Robustness and Contagion in the International Financial Network

Abstract

The recent financial crisis of 2008 and the 2011 indebtedness of Greece highlight the importance of understanding the structure of the global financial network. In this paper we set out to analyze and characterize this network, as captured by the IMF Coordinated Portfolio Investment Survey (CPIS), in two ways. First, through an adaptation of the “error and attack” methodology[1], we show that the network is of the “robust-yet-fragile” type, a topology found in a wide variety of evolved networks. We compare these results against four common null-models, generated only from first-order statistics of the empirical data. In addition, we suggest a fifth, log-normal model, which generates networks that seem to match the empirical one more closely. Still, this model does not account for several higher order network statistics, which reenforces the added value of the higher-order analysis. Second, using loss-given-default dynamics[2], we model financial interdependence and potential cascading of financial distress through the network. Preliminary simulations indicate that default by a single relatively small country like Greece can be absorbed by the network, but that default in combination with defaults of other PIGS countries (Portugal, Ireland, and Spain) could lead to a massive extinction cascade in the global economy.

Intro

Globalization has created an international financial network of countries linked by trade in goods and assets. These linkages allow for more efficient resource allocation across borders, but also create potentially hazardous financial interdependence, such as the global ripple following the 2008 collapse of Lehman Brothers and the potential financial distress that may follow the potential restructuring of Greece’s debt obligations. Increasingly, the tools of network science are being used as a means of articulating in a quantitative way measures of financial interdependence and stability.

Network approaches have proved useful for articulating the interdependence of many kinds of complex systems, including economic systems and the global economy (see e.g., [3, 4]). Of particular relevance are the studies of the World Trade Web (WTW), derived from OECD data[5], in which countries are linked according to the value of exports between them. The WTW articulates just one aspect of the global economy and the focus herein is on the international financial asset network as derived from the CPIS, a key financial network whose assets grew by a factor of in real US dollars in the three decades leading up to the 2008 financial crisis[6], exceeding annual world GDP in 2006 and 2007. Our interest is in characterizing the structure of the CPIS network, especially as it relates to aspects of systemic risk related to nation default. While the related problem of bank “contagion” in interbank networks has drawn much interest (see e.g., [7, 8, 9, 10]), the analogous problem considered at the scale of nations in the network of inter-nation investment has attracted much less research attention, in spite of its acknowledged and reported importance for the safety and health of the global economy [11]. Initial efforts in this direction have been made via the study of degree distributions [12, 13].

In particular, in this paper we perform two kinds of analyses. In the first we perform so-called “knockout experiments” on a network of countries connected according to a threshold in their CPIS financial relationship. In these experiments countries are removed one by one from the network (via some criteria explained below) and with this, all connections to and from the corresponding nodes. Robustness is measured according to the degradation in connectivity as measured by an increase in the average shortest path length (ASPL) of the network; ASPL provides a natural proxy for financial integration. Knockout methodology has already been applied in a variety of contexts, including the World Wide Web (WWW) [1], metabolic networks [14], protein networks [15], and in the form of extinction analyses conducted on food web models of ecosystems (see e.g., Section 4.6 of [16] and the many references therein as well as [17]). In the economic context knockouts have very recently been applied to study the WTW [18].

The Network

We derive the international financial network structures from the IMF’s CPIS database. The IMF CPIS comprises bilateral annual data from 2001 to 2009 derived from the external portfolio of financial assets aggregated at the country level from up to reporting countries vis-à-vis countries[19, 20]. External assets are reported in terms of millions of current US dollars (USD) and thresholded at USD. If we restrict the network to reporting countries with available GDP data[21, 22], we obtain a subset of at least countries for each year. The portfolios of these countries restricted to the same subset give a self-contained network that accounts for at least percent of their total external assets. For the sake of analytical consistency, we restrict our analysis to these core subsets.

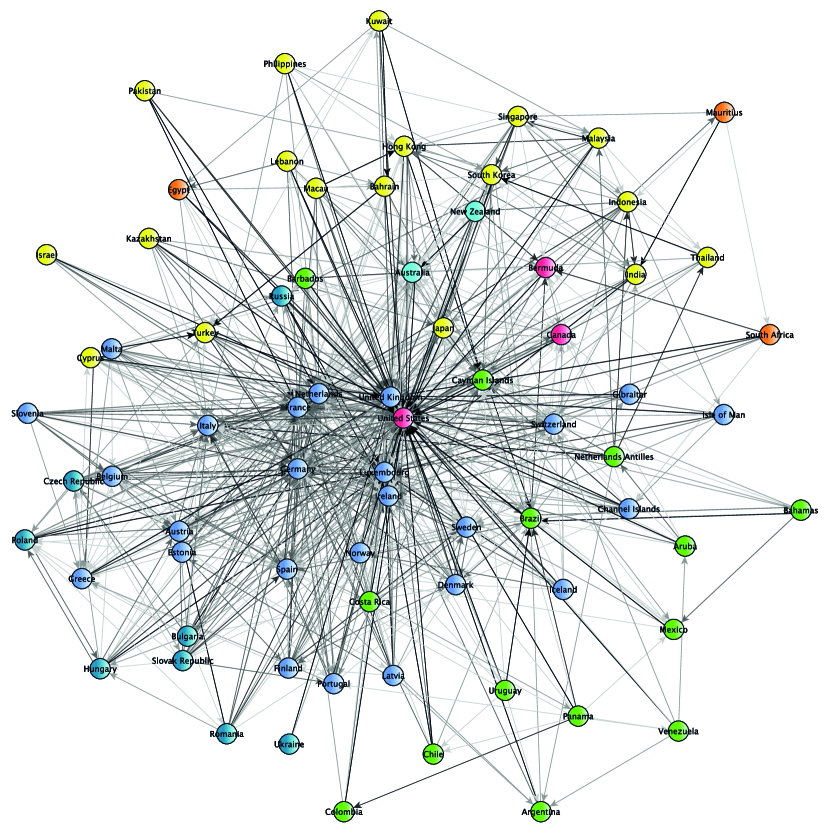

We encode a principal binary network structure for these core subsets in two adjacency matrices and , by applying two different thresholding rules. For a given year, let denote the amount of country ’s assets issued by residents of country and let be the number of countries in the core subset under investigation. Then, matrix encodes an edge () if , that is, if country ’s portfolio contains above average exposure to country . See Figure 1 for a visualization of the representation of for the 2009 data. Matrix , on the other hand, encodes an edge ( if exceeds a threshold , representing the average percent GDP-normalized investment in these networks. We choose these two simplified representations of the network, but acknowledge the hidden complexity that is missed in the aggregation of assets in the CPIS data and simplified international financial links. Future work should work to articulate the finer detail; we see this paper as a first and necessary step toward a more sophisticated analysis.

Given the binary directed networks, we generate comparison networks according to four common null-models. For the simplest, Erdós-Renyi (ER) model, has nodes and an edge between any two nodes exist with probability , where is the average out-degree of the empirical network. For the second and third models, and have an edge between countries and with probabilities and , where and are country and ’s empirical out- and in-degree. Finally, the fourth model assigns equal probability to all graphs that preserve the in- and out-degree of . To generate such graphs, we use the rewiring approach (see e.g., [23]). Thus, these four null models each generate networks based only on an increasing number of first order characteristics of the empirical binary network.

We also make use of a fifth null comparison model that takes into account the weight distribution of the original asset network. We find a reasonable fit to the asset distributions by using a log-normal model with country dummies

| (1) |

where and are constants for each country as q holder and issuer of assets, and . The plus one term on the LHS is a work-around, given that the CPIS data is left censored. We use maximum-likelihood estimation to predict the ’s, ’s and .111Noting that the left-censoring and rounding implicit in the CPIS data downward biases the estimate, we scale this estimate by 1.183, as suggested by fitting the model to generated but left-censored and rounded data. Figure 2(a) shows the distribution of predicted after fitting this model to all nine years of available data. While a Jarque–Bera test rejects that these residuals are normally distributed for several years, this test similarly results in a type I error when applied to data generated by the log-normal model but was left-censored and rounded. Comparing the predicted residual distributions of the empirical and generated data visually provides further evidence that this simple model fits the empirical data surprisingly well.

Error and Attack

We test the robustness of the CPIS network as captured by matrices or via the effect of “error and attack” simulations [1] on the average shortest path length (ASPL) in the network. Here the network is subjected to the iterated removal of either a random node (via “error”) or the most “important” (via “attack”), as measured by the sum of a node’s in- and out-degree. While other measures of importance can also be used, our measure follows intuitively as this ‘attack’ takes out the greatest number of direct paths, thus attacking the tracked ASPL measure.

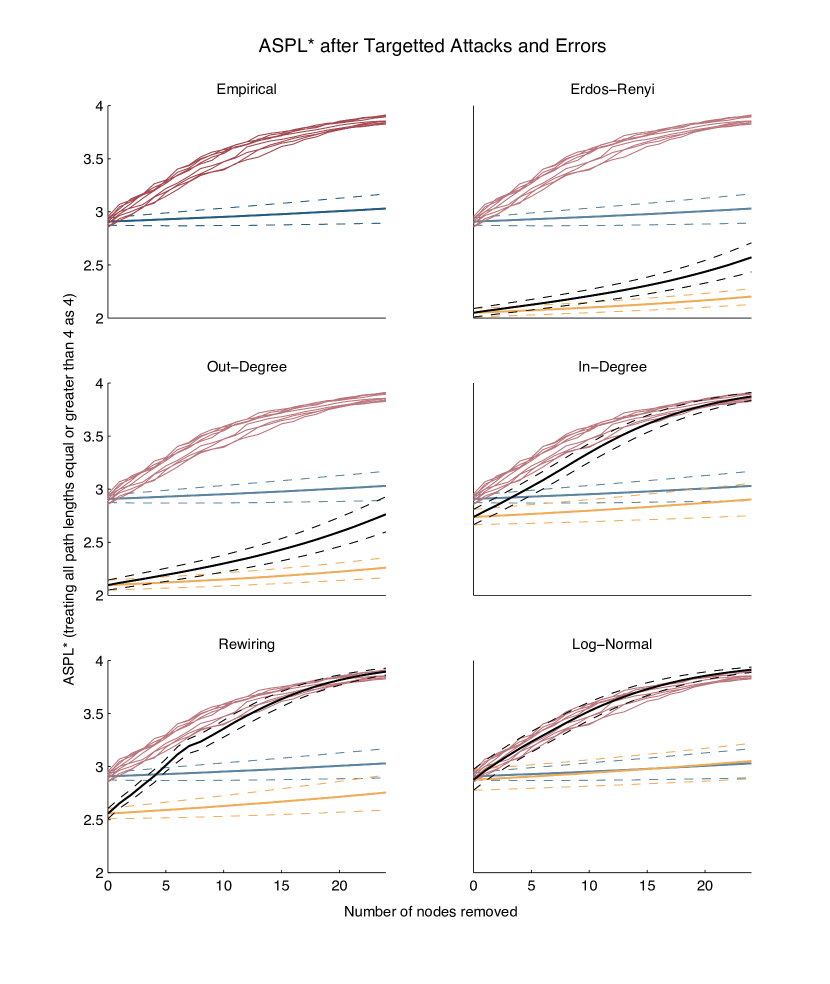

The shortest path length (SPL) between any two nodes is a useful proxy for financial integration; a low SPL indicates a high degree of direct investment (a shortest path length of one) and common investment through cross-border positions of intermediate countries (a shortest path length of two). However, as the length of the SPL grows it becomes a less useful indicator. Also, not all pairs of nodes have paths between them. Thus we choose a modified measure of the ASPL, by treating all SPLs greater than three as having a length of four.222We also tracked the evolution of simpler measures, such as the fraction of SPLs equal or less than two. These measured provided qualitatively very similar results. Figures 3 and 4 show the general evolution of the modified ASPL under repeated error or attack for the empirical as well as the null model networks, given the two specifications.

The simulations reflect the existence of key financial centers. While random removal of nodes does not noticeably affect ASPL, targeted removal causes an immediate and rapid increase for both types of thresholding. The simulations on networks of type , point to the importance of financial hubs. The empirical network starts out significantly less ‘integrated’ than the first four null models. Further, the attack method affects ASPL significantly less in the first two null models which disregard the in-degrees of countries in the empirical model. As simulations on the third and fourth null models show, matching the empirical in-degree sequence is still insufficient to explain the networks lack of greater integration as proxied by ASPL; though, the log-normal model appears to match the empirical results very well.

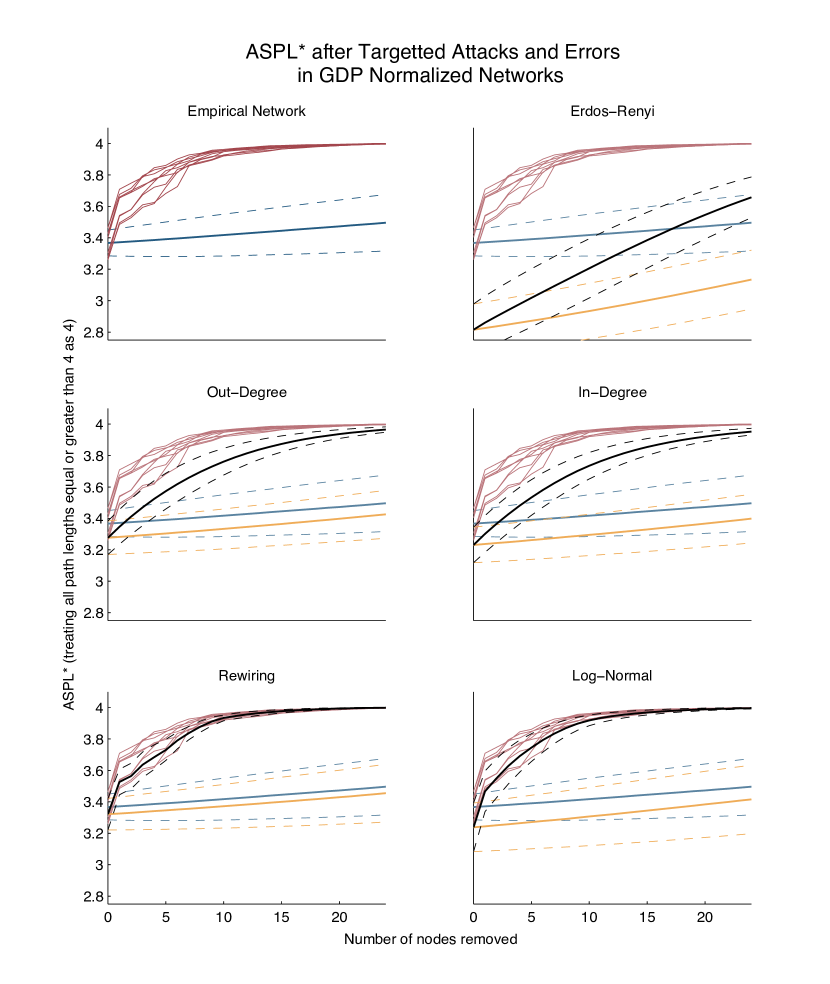

For simulations on the GDP thresholded networks, the rewiring null model appears to match the empirical model best. Again, the empirical model starts less integrated than the first three null models and is particularly susceptible to the first attack, the removal of the worlds largest economy, the US. The rewiring and the log-normal model both seem to match these results closely, with the former doing slightly better. Thus, it appears the observed error-attack effect on the networks’ ASPL may already be encoded in the first order statistics used for the null model.

We formally test whether the ASPL, as well as several other higher order statistics of the empirical networks, are outliers within the null model families. For each empirical network we generated 10000 networks of each null-model and constructed 95 percent confidence intervals for the ASPL and 5 other network statistics. Table 1) summarizes how often the empirical networks produced measures below or above these confidence intervals. The results support several of our above conjectures; e.g we find that the ASPL of the networks is indeed best matched rewiring null model. Still, none of the null models can properly account for all the listed higher order statistics. Notably, the last measure, the probability that country has a path to conditional on having path to and a path to is above the confidence intervals of all null models for all years and specifications. Hence, the null models’ first-order statistics appear unable to account for several relevant characteristics of the empirical network structure.

| ER | Out-deg. | In-deg. | Rewiring | Log-Normal | ||||||

| Network Measure | A | B | A | B | A | B | A | B | A | B |

| Fraction of SP | -1 | -1 | -1 | 0 | -.79 | -.33 | -1 | -.56 | 0 | -.11 |

| Fraction of SP | -1 | -1 | -1 | -.33 | -1 | -.78 | -1 | -.56 | -.11 | -.67 |

| Modified ASPL | 1 | 1 | 1 | .33 | .89 | .78 | 1 | .67 | 0 | .44 |

| Assortativity | -1 | -1 | -1 | -.89 | 1 | -.89 | 1 | .78 | .11 | 0 |

| Avg. Clustering Coefficent | 1 | 1 | 1 | 1 | 1 | 1 | 1 | -.22 | 1 | 0 |

| Pr | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 |

Preliminary LGD Simulations

The error and attack methodology does not account for any potential dynamics – that is, the simulation proceeds simply by successive deletion of nodes without any accounting for the potential contagion of financial distress. In our second set of simulations we attempt to model such potential economic dynamics, that is, financial interdependence. We adopt so-called loss-given-default (LGD) dynamics, originally developed for modeling cascades of bank failures [25, 2], to provide a method of propagating financial shock. The simulation starts with an initial country or set of countries defaulting on their financial liabilities. Any other country whose financial positions in the defaulted country/countries exceeds certain thresholding conditions will also default, which in turn may result in further defaults. The simulation terminates when no further countries are defaulting. Analogous extinction simulations are common as a means for understanding the robustness of food webs [26], ecological networks whose nodes represent species in an ecosystem wherein species is linked to species if preys on (so that provides resources to ) [26, 16, 27]. More recently, these kinds of extinction studies have been analogized to the WTW [18].

We acknowledge that such simulations may be overly simplistic, given the degree of aggregation of the CPIS data and the great heterogeneity of international banking activities. Nonetheless, they provide an interesting start for modeling potentially severe global cascades of financial distress. As a result, the following analysis is still preliminary.

For the LGD simulations, we specify two separate thresholding conditions. A country will default if its total investment in the defaulted countries both exceeds some fraction () of its total external investment and some fraction () of its GDP; that is, country will default if and , with D being the set of defaulted countries. As a result, threshold incorporates a general ability of countries to absorb sufficiently small losses relative to its portfolio and threshold assumes a country-specific ability to absorb losses of assets proportional a country’s economic output. Note, we may incorporate a fact, that a default us unlikely to yield a complete loss of financial assets of the defaulting country (but a certain haircut) by scaling and appropriately.

As an example, if we choose and initialize by defaulting any one of the PIGS countries in the 2007 network, there is at most a single subsequent default. However if we initialize by defaulting both Greece and Ireland (while using the same threshold values) then we see (Figure 5) six subsequent rounds of defaults in a sequence that reflects financial interdependence spreading initially across Western Europe, which subsequently affects the US and the rest of the world. In the end, only a subset of mostly emerging market economies survives the default cascade, as their total amounts of international financial assets are small relative to their respective GDP.

|

|

|

|

|

|

|

|

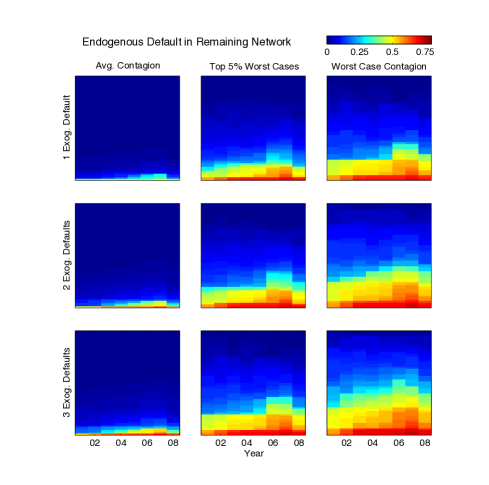

A broad set of LGD simulations under a range of values for and shows a notable increase in financial interdependence (as external positions increased) from 2001 to 2007. We consider all possible model specifications with , excluding the trivial case . For each threshold specification and year, all possible combinations of the initial default of and countries were simulated, to produce the measures of the mean, mean of the worst 5%, and worst-case impact on . Impact is measured in terms of the fraction of countries that eventually default under LGD. The analysis shows a general increase in severity of worst-case contagion from 2001 to 2007; most notably, the number of specifications that produce a default of more than of the network in the worst case doubles in 2006 and 2007 (see Figure 6). The LGD simulations show a decrease in financial interdependence at the end of 2008. The result may appear counterintuitive. However, the 2008 crises yielded a substantial amount of asset losses, and an overall reduction in country-to-country foreign asset positions. Thus, financial interdependence appears lower at the end of 2008, as the LGD model does not account for already incurred losses. Incorporating such dynamic aspects may be one area for improvement of our models. Similarly, simulations could benefit from improved foundations for thresholding conditions. Average contagion remains very limited over all years, pointing once more to the general robustness of the network.

The simulations also identify the countries responsible for worst-case impact. Table Preliminary LGD Simulations lists the ten most influential countries and ten most influential combinations of two or three countries as measured by their worst case default scenarios. The US is the single most contagious country followed by financial centers like the UK, the Cayman Islands and Luxembourg (which is tied with Germany for fourth place). More interesting is the frequent appearance of Brazil, as a partner (with the United States) in the second most influential pair of countries and then its prevalence among the most influential triples. Similarly, middle income countries like Turkey and Indonesia also appear in the top 10 list of influential pairs or triples. Note, that western countries tend to be strongly linked with the US, while financial exposure of emerging market economies relative to their GDP tend to substantially lower. Subsequently, in model specification where a default of the US is sufficient to bring down the western world, countries like Brazil gain in importance; they can still spur further default within the small remaining network of emerging market economies, noted above.

Global concerns over the solvency of the PIGS nations motivates us to consider a restricted study of the initial defaults by PIGS countries in 2007. In this we see the different effects of the two thresholds. Figure 7 shows the degree of the network’s financial interdependence with respect to any combination of up to three PIGS countries, with the portfolio threshold (with increments of ) and the GDP threshold (with increments of ). For fixed , the portfolio threshold (on the y-axis) in most cases yields only a unique threshold which determines whether or not a specific initial default leads to further defaults, and when it does, the scenario is generally constant. Conversely, for fixed , we see a more graduated behavior in terms of number of defaults, steadily decreasing as the threshold increases.

Global concerns over the solvency of the PIGS nations motivates us to consider a restricted study of the initial defaults by PIGS countries in 2007. In this we see the different effects of the two thresholds. Figure 7 shows the degree of the network’s financial interdependence with respect to any combination of up to three PIGS countries, with the portfolio threshold (with increments of ) and the GDP threshold (with increments of ). For fixed , the portfolio threshold (on the y-axis) in most cases yields only a unique threshold which determines whether or not a specific initial default leads to further defaults, and when it does, the scenario is generally constant. Conversely, for fixed , we see a more graduated behavior in terms of number of defaults, steadily decreasing as the threshold increases.

Conclusion

We believe that the robustness studies undertaken here are an important first step in the development of metrics for the study of systemic risk in the global economy. The application of error and attack analysis on the CPIS network and its effect on the average shortest path length produce robustness results similar to those of a scale-free network, indicating robust-yet-fragile structure. Loss-given-default dynamics produce simulations that show an increase from 2001 to 2007 in network fragility with respect to failure of key countries. The different analytical tools all highlight the key importance of the United States and the centrality of european countries. In general, most simulations support the idea that a failure of the US in 2008 would have had far reaching consequences for the entire network. Similarly, the concerns over the default of Greece seem real as simulations indicate that with the failure of Greece (or any of the PIGS nations) the global economy was one default away from a contagion cascade. Models that assume low thresholds for contagion also predict that the default of a combination of PIGS countries may be similarly severe. The only countries relatively unaffected by such global finical crisis seem to be middle income countries, whose external financial assets are relatively small as a share of their GDP. We believe that these and analogous knock-out studies may be of use in further refining our understanding of the global financial network. Further, more targeted simulations may help informing important policy decisions.

References

- [1] Albert, R., Jeong, H. & Barabasi, A.-L. Error and attack tolerance of complex networks. Nature 406, 378 (2000).

- [2] Upper, C. Using counterfactual simulations to assess the danger of contagion in interbank markets. BIS Working Papers (2007).

- [3] Schweitzer, F. et al. Economic networks: The new challenges. Science 325 (2009).

- [4] Garas, A., Argyrakis, P., Rozenblat, C., Tomassini, M. & Havlin, S. Worldwide spreading of economic crisis. New J. Phys. 12 (2010).

- [5] http://privatewww.essex.ac.uk/ksg/exptradegdp.html.

- [6] Guide to the International Financial Statistics. Working Paper Series (Bank for International Settlements, 2008). URL http://www.bis.org/statistics/locbankstatsguide.pdf. Authored by the Monetary and Economic Department.

- [7] Gai, P. & Kapadia, S. Contagion in financial networks. Proceedings of the Royal Society A 466, 2401–2423 (2010).

- [8] Aikman, D. et al. Funding liquidity risk in a quantitative model of systemic stability. Bank of England Working Paper (2009).

- [9] Alessandri, P., Gai, P., Kapadia, S., Mora, N. & Puhr, C. Towards a framework for quantifying systemic stability. International Journal of Central Banking 5, 47–81 (2009).

- [10] Boss, M., Summer, M. & Thurner, S. Contagion flow through banking networks. Lecture Notes in Computer Science 3038, 1070–1077 (2004).

- [11] A very european crisis. The Economist (2010). URL http://www.economist.com/node/15452594.

- [12] Song, D.-M., Jiang, Z.-Q. & Zhou, W.-X. Statistical properties of world investment networks. Physica A: Statistical Mechanics and its Applications 388, 2450 – 2460 (2009).

- [13] Kubelec, C. & Sá, F. The geographical composition of national external balance sheets: 1980-2005. Working Paper, Bank of England (2008).

- [14] Jeong, H., Tombor, B., Albert, R., Oltvai, Z. N. & Barabási, A.-L. The large-scale organization of metabolic networks. Nature 407, 651–654 (2000).

- [15] Jeong, H., Mason, S. P., Barabási, A.-L. & Oltvai, Z. N. Lethality and centrality in protein networks. Nature 411, 41 (2001).

- [16] Dunne, J. A. The network structure of food webs. In Pascual, M. & Dunne, J. A. (eds.) Ecological Networks: Linking Structure to Dynamics in Food Webs, 27–86 (Santa Fe Institute Studies on the Sciences of Complexity Series: Oxford University Press, New York, 2006).

- [17] Allesina, S. & Mercedes, M. Googling food webs: Can an eigenvector measure species’ importance for coextinctions? PLoS Comput Biol 5, e1000494 (2009). URL http://dx.doi.org/10.1371%2Fjournal.pcbi.1000494.

- [18] Foti, N., Pauls, S. & Rockmore, D. Stability of the world trade web over time - an extinction analysis. arXiv:1104.4380v2 [q-fin.GN] (2011).

- [19] IMF Task Force on Coordinated Portfolio Investment Survey. Coordinated portfolio investment survey guide (International Monetary Fund, Washington, D.C., 2002), 2nd edn.

- [20] http://www.imf.org/external/np/sta/pi/cpis.htm.

- [21] http://www.imf.org/external/data.htm.

- [22] http://data.worldbank.org/data-catalog/world-development-indicators.

- [23] Maslov, S. & Sneppen, K. Specificity and stability in topology of protein networks. Science 296, 910–913 (2002). URL http://www.sciencemag.org/content/296/5569/910.abstract. http://www.sciencemag.org/content/296/5569/910.full.pdf.

- [24] https://sites.google.com/a/brain-connectivity-toolbox.net/bct/Home.

- [25] Furfine, C. H. Interbank exposures: Quantifying the risk of contagion. Journal of Money, Credit and Banking 35, 111–128 (2003).

- [26] Allesina, S. & Pascual, M. Googling food webs: Can an eigenvector measure species’ importance for coextinctions? Issue of PLoS Computational Biology 5 (2009).

- [27] Dunne, J. A., Williams, R. J. & Martinez, N. D. Network structure and robustness of marine food webs. Mar. Ecol. Prog. Ser. 273, 291–302 (2004).