1 Introduction

This work deals with a general method for building

stochastic processes for which certain aspects of the local form are prescribed.

We will mainly be interested here in local Hölder regularity and local intensity

of jumps, but our construction allows in principle to control

other properties that could be of interest. Our approach

is in the same spirit as the one proposed in [9], but it

uses different methods. In particular, in [9],

multistable processes, that is localisable processes which

are locally -stable, but where the index of stability

varies with time, were constructed using sums over

Poisson processes. We present here an alternative construction

of such processes, based on the Ferguson - Klass - LePage

series representation of stable stochastic processes [10, 13, 14].

This representation is a powerful tool for the study of various

aspects of stable processes, see for instance [3, 18].

A comprehensive reference for the properties of this representation

that will be needed here is [19].

Stochastic processes where the local Hölder regularity

varies with a parameter are interesting

both from a theoretical and practical point of view.

A well-known example is multifractional

Brownian motion (mBm), where the Hurst index of fractional

Brownian motion [12, 15] is replaced by a functional

parameter , permitting the Hölder exponent to

vary in a prescribed manner [1, 2, 11, 16].

This allows in addition local regularity

and long range dependence to be decoupled

to give sample paths that are both highly

irregular and highly correlated, a useful feature

for instance in terrain or TCP traffic modeling.

However, local regularity, as measured by the Hölder exponent, is not

the only local feature of a process that is useful

in theory and applications. Jump characteristics also

need to be accounted for, e.g. for studying processes

with paths in (the space of càdlàg functions,

i.e. functions which are continuous on the right and

have left limits at all ). This has applications for

instance in the modeling of financial or medical data.

Stable non-Gaussian processes yield relevant models for

data containing discontinuities, with the stability

index controlling the distribution of jumps.

Just for the same reason why it is interesting to consider stochastic processes whose

local Hölder exponent changes in a controlled manner, tractable models where

the “jump intensity” is allowed to vary in time

are needed, for instance to obtain a more accurate description of

some aspects of the local structure of functions in .

The approach described in this work allows in particular

to construct processes where both and

evolve in time in a prescribed way. Having two functional parameters allows

to finely tune the local properties of these processes. This may prove

useful to model two distinct aspects of financial risk,

to describe epileptic episodes in EEG

where for some periods there may be

only small jumps and at other instants very large ones,

or to study textured images where both Hölder regularity and

the distribution of discontinuities vary.

Let us now recall the definition of

a localisable process [6, 7]:

is said to be localisable at if there exists an

and a non-trivial limiting process such that

|

|

|

(1.1) |

(Note may and in general will vary with .) When the limit exits,

is termed the local form or tangent

process of at (see [2, 16] for similar notions).

The limit (1.1) may

be taken in several ways. In this work, we will only

deal with the case where convergence occurs

in finite dimensional distributions (equality in

finite dimensional distributions is denoted ). When convergence

takes place in distribution, the process is called

strongly -localisable (equality in

distributions is denoted ).

As mentioned above, a now classical example is

multifractional Brownian motion

which “looks like” index- fractional

Brownian motion close to time but where varies, that is

|

|

|

(1.2) |

where is index- fractional Brownian motion.

A generalization of mBm, where the Gaussian

measure is replaced by an -stable one, leads to

multifractional stable processes, where the

local form is an -self-similar linear

-stable motion [20, 21].

The -local form at , if it exists,

must be -self-similar, that is

for . In addition, as shown in [6, 7], under quite general

conditions, must also have stationary increments at almost all at

which there is strong localisability. Thus, typical local forms

are self-similar with stationary increments (sssi), that is

for

all and . Conversely, all sssi processes are localisable.

Classes of known sssi processes include fractional Brownian

motion, linear fractional stable motion and -stable Lévy

motion, see [5, 19].

Similarly to [9], our method for constructing localisable processes

is to make use of stochastic fields

, where is time, and where the process

is localisable for all . This field will allow to control

the local form of a ‘diagonal’ process

. For instance, in the case

of mBm, will be a field of fractional Brownian motions, i.e.

, where is a smooth function of

ranging in . This is the approach that was used originally

in [1] for studying mBm. From a heuristic point of view, taking

the diagonal of such a stochastic field constructs a new process with

local form depending on by piecing together

known localisable processes. In other words, we shall use random fields

such that

for each the local form of at

is the desired local

form of at . An easy situation is when, for each , the

process is sssi, since this automatically entails

localisability.

It is clear that, in this approach, the structure of

for in a neighbourhood of will be crucial to

determine the local

behaviour of near . A simple way to control this structure

is to define the random field as

an integral or sum of functions that depend on and with

respect to a single underlying random measure so as to

provide the necessary correlations.

General criteria that guarantee the transference of

localisability from the to

were obtained in [9]. We will make use of the

following one:

Theorem 1.1

Let be an interval with an interior point.

Suppose that for some the process

is -localisable at

with local form and

|

|

|

(1.3) |

as . Then is -localisable at

with .

In the sequel, we shall consider specific classes of random fields

and use Theorem 1.1 to build localisable processes with

interesting local properties. As a particular case, we will study

multifractional multistable processes, where both the local Hölder regularity

and intensity of jumps will evolve in a controlled manner.

The remaining of this article is organized as follows: we first

collect some notations in section 2.

We then build localisable processes using a series representation that

yields the necessary flexibility required for our purpose.

We need to distinguish between the

situations where the underlying space is finite (section 3),

or merely finite (section 4). In each case,

we define a random field depending on a “kernel” , and give

conditions on ensuring localisability of the diagonal process.

We then consider in section 5 some examples:

multistable Lévy motion, multistable reverse Ornstein-Uhlenbeck process,

log-fractional multistable motion and linear multistable multifractional motion.

Section 6 is devoted to computing the finite dimensional

distributions of our processes, and proving that they are the

same as the ones of the corresponding processes constructed in [9].

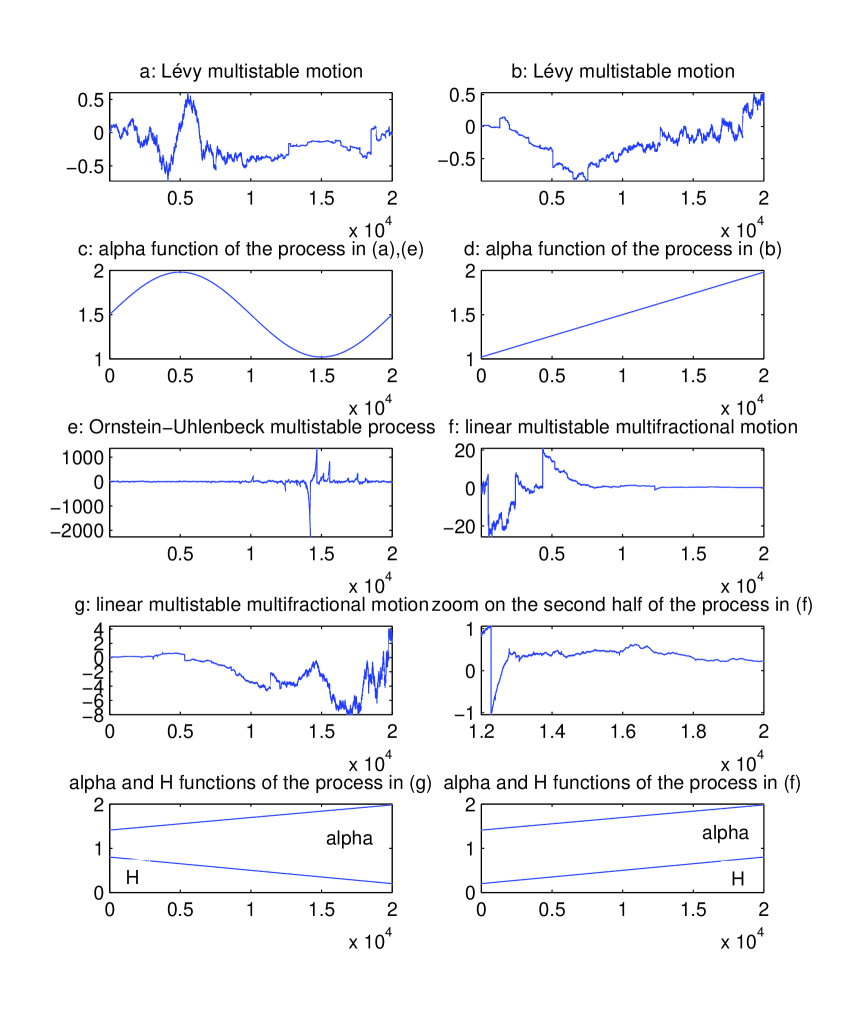

Finally, section 7 displays graphs of certain localisable

processes of interest, in particular multifractional multistable ones.

Before we proceed, we note that constructing localisable processes

using a stochastic field composed of sssi processes is obviously

not the only approach that one can think of.

It is for instance possible to follow a rather different path and construct

localisable processes from moving average ones by imposing

conditions on the kernel defining the moving average. See [8] for details.

3 A Ferguson - Klass - LePage series representation of localisable processes in the finite measure space case

A well-known representation of stable random variables is the

Ferguson - Klass - LePage series one [3, 10, 13, 14, 18].

This representation is particularly adapted for our purpose since,

as we shall see, it allows for

easy generalization to the case of varying .

In this work, we will use the following version:

Theorem 3.2

Let be a finite measure space, and be a symmetric -stable random measure with and finite control measure . Let be a sequence of arrival times of a Poisson process with unit arrival time, be a sequence of i.i.d. random variables with distribution on , and be a sequence of i.i.d. random variables with distribution . Assume finally that the three sequences , , and are independent. Then, for any ,

|

|

|

(3.7) |

where for , (Theorem 3.10.1 in [19] is more general, as it extends to non-symmetric stable processes, that are not considered here.) As mentioned above, a relevant feature of this representation for us is that the distributions of all random variables appearing in the sum are independent of . We will use (3.7) to contruct processes with varying as described in the following Theorem.

Theorem 3.3

Let be a finite measure space. Let be a function defined on and ranging in . Let be a function defined on . Let be a family of functions such that, for all , . Let be a sequence of arrival times of a Poisson process with unit arrival time, be a sequence of i.i.d. random variables with distribution on , and be a sequence of i.i.d. random variables with distribution . Assume finally that the three sequences , , and are independent.

Consider the following random field:

|

|

|

(3.8) |

where .

Assume that (as a process in ) is localisable at with exponent and local form . Assume in addition that:

-

•

(C1) The family of functions is differentiable for all in a neighbourhood of and almost all in . The derivatives of with respect to are denoted by .

-

•

(C2) There exists such that:

|

|

|

(3.9) |

-

•

(C3) There exists such that:

|

|

|

(3.10) |

-

•

(C4) There exists such that:

|

|

|

(3.11) |

Then is localisable at with exponent and local form .

The function is since ranges in . We shall denote . The function is thus also . We want to apply Theorem 1.1. With that in view, we estimate, for

(the ball centered at with radius ),

|

|

|

where

|

|

|

and

|

|

|

The reason for introducing the and the is that the

random variables are not independent, which complicates their study.

We shall decompose the sum involving the into series of independent

random variables which will be dealt with using the three series theorem.

The sum involving the will be studied by taking advantage of the

fact that, for large enough , each is “close” to in some

sense.

In the sequel, since only the values of inside

matter, we shall agree by convention that denotes in fact

and likewise

. Note that, by decreasing

, may be made arbitrarily small.

Thanks to the assumptions on and , and are differentiable and one computes:

|

|

|

and

|

|

|

|

|

|

The mean value theorem yields that there exists a sequence of independent random numbers (or ) and a sequence of random numbers (or ) such that:

|

|

|

where

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Note that each depends on , but not on . This remark will be useful in the sequel.

The remainder of the proof is divided into four steps. The first step will apply the three-series theorem to show that each series converges almost surely. In the

second step, we will prove that also

converges almost surely for . In the third step

we will prove that condition (1.3) is verified by . Finally, step four will prove

the same thing for .

First step: almost sure convergence of .

Consider . Fix . We shall deal successively

with the three series involved the three-series theorem.

First series: .

|

|

|

|

|

|

|

|

|

|

Note that, since is bounded on the compact interval ,

is

strictly positive.

|

|

|

|

|

|

|

|

|

|

Thus

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Second series: .

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

where we have used the facts that is independent of and . As a consequence,

.

Third series: The final series we need to consider is . Take .

Let be such that .

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Now, for all in ,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

where is

strictly positive. Thus,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The case of the is treated similarly, since the conditions required on in the proof above are also satisfied by .

Consider finally . Fix .

First series: .

|

|

|

|

|

|

|

|

|

|

where

is strictly positive by the assumptions on and . In the sequel, will always denote a finite positive constant, that may however change from line to line.

Let for and . For large enough and for all , is strictly increasing and . For large enough (independently of ),

|

|

|

|

|

|

|

|

|

|

Let be such that: .

Let .

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

On the one hand, vanishes for i large. On the other hand, by (C3),

|

|

|

|

|

|

|

|

|

|

and thus .

Second series: .

For the same reason as in the case of (i.e. is independent of ), , .

Third series: . Take again .

Let be such that , and be such that . Using the same line of reasoning as in the case of ,

|

|

|

|

|

We have, for all in ,

|

|

|

|

|

|

|

|

|

|

where

is strictly positive by the assumptions on and .

|

|

|

|

|

Let us deal with the first term of the sum in the right hand side of the above inequality.

|

|

|

|

|

for large enough, i.e. , where depends only on and . As a consequence

:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

But and thus

|

|

|

|

|

Now for the second term in the sum:

|

|

|

|

|

|

|

|

|

and as a consequence

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

We have thus verified all the conditions in the three series theorem, and

shown that the series and are almost surely convergent.

Second step: almost sure convergence of .

To prove that the series converge almost surely, we will first show that it is enough to prove that converges almost surely

for . Indeed, we prove now that

, where denotes

the complementary set of the set .

|

|

|

|

|

|

|

|

|

|

, as a sum of independent and identically distributed exponential random variables with mean , satisfy a Large Deviation Principle with rate function for and infinity for (see for instance [4] p.35), thus and .

Consider now for .

Case or :

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

thus

For

|

|

|

|

|

is bounded on , thus there exists such that

|

|

|

which entails that

We are thus left with proving that converges almost surely for .

In that view, we shall apply the following well-known lemma:

Lemma 3.4

Let be a sequence of random variables such that , then converges almost surely.

Let us show that .

|

|

|

|

|

|

|

|

|

|

Let .

Using the finite-increments formula applied to the function on , one easily shows that

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

where is strictly positive by the assumptions on and . Thus

|

|

|

|

|

Fix (since is continuous and

, by decreasing if necessary , one may ensure that

). By Markov and Hölder inequalities,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

where we have used that the variance of is equal to , and

K does not depend on thanks to assumption (C2).

Thus where .

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

thus with .

The case of is treated similarly, since the conditions required on in the proof above are also satisfied by .

We now consider .

Again by the finite-increments formula, there exists a constant , which depends on and , such that, for ,

|

|

|

|

|

|

|

|

|

|

|

|

|

Fix .

|

|

|

|

|

|

|

|

|

|

As a conclusion, for , converges almost surely.

We now move to the last two steps of the proof: to verify -localisability, we need to check that for some such that ,

and tend to 0 when tends to , for .

Third step: verification of (1.3) for .

We need to estimate .

Let .

|

|

|

|

|

|

|

|

|

|

Since is independent from for and is independent of

, Markov inequality yields

|

|

|

Let . For any , using the same computations as in the first step, third series (page 3), we get:

|

|

|

|

|

|

thus

|

|

|

The same conclusion holds for :

|

|

|

For , choose , and compute as on page 3:

|

|

|

|

|

|

|

|

|

|

For large enough, where depends only on and ,

|

|

|

thus

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

As a consequence, for :

|

|

|

|

|

|

|

|

|

|

Since

|

|

|

we get

|

|

|

Let . Using previously obtained inequalities, we get, for :

|

|

|

and

|

|

|

We consider now the second term .

Let . Since ,

the Borel-Cantelli lemma yields . As a consequence,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For , .

For , ,

and thus

|

|

|

|

|

|

|

|

|

|

For ,

|

|

|

and for ,

|

|

|

|

|

|

|

|

|

|

We have shown previously that the second term in the sum on the right hand side of the above inequality

is bounded from above by .

Finally,

|

|

|

Fourth step: verification of (1.3) for .

We consider now .

Let . Since ,

the Borel-Cantelli lemma yields . As a consequence,

|

|

|

|

|

Let .

Our strategy is the following: we show that, for each fixed , tend to 0 when tends to . Then

we prove that there exists a summable sequence such that, for all and all , . We conclude using the dominated convergence theorem that tends to 0 when tends to .

For all ,

|

|

|

|

|

For , consider .

|

|

|

|

|

Let With a positive constant that may change from line to line and depend on but not on , we have, for :

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Using the independence of and and Markov inequality,

|

|

|

|

|

|

|

|

|

|

It remains to check that the expectation in the right hand side of the above inequality is finite:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Since , and (this is easily verified by computing these expectations using the density of ). Thus we have , and

|

|

|

Since the conditions required on are also satisfied by ,

|

|

|

We consider now the case . When :

|

|

|

|

|

|

|

|

|

|

where again depends on but not on .

Since and is bounded, , and

|

|

|

For ,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

and

|

|

|

|

|

Since , the four terms in the right hand sides of the two last inequalities are finite (use again the density of ) and thus . As a consequence,

|

|

|

Finally, we have, for ,

|

|

|

Let us now consider, for , :

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(recall that the constants used in bounding the series do not depend on ). Thus

when for each .

In view of using the dominated convergence theorem, we compute (recall that ):

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For and ,

|

|

|

and if ,

|

|

|

The same conclusion holds for , while, for ,

|

|

|

5 Examples of localisable processes

In this section, we apply the results above and obtain some localisable

processes of interest. In particular, we consider “multistable versions” of several

classical processes. Similar multistable extensions were considered in

[9], to which the interested reader might refer for comparison.

We first recall some definitions. In the sequel, will denote

a symmetric -stable ()

random measure on with control measure Lebesgue measure .

We will write

|

|

|

for -stable Lévy motion.

The log-fractional stable motion is defined as

|

|

|

This process is well-defined only for

(the integrand does not belong to for ).

Both Lévy motion and log-fractional stable motion

are -self-similar with stationary increments.

The following process is called linear fractional -stable motion:

|

|

|

where , , , and

|

|

|

|

|

|

|

|

is again an sssi process. When , this process

is called well-balanced linear fractional -stable motion and denoted .

Finally, for , the stationary process

|

|

|

is called reverse Ornstein-Uhlenbeck process.

The localisability of Lévy motion, log-fractional stable motion and

linear fractional -stable motion simply stems from the fact that

they are sssi. The localisability of the reverse Ornstein-Uhlenbeck process

is proved in [8].

We will now define multistable versions of these processes.

For the multistable Lévy motion, we give two versions: one is fitted to

the case where the time parameter varies in a compact interval , and one

where it spans .

Theorem 5.6

(symmetric multistable Lévy motion, compact case).

Let and

be continuously differentiable. Let be a sequence of arrival times of a Poisson process with unit arrival time,

be a sequence of i.i.d. random variables with distribution , the uniform distribution on ,

and be a sequence of i.i.d. random variables with distribution .

Assume finally that the three sequences , , and are independent and

define

|

|

|

(5.17) |

then is -localisable at any

,

with local form .

The proof is a simple application of Theorem 3.3, and is omitted.

Theorem 5.7

(symmetric multistable Lévy motion, non-compact case).

Let and

be continuously differentiable. Let be a sequence of arrival times of a Poisson process with unit arrival time,

be a sequence of i.i.d. random variables with distribution on ,

and be a sequence of i.i.d. random variables with distribution .

Assume finally that the three sequences , , and are independent and

define

|

|

|

(5.18) |

then is -localisable at any

,

with local form .

We apply Theorem 4.5 with , , and the random field

|

|

|

is the symmetrical -Lévy motion [19] and is thus -localisable with local form .

-

•

(Cs1) The family of functions is differentiable for all in a neighbourhood of and almost all in . The derivatives of with respect to vanish.

-

•

(Cs2)

|

|

|

thus

|

|

|

and (Cs2) holds.

-

•

(Cs3) so (Cs3) holds.

-

•

(Cs4) so (Cs4) holds.

-

•

|

|

|

|

|

|

|

|

|

|

thus

|

|

|

and (Cs5) holds

Theorem 5.8

(Log-fractional multistable motion).

Let and

be continuously differentiable. Let be a sequence of arrival times of a Poisson process with unit arrival time,

be a sequence of i.i.d. random variables with distribution on , and be a sequence of i.i.d. random variables with distribution . Assume finally that the three sequences , , and are independent and

define

|

|

|

(5.19) |

then is -localisable at

any ,

with .

We apply Theorem 4.5 with , , and the random field

|

|

|

is the symmetrical -Log-fractional motion. It is -localisable with local form [9].

-

•

(Cs1) The family of functions is differentiable for all in a neighbourhood of and almost all in . The derivatives of with respect to vanish.

-

•

(Cs2) , such that so

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

and

|

|

|

|

|

thus (Cs2) holds.

-

•

(Cs3) so (Cs3) holds.

-

•

(Cs4)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

We shall bound each of the three terms that are added up in the right hand side

of the above inequality.

For the first term,

|

|

|

For the second term, fix , such that .

|

|

|

|

|

For the third term,

fix and such that

|

|

|

then

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The function is bounded for . With denoting an upper bound of this function, one has

|

|

|

|

|

With , we obtain

|

|

|

|

|

|

|

|

|

|

where and are numbers verifying and .

For the same reason, .

We conclude that

|

|

|

-

•

(Cs5)

|

|

|

|

|

|

|

|

|

|

For large enough (), ). Thus

|

|

|

|

|

To conclude, note that

|

|

|

|

|

|

|

|

|

|

Theorem 5.9

(Linear multistable multifractional motion).

Let

, and

be continuously differentiable.

Let be a sequence of arrival times of a Poisson process with unit arrival time,

be a sequence of i.i.d. random variables with distribution on , and be a sequence of i.i.d. random variables with distribution . Assume finally that the three sequences , , and are independent and

define for

|

|

|

(5.20) |

The process is -localisable

at all , with (the well balanced linear fractional stable motion).

We apply Theorem 4.5 with , , and the random field

|

|

|

is the ()-well balanced linear fractional stable motion and it is -localisable with local form [9].

-

•

(Cs1) The family of functions is differentiable for all in a neighbourhood of and almost all in . The derivatives of with respect to read:

|

|

|

-

•

(Cs2) In [9], it is shown that, given , one may choose small enough and numbers with

, and

such that, for all and in and all real :

|

|

|

(5.21) |

where

|

|

|

(5.22) |

for appropriately chosen constants and . The conditions on entail that

and (Cs2) hold.

-

•

(Cs3) is obtained with (5.21) for the same reason as in (Cs2).

-

•

|

|

|

|

|

|

|

|

|

|

Since

|

|

|

(5.23) |

one gets

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fix such that and such that .

|

|

|

|

|

|

|

|

|

|

and thus (Cs4) holds.

-

•

(Cs5) For large enough (),

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Thus

|

|

|

|

|

To conclude, note that

|

|

|

|

|

|

|

|

|

|

Theorem 5.10

(Multistable reverse Ornstein-Uhlenbeck process).

Let , and

be continuously differentiable. Let be a sequence of arrival times of a Poisson process with unit arrival time, be a sequence of i.i.d. random variables with distribution on , and be a sequence of i.i.d. random variables with distribution . Assume finally that the three sequences , , and are independent and

define

|

|

|

(5.24) |

Then is -localisable at any

,

with local form .

We apply Theorem 4.5 with , , and the random field

|

|

|

is the symmetrical -reverse Ornstein-Uhlenbeck process and is -localisable with local form [8].

-

•

(Cs1) The family of functions is differentiable for all in a neighbourhood of and almost all in . The derivatives of with respect to vanish.

-

•

(Cs2)

|

|

|

and

|

|

|

|

|

|

|

|

|

|

thus (Cs2) holds.

-

•

(Cs3) so (Cs3) holds.

-

•

|

|

|

as a consequence

|

|

|

|

|

|

|

|

|

|

-

•

(Cs5)

|

|

|

Fix large enough such that for all , . Then

|

|

|

|

|

|

|

|

|

|

|

|

|