A Probabilistic Numerical Method for Fully Nonlinear Parabolic PDEs

Abstract

We consider the probabilistic numerical scheme for fully nonlinear PDEs suggested in [12], and show that it can be introduced naturally as a combination of Monte Carlo and finite differences scheme without appealing to the theory of backward stochastic differential equations. Our first main result provides the convergence of the discrete-time approximation and derives a bound on the discretization error in terms of the time step. An explicit implementable scheme requires to approximate the conditional expectation operators involved in the discretization. This induces a further Monte Carlo error. Our second main result is to prove the convergence of the latter approximation scheme, and to derive an upper bound on the approximation error. Numerical experiments are performed for the approximation of the solution of the mean curvature flow equation in dimensions two and three, and for two and five-dimensional (plus time) fully-nonlinear Hamilton-Jacobi-Bellman equations arising in the theory of portfolio optimization in financial mathematics.

keywords:

[class=AMS]keywords:

math.0905.1863 \startlocaldefs \endlocaldefs

T2We are grateful to Mete Soner, Bruno Bouchard, Denis Talay, and Frédéric Bonnans for fruitful comments and suggestions. T1This research is part of the Chair Financial Risks of the Risk Foundation sponsored by Société Générale, the Chair Derivatives of the Future sponsored by the Fédération Bancaire Française, the Chair Finance and Sustainable Development sponsored by EDF and Calyon.

, and

1 Introduction

We consider the probabilistic numerical scheme for the approximation of the solution of a fully-nonlinear parabolic Cauchy problem suggested in [12]. In the latter paper, a representation of the solution of the PDE is derived in terms of the newly introduced notion of second order backward stochastic differential equations, assuming that the fully-nonlinear parabolic Cauchy problem has a smooth solution. Then, similarly to the case of backward stochastic differential equations which are connected to semi-linear PDEs, this representation suggests a backward probabilistic numerical scheme.

The representation result of [12] can be viewed as an extension of the Feynman-Kac representation result, for the linear case, which is widely used in order to approach the numerical approximation problem from the probabilistic viewpoint, and to take advantage of the high dimensional properties of Monte Carlo methods. Previously, the theory of backward stochastic differential equations provided an extension of these approximation methods to the semi-linear case. See for instance Chevance [13], El Karoui, Peng and Quenez [18], Bally and Pagès [2], Bouchard and Touzi [9] and Zhang [32]. In particular, the latter papers provide the convergence of the “natural” discrete-time approximation of the value function and its partial space gradient with the same error of order , where is the length of time step. The discretization involves the computation of conditional expectations, which need to be further approximated in order to result into an implementable scheme. We refer to [2], [9] and [20] for an complete asymptotic analysis of the approximation, including the regression error.

In this paper, we observe that the backward probabilistic scheme of [12] can be introduced naturally without appealing to the notion of backward stochastic differential equation. This is shown is Section 2 where the scheme is decomposed into three steps:

(i) The Monte Carlo step consists in isolating the linear generator of some underlying diffusion process, so as to split the PDE into this linear part and a remaining nonlinear one.

(ii) Evaluating the PDE along the underlying diffusion process, we obtain a natural discrete-time approximation by using finite differences approximation in the remaining nonlinear part of the equation.

(iii) Finally, the backward discrete-time approximation obtained by the above steps (i)-(ii) involves the conditional expectation operator which is not computable in explicit form. An implementable probabilistic numerical scheme therefore requires to replace such conditional expectations by a convenient approximation, and induces a further Monte Carlo type of error.

In the present paper, we do not require the fully nonlinear PDE to have a smooth solution, and we only assume that it satisfies a comparison result in the sense of viscosity solutions. Our main objective is to establish the convergence of this approximation towards the unique viscosity solution of the fully-nonlinear PDE, and to provide an asymptotic analysis of the approximation error.

Our main results are the following. We first prove the convergence of the discrete-time approximation for general nonlinear PDEs, and we provide bounds on the corresponding approximation error for a class of Hamilton-Jacobi-Bellman PDEs. Then, we consider the implementable scheme involving the Monte Carlo error, and we similarly prove a convergence result for general nonlinear PDEs, and we provide bounds on the error of approximation for Hamilton-Jacobi-Bellman PDEs. We observe that our convergence results place some restrictions on the choice of the diffusion of the underlying diffusion process. First, a uniform ellipticity condition is needed; we believe that this technical condition can be relaxed in some future work. More importantly, the diffusion coefficient is needed to dominate the partial gradient of the remaining nonlinearity with respect to its Hessian component. Although we have no theoretical result that this condition is necessary, our numerical experiments show that the violation of this condition leads to a serious mis-performance of the method, see Figure 5.

Our proofs rely on the monotonic scheme method developed by Barles and Souganidis [7] in the theory of viscosity solutions, and the recent method of shaking coefficients of Krylov [24], [25] and [26] and Barles and Jakobsen [6], [5] and [4]. The use of the latter type of methods in the context of a stochastic scheme seems to be new. Notice however, that our results are of a different nature than the classical error analysis results in the theory of backward stochastic differential equations, as we only study the convergence of the approximation of the value function, and no information is available for its gradient or Hessian with respect to the space variable.

The following are two related numerical methods based on finite differences in the context of Hamilton-Jacobi-Bellman nonlinear PDEs:

-

•

Bonnans and Zidani [8] introduced a finite difference scheme which satisfies the crucial monotonicity condition of Barles and Souganidis [7] so as to ensure its convergence. Their main idea is to discretize both time and space, approximate the underlying controlled forward diffusion for each fixed control by a controlled local Markov chain on the grid, approximate the derivatives in certain directions which are found by solving some further optimization problem, and optimize over the control. Beyond the curse of dimensionality problem which is encountered by finite differences schemes, we believe that our method is much simpler as the monotonicity is satisfied without any need to treat separately the linear structures for each fixed control, and without any further investigation of some direction of discretization for the finite differences.

-

•

An alternative finite-differences scheme is the semi-Lagrangian method which solves the monotonicity requirement by absorbing the dynamics of the underlying state in the finite difference approximation, see e.g. Debrabant and Jakobsen [15], Camilli and Jacobsen [11], Camilli and Falcone [10], and Munos and Zidani [30] . Loosely speaking, this methods is close in spirit to ours, and corresponds to freezing the Brownian motion , over each time step , to its average order . However it does not involve any simulation technique, and requires the interpolation of the value function at each time step. Thus it is also subject to the curse of dimensionality problems.

We finally observe a connection with the recent work of Kohn and Serfaty [23] who provide a deterministic game theoretic interpretation for fully nonlinear parabolic problems. The game is time limited and consists of two players. At each time step, one tries to maximize her gain and the other to minimize it by imposing a penalty term to her gain. The nonlinearity of the fully nonlinear PDE appears in the penalty. Also, although the nonlinear penalty does not need to be elliptic, a parabolic nonlinearity appears in the limiting PDE. This approach is very similar to the representation of [12] where such a parabolic envelope appears in the PDE, and where the Brownian motion plays the role of Nature playing against the player.

The paper is organized as follows. In Section 2, we provide a natural presentation of the scheme without appealing to the theory of backward stochastic differential equations. Section 3 is dedicated to the asymptotic analysis of the discrete-time approximation, and contains our first main convergence result and the corresponding error estimate. In Section 4, we introduce the implementable backward scheme, and we further investigate the induced Monte Carlo error. We again prove convergence and we provide bounds on the approximation error. Finally, Section 5 contains some numerical results for the mean curvature flow equation on the plane and space, and for a five-dimensional Hamilton-Jacobi-Bellman equation arising in the problem of portfolio optimization in financial mathematics.

Notations For scalars , we write , , , and . By , we denote the collection of all matrices with real entries. The collection of all symmetric matrices of size is denoted , and its subset of nonnegative symmetric matrices is denoted by . For a matrix , we denote by its transpose. For , we denote . In particular, for , and are vectors of and reduces to the Euclidean scalar product.

For a function from to , we say that has polynomial growth (resp. exponential growth) if

| (resp. |

For a suitably smooth function on , we define

| and |

Finally, we denote the norm of a r.v. by .

2 Discretization

Let and be two maps from to and , respectively. With . We define the linear operator:

Given a map

we consider the Cauchy problem:

| (2.1) | |||

| (2.2) |

Under some conditions, a stochastic representation for the solution of this problem was provided in [12] by means of the newly introduced notion of second order backward stochastic differential equations. As an important implication, such a stochastic representation suggests a probabilistic numerical scheme for the above Cauchy problem.

The chief goal of this section is to obtain the probabilistic numerical scheme suggested in [12] by a direct manipulation of (2.1)-(2.2) without appealing to the notion of backward stochastic differential equations.

To do this, we consider an -valued Brownian motion on a filtered probability space , where the filtration satisfies the usual completeness conditions, and is trivial.

For a positive integer , let , , , and consider the one step ahead Euler discretization

| (2.3) |

of the diffusion corresponding to the linear operator . Our analysis does not require any existence and uniqueness result for the underlying diffusion . However, the subsequent formal discussion assumes it in order to provides a natural justification of our numerical scheme.

Assuming that the PDE (2.1) has a classical solution, it follows from Itô’s formula that

where we ignored the difficulties related to local martingale part, and denotes the expectation operator conditional on . Since solves the PDE (2.1), this provides

By approximating the Riemann integral, and replacing the process by its Euler discretization, this suggest the following approximation of the value function

| and | (2.4) |

where we denoted for a function with exponential growth:

| (2.5) | |||

| (2.6) |

and is the th order partial differential operator with respect to the space variable . The differentiations in the above scheme are to be understood in the sense of distributions. This algorithm is well-defined whenever has exponential growth and is a Lipschitz map. To see this, observe that any function with exponential growth has weak gradient and Hessian because the Gaussian kernel is a Schwartz function, and the exponential growth is inherited at each time step from the Lipschitz property of .

At this stage, the above backward algorithm presents the serious drawback of involving the gradient and the Hessian in order to compute . The following result avoids this difficulty by an easy integration by parts argument.

Lemma 2.1.

For every function with exponential growth, we have:

where and

| (2.7) |

Proof. The main ingredient is the following easy observation. Let be a one dimensional Gaussian random variable with unit variance. Then, for any function with exponential growth, we have:

| (2.8) |

where is the th order derivative of in the sense of distributions, and is the one-dimensional Hermite polynomial of degree .

1 Now, let be a function with exponential growth. Then, by direct conditioning, it follows from (2.8) that

and therefore:

2 For , it follows from (2.8) that

and for :

This provides:

In view of Lemma 2.1, the iteration which computes out of in (2.4)-(2.5) does not involve the gradient and the Hessian of the latter function.

Remark 2.2.

Observe that the choice of the drift and the diffusion coefficients and in the nonlinear PDE (2.1) is arbitrary. So far, it has been only used in order to define the underlying diffusion . Our convergence result will however place some restrictions on the choice of the diffusion coefficient, see Remark 3.4.

Once the linear operator is chosen in the nonlinear PDE, the above algorithm handles the remaining nonlinearity by the classical finite differences approximation. This connection with finite differences is motivated by the following formal interpretation of Lemma 2.1, where for ease of presentation, we set , , and :

-

•

Consider the binomial random walk approximation of the Brownian motion , , where are independent random variables distributed as . Then, this induces the following approximation:

which is the centered finite differences approximation of the gradient.

-

•

Similarly, consider the trinomial random walk approximation , , where are independent random variables distributed as , so that for all integers . Then, this induces the following approximation:

which is the centered finite differences approximation of the Hessian.

In view of the above interpretation, the numerical scheme studied in this paper can be viewed as a mixed Monte Carlo–Finite Differences algorithm. The Monte Carlo component of the scheme consists in the choice of an underlying diffusion process . The finite differences component of the scheme consists in approximating the remaining nonlinearity by means of the integration-by-parts formula of Lemma 2.1.

3 Asymptotics of the discrete-time approximation

3.1 The main results

Our first main convergence results follow the general methodology of Barles and Souganidis [7], and requires that the nonlinear PDE (2.1) satisfies a comparison result in the sense of viscosity solutions.

We recall that an upper-semicontinuous (resp. lower semicontinuous) function (resp. ) on , is called a viscosity subsolution (resp. supersolution) of (2.1) if for any and any smooth function satisfying

we have:

Definition 3.1.

We say that (2.1) has comparison for bounded functions if for any bounded upper semicontinuous subsolution and any bounded lower semicontinuous supersolution on , satisfying

we have .

Remark 3.2.

Barles and Souganidis [7] use a stronger notion of comparison by accounting for the final condition, thus allowing for a possible boundary layer. In their context, a supersolution and a subsolution satisfy:

| (3.1) | |||||

| (3.2) |

We observe that, by the nature of our equation, (3.1) and (3.2) imply that the subsolution and the supersolution , i.e. the final condition holds in the usual sense, and no boundary layer can occur. To see this, without loss of generality we suppose that is decreasing with respect to (see Remark 3.13). Let be a function satisfying

Then define for . Then also has a maximum at , and the subsolution property (3.1) implies that

For a sufficiently large , this provides the required inequality . A similar argument shows that (3.1) implies that .

In the sequel, we denote by , and the partial gradients of with respect to , and , respectively. We also denote by the pseudo-inverse of the non-negative symmetric matrix . We recall that any Lipschitz function is differentiable a.e.

Assumption F (i) The nonlinearity is Lipschitz-continuous with respect to uniformly in , and ;

(ii) is elliptic and dominated by the diffusion of the linear operator , i.e.

| on | (3.3) |

(iii) and .

Remark 3.3.

Assumption F (iii) is equivalent to

| where | (3.4) |

This is immediately seen by recalling that, by the symmetric feature of , any has an orthogonal decomposition , and by the nonnegativity of :

Remark 3.4.

The above Condition (3.3) places some restrictions on the choice of the linear operator in the nonlinear PDE (2.1). First, is required to be uniformly elliptic, implying an upper bound on the choice of the diffusion matrix . Since , this implies in particular that our main results do not apply to general degenerate nonlinear parabolic PDEs. Second, the diffusion of the linear operator is required to dominate the nonlinearity which places implicitly a lower bound on the choice of the diffusion .

Example 3.5.

Let us consider the nonlinear PDE in the one-dimensional case where are given constants. Then if we restrict the choice of the diffusion to be constant, it follows from Condition F that , which implies that . If the parameters and do not satisfy the latter condition, then the diffusion has to be chosen to be state and time dependent.

Theorem 3.6 (Convergence).

Remark 3.7.

Under the boundedness condition on the coefficients and , the restriction to a bounded terminal data in the above Theorem 3.6 can be relaxed by an immediate change of variable. Let be a function with exponential growth for some . Fix some , and let be an arbitrary smooth positive function with:

| for |

so that both and are bounded. Let

| for |

Then, the nonlinear PDE problem (2.1)-(2.2) satisfied by converts into the following nonlinear PDE for :

| (3.5) | |||||

where

Recall that the coefficients and are assumed to be bounded. Then, it is easy to see that satisfies the same conditions as . Since is bounded, the convergence Theorem 3.6 applies to the nonlinear PDE (3.5).

Remark 3.8.

Theorem 3.6 states that the inequality (3.3) (i.e. diffusion must dominate the nonlinearity in ) is sufficient for the convergence of the Monte Carlo–Finite Differences scheme. We do not know whether this condition is necessary:

Subsection 3.4 suggests that this condition is not sharp in the simple linear case,

however, our numerical experiments of Section 5 reveal that the method may have a poor performance in the absence of this condition, see Figure 5.

We next provide bounds on the rate of convergence of the Monte Carlo–Finite Differences scheme in the context of nonlinear PDEs of the Hamilton-Jacobi-Bellman type in the same context as [6]. The following assumptions are stronger than Assumption and imply that the nonlinear PDE (2.1) satisfies a comparison result for bounded functions.

Assumption HJB The nonlinearity satisfies Assumption F(ii)-(iii), and is of the Hamilton-Jacobi-Bellman type:

where the functions , , , , and satisfy:

Assumption HJB+ The nonlinearity satisfies HJB, and for any , there exists a finite set such that for any :

Remark 3.9.

The assumption HJB+ is satisfied if is a separable topological space and , , and are continuous maps from to ; the space of bounded maps which are Lipschitz in and –Hölder in .

Theorem 3.10 (Rate of Convergence).

Assume that the final condition is bounded Lipschitz-continuous. Then, there is a constant such that:

-

(i)

under Assumption HJB, we have ,

-

(ii)

under the stronger condition HJB+, we have .

The above bounds can be improved in some specific examples. See Subsection 3.4 for the linear case where the rate of convergence is improved to .

We also observe that, in the PDE Finite Differences literature, the rate of convergence is usually stated in terms of the discretization in the space variable . In our context of stochastic differential equation, notice that is or the order of . Therefore, the above upper and lower bounds on the rate of convergence corresponds to the classical rate and , respectively.

3.2 Proof of the convergence result

We now provide the proof Theorem 3.6 by building on Theorem 2.1 and Remark 2.1 of Barles and Souganidis [7] which requires the scheme to be consistent, monotone and stable. Moreover, since we are assuming the (weak) comparison for the equation, we also need to prove that our scheme produces a limit which satisfies the terminal condition in the usual sense, see Remark 3.2.

Throughout this section, all the conditions of Theorem 3.6 are in force.

Lemma 3.11.

Let be a smooth function with bounded derivatives. Then for all :

The proof is a straightforward application of Itô’s formula, and is omitted.

Lemma 3.12.

Proof. By Lemma 2.1 the operator can be written as:

Let where and are as in the statement of the lemma. Let denote the partial gradient with respect to . By the mean value Theorem:

for some . By the definition of :

where the dependence on and has been omitted for notational simplicity. Since by (3.4) of Assumption , we have and therefore:

Let , where the function is defined in (3.4). Under Assumption F, we have , then

one can write,

for some constant , where the last inequality follows from (3.4).

The following observation will be used in the proof of Theorem 3.10 below.

Remark 3.13.

The monotonicity result of the previous Lemma 3.12 is slightly different from that required in [7]. However, as it is observed in Remark 2.1 in [7], their convergence theorem holds under this approximate monotonicity. From the previous proof, we observe that if the function satisfies the condition:

| (3.7) |

then, the standard monotonicity condition

| (3.8) |

holds. Using the parabolic feature of the equation, we may introduce a new function which solves a nonlinear PDE satisfying (3.7). Indeed, direct calculation shows that the PDE inherited by is:

| on | (3.9) | ||||

| on | (3.10) |

where . Then, it is easily seen that satisfies the same conditions as together with (3.7) for sufficiently large .

Lemma 3.14.

Let be two bounded functions. Then there exists a constant such that

In particular, if is bounded, the family defined in (2.4) is bounded, uniformly in .

Proof. Let . Then, arguing as in the previous proof,

where

Since , , and by Assumption , it follows that

But, . Therefore, by Assumption F

To prove that the family is bounded, we proceed by backward induction. By the assumption of the lemma is bounded. We next fix some and we assume that for every . Proceeding as in the proof of Lemma 3.12 with and , we see that

Since is bounded by Assumption , it follows from the discrete Gronwall inequality that for some constant independent of .

Remark 3.15.

Lemma 3.16.

The function is Lipschitz in , uniformly in .

Proof. We report the following calculation in the one-dimensional case in order to simplify the presentation.

1. For fixed , we argue as in the proof of Lemma 3.12 to see that for with :

| (3.11) |

where, denoting for :

by Assumption F (i). By Lemma 2.1 we write for :

Then, dividing both sides of (3.11) by and taking limsup, if follows from the above equalities that

2. Assume is Lipschitz with constant . Then

Observe that

Since all terms on the right hand-side are bounded, under our assumptions, it follows that (we emphasize that the geometric structure imposed in Assumption F (iii) provides this result in any dimension). Then:

3. Let be the probability measure equivalent to defined by the density

| where |

Then,

By Cauchy–Schwartz inequality, we have

By writing back the expectation in terms of probability ,

By expanding the quadratic term inside the expectation, we observe that expectation of all the terms having , is zero. Therefore,

which leads to

for some constants .

Finally, we prove that the terminal condition is preserved by our scheme as the time step shrinks to zero.

Lemma 3.17.

For each and with , we have;

Proof. 1. By the same argument as in the proof of Lemma 3.14, we have: and for :

where , , , are adapted random variables defined as in the proof of Lemma 3.14 at , and has a standard Gaussian distribution. Combine the above formula for from to , we see that

where a.s. for all and . Obviously is a martingale for all , a property which will be used later. Since , and using Assumption F and Lemmas 3.16 and 3.14:

| (3.12) |

2. Let be the family of smooth functions obtained from by convolution with a family of mollifiers , i.e. . Note that we have

| and | (3.13) |

Then:

| (3.14) | |||||

where we denoted and for and . We next estimate each term separately.

2.a. First, since is a martingale:

Notice that

Using Lemma 2.1 and (3.13), this provides:

| (3.15) | ||||

| (3.16) |

2.c. By (3.13) and the boundedness of and , we also estimate that:

| (3.17) |

2.b. Plugging (3.16) and (3.17) into (3.14), we obtain:

which by (3.12) provides:

The required result follows from the choice .

Corollary 3.18.

The function is 1/2-Hölder continuous on uniformly on .

Proof. The proof of -Hölder continuity with respect to could be easily provided by replacing and in the assertion of Lemma respectively by and and consider the scheme from to time with time step equal to . Therefore, we can write;

where could be chosen independent of for .

3.3 Derivation of the rate of convergence

The proof of Theorem 3.10 is based on Barles and Jakobsen [6], which uses switching systems approximation and the Krylov method of shaking coefficients [24].

3.3.1 Comparison result for the scheme

Because does not satisfy the standard monotonicity condition (3.8) of Barles and Souganidis [7], we need to introduce the nonlinearity of Remark 3.13 so that satisfies (3.7). Let be the familiy of functions defined by

| (3.18) |

where for a function from to with exponential growth:

and set

| (3.19) |

The following result shows that the difference is of higher order, and thus reduces the error estimate problem to the analysis of the difference .

Lemma 3.19.

Under Assumption , we have

Proof. By definition of , we directy calculate that:

Since , this shows that . By lemma 3.14, we conclude that:

which shows by the Gronwall inequality that for all .

By Remark 3.13, the operator satisfies the standard monotonicity condition (3.8):

| (3.20) |

The key-ingredient for the derivation of the error estimate is the following comparison result for the scheme.

Proposition 3.20.

Let Assumption holds true, and set . Consider two arbitrary bounded functions and satisfying:

| and | (3.21) |

for some bounded functions and . Then, for every :

| (3.22) |

To prove this comparison result, we need the following strengthening of the monotonicity condition:

Lemma 3.21.

Let Assumption hold true and let . Then, for every , and every bounded functions , the function satisfies:

Proof. Because does not depend on , we have , where . Then, it follows from the regularity of that there exist some such that:

and

Since satisfies the standard monotonicity condition (3.20), this provides:

| where |

It remains to prove that . From the smoothness of , we have for some . Then, since is decreasing in , we see that

and the required estimate follows from the restriction .

Proof of Proposition 3.20. We may refer directly to the similar result of [6]. However in our context, we give the following simpler proof. Observe that we may assume without loss of generality that

| and | (3.23) |

Indeed, one can otherwise consider the function

| where |

and is the parameter defined in the previous Lemma 3.21, so that and, by Lemma (3.21), . Hence (3.23) holds true for and .

3.3.2 Proof of Theorem 3.10 (i)

Under the conditions of Assumption HJB on the coefficients, we may build a bounded subsolution of the nonlinear PDE, by the method of shaking the coefficients, which is Lipschitz in , Hölder continuous in , and approximates uniformly the solution :

Let be a positive function supported in with unit mass, and define

| where | (3.24) |

so that, from the convexity of the operator ,

| is a subsolution of (2.1), | (3.25) |

Moreover, since is Lipschitz in , and Hölder continuous in ,

| and | ||||

| for any |

where , and is some constant. As a consequence of the consistency result of Lemma 3.11 above, we know that

converges to as . The next key-ingredient is to estimate the rate of convergence of to zero:

Lemma 3.22.

For a family of smooth functions satisfying (3.3.2), we have:

| for some constant |

The proof of this result is reported at the end of this section. From the previous estimate together with the subsolution property of , we see that . Then, it follows from Proposition 3.20 that

| (3.27) |

We now use (3.25) and (3.27) to conclude that

Minimizing the right hand-side estimate over the choice of , this implies the upper bound on the error :

| (3.28) |

3.3.3 Proof of Theorem 3.10 (ii)

The results of the previous section, together with the reinforced assumption HJB+, allow to apply the switching system method of Barles and Jakobsen [6] which provides the lower bound on the error:

for some constants . The required rate of convergence follows again from Lemma 3.19 which states that the difference is dominated by the above rate of convergence.

Proof of Lemma 3.22 Notice that the evolution of the Euler approximation between and is driven by a constant drift and a constant diffusion . Since is bounded, it follows from Itô’s formula that:

where is the Dynkin operator associated to the Euler scheme:

Applying again Itô’s formula, and using the fact that is bounded, leads to

Using the boundedness of the coefficients and , it follows from (3.3.2) that for :

Step 2 This implies that

| (3.29) | |||||

by the Lipschitz continuity of the nonlinearity .

By a similar calculation as in Step 1, we see that:

which, together with (3.29), provides the required result.

3.4 The rate of convergence in the linear case

In this subsection, we specialize the discussion to the linear one-dimensional case

| (3.30) |

for some . The multi-dimensional case can be handled similarly. Assuming that is bounded, the linear PDE (2.1)-(2.2) has a unique bounded solution

| for | (3.31) |

We also observe that this solution is with

| (3.32) |

This shows in particular that has bounded derivatives of any order, whenever the terminal data is and has bounded derivatives of any order.

Of course, one can use the classical Monte Carlo estimate to produce an approximation of the function of (3.31). The objective of this section is to analyze the error of the numerical scheme outlined in the previous sections. Namely:

| (3.33) |

Here, and are used to write the above scheme.

Proposition 3.23.

Consider the linear of (3.30), and assume that is bounded for every . Then

Proof. Since has bounded first derivative with respect to , it follows from Itô’s formula that:

Then, in view of Lemma 2.1, the error satisfies and for :

| (3.34) | |||||

where is the expectation operator conditional on .

Step 1

Set

and we introduce the matrices

and we observe that (3.34) implies that the vectors and satisfy for all , and therefore:

| (3.36) |

By direct calculation, we see that the powers are given by:

| for all |

In particular, because , . Iterating (3.36), this provides:

and therefore:

| (3.37) |

Because of

| for all |

we can write (3.37):

By changing the order of the summations in the above we conclude that:

| (3.38) |

Step 2 From our assumption that is bounded for every , it follows that

for some constant . We then deduce from (3.38) that:

So,

4 Probabilistic Numerical Scheme

In order to implement the backward scheme (2.4), we still need to discuss the numerical computation of the conditional expectations involved in the definition of the operators in (2.5). In view of the Markov feature of the process , these conditional expectations reduce to simple regressions. Motivated by the problem of American options in financial mathematics, various methods have been introduced in the literature for the numerical approximation of these regressions. We refer to [9] and [20] for a detailed discussion.

The chief object of this section is to investigate the asymptotic properties of our suggested numerical method when the expectation operator in (2.4) is replaced by some estimator corresponding to a sample size :

| (4.1) | |||||

| (4.2) |

where

where

| and |

The above bounds are needed for technical reasons which were already observed in [9].

With these notations, the implementable numerical scheme is:

| (4.3) |

where is defined in (4.1)-(4.2), and the presence of throughout this section emphasizes the dependence of our estimator on the underlying sample.

Let be the family of random variables of the form where is a function with and ’s are the Hermite polynomials:

Assumption E There exist constants such that

for every , for some .

Example 4.1.

Consider the regression approximation based on the Malliavin integration by parts as introduced in Lions and Reigner [27], Bouchard, Ekeland and Touzi [3], and analyzed in the context of the simulation of backward stochastic differential equations by [9] and [14]. Then Assumption E is satisfied for every with the constants and , see [9].

Our next main result establishes conditions on the sample size and the time step which guarantee the convergence of towards .

Theorem 4.2.

Let Assumptions E and F hold true, and assume that the fully nonlinear PDE (2.1) has comparison with growth . Suppose in addition that

| (4.4) |

Assume that the final condition is bounded Lipschitz, and the coefficients and are bounded. Then, for almost every :

| locally uniformly, |

where v is the unique viscosity solution of (2.1).

Proof. We adapt the argument of [7] to the present stochastic context. By Remark 3.13 and Lemma 3.19, we may assume without loss of generality that the strict monotonicity (3.7) holds.

By (4.2), we see that is uniformly bounded. So, we can define:

| and | (4.9) |

Our objective is to prove that and are respectively viscosity superpersolution and subsolution of (2.1). By the comparison assumption, we shall then conclude that they are both equal to the unique viscosity solution of the problem whose existence is given by Theorem 3.6. In particular, they are both deterministic functions.

We shall only report the proof of the supersolution property, the subsolution property follows from the same type of argument.

In order to prove that is a supersolution of (2.1), we consider together with a test function , so that

By classical manipulations, we can find a sequence so that and

Then, , and it follows from the monotonicity of the operator that:

By the definition of in (4.3), this provides:

where, for ease of notations, the dependence on has been dropped. Because , the last inequality gives:

where

We claim that

| (4.10) |

Then, after passing to the subsequence, dividing both sides by , and sending , it follows from Lemma 3.11 that:

which is the required supersolution property.

It remains to show (4.10). We start by bounding with respect to the error of estimation of conditional expectation. By Lemma 3.14, and so by (4.2), we can write:

| (4.11) |

By the Lipschitz-continuity of , we have:

where:

Therefore,

where , and is Hermite polynomial of degree . This leads the following estimate for the error :

| (4.12) |

Because with bound obtained in Lemma 3.14 by Assumption E we have,:

We finally discuss the choice of the sample size so as to keep the same rate for the error bound.

Theorem 4.3.

Let the nonlinearity be as in Assumption HJB, and consider a regression operator satisfying Assumption E. Let the sample size be such that

| (4.13) |

Then, for any bounded Lipschitz final condition , we have the following bounds on the rate of convergence:

Proof. By Remark 3.13 and Lemma 3.19, we may assume without loss of generality that the strict monotonicity (3.7) holds true.

We proceed as in the proof of Theorem 3.10 to see that

Since satisfies (4.3),

| where |

where, in the present context, is a non-zero stochastic term. By Proposition 3.20, it follows from the last inequality that:

where the constant depends only on the Lipschitz coefficient of , in Lemma 3.21 and the constant in Lemma 3.22.

Similarly, we follow the line of argument of the proof of Theorem 3.10 to show that a lower bound holds true, and therefore:

We now use (4.13) and proceed as in the last part of the proof of Theorem 4.2 to deduce from (4.12) and Assumption F that

With this choice of the sample size , the above error estimate reduces to

and the additional term does not affect the minimization with respect to .

Example 4.4.

Let us illustrate the convergence results of this section in the context of the Malliavin integration by parts regression method of [27] and [9] where and for every . So, for the convergence result we need to choose of the order of with . For the -rate of convergence result, we need to choose of the order of with .

5 Numerical Results

In this section, we provide an application of the Monte Carlo-finite differences scheme suggested in this paper in the context of two different types of problems. We first consider the classical mean curvature flow equation as the simplest front propagation example. We test our backward probabilistic scheme on the example where the initial data is given by a sphere, for which an easy explicit solution is available. A more interesting geometric example in space dimensions 2 is also considered. We next consider the Hamilton-Jacobi-Bellman equation characterizing the classical optimal investment problem in financial mathematics. Here, we again test our scheme in dimension two where an explicit solution is available, and we consider more involved examples in space dimension 5, in addition to the time variable.

In all examples considered in this section the operator does not depend on the variable. We shall then drop this variable from our notations, and we simply write the scheme as:

| (5.1) |

where

and and are defined in Lemma 2.1. We recall from Remark 2.2 that:

| (5.2) |

The second representation is the one reported in [12] where the present backward probabilistic scheme was first introduced. These two representations induce two different numerical schemes because once the expectation operator is replaced by an approximation , equality does not hold anymore in the latter equation for finite . In our numerical examples below, we provide results for both methods. The numerical schemes based on the first (resp. second) representation will be referred to as scheme 1 (resp. 2). An important outcome of our numerical experiments is that scheme 2 turns out to have a significantly better performance than scheme 1.

Remark 5.1.

The second scheme needs some final condition for . Since is smooth in all our examples, we set this final condition to . Since the second scheme turns out to have a better performnace, we may also use the final condition for suggested by the first scheme.

We finally discuss the choice of the regression estimator in our implemented examples. Two methods have been used:

-

•

The first method is the basis projection a la Longstaff and Schwartz [28], as developed in [20]. We use regression functions with localized support : on each support the regression functions are chosen linear and the size of the support is adaptative according to the Monte Carlo distribution of the underlying process.

-

•

The second method is based on the Malliavin integration by parts formula as suggested in [27] and further developed in [3]. In particular, the optimal exponential localization function in each direction is chosen as follows. The optimal parameter is provided in [3] and should be chosen for each conditional expectation depending on . Our numerical experiments however revealed that such optimal parameters do not provide sufficiently good performance, and more accurate results are obtained by choosing for all values of .

5.1 Mean curvature flow problem

The mean curvature flow equation describes the motion of a surface where each point moves along the inward normal direction with speed proportional to the mean curvature at that point. This geometric problem can be characterized as the zero-level set of a function depending on time and space satisfying the geometric partial differential equation:

| and | (5.3) |

and is a bounded Lipschitz-continuous function. We refer to [31] for more details on the mean curvature problem and the corresponding stochastic representation.

To model the motion of a sphere in with radius , we take so that is positive inside the sphere and negative outside. We first solve the sphere problem in dimension 3. In this case, it is well-known that the surface is a sphere with a radius for . Reversing time, we rewrite (5.3) for with :

| and | (5.4) |

where

We implement our Monte Carlo-finite differences scheme to provide an approximation of the function . As mentioned before, we implement four methods: Malliavin integration by parts-based or basis projection-based regression, and scheme 1 or 2 for the representation of the Hessian.

Given the approximation , we deduce an approximation of the surface by using a dichotomic gradient descent method using the estimation of the gradient estimated along the resolution. The dichotomy is stopped when the solution is localized within accuracy.

Remark 5.2.

Of course the use of the gradient is not necessary in the present context where we know that is a sphere at any time . The algorithm described above is designed to handle any type of geometry.

Remark 5.3.

In our numerical experiments, the nonlinearity is truncated so that it is bounded by an arbitrary value taken equal to .

Our numerical results show that Malliavin and basis projection methods give similar results. However, for a given number of sample paths, the basis projection method of [20] are slightly more accurate. Therefore, all results reported for this example correspond to the basis projection method.

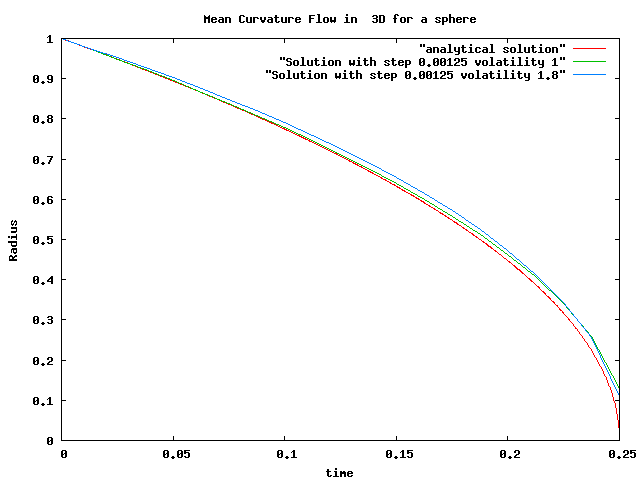

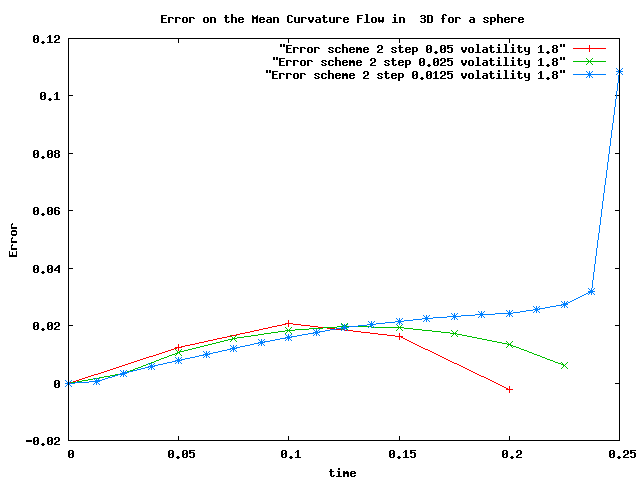

Figure 1 provides results obtained with one million particles and mesh with a time step equal to . The diffusion coefficient is taken to be either or . We observe that results are better with . We also observe that the error increases near time corresponding to an acceleration of the dynamics of the phenomenon, and suggesting that a thinner time step should be used at the end of simulation.

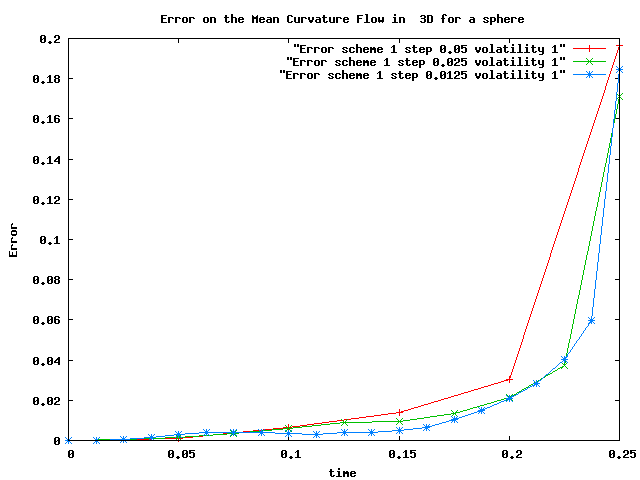

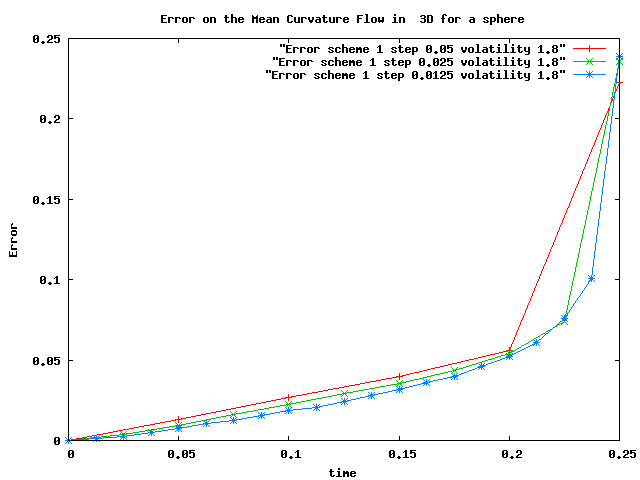

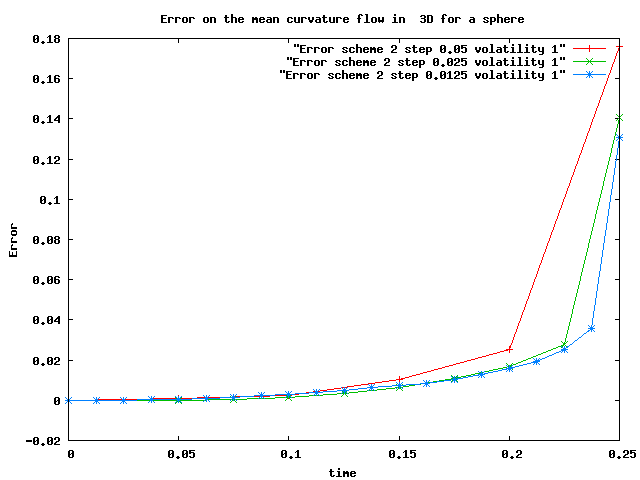

Figure 2 plots the difference between our calculation and the reference for scheme 1 and volatility 1 and 1.8 for varying time step. The corresponding results with scheme 2 are reported in figure 3. We notice that some points at time are missing due to a non convergence of the gradient method for a diffusion . We observe that results for scheme 2 are slightly better than results for scheme 1. With , it takes 150 seconds on a Nehalem intel processor 2.9 GHz to obtain the result at time with the regression method, while it takes 1500 seconds with the Malliavin method (notice that the dichotomy used with the gradient method is a very inefficient method).

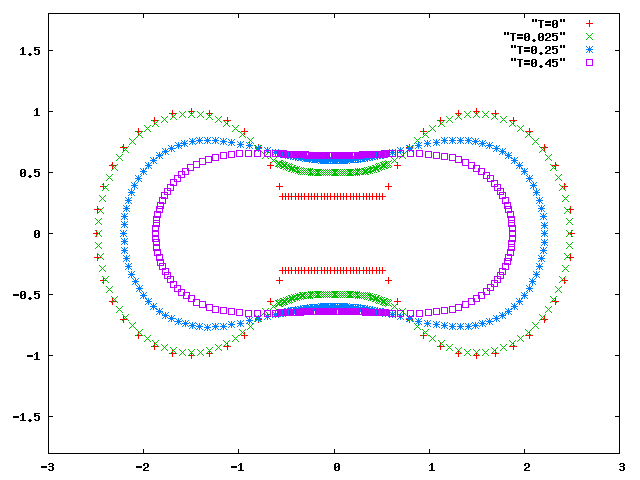

We finally report in Figure 4 some numerical results for the mean curvature flow problem in dimension 2 with a more interesting geometry: the initial surface (i.e. the zero-level set for ) consists of two disks with unit radius, with centers positioned at -1.5 and 1.5 and connected by a stripe of unit width. We give the resulting deformation with scheme 2 for a diffusion , a time step , and one million particles. Once again, the Malliavin integration by parts based regression method and the basis projection method with meshes produce similar results. We used points to describe the surface.

One advantage of this method is the total parallelization that can be performed to solve the problem for different points on the surface : for the results given parallelization by Message Passing (MPI) was achieved.

5.2 Continuous-time portfolio optimization

We next report an application to the continuous-time portfolio optimization problem in financial mathematics. Let be an Itô process modeling the price evolution of financial securities. The investor chooses an adapted process with values in , where is the amount invested in the th security held at time . In addition, the investor has access to a non-risky security (bank account) where the remaining part of his wealth is invested. The non-risky asset is defined by an adapted interest rates process , i.e. , . Then, the dynamics of the wealth process is described by:

where . Let be the collection of all adapted processes with values in , which are integrable with respect to and such that the process is uniformly bounded from below. Given an absolute risk aversion coefficient , the portfolio optimization problem is defined by:

| (5.5) |

Under fairly general conditions, this linear stochastic control problem can be characterized as the unique viscosity solution of the corresponding HJB equation. The main purpose of this subsection is to implement our Monte Carlo-finite differences scheme to derive an approximation of the solution of the fully nonlinear HJB equation in non-trivial situations where the state has a few dimensions. We shall first start by a two-dimensional example where an explicit solution of the problem is available. Then, we will present some results in a five dimensional situation.

5.2.1 A two dimensional problem

Let , for all , and assume that the security price process is defined by the Heston model [21]:

where is a Brownian motion in . In this context, it is easily seen that the portfolio optimization problem (5.5) does not depend on the state variable . Given an initial state at the time origin given by , the value function solves the HJB equation:

| (5.6) |

A quasi explicit solution of this problem was provided by Zariphopoulou [33]:

| (5.7) |

where the process is defined by

| and |

In order to implement our Monte Carlo-finite differences scheme, we re-write (5.6) as:

| (5.8) |

where and the nonlinearity is given by:

Notice that the nonlinearity does not to satisfy Assumption F, we consider the truncated nonlinearity:

for some jointly chosen with so that Assumption F holds true. Under this form, the forward two-dimensional diffusion is defined by:

| and | (5.9) |

In order to guarantee the non-negativity of the discrete-time approximation of the process , we use the implicit Milstein scheme [22]:

| (5.10) |

where is a sequence of independent random variable with distribution .

Our numerical results correspond to the following values of the parameter: , , , , , . The initial value of the portfolio is , the maturity is taken equal to one year. With this parameters, the value function is computed from the quasi-explicit formula (5.7) to be .

We also choose for the truncation of the nonlinearity. This choice turned out to be critical as an initial choice of produced an important bias in the results.

The two schemes have been tested with the Malliavin and basis projection methods. The latter was applied with basis functions. We provide numerical results corresponding to 2 millions particles. Our numerical results show that the Malliavin and the basis projection methods produce very similar results, and achieve a good accuracy: with 2 millions particles, we calculate the variance of our estimates by performing 100 independent calculations:

-

•

the results of the Malliavin method exhibit a standard deviation smaller than for scheme one (except for a step equal to and a volatility equal to where standard deviation jumped to ), for scheme two with a computing time of 378 seconds for 40 time steps,

-

•

the results of the basis projection method exhibit a standard deviation smaller than for scheme 1 and for scheme two with a computing time of 114 seconds for 40 time steps.

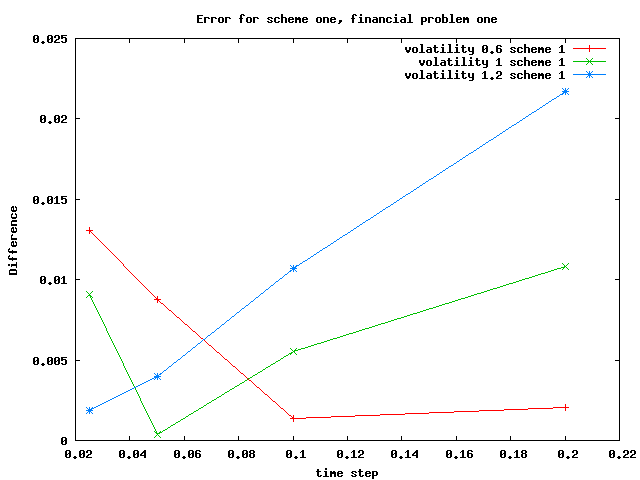

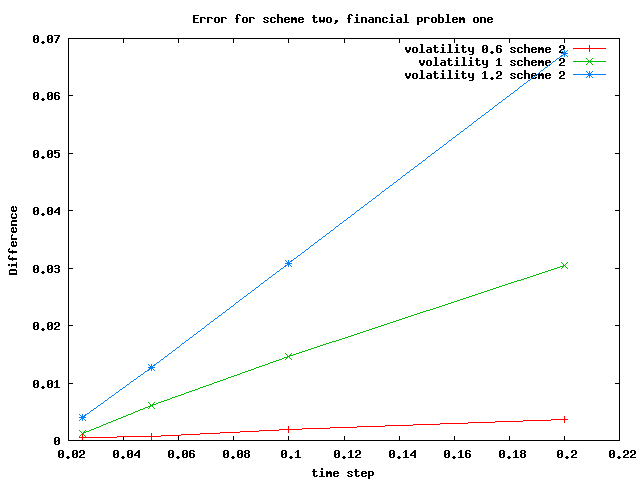

Figure 5 provides the plots of the errors obtained by the integration by parts-based regression with Schemes one and two. All solutions have been calculated as the average of 100 calculations. We first observe that for a small diffusion coefficient , the numerical performance of the algorithm is very poor: surprisingly, the error increases as the time step shrinks to zero and the method seems to be biased. This numerical result hints that the requirement that the diffusion should dominate the nonlinearity in Theorem 3.6, might be a sharp condition.

We also observe that scheme one has a persistent bias even for a very small time step, while scheme two exhibits a better convergence towards the solution.

5.2.2 A five dimensional example

We now let , and we assume that the interest rate process is defined by the Ornstein-Uhlenbeck process:

While the price process of the second security is defined by a Heston model, the first security’s price process is defined by a CEV-SV models, see e.g. [29] for a presentation of these models and their simulation:

where is a Brownian motion in , and for simplicity we considered a zero-correlation between the security price process and its volatility process.

Since , the value function of the portfolio optimization problem (5.5) does not depend on the variable. Given an initial state at the time origin , the value function satisfies the HJB equation:

| (5.11) |

where

In order to implement our Monte Carlo-finite differences scheme, we re-write (5.11) as:

| (5.12) |

where , and the nonlinearity is given by:

where . We next consider the truncated nonlinearity:

where are jointly chosen with so that Assumption F holds true. Under this form, the forward two-dimensional diffusion is defined by:

| (5.13) |

The component is simulated according to the exact discretization:

where is a sequence of independent random variable with distribution . The following scheme for the price of the asset guarantees non-negativity (see [1]) :

where . We take the following parameters , , for the first asset, , , for the diffusion process of the first asset. The second asset is defined by the same parameters as in the two dimensional example: , , and . As for the interest rate model we take , , .

The initial values of the portfolio the assets prices are all set to 1. For this test case we first use the basis projection regression method with meshes and three millions particles which, for example, takes 520 seconds for 20 time steps. Figure 6 contains the plot of the solution obtained by scheme 2, with different time steps. We only provide results for the implementation of scheme 1 with a coarse time step, because the method was diverging with a thinner time step. We observe that there is still a difference for very thin time step with the three considered values of the diffusion. This seems to indicate that more particles and more meshes are needed. While doing many calculation we observed that for the thinner time step mesh, the solution sometimes diverges. We therefore report the results corresponding to thirty millions particles with meshes. First we notice that with this discretization all results are converging as time step goes to zero: the exact solution seems to be very closed to . During our experiments with thirty millions particles, the scheme was always converging with a very low variance on the results. A single calculation takes 5100 seconds with 20 time steps.

Remark 5.4.

With thirty millions particles, the memory needed forced us to use 64-bit processors with more than four gigabytes of memory.

5.2.3 Conclusion on numerical results

The Monte Carlo-Finite Differences algorithm has been implemented with both schemes suggested by (5), using the basis projection and Malliavin regression methods. Our numerical experiments reveal that the second scheme performs better both in term of results and time of calculation for a given number of particles, independently of the regeression method.

We also provided numerical results for different choices of the diffusion parameter in the Monte Carlo step. We observed that small diffusion coefficients lead to poor results, which hints that the condition that the diffusion must dominate the nonlinearity in Assumption F (iii) may be sharp. On the other hand, we also observed that large diffusions require a high refinement of the meshes meshes, and large number of particles, leading to a high computational time.

Finally, let us notice that a reasonable choice of the diffusion could be time and state dependent, as in the classical importance sampling method. We have not tried any experiment in this direction, and we hope to have some theoretical results on how to choose optimally the drift and the diffusion coefficient of the Monte Carlo step.

References

- [1] Andersen, L.B.G. and Brotherton-Ratcliffe, R.(2005). “Extended LIBOR market models with stochastic volatility.” Journal of Computational Finance, Vol.9,1, 1-40,

- [2] Bally, V. (1995). “An Approximation Schemes For BSDEs and Applications to Control and Nonlinear PDEs”. Prepublication 95-15 du Laboratoire de Statistique et Processus de l’Universite du Maine.

- [3] Bouchard, B. and Ekeland, I. and Touzi, N. (2004) “On the Malliavin approach to Monte Carlo approximation of conditional expectations”. Finance and Stochastics, 8, 45-71.

- [4] Barles, G. and Jakobsen, E.R., “On the convergence rate of approximation schemes for Hamilton-Jacobi-Bellman equations”. Mathematical Modelling and Numerical Analysis, ESAIM, M2AM, Vol. 36 (2002), No. 1, 33-54.

- [5] Barles, G. and Jakobsen, E.R., “Error Bounds For Monotone Approximation Schemes For Hamilton-Jacobi-Bellman Equations”. SIAM J. Numer. Anal., Vol. 43 (2005), No. 2, 540-558.

- [6] Barles, G. and Jakobsen, E.R., “Error Bounds For Monotone Approximation Schemes For Parabolic Hamilton-Jacobi-Bellman Equations”. Math. Comp., 76(240):1861-1893, 2007.

- [7] Barles, G. and Souganidis, P. E. (1991) “Convergence of Approximation Schemes for Fully Non-linear Second Order Equation”. Asymptotic Anal., 4, pp. 271–283.

- [8] Bonnans, F. and Zidani, H. (2003). “Consistency of Generalized Finite Difference Schemes for the Stochastic HJB Equation”. SIAM J. Numerical Analysis 41-3, 1008-1021

- [9] Bouchard, B. and Touzi, N. (2004). “Discrete-time approximation and Monte Carlo simulation of backward stochastic differential equations”. Stochastic Processes and their Applications 111, 175–206.

- [10] Camilli, F. and Falcone, M. (1995) “An approximation scheme for the optimal control of diffusion processes”. RAIRO Modél. Math. Anal. Numér 29, 97–122.

- [11] Camilli, F. and Jakobsen, E.R., “A Finite Element like Scheme for Integro-Partial Differential Hamilton-Jacobi-Bellman Equations”. SIAM J. Numer. Anal. 47(4): 2407-2431, 2009.

- [12] P. Cheridito, Soner, H. M. Touzi, N. N. Victoir, “Second Order Backward Stochastic Differential Equations and Fully Non-Linear Parabolic PDEs”. Communications on Pure and Applied Mathematics, Volume 60, Issue 7, Date: July 2007, Pages: 1081-1110.

- [13] D. Chevance, “Ph.D. thesis”. Univ. Provence, (1996).

- [14] D. Crisan, K. Manolarakis, Touzi, N. “On the Monte Carlo simulation Of BSDE’s: An improvement on the Malliavin weights”. to appear in Stochastic Processes and their Applications.

- [15] Debrabant, K. and Jakobsen, E.R.. “Semi-Lagrangian schemes for linear and fully non-linear diffusion equations”. Preprint, 2009.

- [16] F. Delarue and S. Menozzi, “A Forward-Backward Stochastic Algorithm for Quasi-Linear PDEs”. Annals of Applied Probability, Vol. 16, No. 1, 140-184, 2006.

- [17] H. Dong, N. V. Krylov, “On The Rate Of Convergence Of Finite-Difference Approximations For Bellman’s Equations With Constant Coefficients”. St. Petersburg Math. J., Vol. 17 (2005), No. 2, 108-132.

- [18] N. El Karoui, S. Peng, M. C. Quenez, “Backward Stochastic Differential Equations in Finance”. Mathematical Finance, 7, 1-71 (1997).

- [19] L. C. Evans and A. Friedman, “Optimal stochastic switching and the Dirichlet problem for the Bellman equation”. Trans. Amer. Math. Soc. 253:365-389 (1979).

- [20] E. Gobet, J. P. Lemor, X. Warin “A regression-based Monte-Carlo method to solve backward stochastic differential equations”. Annals of Applied Probability, Vol.15(3), pp.2172-2002 - 2005.

- [21] S. L. Heston, “A Closed-Form Solution for Options with Stochastic Volatility with Applications to Bond and Currency Options”. The Review of Financial Studies, Vol.6(2), 327-343, 1993.

- [22] C. Kahl, P. Jackel “Fast strong approximation Monte Carlo schemes for stochastic volatility models” Quantitative Finance,Vol.6(6),513-536, 2006.

- [23] R. V. Kohn, S. Serfaty, “A deterministic-control-based approach to fully nonlinear parabolic and elliptic equations”. Preprint, to appear in Comm. Pure Appl. Math.

- [24] N. V. Krylov, “On The Rate Of Convergence Of Finite-Difference Approximations For Bellman’s Equations”. St. Petersburg Math. J., Vol. 9 (1997), No. 3, 245-256.

- [25] N. V. Krylov, “On The Rate Of Convergence Of Finite-Difference Approximations For Bellman’s Equations With Lipschitz Coefficients”. Applied Math. and Optimization, Vol. 52 (2005), No. 3, 365-399.

- [26] N. V. Krylov, “On The Rate Of Convergence Of Finite-Difference Approximations For Bellman’s Equations With Variable Coefficients”. Probab. Theory Ralat. fields, 117:1-16, 2000.

- [27] Lions, P.L., Regnier, H. (2001). Calcul du prix et des sensibilités d’une option américaine par une méthode de Monte Carlo. Preprint.

- [28] Longstaff, F.A. and Schwartz, R.S. (2001). Valuing American options by simulation: a simple least-square approach, Review of Financial Studies 14, pp. 113–147.

- [29] R. Lord, R. Koekkoek, D Van Dijk, “A comparison of biased simulation schemes for stochastic volatility models”. Quantitative Finance, vol. 10, no. 2, pp. 177-194, (2005).

- [30] Munos, R. and Zidani, H. (2010). “Consistency of a simple multidimensional scheme for Hamilton–Jacobi–Bellman equations”. C. R. Acad. Sci. Paris, Ser. I 340, pp. 499–502.

- [31] Soner, H. M. and Touzi, N. (2003). “A stochastic representation for mean curvature type geometric flows”. The Annals of Probability, Vol 31(3),1145-1165.

- [32] Zhang, J. (2004). “A numerical scheme for backward stochastic differential equations”. Annals of Applied Probability. 14 (1), 459-488.

- [33] Zariphopoulou, T. (2001). “A solution approach to valuation with unhedgeable risks”. Finance and Stochastics, 5 61-82.