Pricing Bermudan options using nonparametric regression: optimal rates of convergence for lower estimates

Abstract

The problem of pricing Bermudan options using Monte Carlo and a nonparametric regression is considered. We derive optimal non-asymptotic bounds for a lower biased estimate based on the suboptimal stopping rule constructed using some estimates of continuation values. These estimates may be of different nature, they may be local or global, with the only requirement being that the deviations of these estimates from the true continuation values can be uniformly bounded in probability. As an illustration, we discuss a class of local polynomial estimates which, under some regularity conditions, yield continuation values estimates possessing this property.

Keywords: Bermudan options, Nonparametric regression, Boundary condition, Suboptimal stopping rule

1 Introduction

An American option grants the holder the right to select the time at which to exercise the option, and in this differs from a European option which may be exercised only at a fixed date. A general class of American option pricing problems can be formulated through an Markov process defined on a filtered probability space . It is assumed that is adapted to in the sense that each is measurable. Recall that each is a -algebra of subsets of such that for . We interpret as all relevant financial information available up to time . We restrict attention to options admitting a finite set of exercise opportunities , sometimes called Bermudan options. If exercised at time , the option pays , for some known functions mapping into . Let denote the set of stopping times taking values in . A standard result in the theory of contingent claims states that the equilibrium price of the American option at time in state given that the option was not exercised prior to is its value under an optimal exercise policy:

Pricing an American option thus reduces to solving an optimal stopping problem. Solving this optimal stopping problem and pricing an American option are straightforward in low dimensions. However, many problems arising in practice (see e.g. Glasserman (2004)) have high dimensions, and these applications have motivated the development of Monte Carlo methods for pricing American option. Pricing American style derivatives with Monte Carlo is a challenging task because the determination of optimal exercise strategies requires a backwards dynamic programming algorithm that appears to be incompatible with the forward nature of Monte Carlo simulation. Much research was focused on the development of fast methods to compute approximations to the optimal exercise policy. Notable examples include the functional optimization approach in Andersen (2000), mesh method of Broadie and Glasserman (1997), the regression-based approaches of Carriere (1996), Longstaff and Schwartz (2001), Tsitsiklis and Van Roy (1999) and Egloff (2005). A common feature of all above mentioned algorithms is that they deliver estimates for the so called continuation values:

| (1.1) |

An estimate for , the price of the option at time can then be defined as

This estimate basically inherits all properties of . In particular, it is usually impossible to determine the sign of the bias of since the bias of may change its sign. One way to get a lower bound (low biased estimate) for is to construct a (generally suboptimal) stopping rule

with by definition. Simulating a new independent set of trajectories and averaging the pay-offs stopped according to on these trajectories gives us a lower bound for . As was observed by practitioners, the so constructed estimate has rather stable behavior with respect to the estimates of continuation values , that is even rather poor estimates of continuation values may lead to a good estimate The aim of this paper is to find a theoretical explanation of this observation and to investigate the properties of . In particular, we derive optimal non-asymptotic bounds for the bias assuming some uniform probabilistic bounds for . It is shown that the bounds for are usually much tighter than ones for implying a better quality of as compared to the quality of constructed using one and the same set of estimates for continuation values. As an example, we consider the class of local polynomial estimators for continuation values and derive explicit convergence rates for in this case.

The issues of convergence for regression algorithms have been already studied in several papers. Clément, Lamberton and Protter (2002) were first who proved the convergence of the Longstaff-Schwartz algorithm. Glasserman and Yu (2005) have shown that the number of Monte Carlo paths has to be in general exponential in the number of basis functions used for regression in order to ensure convergence. Recently, Egloff, Kohler and Todorovic (2007) have derived the rates of convergence for continuation values estimates obtained by the so called dynamic look-ahead algorithm (see Egloff (2004)) that “interpolates” between Longstaff-Schwartz and Tsitsiklis-Roy algorithms. As was shown in these papers the convergence rates for coincide with the rates of and are determined by the smoothness properties of the true continuation values . It turns out that the convergence rates for depend not only on the smoothness of continuation values (as opposite to ), but also on the behavior of the underlying process near the exercise boundary. Interestingly enough, there are some cases where these rates become almost independent either of the smoothness properties of or of the dimension of and the bias of decreases exponentially in the number of Monte Carlo paths used to construct .

The paper is organized as follows. In Section 2.1 we introduce and discuss the so called boundary assumption which describes the behavior of the underlying process near the exercise boundary and heavily influences the properties of . In Section 2.2 we derive non-asymptotic bounds for the bias and prove that these bounds are optimal in the minimax sense. In Section 2.3 we consider the class of local polynomial estimates and propose a sequential algorithm based on the dynamic programming principle to estimate all continuation values. Finally, under some regularity assumptions, we derive exponential bounds for the corresponding continuation values estimates and consequently the bounds for the bias .

2 Main results

2.1 Boundary assumption

For the considered Bermudan option let us introduce a continuation region and an exercise (stopping) region :

| (2.2) | |||||

Furthermore, let us assume that there exist constants , and such that the inequality

| (2.3) |

holds for all , where is the conditional distribution of given . Assumption (2.3) provides a useful characterization of the behavior of the continuation values and payoffs near the exercise boundary . Although this assumption seems quite natural to look at, we make in this paper, to the best of our knowledge, a first attempt to investigate its influence on the convergence rates of lower bounds based on suboptimal stopping rules. We note that a similar condition, although much simpler, appears in the context of statistical classification problem (see, e.g. Mammen and Tsybakov (1999) and Audibert and Tsybakov (2007)).

In the situation when all functions are smooth and have non-vanishing derivatives in the vicinity of the exercise boundary, we have . Other values of are possible as well. We illustrate this by two simple examples.

Example 1

Fix some and consider a two period () Bermudan power put option with the payoffs

| (2.4) |

Denote by the length of the exercise period, i.e. If the process follows the Black-Scholes model with volatility and zero interest rate, then one can show that

with being the cumulative distribution function of the standard normal distribution,

and As can be easily seen, the function satisfies for and for all if . Hence

Taking different in the definition of the payoffs (2.4), we get (2.3) satisfied for ranging from to .

In fact, even the extreme case “” may take place as shown in the next example.

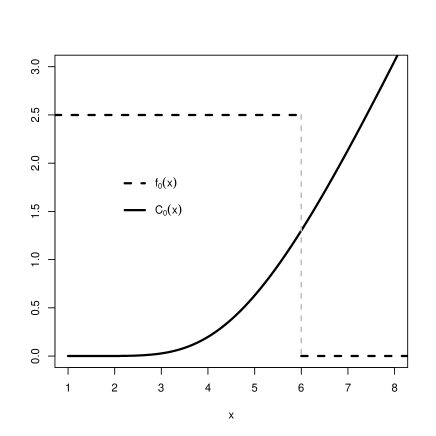

Example 2

Let us consider again a two period Bermudan option such that the corresponding continuation value is positive and monotone increasing function of on any compact set in . Fix some and choose satisfying . Define the payoff function in the following way

So, has a “digital” structure. Figure 1 shows the plots of and in the case where follows the Black-Scholes model and . It is easy to see that

On the other hand

So, both continuation and exercise regions are not trivial in this case.

The last example is of particular interest because as will be shown in the next sections the bias of decreases in this case exponentially in the number of Monte Carlo paths used to estimate the continuation values, the lower bound was constructed from.

2.2 Non-asymptotic bounds for

Let be some estimates of continuation values obtained using paths of the underlying process starting from at time . We may think of as being a vector process on the product probability space with -algebra and the product measure defined on via

with . Thus, each is measurable with respect to . The following proposition provides non-asymptotic bounds for the bias given uniform probabilistic bounds for .

Proposition 2.1.

Suppose that there exist constants and a positive sequence such that for any it holds

| (2.5) |

for almost all with respect to , the conditional distribution of given , . Define

| (2.6) |

with

| (2.7) |

If the boundary condition (2.3) is fulfilled, then

with some constant depending only on , and .

The above convergence rates can not be in general improved as shown in the next theorem.

Proposition 2.2.

Let . Fix a pair of non-zero payoff functions such that and on Let be a class of pricing measures such that the boundary condition (2.3) is fulfilled with some . For any positive sequence satisfying

there exist a subset of and a constant such that for any , any stopping rule and any set of estimates measurable w.r.t. , we have for some and

for almost all w.r.t. any and

Finally, we discuss the case when “”, meaning that there exists such that

| (2.8) |

for This is very favorable situation for the pricing of the corresponding Bermudan option. It turns out that if the continuation values estimates satisfy a kind of exponential inequality and (2.8) holds, then the bias of converges to zero exponentially fast in .

Proposition 2.3.

Suppose that for any there exist constants possibly depending on and a sequence of positive numbers not depending on such that

| (2.9) |

for almost all with respect to , . Assume also that there exists a constant such that

| (2.10) |

If the condition (2.8) is fulfilled with some , then

with some constant and depending only on , and .

Discussion

Let us make a few remarks on the results of this section. First, Proposition 2.1 implies that the convergence rates of , a Monte Carlo estimate for , are always faster than the convergence rates of provided that . Indeed, while the convergence rates of are of order , the bias of converges to zero as fast as As to the variance of , it can be made arbitrary small by averaging over a large number of sets, each consisting of trajectories, and by taking a large number of new independent Monte Carlo paths used to average the payoffs stopped according to

Second, if the condition (2.8) holds true, then the bias of decreases exponentially in , indicating that even very unprecise estimates of continuation values would lead to the estimate of acceptable quality.

Finally, let us stress that the results obtained in this section are quite general and do not depend on the particular form of the estimates , only the inequality (2.5) being crucial for the results to hold. This inequality holds for various types of estimators. These may be global least squares estimators, neural networks (see Kohler, Krzyzak and Todorovic (2009)) or local polynomial estimators. The latter type of estimators has not yet been well investigated (see, however, Belomestny et al. (2006) for some empirical results) in the context of pricing Bermudan option and we are going to fill this gap. In the next sections we will show that if all continuation values belong to the Hölder class and the conditional law of satisfies some regularity assumptions, then local polynomial estimates of continuation values satisfy inequality (2.5) with for some .

Remark 2.4.

In the case of projection estimates for continuation values, some nice bounds were recently derived in Van Roy (2009). Let be an ergodic Markov chain with the invariant distribution and then provided that is distributed according to . Furthermore, suppose that an estimate for the continuation value is available and satisfies a projected Bellman equation

| (2.11) |

where is the corresponding projection operator. Define

with

then as shown in Van Roy (2009)

| (2.12) |

with some absolute constant depending on only. The inequality (2.12) indicates that the quantity

might be much smaller than and hence qualitatively supports the same sentiment as in our paper.

2.3 Local polynomial estimation

We first introduce some notations related to local polynomial estimation. Fix some such that and suppose that we want to estimate a regression function

with . Consider trajectories of the process

all starting from , i.e. . For some , , an integer and a function , denote by a polynomial on of degree (maximal order of the multi-index is less than or equal to ) which minimizes

| (2.13) |

where . The local polynomial estimator of order for the value of the regression function at point is defined as if is the unique minimizer of (2.13) and otherwise. The value is called the bandwidth and the function is called the kernel of the local polynomial estimator.

Let denote the coefficients of indexed by the multi-index , . Introduce the vectors and with

Let be the vector of all monomials of order less than or equal to and the matrix be defined as

| (2.14) |

The following result is straightforward.

Proposition 2.5.

If the matrix is positive definite, then there exists a unique polynomial on of degree minimizing (2.13). Its vector of coefficients is given by and the corresponding local polynomial regression function estimator has the form

| (2.15) |

Remark 2.6.

From the inspection of (2.15) it becomes clear that any local polynomial estimator can be represented as a weighted average of the “observations” with a special weights structure. Hence, local polynomial estimators belong to the class of mesh estimators introduced by Broadie and Glasserman (1997) (see also Glasserman, 2004, Ch. 8). Our results will show that this particular type of mesh estimators has nice convergence properties in the class of smooth continuation values.

2.4 Estimation algorithm for the continuation values

According to the dynamic programming principle, the optimal continuation values (1.1) satisfy the following backward recursion

with . Consider paths of the process , all starting from and define estimates recursively in the following way. First, we put . Further, if an estimate of is already constructed we define as the local polynomial estimate of the function

| (2.16) |

based on the sample

Note that all are measurable random variables because the expectation in (2.16) is taken with respect to a new -algebra which is independent of (one can start with the enlarged product -algebra and take expectation in (2.16) w.r.t. the first coordinate). The main problem arising by the convergence analysis of the estimate is that all errors coming from the previous estimates have to be taken into account. This problem has been already encountered by Clément, Lamberton and Protter (2002) who investigated the convergence of the Longstaff-Schwartz algorithm.

2.5 Rates of convergence for

Let . Denote by the maximal integer that is strictly less than . For any and any times continuously differentiable real-valued function on , we denote by its Taylor polynomial of degree at point

where is a multi-index, and denotes the differential operator . Let . The class of -Hölder smooth functions, denoted by , is defined as the set of functions that are times continuously differentiable and satisfy, for any , the inequality

Let us make two assumptions on the process

- (AX0)

-

There exists a bounded set such that and for all and satisfying

- (AX1)

-

All transitional densities of the process are uniformly bounded on and belong to the Hölder class as functions of , i.e. there exists with and a constant such that the inequality

holds for all and

Consider a matrix valued function with elements

for any

- (AX2)

-

We assume that the minimal eigenvalue of satisfies

with some and

Moreover, we shall assume that the kernel fulfils the following conditions

- (AK1)

-

integrates to on and

- (AK2)

-

is in the linear span (the set of finite linear combinations) of functions satisfying the following property: the subgraph of can be represented as a finite number of Boolean operations among the sets of the form , where is a polynomial on and is an arbitrary real function.

Discussion

The assumption (AX0) may seem rather restrictive. In fact, as mentioned in Egloff, Kohler and Todorovic (2007), one can always use a kind of “killing” procedure to localize process to a ball in around of radius . Indeed, one can replace process with the process killed at first exit time from . This new process is again a Markov process and is connected to the original process via the identity

that holds for any integrable with and . This implies that

| (2.17) |

with . The r.h.s of (2.17) can be made arbitrary small by taking large values of (the exact convergence rates depend, of course, on the properties of the process ).

Instead of “killing” the process upon leaving one can reflect it on the boundary of As can be seen a new reflected process satisfies (2.17) as well.

Example

Let process be a -dimensional diffusion process satisfying

Denote by the transition density of the process . Assume that a drift coefficient and a diffusion coefficient are regular enough and satisfies the so called uniform ellipticity condition on compacts, i. e. for each compact set

- (AD1)

-

and for some natural

- (AD2)

-

there is such that for any it holds

Then (see e.g. Friedman (1964)) for any fixed , is a function in . Moreover, as shown in Kim and Song (2007) (see also Bass (1997)) under assumptions (AD1) and (AD2) there exist positive constants such that

for all where

Let us check now assumption (AX2) in the case when . We have for any fixed and with

with some positive constant depending on and , and Introduce

Since we get

Using now the fact that the Lebesgue measure of the set is larger than some positive number for all where depends on and but does not depend on we get

by the compactness argument. Thus, assumption (AX2) is fulfilled with

Let us now reflect the diffusion process instead of “killing” it by defining a reflected process which satisfies a reflected stochastic differential equation in , with oblique reflection at the boundary of in the conormal direction, i.e.

where is the inward normal vector on the boundary of and is a local time process which increases only on i.e. Denote by a transition density of . It satisfies a parabolic partial differential equation with Neumann boundary conditions. Under (AD1) it belongs to (see Sato and Ueto (1965)) for any fixed Moreover, using a strong version of the maximum principle (see, e.g. Friedman, 1964, Theorem 1 in Chapter 2) one can show that under assumption (AD2) the transition density is strictly positive on . Similar calculations as before show that in this case

and hence assumption (AX2) holds with

Remark 2.7.

It can be shown that (AK2) is fulfilled if for some polynomial and a bounded real function of bounded variation. Obviously, the standard Gaussian kernel falls into this category. Another example is the case where is a pyramid or .

In the sequel we will consider a truncated version of the local polynomial estimator which is defined as follows. If the smallest eigenvalue of the matrix defined in (2.14) is greater than we set to be equal to the projection of on the interval with ( is finite due to (AX0) and (AX1)). Otherwise, we put . The following propositions provide exponential bounds for the truncated estimator .

Proposition 2.8.

Let condition (AX0)-(AX2),(AK1) and (AK2) be satisfied and let be the continuation values estimates constructed as described in Section 2.4 using truncated local polynomial estimators of degree . Then there exist positive constants , and such that for any satisfying and any with some it holds

for . As a consequence, we get with and any

Proposition 2.9.

Let condition (AX0)-(AX2),(AK1) and (AK2) be satisfied, then for any there exist positive constants and such that

for

Remark 2.10.

Theorem 2.11.

Let conditions (AX0)-(AX2), (AK1) and (AK2) be satisfied. Define

with

where are continuation values estimates constructed using truncated local polynomial estimators of degree . If the boundary condition (2.3) is fulfilled for some , then

with some constant . On the other hand, if the condition (2.8) is satisfied with some , then the bias of decreases exponentially in , i.e. there exist positive constants and , such that

Discussion

As we can see, the rates of convergence for are of order

which can be proved to be optimal under assumption (AX2), up to a logarithmic factor, for the class of Hölder smooth continuation values . On the other hand, the rates of convergence for are of order

and are always faster than ones of provided that . The most interesting behavior of the lower bound can be observed if the condition (2.8) is fulfilled. In this case the bias of becomes as small as . This means that even in the class of continuation values with an arbitrary low (but positive) Hölder smoothness (e.g. in the class of non-differentiable continuation values) and therefore with an arbitrary slow convergence rates of the estimates the bias of the lower bound converges exponentially fast to zero.

3 Numerical example: Bermudan max call

This is a benchmark example studied in Broadie and Glasserman (1997) and Glasserman (2004) among others. Specifically, the model with identically distributed assets is considered, where each underlying has dividend yield . The risk-neutral dynamic of assets is given by

where , are independent one-dimensional Brownian motions and are constants. At any time the holder of the option may exercise it and receive the payoff

We take , , , , and , with as in Glasserman (2004, Chapter 8). First, we estimate all continuation values using the dynamic programming algorithm and the so called Nadaraya-Watson regression estimator

| (3.18) |

with Here is a kernel, is a bandwidth and is a set of paths of the process , all starting from the point at . As can be easily seen the estimator (3.18) is a local polynomial estimator of degree . Upon estimating , we define a first estimate for the price of the option at time as

Next, using the previously constructed estimates of continuation values, we pathwise compute a stopping policy via

where is a new independent set of trajectories of the process , all starting from at . The stopping policy yields a lower bound

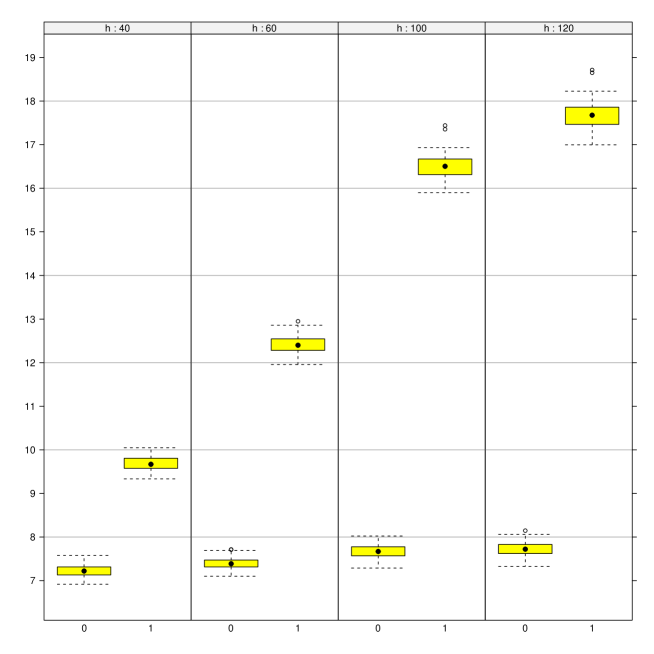

In Figure 2 we show the boxplots of and based on sets of trajectories each of the size () for different values of the bandwidth , where the triangle kernel is used to construct (3.18). The true value of the option (computed using a two-dimensional binomial lattice) is in this case. Several observations can be made by an examination of Figure 2. First, while the bias of is always smaller then the bias of , the largest difference takes place for large . This can be explained by the fact that for large more observations with lying far away from the given point become involved in the construction of . This has a consequence of increasing the bias of the estimate (3.18) and quickly deteriorates with increasing . The most interesting phenomenon is, however, the behavior of which turns out to be quite stable with respect to . So, in the case of rather poor estimates of continuation values (when is increases) looks very reasonable and even becomes closer to the true price.

We stress that the aim of this example is not to show the strength of the local polynomial estimation algorithms (although the performance of for is quite comparable to the performance of a linear regression algorithm reported in Glasserman (2004)) but rather to illustrate the main message of this paper, namely the message about the efficiency of as compared to the estimates based on the direct use of continuation values estimates.

4 Conclusion

In this paper we derive optimal rates of convergence for low biased estimates for the price of a Bermudan option based on suboptimal exercise policies obtained from some estimates of the optimal continuation values. We have shown that these rates are usually much faster than the convergence rates of the corresponding continuation values estimates. This may explain the efficiency of these lower bounds observed in practice. Moreover, it turns out that there are some cases where the expected values of the lower bounds based on suboptimal stopping rules achieve very fast convergence rates which are exponential in the number of paths used to estimate the corresponding continuation values.

5 Proofs

5.1 Proof of Proposition 2.1

Define

and

The so called Snell envelope process is related to via

The following lemma provides a useful inequality which will be repeatedly used in our analysis.

Lemma 5.1.

For any , it holds with probability one

| (5.19) |

Proof.

We shall use induction to prove (5.19). For we have

| (5.20) |

since events and are measurable w.r.t. . Thus, (5.19) holds with . Suppose that (5.19) holds with . Let us prove it for . Consider a decomposition

with

Since

and

we get with probability one

Our induction assumption implies now that

and hence (5.19) holds for . ∎

5.2 Proof of Proposition 2.2

We have

| (5.21) |

For an integer consider a regular grid on defined as

Let be the closest point to among points in . Consider the partition of canonically defined using the grid ( and belong to the same subset if and only if ). Fix an integer . For any , define and , so that form a partition of . Denote by the ball with the center in and radius .

Define a hypercube of probability distributions of the r.v. valued in as follows. For any the marginal distribution of (given ) does not depend on and has a bounded density w.r.t. the Lebesgue measure on such that and

for some . In order to ensure that the density remains bounded we assume that .

The distribution of given is determined by the probability which is equal to . Define

and on , where , with some constant and with being a non-increasing infinitely differentiable function such that on and on . Furthermore, there exist two real numbers such that Taking small enough, we can then ensure that on . Obviously, it holds for . As to the boundary assumption (2.3), we have

and (2.3) holds provided that . Let be a stopping time measurable w.r.t. , then the identity (5.21) leads to

with . By conditioning on we get

Using now a well known Birgé’s or Huber’s lemma (see, e.g. Devroye, Györfi and Lugosi, 1996, p. 243), we get

where and is a Kullback-Leibler distance between two measures and . Since for any two measures and from with it holds

for small enough , and , we get

provided that for some and where is a positive constant depending on and Using similar arguments, we derive

for almost w.r.t. , some and any estimator measurable w.r.t. .

5.3 Proof of Proposition 2.3

Using the arguments similar to ones in the proof of Proposition 2.1, we get

| (5.22) |

with defined as in the proof of Proposition 2.1. The first summand on the right-hand side of (5.22) is equal to zero due to (2.8). Hence, Cauchy-Schwarz and Minkowski inequalities imply

Now the application of (2.9) finishes the proof.

5.4 Proof of Proposition 2.8

Denote

and

for . Using the elementary inequality which holds for any real numbers , and , we get

and hence

Note that we take expectation in (5.4) with respect to a new -algebra which is independent of and are measurable w.r.t . Hence, random variables are measurable as well. According to Lemma 5.2 (see below)

for almost all w.r.t. . Thus,

Analogously, using Lemma 5.3 one can prove that

with some positive constants and

Lemma 5.2.

Let assumptions (AX0)-(AX2), (AK1) and (AK2) be fulfilled. Then there exist positive constants , and , such that for any satisfying the estimates based on the truncated local polynomials estimators of degree fulfill

for all and .

Lemma 5.3.

Let assumptions (AX0)-(AX2), (AK1) and (AK2) be fulfilled and for Then there exist positive constants , and such that for any the inequality

holds for all .

Proof.

We give the proof only for Lemma 5.2. Lemma 5.3 can be proved in a similar way. Fix some natural such that and consider the matrix with elements

The smallest eigenvalue of the matrix satisfies

| (5.24) | |||||

By Assumption (AX2)

with some For and any multi-indices , such that , define

We have ,

and

where and are two positive constants. Due to assumption (AK2), the class of functions

is a bounded Vapnik-Červonenkis class of measurable functions (see Dudley (1999)). According to Proposition 6.1 (see Appendix), we have for any

| (5.25) |

with some positive constants and . Combining (5.24) and ((AX2)) with (5.25), we get

where is the number of elements in the matrix Assume that is large enough so that Then on the set we have

since Therefore, it holds for any

Introduce the matrix with elements

Denote by the th column of and define

Since , we get for any with Hence . Thus, we can write

where is a vector valued function with components

and So, on the set we get

Denote

It holds

Note that and

with some positive constants , , and not depending on . Proposition 6.1 implies that for any

with some positive constants and . Furthermore, due to the representation

we get for any two points and in

Now it can be shown (see Dudley (1999)) that the class

is a bounded Vapnik-Červonenkis class of measurable functions. Hence

for and some positive constants and Furthermore, using the inequality we arrive at

with some positive constants and , provided that ∎

6 Appendix

6.1 Some results from the theory of empirical processes

Definition

A class of functions on a measurable space is called a bounded Vapnik-Červonenkis class of functions if there exist positive numbers and such that, for any probability measure on and any

| (6.26) |

where denotes the -covering number of in a metric , and is the envelope of . The following proposition is a key tool for obtaining convergence rates for local type estimators.

Proposition 6.1 (Talagrand (1994), Giné and Guillou (2001)).

Let be a measurable uniformly bounded VC class of functions, and let and be any numbers such that , and . Then, there exist a universal constant and constants and , depending only on the VC characteristics and of the class , such that

If moreover there exist constants and which depend only on the VC characteristics of , such that, for all and satisfying

References

- Andersen (2000) L. Andersen (2000). A simple approach to the pricing of Bermudan swaptions in the multi-factor Libor Market Model. Journal of Computational Finance, 3, 5-32.

- Audibert and Tsybakov (2007) J.-Y. Audibert and A. Tsybakov (2007). Fast learning rates for plug-in classiffiers under the margin condition. Annals of Statistics 35, 608 - 633.

- Bass (1997) R. Bass (1997). Diffusions and Elliptic Operators. Springer.

- Belomestny et al. (2006) D. Belomestny, G.N. Milstein and V. Spokoiny (2006). Regression methods in pricing American and Bermudan options using consumption processes, Quantitative Finance, 9(3), 315-327.

- Belomestny et al. (2007) D. Belomestny, Ch. Bender and J. Schoenmakers (2007). True upper bounds for Bermudan products via non-nested Monte Carlo, Mathematical Finance, 19(1), 53-71.

- Broadie and Glasserman (1997) M. Broadie and P. Glasserman (1997). Pricing American-style securities using simulation. J. of Economic Dynamics and Control, 21, 1323-1352.

- Carriere (1996) J. Carriere (1996). Valuation of early-exercise price of options using simulations and nonparametric regression. Insuarance: Mathematics and Economics, 19, 19-30.

- Clément, Lamberton and Protter (2002) E. Clément, D. Lamberton and P. Protter (2002). An analysis of a least squares regression algorithm for American option pricing. Finance and Stochastics, 6, 449-471.

- Devroye, Györfi and Lugosi (1996) L. Devroye, L. Györfi and G. Lugosi (1996). A probabilistic theory of pattern recognition. Application of Mathematics (New York), 31, Springer.

- Dudley (1999) R. M. Dudley (1999). Uniform Central Limit Theorems, Cambridge University Press, Cambridge, UK.

- Egloff (2005) D. Egloff (2005). Monte Carlo algorithms for optimal stopping and statistical learning. Ann. Appl. Probab., 15, 1396-1432.

- Egloff, Kohler and Todorovic (2007) D. Egloff, M. Kohler and N. Todorovic (2007). A dynamic look-ahead Monte Carlo algorithm for pricing Bermudan options, Ann. Appl. Probab., 17, 1138-1171.

- Friedman (1964) A. Friedman(1964). Partial Differential Equations of Parabolic Type. Prentice-Hall, Englewood Cliffts, NJ.

- Giné and Guillou (2001) E. Giné and A. Guillou (2001). A law of the iterated logarithm for kernel density estimators in the presence of censoring. Ann. I. H. Poincaré, 37, 503-522.

- Glasserman (2004) P. Glasserman (2004). Monte Carlo Methods in Financial Engineering. Springer.

- Glasserman and Yu (2005) P. Glasserman and B. Yu (2005). Pricing American Options by Simulation: Regression Now or Regression Later?, Monte Carlo and Quasi-Monte Carlo Methods, (H. Niederreiter, ed.), Springer, Berlin.

- Kim and Song (2007) P. Kim and R. Song (2007). Estimates on Green functions and Schrëdinger-type equations for non-symmetric diffusions with measure-valued drifts. J. Math. Anal. Appl., 332, 57-80.

- Kohler, Krzyzak and Todorovic (2009) M. Kohler, A. Krzyzak and N. Todorovic (2009). Pricing of high-dimensional American options by neural networks. To appear in Mathematical Finance.

- Lamberton and Lapeyre (1996) D. Lamberton and B. Lapeyre (1996). Introduction to Stochastic Calculus Applied to Finance. Chapman & Hall.

- Longstaff and Schwartz (2001) F. Longstaff and E. Schwartz (2001). Valuing American options by simulation: a simple least-squares approach. Review of Financial Studies, 14, 113-147.

- Mammen and Tsybakov (1999) E. Mammen and A. Tsybakov (1999). Smooth discrimination analysis. Ann. Statist., 27, 1808-1829.

- Sato and Ueto (1965) K. Sato and T. Ueto (1965). Multi-dimensional diffusion and the Markov process on the boundary. J. Math. Kyoto Univ., 4-3, 529-605.

- Talagrand (1994) M. Talagrand (1994). Sharper bounds for Gaussian and empirical processes. Ann. Probab., 22, 28-76.

- Tsitsiklis and Van Roy (1999) J. Tsitsiklis and B. Van Roy (1999). Regression methods for pricing complex American style options. IEEE Trans. Neural. Net., 12, 694-703.

- Van Roy (2009) B. Van Roy (2009). On regression-based stopping times, forthcoming in Discrete Event Dynamic Systems.