Archimedean Survival Processes

Abstract

Archimedean copulas are popular in the world of multivariate modelling as a result of their breadth, tractability, and flexibility. McNeil and Nešlehová (2009) showed that the class of Archimedean copulas coincides with the class of positive multivariate -norm symmetric distributions. Building upon their results, we introduce a class of multivariate Markov processes that we call ‘Archimedean survival processes’ (ASPs). An ASP is defined over a finite time interval, is equivalent in law to a vector of independent gamma processes, and its terminal value has an Archimedean survival copula. There exists a bijection from the class of ASPs to the class of Archimedean copulas. We provide various characterisations of ASPs, and a generalisation.

keywords:

Archimedean copula, gamma process, gamma bridge, multivariate Liouville distribution1 Introduction

The use of copulas has become commonplace for dependence modelling in finance, insurance, and risk management (see, for example, Cherubini et al. [4], Frees and Valdez [6], and McNeil et al. [11]). From a modelling perspective, one of the attractive features of copulas is that they allow the fitting of one-dimensional marginal distributions to be performed separately from the fitting of cross-sectional dependence.

The Archimedean copulas—a subclass of copulas—have received particular attention in the literature for both their tractability and practical convenience (see, for example, Genest and MacKay [7, 8] and Nelsen [14, chap. 4]). We introduce a family of multivariate stochastic processes that we call Archimedean survival processes (ASPs). ASPs are constructed in such a way that they are naturally linked to Archimedean copulas. An ASP is defined over a finite time horizon, and its terminal value has a multivariate -norm symmetric distribution. This implies that the terminal value of an ASP has an Archimedean survival copula. Indeed, there is a bijection from the class of Archimedean copulas to the class of ASPs.

Norberg [15] suggested using a randomly-scaled gamma bridge (also called a Dirichlet process) for modelling the cumulative payments made on insurance claims (see also Brody et al. [3]). Such a process can be constructed as , where is a positive random variable independent of a gamma bridge satisfying and , for some . This is an increasing process and so lends itself to the modelling of cumulative gains or losses; in this case the random variable represents the total, final gain. We can interpret as a signal and the gamma bridge as independent multiplicative noise. The process can be considered to be a gamma process conditioned so that has the law of , and so belongs to the class of Lévy random bridges (see Hoyle et al. [10]). As such, we call the process a ‘gamma random bridge’ (GRB).

ASPs are an -dimensional extension of gamma random bridges. Each one-dimensional marginal process of an ASP is a GRB. We shall construct each by splitting a ‘master’ GRB into non-overlapping subprocesses. This method of splitting a Lévy random bridge into subprocesses (which are themselves Lévy random bridges) was used by Hoyle et al. [9] to develop a bivariate insurance reserving model based on random bridges of the stable-1/2 subordinator. A remarkable feature of the proposed construction is that the terminal vector has a multivariate -norm symmetric distribution, and hence an Archimedean survival copula.

We shall also construct Liouville processes by splitting a GRB into pieces. By allowing more flexibility in the splitting mechanism and by employing some deterministic time changes, a broader range of behaviour can be achieved by Liouville processes than ASPs. For example, the one-dimensional marginal processes of a Liouville process are in general not identical in law.

A direct application of ASPs and Liouville processes is to the modelling of multivariate cumulative gain (or loss) processes. Consider, for example, an insurance company that underwrites several lines of motor business (such as personal motor, fleet motor or private-hire vehicles) for a given accident year. A substantial payment made on one line of business is unlikely to coincide with a substantial payment made on another line of business (e.g. a large payment is unlikely to be made on a personal motor claim at the same time as a large payment is made on a fleet motor claim). However, the total sums of claims arising from the lines of business will depend on certain common factors such as prolonged periods of adverse weather or the quality of the underwriting process at the company. Such common factors will produce dependence across the lines. An ASP or a Liouville process might be a suitable model for the cumulative paid-claims processes of the lines of motor business. The one-dimensional marginal processes of a Liouville process are increasing and do not exhibit simultaneous large jumps, but they can display strong correlation.

ASPs can be used to interpolate a dependence structure when using Archimedean copulas in discrete-time models. Consider a risk model where the marginal distributions of the returns on assets are fitted for the future dates . An Archimedean copula is used to model the dependence of the returns to time . At this stage we have a model for the joint distribution of returns to time , but we have only the one-dimensional marginal distributions at the intertemporal times . The problem then is to choose copulas to complete the joint distributions of the returns to the times in a way that is consistent with the time- joint distribution. For each time , this can be achieved by using the time- survival copula implied by the ASP with survival copula at terminal time .

This paper is organized as follows: In Section 2, we review multivariate -norm symmetric distributions, multivariate Liouville distributions, Archimedean copulas and gamma random bridges. In Section 3, we define ASPs and provide various characterisations of their law. We detail how to construct a multivariate process such that each one-dimensional marginal is uniformly distributed. An application is then given where an ASP is used to solve an Archimedean copula interpolation problem. In Section 4, we generalise ASPs to Liouville processes. We apply Liouville processes to the intraday forecasting of realized variance. In Section 5, we state our conclusions.

2 Preliminaries

We fix a probability space and assume that all processes under consideration are càdlàg, and all filtrations are right-continuous. We let denote the generalised inverse of a monotonic function . Thus, if is decreasing then . We denote the norm of a vector by , i.e. .

We present some definitions and results from the theory of multivariate distributions and refer the reader to Fang et al. [5] for further details.

Let be a vector of independent random variables such that is a gamma random variable with shape parameter and unit scale parameter. Then the random vector has a Dirichlet distribution with parameter vector . In two dimensions, a Dirichlet random variable can be written as , where is a beta random variable. If all the elements of the parameter vector are identical, then is said to have a symmetric Dirichlet distribution.

A random variable taking values in has a multivariate Liouville distribution if , for a random variable, and a Dirichlet random variable, independent of , with parameter vector . We call the law of the generating law and the parameter vector of the distribution. In the case where is positive and has a density , the density of exists and can be written as

| (1) |

for , where is the gamma function [1, 6.1]. In the case , has a multivariate -norm symmetric distribution. A multivariate -norm symmetric distribution is characterised by its generating law.

McNeil and Nešlehová [12] give an account of how Archimedean copulas coincide with survival copulas of -norm symmetric distributions which have no point-mass at the origin. Then in [13], McNeil and Nešlehová generalise Archimedean copulas to so-called Liouville copulas, which are defined as the survival copulas of multivariate Liouville distributions.

A copula is a distribution function on the unit hypercube with the added property that each one-dimensional marginal distribution is uniform. Archimedean copulas are copulas that take a particular functional form. The following definition given in [12] is convenient for the present work: A decreasing and continuous function which satisfies the conditions and , and is strictly decreasing on is called an Archimedean generator. An -dimensional copula is called an Archimedean copula if it permits the representation

for some Archimedean generator with inverse , where we set and .

If has an -variate -norm symmetric distribution with generating law and , then has an Archimedean survival copula with generator

| (2) |

McNeil and Nešlehová [12] showed that the converse is also true: If has an -dimensional Archimedean copula with generator , then has a multivariate -norm distribution with survival copula and generating law given by

| (3) |

where is the th derivative of , and is the right-hand sided derivative of order .

A gamma random bridge is an increasing stochastic process, and both the gamma process and gamma bridge are special cases. A gamma process is a subordinator (an increasing Lévy process) with gamma distributed increments (see, for example, Sato [16]). The law of a gamma process is uniquely determined by its mean and variance at time 1, which are both positive. Let be a gamma process with mean and variance at time 1; then , and . The density of is .

A gamma bridge is a gamma process conditioned to have a fixed value at a fixed future time. A gamma bridge is a Lévy bridge, and hence a Markov process. Let be a gamma bridge identical in law to the gamma process pinned to the value 1 at time . The transition law of is given by

| (4) |

for and . Here is the beta function [1, 6.2]. We say that is the activity parameter of . If the gamma bridge has reached the value at time , then it must yet travel a distance over the time period . Equation (4) shows that the proportion of this distance that the gamma bridge will cover over is a random variable with a beta distribution.

It is a property of gamma processes that the renormalised process is independent of . This leads to the remarkable identity , which we refer to as the ratio property of the gamma bridge. It follows that the joint distribution of increments of a gamma bridge is Dirichlet.

Definition 2.1.

The process is a gamma random bridge (GRB) if

| (5) |

for a random variable, and a gamma bridge independent of . We say that has generating law and activity parameter , where of is the law of and is the activity parameter of .

Suppose that is a GRB satisfying (5). If for some , then is a gamma bridge. If is gamma random variable with shape parameter and scale parameter , then is a gamma process such that and , for .

GRBs fall within the class of Lévy random bridges described in [10]. The process is a Markov process with stationary increments, and is identical in law to a gamma process defined over conditioned to have the law of at time . The bridges of a GRB are gamma bridges. Since increments of a gamma bridge have a Dirichlet distribution, it follows that the increments of a GRB have a multivariate Liouville distribution.

Define the subprocesses , , by

where the intervals , , are non-overlapping except possibly at the endpoints. It follows from [10, Corollary 3.12] that each is a GRB with generating law

Furthermore, we can construct an -dimensional Markov process by setting .

3 Archimedean survival process

We construct an ASP by splitting a gamma random bridge into non-overlapping subprocesses. We start with a ‘master’ GRB with activity parameter and generating law , where , . In this section, we write for the gamma density with shape parameter unity and scale parameter unity. That is .

Definition 3.2.

The process is an -dimensional Archimedean survival process if

where is a gamma random bridge with activity parameter . We say that the generating law of is the generating law of .

Note that from Definition 2.1 , and so . Each one-dimensional marginal process of an ASP is a subprocess of a GRB, and hence a GRB. Thus ASPs are a multivariate generalisation of GRBs. We defined ASPs over the time interval ; it is straightforward to restate the definition to cover an arbitrary closed interval.

Proposition 3.3.

The terminal value of an ASP has an Archimedean survival copula.

Proof.

Let be an -dimensional ASP with generating law . Then we have

for , where is a random variable with law and is a gamma process, independent of , such that has density . Each increment has an exponential distribution (with unit rate). Thus , for an -vector of independent, identically-distributed, exponential random variables. Hence has a multivariate -norm symmetric distribution. Therefore, it has an Archimedean survival copula. ∎

Remark 3.4.

Let be strictly decreasing for , and let be an ASP. Then the vector-valued process has an Archimedean copula at time .

3.1 Characterisations

In this subsection we shall characterize ASPs first through their finite-dimensional distributions, and then through their transition probabilities.

We shall show that the joint distribution of increments of an ASP are multivariate Liouville. To this end, we first show that the joint distribution of increments of a GRB are multivariate Liouville. The finite-dimensional distributions of the master process are given by

where , for all , all partitions , all , and all . It was mentioned earlier that the bridges of a GRB are gamma bridges. Hence, for a gamma process such that and , we have

Using the ratio property of the gamma bridge and (5), we have

Hence has a multivariate Liouville distribution with generating law and parameter vector .

We can use these results to characterise the law of the ASP through the joint distribution of its increments. Fix and the partitions , for . Then define the non-overlapping increments by , for and . The distribution of the -element vector characterises the finite-dimensional distributions of the ASP . Thus it follows from the Kolmogorov extension theorem that the distribution of characterises the law of . Note that contains non-overlapping increments of the master GRB such that . Hence has a multivariate Liouville distribution with parameter vector , and the generating law .

We denote the filtration generated by by . Then is a Markov process with respect to .

For a set and a constant , we write for the shifted set . We define the process by setting

Note that the terminal value of is the terminal value of the master process , i.e. . We define a family of unnormalised measures, indexed by and , as follows: and

for . We also write .

Proposition 3.5.

The ASP is a Markov process with the transition law given by

| (6) |

and

| (7) |

where , , and .

Proof.

We begin by verifying (6). From the Bayes theorem we have

| (8) |

From [10, Section 3.2] we have

| (9) |

The law of is ; hence using (9) the numerator of (8) is

| (10) |

and the denominator is

| (11) | ||||

| (12) |

In (10) we have used the fact that, given , is a vector of subprocesses of a gamma bridge. Equation (11) follows from the stationary increments property of GRBs and (12) follows from (9). Dividing (10) by (12) yields the claim.

Remark 3.6.

When the generating law admits a density , (8) is equivalent to

| (15) |

3.1.1 Increments of ASPs

We shall show that increments of an ASP have -dimensional Liouville distributions. Indeed, at time , the increment , , has a multivariate Liouville distribution with a generating law that can be expressed in terms of the -conditional law of the norm variable . Before we show this, we first examine the law of the process .

We define the measure , , by

Proposition 3.7.

The process is a GRB with generating law and activity parameter . That is,

| (16) | ||||

| and | ||||

| (17) | ||||

for .

After simplification, (16) and (17) are consistent with the transition probabilities given for a GRB in [10, Section 3.4].

Proof.

Note that for . This is not surprising since is a GRB, and hence a Markov process with respect to its natural filtration.

When admits a density, we denote it by . We see from (16) that exists for . It follows from the definition of that only exists if admits a density.

Proposition 3.8.

Fix . Given , the increment , , has an -variate Liouville distribution with generating law

| (18) |

and parameter vector .

Proof.

Consider the case when admits a density . In this case the density exists. From (15) and (17), we have

| (19) |

Comparing (19) to (1) shows it to be the law of Liouville distribution with generating law and parameter vector , as required.

The case when is similar since the density exists.

For the final case where and has no density we only outline the proof since the details are far from illuminating. Given , the law of is characterised by (6). We then need to show that this law is equal to the law of , where is a random variable with law given by (18), and is a Dirichlet random variable, independent of , with parameter vector . This is possible by mixing a Dirichlet density with the random scale parameter .

∎

3.2 Moments

In this subsection we fix a time , and we assume that the first two moments of exist and are finite.

Proposition 3.9.

The first- and second-order moments of , , are

| (a) | |||

| (b) | |||

| (c) |

where

Proof.

Fix . From Proposition 3.8, given , the increment has an -dimensional Liouville distribution with generating law , and with parameter vector . Defining

| and | ||||

the equations (a)-(c) in the statement of the proposition hold from [5, Theorem 6.3].

It remains to simplify the expressions for and . For this we use two results about Lévy random bridges. First, from [10, Corollary 3.10] we can write

The expression for then follows directly. Second, given , the process is a GRB with generating law and activity parameter [10, Section 3.7]. Hence, given ,

where is a random variable with law , and is a gamma bridge with activity parameter , independent of , satisfying and . Note that , , is a beta random variable with parameters and . Thus

∎

3.3 Measure change

In this section we show that is a positive martingale with respect to the filtration . Through , we are able to define a new measure under which the ASP is a vector of independent gamma processes.

Fix . Then we have

Noting that , we see that is a Radon-Nikodym derivative process. Hence we can define a probability measure by

Proposition 3.10.

Under , is a vector of independent gamma processes such that

for .

Proof.

Since is Markov under , it suffices to verify that the transition law of is that of a vector of independent gamma processes. For , we have

∎

3.4 Independent gamma bridges representation

The increments of an -dimensional ASP are identical in law to a positive random variable multiplied by the Hadamard product of an -dimensional Dirichlet random variable and a vector of independent gamma bridges. For notational convenience, in this subsection we denote a gamma bridge defined over as (instead of ).

For vectors , we denote their Hadamard product as . That is,

Proposition 3.11.

Given the value of , the ASP satisfies the following identity in law:

where

-

1.

is a symmetric Dirichlet random variable with parameter vector ;

-

2.

is a vector of independent gamma bridges, each with activity parameter , starting at the value 0 at time , and terminating with unit value at time 1;

-

3.

is a random variable with law given by

-

4.

, , and are mutually independent.

Proof.

Fix and the partition , for . Then define the non-overlapping increments and the vectors and in a similar way to Section 3.1. The distribution of characterises the finite-dimensional distributions, and hence the law, of the process . Note that are non-overlapping increments of the master GRB . Thus, given , has a multivariate Liouville distribution with parameter vector and generating law , for . It follows from [5, Theorem 6.9] that

where (i) has law , (ii) has a Dirichlet distribution with parameter vector , (iii) has a Dirichlet distribution with parameter vector , (iv) , , and are mutually independent.

Let be a gamma bridge with activity parameter such that and . Then the increment vector

| (20) |

has a Dirichlet distribution with parameter vector . Hence the increment vector (20) is identical in law to . From the Kolmogorov extension theorem, this identity characterises the law of . It follows that

which completes the proof. ∎

3.5 Uniform process

We construct a multivariate process from the ASP such that each one-dimensional marginal is uniformly distributed for each .

Fix a time . Each is a scale-mixed beta random variable with survival function

where is the regularized incomplete Beta function [1, 6.6]. The random variables , , are then uniformly distributed.

We now define a process by

By construction, each one-dimensional marginal is uniform for .

3.6 Application

We give an example of how an ASP can be used in a copula-interpolation problem. Consider an -period model where is a vector of uniform random variables for . Suppose that has an Archimedean copula with generator . Given no further information, how might one simulate the vector , , or in a reasonable way? The solution we propose is to assume that

where is an -dimensional ASP with the generating law found by substituting into (3). Simulating a sample path of an ASP is straightforward if one can generate variates from its generating law. Simulating is then a matter of numerically evaluating the survival function .

In a financial setting, this method could be applied to risk modelling. Let be the cumulative log-returns of assets over the next days. Suppose that we wish to simulate , for each , in order to calculate some risk measure (e.g. value-at-risk). Assume that we have estimated the distribution function of each one-dimensional marginal (with sufficient historical data, this is usually straightforward). Assume further that the Archimedean copula with generator provides an adequate fit to historical observations of . We can then jointly simulate by simulating and setting . Using the ASP in this way imposes a significant amount of structure on the copula of . Indeed, we have exactly one functional degree of freedom, the choice of . This structure may be unnecessarily rigid when data and computational time are abundant. However, in situations where cross-sectional (and temporal) relationships are uncertain, this structure may provide welcome parsimony; and in situations where resources are scarce, reducing the problem of fitting the copula of to fitting the copula of may save valuable labour.

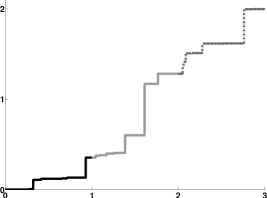

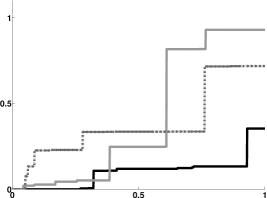

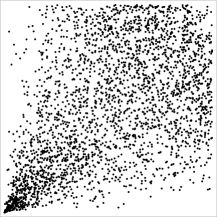

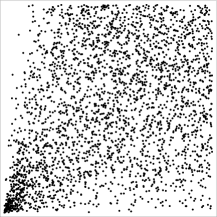

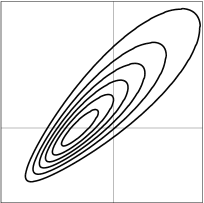

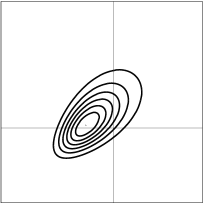

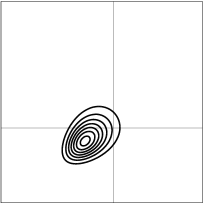

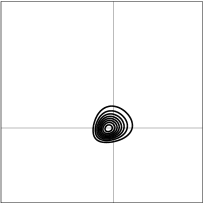

In Figure 2 we show some simulations of when , , and

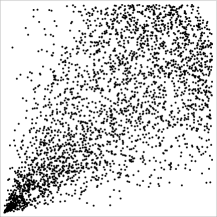

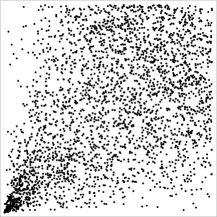

for and constant and . From (2), we see that in this case the generating law of is inverse Gaussian. In Figure 3 we demonstrate some of the temporal dependencies in .

4 Liouville process

We generalise ASPs to a family of stochastic processes that we call Liouville processes. A Liouville process is a Markov process whose increments have multivariate Liouville distributions. Liouville processes display a broader range of dynamics than ASPs. The one-dimensional marginal processes of a Liouville process are in general not identical. This generalisation comes at the expense of losing the direct connection to Archimedean copulas. However, in the language of McNeil and Nešlehová [13], the terminal value of a Liouville process has a Liouville copula; that is, the survival copula of the terminal value is the survival copula of a multivariate Liouville distribution.

We provide the transition law, moments and an independent gamma bridge representation of a Liouville process. Proofs are omitted since they are similar to the proofs in Section 3.

Definition 4.12.

Fix , , and the vector satisfying , . Define the strictly increasing sequence by and , . Then a process satisfying

for a GRB with activity parameter , is an -dimensional Liouville process. We say that the generating law of is the generating law of and the activity parameter of is .

Note that allowing the activity parameter of the master process to differ from unity in Definition 4.12 would not broaden the class of processes. Indeed, changing the activity parameter of the master process would be equivalent to multiplying the vector by a scale factor.

We define a family of unnormalised measures, indexed by and , by

for where . Again we write and . The process is a GRB with activity parameter . Given , the law of is , and law of is

for . Then the Liouville process is a Markov process with the transition law given by

and

where , , and .

Similar to an ASP, the joint distribution of the increments of a Liouville process are multivariate Liouville. In particular, given and , the increment has a Liouville distribution with the generating law , , and parameter vector . From this we find that, for fixed , the first- and second-order moments of , are

where

The law of the increments of an -dimensional Liouville process can be characterised by a positive random variable multiplied by the Hadamard product of an -dimensional Dirichlet random variable and a vector of independent gamma bridges. In particular, given the value of , satisfies the following identity in law:

where (a) has a Dirichlet distribution with parameter vector ; (b) is a vector of independent gamma bridges, such that the th marginal process is a gamma bridge with activity parameter , starting at the value 0 at time , and terminating with unit value at time 1; (c) is a random variable with law , ; (d) , , and are mutually independent.

4.1 Application

In financial markets, volatility estimates play an important role in both trading and risk management. Volatility is unobserved and there is a large body of literature covering its measurement and forecasting (see, for example, Andersen et al. [2]). One method of circumventing the intangible nature of volatility is to consider realized volatility, or equivalently realized variance (RV). For a given time period (usually one trading day) the RV of an asset is defined as

where are the prices of the asset taken at regular intervals throughout the time period (e.g. every five minutes). Realized volatility is then defined as .

In this application, we model the intraday accumulation of two stock-index RVs using a Liouville process. A day trader may wish to trade DAX and FTSE futures as a pair in the afternoon, based on some price divergence during the morning. In order to size the trade appropriately and to manage risk, measures of volatilities for the futures may be required. Currently, it is common for volatilities to be forecast using information up to the previous day’s close-of-business. However, the proposed model can further incorporate the morning’s price movements for an updated, and potentially superior, joint forecast of the afternoon’s futures volatilities. The methods outlined here can be adapted to the modelling of other cumulative phenomena, such as insurance claims as described in Section 1.

We define a process taking values in by , , where is a Liouville process with activity parameter , and the deterministic time-change function is continuous, increasing, and satisfies and . Thus is a time-changed Liouville process. The time change is employed to capture any intraday seasonality observed in market volatility.

We fix a trading day and assume that satisfies

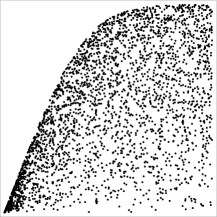

for , , where and are the intraday prices of FTSE and DAX futures, respectively. Thus and are the start and the end of the trading day, and is a vector of the day’s FTSE and DAX RVs. See Figure 4 for a sample path of the accumulation of FTSE and DAX RV during a trading day.

Before the start of the trading day, we can use a time-series model, fitted to historical data, to provide the generating law of the Liouville process. The generating law is the law of the sum of the day’s FTSE and DAX RV.

We define

then the vector has a Dirichlet distribution with parameter vector , where , for and . Once we have the generating law, it remains to estimate the activity parameter , and the time-change increments and . Using historical intraday prices, these can be jointly fitted using maximum likelihood estimation or moment matching. This two-stage fitting of the distributions of and is natural since they are independent.

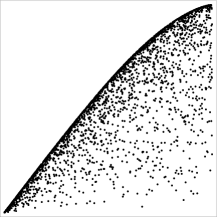

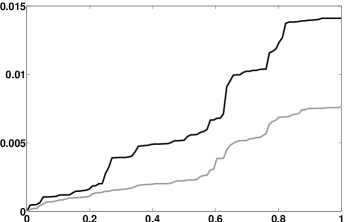

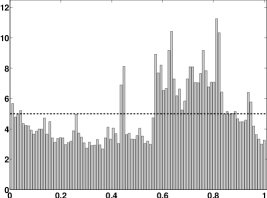

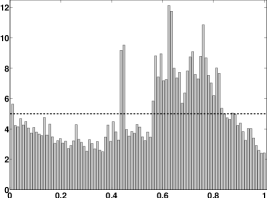

To demonstrate the feasibility of this approach, we implemented the model using five-minute prices of FTSE and DAX futures contracts. We fixed the market opening time () at 9am (GMT) and the market closing time () at 5pm (GMT). We used the auto-regressive fractionally-integrated model described in [2] to construct a log-normal generating law. The values of and were fitted by moment matching. An increase in the volatility of FTSE and DAX futures in the European afternoon can be observed in these values coinciding with the opening of financial markets in the US (see Figure 5). Given the values of and , we fitted the activity parameter by maximum likelihood estimation. This value implies that the observed dynamics differ significantly from those of an ASP. In particular, large values for the activity parameter imply that the observed trajectories increase gradually, exhibiting few large jumps. This is in contrast to the trajectories of an ASP which increase little between frequent large jumps (cf. Figure 1). We used the fitted model to update the joint density of FTSE and DAX RV at various times during a trading day. As time passes, the joint density converges to a delta function at the actual values of the day’s RVs (see Figure 6).

5 Conclusion

Through ASPs, we have presented an avenue to extend the theory and application of Archimedean copulas in multi-period and continuous-time frameworks. Liouville processes are similarly useful in extending Liouville distributions and Liouville copulas. We have also shown that Liouville processes are a natural multivariate extension of GRBs, and thus are a flexible tool in the modelling of cumulative processes.

Acknowledgements

The authors are grateful to two anonymous referees whose comments led to significant improvement in this paper.

References

- Abramowitz and Stegun [1964] M. Abramowitz, I.A. Stegun, Handbook of mathematical functions with formulas, graphs, and mathematical tables, Dover, New York, 1964.

- Andersen et al. [2003] T.G. Andersen, T. Bollerslev, F.X. Diebold, P. Labys, Modeling and forecasting realized volatility, Econometrica 71 (2003) 579–625.

- Brody et al. [2008] D.C. Brody, L.P. Hughston, A. Macrina, Dam rain and cumulative gain, Proceedings of the Royal Society A 464 (2008) 1801–1822.

- Cherubini et al. [2004] U. Cherubini, E. Luciano, W. Vecchiato, Copula methods in finance, Wiley, Chichester, 2004.

- Fang et al. [1990] K.-T. Fang, S. Kotz, K.W. Ng, Symmetric Multivariate and Related Distributions, Chapman & Hall, New York, 1990.

- Frees and Valdez [1998] E.W. Frees, E.A. Valdez, Understanding relationships using copulas, North American Acturial Journal 2 (1998) 1–25.

- Genest and MacKay [1986a] C. Genest, J. MacKay, Copules archimédiennes et familles de lois bidimensionnelles dont les marges sont données, The Canadian Journal of Statistics 14 (1986a) 145–159.

- Genest and MacKay [1986b] C. Genest, J. MacKay, The joy of copulas: Bivariate distributions with uniform marginals, The American Statistician 40 (1986b) 280–283.

- Hoyle et al. [2010] E. Hoyle, L.P. Hughston, A. Macrina, Stable-1/2 bridges and insurance: a Bayesian approach to non-life reserving, arXiv:1005.0496 (2010).

- Hoyle et al. [2011] E. Hoyle, L.P. Hughston, A. Macrina, Lévy random bridges and the modelling of financial information, Stochastic Processes and their Applications 121 (2011) 856–884.

- McNeil et al. [2005] A.J. McNeil, R. Frey, P. Embrechts, Quantitative Risk Management, Princeton University Press, 2005.

- McNeil and Nešlehová [2009] A.J. McNeil, J. Nešlehová, Multivariate Archimedean copulas, -monotone functions and -norm symmetric distributions, Annals of Statistics 37 (2009) 3059–3097.

- McNeil and Nešlehová [2010] A.J. McNeil, J. Nešlehová, From Archimedean to Liouville copulas, Journal of Multivariate Analysis 101 (2010) 1772–1790.

- Nelsen [1999] R.B. Nelsen, An Introduction to Copulas, Springer, New York, 1999.

- Norberg [1999] R. Norberg, Prediction of outstanding liabilities II: model variations and extensions, ASTIN Bulletin 29 (1999) 5–25.

- Sato [1999] K. Sato, Lévy processes and infintely divisible distributions, Cambridge Univeristy Press, Cambridge, 1999.