Variance Estimation Using Refitted Cross-validation in Ultrahigh Dimensional Regression

Abstract

Variance estimation is a fundamental problem in statistical modeling. In ultrahigh dimensional linear regression where the dimensionality is much larger than sample size, traditional variance estimation techniques are not applicable. Recent advances on variable selection in ultrahigh dimensional linear regression make this problem accessible. One of the major problems in ultrahigh dimensional regression is the high spurious correlation between the unobserved realized noise and some of the predictors. As a result, the realized noises are actually predicted when extra irrelevant variables are selected, leading to serious underestimate of the noise level. In this paper, we propose a two-stage refitted procedure via a data splitting technique, called refitted cross-validation (RCV), to attenuate the influence of irrelevant variables with high spurious correlations. Our asymptotic results show that the resulting procedure performs as well as the oracle estimator, which knows in advance the mean regression function. The simulation studies lend further support to our theoretical claims. The naive two-stage estimator and the plug-in one stage estimators using LASSO and SCAD are also studied and compared. Their performances can be improved by the proposed RCV method.

Keywords: Data splitting; Dimension reduction; High dimensionality; Refitted cross-validation; Sure Screening; Variance estimation; Variable selection.

Dedicated to Peter J. Bickel on his occasion of the 70th birthday.

1 Introduction

Variance estimation is a fundamental problem in statistical modeling. It is prominently featured in the statistical inference on regression coefficients. It is also important for variable selection criteria such as AIC and BIC. It provides also a benchmark of forecasting error when an oracle actually knows the regression function and such a benchmark is very important for forecasters to gauge their forecasting performance relative to the oracle. For conventional linear models, the residual variance estimator usually performs well and plays an important role in the inferences after model selection and estimation. However, the ordinary least squares methods don’t work for many contemporary datasets which have more number of covariates than the sample size. For example, in disease classification using microarray data, the number of arrays is usually in tens, yet tens of thousands of gene expressions are potential predictors. When interactions are considered, the dimensionality grows even more quickly, e.g. considering possible interactions among thousands of genes or SNPs yields the number of parameters in the order of millions. In this paper, we propose and compare several methods for variance estimation in the setting of ultrahigh dimensional linear model. A key assumption which makes the high dimensional problems solvable is the sparsity condition: the number of nonzero components is small compared to the sample size. With sparsity, variable selection can identify the subset of important predictors and improve the model interpretability and predicability.

Recently, there have been several important advances in model selection and estimation for ultrahigh dimensional problems. The properties of penalized likelihood methods such as the LASSO and SCAD have been extensively studied in high and ultrahigh dimensional regression. Various useful results have been obtained. See, for example, Fan and Peng (2004); Zhao and Yu (2006); Bunea et al. (2007); Zhang and Huang (2008); Meinshausen and Yu (2009); Kim et al. (2008); Meier et al. (2008); Lv and Fan (2009); Fan and Lv (2009). Another important model selection tool is the Dantzig selector proposed by Candes and Tao (2007) which can be easily recast as a linear program. It is closely related to LASSO, as demonstrated by Bickel et al. (2009). Fan and Lv (2008) showed that correlation ranking possesses a sure screening property in the Gaussian linear model with Gaussian covariates and proposed a sure independent screening (SIS) and iteratively sure independent screening (ISIS) method. Fan et al. (2009) extended ISIS to a general pseudo-likelihood framework, which includes generalized linear models as a special case. Fan and Song (2010) have developed general conditions under which the marginal regression possesses a sure screening property in the context of generalized linear model. For an overview, see Fan and Lv (2010).

In all the work mentioned above, the primary focus is the consistency of model selection and parameter estimation. The problem of variance estimation in ultrahigh dimensional setting has hardly been touched. A natural approach to estimate the variance is the following two-stage procedure. In the first stage, a model selection tool is applied to select a model which, if is not exactly the true model, includes all important variables with moderate model size (smaller than the sample size). In the terminology of Fan and Lv (2008), the selected model has a sure screening property. In the second stage, the variance is estimated by ordinary least squares method based on the selected variables in the first stage. Obviously, this method works well if we are able to recover exactly the true model in the first stage. This is usually hard to achieve in ultrahigh dimensional problems. Yet, sure screening properties are much easier to obtain. Unfortunately, this naive two-step approach can seriously underestimate the noise level even with the sure screening property in the first stage due to spurious correlation inherent in ultrahigh dimensional problems. When the number of irrelevant variables is huge, some of these variables have large sample correlations with the realized noises. Hence, almost all variable selection procedures will, with high probability, select those spurious variables in the model when the model is over fitted, and the realized noises are actually predicted by several spurious variables, leading to serious underestimate of the residual variance.

The above phenomenon can be easily illustrated in the simplest model, in which the true coefficient . Suppose that one extra variable is selected by a method such as the LASSO or SIS in the first stage. Then, the ordinary least squares estimator is

| (1) |

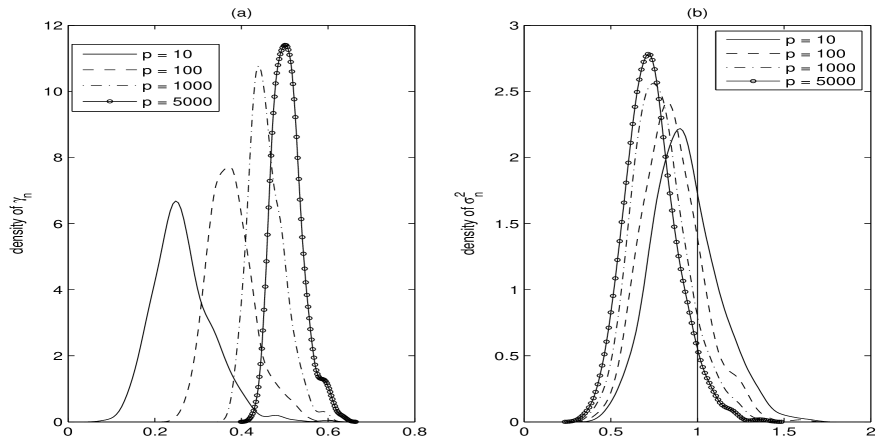

where is the sample correlation of the spurious variable and the response, which is really the realized noise in this null model. Most variable selection procedures such as stepwise addition, SIS and LASSO will first select the covariate that has highest sample correlation with the response, namely, . In other words, this extra variable is selected to best predict the realized noise vector. However, as Fan and Lv (2008) stated, the maximum absolute sample correlation can be very large, which makes seriously biased. To illustrate the point, we simulated 500 data sets with sample size and the number of covariates , , and , with and noise from the standard normal distribution. Figure 1(a) presents the densities of across the 500 simulations and Figure 1(b) depicts the densities of the estimator defined in (1). Clearly, the biases of become larger as increases.

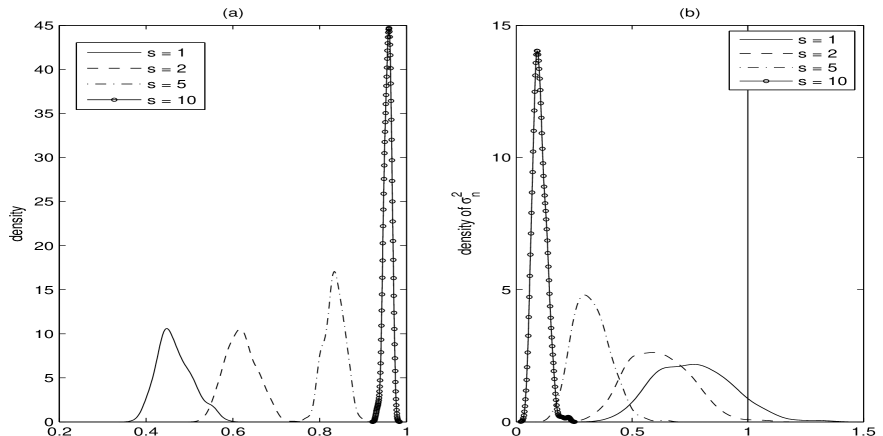

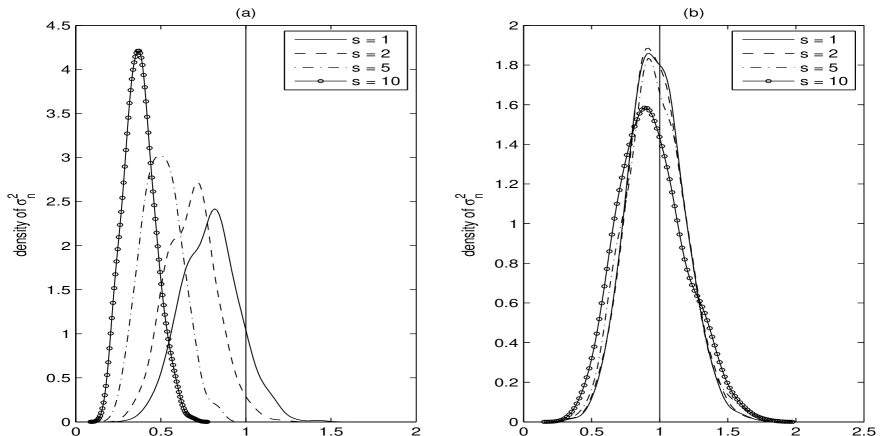

The bias gets larger when more spurious variables are recruited in the model. To illustrate the point, let us use the stepwise addition to recruit variables to the model. Clearly, the realized noises are now better predicted, leading to even more severe underestimate of the noise level. Figure 2 depicts the distributions of spurious multiple correlation with the response (realized noise) and the corresponding naive two-stage estimator of variance for and , keeping fixed. Clearly, the biases get much larger with . For comparison, we also depict similar distributions based on SIS, which selects variables that are marginally most correlated with the response variable. The results are depicted in Figure 3 (a). While the biases based on the SIS method are still large, they are smaller than those based on the stepwise addition method, as the latter chose the coordinated spurious variables to optimize the prediction of the realized noise.

A similar phenomenon was also observed in classical model selection by Ye (1998). To correct the effects of model selection, Ye (1998) developed a concept of generalized degree of freedom (GDF) but it is computationally intensive and can only be applied to some special cases.

To attenuate the influence of spurious variables entered into the selected model and to improve the estimation accuracy, we introduce a refitted cross-validation (RCV) technique. Roughly speaking, we split the data randomly into two halves, do model selection using the first half dataset, and refit the model based on the variables selected in the first stage, using the second half data, to estimate the variance, and vice versa. The proposed estimator is just the average of these two estimators. The results of the RCV variance estimators with and 10 are presented in Figure 3(b). The corrections of biases due to spurious correlation are dramatic. The essential difference of this approach and the naive two-stage approach is that the regression coefficients in the first stage are discarded and refitted using the second half data and hence the spurious correlations in the first stage are significantly reduced at the second stage. The variance estimation is unbiased as long as the selected models in the first stage contain all relevant variables, namely, possess a sure screening property. It turns out that this simple RCV method improves dramatically the performance of the naive two-stage procedure. Clearly, the RCV can also be used to do model selection itself, reducing the influence of spurious variables.

To appreciate why, suppose a predictor has a big sample correlation with the response (realized noise in the null model) over the first half dataset and is selected into the model by a model selection procedure. Since the two halves of the dataset are independent and the chance that a given predictor is highly correlated with realized noise is small, it is very unlikely that this predictor has a large sample correlation with the realized noise over the second half of the dataset. Hence, its impact on the variance estimation is very small when refitted and estimating the variance over the second half will not cause any bias. The above argument is also true for the non-null models provided that the selected model includes all important variables.

To gain better understanding of the RCV approach, we compare our method with the direct plug-in method, which computes the residual variance based on a regularized fit. This is inspired by Greenshtein and Ritov (2004) on the persistence of the LASSO estimator. An interpretation of their results is that such an estimator is consistent. However, there is a bias term of order inherent in the LASSO-based estimator, when the regularization parameter is optimally tuned. When the bias is negligible, the LASSO based plug-in estimator is consistent. The plug-in variance estimation based on the general folded-concave penalized least squares estimators such as SCAD are also discussed. In some cases, this method is comparable with the RCV approach.

The paper is organized as following. Section 2 gives some additional insights into the challenges of high dimensionality in variance estimation. In Section 3, the RCV variance estimator is proposed and its sampling properties are established. Section 4 studies the variance estimation based penalized likelihood methods. Extensive simulation studies are conducted in Section 5 to illustrate the advantage of the proposed methodology. Section 6 is devoted to a discussion and the detailed proofs are provided in the Appendix.

2 Insights into challenges of High Dimensionality in variance estimation

Consider the usual linear model

| (2) |

where is an -vector of responses, is an matrix of independent and identically distributed () variables ,…, , is a -vector of parameters and is an -vector of random noises with mean 0 and variance . We always assume the noise is independent of predictors. For any index set , denotes the sub-vector containing the components of the vector that are indexed by , denotes the sub-matrix containing the columns of that are indexed by , and is the projection operator onto the linear space generated by the column vectors of .

When or , it is often assumed that the true model is sparse, i.e. the number of non-zero coefficients is small. It is usually assumed that is fixed or diverging at a mild rate. Under various sparsity assumptions and regularity conditions, the most popular variable selection tools such as LASSO, SCAD, adaptive LASSO, SIS and Dantzig selector possess various good properties regarding model selection consistency. Among these properties are the sure screening property, model consistency, sign consistency, weak oracle property and oracle property, from weak to strong. Theoretically, under some regularity conditions, all aforementioned model selection tools can achieve model consistency. In other words, they can exactly pick out the true sparse model with probability tending to one. However, in practice, these conditions are impossible to check and hard to meet. Hence, it is often very difficult to extract the exact subset of significant variables among a huge set of covariates. One of reasons is the spurious correlation, as we now illustrate.

Suppose that unknown to us the true data generating process in model (2) is

where is the -dimensional vector of the realizations of the covariate . Furthermore, let us assume that and follow independently the standard normal distribution. As illustrated in Figure 1(a), where is large, there are realizations of variables that have high correlations with . Let us say . Then, can even have a better chance to be selected than . Here and hereafter, we refer the spurious variables to those variables selected to predict the realized noise and their associated sample correlations are called spurious correlations.

Continued with the above example, the naive-two stage estimator will work well when the model selection is consistent. Since we may not get model consistency in practice and have no way to check even if we get it by chance, it is natural to ask whether the naive two-stage strategy works if only sure screening can be achieved in the first stage. In the aforementioned example, let us say a model selector chooses the set , which contains all true variables. However, in the naive two-stage fitting, is used to predict , resulting in substantial underestimate of . Upon both variables and are selected, all spurious variables are recruited to predict . The more spurious variables are selected, the better is predicted, the more serious underestimation of by the naive two stage estimation.

We say a model selection procedure satisfies sure screening property if the selected model with model size includes the true model with probability tending to one. Explicitly,

The sure screening property is a crucial criterion when evaluating a model selection procedure for high or ultrahigh dimensional problems. Among all model consistent properties, the sure screening property is the weakest one and the easiest to achieve in practice.

Let us demonstrate the naive two-stage procedure in detail. Assume that the selected model in the first stage includes the true model . The ordinary least squares estimator at the second stage, using only the selected variables in , is

| (3) |

where is the identity matrix. How does this estimator perform? To facilitate the notation, denote the naive estimator by . Then, the estimator (3) can be written as

where Let us analyze the asymptotic behavior of this naive two-stage estimator.

Theorem 1

Under the assumptions (A1)-(A2) together with (A3)-(A4) or (A5)-(A6) in the Appendix, we have

-

1.

If a procedure satisfies the sure screening property with where is given in Assumption (A2), then converges to in probability as . Furthermore,

where ‘’ stands for ‘convergence in distribution’.

-

2.

If, in addition, , then .

It is perhaps worthwhile to make a remark about Theorem 1. plays an important role on the performance of . It represents the fraction of bias in . The slower converges to zero, the worse performs. Moreover, if converges to a positive constant with a non-negligible probability, it will lead to an inconstant estimator. The estimator can not be root-n consistent if . This explains the poor performance of , as demonstrated in Figures 2 and 3. While Theorem 1 gives an upper bound of , it is often sharp. For instance, if and are standard normal distribution and , then is just the maximum absolute sample correlation between and . Denote the th sample correlation by , . Applying the transformation , we get a sequence with Student’s distribution with degrees of freedom. Simple analysis on the extreme statistics of the sequences and shows that for any such that , we have

| (4) |

which implies the sharpness of Theorem 1 in this specific case. Furthermore, when ,

with the limiting distribution is given by

| (5) |

where . See Appendix A.5 for details.

3 Variance estimation based on refitted cross-validation

3.1 Refitted cross-validation

In this section, we introduce the refitted cross-validation method to remove the influence of spurious variables in the second stage. The method requires only that the model selection procedure in stage one has a sure screening property. The idea is as follows. We assume the sample size is even for simplicity and split randomly the sample into two groups. In the first stage, an ultrahigh dimensional variable selection method like SIS is applied to these two datasets separately, which yields two small sets of selected variables. In the second stage, the ordinary least squares (OLS) method is used to re-estimate the coefficient and variance . Different from the naive two-stage method, we apply again OLS to the first subset of the data with the variables selected by the second subset of the data and vice versa. Taking the average of these two estimators, we get our estimator of . The refitting in the second stage is fundamental to reduce the influence of the spurious variables in the first stage of variable selection.

To implement the above idea of the refitted cross-validation, consider a dataset with sample size , which is randomly split to two even datasets and . First, a variable selection tool is performed on and let denote the set of selected variables. The variance is then estimated on the second dataset , namely,

where . Similarly, we use the dataset two to select the set of important variables and the first dataset for estimation of , resulting in

We define the final estimator as

| (6) |

An alternative is the weighted average defined by

| (7) |

When , we have .

In the above procedure, although includes some extra unimportant variables besides the important ones, these extra variables will play minor roles when we estimate using the second dataset along with refitting since they are just some random unrelated variables over the second dataset. Furthermore, even when some important variables are missed in the first stage of model selection, they have a good chance being well approximated by the other variables selected in the first stage to reduce modeling biases. Thanks to the refitting in the second stage, the best linear approximation of those selected variables is used to reduce the biases. Therefore, a larger selected model size gives us not only a better chance of sure screening, but also a way to reduce modeling biases in the second stage when some important variables are missing. This explains why the RCV method is relatively insensitive to the selected model size, demonstrated in Figures 3 and 6 below. With a larger model being selected in the stage one, we may lose some degrees of freedom and hence get an estimator with slightly larger variance than the oracle one at finite sample. Nevertheless, the RCV estimator performs well in practice and asymptotically optimal when . The following theorem gives the property of the RCV estimator. It requires only a sure screening property, studied by Fan and Lv (2008) for normal multiple regression, Fan and Song (2010) for generalized linear models, and Zhao and Li (2010) for Cox regression model.

Theorem 2

Assume the regularity conditions (A1) and (A2) hold and . If a procedure satisfies the sure screening property with and , then

| (8) |

Theorem 2 reveals that the RCV estimator of variance has an oracle property. If the regression coefficient is known by oracle, then we can compute the realized noise and get the oracle estimator

| (9) |

This oracle estimator has the same asymptotic variance as .

There are two natural extensions of the aforementioned refitted cross-validation techniques.

K-fold data splitting: The first natural extension is to use K-fold data splitting technique rather than two-fold spliting. We can divide the data into K groups, select the model with all groups except one, which is used to estimate the variance with refitting. We may improve the sure screening probability with this K-fold method since there are now more data in the first stage. However, there are only data points on the second stage for refitting. This means that the number of variables selected in the first stage should be much less than . This makes the ability of sure screening hard in the first stage. For this reason, we work only on the two-fold refitted cross-validation.

Repeated data splitting: There are many ways to randomly split the data. Hence, many RCV variance estimators can be obtained. We may take the average of the resulting estimators. This reduces the influence of the randomness in the data splitting.

Remark 1. The RCV procedure provides an efficient method for variance estimation. Those technical conditions in Theorem 2 may not be weakest possible. They are imposed to facilitate the proofs. In particular, we assume that for all , which implies that the selected variables in stage one are not highly correlated. Other methods beyond least squares can be applied in the refitted stage when those assumptions are possibly violated in practice. For instance, if some selected variables in stage one are highly correlated or the selected model size is relatively large, ridge regression or penalization methods can be applied in the refitted stage. Moreover, if the density of the error seems heavy-tailed, some classical robust methods can also be employed.

Remark 2. The paper focuses on variance estimation under the exact sparsity assumption and sure screening property. It is possible to extend our results to nearly sparse cases. For example, the parameter is not sparse but satisfies some decay condition such as for some positive constant . In this case, we do not have to worry too much whether a model selection procedure can recover small parameters. In this case, so long as a model selection method can pick up a majority of all variables with large coefficients in the first stage, we would expect that the RCV estimator performs well.

3.2 Applications

Many statistical problems require the knowledge of the residual variance, especially for high or ultra-high dimensional linear regression. Here we brief a couple of applications.

(a) Constructing confidence intervals for coefficients. A natural application is to use estimated to construct confidence intervals for non-vanishing estimated coefficients. For example, it is well known that the SCAD estimator possesses an oracle property (Fan and Li, 2001; Fan and Lv, 2009). Let be the SCAD estimator, with corresponding design matrix . Then, for each , confidence interval for is

| (10) |

in which is the diagonal element of the matrix that corresponds to the variable. Our simulation studies show that such a confidence interval is accurate and has a similar performance to the case where is known.

The confidence intervals can also be constructed based on the raw materials in the refitted cross validation. For example, for each element in , we can take the average of the refitted coefficients as the estimate of the regression coefficients in the set , and as the corresponding estimated covariance matrix, where is computed based on the first half of the data at the refitting stage and is computed based on the second half of the data. In addition, some ‘cleaning’ techniques through -values can be also applied here. In particular, Wasserman and Roeder (2009) and Meinshausen, et al. (2009) studied these techniques to reduce the number of falsely selected variables substantially.

(b) Genomewide association studies. Let be the coding of the th Single Nucleotide Polymorphism (SNP) and be the observed phenotype (e.g. height or blood pressure) or the expression of a gene of interest. In such a quantitative trait loci (QTL) or eQTL study, one frequently fits the marginal linear regression

| (11) |

based on a sample of size individuals, resulting in the marginal least-squares estimate . The interest is to test simultaneously the hypotheses . If the conditional distribution of given is , then it can easily be shown (Han et al., 2010) that , where the element of S is the sample covariance matrix of and divided by their sample variances. With estimated by the RCV, the P-value for testing individual hypothesis can be computed. In addition, the dependence of the least-squares estimates is now known and hence the false discovery proportion or rate can be estimated and controlled (Han et al., 2010).

(c) Model selection. Popular penalized approaches for variable selection such as LASSO, SCAD, adaptive LASSO and elastic-net often involve the choice of tuning or regularization parameter. A proper tuning parameter can improve the efficiency and accuracy for variable selection. Several criteria, such as Mallaw’s , AIC and BIC, are constructed to choose tuning parameters. All these criteria rely heavily on a common parameter, the error variance. As an illustration, consider estimating the tuning parameter of LASSO (See also Zou, et al. (2007)). Let be the tuning parameter with the fitted value . Then AIC and BIC for the LASSO are written as

and

It is easily seen that the variance has an important impact on both AIC and BIC.

4 Folded-concave Penalized least squares

In this section, we discuss some related methods on variance estimation and their corresponding asymptotic properties. The oracle estimator of is

A natural candidate to estimate the variance is , where is the LASSO or SCAD estimator of . Greenshtein and Ritov (2004) showed the persistent property for the LASSO estimator . Their result, interpreted in the linear regression setting, implies in probability, where . In fact, it is easy to see that their result implies

In other words, is a consistent estimator for the variance.

Recall the LASSO estimator is defined as

| (12) |

To make consistent, Greenshtein and Ritov (2004) suggested asymptotically. Wasserman and Roeder (2009) showed the consistency still holds when is chosen by cross-validation. Therefore, we define the LASSO variance estimator by

| (13) |

where .

We shall see that usually underestimates the variance due to spurious correlation, as the LASSO shares a similar spirit of the stepwise addition (see the LARS algorithm by Efron et al. (2004)). Thus, we also consider the leave-one-out LASSO variance estimator

| (14) |

where is the LASSO estimator using all samples except the th one. In practice, -fold ( equals or ) cross-validated LASSO estimator is often used and shares the same spirit as (14). We divide the dataset into parts, say and define

| (15) |

where is the LASSO estimator using all data except ones in with tuning parameter . This estimator differs from the plug-in method (13) in that multiple estimates from training samples are used to compute residuals from the testing samples. We will see that the estimator is typically closer to than , but it usually somewhat overestimates the true variance from our simulation experience. The following theorem shows the convergence rate for the LASSO estimator.

Theorem 3

Suppose the assumptions (A1) - (A4) and (A7) hold. If the true model size for some , then, we have

If , we have

The factor reflects the bias of the penalized -estimator. It can be non-negligible. When it is negligible, the plug-in LASSO estimator possesses also the oracle property. In general, it is difficult to study the asymptotic distribution of the LASSO estimator when the bias is not negligible. In particular, we can not obtain the standard error for the estimator. Even for finite , Knight and Fu (2000) investigated the asymptotic distribution of LASSO-type estimators but it is too complicated to be applied for inference. To tackle this difficulty, Park and Casella (2008) and Kyung, et al. (2010) used the hierarchical Bayesian formulation to produce a valid standard error for LASSO estimator, and Chatterjee and Lahiri (2010) proposed a modified bootstrap method to approximate the distribution of LASSO estimator. But it is unclear yet whether or not their methods can be applied to high or ultra-high dimensional setting.

Recently, Fan and Lv (2009) studied the oracle properties of non-concave penalized likelihood method in the ultrahigh dimensional setting. Inspired by their results, the variance can be consistently and efficiently estimated. The SCAD penalty (Fan and Li, 2001) is the function whose derivative is given by

where is often used. Denote by

| (16) |

and let be a local minimizer of with respect to . Thus, the variance can be estimated by

where .

The following theorem shows the oracle property and convergence rate for the SCAD estimator.

Theorem 4

Assume and the true model size , where . Suppose that the assumptions (A1), (A3)-(A4) (or (A5)-(A6)) and (A8)-(A9) in the Appendix are satisfied. Then,

-

1.

(Model Consistency) There exists a strictly local minimizer of such that

with probability tending to one;

-

2.

(Asymptotic Normality) With this estimator , we have

Theorem 4 reveals that, if is chosen reasonably, works as well as the RCV estimator and better than . However, it is hard to achieve this oracle property sometimes.

5 Numerical Results

5.1 Simulation Study

In this section, we illustrate and compare the finite sample performance of the methods described in the last three sections. We applied these methods to three examples: the null model and two sparse models. The null model (Example 1) is given by

| (17) |

where , , , are random variables, following the standard Gaussian distribution. This is the sparsest possible model. The second sparse model (Example 2) is given by

| (18) |

with different representing different levels of signal-to-noise ratio (SNR). The covariates associated with model (18) are jointly normal with equal correlation , and marginally .

The third sparse model (Example 3) is more challenging, with 10 nontrivial coefficients, . The covariates are jointly normal with . The nonzero coefficients vector is

where b varies to fit different SNR levels. The random error follows the standard normal distribution.

In each of these settings, we test the following four methods to estimate the variance.

Method 1: Oracle estimator (9), which is not a feasible estimator whose performance provides a benchmark.

Method 2: Naive two-stage method, denoted by N-SIS, if SIS is employed in the model selection step.

Method 3: Refitted cross-validation variance estimator (6), denoted by RCV.

Method 4: One step method via penalized least squares estimators. We introduced this method in Section 4 and recommended two formulas to estimate the variance, direct plug-in method (P) like formula (13) and cross-validation method (CV) like formula (15).

In methods 2–4, we employed (I)SIS, SCAD, LASSO as our model selection tools. For SCAD and LASSO, the tuning parameters were chosen by 5-fold or 10-fold cross-validation. For (I)SIS, the predetermined model size is always taken to be 5 in the null model and in the sparse model, unless specified explicitly. The principled method of Zhao and Li (2010) can be employed to automatically choose the model size.

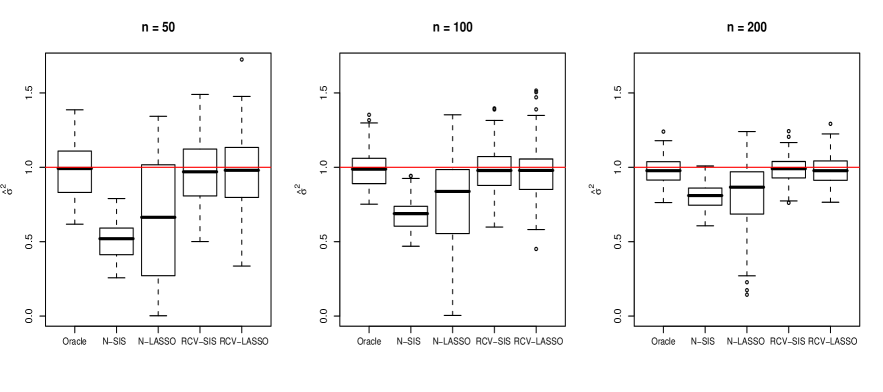

Example 1. Assume the response is independent of all predictors ’s, which follow standard Gaussian distribution. We consider the cases when numbers of covariates vary from 10, 100 to 1000 and the sample sizes equal 50, 100 and 200. The simulation results are based on 100 replications and summarized in Table 1. In Figure 4, three boxplots are listed to compare the performance of different methods for the case and . From the simulation results, we can see the improved two-stage estimators (RCV-SIS and RCV-LASSO) are comparable with the oracle estimator and much better than the naive ones, especially in the case when . This coincides with our theoretical result. RCV improves dramatically the naive (natural) method, no matter SIS or LASSO is used.

| Method | BIAS | SE | AMS | BIAS | SE | AMS | BIAS | SE | AMS |

|---|---|---|---|---|---|---|---|---|---|

| Oracle | 0.006 | 0.220 | 0 | -0.023 | 0.144 | 0 | -0.015 | 0.109 | 0 |

| N-SIS | -0.072 | 0.209 | 5 | -0.064 | 0.142 | 5 | -0.030 | 0.109 | 5 |

| RCV-SIS | 0.017 | 0.234 | 5 | -0.029 | 0.150 | 5 | -0.013 | 0.114 | 5 |

| N-LASSO | -0.052 | 0.211 | 1.08 | -0.051 | 0.148 | 1.01 | -0.028 | 0.108 | 0.94 |

| RCV-LASSO | -0.003 | 0.219 | 1.41 | -0.026 | 0.149 | 1.24 | -0.015 | 0.110 | 1.02 |

| Method | BIAS | SE | AMS | BIAS | SE | AMS | BIAS | SE | AMS |

| Oracle | -0.011 | 0.205 | 0 | 0.023 | 0.154 | 0 | -0.010 | 0.154 | 0 |

| N-SIS | -0.325 | 0.151 | 5 | -0.164 | 0.135 | 5 | -0.112 | 0.135 | 5 |

| RCV-SIS | -0.004 | 0.216 | 5 | 0.018 | 0.165 | 5 | -0.009 | 0.165 | 5 |

| N-LASSO | -0.272 | 0.319 | 5.90 | -0.153 | 0.279 | 13.56 | -0.073 | 0.279 | 3.16 |

| RCV-LASSO | 0.032 | 0.359 | 4.67 | 0.022 | 0.171 | 5.89 | -0.010 | 0.171 | 12.41 |

| Method | BIAS | SE | AMS | BIAS | SE | AMS | BIAS | SE | AMS |

| Oracle | -0.011 | 0.176 | 0 | -0.015 | 0.130 | 0 | -0.015 | 0.095 | 0 |

| N-SIS | -0.488 | 0.118 | 5 | -0.314 | 0.098 | 5 | -0.192 | 0.079 | 5 |

| RCV-SIS | -0.017 | 0.211 | 5 | -0.018 | 0.144 | 5 | -0.012 | 0.098 | 5 |

| N-LASSO | -0.351 | 0.399 | 7.47 | -0.256 | 0.330 | 9.37 | -0.196 | 0.251 | 9.90 |

| RCV-LASSO | -0.029 | 0.266 | 5.03 | -0.022 | 0.186 | 8.27 | -0.014 | 0.103 | 8.79 |

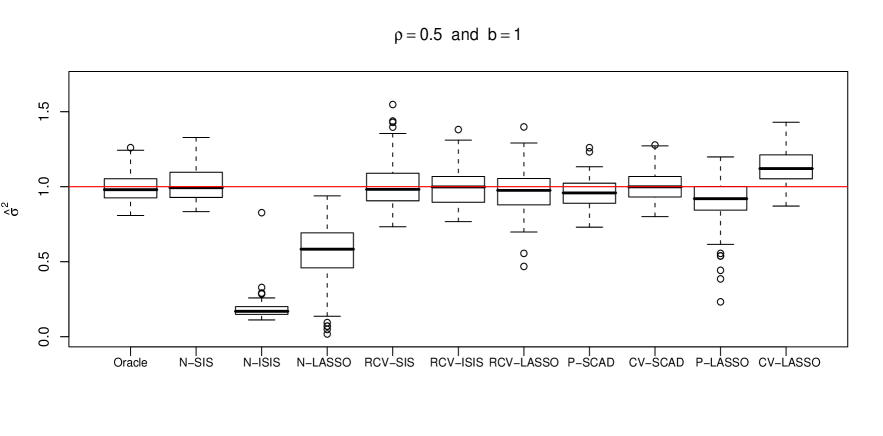

Example 2. We now consider the the model (18) with , and . Moreover, we consider three values of coefficients , and , corresponding to different levels of SNR , and for each case when . The results depicted in Table 2 are based on 100 replications (The results for are presented in Figure 5 and are omitted from the table). The boxplots of all estimators for the case and are shown in Figure 5. They indicate that the RCV methods behave as well as oracle, and much better than naive two-stage methods. Furthermore, the performance of the naive two-stage method depends highly on the model selection technique. The one-step methods perform also well, especially P-SCAD and CV-SCAD. P-LASSO and CV-LASSO behave slightly worse than SCAD methods. These simulation results lend further support to our theoretical conclusions in earlier sections.

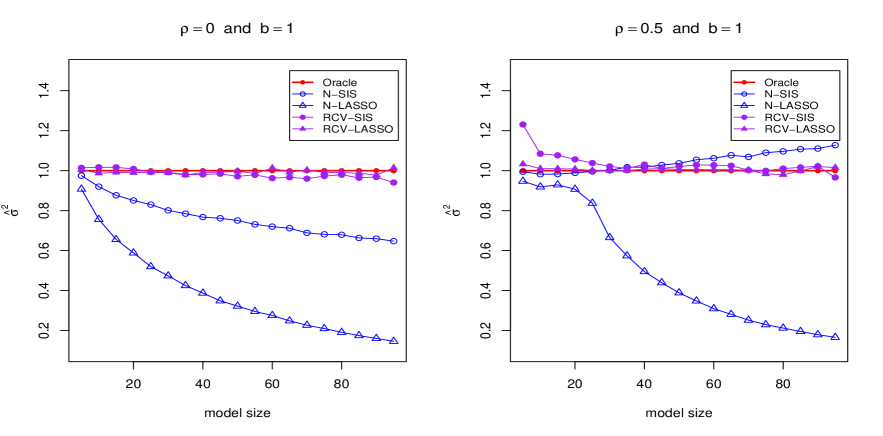

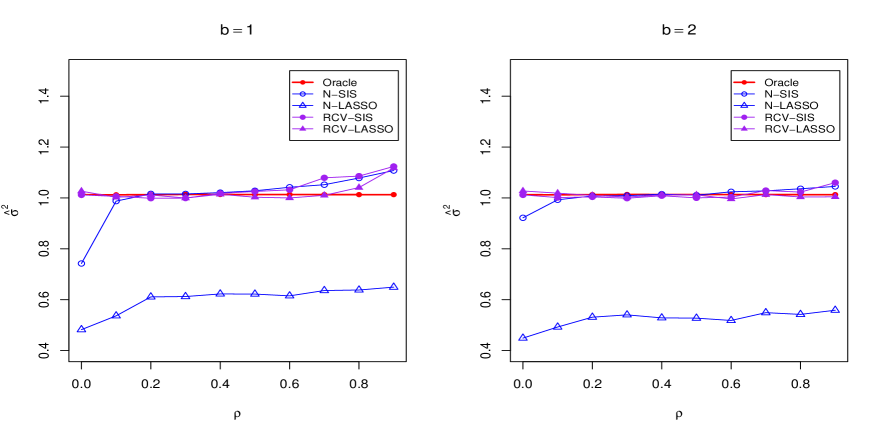

To test the sensitivity of the RCV procedure to the model size and covariance structure among predictors, additional simulations have been conducted and their results are summarized in Figure 6 and 7. From Figure 6, it is clear that RCV method is insensitive to model size , as explained before Theorem 2. Figure 7 shows the RCV methods are also robust with respect to the covariance structure. In contrast, N-LASSO always underestimates the variance.

| Method | BIAS | SE | AMS | SSP | BIAS | SE | AMS | SSP |

|---|---|---|---|---|---|---|---|---|

| Oracle | -0.014 | 0.089 | 3.000 | 1.000 | -0.014 | 0.090 | 3.000 | 1.000 |

| N-SIS | -0.111 | 0.096 | 50.000 | 1.000 | -0.011 | 0.102 | 50.000 | 1.000 |

| N-ISIS | -0.791 | 0.073 | 49.130 | 1.000 | -0.821 | 0.036 | 46.870 | 1.000 |

| N-LASSO | -0.581 | 0.163 | 41.460 | 1.000 | -0.526 | 0.172 | 43.310 | 1.000 |

| RCV-SIS | -0.030 | 0.132 | 50.000 | 1.000 | 0.025 | 0.279 | 50.000 | 0.960 |

| RCV-ISIS | -0.017 | 0.113 | 25.770 | 1.000 | -0.020 | 0.106 | 22.185 | 1.000 |

| RCV-LASSO | -0.004 | 0.130 | 34.230 | 1.000 | -0.026 | 0.147 | 34.990 | 1.000 |

| P-SCAD | -0.048 | 0.109 | 7.810 | 1.000 | -0.036 | 0.097 | 6.080 | 1.000 |

| CV-SCAD | 0.000 | 0.095 | 7.810 | 1.000 | 0.001 | 0.096 | 6.080 | 1.000 |

| P-LASSO | -0.102 | 0.195 | 41.460 | 1.000 | -0.113 | 0.164 | 43.310 | 1.000 |

| CV-LASSO | 0.141 | 0.111 | 41.460 | 1.000 | 0.127 | 0.116 | 43.310 | 1.000 |

| Method | BIAS | SE | AMS | SSP | BIAS | SE | AMS | SSP |

| Oracle | -0.014 | 0.090 | 3.000 | 1.000 | -0.014 | 0.090 | 3.000 | 1.000 |

| N-SIS | 0.010 | 0.105 | 50.000 | 1.000 | 0.046 | 0.107 | 50.000 | 0.980 |

| N-ISIS | -0.817 | 0.077 | 46.400 | 1.000 | -0.809 | 0.099 | 46.250 | 1.000 |

| N-LASSO | -0.445 | 0.202 | 39.290 | 1.000 | -0.381 | 0.239 | 37.140 | 1.000 |

| RCV-SIS | 0.017 | 0.164 | 50.000 | 0.880 | 0.057 | 0.158 | 50.000 | 0.430 |

| RCV-ISIS | -0.002 | 0.122 | 22.225 | 0.970 | 0.113 | 0.161 | 22.445 | 0.150 |

| RCV-LASSO | -0.029 | 0.147 | 33.470 | 0.990 | 0.046 | 0.161 | 31.890 | 0.450 |

| P-SCAD | -0.036 | 0.096 | 6.110 | 1.000 | -0.066 | 0.102 | 14.520 | 1.000 |

| CV-SCAD | 0.003 | 0.096 | 6.110 | 1.000 | 0.079 | 0.124 | 14.520 | 1.000 |

| P-LASSO | -0.097 | 0.171 | 39.290 | 1.000 | -0.089 | 0.171 | 37.140 | 1.000 |

| CV-LASSO | 0.126 | 0.116 | 39.290 | 1.000 | 0.125 | 0.116 | 37.140 | 1.000 |

To show the effectiveness of in the construction of confidence intervals, we calculate the coverage probability of the confidence interval (10) based on 10,000 simulations. This was conducted for , and with , 1, and 2 and and . To save the space of the presentation, we present only one specific case for with in Table 3.

| 80% | 90% | 95% | 99% | 80% | 90% | 95% | 99% | |

|---|---|---|---|---|---|---|---|---|

| Oracle | 0.7967 | 0.8974 | 0.9476 | 0.9874 | 0.7931 | 0.9006 | 0.9483 | 0.9865 |

| RCV | 0.7919 | 0.8928 | 0.9435 | 0.9847 | 0.8042 | 0.9022 | 0.9518 | 0.9871 |

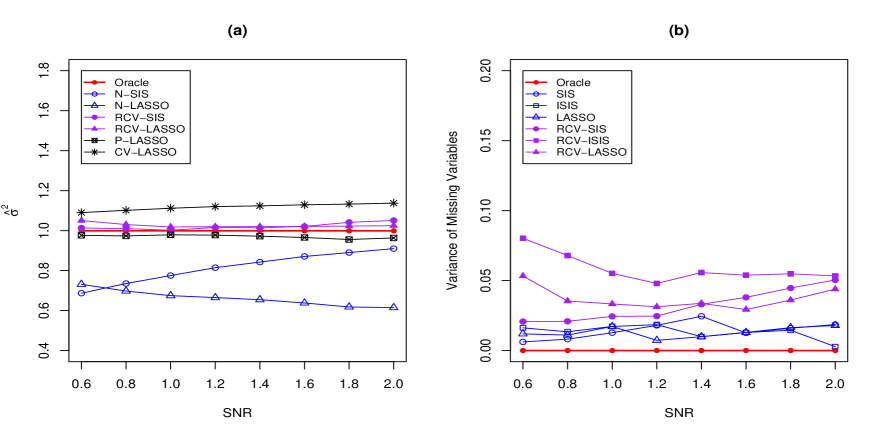

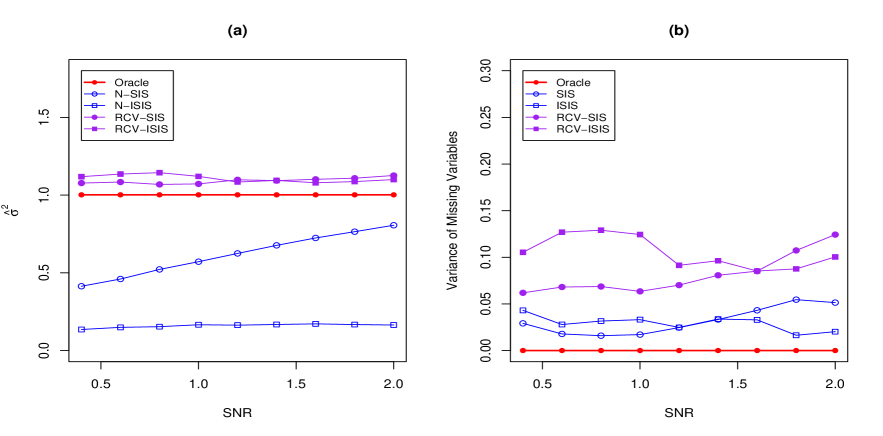

Example 3. We consider a more realistic model with 10 important predictors, detailed at beginning of this section. Since some non-vanishing coefficients are very small, no method can guarantee all relevant variables are chosen in the selected model, i.e. possess a sure screening property. To quantify the severity of missing relevant variables, we use the quantity Variance of Missing Variables (VMV), to measure, where is the set of important variables not included in the selected model and is their regression coefficients in the simulated model. For RCV methods, the VMV is the average of VMVs for two halves of the data. Figure 8 summarizes the simulation results for , whereas Figure 9 depicts the results for when the penalization methods are not easily accessible. The naive methods seriously underestimate the variance and sensitive to the model selection tools, dimensionality, SNR, among others. In contrast, the RCV methods are much more stable and only slightly overestimate the variance when the sure screening condition is not satisfied. The one-step methods, especially plug in methods, perform also well.

5.2 Real data analysis

We now apply our proposed procedure to analyze a recent house price data from 1996-2005. The data set consists of 119 months of appreciations of national House Price Index (HPI), defined as the percent of monthly log-HPI changes in 381 Core Based Statistical Areas (CBSA) in the United States. The goal is to forecast the housing price appreciation (HPA) over those 381 CBSAs over the next several years. Housing prices are geographically dependent. They depend also on macroeconomic variables. Their dependence on macroeconomic variables can be summarized by the national HPA. Therefore, a reasonable model for predicting the next period HPA in a given CBSA is

| (19) |

where stands for the national HPA, are the HPAs in those 381 CBSAs, and is a random error independent of . This is clearly a problem with the number of predictors more than the number of covariates. However, conditional on the national HPA , it is reasonable to expect that only the local neighborhoods have non-negligible influence, but it is hard to pre-determine those neighborhoods. In other words, it is reasonable to expect that the coefficients are sparse.

Our primary interest is to estimate the residual variance , which is the prediction error of the benchmark model. We always keep the variables and , which is the lag 1 HPA of the region to be predicted. We applied the SCAD using the local linear approximation (Zou and Li, 2008), which is the iteratively re-weighted LASSO, to estimate coefficients in (19). We summarize the result, , as a function of the selected model size , to examine the sensitivity to the selected model size. Reported also is the percent of variance explained which is defined as

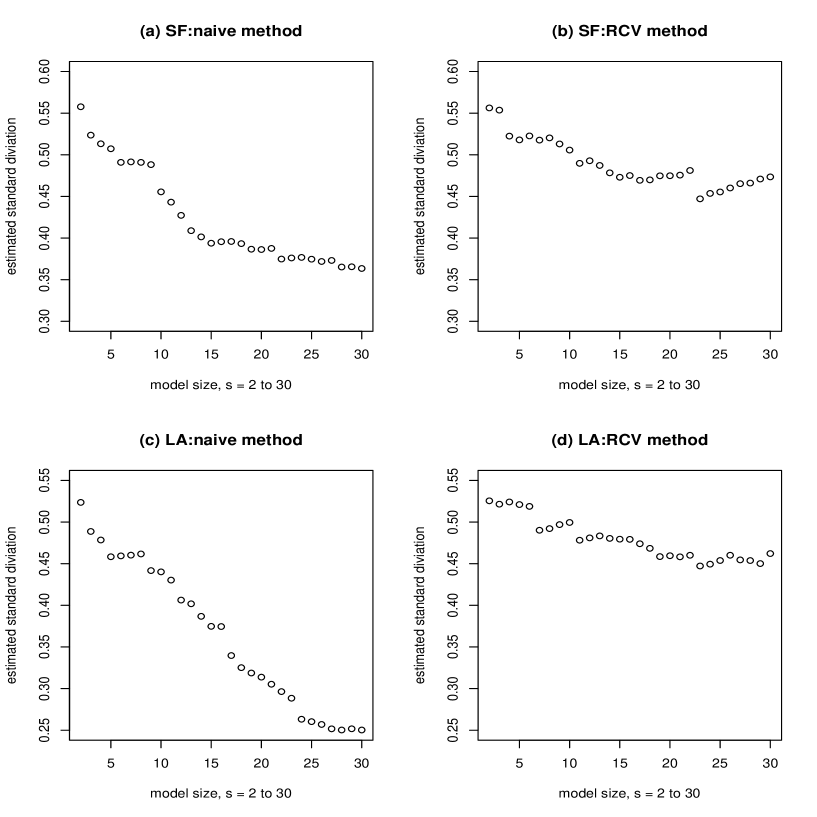

where is the sample average of the time series. For illustration purpose, we only focus on one CBSA in San Francisco and one in Los Angeles. The results are summarized in Table 3 and Figure 10, in which the naive two-stage method is also included for comparison.

First of all, as shown in Figure 10, the influence of the naive method by the selected model size is much larger than that of the RCV method. This is due to the spurious correlation as we discussed before. The RCV estimate is reasonably stable, but it is also influenced by the selected model size when it is large. This is understandable given the sample size of 119.

In the case of San Francisco, from Figure 10(b), the RCV method suggests that the standard deviation should be around , which is reasonably stable for in the range of to 8. By inspection of the solution path of the naive two-stage method, we see that besides and , first selected is the variable , which corresponds to CBSA San Jose-Sunnyvale-Santa Clara (San Benito County, Santa Clara County). The variable also enters into both models when in the RCV method. Therefore, we suggest that the selected model consist of at least variables , and . As expected, in the RCV method, the fourth selected variables are not the same for the two splitted subsamples. The variance explained by regression takes of total variance.

Similar analysis can be applied to the Los Angeles case. Figure 10(d) suggests the standard deviation should be around (when is between and ). From the solution path, we suggest that the selected model consist of at least variables , and which corresponds to CBSA Oxnard-Thousand Oaks-Ventura (Ventura County). The variance explained by regression takes of total variance.

| San Francisco | |||||||

|---|---|---|---|---|---|---|---|

| Model size | 2 | 3 | 5 | 10 | 15 | 20 | 30 |

| Naive | 0.5577 | 0.5236 | 0.5072 | 0.4555 | 0.3938 | 0.3862 | 0.3635 |

| RCV | 0.5563 | 0.5536 | 0.5179 | 0.5057 | 0.4730 | 0.4749 | 0.4735 |

| variance explained | 76.92 | 79.83 | 81.40 | 85.67 | 89.79 | 90.66 | 92.58 |

| Los Angeles | |||||||

| Model size | 2 | 3 | 5 | 10 | 15 | 20 | 30 |

| Naive | 0.5236 | 0.4887 | 0.4583 | 0.4401 | 0.3747 | 0.3137 | 0.2503 |

| RCV | 0.5255 | 0.5214 | 0.5210 | 0.4995 | 0.4794 | 0.4596 | 0.4621 |

| variance explained | 88.68 | 90.23 | 91.56 | 92.56 | 94.86 | 96.57 | 98.05 |

6 Discussion

Variance estimation is important and challenging for ultrahigh dimensional sparse regression. One of the challenges is the spurious correlation: covariates can have high correlations with the realized noise and hence are recruited to predict the noise. As a result, the naive (natural) two-stage estimator seriously underestimates the variance. Its performance is very unstable and depends largely on the model selection tool employed. The RCV method is proposed to attenuate the influence of the effect of spurious variables. Both the asymptotic theory and empirical result show that the RCV estimator is the best among all estimators. It is accurate and stable, insensitive to the model selection tool and the size of the selected model. Therefore, we may employ fast model selection tool like SIS for computational efficiency for the RCV variance estimation. We also compare the RCV method with the direct plug-in method. When choosing tuning parameters of a penalized likelihood method like the LASSO, we suggest using a more conservative cross-validation rather than aggressive BIC. However, the LASSO method can still yield a non-negligible bias for variance estimation in ultrahigh dimensional regression. The SCAD method is almost as good as the RCV method, but it is computational more expensive than RCV-SIS.

Appendix

Notation and conditions

We first state the following assumptions, which are standard in the literatures of high dimensional statistical learning. For convenience, define and where and denote the smallest and largest eigenvalues of a matrix , respectively.

For a vector , we use standard natation and . For a matrix , we use three different norms. is defined in Assumption (A8) below; denotes the usual operator norm, i.e. ; is the usual sup-norm.

- (A1)

-

The errors are with zero mean and finite variance and independent of the design matrix .

- (A2)

-

There exists a constant and such that such that for all .

- (A3)

-

There exists a constant such that , where is the element of the design matrix X.

- (A4)

-

for some finite constants .

We have no intent to make the assumptions the weakest possible. For example, Assumption (A3) can be relaxed to for any or further relaxation. The aim of the assumptions (A3) and (A4) is to guarantee that in Theorem 1 is of the order .

Theorem 1 still holds under the random design with assumptions below.

- (A5)

-

The random vectors are and there exists a constant such that for all and some constants , and , where is the th element of .

- (A6)

-

satisfies that for some finite positive constants and , where is defined by Assumption (A5).

For instance, when and are sub-Gaussian () for each and , the assumptions (A5) and (A6) are satisfied.

The following assumption (A7) is imposed for proving Theorem 3. For fixed design matrix , the corresponding condition is also imposed in Meinshausen and Yu (2009) and some discussions of weaker conditions are shown in Bickel et al. (2009).

- (A7)

-

There exist constants such that

and

The following two additional assumptions are stated for proving Theorem 4. These conditions correspond to Conditions 4 and 5 in Fan and Lv (2009). Without loss of generality, assume that the true value with each component of nonzero and . Let and be the submatrices of design matrix with columns corresponding to and , respectively.

- (A8)

-

There exist constants such that

and

as , where

- (A9)

-

Denote Assume that with . Take and , where is defined in Theorem 4.

Remark: The norm is somewhat abstract. It can easily be shown that

where is the number of columns of B, which is a crude upper bound. Using this and the argument in the proof of Theorem 4, if

and and , then the conclusion of Theorem 4 holds.

A.1. Proof of Theorem 1

Part 1 follows the standard law of large numbers and central limit theorem. Now we prove the second part under assumptions (A1)- (A4). By Assumption (A2),

| (20) |

Let denote the -th column vector of the design matrix . For a large constant , consider the event Under the event , it follows from equation (20) that

Together with the fact , we get

Hence it suffices to show that as for some constant . Observe that, by Assumptions (A3)-(A4), for each ,

Using Bernstein’s inequality (e.g. Lemma 2.2.11 of van der Vaart and Wellner (1996) ), we have

| (21) | |||||

For sufficient large , we have since is bounded. Therefore, the power in (21) goes to negative infinity as . It follows that .

Next we show the second part of the theorem still holds under Assumptions (A5)-(A6) instead of Assumptions (A3)-(A4). It is sufficient to verify as for some constant . The key step is to establish the inequality

| (22) |

for each . Note that

for and random variables and . Thus, for any and each ,

If is a nonnegative random variable with its distribution and tail probability for some constant and each , then by integration by parts

As a result, it follows that, for each ,

Thus, for each positive integer and ,

Theorem 1 is proved.

A.2. Proof of Theorem 2

Define sequences of events , and . On the event , we have

where and correspond to and , respectively. Decompose now on the event as

We now prove .

First, consider the quadratic form where is a symmetric matrix, and are . Assume that , and the fourth moment . Let be the th element of the matrix . Then,

and

where the last inequality holds since .

Observe that, . Hence, on the event , we have

and

Using Markov inequality, it follows that, under the event ,

Combining with the assumptions and , we obtain that

As a result,

Similarly, we conclude that

Therefore, using the last two results, we have

which implies that . The Proof of Theorem 2 is completed.

To prove Theorem 3, we will use the following lemma. The results are stated and proved in Meinshausen and Yu (2009) and Bickel et al. (2009).

Lemma 1

Consider the LASSO selector defined by (12) with . Under the assumptions (A1)-(A4) and (A7), for , there exists a constant such that, with probability tending to 1 for ,

and

A.3. Proof of Theorem 3

can be decomposed as

The classical central limit theorem yields . Note that

By (21) and Lemma 1, it follows that

In addition, by the third conclusion in Lemma 1, . Therefore, the conclusion holds.

A.4. Proof of Theorem 4

Let with be the oracle estimator. The key step is to show that, with probability tending to 1, the oracle estimator is a strictly local minimizer of defined by (16). To prove it, by Theorem 1 of Fan and Lv (2009), it suffices to show that, with probability tending to 1, satisfies

| (23) | |||

| (24) | |||

| (25) |

where and

Let and . Consider the events

Observe that . Then, we get and hence, under the event ,

for some constant not depending on . Note that, in the above inequalities, we use that facts and .

Since with and , as addressed in Assumption (A9), we have, under the event ,

for sufficiently large . As a result, this leads to and and hence imply that (23) and (25) hold under the event .

Now turn to prove the inequality (24). Under the event , we have

for sufficiently large . This shows that the inequality (24) holds for sufficiently large under the event . By taking , similar arguments to Theorem 1 lead to

as . Thus, we have proven that is a strictly local minimizer of with large probability tending to one. Consequently, .

Now consider the asymptotic distribution of . Observe that . Under the event ,

Hence, we have that

which also implies that . The proof is complete.

Let and be the c.d.f. of standard Gaussian and student’s distribution with degrees of freedom. For large ,

Therefore, satisfies . The classical result that are distribution entails that

which, by the choice of , is further bounded from below by

References

- Bickel et al. (2009) Bickel, P. J., Ritov, Y. and Tsybakov, A. (2009) Simultaneous analysis of lasso and dantzig selector. Ann. Statist., 37, 1705–1732.

- Bunea et al. (2007) Bunea, F., Tsybakov, A. and Wegkamp, M. (2007) Sparsity oracle inequalities for the lasso. Elect. J. Statist., 1, 169–194.

- Candes and Tao (2007) Candes, E. and Tao, T. (2007) The dantzig selector: statistical estimation when is much larger than (with discussion). Ann. Statist., 35, 2313–2351.

- Chatterjee and Lahiri (2010) Chatterjee A. and Lahiri S. N. (2010) Bootstrapping lasso estimators. Manuscript.

- Efron et al. (2004) Efron, B., Hastie, T., Johnstone, I. and Tibshirani, R. (2004) Least angle regression (with discussions). Ann. Statist., 32, 409-499.

- Fan and Li (2001) Fan, J. and Li, R. (2001). Variable selection via nonconcave penalized likelihood and its oracle properties. Journal of American Statistical Association, 96, 1348-1360.

- Fan and Lv (2008) Fan, J. and Lv, J. (2008) Sure independence screening for ultrahigh dimensional feature space (with discussion). J. R. Statist. Soc. B, 70, 849–911.

- Fan and Lv (2009) Fan, J. and Lv, J. (2009) Properties of non-concave penalized likelihood with NP-dimensionality. Manuscript.

- Fan and Lv (2010) Fan, J. and Lv, J. (2010) A selective overview of variable selection in high dimensional feature space. Statist. Sinica., 20, 101–148.

- Fan and Peng (2004) Fan, J. and Peng, H. (2004) Nonconcave penalized likelihood with a diverging number of parameters. Ann. Statist., 32, 928–961.

- Fan et al. (2009) Fan, J., Samworth, R. and Wu, Y. (2009) Ultrahigh dimensional feature selection: Beyond the linear model. J. Mach. Learn., Res., 10, 2013–2038.

- Fan and Song (2010) Fan, J. and Song, R. (2010) Sure independence screening in generalized linear models with NP-dimensionality. Ann. Statist., to appear.

- Greenshtein and Ritov (2004) Greenshtein, E. and Ritov, Y. (2004) Persistence in high-dimensional linear predictor selection and the virtue of overparametrization. Bernoulli, 10, 971–988.

- Han et al. (2010) Han, X., Gu, W., and Fan, J. (2010). Control of the false discovery rate under arbitrary covariance dependence. Manuscript.

- Kim et al. (2008) Kim, Y., Choi, H. and Oh, H.-S. (2008) Smoothly clipped absolute deviation on high dimensions. J. Am. Statist. Assoc., 103, 1665–1673.

- Knight and Fu (2000) Knight, K. and Fu, W.(2000) Asymptotics for lasso-type estimators. Ann. Statist., 28, 1356-1378.

- Kyung, et al. (2010) Kyung M., Gill, J., Ghosh M. and Casella G. (2010) Penalized regression, standard errors and Bayesian lassos. Bayesian analysis, 5(2), 369-412.

- Lv and Fan (2009) Lv, J. and Fan, Y. (2009). A unified approach to model selection and sparse recovery using regularized least squares. Ann. Statist. 37, 3498–3528.

- Meier et al. (2008) Meier, L., van de Geer, S. and Bühlmann, P. (2008). The group LASSO for logistic regression. Journal of the Royal Statistical Society, B, 70, 53-71.

- Meinshausen, et al. (2009) Meinshausen, N., Meier, L. and Bhlmann P. (2009) p-Values for high-dimensional regression. J. Am. Statist. Assoc., 104, 1671-1681.

- Meinshausen and Yu (2009) Meinshausen, N. and Yu, B. (2009) LASSO-type recovery of sparse representations for high-dimensional data. Ann. Statist., 37, 246–270.

- Park and Casella (2008) Park, T. and Casella, G. (2008) The Bayesian lasso. J. Am. Statist. Assoc., 103, 681-686.

- Wasserman and Roeder (2009) Wasserman, L. and Roeder, K. (2009) High dimensional variable selection. Ann. Statist., 37, 2178–2201.

- van der Vaart and Wellner (1996) van der Vaart, A.W. and Wellner, J.A. (1996). Weak Convergence and Empirical Processes. Springer, New York.

- Ye (1998) Ye, J. (1998) On measuring and correcting the effects of data mining and model selection. J. Am. Statist. Assoc., 93, 120–131.

- Zhang and Huang (2008) Zhang, C. H. and Huang, J. (2008) The sparsity and bias of the lasso selection in high-dimensional linear regression. Ann. Statist., 36, 1567–1594.

- Zhao and Li (2010) Zhao, S. and Li, Y. (2010) Principled sure independence screening for Cox models with ultra-high-dimensional covariates. Preprint .

- Zhao and Yu (2006) Zhao, P. and Yu, B. (2006) On model selection consistency of lasso. J. Mach. Learn. Res., 7, 2541–2563.

- Zou (2006) Zou, H. (2006) The adaptive Lasso and its oracle properties. J. Am. Statist. Assoc., 101, 1418–1429.

- Zou and Li (2008) Zou, H. and Li, R. (2008). One-step Sparse Estimates in Nonconcave Penalized Likelihood Models (with discussion). Ann. Statist., 36, 1509-1533.

- Zou, et al. (2007) Zou, H., Hastie, T. and Tibshirani, R (2007). On the “degrees of freedom” of the lasso. Ann. Statist., 35, 2173-2192.