Regularity of the Exercise Boundary for

American Put Options on Assets with Discrete Dividends

B. Jourdain and M. Vellekoop

Université Paris-Est, CERMICS, Projet MathFi

ENPC-INRIA-UMLV, 6 et 8 avenue Blaise Pascal, 77455 Marne La Vallée, Cedex

2, France, e-mail : jourdain@cermics.enpc.fr. This research benefited

from the support of the “Chair Risques Financiers”, Fondation du

Risque. Research was partially completed while the author was visiting the Institute for Mathematical Sciences, National University of Singapore in 2009. The visit was supported by the institute.

Corresponding Author, University of Amsterdam,

Faculty of Economics and Business,

Department of Quantitative Economics,

Section Actuarial Science,

Roetersstraat 11,

1018 WB Amsterdam, e-mail : m.h.vellekoop@uva.nl

Abstract

We analyze the regularity of the optimal exercise boundary for the American Put option

when the underlying asset pays a discrete dividend at a known

time during the lifetime of the option. The ex-dividend asset price

process is assumed to follow Black-Scholes dynamics and the dividend

amount is a deterministic function of the ex-dividend asset price just

before the dividend date. The solution to the associated optimal

stopping problem can be characterised in terms of an optimal exercise

boundary which, in contrast to the case when there are no dividends, may

no longer be monotone. In this paper we prove that when the dividend

function is positive and concave, then the boundary is non-increasing in a left-hand

neighbourhood of , and tends to

as time tends to with a speed that we can

characterize. When the dividend function is linear in a neighbourhood of zero, then we show continuity of the exercise boundary and a high contact principle in the left-hand neighbourhood of . When it is globally linear, then right-continuity of the boundary and the high contact principle are proved to hold globally. Finally, we show how all the previous results can be extended to multiple

dividend payment dates in that case.

Introduction

We consider the American Put option with strike and maturity

on an underlying stock. We assume that the stochastic dynamics of the ex-dividend price process of this stock can be modelled by

the Black-Scholes model and that at the given times in the time interval , discrete stock dividends are paid.

The case without dividends is denoted by and we will use the convention that and throughout the paper. The value of the dividend payments

are functions () of the ex-dividend asset price. This means that the stock price process satisfies

(0.1)

for an initial price , interest rate and volatility which are assumed to be

positive and with a standard Brownian Motion.

Throughout the paper we assume that

the dividend functions are non-negative and non-decreasing for all

and such that is non-negative and non-decreasing.

We will pay particular attention to the following special cases :

•

where , which we will call the proportional

dividend case,

•

with , which we will call the constant dividend case, and

•

with and , which we call the mixed dividend case.

We will see that the behaviour of around zero determines the behaviour

of the exercise boundary at the dividend dates so the latter case will turn out to be very similar to the one where we have proportional dividends.

For , let

(0.2)

denote the price at time

of the American Put option, where is the set of stopping times with respect to the

filtration

taking values in .

The solution to this optimal stopping problem for the case without

dividends (i.e. ) goes back to the work of McKean [16] and Van Moerbeke

[21]. The optimal stopping time is the first time that the

asset price process falls below a time-dependent value (the so-called

exercise boundary which we will denote by ), and McKean

derived a free-boundary problem involving both the pricing function

such that and . Van Moerbeke

derived an integral equation which involves both and its

derivative, but in later work by Kim [14], Jacka [12] and

Carr, Jarrow and Myneni [3] an integral equation was

derived which only involves itself. The regularity and

uniqueness of solutions to this equation was left as an open problem in

those papers. Uniqueness was proven by Peskir

[19], using his change-of-variable formula with

local time on curves [18]. It is known that the

optimal exercise boundary is convex

[5, 6] and its asymptotic

behaviour at maturity is given in [15]. But although it was

claimed in several papers (for example [17]) that it is

at all points prior to maturity, a complete proof has been given only

recently by Chen and Chadam [4]. In fact, in that paper it

was actually shown that it is in all those points and a later

paper by Bayraktar and Xing [2] shows that this remains

true if the underlying asset pays continuous dividends at a fixed

rate.

In practice, continuous dividends are not a satisfying model since

dividends are paid once a year or quarterly. That is why we are

interested in dividends that are paid at a number of discrete points in time.

To begin with, we deal in this paper

with the simplest situation where there is only one dividend time

before the maturity of the Put option111When there is only one dividend

date, i.e. , we will often suppress the value in our notation,

so we will write instead of , for and so on..

Afterwards we show how some results can be extended to the case of multiple dividends.

When we assume discrete dividend payments such as the proportional

or fixed dividend payments mentioned above, the optimal exercise

boundary will become discontinuous at the dividend dates and before the

dividend dates it may not be monotone (see Figure 1).

Integral formulas for the

exercise boundary which are similar to the ones in

[3] have been derived under the assumption that the

boundary is Lipschitz continuous (see Göttsche and Vellekoop

[10]) or locally monotonic (Vellekoop &

Nieuwenhuis [23]). In this

paper we therefore study conditions under which such regularity

properties of the optimal exercise boundary under discrete dividend

payments can be proven.

In the first Section, we introduce the pricing functions of the

American Put option in the model (0.1) for and the associated

exercise boundaries where the means for that only at the times dividends are being paid while means that no dividends are being paid.

We then explain that for , on the time-interval

, the American Put

price is equal to the price of an American option in the Black-Scholes model with no

dividends if we take its maturity and its payoff when exercised early and a modified

payoff when

exercised at the maturity time . Studying the properties of the single dividend case will then allow us to derive properties of the sequence of functions and in a recursive manner.

In the second Section, we therefore first look at the single dividend case only and prove that when the dividend function is positive and concave, then the boundary is non-increasing in a left-hand

neighbourhood of , and tends to

as time tends to with a speed that we can

characterize. In the third Section we assume moreover that the dividend function is linear in a

neighbourhood of , a condition satisfied in the proportional, the constant and the mixed dividend cases. Then we show that the exercise boundary is continuous

and a high contact principle holds in a left-hand

neighbourhood of . In the proportional dividend case, right-continuity of the boundary and the high contact principle are proved to hold globally. Finally, we show how results for a single dividend date can be extended to multiple dividend dates

in that case.

Notations and definitions :

•

For and , we use the notation for the stock price at time when

the initial price is equal to and when there is no

dividend (i.e. ). We also denote by the local time at level and

time of the process and by the density of with respect to the

Lebesgue measure when .

•

Let denote the infinitesimal generator of the

Black-Scholes model without dividends : .

•

If and we write for the solution to

(0.3)

for

under the initial condition that . Note that we still retain the notation introduced in (0.1) so .

•

Let be the

cumulative distribution function of the standard normal law.

•

Let denote a constant with may change from line to line.

•

We say that is positive when , .

•

By a left-hand neighbourhood of , we mean an open interval

for some .

•

We will often denote the value function for the case without dividends by and the value function for the case of one dividend by .

1Preliminary results

The following results, which have been proven in

[7, 8, 11, 20],

provide an optimal stopping time in (0.2).

Proposition 1.1

Let be an -adapted

right-continuous upper-semicontinuous process with .

Then the càdlàg version of the Snell

envelope is continuous on and the stopping

time is optimal : .

The conditions for this result are satisfied by

since for all we have

and is right-continuous and upper semicontinuous for all since the jump sizes of at are non-positive for all (for a Call option is no longer upper-semicontinuous and, in the single dividend case, Battauz and Pratelli [1] artificially stretch

the time-interval by introducing a ficticious interval where denotes the end of the cum-dividend date and the beginning of the ex-dividend date to reduce the evaluation problem to the computation of the Snell envelope on stopping times taking values in ).

According to [8], there thus exists pricing

functions defined as follows:

Proposition 1.2

Take and a constant . The Snell envelop of is such

that where

Moreover the previous supremum is attained for .

Let us now derive some properties of the pricing functions and define the exercise boundaries .

Lemma 1.3

Let for all the dividend functions be non-negative, non-decreasing

and such that is non-negative and

non-decreasing. Then we have

(1.1)

For , let

Then for and we have that . Last the functions

cannot vanish on an interval.

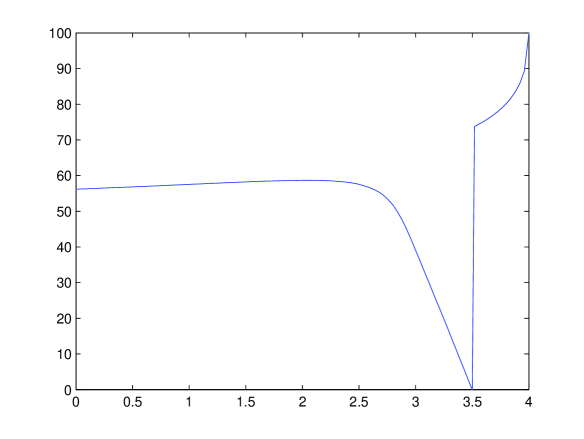

Figure 1 plots the exercise boundary of

the Put option with strike and maturity in the model

(0.1) with , , and proportional dividends

with . This exercise boundary was computed by a binomial tree

method (see [22]).

Figure 1: Exercise boundary (, , , ,

, proportional dividends : ) obtained by a

binomial tree method

Proof . For the first part, we use a similar proof as in

[10]. For a fixed take which,

with the monotonicity of for all implies that

for all . Now fix the value of with .

For such

that , since need not be optimal for the case where the stock price at time

equals , we deduce

For such that

,

because and the function is non-decreasing.

Since for all and , the

definition of implies that for and by the continuity of

this must then be true for as well when . When

, . If then, by

definition of there

exists such that and . For , since ,

one deduces that for and that . Last, . Assume that there exists an interval with such

that is zero in every point of this interval, and for , let be such that

we have that

. Then

so . Letting ,

one deduces that .

Let us now prove some regularity properties of the pricing functions .

Lemma 1.4

Let . Under the assumptions of Lemma 1.3,

the function is continuous on the sets , , ,…, and for all and all outside

the at most countable set of discontinuities of , the limit exists and is equal to . Moreover, the exercise boundary is upper-semicontinuous on .

Last, for all points in the set the partial derivatives , and exist and satisfy , and is on this set.

Proof . Let us check the behaviour of as for ; the continuity of

follows from a similar but easier

argument. Since , one has, using (1.1) for the

inequality,

By continuity of the process

, which is ensured by Propositions 1.1 and 1.2, one deduces that a.s., . Since admits a

positive density w.r.t. the Lebesgue measure on , a.e. . By

continuity of , the function is

continuous outside the at most countable set of discontinuities of the

non-decreasing function . With (1.1), one deduces that for

all outside this set, and that , which ensures that . Since according to Lemma 1.3, for , , the continuity properties of imply that is upper-semicontinuous on the sets , , and therefore on .

Let . By continuity of on , the set is an open subset of .

Let and be an open neighbourhood of with regular boundary such that is included in the connected component of which contains . Define the stopping times

and . The flow property

for the Black-Scholes model without dividends implies that for ,

and

. Using the strong Markov property for the third equality,

one deduces

(1.2)

Let be a solution to the Dirichlet problem where on and on . By Theorem 3.6.3. in [9] this function is in and continuous on . But then

by optional sampling so on and therefore its partial derivatives exist in and they satisfy .

The characterization of the restriction of to as

the pricing function of an American option in the Black-Scholes model

without dividends, as stated in the next proposition, is the key to the study

of the exercise boundaries performed in the following sections.

Proposition 1.5

Under the assumptions of Lemma 1.3, we have for all ,

where and for , and the supremum is attained for

(with the convention that

).

Moreover, for all and , we have that and for all positive .

Proof . For the statement is trivial so assume .

The last statement of the proposition is obvious because when , the optimal stopping problems in proposition 1.2 which define the values and and the values and are the same

for and because we then have that for .

Take and and define .

Arguing like in the derivation of (1.2), one easily checks that

where we used the previous result for to obtain the second equality. We thus

deduce that

when . Let now be any stopping time in . For such that , the random variable

belongs to and is such that

This result shows that it is natural to consider the case with only one dividend date first and then use the results to

generalize to multiple dividend dates. This will allow us to prove the following result for the multiple dividend problem:

Theorem 1.6

Let for all the dividend functions be non-negative, non-decreasing

and such that is non-negative and

non-decreasing. Then for all the exercise boundaries are strictly positive and locally bounded away from zero

on . If is positive, then with as when is also concave. Moreover, if for all we have for some then

•

for all the value function is convex in ,

•

is right-continuous on and , i.e. the smooth contact property holds, and

•

there exist such that on , the function is continuous and non-increasing with

as .

The proof for this Theorem can be found in the Appendix. It is based on the stronger results that we will prove for the single dividend case in this section and the next two sections. Remember that in the single dividend case we use the shorthand notation , , and and that and are used for the case when no dividends are present. We will also write for now that .

We first derive some properties of the function .

Lemma 1.7

Assume that is a non-negative concave function such that

is non-negative. Then is continuous, non-decreasing and

such that is non-decreasing. Let and

respectively denote the left-hand

derivative of and the non-positive Radon measure equal to the second order

distribution derivative of on . The function is continuous,

non-increasing and for all .

The function

where, by convention, ,

is not greater than on where , and globally bounded.

If is convex, then there is a constant

such that and for , the second order distribution

derivative of admits a density w.r.t. the Lebesgue measure

and is equal to

on and a.e. on , .

To prove this lemma, we need the following properties of the pricing

function in the model without dividends.

Lemma 1.8

For the case without dividends we have that

the partial derivatives , and

exist and for all and

. Moreover, , is

convex and on . Last,

Before proving these Lemmas, let us give some examples of functions

obtained for different choices of the dividend function .

Examples of functions :

•

In the constant dividend case, and the function

is equal to on and to for

, on with taking its

values in , on

and such that

where

is equal to on and to on .

•

In the proportional dividend case, and

is convex, with taking its values in

and on .

•

The proportional dividend case provides an example of a non-negative

concave function such that

is non-negative which leads to a convex function . This

example is not unique. For instance, let . The

function is convex positive nonincreasing and such

that . So it is continuous and

decreasing and admits an inverse . For

, we set . The

continous function

is non-increasing on

by the non-increasing property of both and

and the positivity of this last function. It tends

respectively to and as and . Let

. One has

which also writes . The function

is non-negative, concave and such that is non-negative. The

convexity of combined with the equality

implies that

is convex.

Figure 2 illustrates the construction of the function

from on the three previous examples of

dividend functions.

\psfrag{x}{\Large$x$}\psfrag{K}{\Large$K$}\psfrag{D}{\Large$D$}\psfrag{ctd}{\Large$\bar{c}(t_{d})$}\psfrag{x0}{\Large$x_{0}$}\psfrag{u(td,x)}{\Large$\bar{u}(t_{d},x)$}\psfrag{const div D=1}{\Large Const div $D=1$}\psfrag{prop div rho=0.55}{\Large Prop div $\rho=0.75$}\psfrag{convex example}{\Large Convex example}\includegraphics{functg.eps}

Figure 2: Examples of functions

Proof of Lemma 1.7.

Since the concave function is non-negative, it is continuous and

non-decreasing. And since is non-negative, . The convex

function being non-negative and equal to for , is non-decreasing.

Since is continuous, non-increasing and not

smaller than , the same properties hold for . For ,

.

By concavity of ,

(1.3)

So is not greater than on . The

constant is infinite if and only if is the identity

function and then is constant and equal to . When

, is bounded from below by

on . Moreover, since is concave, continuous and ,

(1.4)

One has

(1.5)

where the last term is non-positive by (1.3) and since

.

Define

which is finite by Lemma 1.8.

Since

is non-increasing by convexity of

and equal to on , one deduces

(1.6)

With , which is larger than , substituted in

(1.6), and using (1.4) and , one

concludes that when ,

For , since and

are non-negative and , we have by (1.5),

where we used that by

(1.4) for the second inequality and the smooth fit property

and a partial integration

for the equality.

Last, assume that is convex. If and respectively denote the right-hand derivatives of and , one has and

since

is negative and non-positive, the

right-hand-side of this equality is non-positive and the left-hand-side

is non-negative. So both are zero and

the functions and are with

. The first factor in the

right-hand-side being

globally continuous and on , one deduces that the

distribution derivative of is equal to

.

This measure being non-negative by convexity of , is absolutely

continuous with respect to the Lebesgue measure and so is the second

order distribution derivative of . For ,

where the left-hand-side is non-decreasing and the

right-hand-side non-increasing. So there is a constant

such that and for . As a consequence

and on

. The convexity of implies that is

non-decreasing and therefore that a.e. on ,

.

Proof of Lemma 1.8. The proof of the first statement

is similar to the one of the last statement in Lemma

1.4. Moreover, is convex as the supremum of

convex functions. We refer for instance to Lemma 7.8 in Section 2.6

[13] for the continuous differentiability property of

this function. Let , , and take such that and

. One has

By Tanaka’s formula, when ,

One deduces that

2Limit behaviour and monotonicity of the exercise boundary as

Using the results in the previous section, we first

check that tends to as if is positive

(i.e. , ).

Lemma 2.1

Let be a non-negative and non-decreasing

function s.t. is non-negative and

non-decreasing.

Assume moreover that there exists a such that is zero on and positive on , then we have . When i.e. is positive, then and

•

if is such that admits a finite limit as then as ,

•

if is concave, is convex and the constant such that, according to Lemma

1.7, , belongs to then

. When i.e. is the identity function, then .

Note that when is postive and concave, then admits a finite limit as which is equal to .

Proof . Suppose that , then there exists a and a sequence such that with

and since we have and we may choose such that it is not one of the countably many discontinuity points of .

Then for all and taking the limit and applying Lemma 1.4 gives that but either and then or and then so in both cases we get a contradiction.

Assume that is such that exists and is finite. Since both and are non-negative, necessarily . For ,

For and , which implies

.

With , one deduces that, as , for , where the does not depend on . One easily deduces the desired upper-bound for .

When is also convex, according to Lemma 1.7, either is the identity function and

is constant and equal to or there is a constant

such that for . In the latter

case, one has

for and for .

As a consequence,

.

One deduces that when ,

which implies that

. When is the identity function, the inequality is obvious.

We now obtain monotonicity of the exercise boundary in a left-hand

neighbourhood of the dividend date .

Proposition 2.2

If is a positive concave function such that is non-negative, there exists a constant such that for , is non-decreasing on

.

Moreover, we have for all and all that

(2.1)

(2.2)

Last, for any such that , and admits a right-hand limit as .

One easily deduces the following Corollary.

Corollary 2.3

If the dividend function is non-negative, non-decreasing

and such that is non-negative and

non-decreasing, then the exercise boundary does not vanish on . Moreover, for all , .

If is a positive concave function such that is

non-negative, then is non-increasing and left-continuous on . Moreover, as .

Remark 2.4

In contrast to the result of Corollary 2.3, we notice that in the alternative model formulation known as the Escrowed model

where is a positive constant, the boundary is actually equal to on a left-hand neighbourhood of . Indeed, reasoning like in the proof of Proposition 1.5, one can check that for , the value function in this model is

where . Since

early exercise is never optimal when i.e. .

Proof of Corollary 2.3.

For , is larger than the exercise boundary of the perpetual Put in the Black-Scholes model without dividends. For , by Proposition 1.5, the pricing function is smaller than the one corresponding to the identity dividend function. Therefore for , is larger than the associated boundary. For the identity dividend function the function is constant and equal to so that the exercise boundary is non-increasing on by (2.1) and therefore does not vanish by Lemma 1.3.

Let us now assume that is a positive concave function such that is

non-negative. The monotonicity of is a consequence of Proposition 2.2 and the left continuity

then follows from the upper-semicontinuity.

Let us now assume that is not equivalent to where as and obtain a contradiction. Because of the upper-bound stated in Lemma 2.1, this implies the existence of a constant and a sequence in such that and , . For , let and denote the optimal stopping time starting from at time . One has

(2.3)

where we used the monotonicity of on for the first inequality and

a reasoning similar to the one made when is concave in the proof of Lemma 2.1 for the last equality.

Assume that is not the identity function which implies . Using the monotonicity of both and , one gets that for , is not greater than

Hence for , with the not depending on . This inequality still holds when is the identity function, since then and .

With (2.3), one deduces that

. Hence for large enough which provides the desired contradiction.

Proof of Proposition 2.2. Let ,

and be such that

.

Since by Lemma 1.7, , ,

(2.4)

By Tanaka’s formula,

In particular .

The function is convex and on

and on and . Hence its second order

distribution derivative is equal to where, by

convention, .

Applying again Tanaka’s formula and the occupation times formula, one

deduces that

The process

is a martingale since by (1.1) and

according to Lemma 1.7. With (2.4), one deduces that

(2.6)

One easily deduces (2.1) and, since by Lemma

1.7, and is not

greater than

for ,

(2.7)

Define and

let be such that

. The existence of

is ensured

by Lemma 2.1 which applies since, according to the proof of

Lemma 1.7, the function is continuous and both and

are non-decreasing. We now choose and where . One has

with

convention . Let . For , by the Markov

property, one has

In the same time,

Combining both inequalities, one obtains

The ratio equals

and for and

this converges to as and go to while goes to .

Since by Lemma 2.1, converges to as

goes to , one may choose positive constants such that

and

Since for and ,

with

according to (1.1) and , (2.2) easily follows from (2.1).

Let be such that . For , one has

. By (1.1),

. With (2.2), one deduces that

is integrable on

and the right-hand limit makes

sense.

Remark 2.5

When i.e. when the Put option is perpetual,

In the

proportional dividend case, since for .

With (2.6), one deduces that for any , is

non-decreasing on .

In the constant dividend case,

is positive on .

3Continuity of the exercise boundary and high contact principle

We can now state our main result concerning the

continuity of the exercise

boundary for the single dividend case. Note that it applies to the

proportional, the constant and the more general mixed dividend cases.

Proposition 3.1

Assume that is a positive concave function such that is

non-negative. Then for such that is

right-continuous at , the smooth contact

property holds and .

If is convex, then is right-continuous on

. More generally, if is such that

(3.1)

then there exists an such that is continuous on .

Remark 3.2

On any open interval on which is non-decreasing, it is right-continuous by upper-semicontinuity and therefore the smooth contact

property holds.

In order to prove the Proposition, we will need the following

estimations of the first order time

derivative and the second order spatial derivative of the pricing function

in the continuation region.

Lemma 3.3

Assume that is a non-negative concave function such that is

non-negative. Then

(3.2)

and

(3.3)

If is

convex, then for , is convex and for , and .

More generally, under (3.1), there

exists such that

for all and for all we have .

Proof of Proposition 3.1.

For , by Corollary 2.3, and by

Proposition 2.2, the following Taylor expansion makes sense

(3.4)

Substituting for in (3.4) and subtracting the result from (3.4) itself gives for

(3.5)

If is such that , choosing and computing from

(3.5) written with replacing , one deduces that for ,

(3.6)

We decompose the proof in three steps using the above expansions. First we check that when is such that is right-continuous at , then . In the second step, we check that when is right-continuous at , then the smooth contact property holds at . In the last step, we prove that is right-continuous at for close to under (3.1) and with no restriction in the convex case.

Step 1 : Let be such that is right-continuous at and . For such that , by (3.6), is smaller than

By continuity of , the first term converges to

as . Moreover, (2.2) and (3.3)

ensure that the second term is

arbitrarily small uniformly for when is close

enough to . Last, with the right-continuity of at , the third

term converges to as , which ensures the desired right-continuity property. Step 2 : Let us now assume that for such that is right-continuous at , and obtain a

contradiction.

Let be such that . According to (3.2) and (3.3), there exists a constant

such that and

. Writing (3.4) for , one deduces that

Since tends to as

and is right-continuous at , one deduces the existence of

such that

(3.7)

For , let

denote the stopping time such that

One has

.

Computing the difference, using the monotonicity of and the

Lipschitz continuity of one deduces that

(3.8)

By (3.7), . When

tends to , converges a.s. to which is

equal to according to the iterated

logarithm law satisfied by the Brownian motion . Hence converge a.s. to as . Since

, by

Lebesgue’s theorem, the

right-hand-side of (3.8) converges to as

which implies the desired contradiction : .

Step 3 : Let

be such that is not right-continuous at . We are going to derive a contradiction when is convex or close to under (3.1). The continuity of on a left-hand neighbourhood of then follows from the left-continuity stated in Corollary 2.3. By the upper-semicontinuity of and the positivity of stated in Corollary 2.3, there exists a sequence in converging to as and such that .

Let with .

For large enough and we may use (3.5) for . The left-hand-side is not smaller than . When tends to , by

continuity of , the first term in the right-hand-side tends to

. Moreover by (3.3), there is a constant not depending on such that

Hence and one deduces

(3.9)

by letting and go to .

By (3.4) and Proposition 2.2,

With the equality and

Lemma 3.3, one deduces that for and close to under (3.1)

and with no restriction in the convex case,

(3.10)

According to (2.2), there is a finite constant such

that , so

if we

take .

With

(3.9) and (3.10), one deduces that for close to under (3.1)

and with no restriction in the convex case, for large enough,

•

,

•

and therefore for with ,

Taking the limit in (3.5) written for , we now obtain , which contradicts (3.9).

Proof of Lemma 3.3.

Let . When is convex, since is also convex, for each

stopping time ,

is convex. So which is equal to the supremum over

of the previous functions is convex. Let now , and be such that

Since , one has

When is convex, according to Lemma 1.7, is

a function bounded from below by , the right-hand-side is equal

to , so one easily concludes.

In general, by (2.5) and the martingale property of the process , the

previous inequality writes

(3.11)

Since , using

the occupation times formula, one deduces that

Since and are both non-decreasing, . Using moreover

one deduces (3.2). The inequality (3.3) follows since for we have .

Assume (3.1). Then is equal to on

, and (3.11) implies that

For , one has . For close enough to we have that

by Lemma 2.1 and

for ,

Bounding from above the two last terms like in the derivation of the upper-bound for in the

proof of Lemma 2.1, one deduces the last assertion.

4Conclusions and Further Research

We have proven local results concerning the regularity of the exercise

boundary for a dividend-paying asset. Even in the simplest case of

proportional dividends, it would be of great interest to

prove the following feature observed in numerical calculations: for a single dividend payment, when

is large, the exercise boundary is non-decreasing for small times

and monotonicity seems to change only once before . We also would like to extend the results that we have obtained for multiple dividend payments in the proportional case to more general functions . The key issue in this perspective is to derive global estimates on the derivatives of the value function before to replace those which follow from the convexity in the variable in the proportional case.

Another interesting matter to investigate would be the optimal exercise

boundary for the alternative model for dividends known as the Escrowed Model.

As we have shown in Remark 2.4, this boundary is zero on an interval

with strictly positive length before every dividend date, but other properties

of this boundary have yet to be established.

The two first statements can easily be deduced by respectively adapting the comparison argument given at the beginning of the proof of Corollary 2.3 and the proof of Lemma 2.1.

Let us now consider the case of multiple proportional dividends. We will prove by induction on that the statement holds together with the following lemma.

Lemma A.1

If for all we have for some then is convex and on and on for . Moreover, the function is equal to on , not smaller than and bounded on and satisfies

(A.1)

(A.2)

For , the result is a consequence of Propositions 2.2 and 3.1, Corollary 2.3 and Lemma 3.3, the refinement over (2.2) in the last inequality in (A.2) following from the monotonicity of which is a consequence of the convexity of .

Assume the induction hypothesis to be true for a certain . Then is convex and arguing like in the beginning of the proof of Lemma 3.3, one obtains that for , is convex and nonincreasing.

The function is on by the smooth contact property for at time and on by the regularity properties of stated in Lemma 1.4. Moreover the function is equal to on , not smaller than and bounded on respectively by convexity of and by the lower bound in (A.1) combined with the equality which is satisfied for . One may now adapt the proofs of Proposition 2.2, Lemma 3.3 and Corollary 2.3 to check

that the exercise boundary is non-increasing and equivalent to in a left-hand neighbourhood of and that (A.1) and (A.2) hold with replacing . Next, with these bounds on the derivatives of , one adapts the proof of Proposition 3.1 to obtain right-continuity of the exercise boundary on and smooth contact : , . This proves the statement for and concludes the proof.

References

[1]

A. Battauz and M. Pratelli.

Optimal stopping and American options with discrete

dividends and exogenous risk.

Insurance: Mathematics and Economics, 35:255-265, 2004.

[2]

E. Bayraktar and H. Xing.

Analysis of the Optimal Exercise Boundary of American Options for Jump Diffusions.

SIAM Journal on Mathematical Analysis, 41 (2):825–860, 2009.

[3]

P. Carr, R. Jarrow, and R. Myneni.

Alternative characterizations of American puts.

Mathematical Finance, 2:87–106, 1992.

[4]

X. Chen and J. Chadam.

Mathematical analysis of the optimal exercise bounary for American

put options.

SIAM Journal on Mathematical Analysis, 38(5):1613–1641,

2006/07.

[5]

X. Chen, J. Chadam, L. Jiang, and W. Zheng.

Convexity of the exercise boundary of the American put option on a

zero dividend asset.

Mathematical Finance, 18:185–197, 2008.

[6]

E. Ekström.

Convexity of the optimal stopping boundary for the American put

option.

Journal of Mathematical Analysis and Applications,

229(1):147–156, 2004.

[7]

N. El Karoui.

Les aspects probabilistes du contrôle stochastique, Lecture

Notes in Mathematics 876.

Springer-Verlag, Berlin, 1981.

[8]

N. El Karoui, J.-P. Lepeltier, and A. Millet.

A probabilistic approach of the reduite.

Probability and Mathematical Statistics, 13:97–121, 1992.

[9]

A. Friedman.

Stochastic Differential Equations and Applications: I.

Academic Press, 1975.

[10]

O. Göttsche and M.H. Vellekoop.

The early exercise premium for the American put under discrete

dividends.

To appear in Mathematical Finance, 2009.

[11]

S. Hamadéne and J.-P. Lepeltier.

Reflected BSDEs and mixed game problem.

Stochastic Processes and their Applications, 85:177–188, 2000.

[12]

S.D. Jacka.

Local times, optimal stopping and semimartingales.

Annals of Probability, 21:329–339, 1993.

[13]

I. Karatzas and S.E. Shreve.

Methods of mathematical finance.Applications of Mathematics, 39, Springer-Verlag, 1998.

[14]

I.J. Kim.

The analytical valuation of American options.

Review of Financial Studies, 3:547–472, 1990.

[15]

D. Lamberton.

Critical price for an American option near maturity.

Seminar on Stochastic Analysis, Random Fields and

Applications (Ascona, 1993),

Progr. Probab., 36:353–358, Birkhäuser, 1995.

[16]

H.P. McKean.

Appendix: a free boundary problem for the heat equation arising from

a problem of mathematical economics.

Ind. Management Rev., 6:32–39, 1965.

[17]

R. Myneni.

The pricing of the American option.

Annals of Applied Probability, 2(1):1–28, 1992.

[18]

G. Peskir.

A change-of-variable formula with local times on curves.

Journal of Theoretical Probability, 18:499–535, 2005.

[19]

G. Peskir.

On the American option problem.

Mathematical Finance, 15:169–181, 2005.

[20]

G. Peskir and A. Shiryaev.

Optimal Stopping and Free-Boundary Problems.

Birkhäuser, Basel, 2006.

[21]

P. Van Moerbeke.

On optimal stopping and free boundary problems.

Arch. Ration. Mech. Anal., 60:101–148, 1976.

[22]

M.H. Vellekoop and J.W. Nieuwenhuis.

Efficient Pricing of Derivatives on Assets with Discrete

Dividends.

Applied Mathematical Finance, 13(3):265–284, 2006.

[23]

M.H. Vellekoop and J.W. Nieuwenhuis.

The early exercise premium for American put options on stocks with

dividends.

Working Paper, 2009.