ON DETERMINING THE NUMBER OF SPIKES IN A HIGH-DIMENSIONAL SPIKED POPULATION MODEL

Abstract

In a spiked population model, the population covariance matrix has all its eigenvalues equal to units except for a few fixed eigenvalues (spikes). Determining the number of spikes is a fundamental problem which appears in many scientific fields, including signal processing (linear mixture model) or economics (factor model). Several recent papers studied the asymptotic behavior of the eigenvalues of the sample covariance matrix (sample eigenvalues) when the dimension of the observations and the sample size both grow to infinity so that their ratio converges to a positive constant. Using these results, we propose a new estimator based on the difference between two consecutive sample eigenvalues.

keywords:

Spiked population model; High-dimensional statistics; Sample covariance matrices; Factor model; Extreme eigenvalues; Tracy-Widom laws.31 March 2011***Preprint of an article submitted for consideration in “Random Matrices: Theory and Applications (RMTA)” ©2010 [copyright World Scientific Publishing Company] \urlhttp://www.worldscinet.com/rmta/

Mathematics Subject Classification 2000: 62F07, 62F12, 60B20

1 Introduction

In a spiked population model, the population covariance matrix has all its eigenvalues equal to units except for a few fixed eigenvalues (spikes). This model appears in many scientific fields often with different names. In economics, it is called “factors model” within the Ross Arbitrage Pricing Theory (APT) and the aim is to relate observed data (assets) to a small dimensional set of unobserved variables which are then estimated [1]. In physics of mixture, “linear mixture model” are naturally considered for various phenomena [2]. In wireless communication, a signal emitted by a source is modulated and received by an array of antennas which will permit the reconstruction of the original signal.

An important question to be addressed under this model is how many factors/ components/signals there are. It is generally a first step preliminary to any further study such as estimation and forecasting.

Many methods for determining the number of factors have been developed, based on the minimum description length (MDL), Bayesian model selection or Bayesian Information Criteria (BIC) (See [3]). Nevertheless, these methods are based on asymptotic expansions for large sample size and may not perform well when the dimension of the data is large compared to the sample size . To avoid this problem of high dimension, several methods have been recently proposed using the random matrix theory, such as Harding [4] or Onatski [5] in economics, and Kritchman & Nadler [6] in array processing or chemometrics literature.

In this paper, we present a new estimator for the number of spikes from high-dimensional data. Our approach is based on the results of Bai & Yao [7] and Paul [8] which give the limiting distributions of the extreme eigenvalues of a sample covariance matrix coming from a spiked population model, and a recent result of Benaych-Georges, Guionnet & Maida [9]. The obtained results are presented in Section 3.

The remaining sections of the paper are organized as follows. In Section 2, we introduce the spiked population model, and recall known results on the almost sure limits of extreme eigenvalues which lead to the idea of our estimator. In Section 3 we define precisely our estimator and prove its consistency in the case of simple spikes with known variance. Next we give a method of estimation in the case of simple spikes with unknown variance. In Section 4, we define the factor/linear mixture model that we link to the spiked population model and we compare our method to those of Harding [4] and Kritchman & Nadler [6]. We consider the case of spikes with greater multiplicity in Section 5. Finally, we discuss the extension to the generalized spiked population model. Throughout the paper, simulation experiments are conducted to access the quality of the proposed estimation.

2 Spiked Population Model

We consider , where is a zero-mean random vector of i.i.d. components, is an orthogonal matrix and

where has non null and non unit eigenvalues with respective multiplicity (). Therefore, the eigenvalues of the population covariance matrix are unit except the , called spike eigenvalues. Notice that, if the observations are Gaussian, we may assume that is diagonal by using a suitable orthogonal transformation.

Let be independent copies of . The sample covariance matrix is

It is assumed in the sequel that is fixed, and and are related so that when , . Moreover, we assumed that for all . For , we define the function

Let be the eigenvalues of the sample covariance matrix . Let for . Baik and Silverstein [10] proved that, under a moment condition on , for each and almost surely,

In other words, with the hypotheses that for all , and has multiplicity , then is the limit of packed sample eigenvalue , . They also prove that for all with a prefixed range almost surely,

Our aim is to estimate when only is known. The idea is to use, as suggested in Onatski [5], differences between consecutives eigenvalues

Indeed, applying the results quoted above it is easy to see that a.s. if , while when , tends to a positive limit if the are different. Thus it is possible to detect from index-numbers where becomes small.

3 Case of Simple Spikes with Known Variance

In this section, we suppose that is known and that all the spikes are simple, i.e . Under these hypotheses the population eigenvalues are

We also need the following assumption:

The entries of the random vector have a symmetric law and a sub-exponential decay, that is there exists positive constants C, C’ such that, for all ,

Especially, the Gaussian vectors satisfy this hypothesis.

As stated previously the main observation is that when one follows the sample eigenvalues in a descending order, the successive spacings shrink to small values when approaching non-spiked values. Therefore, our estimation method will use a carefully determined threshold . We propose to estimate by the following

where is a fixed number big enough, and is a level to determine. In practice, the integer should be thought as a preliminary bound on the number of possible spikes.

3.1 Consistency

Theorem 3.1.

Let be copies i.i.d. of , where is a zero-mean random vector of i.i.d. components which satisfies Assumptions 3 and is an orthogonal matrix. Assume that

where has non null, non unit and different eigenvalues . Assume that when .

Let be a real sequence such that and . Then the estimator is strongly consistent, i.e almost surely when .

In the sequel, we will assume that (If it is not the case, we consider ). For the proof, we need two theorems. The first, Proposition 3.2, shows that the limiting law of is Gaussian (Bai and Yao [7] and Paul [8]):

Proposition 3.2.

Assume that the entries of satisfy , for all and have multiplicity 1. Then as , so that ,

where .

Proposition 3.3.

We also need the following lemma:

Lemma 3.4.

Let be a tight sequence of random variables. Then for all real sequence which diverges to infinity,

Proof 3.5.

As is a tight sequence, for all , it exists a compact such that, for all , . Furthermore, as , it exists such that for all , . So . Consequently, .

Proof 3.6.

Case of . In this case, (non-spike eigenvalues). We consider the following sequence of random variables

By Proposition 3.3, is a tight sequence. So by using Lemma 3.4, for any sequence , we have

Therefore

We choose such that . So we have

with

It follows

Therefore

Case of . These indices correspond to the spike eigenvalues. By using Proposition 3.2 and the previous argument, it is easy to show that we can choose a real sequence , such that and

where

Therefore

-

•

For all , we have

Let

-

•

For , . By using the first section of the proof, one can show that

Let

-

•

Therefore for all we have

As and for all , , it exists ,

So we have

Conclusion. and , therefore

3.2 Simulation experiments

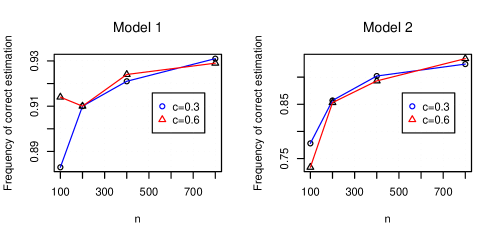

Now we will illustrate the previous result by some simulations. First, we have to chose the sequence to be used. Theoretically speaking, all the sequences satisfying the requirement such that are convenient. We tested several sequences and we decided to take one of the form which a sequence proportional to : this idea came from that, as in the case of the mean of i.i.d random variables, the corresponding to the non-spikes tend to a gaussian law. So we can conjecture a result analog to the law of the iterated logarithm for the , . Finally, we choose and simulate two different models: one with dispersed spikes which should lead to an easier estimation of , and a more difficult case with closer spikes: {itemlist}

Model 1: , ;

Model 2: , . Note that the values of Model 1 have been chosen to be the same as in [4]. For each model, two different values of , 0.3 and 0.6, are considered. We give in Tables 1-2 and 3, respectively, the distribution of , its mean and mean squared error over 1000 independent replications. The frequency of is given in Figure 1.

Mean, mean squared error and empirical distribution of over 1000 independent replications for Model 1. Distribution of Mean MSE 1 2 3 4 5 6 7 (30,100) 5.057 0.212 0.001 0.007 0.009 0.0 0.883 0.1 0.002 (60,200) 5.081 0.107 0.001 0.001 0.0 0.0 0.91 0.088 0.0 (120,400) 5.079 0.073 0.0 0.0 0.0 0.0 0.921 0.079 0.0 (240,800) 5.069 0.064 0.0 0.0 0.0 0.0 0.931 0.069 0.0

(Continued) Mean, mean squared error and empirical distribution of over 1000 independent replications for Model 1. Distribution of Mean MSE 1 2 3 4 5 6 7 (60,100) 5.056 0.139 0.001 0.004 0.003 0.002 0.914 0.076 0.0 (120,200) 5.08 0.098 0.0 0.001 0.002 0.0 0.91 0.087 0.0 (240,400) 5.072 0.079 0.002 0.0 0.0 0.0 0.924 0.075 0.0 (480,800) 5.072 0.069 0.0 0.0 0.0 0.0 0.929 0.07 0.001

Mean, mean squared error and empirical distribution of over 1000 independent replications for Model 2. Distribution of Mean MSE 0 1 2 3 4 5 (30,100) 3.718 1.086 0.0 0.001 0.059 0.0 0.778 0.085 (60,200) 3.925 0.582 0.013 0.024 0.019 0.0 0.857 0.087 (120,400) 4.005 0.331 0.01 0.01 0.001 0.0 0.902 0.077 (240,800) 4.062 0.110 0.002 0.001 0.0 0.0 0.924 0.073 (60,100) 3.478 1.655 0.053 0.086 0.059 0.001 0.734 0.067 (120,200) 3.818 0.823 0.025 0.033 0.024 0.0 0.853 0.065 (240,400) 3.969 0.394 0.009 0.015 0.011 0.0 0.893 0.072 (480,800) 4.051 0.108 0.003 0.0 0.0 0.0 0.934 0.063

In both cases, we can observe the asymptotic consistency of the estimator. Comparing the two models, except the last case , the estimator performs better in Model 1 than in Model 2. This phenomenon is due to the fact that the differences between consecutive eigenvalues are smaller than in Model 2 so that it is more difficult to distinguish spikes from non spikes.

Within a same model, the convergence is slower in the case. We could explain this by the fact that the gap between two consecutive spike eigenvalues stays the same, and when increases, the spectrum of is more dispersed, so that the differences from non- spikes are larger and again our detection problem is more difficult.

It is worth mentioning that the chosen constant leads to a slight over-estimation of for the tested sizes . This finite-sample behaviour could be improved with a more sophisticated choice of which however seems a difficult point to address.

4 Case of Simple Spikes with Unknown Variance

In practice, the scale parameter is also unknown and we need to estimate it as well. First, we will explain how to do in the non-spikes (null) case, i.e. , and then in the case with spikes.

4.1 Estimation of the variance in the white case

We consider a zero-mean random vector with population covariance matrix

We keep the previous assumptions. We will use the law of large numbers to estimate the unknown variance . We have the following theorem (Marčenko and Pastur [11], Bai and Silverstein [12])

Proposition 4.1.

Assume that, for any :

Then, with probability one, the empirical spectral distribution (ESD) of weakly converges to the Marčenko-Pastur distribution with ratio index and scale parameter , denoted by , which has a density function

where and .

Note that represents the mean of the limiting distribution. Moreover, it is well-known that under the condition of the Proposition 4.1, it holds almost surely,

4.2 Determining the number of spikes with an unknown variance.

As we notice in the first section, when the variance is known and different of one, we only have to divide the consecutive difference by this variance. As the variance is unknown, we will replace it by the estimate , which converges almost surely to when . Nevertheless, because of the spikes, the variance of will be greater than the one in the null case. The variance will be minimum if we only take the mean of the non-spike eigenvalues i.e those that have an index . The problem is that we don’t know . By consequence, the idea is to make a first estimation of with . Then, if , we set (So we have ), and we reestimate by using this new estimation. We repeat it until we find an indice such that . If such an indice doesn’t exist, the algorithm will stop at the preliminary bound fixed initially. To sum up, here is the algorithm:

q1=0 sigma2=1/p*(lambda_1+...+lambda_p) q2="estimator of the known variance case with division by sigma2" while q2~=q1 do q1:=q2 sigma2=1/(p-q1)*(lambda_(q1+1)+...+lambda_p q2="estimator of the known variance case with division by sigma2" end result=(q1,sigma2)

4.3 Simulation experiments

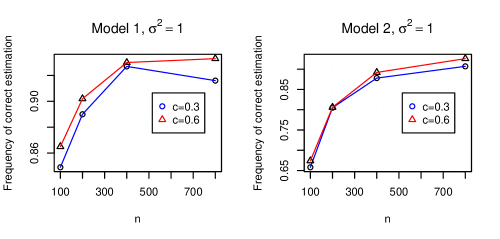

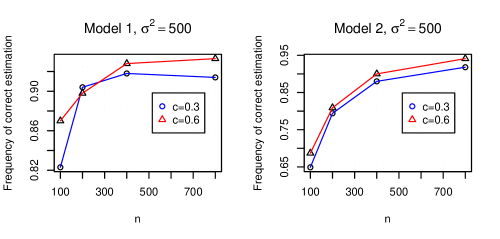

We conduct the simulations with two values of the variance , and to see if a high variance will influence the estimation. We keep the same other parameters as in the previous simulation study of Section 3 and estimate and the number of spikes with the method explained above. Additional to the statistics about the spikes number estimator , we provide also those about the final estimate of the unknown variance. The results are displayed in Tables 4 to 8.

Mean, mean squared error and empirical distribution of , mean and mean squared error of over 1000 independent replications for Model 1 and . Distribution of Mean MSE 1 2 3 4 5 6 7 Mean MSE (30,100) 5.052 0.338 0.003 0.015 0.008 0.0 0.849 0.0 0.125 0.955 0.015 (60,200) 5.108 0.112 0.0 0.001 0.0 0.0 0.89 0.107 0.002 0.97 0.0 (120,400) 5.069 0.076 0.0 0.001 0.0 0.0 0.927 0.072 0.0 0.986 0.0 (240,800) 5.084 0.077 0.0 0.0 0.0 0.0 0.916 0.084 0.0 0.993 0.0

(Continued) Mean, mean squared error and empirical distribution of , mean and mean squared error of over 1000 independent replications for Model 1 and . Distribution of (60,100) 5.087 0.236 0.001 0.009 0.004 0.0 0.865 0.122 0.002 0.943 0.003 (120,200) 5.095 0.092 0.0 0.0 0.001 0.0 0.902 0.097 0.0 0.971 0.0 (240,400) 5.07 0.065 0.0 0.0 0.0 0.0 0.93 0.07 0.0 0.985 0.0 (480,800) 5.067 0.063 0.0 0.0 0.0 0.0 0.933 0.067 0.0 0.993 0.0

Mean, mean squared error and empirical distribution of , mean and mean squared error of over 1000 independent replications for Model 2 and . Distribution of Mean MSE 0 1 2 3 4 5 6 Mean MSE (30,100) 3.362 2.019 0.079 0.078 0.091 0.0 0.658 0.094 0.0 1.052 0.043 (60,200) 3.806 1.023 0.032 0.038 0.026 0.0 0.805 0.098 0.001 0.994 0.005 (120,400) 3.983 0.483 0.019 0.008 0.004 0.0 0.878 0.091 0.0 0.991 0.001 (240,800) 4.071 0.144 0.003 0.001 0.001 0.0 0.907 0.088 0.0 0.994 0.0 (60,100) 3.367 1.898 0.069 0.081 0.096 0.001 0.674 0.079 0.0 1.003 0.012 (120,200) 3.781 1.04 0.034 0.034 0.036 0.0 0.806 0.089 0.001 0.986 0.002 (240,400) 3.965 0.472 0.015 0.015 0.007 0.0 0.892 0.071 0.0 0.99 0.0 (480,800) 4.052 0.125 0.002 0.003 0.0 0.0 0.926 0.069 0.0 0.994 0.0

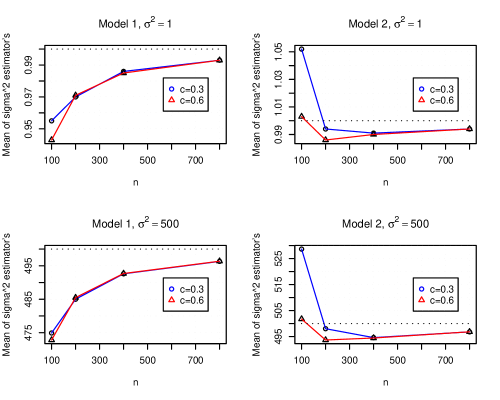

Empirical distribution of , mean and mean squared error of over 1000 independent replications for Model 1 and . Distribution of 1 2 3 4 5 6 7 Mean MSE (30,100) 0.003 0.012 0.005 0.0 0.823 0.155 0.002 474.909 3281.714 (60,200) 0.0 0.001 0.0 0.0 0.904 0.094 0.001 485.019 99.558 (120,400) 0.0 0.001 0.0 0.0 0.918 0.080 0.001 492.608 21.244 (240,800) 0.0 0.0 0.0 0.0 0.914 0.086 0.0 496.316 3.519 (60,100) 0.002 0.008 0.006 0.001 0.870 0.113 0.0 472.816 688.994 (120,200) 0.0 0.002 0.0 0.0 0.898 0.099 0.001 485.49 55.489 (240,400) 0.0 0.0 0.0 0.0 0.928 0.071 0.001 492.699 7.242 (480,800) 0.0 0.0 0.0 0.0 0.933 0.067 0.0 496.377 1.654

Empirical distribution of , mean and mean squared error of over 1000 independent replications for Model 2 and . Distribution of 0 1 2 3 4 5 6 Mean MSE (30,100) 0.079 0.088 0.090 0.0 0.649 0.093 0.001 528.651 11223.872 (60,200) 0.037 0.037 0.029 0.0 0.794 0.103 0.0 498.032 1478.184 (120,400) 0.009 0.01 0.005 0.0 0.880 0.096 0.0 494.613 107.355 (240,800) 0.003 0.0 0.002 0.0 0.918 0.075 0.002 496.813 8.770 (60,100) 0.071 0.104 0.059 0.001 0.687 0.078 0 501.754 3126.083 (120,200) 0.036 0.038 0.043 0.0 0.809 0.074 0.0 493.687 438.063 (240,400) 0.013 0.007 0.009 0.0 0.900 0.071 0.0 494.445 39.686 (480,800) 0.004 0.001 0.0 0.0 0.941 0.054 0.0 496.836 3.576

First, we can see the asymptotic consistancy of the estimator of in all the four cases. If we compare these simulations with the known variance case, we can see that the estimation is less accurate in the small . Furthermore, as in the previous case, the convergence is slower in the case and the estimator performs better in Model 1 than in Model 2, for both values of . The estimation of is more accurate with an unknown variance of .

We also give the mean and mean squared error of in the case (Tables 4-5 and 6) to compare with Tables 1-2 and 3, where also, to see the effect of its estimation. The variance and the bias are higher especially for small values of in this case with unknown variance.

The estimation of performs well, but it seems to be underestimated. There is no particular difference between the two values of in Model 1 but in Model 2, contrary to the estimation of , the convergence seems to be faster in the case for . The variance of the estimator decreases with the increase of and , and is less in the case. As expected, the variance is lower in the case.

5 Comparaison with two Related Methods

In signal processing or econometric literature, the factor model (or linear mixture model) is often used. This model is defined as follows: let be an i.i.d -sample of -dimensional random vectors satisfying

where {itemlist}

are random factors (or signals) assumed to have zero mean, unit variance and mutually uncorrelated;

is a fixed unknown matrix of rank (response vectors or factor loadings);

is the noise level, .

It is easy to show that in this case, the population covariance matrix takes the form of a spiked population model: the spikes are only slightly modified. If we denote by the vector of spikes in the factor model, we have the following relationship with our original vector

Here determining the number of spikes means the detection of the number of factors/signals . We will explain and compare two methods from Econometrics (Harding [4]) and signal processing (Kritchman & Nadler [6]), respectively.

5.1 Method of Harding and comparison

In his paper [4], Harding uses less restrictive hypotheses as the sequence is not necessarily independent, but he simulates a Gaussian model. His general idea is to compare the spectral moments of with the ESD of without the factors (or spikes), and to remove the largest eigenvalues one by one in until a “distance” between the moments is minimum.

More precisely, the variance of the noise is seen as a parameter and his idea is to write () as a sum of a finite rank perturbation of the noise covariance . Let be the vector of the first moments of the empirical spectral distribution (ESD) of the covariance matrix , the equivalent for and its limit as and , . Here is the procedure of Harding: {itemlist}

First, compute the moments of the asymptotic eigenvalue distribution of the covariance matrix of for a large sample.

By Bai and Silverstein ([12]), we have that . Consequently, estimate by:

where is a consistent estimate of , calculate by estimated from a first step estimation with .

Next, remove the largest eigenvalue of the spectrum of and re-estimate the parameter as previously to get a new estimate .

This step is repeated by progressively removing large eigenvalues and for prefixed number of times to get a sequence of estimates , , …etc.

Finally, among the minimized objective functions choose the order one which corresponds to the smallest minimized value:

Actually, we know that for fixed and , , . So the criterion is the minimization of the variance : it decreases until (until we have removed the eigenvalues corresponding to the spikes), then it stays stable. The procedure of Harding leads to an underestimation of , at and fixed. That is why he penalized the function with a function of type , where is the number of eigenvalues removed, is the estimated variance at the step and is a function such that when , . The finally proposed choice for is the following function given by Bai and Ng [3] based on a BIC criterion

For his simulation experiment, he tested four different “distances” but we only keep the one based on the BIC criterion which is the best. Furthermore, we don’t give all cases he tested. The simulation design was a little bit different, indeed Harding does not choose the spikes directly, but he generates as a Gaussian law and in a deterministic way. We calculate the corresponding spikes and it leads to the following values: {itemlist}

:

:

:

: Nonetheless, these cases stay very close. Below we compare his results to ours. We only give in Table 9 the mean and mean squared errors of the estimator as reported in Harding’s paper.

Compared mean and mean squared error of our and and those of Harding over 5000 independent replications and . Harding estimator Our estimator Harding estimator Our estimator Mean MSE Mean MSE Mean MSE Mean MSE (30,100) 5.028 0.028 5.087 0.266 0.942 0.004 0.946 0.008 (90,100) 5.040 0.048 5.049 0.232 0.944 0.001 0.943 0.0 (210,300) 5.004 0.004 5.087 0.082 0.982 0.0 0.980 0.0 (250,500) 5.002 0.002 5.077 0.072 0.989 0.0 0.988 0.0

Both methods perform well and their results are overall very close except that Harding’s estimation yields a slightly smaller MSE for . However, one should have in mind that this estimation has a very complex construction and a rigorous justification of its different steps is still open. Moreover, the spikes in Table 9 are large and well-separated one from another; it remains unclear how this method will perform in a case where the spikes are much smaller and close like in Model 2, considered in Sections 3 and 4. By contrast, our estimator has a very simple construction and we proved its consistency under reasonable assumptions.

5.2 Method of Kritchman & Nadler and comparison

These authors assume the Gaussian case. In the absence of spikes, follows a Wishart distribution with parameters . In this case, Johnstone [13] gave the asymptotic distribution of the largest eigenvalue of .

Proposition 5.1.

Let be the sample covariance matrix of vectors distributed as , and be its eigenvalues. Then, when , such that

where , and is the i-th Tracy-Widom distribution.

Assuming the variance is known. To distinguish a spike eigenvalue from a non-spike one at an asymptotic significance level , their idea is to check whether

| (1) |

where the value of can be found by inverting the Tracy-Widom distribution. This distribution has no explicit expression, but can be computed from a solution of a second order Painlevé ordinary differential equation. Their estimator is based on a sequence of nested hypothesis tests of the following form: for ,

For each value of , they test the likelihood of the -th eigenvalue as arising from a signal or from noise as (1). If (1) is satisfied, is accepted and is increased by one. The procedure stops once an instance of is rejected and the number of spikes is estimated to be . Formally, their estimator is defined by

When is unknown, they estimate it by the same method we used. For their simulations, they use four different settings, with {itemlist}

A1: , (i.e. );

A2: , ;

B1: , (i.e. ;

B2: , ; with and . Notice that contrary to ours and those of Harding, in their simulation, and the difference between two consecutive spikes is higher. We add two settings with different variance {itemlist}

A2’: , , (i.e. );

B2’: , , (i.e. ); and . The results are displayed in tables 10 and 11.

Summary for showing the frequency of . Our estimator Estimator KN A1; 0.943 0.994 A2; 0.966 0.993 A2’; 0.602 0.513 B1; 0.348 0.238 B2; 0.947 0.995 B2’; 0.734 0.682

With small and , both estimator performs well, except for the A2’, B1, and B2’ cases where the spikes are closer to than in the other cases.

Summary for showing the frequency of . Our estimator Estimator KN A1; 0.995 0.994 A2; 0.986 0.993 B1; 0.999 0.999 B2; 0.986 0.994

With larger and , the results from both methods are comparable. Nevertheless, theoritical properties remain unclear for the KN estimator: it is proved that

and, in the one factor case () that

That is by construction, the proposed estimator cannot be fully consistent but nearly consistent with an incompressible asymptotic error of . Actually the authors are using a very small test level in their experiments. Whether this property remains true for general case with more than one spike stays open and even so, this near-consistency is a bit unsatisfactory from a theoretical point a view.

6 Case of Spikes with Multiplicity greater than one

The problem with two identical spikes is that the difference between the corresponding eigenvalues of the sample covariance matrix will tend to zero. Nevertheless, our method still works: we can explain it by the fact that the convergence of the , for (non-spikes) is in , whereas that of the difference corresponding of two identical spikes is in (Consequence of theorem 3.1 of Bai & Yao [7]). Furthermore, the variance in the convergence of this difference is , which is quite high for high spikes. A complete justification of our method in this case with multiple spikes is still under investigation. Here we provide some simulation results in order to have a first idea about its performance.

We will only consider the known variance case. If it is not the case, the procedure explained before will apply without any problem. Here are the results with the same simulation design as previously, except that we introduce multiple spikes. We consider two models:

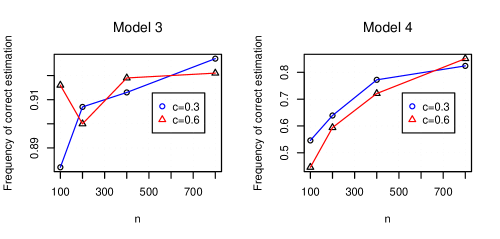

Model 3: , ;

Model 4: , .

For each model, two different values of , 0.3 and 0.6, are considered, and we give in Figure 5 the frequency of and in Table 12 the mean and the mean squared error of our estimator over 1000 independent replications.

Mean and mean squared error of over 1000 independent replications for Model 1 and 2. Model 3, Model 4, Mean MSE Mean MSE (30,100) 6.085 0.168 4.529 4.393 (60,200) 6.077 0.121 4.86 4.199 (120,400) 6.088 0.082 5.31 3.061 (240,800) 6.073 0.068 5.597 2.051 (60,100) 6.043 0.151 4.118 4.797 (120,200) 6.092 0.108 4.614 4.453 (240,400) 6.081 0.074 5.159 3.447 (480,800) 6.079 0.073 5.562 2.058

In both cases, we can observe the asymptotic consistency of the estimator, but the convergence is slower in Model 4: indeed, the eigenvalue spacings are smaller. Furthermore, the values of the spikes are small, so that the variance in the convergence of the spikes is not very high and the fluctuations of the difference are smaller than in Model 3.

7 Extension to the generalized spiked population model

In [14], the author define the generalized spiked population model: the covariance matrix is extended to a general T from I. Once we have corresponding Tracy-Widom limits for sample eigenvalues converging to the edges of support intervals, our approach can be readily adapted to this situation. However such results are lacking.

References

- [1] S.A. Ross, The arbitrage theory of capital asset pricing, J. Economic Theory, 13 (1977) 341–360.

- [2] T. Naes, T. Isaksson, T. Fearn and T. Davies, User-friendly guide to multivariate calibration and classification, NIR Publications, Chichester (2002).

- [3] J. Baik and S. Ng, Determining the number of factors in approximate factor models, Econometrica 70 (2008) 191–221.

- [4] M.C. Harding, Structural estimation of high-dimensional factor models, Econometrica r&r.

- [5] A. Onatski, Testing hypotheses about the number of factors in large factors models, to appear in Econometrica, (2008).

- [6] S. Kritchman and B. Nadler, Determining the number of components in a factor model from limited noisy data, Chem. Int. Lab. Syst 94 (2008) 19–32.

- [7] Z.D. Bai and J.F. Yao, Central limit theorems for eigenvalues in a spiked population model, Ann. Inst. H. Poincar Probab. Statist. 44(3) (2008) 447–474.

- [8] D. Paul, Asymptotic of sample eigenstructure for a large dimensional spiked covariance model, Statistica Sinica 17 (2007) 1617–1642.

- [9] F. Benaych-Georges, A. Guionnet and M. Maida, Fluctuations of the extreme eigenvalues of finite rank deformations of random matrices, Preprint.

- [10] J. Baik and J.W. Silverstein, Eigenvalues of large sample covariance matrices of spiked population models, J. Multivariate Anal. 97 (2006) 1382–1408.

- [11] V.A. Marčenko and L. A. Pastur, Distributions of eigenvalues of some sets of random matrices, Math. USSR-Sb. 1 (1967) 507–536.

- [12] Z.D. Bai and J.W. Silverstein, CLT for linear spectral statistics of large-dimensional sample covariance matrices, Ann. Probab. 32 (2004) 553–605.

- [13] I.M. Johnstone, On the distribution of the largest eigenvalue in principal component analysis, Ann. Stat. 29 (2001) 295–327.

- [14] Z.D. Bai and J.F. Yao, Limit theorems for sample eigenvalues in a generalized spiked population model,Arxiv Preprint arXiv: 0806.114 (2008).