Interplay between positive feedbacks in the generalized CEV process

Abstract

The dynamics of the generalized CEV process is due to an interplay of two feedback mechanisms: State-to-Drift and State-to-Diffusion, whose degrees are and respectively. We particularly show that the gCEV, in which both feedback mechanisms are positive, i.e. , admits a stationary probability distribution provided that , which asymptotically decays as a power law with tail exponent . Furthermore the power spectral density obeys , where , . Bursting behavior of the gCEV is investigated numerically. Burst intensity and burst duration are shown to be related by .

The dynamics of the state of a system which is open to a rapidly fluctuating environment can be described by the non-linear stochastic differential equation

| (1) |

the standard Wiener process, under the assumption that 1.) noise enters linear, and 2.) the White Noise approximation is valid, see HorsthemkeLefever1984 . The drift and the diffusion ‘coefficients’ are depending on the recent state and hence represent ‘State-to-Drift’ or ‘State-to-Diffusion’ feedbacks, respectively. The resulting dynamics and consequently properties like the stationary pdf of the gCEV, the spectral density, and also burst statistics are shown to be due to the interplay between these two feedback mechanisms.

The following (informal) argument shows that if both feedback mechanisms and have a particular functional relation to each other, given by

| (2) |

then their interaction generates a power-law like stationary probability distribution - if it exists - in that

| (3) |

(Here and in the following the notion means that the function for large .) Note that the proportionality factor enters the coefficient of the power-law tail. The process considered in RuseckasKaulakys2010 , , corresponds to and so that the stationary pdf decays as a power-law according to .

I The generalized CEV process (gCEV)

In the following we consider a particular setting which is that the drift and diffusion coefficients obey and . In this case one obtains the Ito diffusion process with positive drift and diffusion parameters given by

| (4) |

This process is a generalization of the Constant - Elasticity - of - Variance model, , which was originally proposed by Cox, Ingersoll and Ross to describe the dynamics of interest rates in an equilibrium economy and which plays an important role in Mathematical Finance, see references below. The gCEV process, eqn 4 describes dynamics by the superposition of two different feedback scenarios: One is the State-to-Drift feedback incorporated in the deterministic part of the gCEV

| (5) |

while the other one concerns State-to-Diffusion feedback due to

| (6) |

In the following, we will focus on the case that both dynamical components exhibits positive feedback simultaneously in that we require

| (7) |

In this case gCEV dynamics results from the interplay of two positive feedback scenarios, each of which generates self-amplifying, i.e. ‘explosive’ behavior in itself. This is easily seen that the drift term with positive feedback gives rise to a Finite-Time-Singularity, i.e. as , where , while the solution on the finite interval is . Positive feedback in the state-to-diffusion term also leads to bursting behavior, in that can attain arbitrary large values while it always remains finite. This follows from the fact that the solution of eqn 6 is the inverse power of a d-dimensional Bessel process , where is a dimensional Brownian motion, where , for details see ReimannSornette2010 . Since therefore , it follows from the transitivity of , that escapes to for slower than a.s., see BorodinSalminen2002 , while the origin is polar, i.e. it will not be touched by . On the other hand has a positive probability to visit any finite -neighborhood of the origin before escaping. Consequently the dynamics exhibits arbitrary high but finite excursions.

Hence, for , both singularities are entirely different: While positive feedback in the state-to-drift component leads to a ’real’ Finite-Time-Singularity in that within, remains finite even if feedback in state-to-diffusion is positive. Nonetheless, if both positive feedback play in concert, the process exhibits a fat-tailed stationary probability distribution, provided that the State-to-Diffusion feedback is positive and strong enough with respect to the State-to-Drift feedback, i.e. . Bursting behavior is reflected in that the stationary pdf decays as a power law for large with an exponent obeying . For large , the tail exponent only depends on the state-to-diffusion feedback parameter , while the state-to-drift feedback parameter determines the pdf only for small .

II Stationary pdf of a generalized CEV process

II.1 The CEV process

The standard CEV process is obtained from eqn 4 for

| (8) |

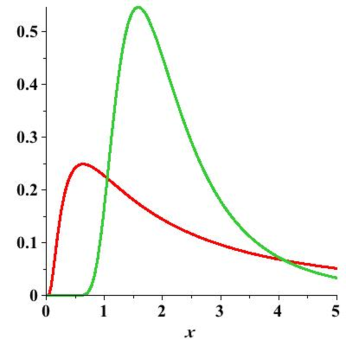

A typical time series generated by the CEV process for is shown in Fig 1. An extensive discussion of the CEV process and its relation to other processes including Bessel processes can be found in JeanblancYorChesney2009 ; BorodinSalminen2002 . While most of former research on the CEV process has been restricted to the case , we instead focus on the case that state-to-diffusion is subject to positive feedback . A detailed discussion of this process and the following theorem as well as the proof can be found in ReimannSornette2010 . As shown there, a CEV process with is equivalent to a radial Ornstein-Uhlenbeck process for order and hence admits a closed form analytical solution given below:

Result 1 (Solution of the CEV process for ).

The unique and strong solution of the CIR-CEV model, eq 8, with is

| (9) |

with , where be a d-dimensional mean-reverting Ornstein-Uhlenbeck process, whose dimension is a function of the feedback parameter given by

| (10) |

Its components obey with and the standard Wiener process, while its square norm is .

The proof is based on the observation that the Lamberti transform of this process 8 takes the form of a radial Ornstein Uhlenbeck process of order , see ReimannSornette2010 . In this note we show that the CEV process eqn. 8 with positive state-to-diffusion feedback () admits a stationary probability distribution, which is uni-modal and asymptotically decays as a power-law with its tail exponent proportional to only.

Result 2 (Stationary pdf for the CEV process for ).

Let [CEV] be defined on the non-negative reals with and the Standard Wiener process. Then, if a stationary probability distribution exists and is similar (not equal) to a Type-2 Gumbel distribution

| (11) |

where and is a normalization constant with . The stationary pdf takes its unique maximum in where is the index of radial Ornstein Uhlenbeck process equivalent to eqn. 8.

Proof.

As shown in ReimannSornette2010 the solution of the CEV process [CEV] is an inverse power of a radial Ornstein Uhlenbeck process of dimension for , given by , whose components obey . Since , and are natural boundaries for the CEV process with , thus the probability current over these boundaries is zero. ∎

For the stationary probability distribution asymptotically decays as a power law for large , more precisely

| (12) |

The pdf is shown in Fig. 3.

The equivalence between the CEV model with and the rOU process of index shows also up in the functional form of the stationary pdf. In fact the distribution can be rewritten as

which shows that the exponential part of the pdf is controlled by the order of the corresponding rOU process. Furthermore, the stationary probability distribution belonging to the CEV process with is uni-modal for all and decays for large as a power-law, i.e. . Its graph is sketched in Fig 2. As an immediate consequence we have

Result 3.

Given the CEV process with feedback parameter and let . Then

| (13) |

where is a small constant. Consequently for .

This follows from the more general case, see below. Note that for and , , so that in this case , see Fig. 4.

II.2 The generalized CEV process with positive feedback

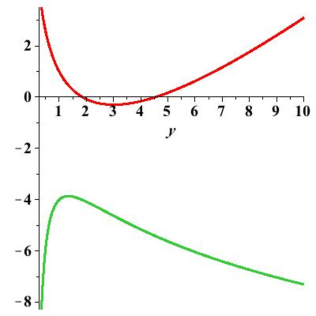

The interplay between state-to-price feedback and state-to-diffusion becomes obvious when considering the Fokker-Planck equation belonging to the gCEV process. Note that by transforming into , the gCEV process becomes with drift

| (14) |

The corresponding potential of the corresponding Fokker-Planck equation is of the form

where if and positive otherwise. Thus there is a bifurcation occurring at , such that is convex for and concave for , see Fig 5. Particularly, for , and are repelling and the potential has a unique minimum. On the other hand, for , both and are attracting, while with some positive for approaching . In terms of this means that for , that small , while large .

While for the gCEV process can be regarded as a diffusion trapped in a convex potential, i.e. behaves locally similar to an Ornstein-Uhlenbeck process, one can expect that in this case it admits a stationary probability density.

Result 4.

The generalized CEV process admits a stationary probability distribution if and . The stationary probability distribution yields , where with normalization constant , and thus asymptotically decays as a power law with tail exponent

Note that this excludes the Geometric Brownian Motion case , while it includes the case that the process exhibits positive feedback of both: state-to-drift feedback as well as state-to-diffusion . In fact, given the degree of positive state-to-drift feedback, then the degree of state-to-diffusion feedback must be positive as well while sufficiently large .

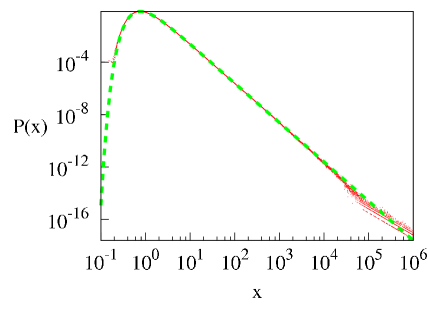

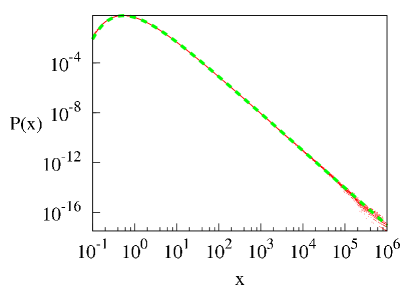

Fig 6 shows the empirical distribution (red) compared to the analytical solution, see eqn 11, (green dashed lines) for the case and , i.e. for the gCEV process in which both partial processes, eqnn 5 and 6 exhibit positive feedback.

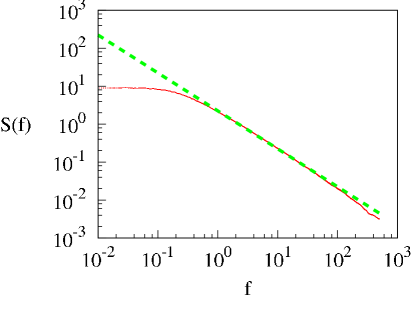

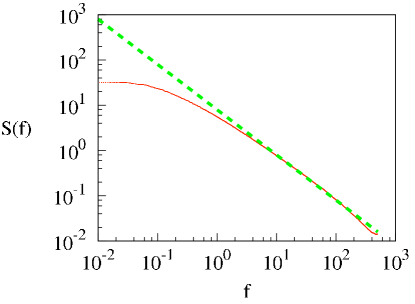

The power spectrum density of a gCEV asymptotically decays as a power-law with tail index , which is a direct function of the index of the related Bessel process and is, particularly independent of the feedback exponent of the drift term.

Result 5.

The gCVE process eqn 8 with feedback parameters admits a power spectrum

| (15) |

where and is the index of the radial Ornstein-Uhlenbeck process equivalent to the CEV process with and is a small parameter.

Proof.

The proof follows from a results in RuseckasKaulakys2010 by noting that the gCEV process for large can be approximated by , where for the coefficient is almost constant for large and approaches from above if . Therefore approximating the gCEV process for large but finite by

| (16) |

we obtain eq. (3) in RuseckasKaulakys2010 with the substitution . According to eqn. (33) in RuseckasKaulakys2010 the spectral density reads , . Inserting we obtain that for the process in eqn 16 which gives the result eqn 15 putting and . ∎

Note that for and , the power-spectrum shows pure behavior, see Fig. 7, while for , the spectrum is flat, .

The -dependence of the spectral density shows up only for small . One can show that for small is an increasing function of .

III Bursts generated in the gCEV process

Regarding the transformed gCEV process for as a diffusion being trapped in a convex potential as in Fig. 5 makes clear that the dynamics of allows for a sequence of arbitrary high but finite outbursts even on short time scales, in agreement with Fig 1. Since the bursting behavior, i.e. large, is governed by the state-to-diffusion feedback parameter , we can restrict ourselves to the case for investigating statistical properties of burst. That is, we will numerically consider the CEV process

in the following. Kaulakys and Alaburda KaulakysAlaburda2009 considered the case in

, for . Note that is the case is distributed according to a power law with tail exponent , as follows from eqn 3. In this particular setting they found numerical evidences for clear power-law statistics of bursts. Since in our case, power-law behavior only exists asymptotically, we can expect power-law burst statistics only asymptotically.

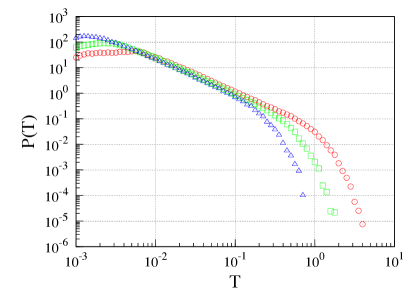

A burst is regarded as a super-threshold event: Let be the solution of a gCEV process. The burst interval of the k-th burst is defined as the time interval between crossing the threshold from below and the smallest time at which the threshold is crossed back from above. By a slight abuse of notation we also denote the length of this burst period by . In Fig 8 its probability distributions are shown for different threshold values: red , green , blue . The distribution of burst durations admits an intermediary power-law regime with .

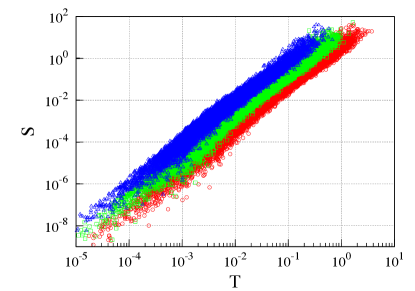

The size of a burst is defined as , i.e. the integral over the super-threshold trajectory in the burst period . It turns out to be related to the burst duration by

| (17) |

IV Acknowledgement

SR is deeply grateful to D. Sornette for numerous helpful discussions about CEV processes and pointing towards the importance of positive feedback. Authors acknowledge the support by EU COST Action MP 0801.

References

- (1) A.N. Borodin and P. Salminen. Handbook of Brownian Motion - Facts and Formulae. Birkhaeuer Boston, Basel, Berlin, 2002.

- (2) Werner Horsthemke and R. Lefever. Noise-induced Transitions: Theory and Applications in Physics, Chemistry, and Biology. Springer, 1984.

- (3) M. Jeanblanc, M. Yor, and M. Chesney. Mathematical Methods for Financial Markets. Springer Finance, 2009.

- (4) B. Kaulakys and M. Alaburda. Modelling scaled processes and 1/f beta noise using nonlinear stochastic differential equations. J. Stat. Mech., (P02051), 2009.

- (5) St. Reimann and D. Sornette. Positive feedback in cev processes. unpublished, 2010.

- (6) J Ruseckas and B. Kaulakys. 1/f noise from nonlinear stochastic differential equations. Phys. Rev. E, 81(031105), 2010.