e-mail: ukandilarov@uni-ruse.bg ,

2Department of Applied Mathematics and Statistics, Comenius University

e-mail: sevcovic@fmph.uniba.sk

Comparison of Two Numerical Methods for Computation of American Type of the Floating Strike Asian Option

Abstract

We present a numerical approach for solving the free boundary problem for the Black-Scholes equation for pricing American style of floating strike Asian options. A fixed domain transformation of the free boundary problem into a parabolic equation defined on a fixed spatial domain is performed. As a result a nonlinear time-dependent term is involved in the resulting equation. Two new numerical algorithms are proposed. In the first algorithm a predictor-corrector scheme is used. The second one is based on the Newton method. Computational experiments, confirming the accuracy of the algorithms are presented and discussed.

1 Introduction

In this paper we consider the problem of pricing American style Asian options, analyzed by Bokes and the second author in [1] (see also [11]). Asian options belong to the group of the so-called path-dependent options. Their pay-off diagrams depend on the spot value of the underlying asset during the whole or some part(s) of the life span of the option. Among path-dependent options, Asian option depend is on the arithmetic or geometric average of spot prices of the underlying asset. During the last decade, the problem of solving the American option problem numerically has been subject for intensive research [1, 6, 9, 10, 13] (see also [11] for overview). A comprehensive introduction to this topic can be found in [6]. Comparison of various analytical and numerical approximation methods of calculation of the early exercise boundary a position of the American put option paying zero dividends is given in [7]. An improvement of Han and Wu’s algorithm [4] is described in [14]. Our goal is to propose and investigate two front-fixing numerical algorithms for solving free boundary value problems. The front-fixing method has been successfully applied to a wide range of applied problems arising from physics and engineering, cf. [3, 8] and references therein. The basic idea is to remove the moving boundary by a transformation of the involved variables. Transformation techniques were used in the analysis and numerical computation of the early exercise boundary in the context of American style of vanilla options [10] as well as Asian floating strike options [1, 11, 12]. In comparison to the existing computational method [1] we do not replace the algebraic constraint by its equivalent integral form (see [1, 12] for details) which is computationally more involved. In this paper we solve the corresponding parabolic equation with an algebraic constraint directly as it was proposed in [11]. The approach presented in [11] however suffered from the necessity of taking very small time discretization steps. Here we overcome this difficulty by proposing two new numerical approximation algorithms (see Section 4). They are based on the novel technique proposed by the first author and Valkov in [5]. We extend this approach for American style of Asian options. In Section 5, a numerical example illustrating the capability of our algorithms are discussed.

2 The Free Boundary Problem

Following the classical Black-Scholes theory, the second author and Bokes [1] analyzed the problem of pricing Asian options with arithmetically averaged strike price by means of a solution to a parabolic PDE with a free boundary :

| (1) |

satisfying the boundary conditions

| for any and , | (2) | ||||

| (3) |

and the terminal condition (terminal pay-off condition) at the maturity time :

| (4) |

Here is the stock price, is the averaged strike price, is the risk-free interest rate, is a continuous dividend rate and is the volatility of the underlying asset returns. The arithmetically averaged price calculated from the price path at the time is defined as . For floating strike Asian options, it is well known (see e.g. [6, 2, 1]) that one can perform a dimension reduction by introducing a new time variable and a similarity variable defined as: . The spatial domain for the reduced equation is given by , , . Following ([10, 13, 1]), we can apply the Landau fixed domain transformation for the free boundary problem by introducing a new state variable and an auxiliary function , representing a synthetic portfolio. Here . In [1, 10, 13] it is shown that under suitable regularity assumptions on the input data the free boundary problem (1)–(4) can be transformed into the initial boundary value problem for parabolic PDE:

| (5) | |||

| (8) |

The coefficients and are defined as follows:

| (9) |

According to [1] the free boundary function and the solution should fulfill the constraint:

| (10) |

As for derivation of the initial free boundary position in (10) we refer to [1] or [6, 2]. A solution to the problem (5)-(10) is continuous for . The discontinuity appears only at the point . The derivatives of the solution exist and are sufficiently smooth in , outside of a small neighbourhood of . Another important fact to emphasize is that for times (i.e. when ) the coefficients become unbounded.

3 Finite Difference Schemes

In order to solve the problem (5)-(10) numerically, we introduce which is sufficiently large upper limit of values of the variable (a safe choice is to take is equal to five times ), where we prescribe . Next, for given positive integers and we define the uniform meshes: and . Our goal is to define a finite difference method which is suitable for computing for and associated front position for . The implicit difference scheme has the following form:

| (14) | |||||

| (15) |

| (16) |

For the initial condition for the free boundary we have . An algebraic nonlinear system of equations can be derived from (14) for , (14) and (16). In [9] the authors apply implicit finite difference scheme, semi-implicit scheme and upwind explicit scheme for the American put option, combining with the penalty method. The time step parameter for the explicit case is very small, . Therefore in this work we consider the case of a fully implicit scheme. One can also apply a scheme of the Crank-Nicolson type.

4 Numerical Algorithms

In order to solve the nonlinear system of algebraic equations we developed the following two algorithms.

Algorithm 1. This algorithm is based on the predictor-corrector scheme and consists in the following steps, (see also [15, 16] for the case of pricing American put options).

Step 1. Predictor. Let the solution and the free boundary position on the time level be known. Instead of (16) we use another approximation of (10) by introducing an artificial spatial node :

| (17) |

An additional equation can be obtained from (5) by taking the limit and using the fact that :

| (18) |

Using (17) we can express as:

| (19) |

Inserting it into (18) we conclude the following equation for the value :

| (20) |

Instead of the implicit scheme (14) we make use of its explicit variant for in order to derive

| (21) |

This way we obtain a nonlinear system (20), (21) for unknowns and . The system is indeed nonlinear as depend on . Now, by replacing and we construct the predictor value of .

Step 2. Corrector. We again use Equation (14) in a slightly different form:

| (22) |

where approximation takes into account the already constructed predictor value , i.e.

| (23) |

Next we use the corrected solution and Equation (16) in order to obtain the corrected value for the free boundary position on the next time layer.

Algorithm 2. We now describe an algorithm based on the Newton method. A variant of this method was applied for an American Call option problem in [5].

Step 1. We eliminate the known boundary values and from (14). Taking into account (16) we obtain a nonlinear system for unknowns: , and . We denote by the vector of these unknowns at the -th iteration.

Step 2. We have to solve the equation with where correspond to Equations (14) and (16), respectively. To this end, we apply the Newton method in the following form: , with the Jacobi matrix defined by: where

where and . Similarly , , . As for the elements of the matrix we have:

and . The iteration process is repeated until the condition is fulfilled.

Step 3. The solution on the -th time layer is considered as an initial iteration for the next time layer. For solving we perform the following stages. First, we solve the linear system of equations . Since the matrix is tridiagonal we can apply the Thomas algorithm to find . Next, we solve

Remark 1

In both algorithms we choose the last time step with , i.e. . To overcome possible numerical instabilities of these methods for (i.e. ) we use the so called upwind and downwind approximations of the term depending of the sign of the term .

5 Numerical Experiments

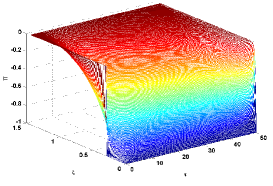

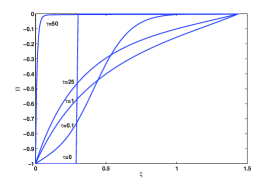

In this section we consider problem (1) with parameter values , , and , taken from examples presented in [1]. Since there exists no analytical solution to the proposed free boundary problem, we use the mesh refinement analysis with doubling the mesh size . In Tab. 1 we present the position of the free boundary position at different times constructed by the Newton method. We also present the difference between two consecutive values and the convergence ratio are presented. The results show nearly first order of accuracy for the free boundary and the CR increases with increasing (see Tab. 1). In Fig. 1a) a 3D plot of the portfolio function for , , is presented. In Fig. 1b) the profiles of the function for obtained by the Newton method are depicted.

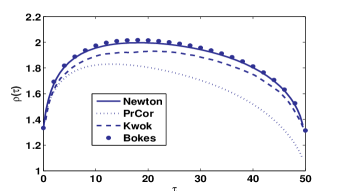

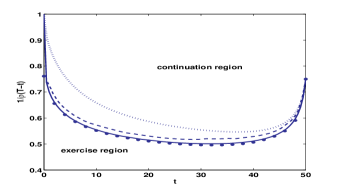

In Fig. 2a) we show a comparison of the free boundary position computed by our two algorithms (Predictor-corrector and Newton’s based method) and by numerical methods from [1] (Bokes) and [2] (Kwok). It turns out that the Newton’s based method gives nearly the same results as those of [1, 2]. On the other hand, predictor-corrector methods slightly underestimates the free boundary position . In Fig. 2b) we show the free boundary position for the original model variables and . The continuation region and exercise region are also indicated.

| difference | CR | difference | CR | difference | CR | ||||

|---|---|---|---|---|---|---|---|---|---|

| 50 | 1.949988 | - | - | 1.991675 | - | - | 1.796663 | - | - |

| 100 | 1.955552 | 5.5640e-3 | - | 1.995525 | 3.8502e-3 | - | 1.803276 | 6.6133e-3 | - |

| 200 | 1.958037 | 2.4850e-3 | 1.16 | 1.996945 | 1.4194e-3 | 1.44 | 1.805149 | 1.8729e-3 | 1.82 |

| 400 | 1,959199 | 1.1617e-3 | 1.10 | 1.997515 | 5.7099e-4 | 1.31 | 1.805667 | 5.1799e-4 | 1.85 |

| 800 | 1.959758 | 5.5965e-4 | 1.05 | 1.997765 | 2.4919e-4 | 1.20 | 1.805813 | 1.4621e-4 | 1.82 |

|

|

| a) | b) |

6 Conclusions

In this paper we have analyzed numerical algorithms for solving the free boundary value problem for American style of floating strike Asian options. To solve corresponding degenerate parabolic problem we have applied Landau’s front fixing transformation method. We proposed two numerical algorithms based on the predictor-corrector scheme and the Newton’s method. The predictor-corrector scheme is computationally faster when compared to the Newton method. It yields a good approximation close to expiry. However, its accuracy is decreased for times close to the initial time. The second algorithm based on Newton’s method yields better approximation results over the whole time interval. Although all finite difference approximations are of second order, due to discontinuity of the initial datum and nonlinear behavior of the coefficients in all discrete equations, the results show nearly the first order rate of convergence.

Acknowledgments

The first author was supported by projects Bg-Sk-203/2008 and DID 02/37-2009. The second author was supported by the project APVV SK-BG-0034-08.

|

|

| a) | b) |

References

- [1] Bokes, T., Ševčovič, D.: Early exercise boundary for American type of floating strike Asian option and its numerical approximation, to appear in: Applied Mathematical Finance, 2011.

- [2] Dai, M., Kwok, Y.K.: Characterization of optimal stopping regions of American Asian and lookback options. Math. Finance 16(1) (2006) 63–82.

- [3] Gupta, S. C.: The Classical Stefan Problem: Basic Concepts, Modelling and Analysis. North-Holland Series in Applied Mathematics and Mechanics, Elsevier, Amsterdam (2003).

- [4] Han, H., Wu X.: A fast numerical method for the Black-Scholes equation of American options. SIAM J. Numer. Anal. 41(6) (2003) 2081–2095.

- [5] Kandilarov, J., Valkov, R.: A Numerical Approach for the American Call Option Pricing Model, Lecture Notes in Computer Science 6046 (2011) 453–460.

- [6] Kwok., J. K.: Mathematical Models of Financial Derivatives. Springer-Verlag (1998).

- [7] Lauko, M., Ševčovič, D.: Comparison of numerical and analytical approximations of the early exercise boundary of the American put option. ANZIAM journal 51 (2010) 430–448.

- [8] Moyano, E., Scarpenttini, A.: Numerical stability study and error estimation for two implicit schemes in a moving boundary problem. Num. Meth. Partial Differential Equations, 16(1) (2000) 42–61.

- [9] Nielsen, B., Skavhaug, O., Tveito, A.: Penalty and front-fixing methods for the numerical solution of American option problems, Journal of Comput. Finance, 5(4) (2002) 69–97.

- [10] Ševčovič, D.: Analysis of the free boundary for the pricing of an American call option. Eur. J. Appl. Math. 12 (2001) 25–37.

- [11] Ševčovič, D.: Transformation methods for evaluating approximations to the optimal exercise boundary for linear and nonlinear Black-Sholes equations. In: M. Ehrhard (ed.), Nonlinear Models in Mathematical Finance: New Research Trends in Optimal pricing, Nova Sci. Publ., New York (2008) 153–198.

- [12] Ševčovič, D., Takáč, M.: Sensitivity analysis of the early exercise boundary for American style of Asian options, to appear in: International Journal of Numerical Analysis and Modeling, Ser. B, 2011.

- [13] Stamicar, R., Ševčovič, D., Chadam, J.: The early exercise boundary for the American put near expiry: Numerical approximation. Canadian Applied Mathematics Quarterly, 7(4) (1999) 427–444.

- [14] Tangman, D. Y., Gopaul, A., Bhuruth, M.: A fast high-order finite difference algorithms for pricing American options. J. Comp. Appl. Math. 222 (2008) 17-29.

- [15] Zhu, S.-P., Zang, J.: A new predictor-corrector scheme for valuing American puts. Applied Mathematics and Computation 217 (2011) 4439–4452.

- [16] Zhu, S.-P., Chen, Wen-Ting: A predictor corrector scheme based on the ADI method for pricing American puts with stochastic volatility. to appear in: Computers & Mathematics (2011)