Further calculations for the McKean stochastic game for a spectrally negative Lévy process: from a point to an interval

E.J. Baurdoux111Department of Statistics, London School of Economics. Houghton street, London, WC2A 2AE, United Kingdom. E-mail: e.j.baurdoux@lse.ac.uk, K. van Schaik222Department of Mathematical Sciences, University of Bath, Claverton Down, Bath, BA2 7AY, United Kingdom. E-mail: k.van.schaik@bath.ac.uk. This author gratefully acknowledges being supported by a post-doctoral grant from the AXA Research Fund

Abstract

Following Baurdoux and Kyprianou [2] we consider the McKean stochastic game, a game version of the McKean optimal stopping problem (American put), driven by a spectrally negative Lévy process. We improve their characterisation of a saddle point for this game when the driving process has a Gaussian component and negative jumps. In particular we show that the exercise region of the minimiser consists of a singleton when the penalty parameter is larger than some threshold and ‘thickens’ to a full interval when the penalty parameter drops below this threshold. Expressions in terms of scale functions for the general case and in terms of polynomials for a specific jump-diffusion case are provided.

Keywords:Stochastic games, optimal stopping, Lévy processes, fluctuation theory

This paper is a follow-up to the paper [2] by Baurdoux and Kyprianou (henceforth BK), in which the solution to the McKean stochastic game driven by a spectrally negative Lévy process is studied.

Let us introduce the setting in BK (and in this paper). Let be a Lévy process defined on a filtered

probability space , where is the filtration generated by which is naturally enlarged (cf. Definition 1.3.38 in Bichteler [6]). For we denote by the law of when it is

started at and we abbreviate . Accordingly we shall write and for the

associated expectation operators. We assume throughout that

is spectrally negative, meaning that it has no positive jumps and that it is not

the negative of a subordinator.

The McKean stochastic game is an example of a type of stochastic games introduced by Dynkin [9]. It is a two-player zero sum game, consisting of a maximiser aiming at maximising over -stopping times the expected payoff according to the (discounted) lower payoff process given by for all and a minimiser aiming at minimising over -stopping times the expected payoff according to the (discounted) upper payoff process given by for all , where . That is, for any pair of stopping times the payoff to the maximiser is

We assume throughout this paper that the discount factor satisfies

(1)

where denotes the Laplace exponent of . For a spectrally negative Lévy process this Laplace exponent is of the form

for .

Here is called the Gaussian coefficient of and is the Lévy measure which satisfies .

Note that since both payoff processes vanish a.s. as , there is no ambiguity in allowing for and to be infinitely valued as we will in this paper. For any , this game has a value if the upper and lower value, and respectively, coincide. Even more, if a pair exists such that

the value exists and equals . In this case is called a saddle point (or Nash equilibrium). For an account of these concepts in a general Markovian setting, see Ekström and Peskir [10] and the references therein. For other examples of stochastic games, see e.g. Kifer [13], Kyprianou [15], Baurdoux and Kyprianou [3], Gapeev and Kühn [11], Baurdoux et al. [4].

Note that the McKean game can be seen as an extension of the classic McKean optimal stopping problem (cf. [17] and Theorem 1 below). In a financial interpretation, this optimal stopping problem is usually referred to as American put option, with the strike price. The McKean game then extends the American put option by introducing the possibility for the writer of the option to cancel the contract, at the expense of paying the intrinsic value plus an extra constant penalty given by the penalty parameter . Cf. e.g. Kifer [13] and Kallsen and Kühn [12] for a general account on the interpretation of stochastic games as financial contracts.

In BK it was shown that a saddle point indeed exists for the McKean game, so in particular the value function is well defined by

The optimal stopping time for the maximiser, , is the first hitting time of an interval of the form for some . For the minimiser the optimal stopping time is as follows. When the penalty parameter exceeds , where denotes the value function of the McKean optimal stopping problem, the minimiser never stops (i.e. ). When , the optimal stopping region for the minimiser is an interval of the form . If the Gaussian component of is equal to zero (note that this corresponds to the situation that does not creep downwards), we have . Furthermore formulae in terms of scale functions for and on were provided.

However, two issues were left open in BK. Firstly, when has a Gaussian component it was not clear when the optimal stopping region for the minimiser consists of a point and when of an interval, i.e. when and when holds. Secondly, no characterisation was given of . In this paper we give an answer to both these issues. In particular, we show that when there exists a critical value such that the stopping region for the minimiser is a single point when and a full interval when , cf. Theorem 6 (see also Remark 4). Furthermore we show that and can be characterised as unique solutions to functional equations using scale functions, cf. Theorem 8.

The rest of this paper is organised as follows. In the remainder of this introduction we introduce scale functions and some notation (Subsection 1.1), and review the results from BK in more detail (Subsection 1.2). In Section 2 we present our new results. Finally, in Section 3 we translate these results to a specific jump-diffusion setting, accompanied by some plots.

1.1 Scale functions

First we introduce some notation for first entry times. For we write

Furthermore we denote the often used first hitting time of for simplicity by , that is .

A useful class of functions when studying first exit problems driven by spectrally negative Lévy processes are so-called scale functions. We shortly review some of their properties as they play an important role in this paper, for a more complete overview the reader is e.g. referred to Chapter VII in Bertoin [5] or Chapter 8 in Kyprianou [16].

For each the scale functions are known to satisfy for all and

(2)

In particular it is evident that for all . Furthermore it is known that is almost everywhere differentiable on , it is right continuous at zero and

(3)

for all , where is the largest root of the equation (of which there are at most two, recall that is the Laplace exponent of ). We shall assume throughout this paper that the jump measure has no atoms when is of bounded variation, which implies that (see [8]).

In case has a Gaussian component it is known that with and . We usually write .

Associated to the functions are the functions defined by

(4)

for . Together the functions and are collectively known as scale functions and predominantly appear in almost all fluctuation identities for spectrally negative Lévy processes. For example, it is also known that for all and

and

(5)

where is to be understood in the limiting sense when .

For , consider the change of measure

(6)

Under , the process is still a spectrally negative Lévy process and we mark its Laplace exponent and scale functions with the subscript . From for we get by taking Laplace transforms

for all and, similarly

1.2 Reviewing the McKean stochastic game

First consider the McKean optimal stopping problem (or American put option) with value function , i.e.

We recall the solution to this problem as it appears in [7] (see also [18]):

Theorem 1.

For the McKean optimal stopping problem under (1) we have

where

which is to be understood in the limiting sense when , in other words, . An optimal stopping time is given by .

Next we recall the main result from BK on a saddle point and the value function for the McKean game:

Theorem 2.

Consider the McKean stochastic game under the assumption (1) and recall that .

(i)

If , then a stochastic saddle point is given by from Theorem 1 and , in which case

(ii)

If , a stochastic saddle point is given by the pair

where uniquely solves

(7)

(the optimal level of the corresponding McKean optimal stopping problem in Theorem 1) and .

Furthermore,

(8)

for and if then for any

where

which is to be understood in the limiting sense when , i.e. .

Hence a saddle point exists, and consists of the first hitting time of for the maximiser and of the first hitting time of for the minimiser. Note that when we know that the value of the McKean is not everywhere equal to that of its one-player counterpart as in that case.

Furthermore, equation (7) gives us a characterisation of , but we know only little about .

In BK, the issue whether or was only answered when has no Gaussian component:

Theorem 3.

Suppose in Theorem 2 that .

If has no Gaussian component, then and necessarily .

Remark 4.

We now discuss the intuitive interpretation of these results.

Due to the fact that has no positive jumps, the choice of has no influence when is started at a value to the left of as the minimiser would stop as soon as the process hits .

However, the situation is different when starting from any , the minimiser could either stop right away and pay to the maximiser, or wait a short time. From the minimiser’s point of view, the latter decision has the advantage of profiting from the discounting, but the disadvantage of the risk that a (large) negative jump could bring (far) below , where a higher payoff than (discounted) can be claimed by the maximiser. The closer is chosen to , the more dominant the disadvantage becomes and hence the exercise region for the minimiser can take the form of an interval .

When is a Brownian motion it is obvious that we have for any (see also [15]) as then the process can only get below by hitting it first.

The above Theorem 3 tells us that the other extreme case, namely for any , i.e. the disadvantage of waiting being dominant for the minimiser, occurs whenever has no Gaussian component.

The interesting question is what happens when has a Gaussian component and negative jumps as then there is a trade-off between the possibility for the process to enter the region continuously (which can only occur when ), leading to a relatively small pay-off and the possibility of passing by a jump potentially leading to a larger pay-off.

It turns out that for large enough, when stopping immediately is relatively expensive, the Gaussian part ‘wins’ in the sense that (the minimiser is happy to take the risk of the process jumping to a less-favourable region), while for small enough, when stopping immediately has become cheaper, the negative jumps ‘win’ in the sense that , see Theorem 6 below. In fact, in Figure 4 at the end of this paper we plot the negative relationship between and in the jump-diffusion case.

2 Single point or interval when has a Gaussian part

Throughout this section we assume that condition (1) holds. Recall that .

Consider the following function

(9)

i.e. the optimal value for the maximiser provided the minimiser only exercises when hits .

We first prove the following technical result.

Lemma 5.

Suppose and .

The function is differentiable on .

Furthermore, on on and is a strictly decreasing continuous function of .

Proof.

Let .

Due to Theorem 2 and the absence of positive jumps we have for

Also, for any

In fact, since stopping is not optimal on as the lower pay-off function is zero there, we deduce that we have for all

(10)

Now, let for some . From the defintion of in (9) we find

Since is a differentiable function on (see equation (27) in BK together with (10)) and using , we deduce that

(11)

showing that is strictly decreasing in .

Also, using (9) and the fact that is a feasible strategy also when , it holds that

where the final inequality follows from the observation that is decreasing in and that .

Note that since is strictly decreasing in for any and thus

because of Lemma 12 in BK.

It follows that

Since is arbitrary, we conclude from this inequality together with (11) that is indeed continuous in for any .

∎

Now we are ready to prove our main result, extending Theorem 2:

Theorem 6.

Suppose . When , then there exists a unique such that an optimal stopping time for the minimiser is given by

(i.e. ) when and by for some when .

Proof.

Let and suppose . We know from Theorem 2 that the stopping region for the minimiser is of the form for some . We claim that setting equal to the unique zero of on yields the result.

First let us show that this unique zero indeed exists. For it holds that (cf. Theorem 1). Using Lemma 5, it suffices to show that there exists some such that . We argue by contradiction, so, again using Lemma 5, suppose that for all . This implies that for each there exists some such that for all Since (Lemma 5) we deduce that for all , hence and in fact (by (9)).

This lower bound is strictly positive for since and does not depend on . Hence for small enough we deduce the existence of some such that , which contradicts with on .

Next for the optimal stopping time of the minimiser. For the same reasoning as above yields .

For the case we note that for any fixed the function is continuous in , as is easily seen from (9). Hence

from which we can deduce that we still have . Finally, let . Again much as above, we then have that and thus there exist for which . Since trivially is bounded above by this upper payoff function, it cannot be true that and thus it can also not be true that , so we indeed arrive at .

∎

Remark 7.

From the proof of the above Theorem 6 we see that this result is essentially due to the upper payoff function having a kink at the point where it first touches the value function as decreases (namely ). That is, if we would only slightly alter the upper payoff function on an environment of so it would have a continuous derivative, we should expect the optimal stopping time for the minimiser to be with for all and any spectrally negative Lévy process .

Next we provide expressions that complement those from Theorem 2. Recall that equation(8) in Theorem 2 provides us with a formula for on , so we can make use of the following function:

(12)

Theorem 8.

Suppose . We have the following.

(i)

Suppose . Then is the unique solution on to the equation in :

(ii)

Suppose (i.e. and , or and ). Then is the unique solution on to the equation in :

(13)

Furthermore, for and for :

(14)

Proof.

First we introduce the function

(15)

for . Observe that by the lack of positive jumps, is the optimal value the maximiser can obtain when the minimiser chooses as stopping region . Hence in particular .

Denote by the resolvent density of started at and killed at first passage below . Invoking the compensation formula (see e.g. Theorem 4.4 in [16]) leads to

where the final equality is due to the fact that on .

We know that (see e.g. Theorem 8.1 and Corollary 8.8 in [16] respectively)

and

hence

(16)

Furthermore, when is of unbounded variation we can compute for

and we can let to arrive at

(17)

Ad (i). Recall the function as defined in (9), and recall in particular from the proof of Lemma 5 that is the unique for which . Furthermore, note that for , since both sides equal the optimal value the maximiser can obtain when the minimiser only stops when hits . Combining these observations with (17) and yields the result.

Ad (ii). We first consider the case when is of bounded variation. We know from Theorem 4 in BK that we have continuous fit, i.e. . Since the integrand in (16) is bounded and equal to zero for we can take the limit inside the integrals to deduce that

so using it follows that indeed solves (13). For uniqueness, the function is strictly decreasing on and Since , the minimiser would not stop at points in from which the process cannot jump into and thus Combining these observations imply that is a strictly decreasing function on .

Next consider the case that is of unbounded variation. Now Theorem 4 in BK tells us that we have smooth fit, i.e. . Using together with (17) yields again that solves (13), uniqueness follows in the same way as in the previous paragraph.

Finally, (14) is readily seen from , (16) and the fact that satisfies (13).

∎

We conclude this section with some properties of as a function of . Note that by spectral negativity, implies .

Theorem 9.

Suppose . Then is continuous and decreasing as a function of , with if (resp. if ) and .

Proof.

We write to stress the dependence of the value function on . Continuity of is clear as the above Theorem 8 (ii) and the fact that is continuous in (see the argument for continuity of below) allow to apply the implicit function theorem.

To see that it is decreasing it suffices to show that is decreasing. For this, take and let denote the saddle point when . Then is the value when the supremum over all is taken in the expected pay-off corresponding to the pair . As is also feasible for the minimiser when we have that is bounded above by the value when the supremum over all is taken in the expected pay-off corresponding to the pair . This yields

(18)

as required.

Next, by the monotonicity the limits mentioned in the theorem exist. First we show , where . Suppose we had , then for some and any we have . So, starting from , if the maximiser chooses he ensures a strictly positive value, independent of . But this of course contradicts with as . If we had , then for some we have for small enough and consequently . But the minimiser can do better, that is in fact we have , as is easily seen. Namely, the minimiser can choose , so that starting from the maximiser can at most get discounted , the discount factor being strictly less than since and is right continuous.

Next suppose and let us show that . Suppose we had . Note that for any , is continuous, since for trivially and (18). So for it would follow that as . But the difference does not vanish as , as follows easily from the homogeneity of . More precisely, denoting by resp. the saddle point when starting from resp. , similar arguments as the ones leading to (18) yield in this case

and

thus

(19)

where . Clearly, since and the rhs of (19) is strictly positive iff . Even after taking the limit for this probability is positive on account of .

Finally, when can be shown by the same arguments, taking into account here one has for .

∎

3 Jump-diffusion case

In this section we translate the general results from the previous Section 2 to the particular case of a jump-diffusion with downwards directed, exponentially distributed jumps. In this case, which is quite popular in practical applications in finance e.g. due to its tractable nature, the expressions become much more explicit. In particular a formula exists that expresses explicit in terms of , cf. Proposition 12 (iv).

For the sequel we set

(20)

where , , is a Poisson process with intensity counting the jumps and is an iid sequence of random variables following an exponential distribution with parameter .

The following Proposition 10 states formulas for the scale functions in this jump-diffusion case (recall as defined in (6)):

Proposition 10.

Let . We have the following for given by (20) under .

(i)

The Laplacian is given by

The function has three zeros , with if ; if and ; if and .

(ii)

In particular, if we have

Define for the constants

We have the following formulas for the scale functions and on .

(iii)

If or we have

otherwise (necessarily ) we have

(iv)

If we have

while .

Proof.

Follows from the definitions (3) and (4) by some elementary calculations. Also, see e.g. [1].

∎

In Propositions 11 and 12 below we assume for simplicity that and , i.e. we set . (Note that condition (1) is met). This means that is a so-called risk neutral measure in the sense that the discounted price process is a -martingale, as required in a financial modelling context. (However the reader should have no difficulties translating the upcoming formulas to the situation for any if required.) Note that the above Proposition 10 (ii) gives explicit formulas for the roots in this case.

First we turn to formulas for the McKean optimal stopping problem (cf. Theorem 1).

Proposition 11.

The value function of the McKean optimal stopping problem is given by

where

Proof.

A direct derivation of these formulas can be found in [14] e.g. Alternatively, plugging the formulas from Proposition 10 in the results from Theorem 1 we see that we can write

(21)

Applying the identity

(22)

to this particular case (i.e. , , ), dividing both sides by and taking the limit for we find

(23)

Plugging this in the equation for we find . Using this expression in (21), together with (from (22) with ), the stated formula for indeed follows.

∎

Now we are ready to turn to formulas for the optimal exercise levels and the value function of the McKean game. Recall that for the game degenerates to the McKean optimal stopping problem.

Proposition 12.

Consider the McKean game driven by (20). Recall . We assume throughout that .

(i)

The optimal level is the unique solution to the equation in :

On we have and on we have

(ii)

The threshold is the unique solution to the equation in :

(iii)

Suppose . We have and on

(iv)

Suppose . We have

On we have and on we have

Proof.

Ad (i). Apply Proposition 10 to the formulas from Theorem 2 (ii).

Ad (iii). Apply Proposition 10 to the formula from Theorem 2 (ii) to obtain

and use (23) to see that the terms involving the exponential of a positive factor times vanish. (Of course, one can also reason directly that they should cancel, since otherwise would not stay bounded for large , which it should by definition).

Ad (iv). For , apply Proposition 10 to Theorem 8 (ii) and simplify to arrive at the stated formula. Note that

For , apply Proposition 10 to Theorem 8 (ii) and simplify, making use of the formula for and in particular Proposition 10 (ii).

∎

We conclude with some plots in this jump-diffusion setting to illustrate the main result from this paper.

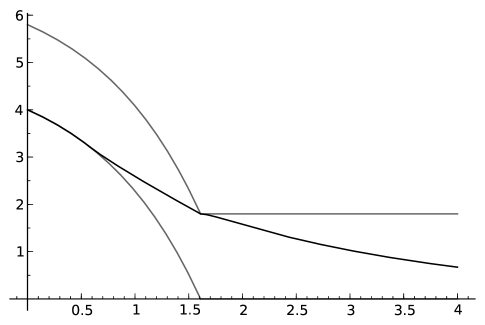

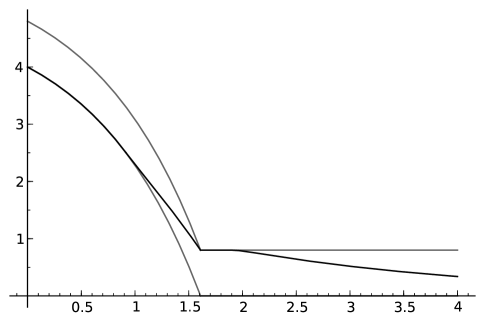

Figures 1 and 2 show the value function in the two different cases and .

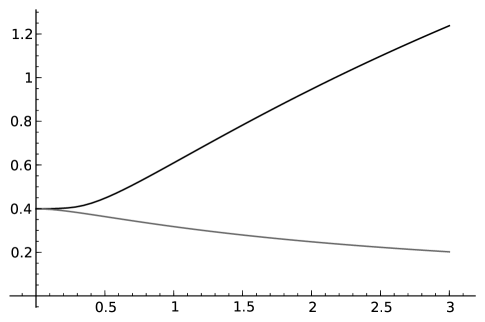

Figure 3 shows a plot of and as a function of . (Note that this really means only changes, hence the equation does not (necessarily) hold as changes with ). This figure can be explained as follows. If , converges to the value of the McKean optimal stopping problem for with and hence also has some limit in the interval . The figure suggests that the difference between and vanishes as , which might be explained as follows. As pointed out in Remark 4, means that when starts above , the probability of hitting before it reaches levels (far) below is large enough to have . Obviously, this probability vanishes together with , and hence the length of the interval vanishes as . Furthermore, as , for the maximizer in the McKean optimal stopping problem the negative effect of discounting vanishes in the sense that first entry time of any interval has a density approaching the Dirac measure in . Hence, and for any . In particular also . The vanishing of as is explained as above by the fact that increasing means that the probability of hitting before falls (far) below increases, and hence the effect of the negative jumps is of vanishing relevance. In the limit therefore the minimizer does not need to choose an for any .

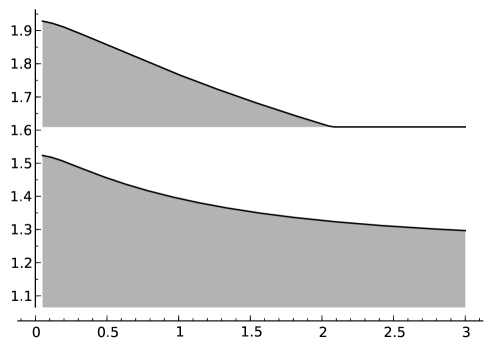

Finally Figure 4 shows how and vary with . Note that the behaviour of is indeed consistent with the structure Figure 3 suggests.

Figure 1: A plot of the value function in the case , so . The grey curves are the upper and lower payoff functions, the black curve is . Here , , , and Figure 2: A plot of the value function in the case , so . The grey curves are the upper and lower payoff functions, the black curve is the value function . Here , and are as in Figure 1; , and Figure 3: A plot of (the black curve) and (the grey curve) as a function of Figure 4: A graphical illustration of the optimal stopping regions (maximizer) and (minimizer) as a function of . The upper black curve is , the lower one is

References

[1] Avram, F. and Kyprianou, A.E. and Pistorius, M. R. (2004) Exit problems for spectrally negative Lévy processes and applications to (Canadized) Russian options. Ann. Appl. Probab.14, 215–238.

[2] Baurdoux, E.J. and Kyprianou, A.E. (2008) The McKean stochastic game driven by a spectrally negative Lévy process. Elec. J. of Probab.8, 173–197.

[3] Baurdoux, E.J. and Kyprianou, A.E. (2008) The Shepp–Shiryaev stochastic game driven by a spectrally negative Lévy process. To appear in Theory of Probability and Its Applications.

[4] Baurdoux, E.J. and Kyprianou, A.E. and Pardo, J.C. (2010) The Gapeev–Kühn stochastic game driven by a spectrally positive Lévy process. Submitted.

[5] Bertoin, J. (1996) Lévy Processes. Cambridge University Press.

[6] Bichteler, K. (2002) Stochastic Integration with jumps. Cambridge University Press MR1906715.

[7] Chan, T. (2004) Some applications of Lévy processes in

insurance and finance. Finance.25, 71–94.

[8]

Doney, R.A. (2005) Some excursion calculations for spectrally one-sided Lévy processes.

Sém. Probab. XXXVIII, 5-15.

[9] Dynkin, E. B. (1969) A game-theoretic version of an optimal stopping problem. Dokl. Akad. Nauk. SSSR185, 16–19.

[10] Ekström, E. and Peskir, G. (2008) Optimal stopping games for Markov processes. SIAM J. Control Optim.2, 684–702.

[11] Gapeev, P. V. and Kühn, C. (2005) Perpetual convertible bonds in jump-diffusion models. Statistics & Decisions23, 15–31

[12] Kallsen, J. and Kühn, C. (2004) Pricing derivatives of American and game type in incomplete markets. Finance and Stochastics8, 261–284.

[13] Kifer, Y. (2000) Game options. Finance and Stochastics4, 443–463.

[14] Kou, S. and Wang, H. (2002) Option pricing under a jump-diffusion model. Management Science50, 1178–1192.

[15] Kyprianou, A. E. (2004) Some calculations for Israeli options. Finance and Stochastics8, 73–86.

[16] Kyprianou, A. E. (2006) Introductory Lectures on Fluctuations of Lévy processes with Applications. Springer.

[17] McKean, H. (1965) Appendix: A free boundary problem for the heat equation arising from a problem of mathematical economics. Ind. Manag. Rev.6, 32–39.

[18] Mordecki, E. (2002) Optimal stopping and perpetual options for Lévy processes. Finance Stoch.6, 473–493.