Spectral estimation of the Lévy density in partially observed affine models

Abstract

The problem of estimating the Lévy density of a partially observed multidimensional affine process from low-frequency and mixed-frequency data is considered. The estimation methodology is based on the log-affine representation of the conditional characteristic function of an affine process and local linear smoothing in time. We derive almost sure uniform rates of convergence for the estimated Lévy density both in mixed-frequency and low-frequency setups and prove that these rates are optimal in the minimax sense. Finally, the performance of the estimation algorithms is illustrated in the case of the Bates stochastic volatility model.

1 Introduction

The problem of nonparametric statistical inference for jump processes or more generally for semimartingales models has long history and goes back to the works of Rubin and Tucker (1959) and Basawa and Brockwell (1982). The recent revival of interest in this topic documented, for example, in Figueroa-López (2004), is mainly related to the wide availability of financial and economical time series data and new types of statistical issues that have not been addressed before. For instance, there is now considerable evidence (see, e.g. Cont and Mancini (2007)) that most financial time series contain a continuous martingale component. This is why in a number of recent works the problem of estimating some characteristics of jumps for the general semimartingale models with a nonzero continuous part was studied. In fact, without any further assumptions such kind of statistical inference would not be possible because the behavior of the jump component becomes statistically indistinguishable from the behavior of the diffusion part as the activity of small jumps increases. In the case of Lévy processes the activity of small jumps can be measured by the so-called Blumenthal-Getoor index. The nearer is the Blumenthal-Getoor index to , the more difficult becomes the problem of separating jump and diffusion components and hence the problem of statistical inference on the characteristics of jumps (see, e.g. Neumann and Reiß (2007)). Suppose that the values of a process on a time grid are observed. If is small (high-frequency data), then a large increment indicates that a jump occurred between time and . Based on this insight and the continuous-time observation analogue, inference for various characteristics of jumps of the underlying semimartingale can be conducted. For example, in Aït-Sahalia and Jacod (2008) the problem of statistical inference on the degree of jump activity in the general semimartingale models based on high-frequency data was considered. They proposed an estimation procedure which is able to “see through” the continuous part of the semimartingale and consistently estimate the degree of small jump activity under some restrictions on the structure of the underlying semimartingale. In fact, these restrictions keep the highest degree of activity of small jumps away from , thus allowing for a consistent estimation of the degree of jump activity.

In this paper we focus on a special class of semimartingale models, namely the so-called affine models. Affine Itô-Lévy models are nowadays rather popular in financial and econometric modeling. Due to their analytical tractability on the one hand and their rather rich dynamics and implied volatility patterns, on the other hand, they are particularly useful in the context of option pricing. Many well known models such as Heston and Bates stochastic volatility models fall into the class of affine Itô-Lévy models. Option pricing in these models can be conveniently done via the Fourier method. The literature on affine processes is rather extensive. Let us mention two seminal papers of Duffie, Pan and Singleton (2000) and Duffie, Filipović and Schachermayer (2003), where theoretical analysis of regular affine models was conducted.

In this work we consider the problem of estimating the characteristics of jumps in a class of affine models with a nonzero continuous part, where it is assumed that only first few components of the underlying affine process are observable at low or mixed-frequency. We propose an approach based on the log-affine representation of the conditional characteristic function of an affine process. This representation together with some transformation allows one to consistently estimate the characteristics of the jump component from low-frequency and mixed-frequency data under some prior bound on the highest degree of activity of small jumps. We present uniform convergence rates for the so constructed estimate of the transformed Lévy density which turn out to be optimal in the minimax sense. As the main technical result, that may be of independent interest, we provide exponential inequalities on the probability of large deviations for the kernel type empirical processes in uniform metric for the case of weakly dependent random variables.

The problem of parametric estimation of the characteristics of an affine jump-diffusion process (processes with finite intensity of jumps) from high-frequency time series of the asset has been recently considered in the literature by Singleton (2000) and Bates (2005). In Singleton (2000) the general method of moments (GMM) based on the empirical characteristic function was employed and the asymptotic properties of the corresponding estimator are investigated. Bates (2005) proposed a filtration-based maximum likelihood methodology for estimating the parameters and the realizations of latent affine processes. Since the characteristics of a general affine process are a priori an infinite-dimensional object, any parametric approach is always exposed to the problem of misspecification, especially if there is no inherent economic foundation for the parameters and they are only used to generate different shapes of possible jump distributions. The problem of semi-parametric inference for the characteristics of special type affine processes was studied in the literature as well. In the case of high-frequency observations, the problem of nonparametric inference on the Lévy measure of the time-changed Lévy processes, belonging sometimes to the class of affine processes, has been recently studied in Figueroa-López (2009). In Jongbloed, van der Meulen and van der Vaart (2005) the case of a one-dimensional Lévy driven Ornstein-Uhlenbeck process, affine process with zero diffusion part, was considered. The authors assumed that the corresponding jump component is self-decomposable and proposed a cumulant -estimator to estimate the so-called canonical function of the driving self-decomposable process from low-frequency data. As to the special case of Lévy processes, semi-parametric estimation for pure Lévy models under low-frequency data has recently been studied in Neumann and Reiß (2007). Let us mention that in Neumann and Reiß (2007) the diffusion component is assumed to be known. Thus, all the above works do not encounter the problem of separating diffusion and jump components as the activity of small jumps increases. Furthermore, the challenge of devising nonparametric estimation methods for the Lévy density in general affine models lies in the fact that the structure of the conditional characteristic function does not have such explicit form as in the case of pure Lévy processes and is related to the parameters of the underlying affine process not directly but via a Riccati equation. The last but not the least: the increments of the general affine process are not independent, hence advanced tools from the time series analysis have to be used.

The paper is organized as follows. In Section 2 we introduce the main object of our study, the affine Itô-Lévy processes and formulate the main existence result. In Section 3 the main ideas behind our estimation methodology are sketched and the notations is introduced. The estimation algorithms for the cases of mixed-frequency and low-frequency data are presented in Section 4 and Section 5, respectively. The asymptotic properties of the constructed estimates are studied in Section 6. Section 7 contains some numerical examples. The exponential inequalities for the kernel type empirical processes are given in Section 8. Finally, the proofs of the main results are collected in Section 9.

2 Main setup

Let us fix a probability space and an information filtration . The process is an affine process if it is stochastically continuous, time-homogenous Markov process with the state space , such that the conditional characteristic function of given is an affine function of the initial state :

| (1) |

The affine process is called regular, if the derivatives

exist and are continuous at As was recently shown by Keller-Ressel, Schachermayer and Teichmann (2008), any affine process is, in fact, regular. The following theorem provides the characterization of affine processes and is proved in Duffie, Filipović and Schachermayer (2003).

Theorem 2.1.

If is a regular affine process, then the complex valued functions and satisfy the following (generalized) Riccati equations

| (2) | |||||

| (3) |

where

for and with

for Here and is a vector of measures on satisfying

where here and in the sequel for any

Under some admissibility conditions a regular affine process is a Feller process in the domain (see Duffie, Filipović and Schachermayer, 2003, Section 2), where the function corresponds to the state-independent part of the infinitesimal operator and is related to the state-dependent one. The admissibility conditions imply, in particular, that

| (4) |

and for In the sequel we assume that the above admissibility conditions hold. Moreover, we restrict our analysis to the class of affine processes with state-independent jumps, i.e.,

| (5) |

On the one hand, this assumption reduces the dimensionality of the jump component of . On the other hand, the class of affine models satisfying (5), remains rather large and includes such well known models as Heston, Bates and Barndorff-Nielsen and Shephard stochastic volatility models. In this paper we study the problem of statistical inference based on partially observed affine processes. In particular, we assume that only the first components of the process are observed (as it is usual in the case of stochastic volatility models). As a result, in order to ensure identifiability, we have to assume additionally that i.e., the positive part of the process does not have jumps.

3 Main ideas

Assume that the process is stationary with the stationary distribution Fix some and denote

| (6) |

for any Introduce the function

| (7) |

Let us now investigate the behavior of the function as (“short time asymptotic”) and (“long time asymptotic”).

Short time asymptotic

Long time asymptotic

If the maximal eigenvalue of the matrix is negative, then the affine process is ergodic, possesses a stationary distribution (see Masuda (2007)) and it holds as with

If

| (10) |

then the admissibility condition (4) implies

| (11) |

for some and Therefore

| (12) |

with some and

| (13) |

where for any set

In the sequel we shall assume that the measure is absolutely continuous w.r.t. Lebesgue measure on and have a bounded density. Then has also a density given by

and the admissibility conditions imply that

Hence, the measures and are absolutely continuous w.r.t. Lebesgue measure on as well and possess bounded densities denoted (with some abuse of notations) by and respectively. Functions and satisfy, due to the Riemann-Lebesgue theorem, the following asymptotic relations

The above relations together with (8) and (11) indicate that one can estimate the Fourier transforms of and if some estimates for the functions and are available. In order to estimate using formula (8) we need to perform numerical differentiation of the function in This calls for the “high-frequency” data. On the other hand, in order to estimate the expectation in by a kind of averaging, we need ergodic theorem which usually holds only under low-frequency sampling. It turns out that by mixing low- and high-frequency data one can consistently estimate As to the function it can be estimated from low-frequency data.

Remark 3.2.

In the case of the more general affine processes, i.e., in the case where for some one can use a similar strategy to reconstruct Indeed, in the general case the function takes the form

| (14) |

where each measure is related to in the same way as was related to Therefore, one can reconstruct the Fourier transforms of all measures if one is able to recover function and its derivative in for (at most) linearly independent vectors In principle, the approach presented in the next section allows one to estimate for arbitrary number of vectors

4 Estimation of in the mixed-frequency setup

4.1 Observations

For our theoretical study we adopt the observational model based on the mixed-frequency random sampling. In particular, we assume that a trajectory of a partially observed process containing the pairs

is observable, where are i.i.d. random variables on for some fixed with a common density and . The latter assumption implies that the time horizon of observations tends to infinity as In the sequel (see Assumption (AG) in Section and Remark 6.5) we will additionally assume that the density of the r.v. does not vanish in the vicinity of meaning that the r.v. can, with positive probability, take values that are arbitrary close to This is the reason why we call the above observation’s scheme mixed-frequency setup. Mixing low-frequency and high-frequency data has become rather popular technique in recent years. It has been, for example, used to improve the volatility estimation (see, e.g., Tao, Wang, Yao and Zou (2010)) or to achieve better forecasts in macro-economical models (see, e.g. Andreou, Ghysels and Kourtellos (2010) and references therein). Let us also note that the high-frequency data is usually not equidistant: the observations are more frequent for busy trading days. In such a situation our random sampling scheme may be appropriate. As we will see, the above sampling scheme will also allow us to consistently estimate the function in (8). Indeed, while the high-frequency sampling scheme (small values of ) makes it possible to estimate the derivative of the function in , the low-frequency data allows us to consistently estimate the function by its empirical counterpart. The condition ensures that the subsequent pairs are only weakly dependent and a kind of ergodic theorem can be applied.

4.2 Estimation of

Assume again that the process is stationary with the stationary distribution In this section we shall, for any fixed estimate the quantity

| (15) |

by local polynomial smoothing (local polynomial of degree in and local linear in ) of the empirical characteristic process

Since the process is stationary, (15) is equal to

The latter quantity can be estimated by performing the local polynomial smoothing w.r.t. the first components of the process and averaging w.r.t to the conditional distribution of the remaining coordinate processes This is basically what we do next. Fix some For some , an integer and a function , let be a solution of the following optimization problem

| (16) |

with where the minimization is performed over the set of all polynomials and on of degree Now define the local polynomial estimates for and where is defined in (6), by

respectively. Furthermore, define an estimate for by plugging the estimate into (7):

Let and denote the coefficients of the polynomials and respectively, indexed by the multi-index , i.e., Introduce the vectors and with

Let be the vector of all monomials in of order less than or equal to and the matrices be defined as

| (17) |

Consider now the vector and the matrix

The following proposition holds.

Proposition 4.3.

If the matrix is positive definite, then there exist unique polynomials and on of degree solving (16). Their vectors of coefficients are given by As a result

| (18) |

4.3 Estimation of

Let be a regularizing kernel supported on and let be a sequence of positive numbers tending to Define an estimate for the limit in (8) as

Next, we reconstruct the Lévy density using the regularized Fourier inversion formula

where is another regularizing kernel.

5 Estimation of using low-frequency data

5.1 Observations

We assume that the time series is observed, where is a deterministic sequence of positive numbers with for some

5.2 Estimation of

By Birkhoff ergodic theorem it holds for any

where stands for the c.f. of the first components of under Therefore it is natural to estimate via

5.3 Estimation of

We again first estimate the limit by

Then the transformed density can be reconstructed using the regularized Fourier inversion formula

6 Asymptotic analysis

In this section we study the asymptotic properties of the estimates and

6.1 Assumptions

We need the following assumptions.

- (AX)

-

The sequence is strongly mixing with the mixing coefficients satisfying

for some and

- (AN)

-

The Lévy measure satisfies for some

where here and in the sequel stands for norm.

Let be the density of under For any fixed and consider a matrix

where are matrices with the elements

Note that We make the following assumption about

- (AG)

-

The minimal eigenvalue of the matrix is bounded away from zero, i.e.,

with some

- (AP)

-

The density is uniformly bounded on

- (AK1)

-

Kernel is bounded and is supported on .

- (AK2)

-

The regularizing kernels and are uniformly bounded, are supported on integrate to and satisfy

with some

Discussion

Exponentially strongly mixing holds for a wide class of Itô-Lévy processes. In Masuda (2007) conditions are formulated that ensure that a multidimensional Itô-Lévy process is exponentially -mixing and hence exponentially -mixing.

Example 6.4.

Let be matrix whose eigenvalues have positive real parts, and let be a nontrivial -dimensional Lévy process. Consider a -dimensional Ornstein-Uhlenbeck process given by

The process is obviously an affine process satisfying (5). If the Lévy measure of the process satisfies and for some then is exponentially -mixing (see Masuda (2007), Theorem 2.6).

Suppose now that is an affine process with the characteristics satisfying admissibility conditions, the condition (5) and for some . If the maximal eigenvalue of the matrix is negative, then both sequences and are exponentially -mixing and hence ergodic.

Remark 6.5.

Let us remark on the assumption (AG). If for any the joint density is strictly positive on where is a ball of radius in , then (AG) holds. Suppose, for simplicity, that is supported on for some (otherwise a truncation argument combined with an assumption on the tails of can be used) and consider the kernel

We have for any with

with some positive constant and

Using now the fact that the Lebesgue measure of the set is larger than some positive number for all where depends on and but does not depend on and we get

with some positive by the compactness argument.

6.2 Minimax upper bounds for

First, introduce a class of Lévy densities for which we are going to derive the minimax rates of convergence. For any let stand for a class of Lévy densities satisfying

| (19) |

for some where the function is related to the Lévy density via (9). Here and in the sequel stands for the Fourier transform of a measure .

Remark 6.6.

The first result of this section concerns the asymptotic properties of the estimate constructed in Section 4.2.

Theorem 6.7.

Suppose that the assumption (AX), (AN), (AG), (AP) and (AK1) hold. Let be the local polynomial estimate of degree (in ) for the function where is defined in (6). Furthermore, let be a monotone positive Lipschitz function on such that

| (20) |

Then under the choices and with some

| (21) |

where

| (22) |

and and are some positive constants.

Remark 6.8.

The condition (20) on the decay of the weighting function can not be, in general, weakened. For example, in the case of a one-dimensional Brownian motion with volatility starting at , the simplest affine process, we get

This means that the approximation errors of the estimates and based on local constant smoothing in (), are of order and respectively. So in order to be able to prove the uniform consistency in we have to assume (20). In fact, the rate (22) can be proved to be optimal, provided the function is at least two times differentiable in and all partial derivatives in up to order exist (see Stone (1982) for lower bounds for local polynomial estimates).

Let be a sequence of positive r.v. and be a sequence of positive real numbers. We shall write if there is a constant such that In the case we shall write Theorem 6.7 implies the following result on the strong uniform rates of convergence for the estimate

6.3 Minimax upper bounds for

For any let stand for a class of Lévy densities satisfying

| (23) |

for some where the function is related to the Lévy density via (9). We need the following assumption concerning the asymptotic behavior of the sequence .

- (AH)

-

The sequence satisfies

for some positive number where

Theorem 6.10.

Suppose that the assumptions (AX), (AN), (AP), (AK1), (AK2) and (AH) hold. Let be the estimate for the transformed Lévy density defined in Section 5 and let be a monotone positive Lipschitz function on satisfying

| (24) |

If for some then

where

Corollary 6.11.

Consider a class of affine models such that and

| (25) |

with some constant Then under the choice

it holds

Remark 6.12.

The condition (25) holds if, for example, with

6.4 Lower risk bounds

The rates of Theorem 6.10 can not be improved in general as the following theorem states

Proposition 6.13.

The following minimax lower risk bounds hold

where is any positive number, is any estimator of based on observations and the supremum is taken over all affine models from the class

7 Numerical example

Let us consider a class of stochastic volatility models of the type

| (26) | |||||

where and are two independent Brownian motions, are positive constants and is a pure-jump Lévy process with Lévy density This is a special type of the model introduced in Bates (2005) that satisfies our assumptions. In our numerical example we take to be -stable Lévy process with stability index , i.e.,

for some constant For the sake of simplicity we consider a fixed design and simulate a set of i.i.d pairs

| (27) |

with some fixed , where

Our aim is to reconstruct using the sample (27). First, compute

and

Remark 7.14.

In the case of mixed-frequency data observations are usually available for different frequency scales and the choice of an appropriate frequency for estimation procedure should be done depending on , the number of points available for the given frequency scale. If is too small then the variance of explodes. On the other hand, if is too large than the approximation error of becomes large.

Next define a parametric family of functions

and find by solving the following minimization problem

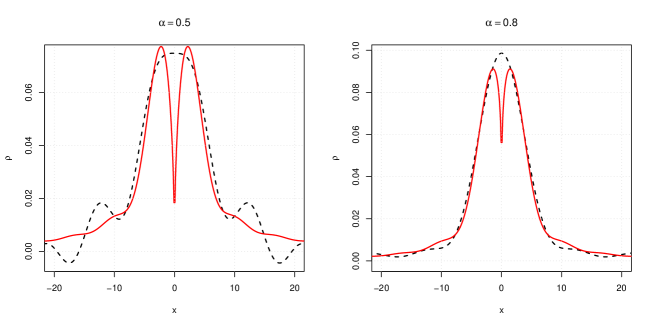

where is a regularization parameter. In fact, this approach for choosing employs additional information about smoothness of and turns out to be rather efficient in practice. In Figure 1 typical results of estimation based on samples (27) with are shown for two specifications of the process

As can be seen the overall quality of estimation is good taking into account severely ill-posedness of the underlying estimation problem. However, the behavior of the transformed Lévy density at zero has not been captured by the estimation method. In order to correct at we separately estimate the stability index using a modification of the spectral algorithm proposed in Belomestny (2009) for Lévy processes. Motivated by relations (2) and (3), we define for any

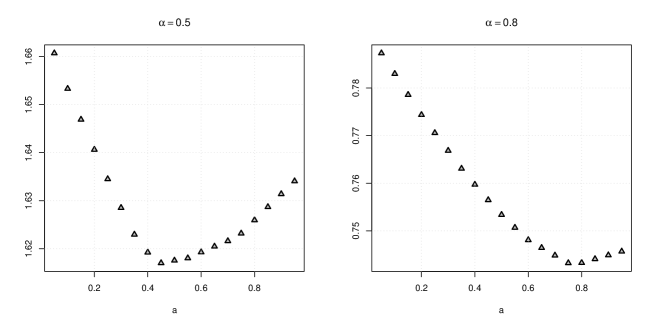

| (28) |

and estimate via In Figure 2 functions based on the same samples as in Figure 1 are shown.

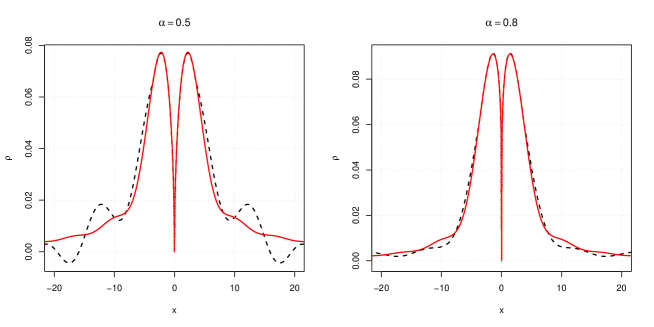

The resulting estimates for are and respectively. Now we correct the estimate by setting

where for any the constant is chosen in such a way that function is continuous. Finally, we find small enough which minimizes the integral . Here again the smoothness of is used. A corrected estimate is shown in Figure 3.

8 Exponential inequalities for dependent sequences

The following theorem can be found in Merlevède, Peligrad and Rio (2009).

Theorem 8.15.

Let be a strongly mixing sequence of centered real-valued random variables on the probability space with the mixing coefficients satisfying

| (29) |

Assume that a.s., then there is a positive constant depending on and such that

for all and where

Corollary 8.16.

Denote

with arbitrary small and suppose that all are finite. Then

for some constant provided (29) holds. Consequently the following inequality holds

Proof.

Due to the Rio inequality

where for any random variable we denote by the quantile function of Define

The Markov inequality implies for small enough

and therefore

Hence

and

with some constant depending on ∎

8.1 Bounds on large deviations probabilities for weighted sup norms

Let be a sequence of random vectors in and let be a sequence of complex-valued functions defined on for some natural number Define

Proposition 8.17.

Suppose that the following assumptions hold:

- (AZ1)

-

The sequence is strictly stationary and is -mixing with the mixing coefficients satisfying

for some and

- (AZ2)

-

It holds for some

- (AG1)

-

Each function is Lipschitz in with (at most) linearly growing (in ) Lipschitz constant, i.e., for any

where are two non-negative real numbers not depending on and the sequence does not depend on

- (AG2)

-

There are two sequences and such that

and the following asymptotic relations are fulfilled

as

Let be Lipschitz continuous, positive, monotone decreasing on function such that

| (30) |

Then there is and , such that the inequality

| (31) |

holds for any some positive constant depending on and arbitrary small

Proof.

Define for

and introduce the process

Consider the sequence and cover each cube with disjoint small cubes , the length of each cube being equal to Let be the centers of these cubes. We have for any natural

Hence

| (32) |

It holds for any

| (33) | |||||

where is the Lipschitz constant of By the Markov inequality

for any Using the moment inequality of Yokoyama (see Yokoyama (1980)), we get

where is some constant depending on and from the assumption (AZ1). Hence

| (34) |

with . Setting

and combining (33) with the inequality (34), we obtain

| (35) |

with some constant depending neither on nor . Turn now to the first term on the right-hand side of (32). If then it follows from Theorem 8.15 and Corollary 8.16

with some constants , and depending only on the characteristics of the process and Indeed, due to (AG2) it holds

with some constant Hence

Taking with some , we get

with some constant Fix such that and compute

If we derive

Taking for large enough , we get (31).

∎

9 Proofs

9.1 Proof of Theorem 6.7

The smallest eigenvalue of the matrix satisfies

| (36) | |||||

By the assumption (AG)

with some For any and any multi-indices , such that , define

We have ,

and

where and are two positive constants. According to Proposition 8.17, we have for any

| (37) |

with some positive constants and . Combining (36) with (37), we get

where is the number of elements in the matrix Introduce the matrices with elements

Set

Denote by the th column of and define

Since , we get . Thus, we can write

where and

where

and

So, on the set we get

Denote

It holds

Note that and

with some positive constants , , and not depending on . Proposition 8.17 implies that

and

for some positive constants and not depending on and Due to Lemma 10.19 and Assumption (AN), the function is at least two times differentiable in Hence

for some constant Using Lemma 10.19, we get

9.2 Proof of Theorem 6.9

9.3 Proof of Theorem 6.10

Fix some and consider the event

By the assumption (AH), it holds on

and hence

with

for some constant and all satisfying On the other hand, Proposition 8.17 (take ) implies

for some and provided is large enough. Therefore it holds on

for some constant and all satisfying The rest of the proof is similar to the proof of Theorem 6.9.

9.4 Proof of Proposition 6.13

In order to prove minimax lower bounds we apply general results from Tsybakov (2008). Let be a semi-parametric class of models. Consider a family of probability measures, indexed by . For any let be a semi-distance between two models and

Lemma 9.18.

Suppose that contains two elements and such that for some and where

for any two measures and . Then

where is constant depending on and infimum is taken over all estimates of based on observations under .

Turn now to the construction of models and from the class . Let us consider a symmetric stable Lévy model with a nonzero diffusion part ()

For any satisfying and define

with

Then is the characteristic function of some Lévy process and

where . Indeed, is continuous, non-positive, symmetric function which is convex on for large enough . According to the well known Pólya criteria (see e.g. Ushakov (1999)), the function is the c. f. of some absolutely continuous distribution for any . In particular, for any natural the function is the c. f. of some absolutely continuous distribution. Hence, is the c.f. of some infinitely divisible distribution. Define now two affine (in fact, Lévy) models and corresponding to the c.f. characteristic exponents and respectively. Let and be the corresponding Lévy measures. It holds

where and are densities corresponding to c.f. and respectively. Using the asymptotic inequality

and the fact that the density of the stable law does not vanish on any compact set in , we derive

for large enough and some constants . Parseval’s identity implies

The choice with some yields

for large enough On the other hand,

with

Using the identity

| (40) |

which holds for any and , we get

for any Denote

then the Fourier inversion formula implies

Asymptotic expansion (40) shows that there is a constant depending on such that

Hence, taking , we conclude that both models and are in the class .

10 Appendix

10.1 Regularity properties of affine processes

The next lemma provides bounds on the growth of the derivatives of the conditional characteristic function of an affine process.

Lemma 10.19.

If for some natural the Lévy measure satisfies

| (42) |

then functions and from the representation (1) are in as functions of . Moreover, for any fixed and the following estimates hold

| (43) |

where is a multi index and is a positive constant depending on and .

Proof.

The existence of derivatives in up to order was proved in Duffie, Filipović and Schachermayer (2003) (Lemma 6.5). As was also shown in Duffie, Filipović and Schachermayer (2003) (Section 7), for any fixed and , the function is a c.f. of some infinitely divisible distribution, implying that

where and is non-negative Borel measure on It remains to note that and depend linearly on and are smooth in provided the condition (42) holds. ∎

References

- Aït-Sahalia and Jacod (2009) Aït-Sahalia, Y. and Jacod, J. (2006). Volatility estimators for discretely sampled Lévy processes. Annals of Statistics, 37, 184–222.

- Aït-Sahalia and Jacod (2008) Aït-Sahalia, Y. and Jacod, J. (2009). Estimating the degree of activity of jumps in high frequency financial data. Annals of Statistics, 37(5A), 2202–2244.

- Andreou, Ghysels and Kourtellos (2010) Andreou, E., Ghysels, E. and Kourtellos, A. (2010). Forecasting with mixed-frequency data. Oxford Handbook on Economic Forecasting edited by Michael P. Clements and David F. Hendry.

- Belomestny (2009) Belomestny, D. (2009). Spectral estimation of the fractional order of a Lévy process. Annals of Statistics, 38(1), 317–351.

- Bates (2005) Bates, D. (2000). Post-’87 crash fears in the S&P 500 futures option market. Journal of Econometrics, 94, 181–238.

- Bates (2005) Bates, D. (2005). Maximum Likelihood Estimation of Latent Affine Processes. Review of Financial Studies, 909–965.

- Basawa and Brockwell (1982) Basawa, I. V. and Brockwell, P. J. (1982). Nonparametric estimation for nondecreasing Lévy processes, J. Roy. Statist. Soc. Ser. B, 44, 262–269.

- Cont and Mancini (2007) Cont, R., and Mancini C. (2004). Nonparametric Tests for Analyzing the Fine Structure of Price Fluctuations, SSRN Paper.

- Duffie, Pan and Singleton (2000) Duffie, D., Pan, J. and Singleton, K. (2000). Transform analysis and asset pricing for affine jump diffusions. Econometrica, 68, 1343–1376.

- Duffie, Filipović and Schachermayer (2003) Duffie, D., Filipović, D. and Schachermayer, W. (2003). Affine processes and applications in finance. Annals of Applied Prob., 13, 984–1053.

- Figueroa-López (2004) Figueroa-López, J.E. (2004). Nonparametric estimation of Lévy processes with a view towards mathematical finance. PhD thesis, Georgia Institute of Technology, http://etd.gatech.edu. No. etd-04072004-122020.

- Figueroa-López (2009) Figueroa-Lopez, J.E. (2009). Nonparametric estimation of time-changed Levy models under high-frequency data. To appear Advances in Applied Probability.

- Glasserman and Kim (2007) Glasserman, P. and Kyoung-kuk Kim (2007). Moment Explosions and Stationary Distributions in Affine Diffusion Models, to appear in Mathematical Finance.

- Jiang and Oomen (2007) Jiang, G. and Oomen, R. (2007). Estimating Latent variables and jump diffusion models using high-frequency data. Journal of Financial Econometrics, 5, 1–30.

- Jongbloed, van der Meulen and van der Vaart (2005) Jongbloed, G., van der Meulen, F.H. and van der Vaart, A.W. (2005). Nonparametric inference for Lévy-driven Ornstein-Uhlenbeck processes. Bernoulli, 11(5), 759–791.

- Keller-Ressel, Schachermayer and Teichmann (2008) Keller-Ressel, M., Schachermayer, W. and Teichmann, J. (2008). Affine processes are regular , to appear in Probabilty Theory and Related Fields.

- Masuda (2007) Masuda, H. (2007). Ergodicity and exponential -mixing bounds for multidimensional diffusions with jumps, Stochastic Process. Appl., 117(1), 35-56.

- Merlevède, Peligrad and Rio (2009) Merlevéde, F., Peligrad, M. and Rio, E. (2009). Bernstein inequality and moderate deviation under strong mixing conditions. Working paper.

- Neumann and Reiß (2007) Neumann, M. and Reiß, M. (2007). Nonparametric estimation for Lévy processes from low-frequency observations. Bernoulli, 15(1), 223-248.

- Rubin and Tucker (1959) Rubin, H. and Tucker, H.G. (1959). Estimating the parameters of a differential process, Ann. Math. Statist., 30, 641-658.

- Sato (1999) Sato, K. (1999). Lévy Processes and Infinitely Divisible Distributions. Cambridge University Press.

- Singleton (2000) Singleton, K. (2001). Estimation of Affine Asset Pricing Models Using the Empirical Characteristic Function. Journal of Econometrics, 10, 111–141.

- Stone (1982) Stone, C.J. (1982). Optimal global rates of convergence for nonparametric regression. Annals of Statistics, 10, 1040–1053.

- Tao, Wang, Yao and Zou (2010) Tao, M., Wang, Y., Yao, Q. and Zou, J. (2010). Large volatility matrix inference via combining low-frequency and high-frequency approaches. Technical report.

- Tsybakov (2008) Tsybakov, A. (2008). Introduction to Nonparametric Estimation, Springer Series in Statistics, Springer.

- Ushakov (1999) Ushakov, N. (1999). Selected topics in characteristic functions. Modern Probability and Statistics. VSP, Utrecht.

- Yokoyama (1980) Yokoyama, R. (1980). Moment bounds for stationary mixing sequences. Z. Wahrsch. Verw. Gebiete., 52, 45–57.