Is the minimum value of an option on variance generated by local

volatility?

Mathias Beiglböck

, Peter Friz

and Stephan Sturm

Mathias BeiglböckFakultät für Mathematik, Universität WienNordbergstraße 15

1090 Wien, Austria

mathias.beiglboeck@univie.ac.atPeter Friz Institut für Mathematik, TU BerlinStraße des 17. Juni 136

10623 Berlin, Germanyand Weierstraß–Institut für Angewandte Analysis und Stochastik

Mohrenstraße 39, 10117 Berlin, Germany

friz@math.tu-berlin.de and friz@wias-berlin.deStephan SturmDepartment of Operations Research and Financial EngineeringPrinceton University116 Sherrerd Hall

Princeton, NJ 08544

ssturm@princeton.edu

Abstract.

We discuss the possibility of obtaining model-free bounds on volatility

derivatives, given present market data in the form of a calibrated local

volatility model. A counter-example to a wide-spread conjecture is given.

keywords: local vol, Dupire’s formula; MSC: 91G99; JEL: G10.

The first author acknowledges support from the Austrian Science

Fund (FWF) under grant P21209. The second and the third author (affiliated to TU Berlin while this work was started) acknowledge support by MATHEON. All authors thank Gerard Brunick, Johannes Muhle-Karbe and Walter Schachermayer for useful comments.

1. Introduction

“… it has been conjectured that the minimum possible value of an

option on variance is the one generated from a local volatility model fitted

to the volatility surface.”; Gatheral [Gat06, page 155].

Leaving precise definitions to below, let us clarify that an

option on variance refers to a derivative whose payoff is a convex

function of total realized variance. Turning from convex to concave, this

conjecture, if true, would also imply that that the maximum possible

value of a volatility swap () is the one generated from a local volatility

model fitted to the volatility surface. Given the well-documented

model-risk in pricing volatility swaps, such bounds are of immediate practical interest.

The mathematics of local volatility theory (à la Dupire, Derman, Kani, …) is intimately related to the following

Assume is a multi-dimensional Itô-process where is a multi-dimensional Brownian motion, are progressively measurable, bounded and for some ( denotes the transpose of ). Then

(1.1)

(where the power denotes the positive square root of a positive definite matrix) has a weak solution such that for all fixed .

We will apply theorem 1 only in the simple one dimensional (resp. two dimensional in section 4 below) setting where it is well known that the solution to (1.1) is unique (cf. [Kry67] or [SV06, Capter 7]).

A generic stochastic volatility model (already written under the appropriate

equivalent martingale measure and with suitable choice of numéraire) is

of the form where

is the (progressively measurable) instantaneous volatility process. (It will

suffice for our application to assume to be bounded from above and

below by positive constants.) Arguing on log-price rather than ,

(1.2)

a classical application of theorem 1 yields the following

Markovian projection result111Let us quickly remark that Markovian projection techniques have led recently

to a number of new applications (see [Pit06], for instance).: the

(weak) solution to

(1.3)

has the one-dimensional marginals of the original process .

Equivalently222The abuse of notation, by writing both and , will not cause

confusion., the process

known as (Dupire’s) local volatility model, gives rise to

identical prices of all European call options .333We emphasize that denotes the price at time of European call with maturity and strike . It easily follows

that is given by Dupire’s formula

(1.4)

Volatility derivatives are options on realized variance; that is,

the payoff is given by some function of realized variance. The latter is

given by

in the model and by

in the corresponding local volatility model.

Common choices of are , the variance swap,

, the volatility swap, or simply , a call-option on realized variance. See [FG05] for instance. As is well-known, see e.g. [Gat06], the pricing

of a variance swap, assuming continuous dynamics of such as those

specified above, is model free in the sense that it can be priced in terms

of a log-contract; that is, a European option with payoff . In

particular, it follows that

Of course this can also be seen from (1.3), after exchanging

and integration over . Passing from to for general this

is not true, and the resulting differences are known in the industry as

convexity adjustment. We can now formalize the conjecture given in the first lines of the introduction444It is tacitly assumed that are integrable..

Conjecture 1.

For any convex one has

Our contribution is twofold: first we discuss a simple (toy) example which

provides a counterexample to the above conjecture; secondly we refine our

example using a 2-dimensional Markovian projection (which may be interesting

in its own right) and thus construct a perfectly sensible Markovian

stochastic volatility model in which the conjectured result fails. All this

narrows the class of possible dynamics for for which the conjecture can

hold true and so should be a useful step towards positive answers.

2. Idea and numerical evidence

Example 2.

Consider a Black–Scholes “mixing” model with time horizon in which is given by or

depending on a fair coin flip (independent of ).

Obviously in this example, hence . On the other

hand, the local volatility is explicitly computable (cf. the following

section) and one can see from simple Monte Carlo simulations that for

thereby (numerically) contradicting conjecture 1, with .

Our analysis of this toy model is simple enough: in section 3 below we prove that . Since and is strictly convex at , Jensen’s inequality then tells us that .

The reader may note that an even simpler construction would be possible, i.e. one could simply leave out the interval where and coincide. We decided not to do so for two reasons. First, insisting on for leads to well behaved coefficients of the SDE describing the local volatility model. Second, we will use the present setup to obtain a complete model contradicting conjecture 1 at the end of the next section.

3. Analysis of the toy example

We recall that it suffices to show that is not a.s. equal to . The distribution of is

simply the mixture of two normal distributions. More explicitly, ,

where . Thus is given by555More general expression for local volatility are found in [BM06, Chapter 4] and [Lee01, HL09]. Note the necessity to keep constant on some interval ], for otherwise the local volatility surface is not Lipschitz in , uniformly as .

(3.1)

Since is bounded, measurable in and Lipschitz in (uniformly w.r.t. ) and

bounded away from zero it follows from [SV06, Theorem 5.1.1] that the

SDE

has a unique strong solution (started from , say). Since is uniformly bounded away from it follows that the

process has full support, i.e. for every

continuous

and every

Indeed, there are various ways to see this: one can apply Stroock–Varadhan’s support theorem, in the form of [Pin95, Theorem 6.3] (several simplifications arise in the proof thanks to the one-dimensionality of the present problem); alternatively, one can employ localized lower heat kernel bounds (à la Fabes–Stroock [FS86]) or exploit that the Itô-map is continuous here (thanks to Doss–Sussman, see for instance [RW00, page 180]) and deduce the support statement from the full support of .

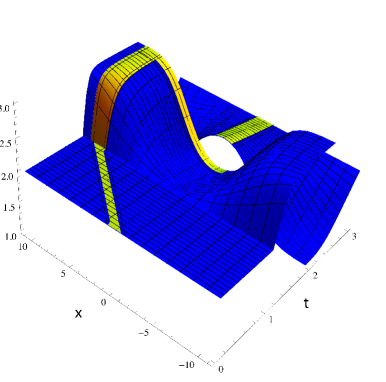

Figure 1. Time evolution of local variance in dependence of log-moneyness. The bright strip indicates a set of paths with realized variance strictly larger than .

Figure 1 illustrates the dependence of on time

and log-moneyness . To gain our end of proving that is not

constantly equal , we can determine a set of paths for which is strictly larger than . In view

of Figure 1 it is natural to consider paths which are large, i.e. , for

and small, i.e. , on the interval . A short mathematica-calculation reveals that for each such path and according to the

full-support statement the set of all such paths has positive probability,

hence is indeed not deterministic.

Using elementary analysis it is not difficult to turn numerical

evidence into rigorous mathematics. Making (3.1) explicit yields that for and that

(3.2)

(3.3)

for . We fix and observe that it is simple to see that , uniformly w.r.t. , and that , uniformly w.r.t. .

It follows that there exists some such that

Thus we obtain

(3.4)

for every path satisfying for and for .

This set of paths has positive probability and the quantity on the right side of (3.4) is strictly larger than provided that was chosen sufficiently small. Hence we find that is not constantly equal to as required.

For what it’s worth, the example can be modified such that volatility is adapted

to the filtration of the driving Brownian motion.

The trick is to choose a random sign depending solely on the behavior of and in such a way that is independent of .

For instance, if we let be the unique number satisfying , it is sensible to define if and otherwise.

We then leave the stock price process unchanged on , i.e. we define and for . On resp. we set resp.

and define as the solution of the SDE

(3.5)

Here (3.5) depends only on and the process ; since both are independent of , we obtain that and are equivalent in law.

It follows that and since and have the same law for each , they induce the same local volatility model and in particular the same (non deterministic) .

4. Counterexample for a Markovian stochastic volatility model

Recall that denotes the log-price process of a general stochastic

volatility model;

where is the (progressively

measurable) instantaneous volatility process666We note that we intend to insert later the volatility of example 2, but so far our considerations hold in general.. Recall also our standing

assumption that is bounded from above and below by positive

constants. We would like to apply theorem 1 to the 2D diffusion where keeps track of the running

realized variance777In other words,

if which we shall assume from here on.. We can only do so

after elliptic regularization. That is, we consider

where is a Brownian motion, independent of of the filtration generated by and . It follows that the following “double-local” volatility model

(with

has the one-dimensional marginals of the original process . That is, for all fixed and ,

Let us also note that the law of is the law of convolved with a standard Gaussian of mean and

variance . The log-price processes and induce the

same local volatility surface. To this end, just observe that implies identical call option prices

for all strikes and maturities and hence (by Dupire’s formula) the same

local volatility:

Since the law of a time inhomogeneous Markov process is fully specified by its generator,

it follows that the law of the local volatility process associated to has the same

law as the local volatility process associated to .

We apply this to the toy model discussed earlier. Recall that in

this example, with

whereas realized variance under the corresponding local volatilty model,

was seen to be random (but with mean , thanks to the matching

variance swap prices). As a particular consequence, using Jensen

We claim that this persists when replacing the abstract stochastic

volatility model by , the first component of a 2D Markov diffusion, for any . Indeed, thanks to the identical laws of the respective local volatility processes the

left-hand side above does not change when replacing by the local volatility process associated to . On the other hand

Thus, insisting again that the process is (in law) the local

volatility model associated to the double local volatility model we

see that

(Observe that is independent of .) Using the Lipschitz property of the hockeystick function, again Gyöngy and the fact that is normally distributed with mean and variance we can conclude that

Now we choose small enough such that , whence the conjecture fails to hold true in the double local volatility model for small enough.

5. Conclusion

Summing up, the double-local volatility model constitutes an example of a continuous

2D Markovian stochastic volatility model, where stochastic volatility is a

function of both state variables, in which conjecture 1 fails,

i.e. in which the minimal possible value of a call option is not generated by a local volatility model.

References

[BM06] D. Brigo and F. Mercurio.

Interest rate models—theory and practice.

Springer Finance.

Springer-Verlag, Berlin, second edition, 2006.

With smile,

inflation and credit.

[FS86]

E. B. Fabes and D. W. Stroock.

A new proof of Moser’s parabolic Harnack inequality using the old

ideas of Nash.

Arch. Rational Mech. Anal., 96(4):327–338, 1986.

[FG05]

P. Friz and J. Gatheral.

Valuation of volatility derivatives as an inverse problem.

Quant. Finance, 5(6):531–542, 2005.

[Gat06] J. Gatheral.

The volatility surface: a

practitioner’s guide.

WILEY, 2006.

[Gyö86] I. Gyöngy.

Mimicking the

one-dimensional marginal distributions of processes having an Itô

differential.

Probab. Theory Relat. Fields, 71(4):501–516,

1986.

[HL09]

P. Henry-Labordère.

Calibration of local stochastic volatility models to market smiles.

Risk magazine, 04 Sept. 2009.

[Kry67]

N. V. Krylov.

The first boundary value problem for elliptic equations of second

order.

Differencial nye Uravnenija, 3:315–326, 1967.

[Lee01]

R. Lee.

Implied and local volatilities under stochastic volatility.

International Journal of Theoretical and Applied Finance, vol

4:45–89, 2001.

[Pin95] R. G. Pinsky.

Positive harmonic

functions and diffusion, volume 45 of Cambridge Studies in Advanced

Mathematics.

Cambridge University Press, Cambridge, 1995.

[Pit06]

V. Piterbarg.

Markovian projection method for volatility calibration.

Available at SSRN: http://ssrn.com/abstract=906473, 2006.

[RW00]

L. C. G. Rogers and D. Williams.

Diffusions, Markov processes, and martingales. Vol. 1.

Cambridge Mathematical Library. Cambridge University Press,

Cambridge, 2000.

Foundations, Reprint of the second (1994) edition.

[SV06] D. W. Stroock and S. R. Srinivasa Varadhan.

Multidimensional diffusion processes.

Classics in

Mathematics. Springer-Verlag, Berlin, 2006.

Reprint of the 1997

edition.