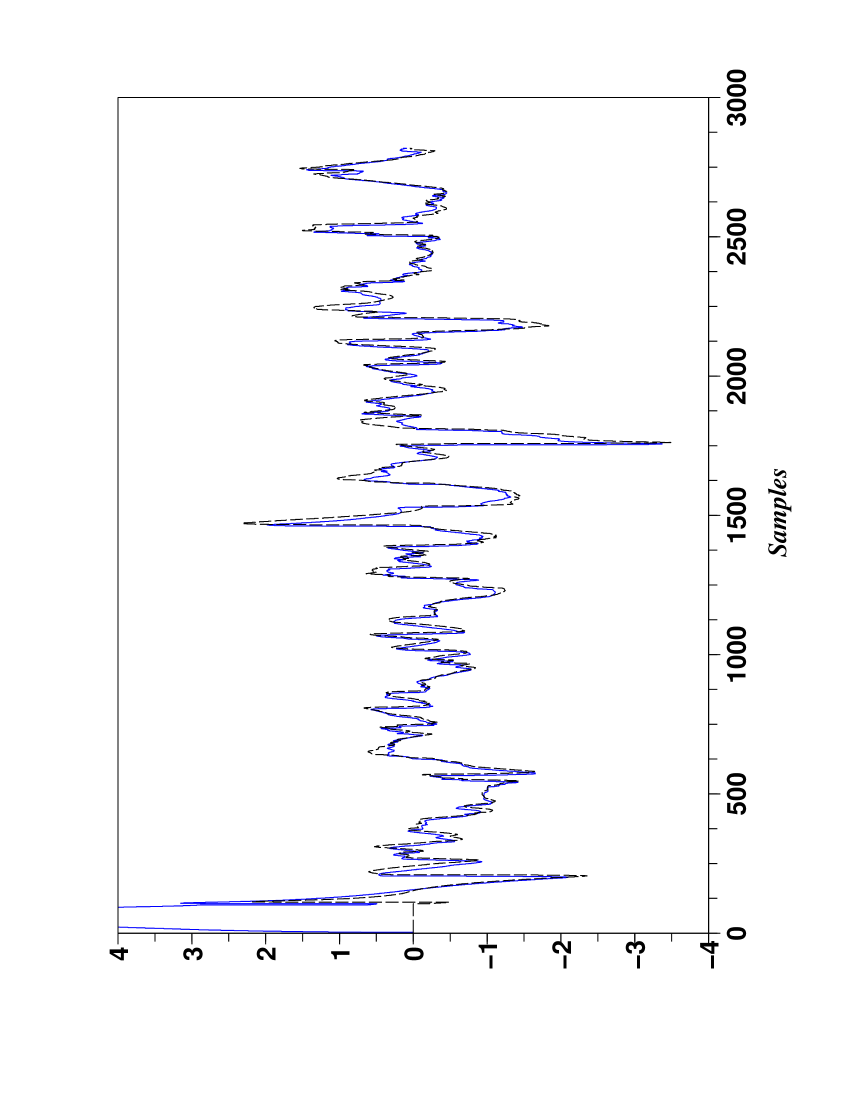

Consider the Arcelor-Mittal daily stock prices from 7 July 1997 until 27 October 2008.171717Those data are borrowed from http://finance.yahoo.com/.

4.1 1 day forecast

-

•

the estimation of the trend thanks to the methods of Sect. 3, with ;

- •

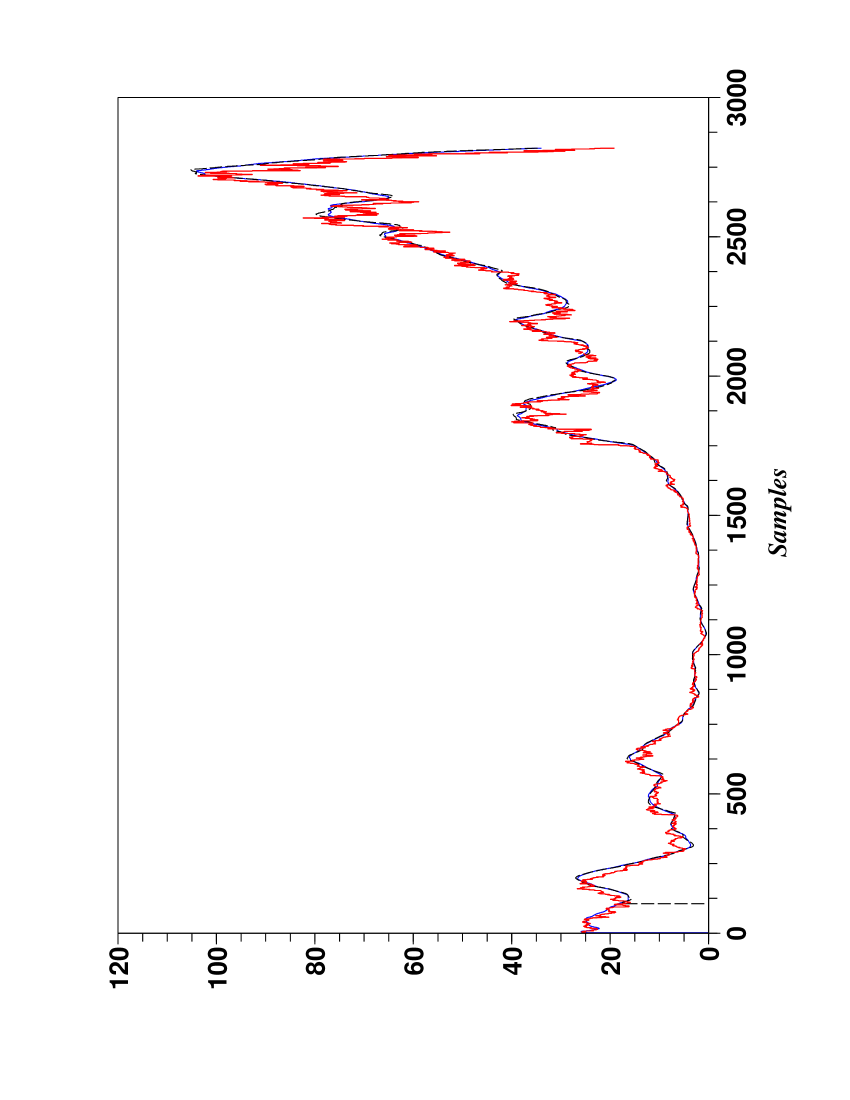

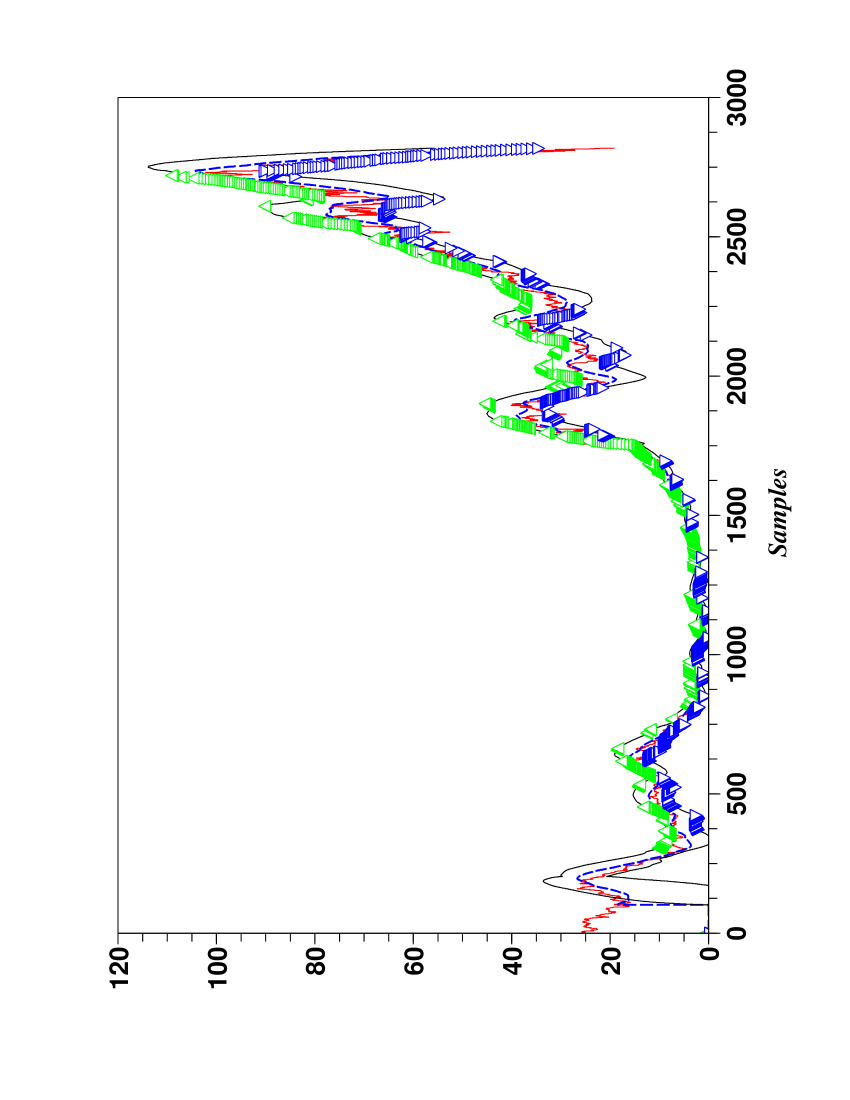

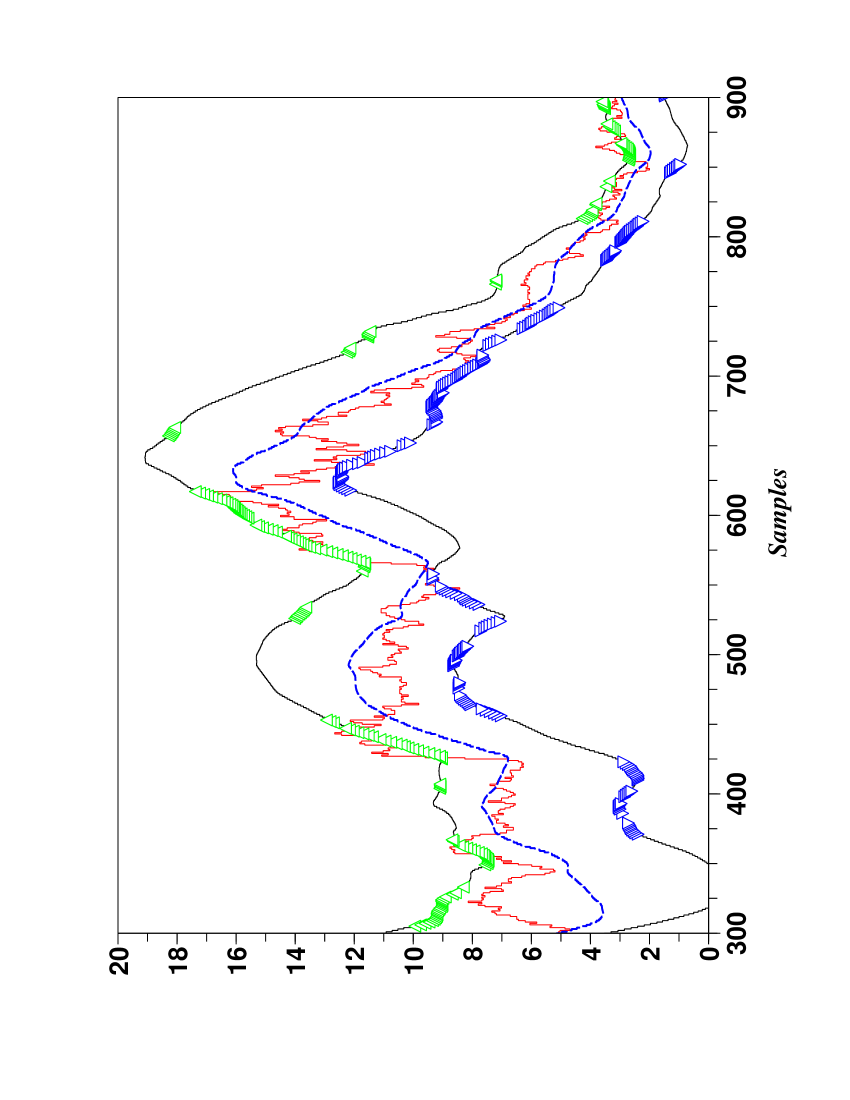

We now look at some properties of the quick fluctuations around the trend of the price (see Eq. (1)) by computing moving averages which correspond to various moments

where

-

•

,

-

•

is the mean of over the samples,191919According to Sect. 2.2 is “small”.

-

•

samples.

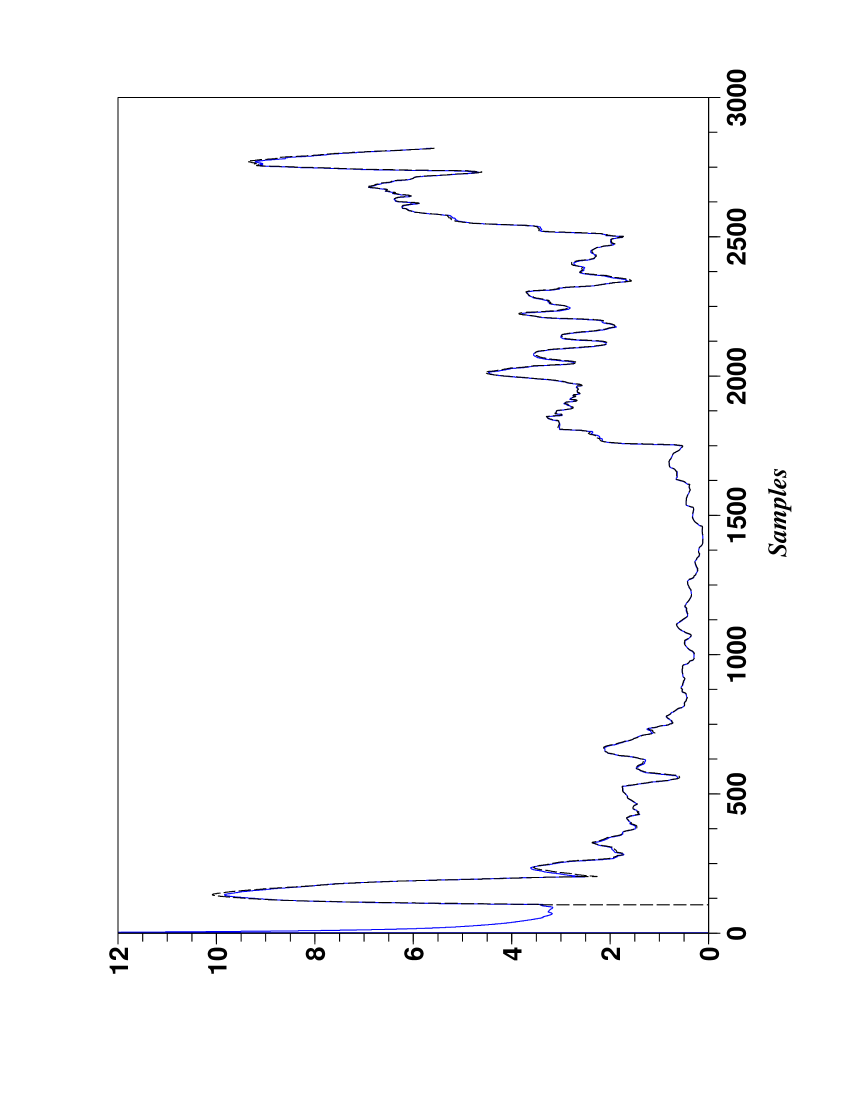

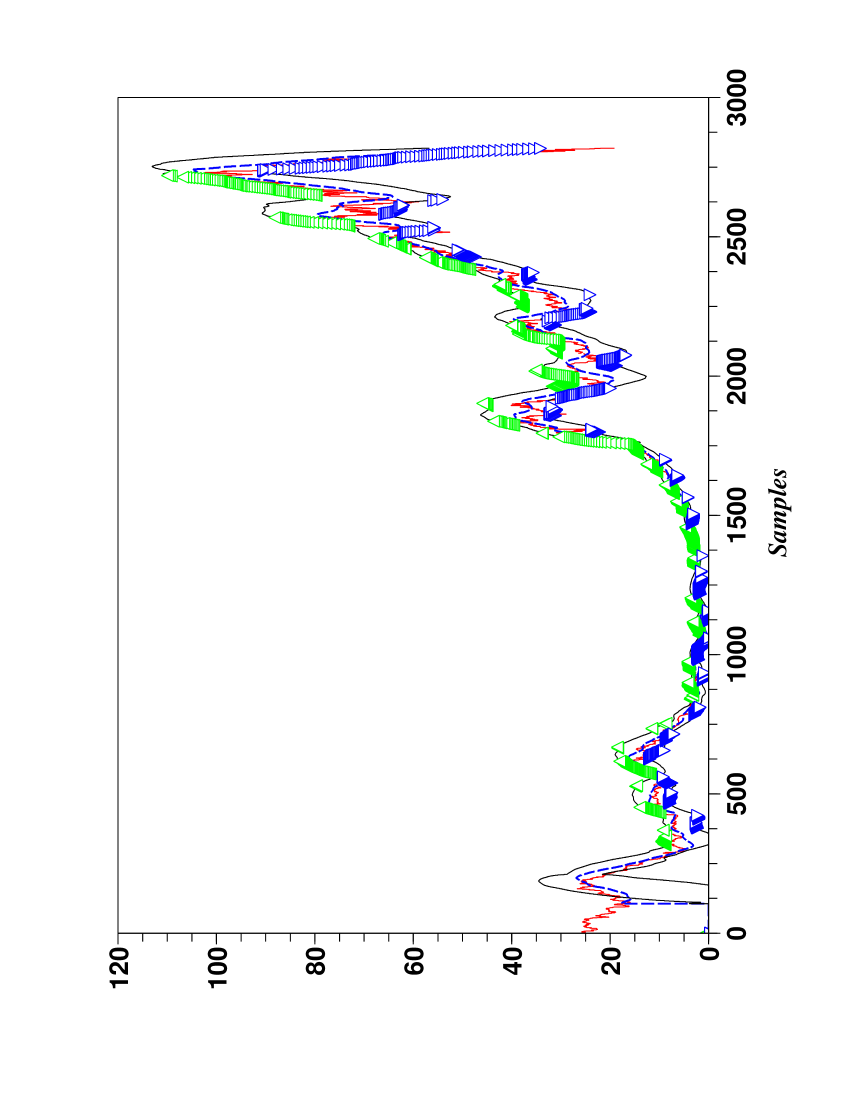

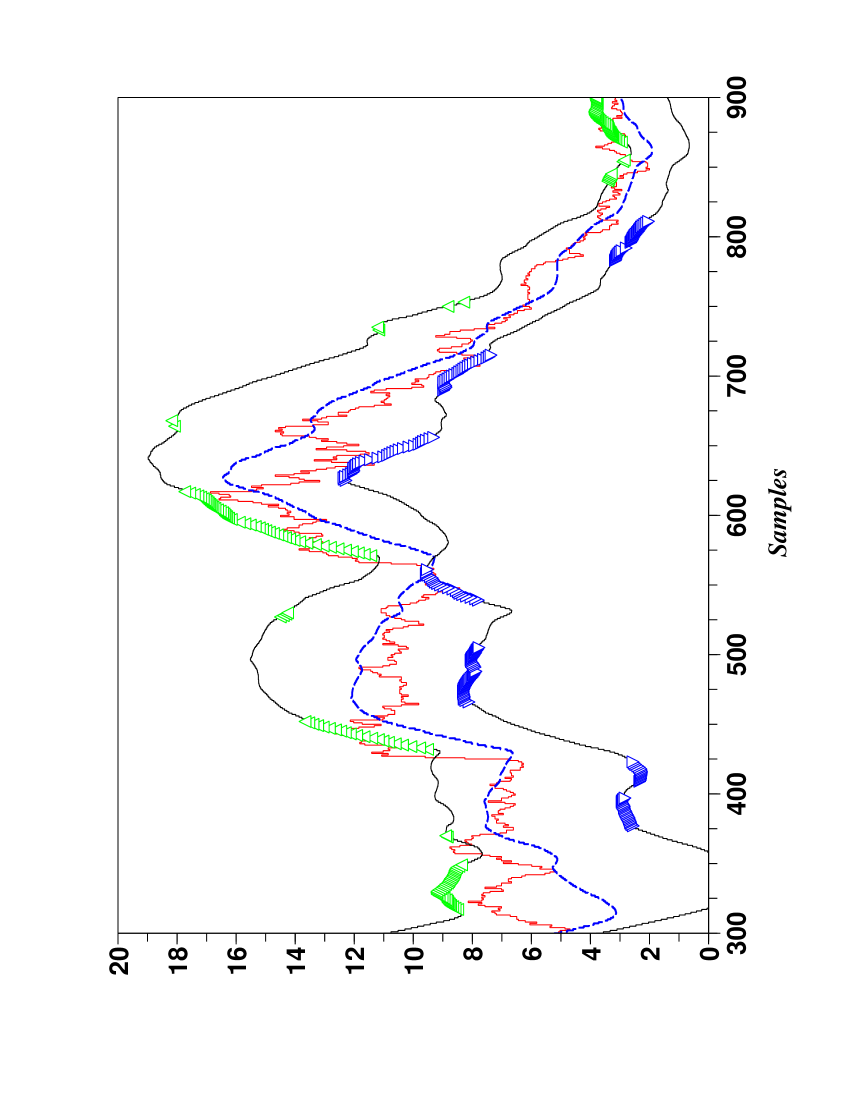

The standard deviation and its day forecast are displayed in Figure 3. Its heteroscedasticity is obvious.

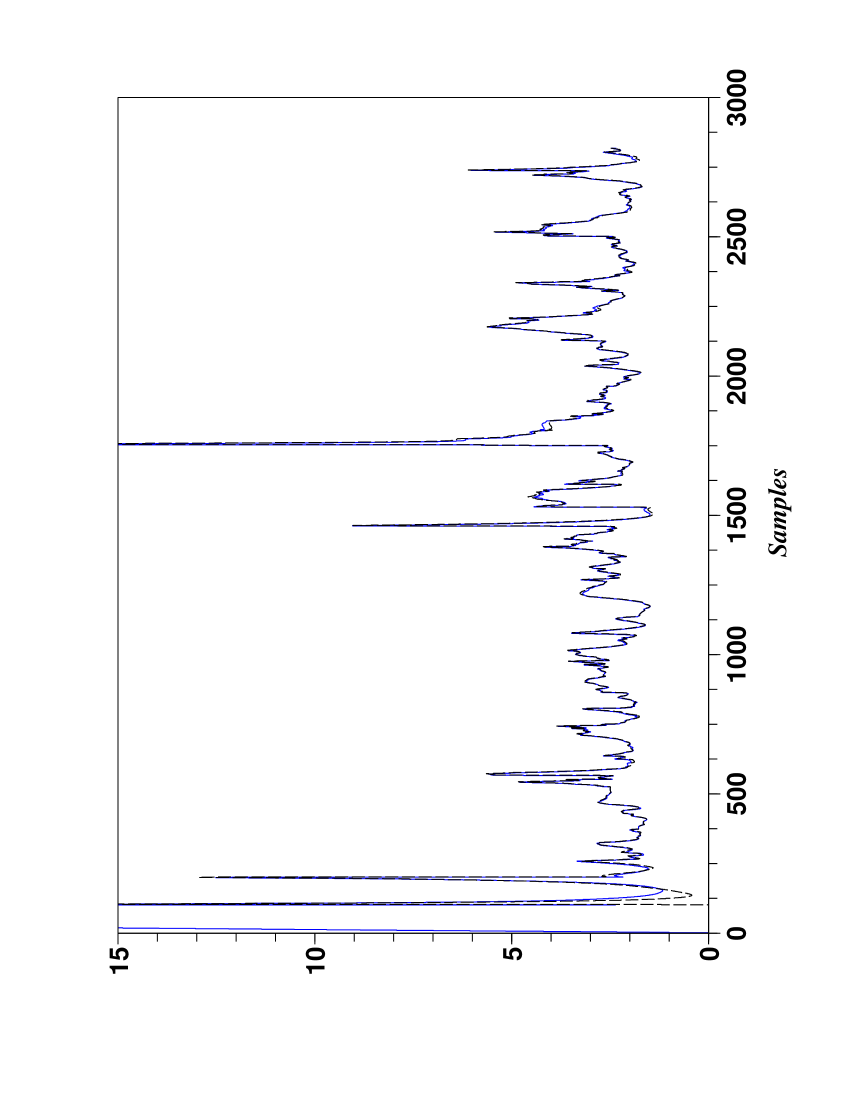

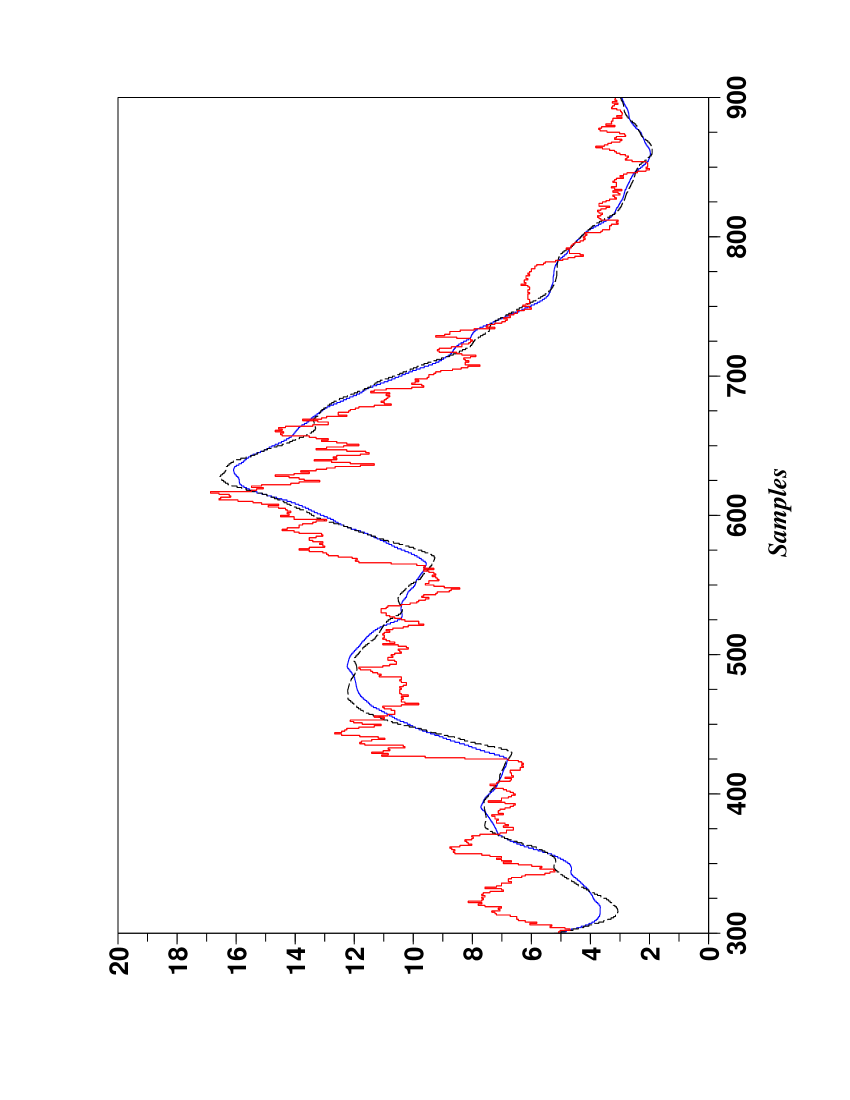

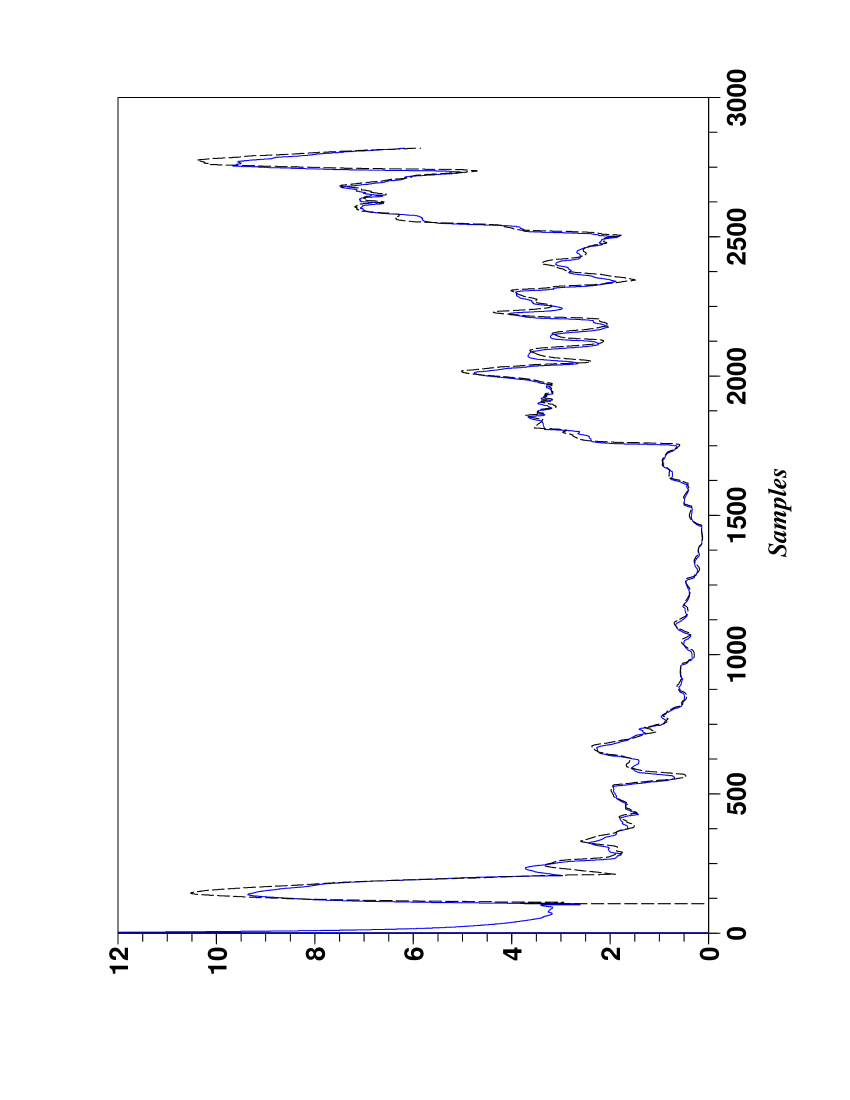

The kurtosis , the skewness , and their day forecasts are respectively depicted in Figures 4 and 5. They show quite clearly that the prices do not exhibit Gaussian properties202020Lack of spaces prevents us to look at returns and log-returns. especially when they are close to some abrupt change.

4.2 5 days forecast

4.3 Above or under the trend?

5 Conclusion: probability in quantitative finance

The following question may arise at the end of this preliminary

study on trends in financial time series:

Is it possible to improve the forecasts given here and in

[20] by taking advantage of a precise probability law for

the fluctuations around the trend?

Although Mandelbrot [38] has shown in a most convincing

way more than forty years ago that the Gaussian character of the

price variations should be at least questioned, it does not seem

that the numerous investigations which have been carried on since

then for finding other probability laws with jumps and/or with “fat

tails” have been able to produce clear-cut results, i.e.,

results which are exploitable in practice (see, e.g., the

enlightening discussions in [29, 39, 54] and the

references therein). This shortcoming may be due to an “ontological

mistake” on uncertainty:

Let us base our argument on new advances in model-free control

[19]. Engineers know that obtaining the differential equations

governing a concrete plant is always a most challenging task: it is

quite difficult to incorporate in those equations

frictions,212121Those frictions have nothing to do with what are

called frictions in market theory! heating effects, ageing,

etc, which might have a huge influence on the plant’s behavior. The

tools proposed in [19] for bypassing those

equations222222The effects of the unknown part of the plant are

estimated in the model-free approach and not neglected as in the

traditional setting of robust control (see, e.g.,

[58] and the references therein). got already in spite of

their youth a few impressive industrial applications. This is an

important gap between engineering’s practice and theoretical physics

where the basic principles lead to equations describing “stylized”

facts. The probability laws stemming from statistical and quantum

physics can only be written down for “idealized” situations. Is it

not therefore quite naïve to wish to exhibit well defined

probability laws in quantitative finance, in economics and

management, and in other social and psychological sciences, where

the environmental world is much more involved than in any physical

system? In other words a mathematical theory of uncertain

sequences of events should not necessarily be confused with

probability theory.232323It does not imply of course that

statistical tools should be abandoned (remember that we computed

here standard deviations, skewness, kurtosis). To ask if the

uncertainty of a “complex” system is of probabilistic

nature242424We understand by “probabilistic nature” a precise

probabilistic description which satisfies some set of axioms like

Kolmogorov’s ones. is an undecidable metaphysical question which

cannot be properly answered via experimental means. It should

therefore be ignored.

Remark 8.

One should not misunderstand the authors. They fully recognize the mathematical beauty of probability theory and its numerous and exciting connections with physics. The authors are only expressing doubts about any modeling at large in quantitative finance, with or without probabilities.

The Cartier-Perrin theorem [10] which is decomposing a time series as a sum of a trend and a quickly fluctuating function might be

-

•

a possible alternative to the probabilistic viewpoint,

-

•

a useful tool for analyzing

-

–

different time scales,

-

–

complex behaviors, including abrupt changes, i.e., “rare” extreme events like financial crashes or booms, without having recourse to a model via differential or difference equations.

-

–

We hope to be able to show in a near future what are the benefits not only in quantitative finance but also for a new approach to time series in general (see [20] for a first draft).

References

- [1]

- [2] Aït-Sahalia Y., Lo A.W. Nonparametric risk management and implied risk aversion. J. Econometrics, 9, (2000) 9–51.

- [3] Albeverio S., Fenstad J.E., Hoegh-Krøhn R., Lindstrøm T. Nonstandard Methods in Stochastic Analysis and Mathematical Physics. Academic Press, 1986.

- [4] Bachelier L. Théorie de la spéculation. Ann. Sci. École Normale Sup. Sér. 3, 17, (1900) 21–86.

- [5] Béchu T., Bertrand E., Nebenzahl J. L’analyse technique (6e éd.). Economica, 2008.

- [6] Benoît E. Diffusions discrètes et mécanique stochastique. Prépubli. Lab. Math. J. Dieudonné, Université de Nice, 1989.

- [7] Benoît E. Random walks and stochastic differential equations. F. & M. Diener (Eds): Nonstandard Analysis in Practice. Springer, 1995, pp. 71–90.

- [8] Bernstein P.L. Capital Ideas: The Improbable Origins of Modern Wall Street. Free Press, 1992.

- [9] Black F., Scholes M. The pricing of options and corporate liabilities. J. Polit. Econ., 81, (1973) 637–654.

- [10] Cartier P., Perrin Y. Integration over finite sets. F. & M. Diener (Eds): Nonstandard Analysis in Practice. Springer, 1995, pp. 195–204.

- [11] Cootner P.H. The Random Characters of Stock Market Prices. MIT Press, 1964.

- [12] Cox J., Ross S., Rubinstein M. Option pricing: a simplified approach. J. Financial Econ., 7, (1979) 229–263.

- [13] Diener F., Diener M. Tutorial. F. & M. Diener (Eds): Nonstandard Analysis in Practice. Springer, 1995, pp. 1–21.

- [14] Diener F., Reeb G., Analyse non standard. Hermann, 1989.

- [15] Dacorogna M.M., Gençay R., Müller U., Olsen R.B., Pictet O.V. An Introduction to High Frequency Finance. Academic Press, 2001.

- [16] Fama E.F. Foundations of Finance: Portfolio Decisions and Securities Prices. Basic Books, 1976.

- [17] Fliess M. Analyse non standard du bruit. C.R. Acad. Sci. Paris Ser. I, 342, (2006) 797–802.

- [18] Fliess M. Critique du rapport signal à bruit en communications numériques. ARIMA, 9, (2008) 419–429. Available at http://hal.inria.fr/inria-00311719/en/.

- [19] Fliess M., Join C. Commande sans modèle et commande à modèle restreint, e-STA, 5, (2008) n∘ 4. Available at http://hal.inria.fr/inria-00288107/en/.

- [20] Fliess M., Join C. Time series technical analysis via new fast estimation methods: a preliminary study in mathematical finance. Proc. 23rd IAR Workshop Advanced Control Diagnosis (IAR-ACD08), Coventry, 2008. Available at http://hal.inria.fr/inria-00338099/en/.

- [21] Fliess M., Join C., Sira-Ramírez H. Non-linear estimation is easy, Int. J. Modelling Identification Control, 4, (2008) 12–27. Available at http://hal.inria.fr/inria-00158855/en/.

- [22] Gençay R., Selçuk F., Whitcher B. An Introduction to Wavelets and Other Filtering Methods in Finance and Economics. Academic Press, 2002.

- [23] Gouriéroux C., Monfort A. Séries temporelles et modèles dynamiques (2e éd.). Economica, 1995. English translation: Time Series and Dynamic Models. Cambridge University Press, 1996.

- [24] Grossman S., Stiglitz J. On the impossibility of informationally efficient markets. Amer. Economic Rev., 70, (1980) 393–405.

- [25] Hamilton J.D. Time Series Analysis. Princeton University Press, 1994.

- [26] Harthong J. Le moiré. Adv. Appl. Math., 2, (1981) 21–75.

- [27] Harthong J. La méthode de la moyennisation. M. Diener & C. Lobry (Eds): Analyse non standard et représentation du réel. OPU & CNRS, 1985, pp. 301–308.

- [28] Harthong J. Comment j’ai connu et compris Georges Reeb. L’ouvert (1994). Available at http://moire4.u-strasbg.fr/souv/Reeb.htm.

- [29] Jondeau E., Poon S.-H., Rockinger M. Financial Modeling Under Non-Gaussian Distributions. Springer, 2007.

- [30] Kaufman P.J. New Trading Systems and Methods (4th ed.). Wiley, 2005.

- [31] Kirkpatrick C.D., Dahlquist J.R. Technical Analysis: The Complete Resource for Financial Market Technicians. FT Press, 2006.

- [32] Lo A.W., MacKinley A.C. A Non-Random Walk Down Wall Street. Princeton University Press, 2001.

- [33] Lo A.W., Mamaysky H., Wang J. (2000). Foundations of technical analysis: computational algorithms, statistical inference, and empirical implementation. J. Finance, 55, (2000) 1705–1765.

- [34] Lobry C. La méthode des élucidations successives. ARIMA, 9, (2008) 171–193.

- [35] Lobry C., Sari T. Nonstandard analysis and representation of reality. Int. J. Control, 81, (2008) 517–534.

- [36] Lowenstein R. When Genius Failed: The Rise and Fall of Long-Term Capital Management. Random House, 2000.

- [37] Malkiel B.G. A Random Walk Down Wall Street (revised and updated ed.). Norton, 2003.

- [38] Mandelbrot B. The variation of certain speculative prices. J. Business, 36, (1963) 394–419.

- [39] Mandelbrot B.B., Hudson R.L. The (Mis)Behavior of Markets. Basic Books, 2004.

- [40] Mboup M., Join C., Fliess M. Numerical differentiation with annihilators in noisy environment. Numer. Algorithm., (2009) DOI: 10.1007/s11075-008-9236-1.

- [41] Merton R.C. Continuous-Time Finance (revised ed.). Blackwell, 1992.

- [42] Mikusinski J. Operational Calculus ( ed.), Vol. 1. PWN & Pergamon, 1983.

- [43] Mikusinski J., Boehme T. Operational Calculus ( ed.), Vol. 2. PWN & Pergamon, 1987.

- [44] Müller T., Lindner W. Das grosse Buch der Technischen Indikatoren. Alles über Oszillatoren, Trendfolger, Zyklentechnik (9. Auflage). TM Börsenverlag AG, 2007.

- [45] Murphy J.J. Technical Analysis of the Financial Markets (3rd rev. ed.). New York Institute of Finance, 1999.

- [46] Nelson E. Internal set theory. Bull. Amer. Math. Soc., 83, (1977) 1165–1198.

- [47] Nelson E. Radically Elementary Probability Theory. Princeton University Press, 1987.

- [48] Paulos J.A. A Mathematician Plays the Stock Market. Basic Books, 2003.

- [49] Reder C. Observation macroscopique de phénomènes microscopiques. M. Diener & C. Lobry (Eds): Analyse non standard et représentation du réel. OPU & CNRS, 1985, pp. 195–244.

- [50] Robert A. Analyse non standard. Presses polytechniques romandes, 1985. English translation: Nonstandard Analysis. Wiley, 1988.

- [51] Robinson A. Non-standard Analysis (revised ed.). Princeton University Press, 1996.

- [52] Rosenberg B., Reid K., Lanstein R. (1985). Persuasive evidence of market inefficiency. J. Portfolio Management, 13, (1985) pp. 9–17.

- [53] Shreve S.J. Stochastic Calculus for Finance, I & II. Springer, 2005 & 2004.

- [54] Sornette D. Why Stock Markets Crash: Critical Events in Complex Financial Systems. Princeton University Press, 2003.

- [55] Taleb N.N. Fooled by Randomness: The Hidden Role of Chance in Life and in the Markets. Random House, 2004.

- [56] Taylor S.J. Modelling Financial Time Series ( ed.). World Scientific, 2008.

- [57] Yosida, K. Operational Calculus: A Theory of Hyperfunctions (translated from the Japanese). Springer, 1984.

- [58] Zhou K., Doyle J.C., Glover K. Robust and Optimal Control. Prentice-Hall, 1996.