On refined volatility smile expansion in the Heston model

Abstract

It is known that Heston’s stochastic volatility model exhibits moment explosion, and that the critical moment can be obtained by solving (numerically) a simple equation. This yields a leading order expansion for the implied volatility at large strikes: (Roger Lee’s moment formula). Motivated by recent “tail-wing” refinements of this moment formula, we first derive a novel tail expansion for the Heston density, sharpening previous work of Drăgulescu and Yakovenko [Quant. Finance 2, 6 (2002), 443–453], and then show the validity of a refined expansion of the type , where all constants are explicitly known as functions of , the Heston model parameters, spot vol and maturity . In the case of the “zero-correlation” Heston model such an expansion was derived by Gulisashvili and Stein [Appl. Math. Optim. 61, 3 (2010), 287–315]. Our methods and results may prove useful beyond the Heston model: the entire quantitative analysis is based on affine principles: at no point do we need knowledge of the (explicit, but cumbersome) closed form expression of the Fourier transform of (equivalently: Mellin transform of ); what matters is that these transforms satisfy ordinary differential equations of Riccati type. Secondly, our analysis reveals a new parameter (“critical slope”), defined in a model free manner, which drives the second and higher order terms in tail- and implied volatility expansions.

1 Introduction

The Heston model [21] is one of the most popular stochastic volatility models used in the financial industry. Furthering its understanding, and in particular the understanding of its implied volatility surface, is of particular interest in the light of the recent financial crisis: the volatility smile (underlying: SPX) did steepen after September 2008, then flattened again; it also steepened substantially after the flash crash in April of 2010 and has since flattened again111From a private communication with a derivative trader at a major investment bank.. It is also worth recalling that the very existence of the volatility smile as we know it was triggered by the events of 1987.

This general motivation is complemented by an everyday question in the financial industry: how to (smoothly) extrapolate the smile seen in the market (typically a stepping stone towards the robust construction of a local volatility surface). Theorem 3 below contributes precisely in this direction and we derive new expansions for the implied volatility in the Heston model. Recall that its dynamics under the forward measure are given by

| (1.1) |

where , , , and with . Observe that our choice , as well as zero drift, entails no loss of generality. As is well-known (cf. [1, 2, 15, 22, 25]), the Heston model, as many other stochastic volatility models, exhibits moment explosion in the sense that

is finite for large enough. (Here and throughout the paper, denotes the risk-neutral expectation.) Differently put, for fixed maturity there will be a (finite) critical moment

(In the Heston model, and many other affine stochastic volatility models, is explicitly known. The critical moment, for fixed , is then found numerically from .) A model free result due to R. Lee, known as moment formula (cf. [4, 23]; see also [2, 3, 14, 19]), then yields

| (1.2) |

where denotes the log-strike, the Black-Scholes implied volatility, and

We remark that, subject to some “regularity” of the moment blowup (fulfilled in all practical cases; cf. [2]), the can be replaced by a genuine limit. Thus, the total implied variance is asymptotically linear in with slope . (Similar results apply in the small strike limit , but the focus of this paper is on .)

Parametric forms of the implied volatility smile used in the industry respect this behavior; a widely used parametrization is the following.

Example 1 (Gatheral’s SVI parametrization [17]).

Our main results are the following two theorems. Remark 15 in Section 3.3 and formula (4.11) in Section 4 complement them by left-tail asymptotics.

Theorem 2.

For every fixed , the distribution density of the stock price in a correlated Heston model with satisfies the following asymptotic formula:

| (1.4) |

as . The constants and are expressed explicitly in terms of critical moment and critical slope

| (1.5) |

as

| (1.6) |

An expression for is presented in Remark 12 below.

Theorem 3.

Under the assumptions of Theorem 2, the Black-Scholes implied volatility admits the expansion

| (1.7) |

as , where

Remark 4.

The restriction to is (mathematically) not essential, but allows to streamline the presentation. As is commonly noticed, this covers essentially all practical applications of the Heston model. We also note that, since , it can be helpful to think of (resp. ) as the speed of mean-reversion (resp. mean-reversion level) of the Heston variance process.

Let us draw attention to the main predecessors of this paper: Drăgulescu–Yakovenko [9] apply a saddle point argument to deduce the leading order behavior of the density in the stationary variance regime; essentially . Gulisashvili–Stein [20] study the “uncorrelated” Heston model () and find the same functional form as in (1.4) and (1.7), with (more involved) explicit expressions for . (Their method relies on representing call prices as average of Black-Scholes prices and does not apply when .) While it is easy to see that, in the case , our expressions for agree, it is checked in Appendix II (for the reader’s peace of mind) that our coincides with their expression for . In Appendix III we present a numerical example that shows the accuracy of our asymptotic formula for the density, and of the resulting implied volatility expansion.

An interesting feature of our approach, somewhat in contrast to most analytic treatments of the Heston model,222Exceptions include [10, 22]. is that our entire quantitative analysis is based on affine principles; at no point do we need knowledge of the (explicit, but cumbersome) closed form expression of the Fourier transform of or, equivalently, the Mellin transform of . (With one inconsequential exception, namely a simplification of the formula for the constant factor .) Instead, we are able to extract all the necessary information on the transform by analyzing the corresponding Riccati equations near criticality, using higher order Euler estimates.333See [16] for more information on the power of Euler estimates. In conjunction with a classical saddle point computation we then “implement” the Tauberian principle that the precise behavior of the transformed function near the singularity (the leading order of which is exactly described by the critical slope!) contains all the asymptotic information about the original function. At this heuristic level, we would expect that the critical slope , as defined in (1.5), is the key quantity that drives the second and higher order terms in tail- and implied volatility expansions of general stochastic volatility models (even in presence of jumps). Back to a rigorous level, it appears that the key ingredients of our analysis are applicable to general affine stochastic volatility models (cf. [22]), and we will take up on this in future work.

The explicit constants for in the above theorem are clearly tied to the Heston model itself. In fact, it is the explicit nature of how these constants depend on the Heston parameters , as well as spot vol and maturity , that furthers our understanding. Let us be explicit. It follows from equation (2.4) below that does not depend on (equivalently: does not depend on ; furthermore as . Moreover, the critical slope is explicitly computable: will be seen to be an explicit fraction involving only and but not (equivalently: . We see furthermore that as . As a consequence of all this, we see that changes in spot vol are second order effects: does not depend on , whereas depends linearly on it. Practically put, we see that increasing spot vol allows to up-shift the smile (intuitively obvious!) but does not affect its slopes at the extremes. We also note that changes in are not seen until looking at . No such information could be extracted from (1.2) and previous works.

Another application concerns the design of parametrizations of the implied volatility: the SVI expansion (1.3) is not compatible with the correct expansion (1.7); the latter has a constant term, , which is not present in (1.3). (We are grateful to J. Gatheral for pointing this out to us.) The solution to this apparent contradiction (recall that SVI was obtained by a analysis of the Heston smile) is simply that In fact, this suggests that SVI type parametrizations could well benefit from additional terms corresponding to such a -term; essentially accounting for the fact that .

2 Moment explosion in the Heston model

2.1 Heston model as an affine model and moment explosion

Consider the correlated Heston model given by (1.1), and set . From basic principles of affine diffusions (see, e.g., [22]) we know that

| (2.1) |

where the functions and satisfy the following Riccati equations:

| (2.2) | ||||

| (2.3) |

with and . In (2.3), and are the partial derivatives with respect to of the functions and , respectively. Our goal in Section 2 is to identify the smallest singularity, , of (2.1), and to analyze the asymptotic behavior of (2.1) in its vicinity. The estimates found will be put to use in Section 3, where we perform the asymptotic inversion of the Mellin transform of the Heston model.

Remark 5.

Given , define the explosion time for the moment of order by

An elementary computation gives

Let us also set . A typical situation in applications (a correlation parameter satisfying , and a non-zero mean reversion ) implies that is negative for . We thus assume in the sequel that

This assumption allows to use the following formula from [22, Theorem 4.2]:

| (2.4) |

2.2 Moment explosion

For , let be the (generalized) inverse of the (decreasing) function , that is

Definition 7.

Given , we call

the “critical moment”. The quantities

are called the “critical slope” and the “critical curvature”, respectively. Note that , , and depend on .

Remark 8.

The critical moment can (and in general: must) be obtained by a simple numerical root-finding procedure.

Let . We know that is the explosion time of . On the other hand, using the Riccati ODE for , we see that

Since as , we obtain

| (2.8) |

uniformly on bounded subintervals of . Next fix . Then we have with . Since the function is continuously differentiable (and even ) in , we have

| (2.9) | ||||

where is the critical slope. Hence

| (2.10) |

It follows from (2.8) and (2.10) that has a logarithmic blowup:

or

The following lemma refines these asymptotic results.

Lemma 9.

For every and for , the following formulas hold:

| (2.11) | ||||

| (2.12) |

Proof. The idea is to use (second order) Euler estimates for the Riccati ODEs near criticality; this yields the limiting behavior of and as , and we complete the proof using (2.9). More precisely, let us introduce time-to-criticality , and set . Observe that and

where . A higher order Euler scheme for this ODE yields

as and stays in a bounded interval. Since and , we obtain

It follows that

| (2.13) |

as . Note that

Hence we obtain

as For the expansion of , we find

| (2.14) |

To see the last equality, note that the integrand of

has an expansion resulting from (2.13), which may be integrated termwise [6]. It now suffices to use (2.9) and (2.14) to see that, as formula (2.12) holds.

Remark 10.

It follows easily from the proof that Lemma 9 also holds as tends to in the complex plane, provided that .

3 Mellin inversion via saddle point method

Our proof of Theorem 2 proceeds by an asymptotic analysis of , where is complex. This is the Mellin transform of the density of . As noted in Section 2.1 above, we can represent it in terms of the functions and appearing in the Riccati ODEs:

The density can be recovered using the Mellin inversion formula, that is

| (3.1) |

where , provided that is in the fundamental strip, .

Remark 11.

The integral in (3.1) exists, since its integrand decays exponentially at (see Lemma 18 in Appendix I). Moreover, if is imaginary, then the characteristic function of the random variable decays exponentially. It follows that (and therefore ) admits a smooth density. Since is (a component) of a locally elliptic diffusion with smooth coefficients, this can also be seen employing classical stochastic or PDE methods (see [7] for some recent advances in this direction).

We will deduce the asymptotics of (3.1) by the saddle point (or steepest descent) method [6, 12]. The main idea is to deform the contour of integration into a path of steepest descent from a saddle point of the integrand. In cases where the method can be applied successfully, the saddle becomes steeper and more pronounced as the parameter ( in our case) increases. We then replace the integrand with a local expansion around the saddle point. The resulting integral, taken over a small part of the contour containing the saddle point, is easy to evaluate asymptotically. Finally, it suffices to show that the tails of the original integral are negligible, in order to establish the asymptotics of the original integral. Our treatment bears similarities to Taylor expansions studied by Wright [28] and to the saddle point analysis of certain Lindelöf integrals [11]. The type of the pertinent singularity (exponential of a pole) is the same in all cases.

3.1 Finding the saddle point

A (real) saddle point of the integrand in formula (3.1) can be found by equating its derivative to zero. Since it usually suffices to calculate an approximate saddle point, we note that Lemma 9 and Remark 10 imply the following expansion, as with :

| (3.2) |

where we put and

| (3.3) |

Retaining only the dominant term of (3.2), we get the approximate saddle point equation:

or equivalently,

The solution to the previous equation,

is the approximate saddle point of the integrand.

3.2 Local expansion around the saddle point

Our next goal is to expand the function at the point . Put , and recall that we use the following notation: and . Since the (approximate) saddle point approaches as , we may find the expansion of the integrand using (3.2). To make the expansion valid uniformly w.r.t. the new integration parameter , we confine to the following small interval:

| (3.4) |

The choice of the upper bound on in (3.4) will be clear from the tail estimates obtained in Appendix I. Since , we have

| (3.5) |

It follows that

Next, plugging the previous expansions, with , into (3.2), we obtain the following asymptotic formula:

| (3.6) |

3.3 Saddle point approximation of the density

For the sake of simplicity, we will first obtain formula (1.4) with a weaker error estimate , where is arbitrary. Then it will be explained how to get the stronger estimate .

We shift the contour in the Mellin inversion formula (3.1) through the saddle point , so that

| (3.7) | ||||

| (3.8) |

The term

will yield the leading-order decay in (1.4); its exponent corresponds to the location of the dominating singularity of the Mellin transform. The lower order factors are dictated by the type of the singularity at , to be unveiled in what follows.

The “tail” of the last integral in (3.8), corresponding to , can be estimated using Lemma 20 (see Appendix I). Therefore,

Next, using (3.6) and the equality , we obtain

| (3.9) |

Evaluating the Gaussian integral, we get

| (3.10) |

Here we use the fact that the tails of the Gaussian integral are exponentially small in . Taking into account (3.9) and (3.10), we can compare the main part of the asymptotic expansion and the two error terms:

| (main part) | |||

| (error from local expansion) | |||

| (error from tail estimate) |

Since , the expression on the second line is asymptotically smaller than the main part. In addition, since , the quantity decays faster than any power of . This shows that the expression on the third line is negligible in comparison with the error term in the local expansion. Hence, it suffices to keep only the error term resulting from the local expansion. As a result, the error term in the asymptotic formula for is . (Take close to .) More precisely, using (3.9) and (3.10), we get the following formula:

| (3.11) |

It follows from (3.11) that formula (1.4), with a weaker error estimate, holds for the correlated Heston model of our interest.

Remark 12.

Our next goal is to show how to obtain the relative error in formula (1.4). Taking two more terms in the expansion (3.5) of , we get

Expanding the logarithm, we obtain

We insert these two expansions into (3.2) to obtain a refined expansion of the integrand:

| (3.12) |

for some constants . Note that the terms with and come from , those involving and from , and the one with from . (To be precise, we have used that the -term in (3.2) is of the form , as is easily seen by a third order Taylor expansion along the lines of Section 2.2.)

We will next reason as in the proof of the weaker error estimate. The main term and the error term from the tail estimate remain the same. The error term from the local expansion can be obtained as follows: Integrate the functions on both sides of formula (3.12) and take into account that

The two integrals resulting from the and -terms in (3.12) are easily calculated; they yield a relative contribution of , which merges with the term . Hence we see that the absolute error term from the local expansion is

This completes the proof of Theorem 2.

Remark 13.

Note that the preceding argument can be extended by taking more terms in the local expansion of the integrand. A full asymptotic expansion in descending powers of can thus be obtained, which replaces the error term in (1.4) by

with some constants and arbitrarily large . This is a typical feature of the saddle point method (see [12], Section VIII.3).

Remark 14.

Remark 15.

We briefly discuss the behavior of the Heston density near zero. Define the lower critical moment by

and the corresponding slope and curvature by

As , the integrand in (3.1) has a saddle point that approaches the singularity at a speed of . All steps of the subsequent analysis precisely parallel the case treated above. The net result is

| (3.13) |

as , where

4 Call pricing functions and smile asymptotics

Recall that our main result (Theorem 2) is the following asymptotic formula for the stock price distribution density in a correlated Heston model with :

| (4.1) |

as . In the present section we will characterize the asymptotic behavior of the call pricing function in such a model, and then prove Theorem 3. The following formula is a generalization of a similar result obtained for uncorrelated Heston models in [19]:

| (4.2) |

as . Formula (4.2) follows from (4.1), Theorem 7.1 in [19], and Remark 6.1 in [19]. Note that .

We will next use the tail-wing formulas obtained in [19] to study the asymptotic behavior of the Black-Scholes implied volatility in a correlated Heston model in the case where the maturity is fixed and the strike approaches infinity or zero. The following statement was established in [19], Section 7. Suppose that the stock price density in a general stock price model satisfies the condition

| (4.3) |

for all large , where , is a slowly varying function, and and are positive constants. Then for every positive function on with , we have the following:

| (4.4) |

as .

A similar assertion holds for small values of the strike price (see [19], Section 7). It can be formulated as follows: Suppose that the stock price density is such that

| (4.5) |

for all sufficiently small , where , is a slowly varying function, and and are positive constants. Let be a positive function on with . Then

| (4.6) |

as .

Remark 17.

The asymptotic formulas in (4.4) and (4.6) are equivalent to similar formulas with and , respectively. Indeed, if for some function and all functions , which tend to infinity, we have as , then as . This can be shown as follows. If the function is not bounded near infinity, then there exists a sequence such that for all . Put , and define the function by linear interpolation. Then as , but as . The proof for is similar. The authors thank Roger Lee for bringing this simple fact to their attention.

Now let us apply (4.4) and (4.6) to the Heston model. It is easy to see from (4.1) that (4.3) holds with and the slowly varying function

It follows from (4.4) and Remark 17 that

| (4.7) |

as . Next, using the mean value theorem, we see that it is possible to replace the term under the square roots in formula (4.7) by the term . Therefore,

| (4.8) |

as . Since as , formula (4.8) implies that

| (4.9) | |||

| (4.10) |

as . Next, using (4.10), we obtain the expansion (1.7) for the implied volatility , considered as a function of the forward-log-in-moneyness . Theorem 3 is thus proved. In the case where , formula (1.7) was obtained in [20] (see [20] and [19] for more details). Note that already the leading order term

gives very good numerical approximation results. This term was obtained in [2]. As a “”-statement, based on Lee’s moment formula, it appears already in [1].

Let us denote by the Black-Scholes implied total variance defined by

Then formula (1.7) implies the following expansion for :

where , , , and are the same as in (1.7).

Similar reasoning can be used in the case where . Put and

where and are defined in Remark 15. In addition, fix a positive function on with . Then (3.13) shows that all the conditions, under which formula (4.6) holds, are satisfied. Next, using (4.6) and simplifying, we obtain the following asymptotic formula for the implied volatility in the Heston model:

| (4.11) |

as . The constants in (4.11) are given by

For the total implied variance, we have

as .

Appendix I: Tail estimates

It is known [8, 26] that all the singularities of the Mellin transform of the stock price density in the Heston model are located on the real line. Therefore, the function is analytic everywhere in the complex plane except the points of singularity on the real line. The next statement justifies the application of the Mellin inversion formula in (3.8), and will be useful in the tail estimate for the saddle point method. By symmetry, it clearly suffices to consider the upper tail .

Lemma 18.

Let and . Then the following estimate holds as :

where the constant depends on , , , and .

Proof. Let and suppose . We will first estimate the function . Recall that

Set and . Then , and we have

Our goal is to show that there exists a positive continuously differentiable function on such that

| (4.12) |

where , , and is large enough. We first observe that satisfies the differential inequality

| (4.13) | ||||

| (4.14) |

for , where depends only on and . Set

Then (4.14) can be rewritten as follows:

| (4.15) |

where .

We will next find a function , with , strictly positive for , and such that the function satisfies the differential inequality

| (4.16) |

Let us first suppose that such a function exists. Then it is clear that given , the initial data match. Now we can use the ODE comparison results and derive from (4.15) and (4.16) that (4.12) holds, which implies the following estimate:

| (4.17) |

for all with large enough and .

We now look for the function satisfying the equation

where is a positive constant, and . The solution of this equation is given by

It follows that for ,

Next, choosing for which , we obtain

| (4.18) |

In (4.18), is large enough and depends only on , and hence on the model parameter and on . This shows that the function satisfies the differential inequality in (4.16), and it follows that estimates (4.12) and (4.17) hold.

Lemma 19.

If is any constant, then the portion of the integral (3.7) where is . (Recall that .)

Proof. If is a sufficiently large positive constant, then it easily follows from Lemma 18 that

(The integral is clearly .) Moreover, since the Mellin transform of does not have singularities outside the real line (see [26]), we have

This completes the proof of Lemma 19.

Lemma 19 shows that the part of the tail integral where is asymptotically much smaller than the central part. We will next estimate the whole tail integral.

Lemma 20.

The following estimate holds for the tail integral:

Proof. We will prove that there exists a constant such that the absolute value of the part of the tail integral where equals

| (4.19) |

It suffices to establish this statement, since Lemma 19 shows that the absolute value of the integral from to is asymptotically smaller than the expression in (4.19). (Indeed: Dividing (4.19) by yields , which tends to infinity. Note that by (3.4).)

It follows from Lemma 9 and Remark 10 that for some constant ,

as tends to inside the analyticity strip. More verbosely, there exists a constant such that for a sufficiently small number and for all in the analyticity strip with and , we have

Hence

We have used that the factor grows only like a power of , since

Furthermore, the quantity

| (4.20) |

decreases w.r.t. . Therefore, the integral of (4.20) can by estimated by the value of its integrand at times the length of the integration path. The latter is absorbed into , and the former is given by

(This can also by obtained by plugging into the singular expansion (3.5) computed above.) Finally, we write the factor as .

Appendix II: Comparison of constants

Since is the order of the critical moment, it is not hard to see that if , then the constant defined by is the same as the constant in [20].

We will next show that for , the constant defined in (1.6) is the same as the corresponding constant in [20]. It follows from (1.6) and from (2.7) that the constant used in the present paper for satisfies

| (4.21) |

with

We will next turn our attention to the constant in [20]. Lemmas 6.6 and 7.3 established in [20] provide an explicit expression for this constant. First note that the quantity in [20] and the quantity in the present paper are related by

| (4.22) |

This follows from the formula for in (1.6) and from Lemmas 6.6 and 7.3 in [20].

It was shown in [20], Lemmas 6.5, 6.6, and 7.3 that the following formula holds:

with

and

Hence,

Here we use the formulas for in (1.6) and in Lemma 7.3 in [20]. Since and formula (4.22) holds, we get the following relation between the constant in [20] and :

Therefore,

| (4.23) |

Next, comparing (4.21) and (4.23), we see that the constant used in the present paper coincides with the corresponding constant in [20].

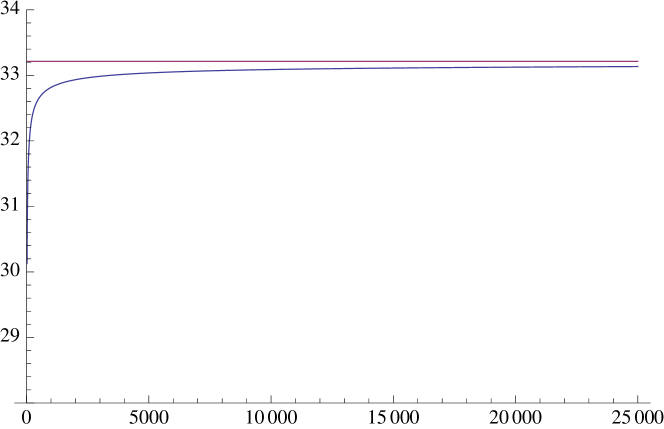

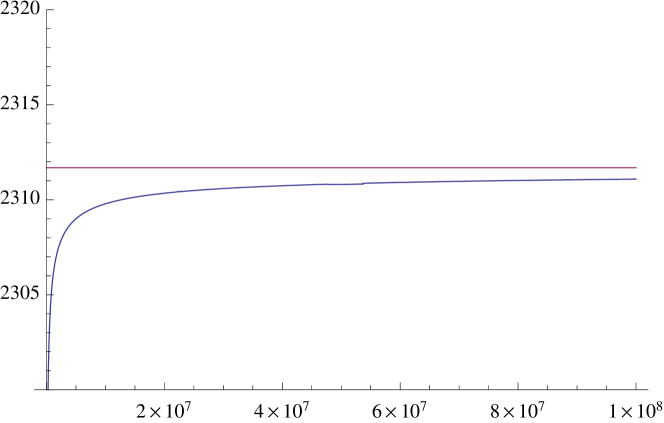

Appendix III: Numerical results

To conclude we illustrate the accuracy of (1.4) by a numerical example, and show plots of the corresponding smile approximations. We will use the parameter values (3.14). Note that (1.4) implies that

| (4.24) | |||

| (4.25) | |||

| (4.26) |

as . Figures 2–4 plot the left- and right-hand sides of (4.24)–(4.26), with on the horizontal axis. The density was evaluated by numerical integration of (3.8), using the explicit expressions [8, 21] for and .

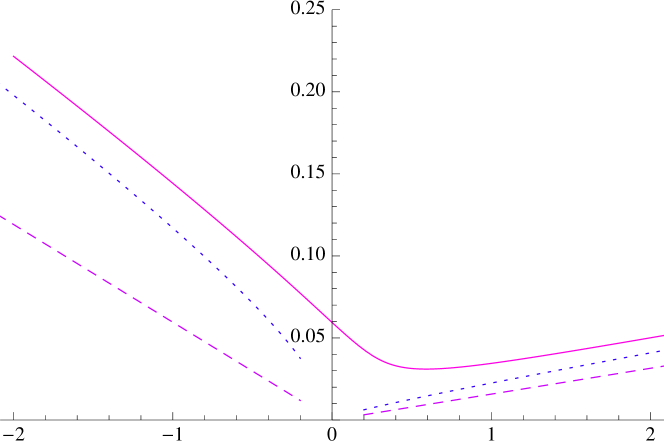

Finally, to show the accuracy of the smile asymptotics, we plot the smile together with the asymptotic approximations. This is done by simply matching Heston prices with Black-Scholes prices by means of a root-finding procedure. To evaluate the Heston prices (with initial stock price ) we use Lee’s formula [24]

where is again the log-strike and is a “damping constant” which we are free to choose, noting only that for this formula gives us call prices whereas for we get the prices of the respective puts. To optimize our results, we will use (following Lee) call options for the out-of-the-money strikes, and put options for the in-the-money strikes, both with maturity . As a good choice for the damping constant we suggest for the calls and for the puts.

The respective Black-Scholes prices are calculated by the Black-Scholes formula, evaluating the cumulative density function of the normal distribution by straightforward numerical integration.444We thank Roger Lee for helpful comments on this numerical evaluation. To get good results for deep in-the-money/out-of-the-money options, we use as starting point for the root-finding procedure the value given by our third order approximation. In the numerical example this leads to a stable evaluation of the smile in a quite large interval, e.g. log-strikes ranging from to . The results, compared with the first- and third order asymptotics, are found in Figure 5. There, the log-strike is confined to the (more realistic) interval .

References

- [1] Andersen, L. B. G., and Piterbarg, V. V. Moment explosions in stochastic volatility models. Finance Stoch. 11, 1 (2007), 29–50.

- [2] Benaim, S., and Friz, P. Smile asymptotics II: Models with known moment generating functions. J. Appl. Probab. 45, 1 (2008), 16–32.

- [3] Benaim, S., and Friz, P. Regular variation and smile asymptotics. Math. Finance 19, 1 (2009), 1–12.

- [4] Benaim, S., Friz, P., and Lee, R. W. The Black Scholes implied volatility at extreme strikes. In Frontiers in Quant. Finance: Volatility and Credit Risk Modeling. Wiley, 2008, ch. 2.

- [5] Bingham, N. H., Goldie, C. M., and Teugels, J. L. Regular variation, vol. 27 of Encyclopedia of Mathematics and its Applications. Cambridge University Press, Cambridge, 1987.

- [6] de Bruijn, N. G. Asymptotic methods in analysis, third ed. Dover Publications Inc., New York, 1981.

- [7] de Marco, S. Smoothness of densities and tail estimates for SDEs with locally smooth coefficients and applications to square-root type diffusions. Scuola Normale, Pisa, Preprint di Matematica N.3, 2009.

- [8] del Baño Rollin, S., Ferreiro-Castilla, A., and Utzet, F. A new look at the Heston characteristic function. Preprint, available at arxiv.org/abs/0902.2154, 2009.

- [9] Drăgulescu, A. D., and Yakovenko, V. M. Probability distribution of returns in the Heston model with stochastic volatility. Quant. Finance 2, 6 (2002), 443–453.

- [10] Fahrner, I. Modern logarithms for the Heston model. To be published in International Journal of Theoretical and Applied Finance, available at SSRN: http://ssrn.com/abstract=954785, 2007.

- [11] Flajolet, P., Gerhold, S., and Salvy, B. Lindelöf representations and (non-)holonomic sequences. Electronic Journal of Combinatorics (2010). To appear.

- [12] Flajolet, P., and Sedgewick, R. Analytic Combinatorics. Cambridge University Press, 2009.

- [13] Forde, M., Jacquier, A., and Mijatovic, A. Asymptotic formulae for implied volatility in the Heston model, 2009.

- [14] Friz, P. Large smile asymptotics. Encyclopedia of Quantitative Finance, Wiley, to appear, 2010.

- [15] Friz, P., and Keller-Ressel, M. Moment explosions in stochastic volatility models. Encyclopedia of Quantitative Finance, Wiley, to appear, 2010.

- [16] Friz, P., and Victoir, N. Euler estimates for rough differential equations. J. Differential Equations 244, 2 (2008), 388–412.

- [17] Gatheral, J. A parsimonious arbitrage-free implied volatility parameterization with application to the valuation of volatility derivatives. Presentation at GlobalDerivatives & Risk Management, Madrid, May 2004, available at www.math.nyu.edu/fellows_fin_math/gatheral/madrid2004.pdf.

- [18] Gatheral, J. The Volatility Surface, A Practitioner’s Guide. Wiley, 2006.

- [19] Gulisashvili, A. Asymptotic formulas with error estimates for call pricing functions and the implied volatility at extreme strikes. SIAM J. Financial Math. 1 (2010), 609–641.

- [20] Gulisashvili, A., and Stein, E. M. Asymptotic behavior of the stock price distribution density and implied volatility in stochastic volatility models. Appl. Math. Optim. 61, 3 (2010), 287–315.

- [21] Heston, S. A closed-form solution for options with stochastic volatility with applications to bond and currency options. Review of Financial Studies 6 (1993), 327–343.

- [22] Keller-Ressel, M. Moment explosions and long-term behavior of affine stochastic volatility models. To appear in Mathematical Finance, available at arxiv.org/abs/0802.1823, 2010.

- [23] Lee, R. W. The moment formula for implied volatility at extreme strikes. Math. Finance 14, 3 (2004), 469–480.

- [24] Lee, R. W. Option pricing by transform methods: Extensions, unification, and error control. Journal of Computational Finance 7, 3 (2004), 51–86.

- [25] Lions, P.-L., and Musiela, M. Correlations and bounds for stochastic volatility models. Ann. Inst. H. Poincaré Anal. Non Linéaire 24, 1 (2007), 1–16.

- [26] Lucic, V. On singularities in the Heston model. Working paper, 2007.

- [27] Schoutens, W., Simons, E., and Tistaert, J. A perfect calibration! Now what? Wilmott Magazine, 2 (2004), 66–78.

- [28] Wright, E. M. The coefficients of a certain power series. J. London Math. Soc. 7 (1932), 256–262.