Outliers in the spectrum of iid matrices with bounded rank perturbations

Abstract.

It is known that if one perturbs a large iid random matrix by a bounded rank error, then the majority of the eigenvalues will remain distributed according to the circular law. However, the bounded rank perturbation may also create one or more outlier eigenvalues. We show that if the perturbation is small, then the outlier eigenvalues are created next to the outlier eigenvalues of the bounded rank perturbation; but if the perturbation is large, then many more outliers can be created, and their law is governed by the zeroes of a random Laurent series with Gaussian coefficients. On the other hand, these outliers may be eliminated by enforcing a row sum condition on the final matrix.

1. Introduction

This paper is concerned with the study of outliers of the circular law for iid random matrices and its variants. To recall this law, we make some definitions:

Definition 1.1 (iid random matrix).

An iid random matrix is an random matrix (or more precisely, a nested sequence of such matrices) whose entries for are independent identically distributed complex entries, which we normalise to have mean zero and variance one. We say that such a matrix has atom distribution if all the have distribution , thus and .

Definition 1.2 (ESD).

Given an complex matrix (not necessarily Hermitian or normal), we define the empirical spectral distribution of to be the probability measure

where for are the eigenvalues of (counting multiplicity, and ordered arbitrarily).

If is a random complex matrix (so that is also random), we say that converges in probability (resp. almost surely) to another (Borel) probability measure on the complex plane if for every smooth, compactly supported function , converges in probability (resp. almost surely) to .

The following theorem is the culmination of the work of many authors [23], [33], [24], [4], [6], [26], [25], [34], [42], [27], [44]:

Theorem 1.3 (Circular law for iid matrices).

Let be an iid random matrix. Then converges almost surely (and hence also in probability) to the circular measure , where .

The result as stated is [44, Theorem 1.15], but this result is based on a large number of partial results (in which more hypotheses are placed on the atom distribution ) which are proven in the previously cited papers.

The circular law implies in particular that the spectral radius

is at least almost surely, where goes to zero as . When the atom distribution has finite fourth moment, we in fact have an asymptotic for the spectral radius:

Theorem 1.4 (No outliers for iid matrices).

Let be an iid random matrix whose atom distribution has finite fourth moment: . Then converges to almost surely (and hence also in probability) as . In fact, for any finite , converges to almost surely (and hence also in probability) as .

Furthermore, if all moments of are finite, one has the tail bound

with overwhelming probability111We say that an event depending on occurs with overwhelming probability if for every there exists such that for all . for each .

Proof.

This follows from what is by now a routine application of the truncation method and the moment method; see [10], [22], or [9, Theorem 5.17]. We remark that the tail bound can also be deduced from the main result using the Talagrand concentration inequality (after first truncating to the case when is bounded); see [28], [1], [32]. The precise expression is not important for our arguments here; any quantity that was subexponential in would have sufficed. ∎

Informally, Theorem 1.4 asserts that when the fourth moment is finite, there are no significant outliers to the circular law: with probability222The asymptotic notation that we use here will be defined in Section 1.3. , all of the eigenvalues of the matrix lie within of the support of the circular law. The fourth moment condition here is necessary for the second conclusion of Theorem 1.4 (see [9]), and it is very likely that it is also necessary for the first conclusion.

Now we consider the circular law and its outliers for random matrices formed as a low-rank perturbation of an iid random matrix. The circular law is stable under such perturbations:

Theorem 1.5 (Circular law for low rank perturbations of iid matrices).

[44, Corollary 1.17] Let be an iid random matrix, and for each , let be a deterministic matrix with rank obeying the Frobenius norm bound

Then converges both in probability and in the almost sure sense to the circular measure .

Remark 1.6.

Thanks to a recent result of Bordenave [16], the bound here can be relaxed to .

However, the low rank perturbation can now create outliers. Our first main result is to describe these outliers in the case when has bounded rank and bounded operator norm, and has finite fourth moment. In this case, it turns out that the outliers of are close to those of . More precisely, we have

Theorem 1.7 (Outliers for small low rank perturbations of iid matrices).

Let be an iid random matrix whose atom distribtuion has finite fourth moment, and for each , let be a deterministic matrix with rank and operator norm . Let , and suppose that for all sufficiently large , there are no eigenvalues of in the band , and there are eigenvalues for some in the region . Then, almost surely, for sufficiently large , there are precisely eigenvalues of in the region , and after labeling these eigenvalues properly, as for each .

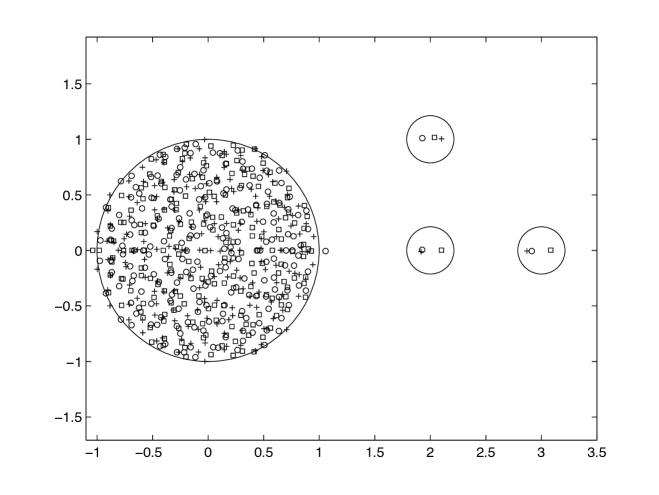

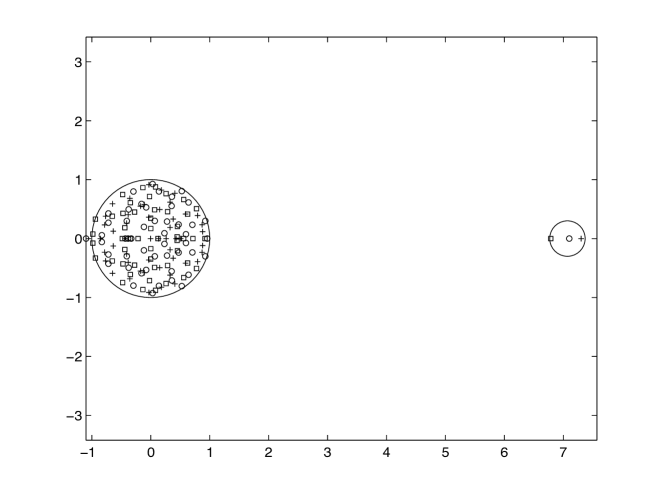

Thus, for instance, if one perturbs by a bounded rank, bounded operator norm matrix whose eigenvalues all lie inside the unit disk (e.g. could be a nilpotent matrix), then no outliers are created; but once has eigenvalues leaving the unit disk, the perturbed matrix will also have outliers in asymptotically the same location. Theorem 1.7 is illustrated in Figures 1, 2.

Remark 1.8.

An analogous result for Wigner matrices instead of iid matrices has recently been established in [18], [37], with more precise control (in particular, a central limit theorem) on the distribution of the outlier eigenvalues; the methods used are somewhat different, but the techniques developed here can be adapted to the Wigner case (Alexander Soshnikov, private communication). See also [21], [13] for further results in the Wigner case, whose methods are close to those used here, [35] for a treatment of the GUE case, [11] for a treatment of the LUE case, and [5], [12], [7] for a treatment of the covariance matrix case. Interestingly, in the Wigner case the outlier eigenvalues of the perturbed matrix are not close to the outlier eigenvalues of the original matrix, but rather to the shifted eigenvalues , where is the variance of the entries of the Wigner matrix . This is ultimately because the powers have a significant presence on the diagonal in the Wigner case, in contrast with the iid case where all entries are small. Alternatively: the Wigner semicircular law has nonzero moments, while all nontrivial (pure) moments of the circular law vanish.

Theorem 1.7 is proven in Section 2. The main tools are asymptotics of Stieltjes transforms outside of the unit disk , combined with the fundamental matrix identity333We thank Percy Deift for emphasising the importance of this identity in random matrix theory.

| (1) |

valid for arbitrary matrices and matrices . Note that the left-hand side is an determinant, while the right-hand side is a determinant. For low rank perturbations, we will be able to apply (1) with bounded and going to infinity, allowing one to transform an unbounded-dimensional problem into a finite-dimensional one.

Theorem 1.7 only deals with perturbations that are relatively small, having an operator norm of . It is also of interest to consider larger perturbations, such as those caused by adjusting the mean of each coefficient of by . Here, the situation is more complicated, and we will consider only a few model perturbations, rather than attempt to obtain the most general result.

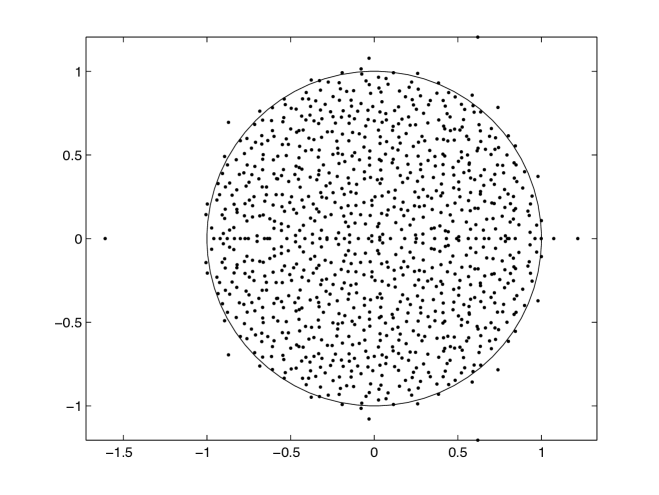

We first consider the case of iid matrices with non-zero mean, which we write as , where is a fixed complex number (independent of ) and is the unit column vector ; this corresponds to shifting the atom distribution by (so that it has mean rather than mean zero). This is a rank one perturbation of . The circular law still holds for this ensemble, thanks to Theorem 1.5 (or the earlier result of Chäfai [19]). However, in view of Theorem 1.7, we expect a single large outlier near . This is indeed the case:

Theorem 1.9 (Outlier for iid matrices with nonzero mean).

Let be an iid random matrix whose atom distribution has finite fourth moment, and let be a non-zero quantity independent of . Then almost surely, for sufficiently large , all the eigenvalues of lie in the disk , with a single exception taking the value .

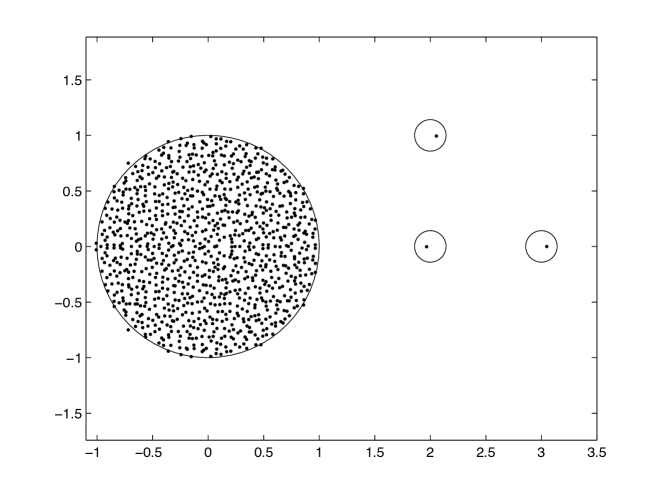

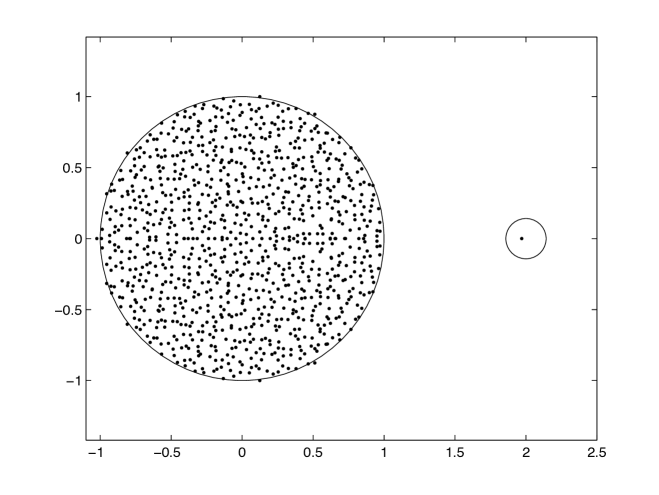

We prove this result in Section 3. One can obtain more precise information on the distribution of this exceptional eigenvalue, particularly if one assumes more moment hypotheses on the atom distribution ; see [41]. The existence of this exceptional eigenvalue was already noted back in [2]. Theorem 1.9 is illustrated in Figure 3. Figure 4 corresponds to the case of a smaller value of , and falls instead under the regime covered by Theorem 1.7.

Next, we consider a model that was introduced in [39], in the context of neural networks. In our notation, this model takes the form

| (2) |

where is a fixed parameter, and is a random matrix (independent of ) such that the columns of are iid, with each column equal to with probability and with probability , for some fixed . (In the notation of [39], the excitatory mean is and the inhibitory mean is , and the excitatory and inhibitory variances are assumed to be equal.) Note that one can write

| (3) |

where is a random vector whose entries are iid and equal with probability and with probability ; with this normalisation, has mean zero and unit variance.

Again, by Theorem 1.5, the ESD of is governed by the circular distribution in the limit ; however, as observed numerically in [39], a small number of outliers also appear for .

It is possible to explain the outliers by the arguments of this paper. However, in contrast to the situations in Theorem 1.7 or Theorem 1.9, in which the outliers essentially have a deterministic location up to errors, for the model (2), the outliers retain significant randomness at macroscopic scales, and need to be modeled by a point process rather than by a deterministic law. To describe this point process, we introduce the -point correlation functions for the ESD of for , defined as the unique symmetric function such that

for all continuous, compactly supported test functions ; note that the right-hand side is not dependent on how one orders the eigenvalues of . Here, denotes two-dimensional Lebesgue measure on . If the atom distribution of is discrete, then needs to be interpreted as a distribution or measure rather than as a function, but this technicality will not concern us here.

It turns out that the correlation functions have a limiting law outside of the unit disk (inside the disk, one expects these functions to go to infinity, thanks to the circular law and the choice of normalisation). We do not have a completely explicit formula for this limit, but can describe it instead as the zeroes of a random Laurent series. More precisely, consider the random Laurent series

where are iid copies of the real Gaussian distribution . From the Borel-Cantelli lemma we see that this Laurent series is almost surely convergent in the complement of the closed unit disk , and almost surely has a finite number of zeroes in the region for any fixed . We then define the limiting correlation function outside of this disk as the unique symmetric function (or more precisely, distribution) such that

| (4) |

for all continuous, compactly supported test functions , where are the zeroes of (counting multiplicity); a little more explicitly, can be defined for distinct as

where is the probability of the event that there is a zero of within of for each .

Remark 1.10.

If the were complex Gaussian instead of real, we normalised , and we replaced the constant coefficient by another complex gaussian , then would be a Gaussian power series (GPS) in the variable . Gaussian power series have been intensively studied (see the recent text [29] and the references therein). In that case, the -point correlation functions are given by the determinantal formula

see [36]. One may then hope that a somewhat analogous formula might be obtained for the random Laurent series considered here, possibly using the explicit formulae for the correlation functions of zeroes of real random polynomials from [38] as a starting point. We will not pursue this matter.

We can now state our main theorem regarding this model, which we prove in Section 5:

Theorem 1.11 (Limiting law).

Let be an iid random matrix whose atom distribution is real-valued and which is either gaussian (i.e. ) or bounded, and let and be fixed. Let , , and be defined as above.

-

(i)

(Crude upper bound) For any , let denote the number of eigenvalues of in the region (counting multiplicity). Then for all and .

-

(ii)

(Limiting law) converges in the vague topology to on . In other words, one has

whenever is continuous and compactly supported (in particular, it is supported in the region for some ). In particular, the limiting distribution is universal with respect to the distribution .

Remark 1.12.

The requirement that all the coefficients of are real is a natural one from the neural net application[39]. However, in view of the better developed theory for complex Gaussian power series[29], it may in fact be more natural from a theoretical perspective to consider the case when the are complex valued, e.g. if the atom distribution is complex Gaussian. In that case, there is a similar result to Theorem 1.11 but with the coefficients of the random Laurent series given by complex Gaussians rather than real Gaussians; we omit the details. The requirement that be either Gaussian or bounded is a technical one, so that one may apply concentration inequalities; it may certainly be relaxed substantially.

1.1. Zero-sum matrices

Next, we consider a different low-rank perturbation of an iid matrix model, in which the row sums of the matrix are forced to equal zero. Introduce the orthogonal projection matrix

thus is the orthogonal projection onto the hyperplane .

Our first result is that the presence of this projection does not affect the circular law, nor does it create any outliers:

Theorem 1.13.

Let be an iid random matrix. Then converges both in probability and almost surely to the circular measure , and almost surely one has .

We prove this theorem in Section 6, using the machinery from [44]. The main difficulty is to ensure that the least singular value of is well controlled for any fixed , but this can be achieved dropping one dimension (and freezing some of the entries of ) to eliminate the role of (at the cost of replacing the deterministic matrix by a more complicated matrix). This result is somewhat analogous to the result of [17] establishing the circular law for random Markov matrices (under an additional bounded density hypothesis on the atom distribution), although the situation is more complicated in that case because a slightly nonlinear transformation is required in order to convert a iid random matrix to a Markov matrix, in contrast to the simple linear transformation required to make the rows sum to zero.

Suppose that is a vector orthogonal to , then and . Then from two applications of (1) we have

We thus see that and have the same characteristic polynomial, and thus the same ESD and the same spectral radius. (One can also establish these facts directly without much difficulty, as was done in [39].) We thus obtain

Corollary 1.14.

Let be an iid random matrix, and for each , let be a (possibly random, and -dependent) vector which is orthogonal to . Then converges both in probability and almost surely to the circular measure , and almost surely one has .

In particular, no outliers are created no matter how large is (or how aligned it is with ). These results were established in [39] in the gaussian case. This is in sharp contrast to the situation in Theorem 1.11 for the model (3), which is similar to the matrix , but without the projection.

Remark 1.15.

Our results here are only effective in the region where the spectral parameter has magnitude larger than that of the spectral radius. It would be of interest to determine what happens in models where the eigenvalue law of the base matrix is not governed by a circular law, but by another law whose support does not occupy the entire disk given by the spectral radius (e.g. matrices whose ESD is concentrated in an annulus). In the covariance matrix case, results in this direction appear in [5], [7].

1.2. Acknowledgments

This work was conducted during a workshop at the American Institute of Mathematics. We thank Larry Abbott for raising these questions. After posing this question at the workshop, Alice Guionnet provided the key insight, namely to reduce matters to studying coefficients of the resolvent of , while Percy Deift emphasised the significance of the identity (1) to questions of this type (and indeed, this identity is crucial in order to efficiently handle the higher rank case ). The author also thanks Sasha Soshnikov and Phillip Wood for useful discussions, Florent Benaych-Georges, Djalil Chafai and Raj Rao for references, and Phillip Wood for corrections. We are also indebted to Phillip Wood for supplying the figures for this paper. Finally, we thank the anonymous referees for many helpful comments, corrections, and references.

1.3. Asymptotic notation

Throughout this paper, is an asymptotic parameter going to infinity. We use to denote any quantity that is bounded in magnitude by an expression that goes to zero as , keeping all other parameters independent of (e.g. ) fixed. Similarly, we use or to denote the estimate where the implied constant is independent of but may depend on on parameters independent of .

2. Small low rank perturbation

We now prove Theorem 1.7. Fix and , as in that theorem. By hypothesis, has rank at most for some independent of , and an operator norm of . By the singular value decomposition, we can write for some and matrices , both of operator norm .

We have the following description444We are indebted to Alice Guionnet for proposing the case of this formula, as well as the basic strategy of proof used in this paper, and Percy Deift for emphasising the importance of the identity (1). of the eigenvalues of in terms of a determinant:

Lemma 2.1 (Eigenvalue criterion).

Let be a complex number that is not an eigenvalue of . Then is an eigenvalue of if and only if

| (5) |

Proof.

Clearly, is an eigenvalue of if and only if

By hypothesis, is invertible and , so we may rewrite this equation as

The claim now follows from (1). ∎

Remark 2.2.

The above argument in fact shows that

whenever the denominator is nonzero. We are indebted to Alice Guionnet for suggesting the use of this type of criterion, versions of which also appear in [3], [8], [18], [13], [14], [15]. For instance, the case of this criterion appears explicitly in [13]. In [3] the expression in this identity (which is stated there in the case of symmetric matrices) is referred to as the modified Weinstein determinant. (We thank Raj Rao for this reference.)

Introduce the functions

These are both meromorphic functions that are asymptotically equal to at infinity, with being a rational function of degree at most with bounded coefficients. Lemma 2.1 tells us that outside of the spectrum of , the zeroes of agree with the eigenvalues of . An inspection of the argument also reveals that the multiplicity of a given such eigenvalue is equal to the degree of the corresponding zero of . Similarly, replacing by the zero matrix in Lemma 2.1, we see that outside of the origin, the zeroes of are precisely the eigenvalues of (counting multiplicity). Indeed, from (1) one has

where are the non-trivial eigenvalues of (some of which may be zero), including of course the eigenvalues of magnitude at least .

By Theorem 1.4, we see that almost surely, the spectrum of is contained in the disk for sufficiently large . In view of Rouche’s theorem (or the argument principle), together with the fact that the coefficients of are bounded, it then suffices to show that the quantity

converges almost surely to zero. Since is fixed and are bounded in operator norm, it suffices to show that

converges almost surely to zero.

By Theorem 1.4, we almost surely have

for each . In particular, there exists such that

for sufficiently large , which also implies that one has

for all and some almost surely finite random variable . This ensures that the Neumann series

is absolutely convergent in the operator norm, uniformly in both and , when is sufficiently large and . By the dominated convergence theorem, it thus suffices to show that the matrix

converges almost surely to zero for each fixed . Breaking and into components, it suffices to show the following claim:

Lemma 2.3 (Coefficient bound).

Let be an iid random matrix whose atom distribution has finite fourth moment. Then

| (6) |

almost surely for each fixed and any fixed (deterministic) sequence of unit vectors .

We now prove the lemma.555We thank Jean Rochet for pointing out an error in a previous version of this argument.

The atom distribution is currently only assumed to have finite fourth moment. However, a standard truncation argument (using the results of [9] to control the contribution of the tail of ) shows that we may almost surely approximate to arbitrary accuracy in operator norm by an iid matrix in which the atom distribution is in fact bounded. As such, it will suffice to prove the lemma under the additional assumption that is bounded. In particular, all moments of are now finite: for all fixed .

By diagonalising the covariance matrix of and , we may assume (after a phase rotation) that and have zero covariance, and have variances and respectively for some . Next, by splitting into real and imaginary parts and renormalising, we may assume without loss of generality that have real coefficients. Finally, by orthogonal decomposition of , we may assume that is either equal to for all , or is orthogonal to for all .

We decompose

where is the projection onto trace zero matrices.

From the circular law (Theorem 1.3), using Theorem 1.4 to control the outliers, we have

almost surely. Thus it suffices to show that

almost surely.

We now use the moment method666We thank David Renfrew and Sean O’Rourke for pointing out an error in the initial version of this manuscript, which only established Lemma 2.3 in probability rather than in the almost sure sense.. It will suffice to show that

| (7) |

Indeed, this implies from Markov’s inequality that with probability , and Lemma 2.3 then follows from the usual truncation argument. The bound is not optimal (the truth should be ), but will suffice for this purpose.

We first deal with the model case when is normally distributed with the the normal distribution (with the real and imaginary parts independent). As is well known, in this case the ensemble is invariant under conjugation by orthogonal matrices. This implies that the expression does not change if we simultaneously conjugate by an orthogonal matrix. In particular, if are orthogonal, we may keep deterministic, but replace by a random unit vector chosen uniformly from the orthogonal complement of on the unit sphere, independently of . However, a short computation in cylindrical coordinates (or Levy’s concentration of measure theorem) shows that for any deterministic vector , one has if is a unit vector drawn uniformly from the orthogonal complement of on the sphere. Thus we can bound the left-hand side of (7) by

By Theorem 1.4, the inner expectation is , and the claim (7) follows in the Gaussian case when and are orthogonal.

Now suppose that . By the conjugation invariance, it suffices to show that

when is drawn uniformly from the unit sphere independently of . For fixed , this expression depends on in a Lipschitz fashion with Lipschitz constant , and its mean is zero since is trace zero. The claim then follows from the Levy concentration of measure theorem and Theorem 1.4. This completes the proof of (7) in the Gaussian case.

To handle the non-gaussian case, it thus suffices to show that

where are the coordinates of the unit vectors , and are iid copies of the complex normal distribution .

Consider the collection of ordered pairs

| (8) |

for . From the iid nature of , and the fact that the random variables and match up to second order, we see that each summand in the above expression vanishes unless each ordered pair appears with multiplicity at least two, and at least one pair appears at least three times; in particular, there are at most distinct ordered pairs. As have all moments finite, we may thus bound the above expression in magnitude by

where denotes the sum over all tuples such that the ordered pairs (8) are such that each pair occurs at least twice, and at least one pair occurs three or more times; in particular there are at most distinct pairs. Our task is now to show that

| (9) |

Suppose that are such that (8) is of the stated form. Let be the unordered looped graph with edges being the unordered pairs associated to (8) and with vertices being the elements of these pairs, and let be the number of connected components of . Then , and has at most edges and thus at most vertices.

We consider first the contribution of those tuples for which has at most vertices; this is for instance the case if contains a cycle or a looped edge, or has strictly fewer than edges. Then if one fixes , then one has fixed at least one vertex in each component of , leaving at most remaining vertices. Thus there are choices for the remaining data ; summing over using the fact that is a unit vector yields that

and similarly

and so by Cauchy-Schwarz the contribution of the tuples to (9) is acceptable.

Now consider the contribution of those tuples for which has exactly vertices, but such that two of the are distinct elements of a common component of . Then as in the case, fixing leaves only choices for the remaining data, so that

while we also have the cruder bound

so by Cauchy-Schwarz this contribution is also acceptable. Similarly if has vertices but two of the are distinct elements of a common component of .

The only remaining contribution comes from the case when has exactly vertices, the agree whenever they lie in a common component of , and agree whenever they lie in a common component of . As discussed previously, the requirement that has exactly vertices forces to be a forest (a union of disjoint trees, with no cycles or looped edges) and to contain exactly edges. Among other things, this implies that the tuples (8) do not contain a loop , nor do these tuples contain a pair together with its reversal . If and (for instance) lie in the same component of , then we must then and , and then for all (otherwise there would be a cycle, looped edge, or a pair and its reversal). Thus each component has edges, which is only consistent with the total edge count of if and But in this case the left-hand side of (9) simplifies to

which is easily seen to be , so that (9) easily follows in this case. This completes the proof of Lemma 2.3 and hence Theorem 1.7.

3. Large mean

Now we prove Theorem 1.9. It suffices to show that for any fixed , almost surely one has exactly one eigenvalue of outside of the disk , with this eigenvalue occuring within of .

Fix . By Theorem 1.4, almost surely there are no eigenvalues of outside of the disk. By Lemma 2.1, the eigenvalues of outside this disk are then precisely the solutions (counting multiplicity) to the equation , where is the meromorphic function

By Neumann series, we may expand

where

| (10) |

From Theorem 1.4, we almost surely have

(say) and

for some fixed integer depending only on , and all sufficiently large ; this gives us the truncated Taylor expansion

for any and , where the implied constant is allowed to depend on but not on . Applying Lemma 2.3, we almost surely obtain

for any fixed uniformly for all , and thus (by letting go slowly to infinity) we almost surely have

uniformly for all . From this and (10) we see that has no zeroes in this region except within a neighbourhood of , and from Rouche’s theorem we see that there is exactly one zero of that latter type when is sufficiently large, and the claim follows.

Remark 3.1.

The eigenvector corresponding to the exceptional zero can be explicitly described, by observing the identity

for all non-zero outside of the spectrum of . In particular, if is the outlier eigenvalue, the is the corresponding eigenvector. From Theorem 1.4 and Neumann series, we see that almost surely, this eigenvector lies within of in norm, and a more accurate description of this eigenvector can be given by expanding out the Neumann series further.

4. A central limit theorem

In Lemma 2.3, we showed that the coefficients decayed almost surely to zero. Now we prove a more refined statement on the rate of decay, which is to Lemma 2.3 as the central limit theorem is to the (strong) law of large numbers. This result will be needed to prove Theorem 1.11. For simplicity we consider only real-valued matrices; there is a complex analogue when the real and imaginary parts of have the same covariance matrix as the complex Gaussian , but we will not state it here.

Proposition 4.1 (Central limit theorem).

Let be an iid random matrix whose atom distribution is real-valued, has mean zeero and has all moments finite. Let be a (deterministic) sequence of unit vectors whose coefficients are asymptotically delocalised in the sense that

| (11) |

Then for any fixed , the random variables

| (12) |

for converge jointly in distribution to the law of independent copies of the real gaussian .

We now prove this proposition. By (the multidimensional version of) Carleman’s theorem (see e.g. [6]), it suffices to prove the moment bounds

| (13) |

for any natural numbers , where are iid copies of the real gaussian .

Fix ; we allow all implied constants to depend on these quantities. The left-hand side can be expanded as

| (14) |

where , ,

and ranges over all tuples of indices with , , .

From (11) and the bounded moment hypotheses, we see that each summand (14) is of size , and so we may freely ignore up to summands whenever desired.

For each tuple in the sum , we consider the ordered pairs with , , . By the iid and mean zero nature of the , we see that this sum vanishes unless each ordered pair appears with multiplicity at least two. In particular each of the indices with must occur with multiplicity at least , leading to at most distinct indices. If there are any fewer than distinct indices, then the contribution of this case to (14) is , so we may assume that there are exactly distinct indices, which implies that each index occurs with multiplicity exactly two. This implies that for , each of the arise exactly twice as the initial vertex of an ordered pair, and each of the arise exactly twice as the final vertex of an ordered pair. Furthermore, the indices must be distinct from the indices with , and similarly the must be distinct from the indices with , as otherwise the fact that each ordered pair appears at least twice will lead to a multiplicity of at least three at the repeated index. This implies that the paths are simple paths, which each occur with multiplicity two but are otherwise disjoint. The total contribution of this case to (14) is then

where the sum is over collections of simple paths in which occur with multiplicity two but are otherwise disjoint; here we use the fact that each ordered pair appears exactly twice, and that has unit variance.

In order for all paths to appear with multiplicity two, each of the must be even. This already gives (13) when at least one of the is odd, so we now assume that the are all even. There are different ways in which the paths can be matched up to multiplicity two. Once one fixes such a matching, there are initial vertices of paths, and final vertices , all distinct from each other; if one fixes these vertices, then one has ways to choose the remaining paths. This gives a total contribution to (14) of

We add back in the contributions in which some of the ; this only affects the sum by , which is acceptable. We are left with

since the and square-sum to , this simplifies to

and (13) follows from the standard computation

for even.

5. Large non-selfadjoint perturbation

We now prove Theorem 1.11. It suffices to work in the exterior region for a fixed . Henceforth all implied constants may depend on , , .

5.1. Crude upper bound

We first show the first part of the theorem, namely that for all . Fix ; we allow all implied constants to depend on . Our task is now to show that for all sufficiently large .

From Theorem 1.4 we know that the spectral radius of is at most with overwhelming probability. Using the trivial bound , we see that the tail event when the spectral radius exceeds thus gives a negligible contribution to and will thus be ignored.

Conditioning on the event that the spectral radius is at most , we may then apply Lemma 2.1 to conclude that the eigenvalues of in are precisely the zeroes in of the random analytic function

| (15) |

In particular, is the number of zeroes of in .

The function is analytic in the disk and equals at the origin, with zeroes in the region . Applying Jensen’s formula to this function, we conclude the upper bound

for any radius between and (note that we allow implied constants to depend on ), where and is arclength measure. Averaging, we conclude that

| (16) |

It will thus suffice to establish the bound

| (17) |

for any fixed and any compact subset of the annulus (allowing implied constants to depend on of course).

We now pause to regularise the logarithm slightly, as this will come in handy later. By Remark 2.2, the function is a linear combination of terms of the form for various complex numbers . As such we have a crude upper bound of the form

| (18) |

thanks to the triangle inequality. From this, we have

and so it suffices to show that

By the Fubini-Tonelli theorem, it thus suffices to show that

uniformly for all in .

It will then suffice to show the following lower tail estimates on :

Lemma 5.1 (Lower tail estimates).

Let be in a compact subset of ; we allow implied constants to depend on .

-

(i)

For every there exists (not depending on ) such that

-

(ii)

For every one has

for some absolute constant .

Indeed, item (i) (with ) allows one to reduce to the case when (it is here that we take advantage of our previous regularisation of the logarithm), and then (ii) and a dyadic decomposition gives the claim.

Proof.

We begin with (i). From (3) and (15) we have the identity

and hence

where is the least singular value of . By Theorem 1.4, we have with overwhelming probability. The claim now follows from the least singular value bounds in [44, Lemma 4.1], [42, Theorem 2.1], or [43, Theorem 4.1], since we may express as the sum of the normalised iid random matrix and the deterministic matrix , which has polynomial size.

Now we prove (ii). Let be the vector . It will suffice to show that

for every interval . From Theorem 1.4 and Neumann series, we see that with overwhelming probability,

| (19) |

and so

Let be a small quantity (independent of ) to be chosen later. Call delocalised if we have for at least of the indices . As the coefficients of are iid (and are independent of ), we see from the Berry-Esséen theorem (see e.g. [20, Chapter XVI]) that the contribution of the delocalised are acceptable. It thus suffices to show that is delocalised with probability for some .

We will use an epsilon-net argument (cf. [31], [40]). If is not delocalised, then lies within in norm of a vector of comparable to that is sparse in the sense that it is supported on at most indices, simply by restricting to those indices for which , and truncating all other coefficients to zero. From (19) and the triangle inequality, we thus have

The number of possible supports for is at most , thanks to Stirling’s formula. Once one fixes the supports, one can cover the range of by balls in norm of radius . Thus, by moving by at most if necessary, we may assume that lies in a net of cardinality

| (20) |

For each fixed , the expression is a convex, -Lipschitz function of as measured using the Frobenius norm . Applying777For an extensive discussion of concentration inequalities, see [30]. Note that many other atom distributions also enjoy concentration inequalities, such as those distributions with the log-Sobolev property; we will not attempt to aim for maximal generality here. either the Talagrand concentration inequality (if is bounded) or the Lévy concentration inequality (if is Gaussian), we conclude that

for some absolute constant , where is the median value of . To compute this median, we first compute the second moment

Expanding this out and using the fact that is an iid random matrix, this simplifies to

In particular, this expression is comparable to . From the concentration inequality, we conclude that

if is small enough. Summing up over all using (20) and the union bound, we obtain the claim. ∎

This concludes the proof of part (i) of Theorem 1.11.

5.2. Correlation functions

Now we prove part (ii) of Theorem 1.11. From part (i), we have the bound

| (21) |

for each fixed . A similar (but simpler) argument also shows that

| (22) |

(the point being that the Gaussian random Laurent series has a Gaussian distribution at each with an explicitly computable variance, so one can easily control the moments of ). As a consequence of these bounds, we can control perturbations to the test functions that are small in the uniform norm.

From Theorem 1.4 we know that the spectral radius of is at most with overwhelming probability. The tail event when the spectral radius exceeds is thus negligible for the purposes of computing the asymptotics of the correlation functions and will thus be ignored.

Conditioning on the event that the spectral radius is at most , we may then apply Lemma 2.1 to conclude that the eigenvalues of in are precisely the zeroes in of the random analytic function

Thus, up to errors of , the correlation function is equal on to the correlation function of the zeroes of (defined as in (4)).

As in previous sections, once the spectral radius is at most , we can expand as a convergent Neumann series

where

To control this expression properly, we will need to work instead with the truncated Neumann series

for any , where the remainder is given by the formula

We now obtain a concentration bound on :

Lemma 5.2.

Let . If is sufficiently large (depending on ), then for each with and all , one has

for some depending only on .

Proof.

Let be an integer such that . By Theorem 1.4, we see that with overwhelming probability, we have

and

and hence by Neumann series

(recall that we allow implied constants to depend on ). Henceforth we condition on the above event. By another application of Theorem 1.4, we see that with overwhelming probability, we have

and hence

Note that the random vector is independent of . The claim then follows from the Azuma-Hoeffding inequality. ∎

Meanwhile, we have the following law for the :

Lemma 5.3.

Let . As , the random variables converge jointly in distribution to iid copies of the real normal distribution .

Proof.

By the central limit theorem, converges in distribution to . Now freeze and thus . By the law of large numbers, has a norm of with probability . Conditioning on this event, we see from Proposition 4.1 that converge in distribution to . Integrating out the conditioning on , we obtain the claim. ∎

In view of this proposition and the Skorokhod representation theorem, we may thus find iid copies of the real normal distribution (depending on ) that are coupled to the in such a way that

| (23) |

uniformly with probability , for each . We thus have

uniformly with probability , for any fixed .

Next, we introduce the function

The correlation functions are the correlation functions of the zeroes of . It thus suffices to show that the correlation functions of the zeroes of converge in the vague topology to the correlation functions of the zeroes of .

For any fixed in , the tail of is Gaussian with mean zero and variance . It thus obeys the same tail bound as Lemma 5.2 (indeed it obeys slightly better bounds). From this, Lemma 5.2, and (23) we conclude that

for any and , where is an absolute constant and the decay rate can depend on . Letting , we conclude that converges in probability to zero for any fixed .

Given any smooth compactly supported function , define the random variables

and

where are the zeroes of respectively (counting multiplicity). By the Stone-Weierstrass theorem (using (21), (22) to control errors that are small in the uniform norm), it suffices to show that

for all smooth compactly supported . From part (i) of Theorem 1.11, we know that is uniformly integrable in (indeed, it has bounded norm for each ). Thus it suffices to show that converges in probability to zero. By another appeal to Theorem 1.11(i), it suffices to show that converges in probability to zero for each .

Fix , and write for . By Green’s theorem, we can write

where is the usual Laplacian. Similarly for . Thus it suffices to show that

converges in probability to zero.

We already know that for fixed , converges in probability to zero. The function is bounded and compactly supported. Also, by Lemma To conclude the claim it then suffices by a truncation argument (cf. [44, Lemma 3.1]) to obtain the uniform integrability bounds

But the bound for follows from (17); the bound for can be deduced from by a Fatou lemma type argument. The proof of Theorem 1.11 is now complete.

6. Zero row sum

We now prove Theorem 1.13. We begin by proving the spectral radius upper bound

which holds almost surely. It will suffice to show that almost surely one has

for each . Writing , expanding, and applying Theorem 1.4 and the fact that the operator norm forms a Banach algebra, it then suffices to show that

almost surely for each fixed , as this handles all but the terms in the expansion that involve at most one factor of , each of which is at worst by Theorem 1.4. But this bound follows from Lemma 2.3.

The spectral radius lower bound will follow from the circular law claim. Since almost sure convergence implies convergence in probability by the dominated convergence theorem, it will suffice to show that and have the same almost sure limit. Applying the replacement principle ([44, Theorem 2.1]), it suffices to show that for almost every complex number , one has

| (24) |

converges almost surely to zero.

Fix ; we may take to be non-zero. We allow implied constants in the notation to depend on . We can rewrite (24) as

| (25) |

where are the ESDs of and respectively.

The matrix is a rank one perturbation of , and so the singular values of the former interlace that of the latter in the sense that

| (26) |

whenever is such that the expressions are well-defined (i.e. for the first inequality and for the second). This adequately controls all of the singular values of except for the smallest and largest. But from Theorem 1.4 we know that the largest singular value of both matrices are . From [44, Lemma 4.1] we almost surely also have a lower bound

for all sufficiently large . So if we can also obtain the corresponding bound

| (27) |

almost surely for all sufficiently large , then by the alternating series test888More precisely, the integrals and are both averages of increasing quantities of size ; by the interlacing property (26) (which bounds the even terms in the latter average by the odd terms in the former, and vice versa), the difference between these two averages can be rearranged as an average of two alternating series whose terms are increasing in magnitude. we see that

as required. So it will suffice to establish the least singular value bound (27). By the Borel-Cantelli lemma, it will suffice to show that

(say) for all sufficiently large , and some absolute constant . Taking transposes, it suffices to show that

Let be chosen later. In order for the above event to hold, there must exist a unit vector such that

We now work to eliminate the role of the projection by dropping a dimension. Taking inner products with , we see that

Since is fixed and non-zero, we thus see that

and thus

If we let , we thus see that is orthogonal to and

and thus

for some complex number . Writing

we thus have

for all . Subtracting off the equation to eliminate , we conclude that

for all . Since has unit norm, has norm between and , and we conclude that

| (28) |

where are the matrices

and

If we condition to be fixed, then is deterministic, while remains an iid random matrix. Applying [44, Lemma 4.1], [42, Theorem 2.1], or [43, Theorem 4.1], we see that the conditional probability of (28) is if is large enough, and if the are bounded by (say) in magnitude. Integrating out the conditioning (and using Chebyshev’s inequality and the union bound to handle the rare event when one of the entries is larger than in magnitude) we obtain the claim. This concludes the proof of Theorem 1.13.

References

- [1] N. Alon, M. Krivelevich, V.H. Vu, On the concentration of eigenvalues of random symmetric matrices, Israel J. Math. 131 (2002) 259- 267.

- [2] A. Andrew, Eigenvalues and singular values of certain random matrices, J. Comput. Appl. Math. 30 (1990), no. 2, 165 171.

- [3] P. Arbenz, W. Gander, G. Golub, Restricted rank modification of the symmetric eigenvalue problem: Theoretical considerations, Linear Algebra and its Applications 104 (1988), 75–95.

- [4] Z. D. Bai, Circular law, Ann. Probab. 25 (1997), 494–529.

- [5] Z. D. Bai, J. Silverstein, Exact separation of eigenvalues of large-dimensional sample covariance matrices, Ann. Probab. 27 (1999), no. 3, 1536 -1555.

- [6] Z. D. Bai and J. Silverstein, Spectral analysis of large dimensional random matrices, Mathematics Monograph Series 2, Science Press, Beijing 2006.

- [7] J. Baik, J. Silverstein, Eigenvalues of large sample covariance matrices of spiked population models. (English summary) J. Multivariate Anal. 97 (2006), no. 6, 1382- 1408.

- [8] D. Bai, J.-F. Yao, Central limit theorems for eigenvalues in a spiked population model, Ann. I.H.P.-Prob. et Stat., 2008, Vol. 44 No. 3, 447- 474.

- [9] Z. D. Bai, Y. Q. Yin, Necessary and sufficient conditions for almost sure convergence of the largest eigenvalue of a Wigner matrix, Ann. Probab. 16 (1988), no. 4, 1729–1741.

- [10] Z. D. Bai, Y. Q. Yin, Limiting behavior of the norm of products of random matrices and two problems of Geman-Hwang, Probab. Theory Relat. Fields 73 (1986), 555–569.

- [11] J. Baik, G. Ben Arous, S. Peche, Phase transition of the largest eigenvalue for nonnull complex sample covariance matrices, Ann. Probab. 33 (2005), no. 5, 1643 -1697.

- [12] J. Baik, J. Silverstein, Eigenvalues of large sample covariance matrices of spiked population models, J. Multivariate Anal. 97 (2006), no. 6, 1382 -1408.

- [13] F. Benaych-Georges, R. Rao, The eigenvalues and eigenvectors of finite, low rank perturbations of large random matrices, preprint.

- [14] F. Benaych-Georges, A. Guionnet, M. Maida, Large deviations of the extreme eigenvalues of random deformations of matrices, preprint.

- [15] F. Benaych-Georges, A. Guionnet, M. Maida, Fluctuations of the extreme eigenvalues of finite rank deformations of random matrices, preprint.

- [16] C. Bordenave, On the spectrum of sum and product of non-hermitian random matrices, preprint. Available at http://arxiv.org/abs/1010.3087.

- [17] C. Bordenave, P. Caputo, D. Chafaï, Circular law theorem for random Markov matrices, preprint. Available at http://arxiv.org/abs/0808.1502.

- [18] M. Capitaine, C. Donati-Martin, D. Féral, Central limit theorems for eigenvalues of deformations of Wigner matrices, preprint. Available at http://arxiv.org/abs/0903.4740.

- [19] D. Chafai, Circular law for non-central random matrices, J. Th. Prob. 23 (2010) 945–950.

- [20] W. Feller, An introduction to probability theory and its applications, volume II. John Wiley & Sons, Inc., New York-London-Sydney, 1971.

- [21] D. Féral, S. Péché, The largest eigenvalue of rank one deformation of large Wigner matrices, Commun. Math. Phys. 272 (2007), 185–228.

- [22] S. Geman, The spectral radius of large random matrices, Ann. Probab. 14 (1986), 1318–1328.

- [23] J. Ginibre, Statistical Ensembles of Complex, Quaternion, and Real Matrices, Journal of Mathematical Physics 6 (1965), 440- 449.

- [24] V. L. Girko, Circular law, Theory Probab. Appl. (1984), 694–706.

- [25] V. L. Girko, The strong circular law. Twenty years later. II. Random Oper. Stochastic Equations 12 (2004), no. 3, 255–312.

- [26] F. Götze, A.N. Tikhomirov, On the circular law. Available at arxiv.org/abs/math/0702386.

- [27] F. Götze, A.N. Tikhomirov, The Circular Law for Random Matrices, Ann. Probab. 38 (2010), no. 4, 1444 -1491.

- [28] A. Guionnet, O. Zeitouni, Concentration of the spectral measure for large matrices, Electron. Comm. Probab. 5 (2000) 119- 136.

- [29] B. J. Hough, M. Krishnapur, Y. Peres, B. Virág, Zeros of Gaussian analytic functions and determinantal point processes. University Lecture Series, 51. American Mathematical Society, Providence, RI, 2009.

- [30] M. Ledoux, The Concentration of Measure Phenomenon. American Mathematical Society, 2001.

- [31] A. Litvak, A. Pajor, M. Rudelson, N. Tomczak-Jaegermann, Smallest singular value of random matrices and geometry of random polytopes, Adv. Math. 195 (2005), no. 2, 491–523.

- [32] M. Meckes, Concentration of norms and eigenvalues of random matrices, J. Funct. Anal. 211 (2004), no. 2, 508- 524.

- [33] M.L. Mehta, Random Matrices and the Statistical Theory of Energy Levels, Academic Press, New York, NY, 1967.

- [34] G. Pan and W. Zhou, Circular law, Extreme singular values and potential theory, J. Multivariate Anal. 101 (2010), no. 3, 645- 656.

- [35] S. Peche, The largest eigenvalue of small rank perturbations of Hermitian random matrices, Probab. Theory Related Fields 134 (2006), no. 1, 127 -173.

- [36] Y. Peres, B. Virág, Zeros of the i.i.d. Gaussian power series: a conformally invariant determinantal process, Acta Math. 194 (2005), no. 1, 1 35.

- [37] A. Pizzo, D. Renfrew, A. Soshnikov, On finite rank deformations of Wigner matrices, preprint.

- [38] T. Prosen, Exact statistics of complex zeros for Gaussian random polynomials with real coefficients, J. Phys. A: Math. Gen. 29 (1996) 4417 -4423.

- [39] K. Rajan, L. F. Abbott, Eigenvalue Spectra of Random Matrices for Neural Networks, Phys. Rev. Lett. 97 (2006), 188104.

- [40] M. Rudelson, R. Vershynin, The Littlewood-Offord problem and invertibility of random matrices, Adv. Math. 218 (2008), no. 2, 600 -633.

- [41] J. Silverstein, The spectral radii and norms of large-dimensional non-central random matrices, Comm. Statist. Stochastic Models 10 (1994), no. 3, 525 532.

- [42] T. Tao and V. Vu, Random Matrices: The circular Law, Communications in Contemporary Mathematics, 10 (2008), 261–307.

- [43] T. Tao and V. Vu, Smooth analysis of the condition number and the least singular value, preprint. Available at http://arxiv.org/abs/0805.3167.

- [44] T. Tao, V. Vu, M. Krishnapur, Random matrices: Universality of ESDs and the circular law, Ann. Probab. 38 (2010), no. 5, 2023 2065.