Extreme value analysis of actuarial risks:

estimation and model validation

Holger Drees111University of Hamburg, Department of Mathematics, SPST, Bundesstr. 55,

20146 Hamburg, Germany; email: drees@math.uni-hamburg.de

Abstract

We give an overview of several aspects arising in the statistical

analysis of extreme risks with actuarial applications in view. In particular it is demonstrated that

empirical process theory is a very powerful tool, both for the

asymptotic analysis of extreme value estimators and to devise

tools for the validation of the underlying model assumptions.

While the focus of the paper is on univariate tail risk analysis,

the basic ideas of the analysis of the extremal dependence

between different risks are also outlined. Here we emphasize some of the

limitations of classical multivariate extreme value theory and

sketch how a different model proposed by Ledford and Tawn can help to

avoid pitfalls. Finally, these theoretical results are used to

analyze a data set of large claim sizes from health insurance.

1 Introduction

In nonlife insurance, usually extreme events constitute a

considerable portion of the total risk covered by an insurance

company. Therefore, in actuarial practice extreme value statistics

(though often in a simplified form) has been used for at least two

decades to assess the risk of large claims. Given their exposure to

huge claims, it is natural that reinsurers were among the first to

emphasize the need for appropriate models of losses exceeding high

thresholds. While the use of Pareto distributions and

generalizations thereof were advocated early (see, e.g., Schmutz and

Doerr (1998)), the fact that they naturally arise as approximative models for exceedances was not always fully

acknowledged, but they were often considered yet another useful

parametric model.

This situation has thoroughly changed. Nowadays it is rarely called

into question that the assessment of “tail risks” requires

specific methods and that extreme value theory often (though not

always) offers efficient and mathematically sound procedures to deal

with such problems. Moreover, several smooth introductions both to

general extreme value statistics and to its application to actuarial

problems have been published; see, e.g., Embrechts et al. (1997),

Beirlant et al. (2004), McNeil (1997) and Cebrián et al. (2003).

For that reason, the present paper focusses on specific aspects

which have perhaps not attracted the attention they deserve:

•

We will show that empirical process theory offers a general

framework to deal with different steps in the risk analysis from

model fitting to model validation and the estimation of risk

measures.

•

An important step in a prudent risk assessment is to

validate the model assumptions on which the statistical analysis

is based. To this end, graphical tools like qq-plots are widely

used but the assessment which deviations from the ideal line

indicate a violation of the model assumptions is largely

subjective, and experience from classical statistical applications

can be misleading if one analyzes heavy-tailed data. Hence in

Section 4 it is described how to refine such tools to obtain a

rigorous statistical test.

•

The analysis of the dependence between different

extreme risks has been extensively discussed in the recent statistical

literature. We will first comment on problems arising when

parametric copula models are used to this end. Then we

discuss how to overcome a serious weakness of classical

multivariate extreme value statistics.

As the choice of topics addressed by such a partial survey is

subjective, it is inevitable that some readers will miss aspects

they consider particularly important. Perhaps the most obvious topic

we only touch on concerns the extreme value analysis of investment

risks. Although recent years have shown that in some instances the

asset side of the balance book contains the most serious risks of

extreme losses, for several reasons here we will nevertheless focus

on “genuine” actuarial problems related to the insured risks.

Firstly, the statistical and economic literature on extreme

investment risks is abound. Secondly, though the very basics of

extreme value theory needed in this context is the same as the one

discussed here, a serious treatment of market risks would require a

lengthy introduction to the extreme value behavior of time series;

we refrain from discussing this topic in detail in order not to

overload the article. Finally, we feel that mathematically

satisfactory solutions are yet to be developed for important

practical problems like the risk assessment for complex portfolios.

An exposition that cannot go into great details carries the risk of

provoking a serious misconception of the solutions that the state of

the art in statistical theory can actually deliver.

As there are plenty of other important problems we can merely touch

on, we will try to mitigate this lack by giving references where

aspects important in actuarial applications are discussed in greater

detail. We do however not aim at giving a full overview over the

rapidly expanding literature relevant in this context. Hence the

present text may be best characterized as a tutorial with particular

emphasis laid on crucial points which, from my personal point of

view, have often not attracted the interest they deserve.

The paper is organized as follows. Section 2 gives

an introduction into the basics of univariate extreme value theory,

with particular emphasis on conditional distributions of exceedances

(instead of the distribution of maxima as in the classical

approach). In Section 3 we discuss how to

construct extreme value estimators of quantities like risk measures

and insurance premiums which depend only on the tail behavior. Then

Section 4 deals with methods to define a tail

region depending on the data and the purpose and methods of the tail

analysis as well as tools for model validation. In both these

sections, a limit theorem for the tail empirical quantile function

proves extremely useful. In Section 5 we outline

how the dependence structure between the components of a vector of

risks can be statistically analyzed. In Section

6 the previously introduced statistical

procedures are used to analyze a data set of large claims in US

health insurances. All proofs are deferred to the final Section

7.

2 Basics of univariate extreme value theory

Classically a synopsis on extreme value theory starts with the

analysis of maxima of independent and identically distributed random

variables (iid rv’s). We prefer to discuss the asymptotic behavior

of excesses over high thresholds, because these naturally arise as

effective claim sizes in insurances with high retention levels,

while the maximum of claim sizes rarely is an economically

meaningful quantity.

In what follows, let denote a rv defined on some probability

space with cumulative distribution function

(cdf) and quantile function (i.e., the generalized

inverse of ). If describes a loss covered by an insurance

with retention level , then

is the cdf of the actual claim size. For a very high retention

level (e.g., in an excess of loss reinsurance against

catastrophes), usually few or none of the losses observed so far

exceed , so that standard methods for risk modeling and premium

calculation do not apply directly. Of course, one could assume a

parametric model for all losses, estimate its parameters (provided

the full losses are observed) and calculate the resulting

conditional cdf of the excesses over . Then, however, the fitted

model for is largely determined by the bulk of losses that are

much smaller than the losses of interest that exceed . Hence such

an approach seems advisable only if one is confident that the same

“stochastic mechanism” generates the moderate losses on the one

hand and large losses on the other hand, and that all these losses

can be well described by the chosen parametric model. As this will

rarely be justified, it is widely accepted that for modeling

one should consult only losses which are large, though perhaps still

smaller than . Sometimes this general idea is subsumed in the

catchy phrase “Let the tails speak for themselves”.

The basic idea of extreme value theory is to tackle this problem by

assuming that, after a suitable normalization, the cdf

converges to a non-degenerate limit as the threshold tends to

the largest possible loss . More precisely, we assume that

for some (measurable) function there exists a non-degenerate

cdf (i.e., ) such that

(2.1)

as for all points of continuity of (i.e.,

weakly). It turns out that then is

necessarily the cdf of a generalized Pareto distribution (GPD), that

is

Here is interpreted as , which is

an exponential cdf. Note that the scale parameter depends on the

choice of the normalizing function ; we can and will always

assume and write instead of .

If (2.1) holds, then the conditional cdf can

be approximated by with , provided is sufficiently large. In that case, the following

approximation of the tail of the loss cdf follows:

(2.2)

for .

Of course, this approximation can also be used for thresholds

different from the retention level at hand. It is important to note

that (almost) always (2.2) is only an approximation to the tail and that its accuracy depends on the

choice of . Hence one should avoid considering the GPD model to

be the “true” one above a certain threshold . As we will

discuss in detail later on, there will always be a bias-variance

trade-off when choosing a threshold to estimate premiums or risk

measures.

The extreme value approach to the analysis of relies on

convergence (2.1). Fortunately, almost all textbook

distributions suggested to model claim sizes fulfill this condition,

that can be reformulated as

(2.3)

for some . It is easily seen that this

condition holds if and only if for

(2.4)

where the right-hand side is interpreted as for

. (Indeed, (2.4) holds for all .)

The so-called extreme value index largely determines

the tail behavior of . If , then the loss distribution

is unbounded and (2.4) is equivalent to the

regular variation of at and of at 1:

(2.5)

(2.6)

In this case, both and are called heavy-tailed. (Notice,

however, that in the literature other meanings of the term

“heavy-tailed distributions” are common, too.) Typical examples

are Burr distributions, loggamma distributions and

distributions. As the survival function roughly decays as

the power function , large losses are the more likely

the larger is. In particular, the loss has infinite

expectation if and it has infinite variance if .

If the extreme value index is negative, then the loss has bounded

support, while for the right endpoint of the loss

distribution can be finite or infinite. For most textbook examples,

including lognormal, gamma and normal distributions, the latter is

true.

This article will mainly focus on the case , that is

obviously the most troublesome from an insurer’s perspective. We

will see that in the statistical analysis it is nevertheless

sometimes better to work with the more general conditions

(2.3) and (2.4) instead of

the simpler conditions (2.5) and

(2.6), that correspond to the particular choice

.

We close this section with a brief outline of the relationship to

the limit behavior of maxima of iid rv’s , , with

cdf . It can be shown that assumption (2.1) is

equivalent to the convergence of the suitably standardized maxima to

the (generalized) extreme value distribution corresponding to ,

i.e.

holds for some , and all points of continuity of

the non-degenerate cdf if and only if (2.1) is

fulfilled with . Then it is said that belongs to

the maximum domain of attraction ( for short), and one

can choose and .

3 Univariate tail risk analysis

To start with a concrete problem, assume that based on observed

losses the fair net premium of a (working)

excess-of-loss (XL-) reinsurance with a cover of in excess of

is to be estimated, that is, the reinsurer has to

pay of all future claims exceeding . After

a suitable correction for inflation, the random variables ,

, shall be regarded as iid with some unknown cdf .

If at most a few observations exceed the retention level , then

the net premium per loss cannot be

directly estimated by the corresponding mean. Therefore, we assume that

fulfills the basic condition (2.3) for some

, so that we may approximate the net premium as

follows:

for some suitable threshold , provided that

. If is sufficiently large, then it

can be estimated by the corresponding empirical probability

. Hence, if one replaces the extreme value and

the scale factor by some estimators and , respectively, then one obtains a reasonable estimator of

the net premium per claim. (To obtain an estimator for the net

premium of the whole XL reinsurance contract, one has to multiply

this expression with some estimator of the expected number of

claims.)

Estimators of and that use only exceedances over the

threshold can be motivated in a similar way. For example, if one

can assume that is strictly positive, then by

(2.5) the conditional distribution of

given may be approximated by a Pareto distribution with

Lebesgue density ,

. Ignoring the approximation error and the fact that the number

of exceedances is also random, we may estimate by a

maximum likelihood approach to obtain

(3.2)

If one starts with condition (2.3) in the

general case , then the conditional distribution of the

excesses given are iid with approximative density

for with

. As the resulting approximative likelihood is

unbounded for , a point of maximum of the

loglikelihood on the

parameter set can be

motivated as an estimator for .

Of course, several other estimators of the extreme value index and

the scale factor have been proposed; see, for instance, de Haan and

Ferreira (2006), Sections 3 and 4.

The performance of all these estimators crucially depends on the

accuracy of the (generalized) Pareto approximation in

(2.3) (respectively (2.5)

in the case ) and the choice of the threshold . Too low

a threshold will lead to a large bias, because the GPD approximation

is inaccurate for the smallest exceedances of . On the other

hand, if is chosen too large, then the estimators use only a

very small fraction of the whole sample and thus their variance will

be large. In Section 4, we will discuss methods to deal with the

bias-variance tradeoff in greater detail.

Because one has to choose the threshold depending on the data,

it seems natural to use a large order statistic

(with denoting the th smallest observation). Then all

estimators under consideration are based on the largest

observations and can therefore be written as functionals of the tail

empirical quantile function

(3.3)

For example, replacing with in

(3.2) yields the well-known Hill estimator

(3.4)

(if there are no ties).

Since the parameters and

are only defined by limit relations like

(2.3) and (2.4), the

performance of their estimators must be analyzed in an asymptotic

framework. (Indeed, there are no unique “true” functions and

, because any function such that as also satisfies

(2.4).) Because the basic condition

(2.4) describes the behavior of

only at its right endpoint , in the asymptotic

setting we must ensure that, while the number of order statistics

used for the statistical tail analysis tends to infinity, all order

statistics tend to , that is, is

a so-called intermediate sequence satisfying

(3.5)

Moreover, should not grow too fast to avoid the aforementioned

bias problems due to a poor GPD approximation. The precise

conditions on will be given below in terms of the

approximation error in (2.4), i.e.

As the randomness of all

extreme value estimators under consideration is captured by the tail

empirical quantile function, it is natural first to establish a

limit theorem for this process and then to conclude the asymptotic

behavior of quite general extreme value estimators (or tests) by a

functional delta method. In what follows, we are focussing on the

case and will often assume that , which

is by far the most relevant case in actuarial applications and helps

to avoid technicalities. The following limit theorem (Drees, 1998a,

Theorem 2.1) is the corner stone for the subsequent risk analysis

Theorem 3.1.

If is an intermediate sequence such that for

some

(3.6)

then for a standard Brownian motion and all we have

(3.7)

weakly in the normed vector space

of functions

which are continuous from the right with left-hand limits and

finite weighted supremum norm

It is noteworthy that, under the basic assumption

(2.4), there always exist intermediate sequences

such that (3.6) is fulfilled. Hence

(3.6) is not a condition on , but it merely

restricts the speed at which grows with the sample size.

Now suppose is a scale and shift invariant

functional (i.e., for all , and ) such that for

, such that the following

(Hadamard) differentiability condition holds: there exists a signed

measure on such that

(3.8)

for all

sequences and all

satisfying . Then one may easily

deduce that

(3.9)

where the right-hand side is normally distributed with expectation 0

and variance

(3.10)

Likewise, the scale factor can be estimated by

, where is a scale equivariant and

shift invariant functional (i.e., for all ,

and ) such that and

for some signed measure on

(3.11)

for all sequences and

. Then we conclude

(3.12)

(In fact, the joint weak convergence of (3.7),

(3.9) and (3.12) holds.)

As an example, consider the functional defined as a

solution of the equations

with , or as if and . Then is the aforementioned maximum

likelihood estimator in the approximating GPD model (or more

precisely, a solution of the corresponding likelihood equations).

Using the methodology sketched above, one can prove that under the

conditions of Theorem 3.1

It can be shown that these estimators have minimal asymptotic

variances among all estimators and of the type

discussed above. (See Drees (1998a) and Drees et al. (2004) for

details.)

If , then one can always choose , so that (3.7) reads as

Hence, in this case, we need not require that is shift

invariant, but merely that it is scale invariant, which allows for a

wider class of functionals. A prominent example is the Hill

estimator with ,

that is scale invariant but not shift invariant. The Hill estimator

is asymptotically normal with asymptotic variance if

condition (3.6) is met for , which reads as

(3.13)

Note that for some cdf’s this condition imposes a much more

severe restriction on the number of order statistics used for

estimation than condition (3.6) for some other choice

of the normalizing function . Thus, even if it is known

(or assumed) in advance that , it may be advisable to use

the shift invariant ML estimator in the GPD model instead of the

Hill estimator, although the latter has a smaller asymptotic

variance.

Example 3.2.

Assume that the following expansion of the quantile function

holds:

(3.14)

for some , and with

if . Then condition

(3.13) ensuring the asymptotic normality of the Hill

estimator is equivalent to

and hence to

. In

contrast, the ML estimator in the GPD model is asymptotically normal if condition (3.6)

holds, e.g., with the choice ,

which is equivalent to and is hence

fulfilled for . For that reason, in the case , the

ML estimator may use many more large order statistics than the

Hill estimator before a significant bias shows up.

Remark 3.3.

It can be shown that, in the situation of Example 3.2,

the shift invariant estimators and are still asymptotically

normal if for some

, but then the limiting normal distribution is no

longer centered. See Drees (1998a) or de Haan and Ferreira (2006),

Section 3, for similar results under second order refinements of

condition (2.4), that are generalizations of

expansion (3.14).

A different type of estimators for the extreme value index that

explicitly uses these second order conditions are discussed in

Section 4.5 of Beirlant et al. (2004). These estimators typically

have a smaller bias in the more restrictive model, but their

consistency is not ensured if only condition

(2.3) or (2.5) is

assumed.

Next we will demonstrate by the example of an estimator for the net

premium of the XL-reinsurance discussed above that the asymptotic

normality of a huge class of extreme value estimators follows by

straightforward (though sometimes lengthy) computations. Replacing

in (3) the threshold with

and the unknown parameters by suitable

estimators, we arrive at

As explained above, we are interested in the case that at most a few

observations exceed the retention level . To reflect this crucial

feature in the asymptotic framework, one must consider a sequence of

retention levels which increases with the sample size. More

precisely, we assume

(3.15)

Despite the quite complex structure of the estimator

, its asymptotic normality follows from the

joint asymptotic normality of and by

rather simple Taylor type expansions. For simplicity, we focus on

the case , but an analogous result can be proved by the

same methodology for all . In the case ,

though, the asymptotic behavior of also depends on the

asymptotics of , while it does not play a role in the

following result.

Corollary 3.4.

Assume that for some , that

is a sequence of retention levels such that (3.15)

holds,

and let

be an intermediate sequence satisfying

(3.6),

(3.16)

and

(3.17)

with

Then

with

Remark 3.5.

(i)

From Corollary 3.4 and its proof, one can easily

conclude that

Hence, if is a consistent estimator of in

the sense that in probability, and if

is a continuous function of , then

from which asymptotic confidence intervals are readily

constructed. If , then

is a consistent estimator of .

(ii)

In the situation of Example 3.2, condition

(3.16) is a direct consequence of condition

(3.6). In general, though, (3.16)

cannot always be fulfilled, if the rate of convergence in

(2.4) is particularly slow. Since in the proof of Corollary 3.4 this

condition is essentially only needed to bound the bias term IV,

a closer inspection of the proof shows that it can be replaced

by a weaker, but more complex condition on which can

always be satisfied.

By the same approach one can construct estimators of all risk

measures or insurance premiums which are smooth functionals of the

tail cdf , , for some large or of the tail quantile

function , , for some small . For example,

the value at risk for small can be

estimated by

(cf. Drees (2003)). Extreme value estimators of reinsurance

premiums according to Wang’s premium principle have been examined by

Vandewalle and Beirlant (2006) in the case (without using

the tail empirical quantile function explicitly).

An advantage of the approach via the tail empirical quantile

function is that, with rather little effort, one can analyze the

asymptotic behavior of a large class of extreme value estimators in

a unified framework, and hence easily compare their performance.

Moreover, the same analysis immediately gives the asymptotic

normality of the estimators if one replaces the assumption of

independence of the observations by more general condition on the

serial dependence structure. Indeed, Drees (2003) proved the

convergence of the tail empirical quantile function towards a

centered Gaussian process for stationary time series which satisfy

suitable mixing conditions. Although all the estimators discussed

above can still be used in this more general setting, usually their

estimation error will be larger than for iid data. In an extensive

simulation study, Drees (2003) showed that then the actual coverage

probability of confidence intervals for extreme quantiles

constructed on the basis of the theory for iid data can be much

smaller than its nominal value. Therefore, it is important not to

use these confidence intervals when analyzing time series of returns

on some investment that usually exhibit quite strong a serial

dependence.

4 Selecting the tail fraction and validating the model

As explained above, in almost all cases there does not exist a

threshold such that the tail cdf , is exactly

equal to some GPD tail, but the accuracy of the GPD approximation

usually increases with the threshold. Consequently, roughly speaking

the modulus of the bias of any of the extreme value estimators

discussed in Section 3 will be a

monotonically decreasing function of , respectively an increasing

function of if the order statistic is used as the

threshold. (This statement should be taken with a pinch of salt: for

very small the bias sometimes becomes larger again, but in an

asymptotic setting the monotonicity can be made precise for

intermediate sequences .) On the other hand, the

variance is an increasing function of and decreasing function of

, respectively. Therefore, choosing an “optimal” sample

fraction of largest observations used for the statistical tail

analysis involves a bias-variance tradeoff. Note that this selection

does not only depend on the data set (or the underlying

distribution), but also on the estimator (or statistical test) used

in the analysis. Moreover, the appropriate balance between bias and

variance may also depend on the purpose of the statistical

analysis: in some applications a non-negligible bias may be

unacceptable when calculating an insurance premium, while such a

bias may be admissible if it helps to reduce the variance of an

estimator of a risk measure. Thus, for a given data set, there does

not exist the optimal choice for or .

This said, widely applicable techniques are needed to select the

number of largest order statistics used in the statistical analysis.

The most popular graphical tool is to plot the estimator under

consideration (based on the largest observations) versus .

Typically, the graph will be rather wiggly for small values of ,

and it will be more or less monotone for large values of due to

the increasing modulus of the bias. Hopefully, there is a range in

between where the plot is relatively stable, indicating that the

bias is not yet dominating, but the variance has already decreased

to an acceptable level. Drees et al. (2000) showed (for the Hill

estimator) that it may be advisable to plot the estimator versus

(as suggested by C. Stărică), because

usually this graph spends a larger portion of time in the

neighborhood of the true value.

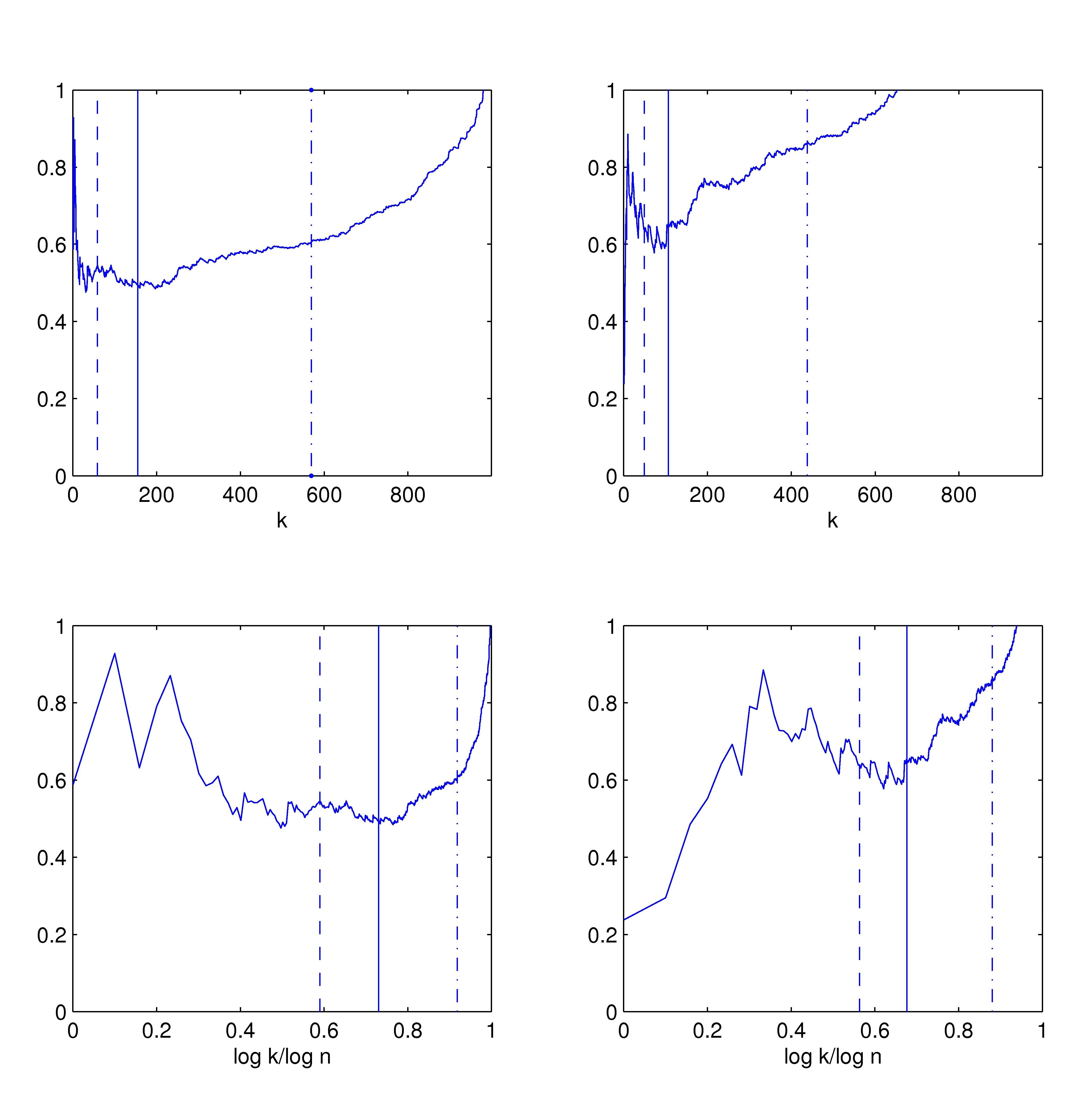

Figure 1 shows such plots for the Hill estimator

calculated for a sample of iid Fréchet rv’s with cdf

on the left-hand side and for a sample

of rv’s with quantile function

on the right-hand side with . The plots for the Fréchet

rv’s are quite stable for around 150 or about

0.7. In contrast, in the right-hand plots for the logarithmically

disturbed Pareto distribution, after strong fluctuations in the

beginning, the graphs immediately show a clear upward trend, and so

no plateau is clearly visible. This different behavior is caused by

the different accuracy of the GPD approximation to the tail. While

the Fréchet distribution satisfies expansion (3.14) with

leading to the optimal rate of convergence when is of

the order , in the case of the logarithmically disturbed

Pareto distribution it can be shown that the squared bias dominates

the variance if is of larger order than . Thus for

the second distribution the increasing bias leads to the clear trend

already for quite small values of .

Figure 1: Hill estimator based on largest

order statistics versus (above) and versus

(below) for iid Fréchet rv’s (left) and logarithmically

disturbed Pareto rv’s (right) with . Estimated optimal

numbers (dashed), (solid) and

(dash-dotted) are indicated by vertical lines.

To give some advice how to choose the sample fraction used in the

tail analysis in such cases and also to avoid subjective choices

which have an influence on the estimation accuracy that is difficult

to quantify, fully automatic data-driven selection procedures have

been proposed that minimize the asymptotic mean squared error of the

estimators under consideration.

Here we consider three different methods to choose the number

of largest order statistics such that the (asymptotic) mean squared

error of the Hill estimator is minimized. See

Section 4.7 of Beirlant et al. (2004) for a more extensive list and

additional references.

Danielsson et al. (2001) used a bootstrap approach to minimize the

mean squared error (MSE). Hill (1990) showed that the standard

bootstrap does not work here, because it does not capture the bias

of the Hill estimator (and other linear statistics) properly, but a

suitable bootstrap may yield a consistent estimator of the MSE in a

restricted model. Instead of trying to minimize the MSE of the Hill

estimator directly, Danielsson et al. (2001) used the auxiliary

statistic with

(4.1)

It can be shown that under a suitable second order condition,

that generalizes assumption (3.14), a sequence which minimizes and a sequence which

minimizes the MSE of the Hill estimator have the

same asymptotic behavior up to a multiplicative constant. Starting

from this fact, Danielsson et al. (2001) developed the following

algorithm:

•

For some , some and

, define , , which

minimizes the conditional expectation of

given the data , where and

are defined as in (3.4) and (4.1),

respectively, but with replaced by and replaced by independently

drawn from (with replacement). Here the

conditional expectation is minimized over , say.

•

The asymptotic MSE of the Hill estimator

is then minimal for

The performance of the data-driven choice of crucially depends

on the value . Using heuristic arguments, Danielsson et al. (2001) proposed to select which minimizes

with

denoting the conditional expectation of

given the

data.

Drees and Kaufmann (1998) suggested a

sequential procedure that was inspired by the so-called

Lepskii-method for adaptive bandwidth selection in curve estimation.

The basic idea of this approach is that too large a difference

between two Hill estimators and

with indicates that the latter exhibits a

large bias. As the random error of the difference is of the order

, an asymptotically optimal choice of the number of order

statistics can be determined from the smallest such that

exceeds a suitable

threshold. More precisely, Drees and Kaufmann (1998) proposed the

following algorithm:

•

For some such that let

•

Fix some such that and calculate a pilot estimate

with denoting the number of positive observations. Then the asymptotic MSE of the Hill

estimator is minimal for

with

Here the specific values of , and (to a lesser extent)

influence the performance of the procedure. the authors

recommended to choose , and

; see Drees and Kaufmann (1998) for further comments on

the implementation of this algorithm.

In yet another approach, Beirlant et al. (2004), Section 4.7.1

(ii), fitted an extended Pareto model with an explicit second order

correction term to the data using a maximum likelihood estimator.

Then they calculated and minimized the MSE of the Hill estimator

directly from this fit. The resulting estimated optimal number will

be denoted by .

In Figure 1 the resulting estimates for the

optimal number of order statistics are indicated by vertical lines.

While the bootstrap (dashed line) and the sequential approach (solid

line) both yield reasonable values, the method which uses an

explicit model for the second order term leads to too large values

and thus a considerable bias. Indeed, it has been observed in

literature that for moderate sample sizes it is notoriously

difficult to estimate the second order parameters like in

expansion (3.14). In contrast, the bootstrap and the

sequential approach both use estimates of this second order

parameter only in an estimate of a multiplicative constant, while

their order of magnitude does not explicitly depend on such an

estimate. Hence they yield reasonable estimates even if this second

order parameter is fixed (e.g., ) and misspecified.

Once the sample fraction of largest order statistics has been

chosen, one should check whether it can be well approximated by a

(generalized) Pareto distribution. A classical graphical tool for

such an model validation is the qq-plot. If for

some and is chosen not too large, then using

(2.6) one can approximate

Hence the points

should approximately lie on the line with slope

through the origin. To assess whether the

observed deviations of the points from this line are probably only

due to their randomness or whether they indicate that the GPD

approximation is inaccurate, we can again use Theorem

3.1.

Corollary 4.1.

Assume that is an intermediate sequence such that

condition (3.13) holds for some .

Then for all and all scale invariant functionals on satisfying

and the differentiability condition

(3.8), we have

(4.2)

weakly in .

Hence,

(4.3)

for all continuous functions such that

as for some .

In particular, for (i.e., equal to the Hill

estimator), we obtain

(4.4)

Under slightly different conditions, a similar result has been

proved by Dietrich et al. (2002) for the Hill estimator.

Using (4.4) one can turn the Pareto qq-plot into a

statistical testing tool with given asymptotic size . To

this end, for some function satisfying the conditions of

Corollary 4.1, using Monte Carlo simulations, one

determines a critical value such that the probability on

the right-hand side of (4.4) equals . Then

with probability of about all points of the Pareto

qq-plot should lie in the band defined by the graphs of the

functions if the GPD

approximation is accurate enough so that the bias of the Hill

estimator is negligible. The choice of the function determines

in which part of the qq-plot deviations are most easily detected:

the larger is, the more narrow is the band at that point.

Because of the condition as , the band always widens for small values of , thus allowing

for larger deviations of the most extreme points of the qq-plot from

the ideal line.

It has been suggested to use such tests also to select the tail

fraction to be analyzed by increasing until the test rejects the

GPD hypothesis (see, e.g., Dietrich et al., 2002, Remark 2). In some

applications this approach may be problematic if is chosen

as small as it is common in testing (e.g., ). Note that

the limiting Gaussian process in (4.2) tends to 0 as

tends to 1, but that the function is assumed continuous and

hence bounded, so that deviations of points of the qq-plot from the

ideal line near (corresponding to the smallest order

statistics taken into account) are usually difficult to detect.

Hence it may happen that one increases the number so much that

the Hill estimator (and other extreme value estimators) are strongly

biased, before the tests acknowledges that the last order statistics

taken into account are poorly fitted. (The same argument also

applies if -type tests like the one examined by Dietrich et

al. (2002) are used.)

To avoid such effects, one might think of choosing a weight function

that tends to as tends to 1 to compensate for the

decrease of the modulus of the limiting Gaussian process. For

instance, as this process has the variance function

if , one might be tempted to

use a weight function of the form for

some small . Unfortunately, without additional conditions on

the smoothness of , convergence (4.4) need not

hold for such a choice of . The reason is that under the general

condition (2.5) small jumps of (or

continuous small but rapid changes) are still possible which lead to

an “unusually” irregular behavior of the tail empirical quantile

function near 1. If one strengthens condition

(2.5) to a regularity condition on the quantile

density function , though, then assertion

(4.2) may also be strengthened. It is well known that

if has a Lebesgue density which is monotonically decreasing in

a neighborhood of 1, then by Karamata’s theorem

(cf. de Haan and Ferreira (2006), Proposition B.1.9 11.). If we

replace condition (3.13) with a condition on in

terms of the function , then convergence (4.2)

can be made more precise in a neighborhood of .

Corollary 4.2.

Assume that is an intermediate sequence such

that for some

(4.5)

and that the functional satisfies the conditions specified in Corollary

4.1. Then for all and for all continuous functions such that

as , and

as , one has

(4.6)

weakly with respect to the supremum norm.

In particular, convergence (4.4)

holds for .

In Section 6 this result is applied to

construct a “confidence band” for the Hill-qq-plot based on claim

sizes from health insurances.

If one uses some estimator of different from the Hill

estimator, then usually the probability on the right-hand side of

(4.3) is a continuous non-linear function of the

unknown extreme value index . In that case, one can still

construct tests with prescribed asymptotic size for the

null hypothesis that (3.13) holds. To this end, one

first estimates consistently by and

then, using Monte Carlo simulations, one determines a critical value

such that the right-hand side of (4.3)

equals when is replaced with .

Since the supremum is difficult to simulate, it seems natural to

simulate the limiting process on a fine grid

, and then to approximate the supremum by

. This can still be

computationally

challenging if one tries to approximate the integral of using some quadrature formula, because the integrand is

unbounded in a neighborhood of zero and a large number of

integration points may be needed to obtain an accurate

approximation. Fortunately, for most estimators, one can avoid numerical integration

using the fact that conditionally on , , the

integrals , , (with ) are independent normal

rv’s with mean

and variance

This statement, in turn, follows from the conditional independence

of the processes which have the same

conditional distribution as

with denoting a Brownian motion independent of .

Hence the limiting Gaussian process can be simulated as

follows if integrals of power functions with respect to can be calculated analytically:

(i)

Simulate independent centered normal rv’s

with variance where and , and let

.

(ii)

Simulate a normal rv with mean and

variance .

(iii)

Then is a (pseudo) realization of .

Note that the variance of does not depend on . In case of

the Hill estimator and equidistant design points , one has

The Corollaries 4.1 and 4.2 describe

tests for the null hypothesis that the left-hand sides of (3.13) and

(4.5), respectively, are negligible. Likewise, one can

devise analogous tests for the validity of condition

(3.6), but the resulting limiting process is more

complicated.

Corollary 4.3.

Suppose that is an intermediate sequence

satisfying condition (3.6) for some , and that

are scale and location invariant functionals such that , and

the differentiability conditions (3.8) and (3.11) are met.

Then for all

weakly in (with

interpreted as for ).

The proof is omitted as the assertion follows readily from Theorem

3.1, (3.10), (3.12)

and a Taylor expansion of .

Similarly as above, from Corollary 4.3 one may

construct bands around the fitted generalized Pareto quantile

function in which all the

points should lie with

probability of about .

5 Analysis of the extremal dependence

In recent years, the analysis of the dependence between the extremes

of the components of a random vector of risks has attracted much

attention. If the random vector describes returns on different

assets, then it is obviously important to assess the risk of large

losses in different assets at the same time. However, extremal

dependence also matters in the analysis of claim sizes from one

customer in different lines of business. For example, if both a

building and its content are insured with the same company, then a

fire will often lead to large claims in both lines of business.

Likewise, some dependence can be expected between the claims in

different types of health insurances (e.g. inpatient and

outpatient cover); cf. Section 6.

In order not to overload this presentation, we will only sketch the

basic theory used in the analysis of extremal dependence, but we

will rather discuss some pitfalls and problems that may arise in

applications in more detail. For simplicity, we mainly consider

bivariate vectors of claim sizes (or risks).

Analogously to our basic assumption (2.1) in the

univariate setting, in classical multivariate extreme value theory

it is assumed that the conditional distribution of the suitably

standardized random vector given that its norm exceeds a high

threshold converges to a non-degenerate limit as the threshold

increases. However, as the components of the vector need not be of

comparable size, the marginal distributions are usually first

standardized, e.g., to the standard Pareto distribution:

(5.1)

Here we assume for simplicity that the marginal cdf’s , , of are continuous.

Now fix some norm on and suppose that

(5.2)

as for some non-degenerate limit distribution . In

that case, and are said to be multivariate regularly

varying.

It can be shown that this condition does not depend on the specific

choice of the norm, while the exact form of the limit distribution

does. For example, if one works with the maximum norm

, then (5.2) is equivalent to

Now standard arguments from the theory of regular variation show

that the limiting distribution must be a product

measure with first factor equal to the standard Pareto distribution

and the second factor being some distribution on the upper

right quadrant of the unit

“circle” with respect to the norm . Unlike in the

univariate setting, all possible limit distributions do not form a

parametric family, because the so-called spectral probability

measure can be any distribution on satisfying the

condition

(5.4)

that follows from the fact that all marginal cdf’s are standard

Pareto.

Remark 5.1.

In the literature, instead of (5.2)

often the equivalent assumption

(5.5)

is considered, where is some Radon measure on

(see e.g. Resnick (2007), Section

6.1). Similarly as before, one can conclude that the measure

induced by the polar transformation is the product of the measure

with Lebesgue density on and a

finite measure on , the so-called spectral

measure. The latter is related to the spectral probability

measure via

For an arbitrary measurable set one has

(5.6)

as , provided the set is continuous with respect to

the limit measure (that is the right-hand side equals 0 if is

replaced with its topological boundary). Hence, to estimate the

probability that some future observation falls into a given

extreme set (e.g.,

describing the event that the claim sizes in both lines of business

exceed a given high threshold) can be estimated as follows:

(i)

Estimate the marginal cdf’s by ; for the

estimation of the tails, the methods discussed in the previous

sections can be used.

(ii)

Transform the data , ,

and the extreme set using the fitted marginal cdf’s:

(iii)

Fix some norm and estimate the corresponding spectral

probability measure by (see below).

(iv)

Use (5.6) and the regular variation of

to approximate

Here we have assumed that for all , while on the other hand

is sufficiently large such that

(5.6) (with instead of ) yields a good

approximation. Moreover, on the one hand must be sufficiently large

such that , while on the

other hand it must be sufficiently small such that

can be well estimated by its empirical counterpart.

As the family of all possible spectral (probability) measures is

nonparametric (infinite dimensional), it is substantially more

complicated to estimate (or ) than to fit the

tail of a univariate cdf. In the last decade, though, a variety of

nonparametric estimators of the spectral measure and related

functions, that also characterize the extremal dependence structure,

have been suggested and analyzed; see, for instance, de Haan and

Ferreira (2006), Chapter 7, Beirlant et al. (2004), Chapter 9, or

Einmahl and Segers (2009). These estimators also use marginally

transformed observations , but, unlike in program to

estimate the probability of extreme events outlined above, here one

may use fully nonparametric estimators of the marginal cdf’s, which

amounts to working with the coordinatewise ranks of the original

observations. In the analysis of the asymptotic behavior of these

estimators, it is important to not assume that the marginal

cdf’s are known, because usually the transformation of the data

using estimated marginal cdf’s (rather than the true ones)

does have a non-negligible influence on the estimation error for

; ignoring it may lead to a wrong assessment of the estimation

accuracy (see, e.g., Einmahl and Segers (2009), p. 2960).

As an alternative approach, it has been suggested to assume some

parametric submodel of spectral (probability) measures and then to

fit this model to the transformed observations using maximum

likelihood or a generalized moment method. Sometimes it is even

assumed that, for some from this parametric family, in

(5.6) equality holds for some sufficiently large

. We consider this approach quite problematic, because it will

rarely be possible to argue for a specific parametric family of

spectral measures based on either experience with similar data sets

or some “physical” reasoning about the process generating the

extremal dependence. Instead, the parametric families are almost

always chosen with mathematical convenience in view, while it is

argued that the family is sufficiently flexible to capture many

different dependence structures. Then, however, one merely trades

the random estimation error, that can be quantified in the

nonparametric framework, for the risk of a model misspecification,

that can hardly be assessed. Hence the seemingly increased

estimation accuracy which comes with the parametric approach if

the model is correct will often be just a chimera, which possibly

leads to an assessment of the insured risk which is not prudent

anymore.

An even more restrictive modeling approach is related to a

reformulation of the multivariate regular variation in terms of

copulas. Any multivariate cdf with marginal cdf’s , , can be represented as where is a so-called copula, i.e. a multivariate

cdf with uniform margins. If all are continuous, then is

unique: it is the joint cdf of . Thus,

the cdf of defined by (5.1) equals

and convergence

(5.3) is equivalent to

for all points of continuity of . Hence the

parametric approach outlined above boils down to assuming that, on a

small neighborhood of the point (1,1), the copula can be well

approximated by a parametric model.

Because the estimation of a general copula is essentially as

difficult as the estimation of a general multivariate cdf (in

particular it is also plagued by the well-known “curse of

dimensionality”), it has been suggested to assume parametric models

for the whole copula . This approach, however, does not only

introduce a modeling error that is difficult to quantify, but it

contradicts the general philosophy of extreme value theory to “let

the tails speak for themselves”. In contrast, while the estimation

error of the aforementioned nonparametric estimators of the extremal

dependence structure can be quite large (in particular in higher

dimensions), it can be well assessed under weak model assumptions

and thus it can be taken into account by the risk manager. For that

reason, with the rare exception of those situations when there are

convincing arguments that a particular family of copulas contains

the true one (and not just a crude approximation to it), one should

take the utmost care in analyzing the tail risk using parametric

copulas, in particular in actuarial applications where prudence is a

time-honored principle. (In this context, the interested reader is

advised to study the article by Mikosch (2006) and the pertaining

discussion for an enlightening and entertaining argument about the

pros and cons of copula modeling.)

While the program sketched above in four steps will often yield a

reasonable assessment of the risk that a future observation falls

into some given extreme set if some nonparametric estimator of

is used, there is one important case in which the result can

be quite misleading. Suppose that large values of one component of

the transformed vector of risks do not usually coincide with

large values of the other component, or more precisely that

(5.7)

as . In that case, and (or and )

are said to be asymptotically independent. Straightforward

calculations show that then the limit measure in

(5.5) has no mass on , i.e., it is

concentrated on the axes. Hence, and have mass

only in the points and if one uses one of the usual

-norms on with . (Indeed, because of the

normalization constraint (5.4), must be the

uniform distribution on .) But then for all sets

that do not intersect with any of the axes, the limit in

(5.6) is 0, which usually is too crude an

approximation for the left-hand side.

Note that asymptotic independence is a property of the copula of

. Many popular parametric families of copulas allow for

asymptotic independence for suitable parameter values. A thorough

analysis of the tail behavior of so-called Archimedean copulas both

in the case of asymptotic independence and of asymptotic dependence

can be found in Charpentier and Segers (2009).

To obtain more useful approximations, one has to specify the rate at

which tends to 0. More precisely, one assumes

that for some nontrivial function

(5.8)

as uniformly for all points with

. As an immediate consequence, one obtains the

regular variation of the function :

(5.9)

as for all and some which is

called the coefficient of tail dependence. Moreover, the

limiting function is homogeneous of order . Since

and are asymptotically independent whenever

, in particular one has asymptotic

independence if . If and are exactly

independent, then , while, roughly speaking, values of

between 1/2 and 1 indicate a positive, but asymptotically

vanishing dependence between the large values of and . A

slight modification of this model was first suggested by Ledford and

Tawn (1996,1997).

To construct estimators of the coefficient of tail dependence, let

, , with denoting the rank of among

. Hence where is essentially the empirical cdf of

, with a minor modification to avoid

division by 0. In view of (5.9), the rv’s

(5.10)

have approximately a Pareto tail with extreme value index ,

that can be estimated by one of the usual estimators discussed in

Section 3 applied to , . Draisma et al. (2004) proved an analog to Theorem

3.1 for the tail empirical quantile function

pertaining to these rv’s. It turned out that in case of asymptotic

independence one obtains the same limit as in Theorem

3.1, so that also all the results on the extreme

value estimators discussed in Section 3 carry

over to the present situation (although the rv’s are not

exactly independent). If the components are not asymptotically

independent, one can still conclude the asymptotic normality of the

estimators of , but the formulas for the asymptotic variance

are more complicated and depend on the positive limit of

.

Drees and Müller (2008) proposed the estimator

(5.11)

of

the limiting function in (5.8) and

proved uniform convergence of the suitably standardized estimation

error towards a centered Gaussian process under suitable

smoothness conditions on . Moreover, they derived statistical

tests and a graphical tool to validate the model assumption

(5.8). Finally, the theory was applied to two

well-known bivariate data sets of claim sizes, the first describing

losses to buildings and losses to their content in Danish fire

insurances, while the second was taken from the Society of Actuaries

Group Medical Insurance Large Claims Database (cf. Section

6). In both cases it seems very likely that

condition (5.8) holds with a coefficient of tail

dependence less than 1. As the point estimates of were

larger than 1/2, the claim sizes in the different lines of business

are probably asymptotically independent, though with a

non-negligible positive dependence for finite levels. Applying

classical bivariate extreme value theory in such cases will usually

lead to a wrong assessment of the true risk insured.

So far, the extremal dependence structure has been analyzed in terms

of the joint distribution of the observations after a

standardization of the marginals to some fixed distribution

(standard Pareto or uniform). Consequently both coordinates of the

random vector have been treated symmetrically. As an alternative, in

recent years the so-called conditional extreme value (CEV) approach

has been considered, where the asymptotic behavior of one component

(after a suitable linear normalization) given that the other

component is large is investigated. For example, Abdous et al. (2005) and Abdous et al. (2008) considered the limit behavior of

(5.12)

as for elliptically distributed vectors ,

and Fougères and Soulier (2010) determined such limit distributions

for more general bivariate distributions in polar representation.

Das and Resnick (2011) examined possible limits in

(5.12) in a general framework of regular variation on

cones and discussed the relationship to the approach by Ledford and

Tawn. In the special case and (coined standard

regular varying case by Das and Resnick), the CEV approach

facilitates the analysis of the extremal dependence between large

claim sizes in absolute terms rather than just a comparison the

behavior of the conditional distribution of one claim size given

that the other is large relative to its unconditional distribution

as in the approach by Ledford and Tawn. Unfortunately, in most

applications one needs different normalizing functions and

to obtain a non-degenerate limit of (5.12).

It is worth mentioning that the methods outlined in this section are

only useful to analyze the dependence between extreme claim sizes

(or losses) observed in a small number of different lines of

insurances (usually sold to the same customer). From an economic

point of view, the dependence between different risks insured in the

same line of business is often more important. For example, in

property insurance a large storm will usually result in many claims

from customers living in the same area. With the present state of

the art, extreme value theory has little to offer to analyze the

extremal dependence in such situations. Instead, approaches using

expert knowledge (e.g., from meteorology) remain the methods of

choice.

6 Analyzing Large Claim Sizes in Health Insurance

In the years 1991 and 1992 the Society of Actuaries collected large

claim sizes (totalling $25,000 or more) in US health insurances.

The resulting large claim size database is available at the website

http://www.soa.org. For each claimant, hospital charges and

other charges were recorded in each year together with the type of

the health insurance plan and the status of the claimant (employee

or dependent), among other information. See Grazier and G’Sell

Associates (1997) for a detailed description of the data set (see

also Cebrián et al. (2003) for a statistical analysis of the total

charges).

A closer inspection of the data reveals that the structure of the

claim sizes depend on the status of the claimant and the type of the

health insurance plan. For example, the large non-hospital costs

were significantly larger for HMO (health maintenance organization),

POS (point of service) and indemnity plans than for PPO (preferred

provider organization), EPO (exclusive provider organization),

comprehensive and other indemnity plans as well as for those records

for which the type of plan was unknown. Therefore, as an example

here we analyze the claims for the second group of health plans in

the year 1992 when the claimant had the status ‘dependent’.

The sampling scheme that only those claims with total costs of at

least $25,000 were recorded introduces an artificial negative

dependence between both components: if the hospital charges were

small, say less than $5,000, then the other charges must be larger

than $20,000, and vice versa. For that reason, here we only

consider those records for which both type of charges were at least

$25,000, leading to a sample of size . (We discuss the

consequences of this choice at the end of the section.)

First we fit Pareto distributions to the marginal tails. Figure

2 shows the maximum likelihood estimator (in the

GPD model) for the extreme value index of the hospital charges

(solid line) and the Hill estimator (dashed line) as a function of

(i.e., the number of largest observations used for estimation

reduced by 1). Obviously, the graph of the ML estimator is much more

stable than that of the Hill estimator. While for the former it

seems reasonable to use at least largest observations, the

Hill plot increases more or less monotonically for , say.

Moreover, the data-driven procedures to select an optimal number of

order statistics yield very small values of for the Hill

estimator (, ).

As explained in Example

3.2, this qualitatively different behavior may be due to

a constant term in the GPD approximation of the tail, that does not

influence the shift invariant ML estimator but that leads to a large

bias of the Hill estimator if is chosen too large. In fact, the

ML estimator fits a shifted Pareto distribution with location

parameter of about for a wide range of -values. If

one adds $300,000 to each of the hospital charges, then the Hill

plot (displayed by the dash-dotted line in Figure

2) becomes very flat so that at first glance the

Hill plot suggests that one may use almost all observations to

estimate . So apparently for this data set the instability

of the Hill estimator is indeed largely due to its sensitivity to

shifts. For the shifted data the optimal number of order statistics

estimated by the bootstrap and the sequential procedure sketched in

Section 4 suggest to use the 143 and 134 largest

order statistics, respectively, resulting in a Hill estimate of

about 0.22.

Figure 2: ML estimator (solid line) and Hill

estimator (dashed line) and the Hill estimator applied to the

data shifted by $ 300,000 (dash-dotted line) based on largest hospital charges versus

; the estimated optimal number for the Hill

estimators are indicated by vertical lines

Figure 3 shows the qq-plot for the shifted data

together with the line with slope equal to the Hill estimate

for . Moreover, the

functions are

displayed as dashed lines. Here, was calculated by

Monte Carlo simulations as described in Section 4

such that the probability that all points of the qq-plot lie between

these graphs is about . (Strictly speaking, the

probability is probably a bit higher, because the band does not take

into account the fact that the shift has been chosen depending on

the data to improve on the Pareto fit.) Indeed, the fit is

reasonably good and all points lie in the band bordered by these

functions. However, for the most extreme points the qq-plot flattens

out, indicating that perhaps the fitted Pareto tail slightly

overstates the actual risk, which may be desirable for a prudent

risk assessment. (If one uses the largest 1900 observations as

suggested by a superficial inspection of the Hill plot, then the

Hill estimate is not changed much and still all points of the

qq-plot lie within the confidence band.)

Figure 3: Pareto-qq-plot of 133 largest hospital

charges together with 0.95%-“confidence band”

Figure 4 displays the ML estimator and the Hill

estimator for the second component describing the other costs. These

plots are less stable than the ones for the hospital charges. For

both estimators it seems certainly advisable to not use many more

than 350 largest observations to fit the tail; the bootstrap and the

sequential procedure suggest to merely use and

largest order statistics for the Hill estimator.

As Hill estimate one obtains

and a -confidence interval of about . Hence,

apparently the other charges are significantly heavier tailed than

the hospital charges.

Figure 4: ML

estimator (solid line) and Hill estimator (dashed line) based on

largest other charges versus

The ML estimator and the Hill estimator of the coefficient of

tail dependence between both types of costs (based on the rv’s

defined by (5.10)) are shown in Figure

5. Here perhaps up to 600 large order statistics of

the can be used for the ML estimator. Note that the

mathematical theory for the data-driven procedures of choosing

has only been developed for the Hill estimator based on iid data.

Hence, strictly speaking, it is not applicable here, but the

aforementioned result by Draisma et al. (2004) suggests that in the

present situation the sequential estimator, that yields , has the same asymptotic behavior as for iid data. The

resulting Hill estimate 0.63 hints at a rather weak, asymptotically

vanishing, but non-negligible dependence, because the pertaining

confidence interval [0.52, 0.74] does neither contain 1 or 1/2.

Figure 5: ML

estimator (solid line) and Hill estimator (dashed line) for

based on order statistics of versus

Finally, we consider the estimate defined in

(5.11). Figure 6 depicts the estimates

From these values and the estimate one can calculate

estimates of for all values because of the

homogeneity of of order :

Figure 6: Estimator of () and

()(solid line); pointwise asymptotic -confidence

intervals are indicated by dashed lines; for comparison, the lines

and are shown by dotted lines

for large . Observe that in Figure 6, the estimate

of this probability is just slightly larger than

. Hence, given that the hospital

charge exceeds a high threshold, the fact that also the other

charges exceed an analogously high threshold does not alter the

conditional distribution of the hospital charges much. The same

observation can be made with the roles of hospital charges and other

charges interchanged. This property should not be confused with the

asymptotic independence condition (5.7) in which one

conditions only at the event that one component is large. Indeed, it

can be shown that to each and each function

that is increasing on and decreasing on

with and , one can find a probability

distribution such that (5.8) holds with

Hence the function whose estimate is shown in Figure 6

can be combined with any value of the coefficient of tail dependence

in to obtain a limiting function in

(5.8). (The converse result that the function

can be represented in such a way is an easy consequence of its

homogeneity; cf. e.g. Charpentier and Juri, 2006, Remark 3.4.)

As we have considered only those claims for which both components

are at least $25,000, in fact we have analyzed the conditional

distribution of the claim sizes given that both components are at

least $25,000. If instead we use all record for which at least one

of the component exceeds $25,000, then a different conditional

distribution is analyzed. Indeed, for this larger data set one

obtains higher estimates of the coefficient of tail dependence,

indicating a stronger extremal dependence between both types of

charges. At first glance, this fact seems counterintuitive, because

in assumption (5.9) only probabilities of events occur

in which both components are large. Notice, however, that the

have been calculated by transforming using the

marginal cdf , and this marginal distribution is different for

the two conditional settings described above. For that reason, in

contrast to the first impression, the parameter and likewise

the limiting function also depend on the stochastic behavior of

the vector on the regions where just one of the components is large.

7 Proofs

Proof of Corollary 3.4. For the sake of simplicity, we assume that is continuous on

for some , but a slight refinement

of the arguments given below shows that the assertion holds without

this continuity assumption.

With

and , the estimation error can be decomposed

as follows:

It will turn out that, under the conditions of the corollary, the

term III dominates all other terms.

Because

(which is interpreted as for

), the mean value theorem shows that

for some between and , which implies .

First consider the case . Then uniformly over the range of integration, because

(7.1)

uniformly for by assumptions (3.16) and (3.17).

It follows that and , and thus by condition (3.17)

uniformly over the range of integration.

Therefore, in the case , , direct calculations yield

where in the last but one step again (7.1) has been

used. For , analogous arguments yield

In the case we have uniformly over the range of

integration. A Taylor expansion of and of at

shows that the integrand of III equals

In view of the asymptotic normality of , the assertion is

obvious if we can show that the other terms in the above

decomposition of the estimation error are of smaller order.

To derive an upper bound for the term , note that by (3.7), (3.12) and

(7.1)

To deal with small values of , recall the following well-known

facts about the order statistics of iid rv’s that are

uniformly distributed over :

(7.2)

and in probability (see, e.g., Shorack and Wellner, 1986, (10.3.7) and (10.3.8)). Because

has the same distribution as

, it follows by assumption

(3.13) that for

(7.3)

one has

uniformly for , where in

the last step we have used (7.2) which implies

Therefore,

in probability uniformly for .

Now assertion (4.2) is obvious from the law of

iterated logarithm for Brownian motions and the fact that is

constant on .

If is bounded, the continuous mapping theorem

yields

(7.4)

Since is constant on intervals of the form

, the continuity of implies

for all . Finally, by the law of iterated logarithm

combined with (7.4)

in probability as , so that assertion (4.3)

follows. The last assertion is immediate from

with

denoting the Dirac measure in 1 (cf. Drees (1998b), Example 3.1).

In view of (4.5) this condition is fulfilled, and so convergence

(4.2) holds.

By the law of the iterated logarithm

as . Hence, in view of (4.2), it

suffices to prove that

(7.6)

in probability for all sequences . Because

as and

, (7.6) would follow

from

(7.7)

To establish (7.7), one may argue similarly as in the second part of the proof of

Corollary 4.1 using the uniform tail empirical

quantile function, but it is easier to work with a Hungarian

construction for partial sums with

, , denoting iid standard exponential rv’s. More concretely, for

suitable versions of there exist a Brownian motion

such that a.s.

Moreover, the variational distance between the distribution of

and the distribution of

tends to 0 (Reiss, 1989,

Theorem 5.4.3). Hence, to verify (7.7), it suffices

to prove that

in probability.

The Hungarian construction and the law of iterated logarithm

imply

uniformly for . Hence, the first term

in (7) is of the stochastic order

in probability, which completes the proof of

(4.6). The second assertion follows exactly as in

the proof of Corollary 4.1.

Acknowledgement: I thank the anonymous referees for their

constructive criticism and remarks that led to a substantial

improvement of the presentation.

References

Abdous, B., Fougères, A.-L., and Ghoudi, K. (2005). Extreme

behavior for bivariate elliptical distributions. rev. Canad. Statist.33, 1095–1107.

Abdous, B., Fougères, A.-L., Ghoudi, K., and Soulier, P. (2008). Estimation of bivariate excess probabilities

for elliptical models. Bernoulli14, 1065 -1088.

Beirlant, J., Goegebeur, Y., Segers, J., Teugels, J., de Waal, D.,

and Ferro, C. (2004). Statistics of Extremes. Wiley.

Cebrián, A.C., Denuit, M., and Lambert, P. (2003).

Generalized Pareto fit to the society of

actuaries large claims database. N. Am. Actuar. J.7, 18–36.

Charpentier, A., and Juri, A. (2006). Limiting dependence structures for tail events, with applications to

credit derivatives. J. Appl. Probab.43, 563–586.

Charpentier, A., and Segers, J. (2009). Tails

of multivariate Archimedean copulas. J. Multiv. Anal.100, 1521–1537.

Danielsson , J., de Haan, L., Peng, L., and de Vries, C.G. (2001).

Using a bootstrap method to choose the sample fraction in tail

index estimation. J. Multiv. Anal.76, 226–248.

Das, B., and Resnick, S.I. (2011). Conditioning on an extreme component:

Model consistency and regular variation on cones. Bernoulli17, 226 -252.

Dietrich, D., de Haan, L., and Hüsler, J. (2002) Testing extreme

value conditions. Extremes5, 71–85.

Draisma, G., Drees, H., Ferreira, A., and de Haan, L. (2004).

Bivariate tail estimation: dependence in asymptotic independence. Bernoulli10, 251–280.

Drees, H. (1998a). On smooth statistical tail functionals.

Scand. J. Statist.25, 187–210.

Drees, H. (1998b). A general class of estimators of

the extreme value index. J. Statist. Plann. Inference66, 95–112.

Drees, H. (2003). Extreme Quantile Estimation for Dependent

Data with Applications to Finance. Bernoulli9, 617–657.

Drees, H., de Haan, L., and Resnick, S. (2000).

How to make a Hill plot. Ann. Statist.28, 254–274.

Drees, H., and Kaufmann, E. (1998). Selecting the optimal

sample fraction in univariate extreme value statistics. Stoch. Processes Appl.75, 149–172.

Drees, H., Ferreira, A., and de Haan, L. (2004). On the maximum likelihood estimation

of the extreme value index. Ann. Appl. Probab.14, 1179–1201.

Drees, H., and Müller, P. (2008). Fitting and validation of a bivariate model for large claims.

Insurance Math. Econom.42, 638–650.

Einmahl, J.H.J., and Segers, J. (2009). Maximum empirical

likelihood estimation of the spectral measure of an extreme value

distribution. Ann. Statist.37, 2953–2989.

Embrechts, P., Klüppelberg, C. and Mikosch, T. (1997).

Modelling Extremal Events, Springer.

Fougères, A.-L., and Soulier, P. (2010). Limit conditional

distributions for bivariate vectors with polar representation.

Stoch. Models26, 54–77.

Grazier, K.L., and G’Sell Associates (1997):

Group Medical Insurance Large Claims Data Base Collection and

Analysis.

SOA Monograph M-HB97-1, Society of Actuaries, Schaumburg,

Illinois.

de Haan, L., and Ferreira, A. (2006). Extreme Value Theory.

Springer.

Ledford, A.W., und Tawn, J.A. (1996). Statistics for near

independence in multivariate extreme values. Biometrika83, 169–187.

Ledford, A.W., and Tawn, J.A. (1997).

Modelling Dependence within Joint Tail Regions,

J. Royal Statist. Soci.59, 475–499.

McNeil, A. (1997). Estimating the tails of loss severity

distributions using extreme value theory. ASTIN Bull.27, 117–137.

Mikosch, T. (2006). Copulas: Tales and facts (with discussion). Extremes. 9, 3–62.

Reiss, R.-D. (1989). Approximate Distributions of Order

Statistics. Springer.

Schmutz, M., and Doerr, R.R. (1998).

The Pareto model in property reinsurance. Swiss Re publication.

Shorack, G.R., and Wellner, J.A. (1986). Empirical Processes

with Applications to Statistics. Wiley.

Vandewalle, B., and Beirlant, J. (2006). On univariate extreme value statistics and the estimation

of reinsurance premiums. Insurance Math. Econom.38,

441–459.