pageheadfootsecnumdepth3\setkomafontcaptionlabel \deffootnote[1em]1em0em\thefootnotemark

Sibuya copulas

Marius Hofert111Department of Mathematics, ETH Zurich, 8092 Zurich, Switzerland, marius.hofert@math.ethz.ch. The author (Willis Research Fellow) thanks Willis Re for financial support while this work was completed., Frederic Vrins222ING Belgium SA, Brussels, frederic.vrins@ing.be

2024-03-10

Abstract

The standard intensity-based approach for modeling defaults is generalized by making the deterministic term structure of the survival probability stochastic via a common jump process. The survival copula of the vector of default times is derived and it is shown to be explicit and of the functional form as dealt with in the work of Sibuya. Besides the parameters of the jump process, the marginal survival functions of the default times appear in the copula. Sibuya copulas therefore allow for functional parameters and asymmetries. Due to the jump process in the construction, they allow for a singular component. Depending on the parameters, they may also be extreme-value copulas or Lévy-frailty copulas. Further, Sibuya copulas are easy to sample in any dimension. Properties of Sibuya copulas including positive lower orthant dependence, tail dependence, and extremal dependence are investigated. An application to pricing first-to-default contracts is outlined and further generalizations of this copula class are addressed.

Keywords Sibuya type distributions, Marshall-Olkin copulas, extreme-value copulas, Lévy-frailty copulas, default modeling, jump processes. \minisecMSC2010 60E05, 62H99, 60G99, 62H05, 62H20.

1 Introduction

A -dimensional copula is a -dimensional distribution function with standard uniform univariate margins. The main goal of the present work is to construct a flexible class of -dimensional copulas based on a multivariate default model and investigate its properties. The multivariate default model considered is a generalization of the standard intensity-based approach by using a common jump process. After presenting this model, the survival copula combining the default times is explicitly derived. It is of the functional form as appearing in Sibuya (1959). The resulting class of “Sibuya copulas” is remarkable in many ways. A first distinguishing feature compared to other copula classes is the fact that Sibuya copulas have functional parameters and therefore quite flexible in terms of its properties. As a second important feature, Sibuya copulas are not restricted to functional symmetry, i.e., exchangeability. This is important in large dimensions when exchangeability becomes a more and more restrictive assumption. Third, due to the construction with a common jump process, Sibuya copulas may have a singular component. This is important for applications such as multivariate default models since it translates to a positive probability that several components of a system default at the same time. Another important feature of large-dimensional copulas in applications is sampling. Due to the construction of Sibuya copulas via a default model, it is easy to draw vectors of random variates from these copulas.

Due to their general functional form, it seems difficult to determine the properties of Sibuya copulas in general. For investigating the properties, we therefore consider a working example throughout the paper. Even for this example, Sibuya copulas are seen to allow for many interesting properties. For example, the considered example is an extreme-value copula and also, as a special case, a Lévy-frailty copula. Further, the lower and upper extremal-dependence coefficients may be derived explicitly. Moreover, for the bivariate case, the working example is of Marshall-Olkin type.

As an application, we consider the valuation of a financial derivative contract, known as first-to-default swaps. We derive the pricing equation in the proposed dependence framework, and obtain an analytical formula for the fair spread of such type of contracts. Finally, possible extensions of the construction principle for Sibuya copulas are given.

The article is organized as follows. Section 2.1 recalls the standard intensity-based approach for default modeling. A generalization utilizing a common jump process is given in Section 2.2. In Section 2.3 we compute the joint survival function of the default times. The corresponding Sibuya type copulas are then derived in Section 2.4. In Section 3 the properties of this distributional class are investigated, including positive lower orthant dependence, tail dependence, extremal dependence, and sampling. Section 4 outlines an application to the pricing of first-to-default contracts, and Section 5 briefly addresses possible extensions of the construction principle for Sibuya copulas. Finally, Section 6 concludes. For the reader’s convenience, proofs are given in the Appendix.

2 A default model and its implied dependence structure

In this section, we derive a dependence structure based on a default model in a stochastic intensity framework. First, the standard intensity-based model is reviewed. Next, the natural extension consisting of making the intensities stochastic is considered. The stochastic intensities are restricted to take the form of a non-decreasing deterministic part and a non-decreasing jump process. The latter, being common to all entities, generates the dependence among the constituents.

2.1 The standard intensity-based default

In the standard intensity-based approach, default times are modeled as the first-jump times of a (possibly non-homogeneous) Poisson process. In other words, the default time of the th of components in a portfolio is modeled by a deterministic, non-negative intensity , . Given the intensity , the survival probability of component until time is given by

| (1) |

for the integrated rate function , . The canonical construction of the default time is then given by

| (2) |

for triggers , , see Bielecki and Rutkowski (2002, pp. 227) or Schönbucher (2003, p. 122). The survival function for the th component at time can now be computed as

Usually, one seeks for generating default times that are mutually dependent. This is already introduced at various points in the literature, including, e.g., Li (2000), Schönbucher and Schubert (2001), or Hofert and Scherer (2010) who introduce dependence by assuming a joint model for the vector of trigger variables . The following section we take another approach. We assume the triggers to be independent (see Section 5 for possible extensions) and introduce dependence by a common jump process.

2.2 A generalized default model

In what follows we generalize Mechanism (1) for modeling the term structure of survival probability of an entity by considering Cox processes instead of Poisson processes. The deterministic survival process is replaced by a stochastic one, i.e.,

| (3) |

where , , are right-continuous, increasing stochastic processes with independent increments and , that we naturally refer to as the integrated intensity process (“IIP”). The idea underlying the stochastic extension (3) of (1) is that samples of the default time may be generated by a more general model without altering the distribution.

As a realistic model for the processes , , we consider

| (4) |

where , , with a deterministic function , analogous to before, and is a right-continuous, increasing jump process with independent increments and .

Remark 2.1

The reader may find quite restrictive to focus on IIP of the form given by (4). However, it is a rather general form, as we now explain. In order for to be an IIP, it needs to be almost surely non-decreasing, otherwise the process may not be a proper survival process. Therefore, if we restrict to be right-continuous, with independent increments and stationary, then by definition is a Lévy subordinator, which in turns, implies that any IIP satisfying these constraints are necessarily of the form where is a non-negative constant, see, e.g., Cont and Tankov (2004, p. 88). The class of IIP we consider in (4) is even more general than Lévy subordinators in the sense that they can be non-stationary via the (possibly non-linear) functions . This shows that the class of IIP defined by (4) already covers an important part of the admissible processes.

The intuition behind (4) is that the individual term structure of the survival probability, modeled via , is hit by the jump process which models common shocks affecting the components. The default of an entity is then modeled similar to (2) via

| (5) |

for , , where is assumed to be independent of , .

Note that the default times , , are naturally dependent due to the common jump process . Our main goal is to investigate this dependence. We first focus on the case where , i.e., the dependence is solely induced by . An extension to nested or hierarchical dependence structures, as well as dependent triggers is discussed in Sections 5.1 and 5.2, respectively.

Since the dependence structure resulting from Construction (3) is quite general, we consider the following working example throughout this article.

Example 2.2 (Working example)

As a working example (“E”), consider to be of the form

for a non-homogeneous Poisson process with and , where for a deterministic, non-negative function such that , and where is a constant. This choice corresponds to the model of Hull and White (2008) where the jump size is set constant and equal to .

2.3 The joint survival function

In this section, we derive the joint survival function associated to our default model, namely , . An analytical expression of this survival distribution can be found in Vrins (2010) in the particular case defined by the working example. In what follows, we need the following lemma.

Lemma 2.3

Let , , , with . Further, let , , such that for and .

-

(1)

, where denotes the th order statistic of , , i.e., .

-

(2)

.

-

Proof

The proof is given in A.1. ∎

The following theorem presents the joint survival function of the default times , . Here, denotes the Laplace-Stieltjes transform of the random variable at , i.e., , .

Theorem 2.4

-

Proof

The proof is given in A.2. ∎

We may infer from (6) that the joint survival function is of a form as dealt with in Anderson et al. (1992). It is parameterized by the corresponding marginal survival functions , , and the common jump process . The following corollary presents the functional form of for the case of our working example.

Corollary 2.5 (Working example)

Let us consider the setup of the working example, i.e., Example 2.2. In this case, the marginal survival functions are given by

Since the non-homogeneous Poisson process has increment distribution and since the Laplace-Stieltjes transform of equals , , , we obtain

| (7) |

By applying Lemma 2.3 (1) with , , (7) can be simplified to

| (8) |

where , denotes the jointure function as introduced in Vrins (2010); note that the function is non-positive for , , and it is decreasing in for any fixed . Further, by applying Lemma 2.3 (2) with , , and , , the joint survival function in (7) can also be expressed as

| (9) |

2.4 The implied dependence structure

With the joint survival function and the corresponding marginal survival functions at hand, one can derive the copula which provides a link between these two pieces of the multivariate default model.

Corollary 2.6

Let and let , , be given as in Theorem 2.4. Further, let denote the generalized inverse corresponding to , , and let denote the th order statistic of , , i.e., . The copula corresponding to the joint survival function (6) is then given by

| (10) |

Since , , if and only if , , the diagonal corresponding to (10) is given by

Remark 2.7

The copula is in fact the survival copula of the vector of default times . From the form above one recognizes that is of the form of a class of distributions introduced by Sibuya (1959), who called

the dependence function of the joint survival function . We therefore refer to class of copulas as given in (10) as Sibuya copulas.

The idea of constructing a copula via a multivariate default model was recently applied by Mai and Scherer (2009a). In their work, takes the form , , for a common Lévy subordinator combined with a rescaling of the time-clock via functions , . This results in a non-stationary, non-decreasing stochastic process . The rescalings are monotonically increasing entity-dependent functions derived from the riskiness of the entities, i.e., the subordinator time is passing more rapidly for riskier entities so that the survival process at some standard time point is lower for riskier entities than for safer ones. This approach also results in a tractable dependence model for defaults. However, the derived copula is restricted to functional symmetry, also known as exchangeability. This drawback is shared by many copula classes including the class of Archimedean copulas and also, partly, by nested Archimedean copulas. It becomes a more and more restrictive assumption in large dimensions since it implies that, e.g., all bivariate margins of the copula are equal. This, in turn, implies that, e.g., it is not possible to construct asymmetric (non-exchangeable) joint distributions if all margins are identical. Such restrictive properties are rarely observed, especially for large-dimensional portfolios. Sibuya copulas do not suffer from this drawback.

Example 2.8 (Working example)

3 Properties of the copula

In this section we investigate some properties of the copula . We present results about positive lower orthant dependence, tail dependence, extremal dependence, and sampling. Due to the quite general form of a Sibuya copula , see (10), it is difficult to investigate tail and extremal dependence, even under (E), i.e., for the case of the working example. In Section 3.2 and 3.3, we therefore work out the details under the additional assumption (“A”), which means , , and , , where and are non-negative constants.

Let us first explore this case a bit. Under (A), the generalized inverses of the marginal survival functions , , are given explicitly by , where we define , , for convenience. In this setup, a Sibuya copula can be expressed as

| (12) |

with . The corresponding diagonal is given by

| (13) |

i.e., a power function, where the subscript stands for the th largest of with .

The following remark addresses several properties of this copula.

Remark 3.1

-

(1)

Assuming , , if or , then is the independence copula . Further, if and , then becomes the upper Fréchet bound copula . We therefore conclude that Sibuya copulas allow to capture the full range of positive lower orthant dependence.

-

(2)

The Sibuya copula as given in (12) allows for asymmetries and therefore more realistic dependence structures, especially in large dimensions.

-

(3)

Also note that this Sibuya copula is max-stable and therefore an extreme-value copula, see, e.g., Nelsen (2007, pp. 95), hence Sibuya copulas can be extreme-value copulas.

- (4)

-

(5)

In the bivariate case, (12) becomes

where , i.e. a Marshall-Olkin copula, see Marshall and Olkin (1967). Note that in this case, one has explicit formulas for Spearman’s rho and Kendall’s tau, see, e.g., Embrechts et al. (2001), for the tail-dependence coefficients Nelsen (2007, p. 215), as well as for the probability of falling on the singular component, see, e.g., Nelsen (2007, p. 54).

3.1 Positive lower orthant dependence

It follows directly from Equation (10) that , i.e., that is positive lower orthant dependent, see Joe (1997, p. 21). For the bivariate case this property is also called positive quadrant dependence and it implies, by definition, that all measures of concordance such as Spearman’s rho, Kendall’s tau are greater than or equal to zero. By Equation (10), the dependence function directly controls this dependence since

| (14) |

Since the left-hand side of (14) can be written as

for any , one also says that the copula has the “bad news propagation” effect.

3.2 Tail dependence

We pursue with a bivariate notion of association known as tail dependence. For , , with joint copula , the lower and upper tail-dependence coefficient and , respectively, are given by

where the limits are assumed to exist. By definition, the lower, respectively upper, tail-dependence coefficient tells us the likelihood, in the limit, that and are both small, respectively large, simultaneously. Note that if , then , the survival copula corresponding to . Therefore, the lower and upper tail-dependence coefficients interchange when going from to its survival copula .

In our case, is the survival copula of the vector of default times . Thus, the lower, respectively upper, tail-dependence coefficient tells us the likelihood, in the limit, that the two default times are jointly large, respectively small. So upper tail dependence means that a joint default model with a Sibuya copula as dependence structure produces joint defaults within a short amount of time.

If one assumes only the setup of the working example, then one can at least say that

Thus, if at least one of the individual survival functions is zero at some finite , then . Further, if is bounded, then . Under (A), is a Marshall-Olkin copula. Thus, the lower and upper tail-dependence coefficients are given by

respectively, see, e.g., Nelsen (2007, p. 215). It follows that or or implies . So if we suppose, in the limit, that entity is extremely safe, i.e., , then also . Further, if and or if and , , then .

3.3 Extremal dependence

The notion of extremal dependence was introduced by Frahm (2006). For , , with joint copula , the lower and upper extremal-dependence coefficient and , respectively, are given by

where the limits are assumed to exist. By definition, the lower (upper) extremal-dependence coefficient tells us the likelihood, in the limit, that the largest (smallest) value of , , is small (large) given that the smallest (largest) value is. Applied to the setup where is the survival copula of the default times, this means that the lower (upper) extremal-dependence coefficient tells us the likelihood that the smallest (largest) default time is large (small) given that the largest (smallest) is. Thus, given that the first default happened within a short amount of time, the upper extremal-dependence coefficient tells us the likelihood of all other defaults also happening within a short amount of time. The following proposition gives explicit formulas for and under (A).

Proposition 3.2

Under (A), the lower and upper extremal-dependence coefficients are given by

respectively, where the sum extends over all subsets of .

-

Proof

The proof is given in A.3. ∎

3.4 Sampling

The intuitive construction principle of Sibuya copulas via a default model can be used for simulation. Principally, we have to simulate the vector of individual default times and then return , a vector of random variates from the Sibuya copula . Sampling a vector involves drawing a vector and sampling a path of the jump process , where is such that for all . Then, is determined. Note that the number of occurrences to be sampled from the jump process depends on the given trigger variates , , as well as on the deterministic functions , . The following algorithm describes the general sampling procedure of .

Algorithm 3.3

| (1) | sample , | ||||

| (2) | , , , and | ||||

| (3) | repeat { | ||||

| (4) | sample the th occurence of the jump process | ||||

| (5) | find | ||||

| (6) | for { | # find for all | |||

| (7) | if | ||||

| (8) | else { | # | |||

| (9) | find on via | ||||

| (10) | } | ||||

| (11) | } | ||||

| (12) | # indices for which have not been determined yet | ||||

| (13) | if () break | ||||

| (14) | else | ||||

| (15) | } | ||||

| (16) | return |

Under (E), is given by , , for . In this case we have , . Further, Step (4) of Algorithm 3.3 can be achieved with the following algorithm, see, e.g., Devroye (1986, p. 257).

Algorithm 3.4

| (1) | sample | |

| (2) | # th occurrence of a homogeneous Poisson | |

| (3) | # process with unit intensity | |

| (4) | # th occurrence of a non-homogeneous Poisson | |

| (5) | # process with integrated rate function |

Note that under (A), Step (9) of Algorithm 3.3 boils down to setting and Step (4) of Algorithm 3.4 to .

Example 3.5

Let us consider the copula as given in (11). Since under (A), the bivariate is a Marshall-Olkin copula, we consider a more general example here. For this, let the “intensities” and , , be linear (instead of constant), i.e., let

where , . Further, let us assume the non-trivial case where not both () and () are zero simultaneously. Letting we obtain

for . The corresponding inverses are

Note that if denotes the th occurrence of the non-homogeneous Poisson process with integrated rate function , then

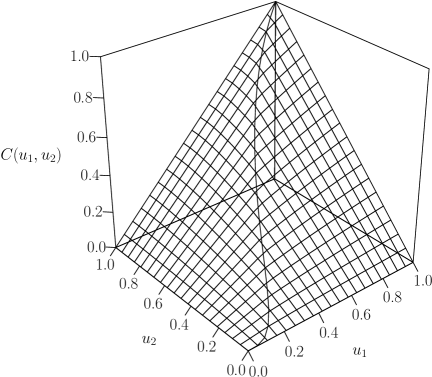

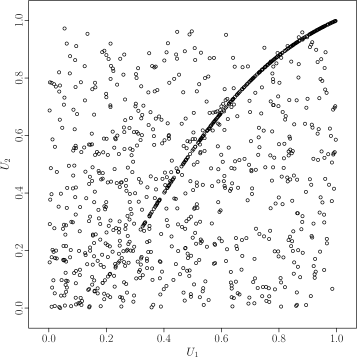

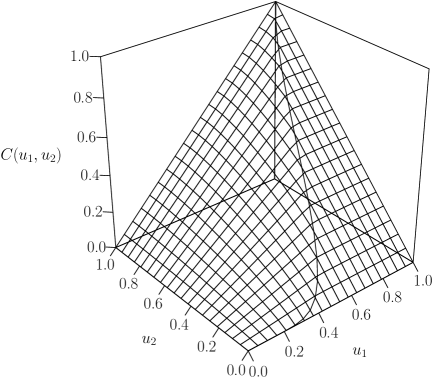

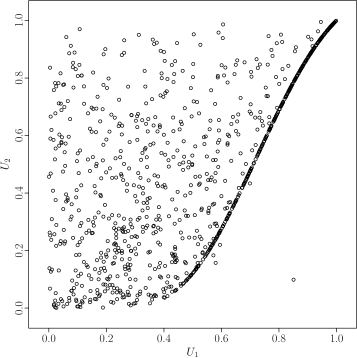

With these quantities one can evaluate the copula and apply Algorithm 3.3 for drawing vectors of random variates from . Figures 1 and 2 show two examples. Note that although we choose linear intensities, the resulting structures are quite different, e.g., see the shape of the singular components. Further, one may again infer that these copulas are able to capture highly asymmetric structures.

\setcapwidth

\setcapwidth

\setcapwidth

\setcapwidth

4 An application to the pricing of first-to-default contracts

In order to illustrate how a joint model with Sibuya dependence structure can be applied, we consider a financial application, consisting in the valuation of contracts known as first-to-default (FTD) swaps. The key element of this contract is a basket, i.e. a pool of entities. The first party, named protection seller agrees to pay the contractual counterparty known as protection buyer a fraction of the contract notional if the first default in the basket happens before the maturity of the contract. The fraction, named as loss given default, is defined by one minus the recovery rate of the defaulted entity. In order to enjoy that protection, the protection buyer is willing to pay the protection seller a given premium at prespecified payment dates (usually quarterly IMM), up to the maturity of the deal or the first default time, whichever comes first. After the first default in the basket or at the maturity, the latest, the contract stops.

Mathematically, risk-neutral pricing theory proves that the above two payment legs are, per unit notional, equal to (the default leg) and (the premium leg; for simplicity, we assume continuous premium payments), where with distribution function , denotes the recovery rate of the th entity (with index “(1)” denoting the recovery rate of the first defaulting entity in the basket), is the agreed spread (running annual premium), is the (assumed constant) risk-free interest rate used for discounting the cashflows, and is the contract’s maturity in years. A basic calculation leads to the present value of such a contract from the protection buyer’s perspective, given by

Another product, known as credit default swaps (“CDS”) allows one to derive risk-neutral default probability curves from market prices. This provides us with univariate default distributions , , . However, this is not enough to infer , the distribution of the first default time . The survival distribution of is given by the diagonal of the joint survival distribution, which we cannot infer solely based on the univariate statistics at our disposal. In order to fill that gap, one needs to assume a dependence structure between the default times, while preserving the (market implied) individual survival probabilities. Here we achieve this with the help of our derived Sibuya copula class. In the following, we shall see how one can derive the FTD default distribution. Interestingly, in our framework, the later will be shown to admit a closed form expression; this is remarkable noting that this is not the case even for the “simple” Gaussian copula model. Since the purpose of this paper is not to discuss how the copula parameters can be calibrated and in order to avoid entering the technical details related to the application, we assume them as given (e.g., by an expert).

For simplicity, assume the individual default times have the same survival function calibrated to CDS market quotes. Technically, this corresponds either to a one-point or to a flat CDS spread curve. For the joint dependence structure of the vector of default times, we use the Sibuya copula as given in (12). Its diagonal is given in (13). Applying Integration by Parts, can be computed as

so that the fair spread, obtained by solving with respect to , is given by

Writing for the exponent appearing in (13), we have , so that

| (15) |

Now let us consider the attainable FTD spreads. The boundary of the -space, i.e., or , corresponds to independence, see (12). In this case takes its largest value (), so does the spread in (15). The lowest attainable FTD spread is obtained for the smallest value of (), which, in turn, is obtained by letting and . The corresponding limiting copula is seen to be the upper Fréchet bound . This corresponds to maximum correlation where all entities default simultaneously when the first jump of the process takes place.

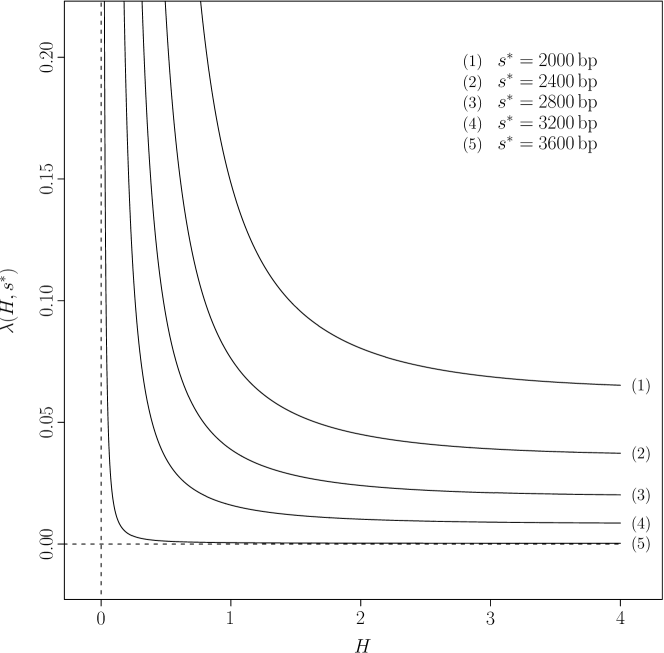

An example of FTD spread level curves is shown in Figure 3.

\setcapwidth

\setcapwidth

0.8

Remark 4.1

The joint default model which led to the Sibuya copula is built on a general default model, assuming stochastic default intensities of some entities. Those should not be confused with the deterministic intensities of the FTD basket constituents, bootstrapped from the CDS market. In other words, there is no obvious link between the functions , , involved in the copula definition (and solely used to build the dependence function) and the univariate survival functions of the constituents of the basket, which will be plugged in the copula in order for the joint survival function to have the market-implied margins. However, in the particular case where one sets the model parameters , , such that the functions are equal to the (CDS-based) survival probability curves , , then the link becomes obvious, namely each realization of the stochastic survival process can be seen as a possible default probability curve for the th entity, to which some probability is assigned, and such that . Thus, the intuitive framework based on random intensities translates to the basket constituents only in this case.

5 Generalizations

A key feature of our model is that it can be easily extended without affecting its tractability. In this section we briefly investigate some generalizations of the copula construction via the default model specified in (3), (4), and (5) and show that it remains perfectly workable. Although a lot of such extensions are possible (for instance, the scalar could be made name-specific so that the jumps are rescaled in a name-specific fashion, or replacing the jump process by a sum of jump processes each with possibly different scaling coefficients, etc.), we restrict ourselves to analyze two possible generalizations. First, we replace the single jump process by a hierarchy of jump processes , . Then, we address the case of dependent trigger variables .

5.1 Generalization to hierarchical jump processes

The jump process is fatal in the sense that it hits all components of the default model simultaneously. In practical applications, it might be the case that only certain subgroups of components get hit. Such a hierarchical or sectorial behavior may be modeled via (possibly dependent) jump processes for , where is the number of sectors or subgroups. These subgroups often arise naturally from the application considered, e.g., by given industry sectors, macroeconomic effects, geographical regions, political decisions, or consumer trends. A default model incorporating such hierarchies can be constructed with the stochastic processes , , in (4) being replaced by

The corresponding individual survival processes are then given by , , and the default time of entity in sector by , where , independent for all , . For simplicity, we assume the jump processes , , to be independent in what follows. Then the joint survival function can be derived similarly as in the proof of Theorem 2.4. First note that the individual survival functions are given by , , , . The joint survival function can then be calculated as

where denotes the th smallest value of all components in sector . The corresponding copula is thus given by

which is a product of Sibuya copulas and therefore itself of the Sibuya type. Therefore, Sibuya copulas are able to capture such hierarchical default dependencies.

5.2 Generalization to dependent trigger variables

Now let us introduce dependence among the default triggers via , i.e., the trigger variables , , are dependent according to the copula . Note that this does not influence the marginal distributions , , as given in (16). Redoing the calculations as carried out in the proof of Theorem 2.4 leads to joint survival function

The corresponding copula is therefore given by

Example 5.1

Let us assume the homogeneous case, i.e., assume that, pointwise, for all . This implies that, pointwise, , . As an example where the copula is given explicitly, consider for , i.e., is a convex combination of the upper Fréchet bound copula and the independence copula . In this case, applying Theorem 2.4 leads to

The copula corresponding to is therefore given by

where . Thus, we recognize that is a convex combination of the upper Fréchet bound copula and the Sibuya copula as given in (10) for the homogeneous case.

6 Conclusion

We introduced an intuitive default model which extends the classical intensity-based approach by allowing the survival process to jump downwards, i.e., to be stochastic. We then derived the survival distribution and, as a corollary, the associated copula which is proven to be of Sibuya type. For that reason, they are named Sibuya copulas. Since the parameters of the marginal survival functions of the default times appear in the copula, Sibuya copulas allow for asymmetries. Due to the jump process in the construction, they allow for a singular component. We also showed that Sibuya copulas may be extreme-value copulas or Lévy-frailty copulas, depending on the functional parameters chosen. From the construction principle presented, a sampling algorithm for these copulas is derived. Further, properties including positive lower orthant dependence, tail dependence, and extremal dependence are investigated. A financial application consisting in the pricing of first-to-default swaps is given, and the nice-looking related expressions further emphasize again the interesting tractability of the model. This tractability most likely results from the relatively simple form of the integrated intensity process (although corresponding to a quite general setup) combined to the Sibuya property. Finally, we showed that the dependence model easily extends in various ways, and, as an illustration, explicitly derived the construction of Sibuya copulas for two of them.

Appendix A Proofs

A.1 Proof of Lemma 2.3

A.2 Proof of Theorem 2.4

-

Proof

First consider the th marginal survival function , . By conditioning on , it can be computed via(16) Given this result and Lemma 2.3 (1) with , , the joint survival function of the default times can be computed via

where, in the second last equality, the independence assumption between any non-overlapping increments of the jump process is used. ∎

A.3 Proof of Proposition 3.2

-

Proof

The survival copula corresponding to can be recovered from by the Poincaré-Sylvester sieve formula. This implieswhere denotes the indicator of being in , . Now consider the term . If there is no such that , i.e., if , then . If there is precisely one such that , then if and if . If there are precisely two different in such that , then if and if . Continuing this way one obtains that

This implies that

where and , . Finally, note that

With these two ingredients, we obtain

The first statement now directly follows from the formula for . For the second statement, apply l’Hôpital’s Rule. ∎

References

- Anderson et al. (1992) J. E. Anderson, T. A. Louis, N. V. Holm, and B. Harvald. Time-Dependent Association Measures for Bivariate Survival Distributions. Journal of the American Statistical Association, 87(419):641–650, 1992.

- Bielecki and Rutkowski (2002) T. Bielecki and M. Rutkowski. Credit Risk: Modeling, Valuation and Hedging. Springer, 2002.

- Cont and Tankov (2004) R. Cont and P. Tankov. Financial Modelling with Jump Processes. Chapman & Hall/CRC Financial MAthematics Series, 2004.

- Devroye (1986) L. Devroye. Non-Uniform Random Variate Generation. Springer, 1986.

- Embrechts et al. (2001) P. Embrechts, F. Lindskog, and A. J. McNeil. Modelling Dependence with Copulas and Applications to Risk Management. 2001. http://www.risklab.ch/ftp/papers/DependenceWithCopulas.pdf (2009-12-30).

- Frahm (2006) G. Frahm. On the extremal dependence coefficient of multivariate distributions. Statistics & Probability Letters, 76:1470–1481, 2006.

- Hofert and Scherer (2010) M. Hofert and M. Scherer. CDO pricing with nested Archimedean copulas. Quantitative Finance, (1):1–13, 2010. http://dx.doi.org/10.1080/14697680903508479 (2010-06-09).

- Hull and White (2008) J. Hull and A. White. Dynamic Models of Portfolio Credit Risk : A simplified Approach. Journal of Derivatives, 15(4):9–28, 2008.

- Joe (1997) H. Joe. Multivariate Models and Dependence Concepts. Chapman & Hall/CRC, 1997.

- Li (2000) D. X. Li. On Default Correlation: A Copula Function Approach. The Journal of Fixed Income, 9(4):43–54, 2000.

- Mai and Scherer (2009a) J.-F. Mai and M. Scherer. A tractable multivariate default model based on a stochastic time-change. International Journal of Theoretical and Applied Finance, 12(2):227–249, 2009a.

- Mai and Scherer (2009b) J.-F. Mai and M. Scherer. Lévy-frailty copulas. Journal of Multivariate Analysis, 100:1567–1585, 2009b.

- Marshall and Olkin (1967) A. W. Marshall and I. Olkin. A multivariate exponential distribution. Journal of the American Statistical Association, 62:30–44, 1967.

- Nelsen (2007) R. B. Nelsen. An Introduction to Copulas. Springer, 2007.

- Schönbucher (2003) P. J. Schönbucher. Credit Derivatives Pricing Models. Wiley, 2003.

- Schönbucher and Schubert (2001) P. J. Schönbucher and D. Schubert. Copula-Dependent Default Risk in Intensity Models. 2001. http://papers.ssrn.com/sol3/papers.cfm?abstract_id=301968 (2009-12-30).

- Sibuya (1959) M. Sibuya. Bivariate extreme statistics, I. Annals of the Institute of Statistical Mathematics, 11(2):195–210, 1959.

- Vrins (2010) F. D. Vrins. Analytical Pricing of Basket Default Swaps in a Dynamic Hull & White Framework. 2010. http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1590932 (2010-05-11).