The cause of universality in growth fluctuations

Abstract

Phenomena as diverse as breeding bird populations, the size of U.S. firms, money invested in mutual funds, the GDP of individual countries and the scientific output of universities all show unusual but remarkably similar growth fluctuations. The fluctuations display characteristic features, including double exponential scaling in the body of the distribution and power law scaling of the standard deviation as a function of size. To explain this we propose a remarkably simple additive replication model: At each step each individual is replaced by a new number of individuals drawn from the same replication distribution. If the replication distribution is sufficiently heavy tailed then the growth fluctuations are Levy distributed. We analyze the data from bird populations, firms, and mutual funds and show that our predictions match the data well, in several respects: Our theory results in a much better collapse of the individual distributions onto a single curve and also correctly predicts the scaling of the standard deviation with size. To illustrate how this can emerge from a collective microscopic dynamics we propose a model based on stochastic influence dynamics over a scale-free contact network and show that it produces results similar to those observed. We also extend the model to deal with correlations between individual elements. Our main conclusion is that the universality of growth fluctuations is driven by the additivity of growth processes and the action of the generalized central limit theorem.

I Introduction

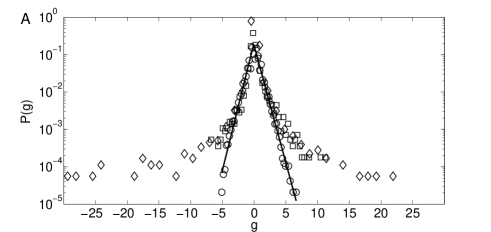

Recent research has revealed surprising properties in the fluctuations in the size of entities such as breeding bird populations along given migration routes Keitt98 , U.S. firm size Stanley96 ; Amaral97a ; Bottazzi03a ; Matia04 ; Bottazzi05 ; Axtell06 , money invested in mutual funds Schwarzkopf08 , GDP Canning98 ; Lee98 ; Castaldi09 , scientific output of universities Matia05 , and many other phenomena Plerou99 ; Keitt02 ; Bottazzi07 ; Podobnik08 ; Rozenfeld08 . This is illustrated in Figures 1 and 2. The first unusual property is in the logarithmic annual growth rates , defined as , where is the size in year . As seen in the top panel of Figure 1, all of the data sets show a similar double exponential scaling in the body of the distribution, indicating heavy tails. The second surprising feature is the power law scaling of the standard deviation with size, as illustrated in Figure 2. In each case the standard deviation scales as with .

These results are viewed as interesting because they suggest a non-trivial collective phenomena with universal properties. If the individual elements fluctuate independently, then (with a caveat we will state shortly) the standard deviation of the growth rates scales as a function of size with an exponent , whereas if the individual elements of the population move in tandem the standard deviation scales with , i.e. it is independent of size. The fact that we instead observe a power law with an intermediate exponent suggests that the individual elements neither change independently nor in tandem. Instead it suggests some form of nontrivial long-range coupling. Why should phenomena as diverse as breeding bird populations and firm size show such similar behavior? There is a substantial body of previous work attempting to explain individual pheomena, such as firm size or GDP Gibrat31 ; Defabritiis03 ; Fu05 ; Riccaboni08 ; Simon58 ; Ijiri75 ; Amaral97b ; Buldyrev97 ; Amaral98 ; Bottazzi01 ; Sutton01 ; Wyart03 ; Bottazzi03b ; Gabaix09 ; Schweiger07 . However none of these theories has the generality to explain how this behavior could occur so widely.

The caveat in the above reasoning is the assumption that the fluctuations of the individual elements are well-behaved, in the sense that they are not too heavy-tailed. As we show in a moment, if the growth fluctuations of the individual elements are sufficiently heavy-tailed then the fluctuations of the population are also heavy tailed, even if there are no collective dynamics. Under the simple additive replication model that we propose the fluctuations in size are Levy distributed in the large limit. This predicts a scaling exponent and the shape parameter of the Levy distribution predicts the value of . We show here that this model provides an excellent fit to the data.

In the first part of this paper we develop the additive replication model and show that it gives a good fit to the data. Our analysis in the first part is predicated on the existence of a heavy-tailed replication distribution. In the second part of the paper we present one possible explanation for the heavy-tailed replication distribution in terms of stochastic influence dynamics on a scale-free contact network, and argue that such an explanation could apply to any of the diverse settings in which these scaling phenomena have occurred. This influence dynamics is an example of “nontrivial” collective dynamics. Thus, the process that generates the heavy tails in individual fluctuations may come from nontrivial collective dynamics even though the replication model does not depend on this.

II The additive replication model

| year | c | |||

|---|---|---|---|---|

| NABB | 1.40 | 0.81 | 0.156 | -0.037 |

| Mutual funds | 1.48 | 0.3 | 0.111 | -0.015 |

| Firms | 1.53 | 0.80 | 0.16 | -0.05 |

We assume an additive replication process: At each time step each individual element is replaced by new elements drawn at random from a replication distribution , where . An individual element could be a bird, a sale by a given firm, or the holdings of a given investor in a mutual fund. By definition the number of elements on the next time step is

| (1) |

where is the number of new elements replacing element at time . The growth is given by

| (2) |

The simplest version of our model assumes that draws from the replication distribution are independent; we later relax this assumption to allow for correlations.

Why might such a model be justified? First note that additivity of the elements is automatic, since by definition the size is the sum of the number of elements. The assumption that each element replicates itself in the next year amounts to a persistence assumption, i.e. that the number of elements in one year is linearly related to the number in the previous year, with each element influencing the next year independently of the others. We also assume uniformity by letting all elements have the same replication distribution . For the case of firms, for example, each sale in year can be viewed as replicating itself in year . This is plausible if the typical customer remains faithful to the same firm, normally continuing to buy the product from the same company, but occasionally changing to buy more or less of the product. For migrating birds this is plausible if the number of birds taking a given route in a given year is related to the number taking it last year, either because of the survival probability of individual birds or flocks of birds, or because individual birds influence other birds to take a given migration route.

III Predictions of the model

Given that the size at time is known and the drawings from are independent, the growth rate is a sum of I.I.D. random variables. Under the generalized central limit theorem Zolotarev86 ; Resnick07 , in the large limit the growth converges to a Levy skew alpha-stable distribution

| (3) |

is the shape parameter, is the asymmetry parameter, is the shift parameter and is a scale parameter.

The normal distribution is a special case corresponding to . This occurs if the second moment of is finite. However, if the second moment diverges according to extreme value theory, under conditions that are usually satisfied, it is possible to write for large 111Under extreme value theory there are distributions for which there is no convergent behavior; the power law assumes convergence.. When the Levy distribution has heavy tails that asymptotically scale as a power law with , where .

The additive replication process theory predicts power law behavior for and predicts its scaling exponent based on the growth distribution. If the growth rate distribution converges to a normal with 222For and there are logarithmic corrections to the results.. However, when , using standard results in extreme value theory Zolotarev86 ; Resnick07 the standard deviation scales as a power law with size, , where

| (4) |

IV Testing the predictions

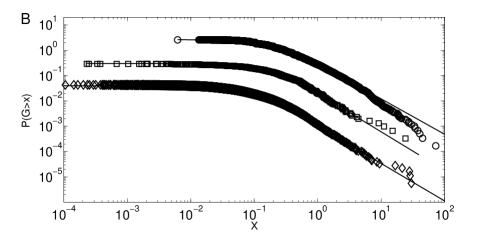

To test the prediction that the data is Levy-distributed, in the central panel of Figure 1 we compare each of our three data sets to Levy distributions. The three data sets are (1) the number of birds of a given species observed along a given migration route, (2) the size of a firm as represented by its sales, and (3) the size of a U.S. mutual fund. The data shown in the middle panel of Figure 1 are exactly the same as in the upper panel, except that we plot the growth fluctuations rather than their logarithmic counterpart , we plot a cumulative distribution rather than a histogram, and we graph the data on double logarithmic scale. The fits are all good.

Because we are lucky enough that the shape parameter and the asymmetry parameter are similar in all three data sets, we can collapse them onto a single curve. This is done by transforming all the data sets to the same scale in by dividing by an empirically computed scale factor equal to the 0.75 quantile minus the 0.25 quantile (we do it this way rather than dividing by the standard deviation because the standard deviation does not exist). It is important that this normalization is done in terms of , in contrast to the standard method which normalizes the logarithmic growth . The standard method, illustrated in the top panel, produces a collapse for the body of the distribution, but there is no collapse for the tails – mutual funds have very heavy tails while the breeding birds closely follow the exponential even for large values of . In contrast, the collapse using as suggested by our theory, illustrated in the bottom panel, works for both the body and the tails.

| year | |||

|---|---|---|---|

| NABB | |||

| Mutual funds | |||

| Firms |

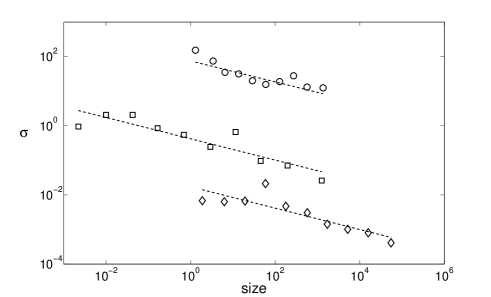

To test the prediction of the power law scaling of the standard deviation with size we estimated from the data shown in Figure 1 and from the data in Figure 2. We then make a prediction for each data set using Eq. 4 and the estimated value of for each data set. The results given in Table 1 are in good statistical agreement in every case. (See Materials and Methods.)

V Why is the replication distribution heavy-tailed?

Part of the original motivation for the interest in the non-normal properties and power law scalings of the growth fluctuations is the possibility that they illustrate an interesting collective growth phenomenon with universal applicability ranging from biology to economics. Our explanation so far seems to suggest the opposite: In our additive replication model each element acts independently of the others. As long as the replicating distribution is heavy tailed the scaling properties illustrated in Figures 1 and 2 will be observed, even without any collective interactions.

There is a subtle point here, however. Our discussion so far leaves open the question of why the replication distribution might be heavy-tailed. Based on the limited data that is currently available there are many possible explanations – it is not possible to choose one over another. One can postulate mechanisms that involve no collective behavior at all, for example, if individual birds had huge variations in the number of surviving offspring. (This might be plausible for mosquitos but does not seem plausible for birds). One can also postulate mechanisms that involve collective behavior, as we do in the next section.

VI The contact network explanation for heavy tails

In this section we present a plausible explanation for power law tails of in terms of random influence on a scale-free contact network. This example nicely illustrates how the heavy tails of the individual replication distribution can be caused by a collective phenomenon.

Assume a contact network Dorogovtsev08 where each node represents individuals. They are connected by an edge if they influence each other. For simplicity assume that influence is bi-directional and equal, i.e. that the edges are undirected and unweighted. Let individual be connected to other individuals, where is the degree of the node. The degree distribution is the probability that a randomly selected node has degree .

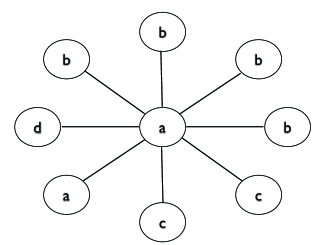

Let each individual belong to one of groups. For example, belonging to group can represent a consumer owning a product of firm , an investor with money in mutual fund , or a bird of a given species taking migration route . The groups are the same as the populations discussed earlier, i.e. is the size of group at time . The dynamics are epidemiological in the sense that an individual will stay in her group unless her contacts influence her to switch. The switching is stochastic: An individual in group with a contact in group will switch to group with a rate . Furthermore, the switching rate is linearly proportional to the number of contacts in that group, i.e. if an individual belonging to group has contacts in group , she will switch with a rate . As an example, the individual in the center of the graph in Fig 3 has a degree and belongs to group . She will switch to group with a rate , to group with a rate and to group d with a rate .

For example consider firm sales. If a given consumer likes the product of a given firm, she might influence her friends to buy more, and if she doesn’t like it, she might influence them to buy less. Thus each sale in a given year influences the sales in the following year. A similar explanation applies to mutual funds, under the assumption that each investor influences her friends, or it applies to birds, under the assumption that each bird influences other birds that it comes into contact with333 It has recently been shown that influence in flocking pigeons is hierarchical. Kurvers09 ; Nagy10 ..

We now show how the contact network gives rise to an additive replication model. To calculate consider each of the individuals in group one at a time. Individual in group replicates if she remains in the group, and/or if one or more of her contacts that belong to other groups join group . She fails to replicate if she leaves the group and also fails to influence anyone else to join. Let the resulting number of individuals that replace individual be . This implies

| (5) |

which is identical to Eq. 1 except for the group label (which was previously implicit).

The replication factor is a random number with values in the range . Given the stochastic nature of the influence process we approximate444 This approximation is valid for random networks, which have a local tree-like structure Dorogovtsev08 . as a Poisson random variable with mean , where is the probability that a randomly selected contact belongs to group . This means that the replication factor is proportional to the degree, i.e. , and that the replication distribution is proportional to the degree distribution,

| (6) |

Thus the influence dynamics of the contact network are an additive replication process with the individual replication distribution proportional to the degree distribution of the network. If the network is scale free, i.e. if for large the degree distribution is a power law with , then the growth fluctuations will be Levy distributed. It is beyond the scope of this paper to explain why the contact groups in the various settings that have been studied might be scale free, but there is at this point a large literature demonstrating that such behavior is common Albert02 ; Newman03 .

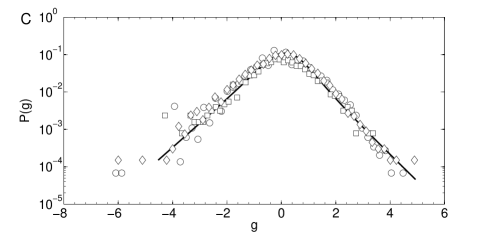

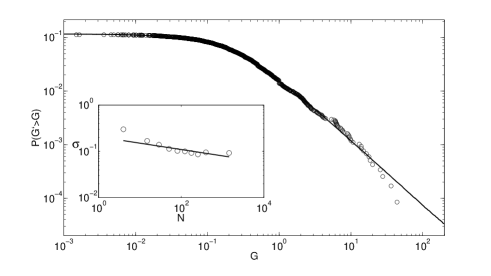

A numerical simulation verifies these results555 The average number of individuals and the average growth rate of a group can be approximated using a mean field approach. The mean field growth rates are given by PastorSatorras01 . and , where is the fraction of individual elements with degree that belong to group . We know of no analytic method to compute the growth fluctuations.. We simulated a network of nodes with a power law tailed degree distribution with and average degree . The dynamics were simulated for groups with a homogeneous switching rate . As expected the growth rates have a Levy distribution as shown in Figure 4. The fitted parameter values are , , and . The fitted value of the fluctuation scaling , shown in the inset of Figure 4, is in agreement with the predicted value of .

VII Correlations and finite size effects

So far we have assumed that the growth process for individual elements is uncorrelated, i.e. that the draws from are I.I.D. Sufficiently strong correlations can change the results substantially. There can be correlations among the individual elements or correlations in time. For example, suppose some groups are intrinsically more or less popular than others. For example, the popularity of a city might depend on its economy and living conditions. This can be modeled by assuming that the replication of individual in group is given by a random variable which is the sum of a random variable that depends on the individual and one that is common for the group, i.e. . We can then write the replication model in the form

| (7) |

As shown in the supplementary materials, for small sizes the individual fluctuations dominate, so that there is a power law scaling of , but for larger sizes the group fluctuations dominate, and becomes constant (i.e. ). This is indeed what we observe for cities666 Note that the nature of the scalings for cities is controversial and strongly depends on how a city is defined – our results are in agreement with those who claim the scaling is not very good Eeckhout04 . Rather than using the census definitions, Rozenfeld et al Rozenfeld08 use a clustering algorithm for defining cities and then the fluctuation scaling (without the group correlations) seems to hold..

We have also assumed in our analysis that the number of elements is infinite, i.e. that there is no upper limit on the replication factors. For finite systems the growth of one group is at the expense of another. This can induce correlations which affect both the growth rate distribution and the fluctuation scaling. Nevertheless, as our simulation shows, under appropriate circumstances the theory can still describe finite systems to a very good approximation. A more detailed discussion is provided in the supplementary materials.

VIII Discussion

The explanation that we offer here is widely applicable and very robust. The idea that a larger entity can be decomposed into a sum of smaller elements, and that the smaller elements can be modeled as if they replicate, is quite generic. As discussed in the previous section this can be broken if the growth of the elements is too correlated. Our explanation for the heavy tailed growth rate distributions and fluctuation scaling requires that the replication distribution is heavy tailed. The key thing we have shown is that when this occurs, the generalized central limit theorem dictates that the growth distribution will be Levy, which in turn dictates the power law size dependence of the standard deviation, .

The previous models which are closest to ours are the model of firm size of Wyart and Bouchaud Wyart03 and the model of GDP due to Gabaix Gabaix09 . Both of these models assume that the size distribution has power law tails and that firms grow via multiplicative fluctuations. They each suggested (without any testing) that additivity might lead to Levy distributions for their specific phenomena (GDP or firm size). This is in contrast to our model, which requires neither the assumption of power tails for size nor multiplicative growth. This is a critical point because the size of mutual funds does not obey a power law distribution Schwarzkopf08 , which rules out both the the Wyart and Bouchaud and Gabaix models as general explanations. We are apparently the first to realize that these diverse phenomena all obey Levy distributions, and that this explains the power law scaling of .

There are many possible explanations that could generate a heavy tailed replication distribution . Here we proposed an influence process on a scale free contact network as a possible example. This mechanism is quite general and relies on the assumption that an individual element’s actions are affected by those of its contacts. Scale free networks are surprisingly ubiquitous and the existence of social, information and biological networks with power law tails with is well documented Albert02 ; Newman03 , and suggests that the assumption that the degree distribution and hence the replication distribution are heavy-tailed is plausible.

The influence model shows that the question of whether the interesting scaling properties of these systems should be regarded as “interesting collective dynamics” can be subtle. On one hand the additive replication model suppresses this – any possibility for collective action is swept into the individual replication process. On the other hand, the influence model shows that the heavy tails may nonetheless come from a collective interaction. More detailed data is needed to make this distinction.

Our model shows that, whenever its assumptions are satisfied, one should expect universal behavior as dictated by the central limit theorem: The growth fluctuations should be Levy distributed (with the normal distribution as a special case). Our model does not suggest that the tail parameter should be universal, though of course this could be possible for other reasons. Based on our model there is no reason to expect that the value of the exponent (or equivalently or ) will not depend on factors that vary from example to example. Thus the growth process is universal in one sense but not in another.

IX Materials and methods

IX.0.1 North american breeding birds dataset

We use the the North American breeding bird survey,

which contains 42 yearly observations for over 600 species along more than 3,000 observation routes.

For each route the number of birds from each species is quoted for each year in the period 1966-2007.

For each year in the data set, from 1966 to 2007, we computed the yearly growth with respect to each species in each route.

The data set can be found online at

ftp://ftpext.usgs.gov/pub/er/md/laurel/BBS/DataFiles/.

IX.0.2 US public firms dataset

We use the 2008 COMPUSTAT dataset containing information on all US public firms. As the size of a firm we use the dollar amount of sales. Growth is given by the 3 year growth in sales.

IX.0.3 US equity mutual fund dataset

We use the Center for Research in Security Prices (CRSP) mutual fund database, restricted to equity mutual funds existing in the years 1997 to 2007. An equity fund is one with at least 80% of its portfolio in stocks. As the size of the Mutual fund we use the total net assets value (TNA) in real US dollars as reported monthly. Growth in the mutual fund industry, measured by change in TNA, is comprised of two sources: growth due to the funds performance and growth due to flux of money from investors, i.e. mutual funds can grow in size if their assets increase in value or due to new money coming in from investors. We define the relative growth in the size of a fund at time as

and decompose it as follows;

| (8) |

where is the fund’s return, quoted monthly in the database, and is the growth due to investors. For our purposes here we only consider , the growth due to investors.

IX.1 Empirical fitting procedures

The empirical investigation is conducted as follows: We first estimate the fluctuation scaling exponent . The relative growth rate distribution is binned into 10 exponentially spaced bins according to size . For each bin , the sample estimate of the variance of the growth rates is estimated in the usual way. Then the logarithm of the measured variances are regressed on the logarithm of the average size

| (9) |

such that the slope is the ordinary least squares (OLS) estimator of .

To estimate the tail exponent we normalize the growth rate such that it has zero mean and we divide by the 0.75 quartile - the 0.25 quartile. We estimate tail exponents using the technique described in Clauset et al Clauset07 . The method used uses the following modified Kolmogorov-Smirnoff statistic

where is the empirical cumulative distribution and is the hypothesized cumulative distribution. Using the maximum likelihood estimator (MLE) of the tail exponent we can predict the fluctuation scaling exponent using Eq. 4. and compare to the measured OLS estimator of .

Acknowledgements.

We gratefully acknowledge financial support from NSF grant HSD-0624351.References

- (1) Keitt, T. H & Stanley, E. H. (1998) Dynamics of north american breeding bird populations. Nature 393, 257–260.

- (2) Stanley, M. H. R, Amaral, L. A. N, Buldyrev, S. V, Havlin, S, Leschhorn, H, Maass, P, Salinger, M. A, & Stanley, H. E. (1996) Scaling behaviour in the growth of companies. Nature 379, 804–806.

- (3) Amaral, L. A. N, Buldyrev, S. V, Havlin, S, Leschhorn, H, Salinger, M. A, Stanley, H. E, & Stanley, M. H. R. (1997) Scaling behavior in economics: I. empirical results for company growth. J. Phys. I France 7, 621–633.

- (4) Bottazzi, G & Secchi, A. (2003) Common properties and sectoral specificities in the dynamics of u.s. manufacturing companies. Review of Industrial Organization 23, 217–232.

- (5) Matia, K, Fu, D, Buldyrev, S. V, Pammolli, F, Riccaboni, M, & Stanley, H. E. (2004) Statistical properties of business firms structure and growth. EUROPHYS LETT 67, 498.

- (6) Bottazzi, G & Secchi, A. (2005) Explaining the distribution of firms growth rates, (Laboratory of Economics and Management (LEM), Sant’Anna School of Advanced Studies, Pisa, Italy), LEM Papers Series 2005/16.

- (7) Axtell, R, Perline, R, & Teitelbaum, D. (2006) Volatility and asymmetry of small firm growth rates over increasing time frames, (U.S. Small Business Administration, Office of Advocacy), The Office of Advocacy Small Business Working Papers 06rarpdt.

- (8) Schwarzkopf, Y & Farmer, J. D. (2008) Time evolution of the mutual fund size distribution, (Santa Fe Institute), SFI Working Paper Series 08-08-31.

- (9) Canning, D, Nunes Amaral, L. A, Lee, Y, Meyer, M, & Stanley, H. E. (1998) Scaling the volatility of gdp growth rates. Economics Letters 60, 335–341.

- (10) Lee, Y, Nunes Amaral, L. A, Canning, D, Meyer, M, & Stanley, H. E. (1998) Universal features in the growth dynamics of complex organizations. Phys. Rev. Lett. 81, 3275–3278.

- (11) Castaldi, C & Dosi, G. (2009) The patterns of output growth of firms and countries: Scale invariances and scale specificities. Empirical Economics 37, 475–495.

- (12) Matia, K, Amaral, L. A. N, Luwel, M, Moed, H. F, & Stanley, H. E. (2005) Scaling phenomena in the growth dynamics of scientific output: Research articles. J. Am. Soc. Inf. Sci. Technol. 56, 893–902.

- (13) Plerou, V, Amaral, L. A. N, Gopikrishnan, P, Meyer, M, & Stanley, H. E. (1999) Ivory tower universities and competitive business firms. Nature 400, 433.

- (14) Keitt, T. H, Amaral, L. A. N, Buldyrev, S. V, & Stanley, E. H. (2002) Scaling in the growth of geographically subdivided populations: invariant patterns from a continent-wide biological survey. The Royal Society B 357, 627–633.

- (15) Bottazzi, G, Cefis, E, Dosi, G, & Secchi, A. (2007) Invariances and diversities in the evolution of manufacturing industries. Small Business Economics 29, 137–159.

- (16) Podobnik, B, Horvatic, D, Pammolli, F, Wang, F, Stanley, H. E, & Grosse, I. (2008) Size-dependent standard deviation for growth rates: Empirical results and theoretical modeling. Physical Review E (Statistical, Nonlinear, and Soft Matter Physics) 77, 056102.

- (17) Rozenfeld, H. D, Rybski, D, Andrade, J. S, Batty, M, Stanley, H. E, & Makse, H. A. (2008) Laws of population growth. Proceedings of the National Academy of Sciences 105, 18702–18707.

- (18) R., G. (1931) Les inégalités économiques. (Librairie du Recueil Sirey).

- (19) De Fabritiis, G, Pammolli, F, & Riccaboni, M. (2003) On size and growth of business firms. PHYSICA A 324, 38.

- (20) Fu, D, Pammolli, F, Buldyrev, S. V, Riccaboni, M, Matia, K, Yamasaki, K, & Stanley, H. E. (2005) The growth of business firms: Theoretical framework and empirical evidence. Proc. Natl. Acad. Sci. 102, 18801–18806.

- (21) Riccaboni, M, Pammoli, F, Buldyrev, S. V, Pontace, L, & Stanley, H. E. (2008) The size variance relationship of business firm growth rates. Proc. Natl. Acad. Sci. 105, 19595–19600.

- (22) Simon, H. A & Bonini, C. P. (1958) The size distribution of business firms. The American Economic Review 48, 607–617.

- (23) Ijiri, Y & Simon, H. (1975) Some distributions associated with bose-einstein statistics. Proc. Nat. Acad. Sci. p. 1654.

- (24) Amaral, L. A. N, Buldyrev, S. V, Havlin, S, Maass, P, Salinger, M. A, Stanley, H. E, & Stanley, M. H. R. (1997) Scaling behavior in economics: The problem of quantifying company growth. Physica A 244, 1–24.

- (25) Buldyrev, S. V, Amaral, L. A. N, Havlin, S, Leschhorn, H, Salinger, M. A, Stanley, H. E, & Stanley, M. H. R. (1997) Scaling behavior in economics: Ii. modeling of company growth. Journal de Physique I France 7, 635–650.

- (26) Amaral, L. A. N, Buldyrev, S. V, Havlin, S, Salinger, M. A, & Stanley, H. E. (1998) Power law scaling for a system of interacting units with complex internal structure. Phys. Rev. Lett. 80, 1385–1388.

- (27) Bottazzi, G. (2001) Firm diversification and the law of proportionate effect, (Laboratory of Economics and Management (LEM), Sant’Anna School of Advanced Studies, Pisa, Italy), LEM Papers Series 2001/01.

- (28) Sutton, J. (2001) The variance of firm growth rates: The scaling puzzle, (Suntory and Toyota International Centres for Economics and Related Disciplines, LSE), STICERD - Economics of Industry Papers 27.

- (29) Wyart, M & Bouchaud, J.-P. (2003) Statistical models for company growth. Physica A: Statistical Mechanics and its Applications 326, 241 – 255.

- (30) Bottazzi, G & Secchi, A. (2003) A stochastic model of firm growth. Physica A: Statistical Mechanics and its Applications 324, 213–219.

- (31) Gabaix, X. (2009) The granular origins of aggregate fluctuations, (National Bureau of Economic Research), Working Paper 15286.

- (32) Schweiger, A. O, Buldyrev, S. V, & Stanley, H. E. (2007) A transactional theory of fluctuations in company size, (arXiv.org), Quantitative Finance physics/0703023.

- (33) Zolotarev, V. M. (1986) One-Dimensional Stable Distributions (Translations of Mathematical Monographs - Vol 65). (American Mathematical Society).

- (34) Resnick, S. I. (2007) Heavy-tail phenomena: probabilistic and statistical modeling. (Springer).

- (35) Dorogovtsev, S. N, Goltsev, A. V, & Mendes, J. F. F. (2008) Critical phenomena in complex networks. Reviews of Modern Physics 80, 1275.

- (36) Kurvers, R. H, Eijkelenkamp, B, van Oers, K, van Lith, B, van Wieren, S. E, Ydenberg, R. C, & Prins, H. H. (2009) Personality differences explain leadership in barnacle geese. Animal Behaviour 78, 447 – 453.

- (37) Nagy, M, Akos, Z, Biro, D, & Vicsek, T. (2010) Hierarchical group dynamics in pigeon flocks. Nature 464, 890–893.

- (38) Albert, R & Barabasi, A.-L. (2002) Statistical mechanics of complex networks. Reviews of Modern Physics 74, 47.

- (39) Newman, M. E. J. (2003) The structure and function of complex networks. SIAM Review 45, 167.

- (40) Pastor-Satorras, R & Vespignani, A. (2001) Epidemic spreading in scale-free networks. Phys. Rev. Lett. 86, 3200–3203.

- (41) Eeckhout, J. (2004) Gibrat’s law for (all) cities. American Economic Review 94, 1429–1451.

- (42) Clauset, A, Shalizi, C. R, & Newman, M. E. J. (2009) Power-law distributions in empirical data. SIAM Review 51, 661.