Cumulant Expansion and Monthly Sum Derivative

Abstract

Cumulant expansion is used to derive accurate closed-form approximation for Monthly Sum Options in case of constant volatility model. Payoff of Monthly Sum Option is based on sum of caped (and probably floored) returns. It is noticed, that can be used as a small parameter in Edgeworth expansion. First two leading terms of this expansion are calculated here. It is shown that the suggest closed-form approximation is in a good agreement with numerical results for typical mode parameters.

1 Introduction

Monthly Sum (MS) Options are embedded into popular fixed index annuities. In contrast to plain vanilla options, the closed-form formula for MS derivative is not known even in the simplest case of constant volatility and we need to use Monte-Carlo simulations to price them. To derive accurate approximation for MS options we can use some sort of expansion with small parameter. In the next section we will shown that MS derivative can be considered as a Call option on underlying with caped (and probably floored) returns. Caped distribution is very different from Gaussian one but, according to the central theorem, in the limit of large number of returns (), the final distribution at time of expiration will be close to the normal one. So, in the leading approximation, we can use standard European Call formula to price MS options[1],[2].

To calculate corrections we need to choose convenient way to approximate non-normal distributions of caped underlyings. Various types of expansions in series of Hermit polynomials are used in science to approximate distributions: namely Gram-Charlier, Gauss-Hermite and Edgeworth. But Gram-Charlier series has poor convergence properties [3]. Gauss-Hermit expansion is better but it has no expansion parameter and therefore it has no intrinsic measure of accuracy. The most prominent is Edgeworth expansion which has an expansion parameter [4]. This expansion is a true asymptotic series and has good convergence properties.

Here we consider Black-Scholes case of constant market volatility. It is shown, that for typical Monthly Sum option and market parameters, first two leading terms of this expansion give a good approximation for MS derivative. Note, that these first two terms of cumulant expansion are identical for all three types of cumulant expansion. But next corrections need to be grouped as terms of Edgeworth series to be a true asymptotic expansion with as a small parameter. Higher terms of cumulant expansion can improve accuracy of this approximation.

2 Monthly Sum Derivative

Monthly Sum option (MS) is defined as a derivative which payoff at the time of expiration is

| (1) |

where

| (2) |

are caped returns.

In the case of small returns we can use logarithmic returns to approximate returns (2)

| (3) |

where , and the derivative payoff is

| (4) |

where

| (5) |

It means that we can consider MS option as a call option on caped distribution.

| (6) |

where is a call payoff on the caped underlying

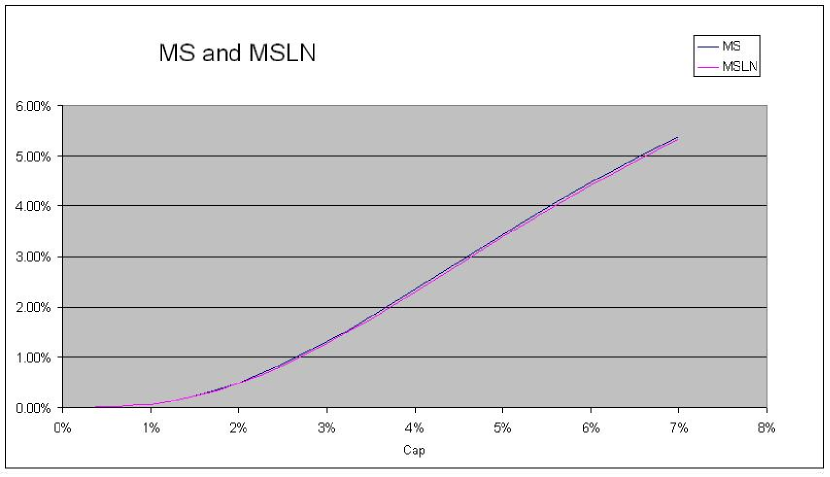

Fig.1 demonstrates that, for typical market parameters, MSLN can be used as an accurate approximation for Monthly Sum derivative.

3 Distribution Function and Cumulant Expansion

To calculate call option value in eq.(6) and therefore to calculate MS derivative, we need to know distribution of caped underlying (5).

To approximate this distribution at expiration time, it is convenient to represent probability distribution function of logarithmic returns at time of expiration in the form of infinite series as

| (7) |

where is a logarithmic return, is a price of caped underlying at time , is -term of Edgeworth expansion, and are Hermit polynomials:

| (8) |

Therefore the value of Monthly Sum derivative is

| (9) |

where

| (10) |

are terms of Edgeworth expansion for Monthly Sum option, is interest rate.

Calculating moments of distribution function we can determine parameters of this expansion:

| (11) |

where are cumulants.

Using the fact that cumulant of sum of independent variables is equal to sum of cumulants, it is easy to calculate cumulants of longer term distributions as

| (12) |

where is number of time intervals (months) and is a cumulant of caped monthly distribution.

Monthly cumulants can be expressed in terms of moments as

| (13) |

where

| (14) |

are moments of caped distribution, is a time interval, is a market volatility,

| (15) |

is a risk neutral drift, is a dividend yield.

First two moments of caped distributions and give us parameters of leading order approximation for distribution function of caped underlying:

| (16) |

It means, that in the leading approximation, MS derivative value is an European ATM call option with volatility and drift . To set correct value for drift we need to adjust dividend yield to its effective value

| (17) |

Then, the price of Monthly Sum derivative in the leading order of cumulant expansion is

| (18) |

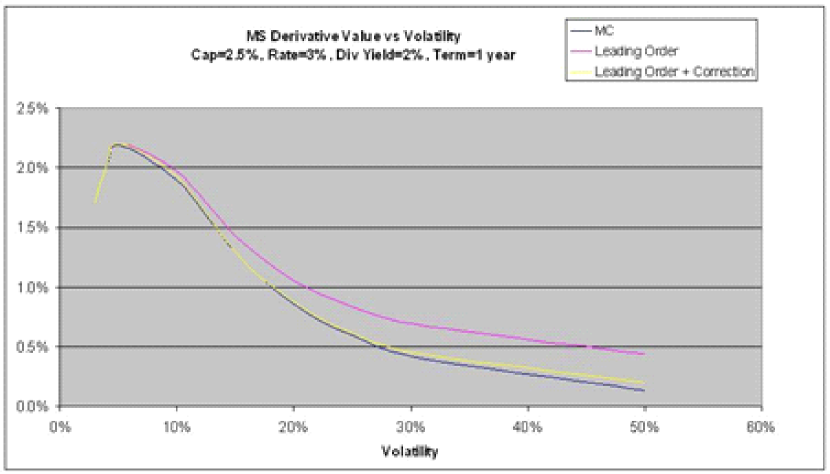

On Fig.2 we can observe that the accuracy of leading order approximation for One Year MS option with is not good for market volatility . To improve accuracy we need to take into account higher terms of cumulant expansion (7).

The first correction to the leading term of cumulant expansion for probability distribution function (7) is

| (19) |

and according to eq.(13)

| (20) |

As can we see on Fig.2 this correction significantly improve accuracy of approximation.

Formulas for moments of caped distribution and integral for ( eq.(10)) are presented in Appendix.A.

We also can consider MS derivative for caped returns with floor:

| (21) |

In this case, moments of this distributions can be calculated as

4 Conclusions

In present paper we apply Cumulant Expansion to derive closed form approximation for Monthly Sum options. It is shown, that for typical MS derivative and market parameters this approximation works well. Calculation of higher terms of Edgeworth expansion can improve accuracy of derived approximation.

References

- [1] F. Black, M. Scholes The Pricing of Options and Corporate Liabilities, Journal of Political Economy, 81 (1973) 637-659.

- [2] R.C. Merton Theory of Rational Option Pricing, Bell Journal of Economics and Management Science, 81 (1973) 141-183.

- [3] H. Cramér, Mathematical Methods of Statistics, Princeton University Press, Princeton (1957).

- [4] S. Blinnikov, R. Moessner, Expansions for neatly Gaussian distributions, Astronomy & Astrophysics Supplement Series 130 (1998), 193-205.

‘ Appendices

Appendix A Moments of caped distributions and correction to MS price.

Below, we present formulas for the first three moments of caped distribution

| (A.1) |

where

| (A.2) |

| (A.5) |

and is Dirac -function.

| (A.6) | |||||

| (A.7) | |||||

| (A.8) | |||||

First correction to the leading approximation (10) has integral which can be presented in the following form:

| (A.9) |

To calculate MS derivative value with local floor, we need to calculate integrals in eq.(22) . This integrals can be presented in the following form

| (A.10) |

where

| (A.11) |

Using that

| (A.12) |

where

| (A.13) |

we obtain the following formulas for the first three moments of the caped-floored distribution

| (A.14) | |||||

| (A.15) | |||||

| (A.16) | |||||