Multiplicative noise, fast convolution, and pricing

Abstract

In this work we detail the application of a fast convolution algorithm computing high dimensional integrals to the context of multiplicative noise stochastic processes. The algorithm provides a numerical solution to the problem of characterizing conditional probability density functions at arbitrary time, and we applied it successfully to quadratic and piecewise linear diffusion processes. The ability in reproducing statistical features of financial return time series, such as thickness of the tails and scaling properties, makes this processes appealing for option pricing. Since exact analytical results are missing, we exploit the fast convolution as a numerical method alternative to the Monte Carlo simulation both in objective and risk neutral settings. In numerical sections we document how fast convolution outperforms Monte Carlo both in velocity and efficiency terms.

Scuola Normale Superiore, Piazza dei Cavalieri 7 Pisa I-56126, Italy

INFN, Sezione di Pavia, via Bassi 6 Pavia I-27100, Italy

Swiss Finance Institute at the University of Lugano, Via Buffi 13 Lugano, Switzerland

JEL codes: C63, G13.

Keywords: Computational Finance, Stochastic Processes, Non-Gaussian Option Pricing, Numerical Methods for Option Pricing.

1 Introduction

Two of the basic problems computational finance has to deal with are the choice of the optimal model driving the stochastic evolution of financial variables and, once a good candidate has been identified, the search of a reliable way for its fast and accurate simulation. The former issue has been widely investigated both by econometricians, mathematicians, and physicists, as demonstrated by the increasing literature on this topic, see for example [15, 29, 30, 13, 31]. Tracing back to the work of [28] and the analysis in [22], empirical studies have shown that financial time series exhibit features departing from the Gaussian assumption. In [17] a detailed review of the stylized empirical facts emerging in various type of financial markets is presented and discussed. These findings are nowadays accepted as universal evidences, shared among different markets in different epochs. From the earlier results on cotton prices of Mandelbrot or the thick tailed nature of the Dow Jones Industrial Average recognized by Fama, very heterogeneous models have been proposed in order to reproduce the degree of asymmetry and the excess of kurtosis of the empirical distributions. Approaches directly developing from distributional assumptions includes the truncated Lévy model discussed in [30], and those employing generalized Student- and exponential distributions, see [13, 32]. Different mechanisms also capturing the observed non trivial structure of higher order correlation functions model the stochastic nature of the return volatility. Continuous time approaches have been extensively analyzed and range from the fractional Brownian motion, [29], to stochastic volatility models, for a review we suggest [24]. Discrete time models include AutoRegressive Conditional Heteroskedastic (ARCH) and Generalized ARCH processes, [21, 5], and multifractal ones, [8], the latter being inspired by cascades originally introduced by Kolmogorov in the context of turbulent flows. Turbulent velocity flows have also led to a series of empirical works testing and strongly relying on the Markovian nature of foreign exchange returns, [25, 23]. The macroscopic description of the observed phenomena is provided in terms of a Fokker-Planck (FP) equation with linear drift and quadratic diffusion coefficients. Processes leading to an equation with the same structure characterize several physical systems, as reviewed in [11]. Also the statistical feedback mechanism proposed in [6, 7] can be recast in terms of non linear diffusion, as originally remarked by [33], who also pointed out potential problems arising when computing expectations under power law tailed distributions. Even though these drawbacks have been later amended in [38], [34] propose to switch to exponential tailed PDFs. In particular, they develop a general approach to generate a Markovian process obeying scaling relations starting from a driftless stochastic differential equation (SDE). In the current paper we focus on the numerical characterization of these latter processes, of the above mentioned quadratic diffusion ones, and in their application in financial modeling. To this respect, especially for pricing purposes, we need to reconstruct the conditional probability density function (PDF) describing the stochastic dynamics in order to evaluate expectations of future payoffs. Yet a closed form expression for the density is rarely available. For this reason several numerical procedures have been developed and have become the common practice, e.g. binomial and multinomial lattice algorithms, Monte Carlo (MC) simulation, and partial differential equation solvers (for a review see [14]). We decide to investigate and widely exploit the fast convolution algorithm (FCA) introduced in [20]. The algorithm applies to Markovian stochastic processes: the repeated application of the Chapman-Kolmogorov equation, and a clever problem re-formulation allow to rewrite functional integrals in terms of Fourier and anti-Fourier transforms of the state vector. Performing these operations via fast Fourier transform (FFT) algorithm, numerical efficiency is achieved and computational complexity is notably reduced.

The structure of the paper is the following. After introducing stochastic models we have chosen to investigate, we detail step by step FCA; in paragraph 2.2 we test its numerical performances against the standard MC approach for different specification of models and parameter values. Section 3 is dedicated to financial applications in the context of option pricing. In 3.1 we derive the risk neutral measure for the piecewise diffusion process of [32], and the exact formula for Plain Vanilla pricing. We then consider geometric Asian options by thoroughly develop the two dimensional setting required by fast convolution, see paragraph 3.2. We exploit the formal analogy between the latter case and the framework discussed by [38, 6, 7] to price Plain Vanilla options in paragraph 3.3, and in the final part we collect numerical distributions and implied volatility surfaces we have obtained to prove the reliability of FCA. We draw relevant conclusions and possible perspectives in section 4.

2 Stochastic processes with multiplicative noise

Multiplicative stochastic processes we investigate in this work correspond to the class of quadratic diffusion described in [11, 19] and of piecewise linear diffusion introduced in [32] and later on rediscussed by [1] in a slightly different flavour.

The SDE describing the quadratic diffusion dynamics under Itô prescription can be written as

| (1) |

with initial time condition; is the standard Brownian increment, and are non-negative smooth functions for . We require with . Equation (1) governs the dynamics of a variety of complex phenomena as reviewed in [11], where an exhaustive description of the process in terms of its moments is also provided. For instance, when is constant, it is possible to characterize analytically the time-scaling adjustment of the process , regulated by the choice of , and its convergence to the stationary state. If is non negative or if is time dependent, lacks stationarity; however, in the final section of this paper we will discuss an application of this latter case to the context of financial option pricing, tracing back to [6, 7], and later revised by [38].

The quadratic diffusion process (1) can be formally manipulated to reduce it in a more convenient form by means of the Lamperti transform, as we will see in Section 2.1. Here, we slightly simplify it introducing a new variable beating the time , which we will refer to as the integral time. In this new setting the process is described by the following dynamics

| (2) |

with and 111By virtue of the properties of , is a monotonously increasing function of , implying the well-definiteness of the inverse function ..

As far as piecewise linear diffusion is concerned, the main property we are interested in is scaling, relating returns over different sampling intervals. More precisely, whenever returns are rescaled by a factor , the shape of their distribution scales according to

| (3) |

where is the so called scaling function. Following [1], piecewise diffusion process can be defined by means of the driftless SDE

| (4) |

Through the analysis of the FP equation satisfied by , it can be readily shown that is the only value of consistent with the scaling assumption (3). In addition to this the FP equation admits the following solution

| (5) |

where and . The interest in previous density is twofold, both because of the emergence of a scaling exponent , in agreement with the empirical findings, and because of the evidence of leptokurtosis. [32, 31] derive closed-form option pricing formulae under the distribution (5); yet they show that consistency between scaling, exponential PDF and martingale option pricing requires the replacement of the Itô correction for under the risk neutral measure with a constant, see section 2 in [34]. We argue this approximation is questionable, and we want to perform option pricing not relying on it, therefore we need a numerical methodology whose efficiency and flexibility promise to compensate for the absence of closed-form solution.

2.1 Fast convolution algorithm

In this section we review the fast convolution algorithm proposed in [20].

Let us consider the generic process , whose dynamics is described by the following general SDE

We start by transforming the process into one with unitary diffusion coefficient. This is performed via the Lamperti transform, see section 1.11.4 in [26], defined as

Under suitable regularity condition Itô Lemma can be applied to and its dynamics turns out to be

| (6) |

with

where is the function evaluated in , and analogously for . Our aim is to provide an approximate expression for the transition probability density function 222From now on we will drop the explicit dependence on the time variable .. We introduce an equally spaced time grid , with , in a similar spirit to the path integral approach, see [18, 37, 12, 2]. The repeated use of the Chapman-Kolmogorov equation in this discrete setting allows to write the transition probability for a generic as a finite high dimensional integral

| (7) |

where , and is the short time transition PDF that we chose equal to the Normal density

By means of the new variables , the transition becomes symmetric under the exchange of with , i.e. . For each one dimensional integration appearing in equation (7), we have

| (8) |

where is the density evaluated in , and similarly for . If we introduce a numerical integration grid of equally spaced points for all and , where neither nor depend on the time label , then the PDF associated to transition of moving from point at time to point at time is function only of the difference , i.e. . The discrete matrix of transition probabilities

| (13) |

is therefore a symmetric Toeplitz matrix , with no dependence on the time variable. Letting

| (26) |

equation (8) can be approximated as

The entries of are computed by means of the linear interpolation operator

| (32) |

applied to . Similarly, equation (7) becomes

| (33) |

Matrix multiplications in previous equation are extremely time consuming. Indeed, while multiplying a -vector by the diagonal matrix requires operations, and analogously for the operator, multiplication of the matrix by a vector requires operations. On top of this, the procedure must be repeated at each time step. As a consequence, the dominant contribution grows as , and choosing a rather thick grid, computational times rapidly explodes. However, the multiplication of a Toeplitz matrix by a vector can be efficiently performed exploiting algorithms coming from digital signal processing. By embedding into a circulant matrix of dimensions

| (42) |

the product of with a generic vector is equal to the first components of , , . Every circulant matrix can be expressed as , where denotes conjugate transpose of , whose columns are for , and , with first row of the circulant matrix. Thanks to this result, the product can be performed exploiting fast Fourier transform (FFT) algorithm

where and are the FFT and anti-FFT operator, respectively, while is the component wise product. With the adoption of this approach, the computational time is noticeably reduced: each FFT computation requires operations. Finally, in order to compute equation (33) we need to repeat the algorithm at each time step, and on the whole the computational burden can be estimated to be of order , which is definitely a satisfactory improvement with respect to the non-FFT based procedure.

2.2 Fast convolution at work: numerical result

Equipped with FCA we are now ready to approach multiplicative processes previously described. We want to check that numerical results obtained by fast convolution converge to the analytical solution, when available, or to the PDF reconstructed by means of MC simulation. Moreover, we show that FCA provides an estimate of the distribution shape even in those low probability regions, such as the tails, which are inefficiently sampled by MC approach.

Lamperti transform for process (2) can be explicitly computed as

| (43) |

with , and .

The related drift function is

where , and the prime is a shorthand for the derivative w.r.t .

The first and simplest case we want to consider corresponds to the SDE (2) with time independent parameter , , and negative . Whenever this conditions are satisfied, the process converges exponentially to the stationary regime with a typical relaxation time given by . Following [3] the stationary PDF can be computed in closed-form expression as

| (44) |

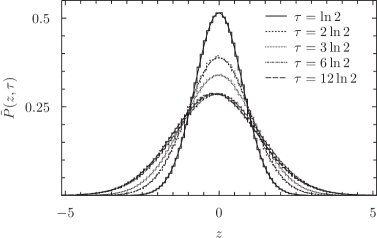

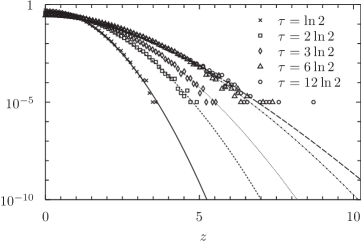

with , and the inverse tangent function continues smoothly at . For illustrative purposes we fix the five free parameters as , , and , while the choice of and is at the moment irrelevant since we work directly with time . As evident from equation (44) all moments of order higher than or equal to diverge: being , only the first nine lowest moments converge. In figure 1a we plot the time evolution of for increasing values of as obtained by means of FCA (, , , and ). For we also plot the histogram corresponding to MC simulation of the discrete process (parameter of the Euler scheme approximation: , and number of MC paths ), while the solid line represents the analytical solution easily derived from equation (44). In figure 1b we show the same results in log-linear scale to emphasize the tail region. The analytical information provides an overall check that the algorithm converges to the correct distribution, however far from stationary regime we have no precise information about the PDF shape. In [11] the scaling of the convergent moments is computed analytically, but it is known that the knowledge of the moments does not allow for a univocal reconstruction of the complete distribution. We can only rely on MC simulation, but sampling of low probability region requires on average a huge statistics (we need to explore a -probability region). At this point the advantages provided by the fast convolution based approach are evident, as clearly shown by both panels. FCA curve for is in perfect agreement with the analytical prediction, both in central and tail regions. MC histograms agree as well, but these results are extremely noisy and very inaccurate for . FCA based results are even more impressive looking at the computational time. Performances are strongly machine dependent, and for this reason we do not quote absolute times, but measured relative values: to obtain bars MC takes ten times more than FCA333Random numbers generators and FFT algorithms are provided by GNU Scientific Library.. As a consequence it needs times more to reach the same accuracy at level.

Similar results are obtained for the slightly more complicated process used in [23] to model foreign exchange rate fluctuations. Their process is still mean reverting with , , , and , though in this case the last parameter has a non trivially time dependence, . Lacking stationarity, every analytical information on the PDF is lost, yet we can see from figures 2a and 2b how the numerical PDF evolves with time and we verify a striking matching between MC and FCA results. Remarks similar to previous case apply.

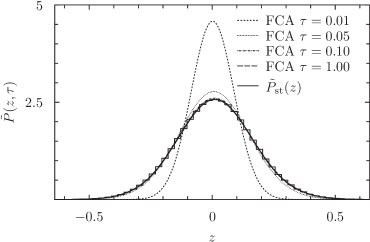

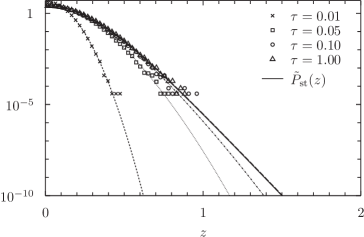

We now turn our attention to piecewise linear diffusion. The procedure is in this case a little bit subtle. While computation of the Lamperti transform of process (4) for and integral time is still feasible providing 444The sign function is defined according to the convention .

the stochastic differential cannot be computed applying Itô Lemma straightforwardly. As a function of and , lacks necessary regularity condition for and . However, both difficulties can be overcome. The process does not suffer any problem in , therefore we can evolve from to , and then exploit the one to one correspondence between and . Moving from to , remains delta distributed around zero, and the same holds true for . For the time derivative needed in can be readily computed. The difficulty arising with the computation of in zero can be dealt by replacing the absolute value with the smooth approximation

This allows us to compute

where in view of our application on a discrete grid the last approximation can be justified for sufficiently large .

We thus end with the following expression for the dynamics of

Numerical results concerning this last process are reported in figure 3a (linear scale) and in figure 3b (log-linear scale). We study the dependence of on . Indeed for , , and the value of the coefficient in the exponential function is crucial to asses the convergence of the expectation of with respect to . We fix , , and . The leptokurtosis of the PDF increases as far as the value of increases. Parameters for the Euler scheme approximation are fixed as in previous examples, while for the FCA we have slightly changed the value of and keeping . For each one of the three cases we also plot the analytical prediction, since for piecewise linear processes the solution is known in closed form. Also in this last case the agreement between analytical and fast convolution PDF is totally satisfactory, while limitations of the MC approach are evident from symbols depicted in Panel (b).

3 Financial applications

In the second part of this work we present and discuss how results achieved in previous sessions can be exploited in finance, and in particular in the context of option pricing. For both quadratic and piecewise diffusion we briefly review how to set the correct risk neutral framework. Then, for explanatory purposes, we apply FCA to price European Plain Vanilla and geometric Asian options, but the approach can be extended to deal with different payoffs and different kind of boundary conditions. For the remaining of this paper, is the logarithmic return obtained from the stochastic process describing the evolution of an asset price. As asset candidates we only consider equities and foreign exchange rates.

3.1 Piecewise diffusion under risk-neutrality: Plain Vanilla pricing

According to risk neutral valuation theory we need to find the dynamics of or, equivalently, under the probability measure which makes all discounted asset prices martingales. Whenever the Novikov condition for the process under consideration is verified, Girsanov theorem gives the recipe for the equivalent measure, and it also explains how the dynamics of coherently modifies. However, [32, 34] show how to compute the desired martingale directly from the Green function solving the FP equation associated to the dynamics

| (45) |

with . Just in the case of the original model of [4, 35], a delta hedged strategy allows to construct a locally risk neutral portfolio and to derive the partial differential equation

| (46) |

that is to be use to solve the pricing problem of a Plain Vanilla option , with risk free interest rate and for suitable boundary conditions. Introducing and substituting in equation (46), it is readily verified that the hat price satisfies an equation formally identical to the backward time FP equation associated with the dynamics (45) with . The fair price of a call option is therefore predicted to be

where is the Green function solving the FP equation in the risk neutral framework, and is the strike price. The dynamics of under the new probability measure reads

| (47) |

At variance with equation (4), a non trivial drift term appears and some comments are mandatory. As recognized by McCauley and collaborators, whenever the drift depends explicitly on there is no way to preserve scaling properties. However, in order to exploit the analytical information provided by equation (5), corresponding to the Green function for the process (4), they provide arguable arguments in order to replace the drift with a constant. We are instead equipped with a computationally efficient algorithm, and so we can get rid of this approximation and price options directly with the process (47). As in section 2, we switch to integral time

and compute the Call option price as

| (48) |

with , discounted price and log-moneyness . The vector of transition probability between and under the risk neutral measure has to be computed with the fast convolution procedure described in section 2.1.

3.2 Exotic options: the geometric Asian case

Formula (48) can be extended to deal with payoffs with different dependence on , e.g. digital options, covered call or strongly non linear function , the only constraint being . The case of a functional payoff depending multiplicatively on the price along the path, i.e. , is just slightly more complicated but in fact can be easily managed, see [16] for an application to bond pricing. In this section we address the problem of pricing a geometric Asian option, which requires to compute the expected value

| (49) |

Being the positive part function non linear, previous expression is quite tricky to be evaluated and requires some careful manipulations. Defining , the Asian price is given by

| (50) |

We exploit the discretization of the time interval in equally spaced intervals of amplitude , and we replace the integral expression with a finite sum . We then introduce the ancillary variables satisfying the following recursive relation

| (51) |

for and . Exploiting the one to one correspondence between and , it is possible to rewrite the Asian price as

with . The only unknown quantity in previous expression is the joint distribution of and , whose computation requires a recursive relation allowing to propagate to with the associated initial time condition . The following equation holds

| (52) |

and to proceed it is useful to explicit the dependence of on in equation (51)

| (53) |

where is coupled with the dummy variable . From previous relations we have

| (54) |

where the Jacobian is equal to . Therefore starting from the distribution , and following the above procedure, after steps we obtain the desired . Introducing -node grid for and -node grid for , we can approximate the distribution with a matrix , the row index running over the nodes of , the column index over those of . The Asian price can therefore be approximated by

Since the time evolution corresponding to equation (52) is the most computationally intensive operation implicit in previous approximation, we can perform it at each node by means of FCA. The overall numerical complexity of the algorithm is essentially linear in the total number of grid nodes, i.e .

3.3 The Vellekoop-Nieuwenhuis-Borland model

The geometric Asian case just described is useful also in view of the last application we present, which is related to the model for the stock price dynamics introduced in [6, 7]. Borland model tries to generalize the standard Black&Scholes to account for the empirical evidences of fat tailed return distributions, still keeping a closed form formula for the price of Plain Vanilla instruments. It is a sort of hybrid between a stochastic volatility model and the standard Black&Scholes: the volatility is stochastic, but the stock price and the volatility itself are driven by the same Brownian motion. Despite its theoretical elegance, the model contains some weaknesses extensively analyzed in [38]. They raised two main objections by proving the Borland model to suffer arbitrage opportunities and diverging payoff expectation, as a consequence of the thickness of the tails. However, they preserved the main idea of the model and they amended it from both drawbacks. In their modified version they introduce the following dynamics

| (55) | ||||

| (56) |

with

| (57) |

with , , , and . In [38] the existence of a solution for equation (56) is proved, and it is shown how the unconditional distribution (i.e. for ) reduces to the generalized Student- distribution. In general the conditional distribution deviates from it. The log-return satisfies the equation

for . They verify that sufficient conditions hold for the applicability of the Girsanov theorem, and they derive the risk neutral dynamics

| (58) |

This last process does not suffer anymore of previous problems, however does not satisfy the Markov property, yet only jointly with . In addition, the price of Plain Vanilla instruments cannot be given in closed form formula. Indeed, according to pricing theory we have

and the expectation can only be computed via numerical techniques.

Given (57), we observe that the equation governing the evolution of belongs to the class of quadratic diffusion

processes (1) through the identifications , ,

, and .

Switching to the integral time for , and recalling equation (43), is readily computed

| (59) |

where . The price of a Plain Vanilla instrument can be computed as

| (60) |

with . Defining the set of ancillary variables satisfing the recursive relation

| (61) |

with , the formal analogy with the Asian case discussed in previous section is evident. Computation of the expectation in (60) requires estimation of the joint probability . The procedure is identical to the Asian case; equation (52) is still valid, while the system (53) has to be coherently modified in

The Jacobian in equation (54) simplifies to one, and, eventually, we can approximate the Plain Vanilla price as

where , and compute it by means of fast convolution.

3.4 Numerical results

In this final section we sum up numerical results for the financial applications described in paragraphs

3.1, 3.2, and 3.3.

Whenever we switch to the risk neutral measure for the piecewise linear process, corrections terms in the SDE appear and an

analytical expression for the density is not available anymore.

Numerical simulation is mandatory, and the FCA algorithm, being both faster and much more efficient, is a natural competitor to MC approach.

The transformed process is enriched by the risk neutral correction (the last but one term in squared brackets)

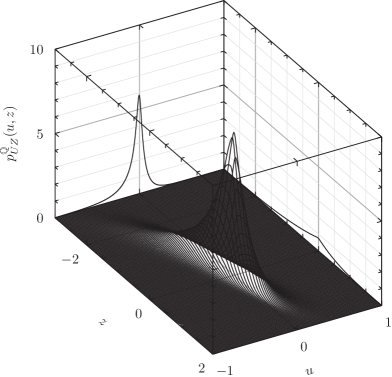

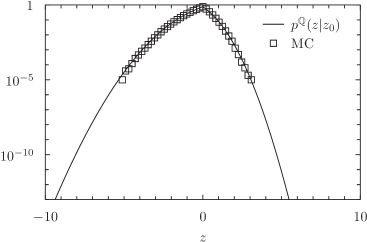

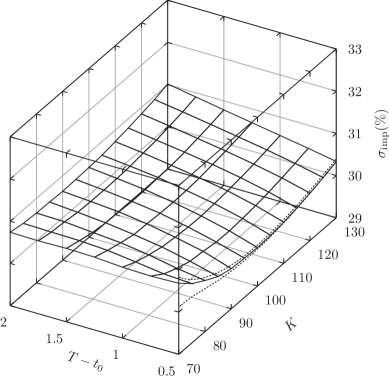

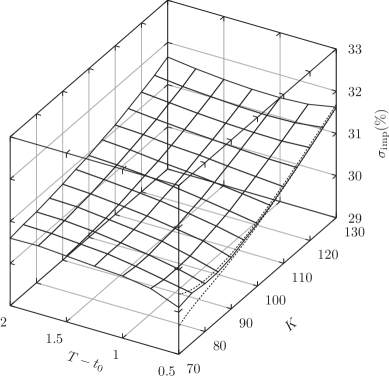

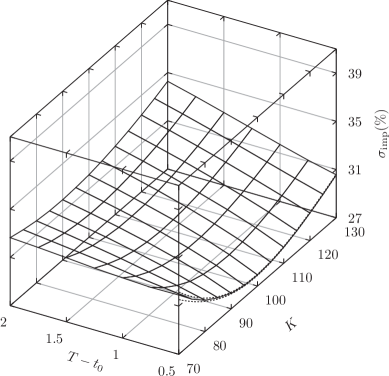

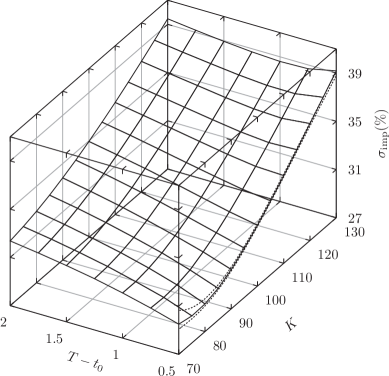

where is the risk free rate. In figures 4a and 4b we draw risk neutral PDFs for and remaining parameters as in figures 3a and 3b. The effect of the additional terms is evident from their comparison. In particular, it is remarkable the increase of the skewness induced by the risk neutral correction from linear plots in Panel (a). Turning our attention to the pricing of Asian options, Figure 5a plots the joint density , and associated marginals for , , , and . Parameters of the fast convolution are , , , , and . In figure 5b we compare the marginal PDF of , and analogously to paragraph 2.2 the agreement between FCA and MC is striking in the central region.

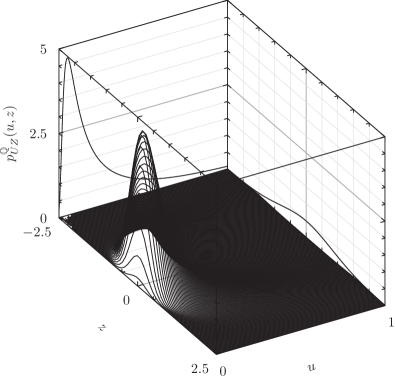

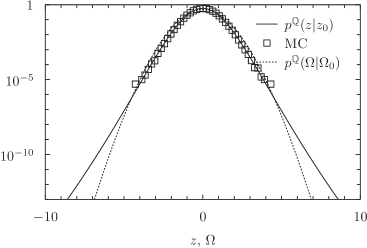

As far as the pricing under Vellekoop-Nieuwenhuis-Borland model is concerned, we start plotting in figure 6a the joint bivariate density for parameter values , , , , , , , , and . We notice that fast convolution algorithm correctly predicts a non negative support for the variable, even though the numerical grid spans uniformly the interval . In figure 6b we compare the distribution of obtained by means of FCA and MC, finding perfect matching, and we also plot PDF, easily derived given the relationship between the two variables, see equation (59). In light of the agreement between the two numerical procedures, we can use the FCA approach to efficiently price European Call options, as explained in paragraph 3.3. In this respect in figures 7a, 7b, 8a, and 8b we present our results in terms of implied Black-Scholes volatilities. Our choices of the parameters are , , , , , , , and . MC bands at Confidence Level are plotted as dashed lines for the shortest time to maturity, with . FCA and MC volatility curves are fully consistent. As expected surfaces exhibit a volatility smile, more pronounced for small maturities and for values deviating from zero. As already pointed out by Vellekoop and Niueuwenhuis, a wider variety of volatility surfaces and flexibility of the model can be obtained by playing with different values of .

4 Conclusions and perspectives

In this paper we have addressed the problem of investigating performances of the fast convolution algorithm introduced by [20]. Choosing different specifications of the stochastic process, this has been carried out both with the reconstruction of conditional probability densities at different time horizons and with the computation of prices of financial derivatives. FCA is an efficient grid algorithm relying on restating functional integrals as sequences of ordinary finite dimensional integrals, and on converting the stochastic process to a unitary diffusion one by means of the Lamperti transform. A bright formulation of the problem, then, allows those integrals to be evaluated efficiently by the use of fast Fourier transform techniques.

The stochastic processes we have investigated belongs to two classes of multiplicative noise processes: the family of quadratic diffusion, see [11, 19], and piecewise linear diffusions, see [32, 1]. The analysis performed in this work provides a natural complement to the analytical results obtained in [11], where closed form solutions for the stationary PDF and for the convergent moments at arbitrary time had been obtained. We have detailed a step by step numerical procedure able to provide an accurate estimate for the probability distribution of the process even far from the stationary regime. Similar results have been found for the piecewise diffusion. In this latter case, if the dynamics is enriched with a non trivial drift term, scaling properties are not preserved anymore and every analytical information is lost. Being this exactly the situation we faced when switching to the risk neutral setting, FCA proved to be a very efficient and reliable approach to the problem of option pricing. A detailed empirical analysis for different specifications of the parameter values documents the superiority of the FCA approach to standard Monte Carlo simulations. We have also demonstrated the flexibility of the approach when dealing with exotic instruments, and exploited the formal analogy between geometric Asian option pricing and Plain Vanilla pricing under Vellekoop-Nieuwenhuis-Borland dynamics. Being an interesting hybrid between a geometric Brownian motion and a stochastic volatility model, the latter provides a realistic description of the dynamics implied in the option market. FCA is able to numerically reproduce a rich variety of implied volatility surfaces improving the standard Monte Carlo approach.

Since, as documented, FCA turns out to be highly successful also in the case of the Vellekoop-Nieuwenhuis-Borland model, a natural perspective is to concentrate future research efforts on the extension of FCA to higher dimensional stochastic systems. This is precisely the case of continuous time stochastic volatility models, see [24]. These models provide a flexible framework when modeling volatility, and they allow to reproduce several observed statistical regularities. For this reason they are nowadays extensively exploited by quantitative sectors of banks and financial institutions. Given the ability of the fast convolution to reconstruct densities over tail regions, and of the investigated models to generate leptokurtic and scaling distributions, the present approach is naturally suited for application in the context of financial risk management, e.g. Value-at-Risk and coherent risk measures computation, see [27, 36, 10, 9].

Acknowledgements

The authors acknowledge the support of the Scuola Normale Superiore Grant ‘Giovani Ricercatori (2011/2012)’.

References

- [1] Alejandro-Quiñones, A. L., Bassler, K. E., Field, M., McCauley, J. L., Nicol, M., Timofeyev, I., Török, A. and Gunaratne, G. H., A theory of fluctuations in stock prices. Physica A, 2006, 363, 383–392.

- [2] Baaqui, B. E., Quantum Finance: Path Integrals and Hamiltonians for Options and Interest Rates, 2007 (Cambridge: Cambridge Univeristy Press).

- [3] Biró, T. S., and Jakovác, A., Power-Law tails from multiplicative noise. Phys. Rev. Lett., 2005, 94, 132302-1–4.

- [4] Black, F. , and Scholes, M., The pricing of options and corporate liabilities. J. Political Econ., 1973, 8, 637–654.

- [5] Bollerslev, T., Generalized autoregressive conditional heteroskedasticity. J. Econometrics, 1986, 31, 307–327.

- [6] Borland, L., Option pricing formulas based on a non-Gaussian stock price model. Phys. Rev. Lett., 2002a, 89, 098701-01.

- [7] Borland, L., A theory of non-Gaussian option pricing. Quant. Finance, 2002b, 2, 415–431.

- [8] Borland, L., Bouchaud, J. P., Muzy, J. F. and Zumbach, G., The dynamics of financial markets: Mandelbrot’s multifractal cascades, and beyond. Wilmott Magazine, March 2005.

- [9] Bormetti, G., Cazzola, V., Livan, G., Montagna, G. and Nicrosini, O., A generalized Fourier transform approach to risk measures. J. Stat. Mech., 2010, P01005.

- [10] Bormetti, G., Cisana, E., Montagna, G. and Nicrosini, O., A non-Gaussian approach to risk measures. Physica A, 2007, 376, 532–542.

- [11] Bormetti, G., and Delpini, D., Exact moment scaling from multiplicative noise. Phys. Rev. E, 2010, 81, 032102-1–4.

- [12] Bormetti, G., Montagna, G., Moreni, N. and Nicrosini, O., Pricing exotic options in a path integral approach. Quant. Finance, 2006, 6, 55–66.

- [13] Bouchaud, J., P. and Potters, M., Theory of Financial Risk and Derivative Pricing: from Statistical Physics to Risk Management, 2003 (Cambridge: Cambridge University Press).

- [14] Brandimarte P., Numerical Methods in Finance and Economics, 2006 (Hoboken: John Wiley & Sons).

- [15] Campbell, J., Lo, A. H. and McKinlay, C., The Econometrics of Financial Markets, 1997 (Princeton: Princeton University Press).

- [16] Chiarella, C., and El-Hassan, N., Evaluation of derivative security prices in the Heath-Jarrow-Morton framework as path integrals using fast Fourier transform techniques. J. Finan. Engineering, 1997, 6, 121–147.

- [17] Cont, R., Empirical properties of asset returns: stylized facts and statistical issues. Quant. Finance, 2001, 1, 223–236.

- [18] Dash, J., Path integrals and options, Parts I, II. 1989, Centre Nationale de la Recherche Scientifique.

- [19] Delpini, D., and Bormetti, G., Minimal model of financial stylized facts. Phys. Rev. E, 2011, 83, 041111-1–4.

- [20] Eydeland, A., A fast algorithm for computing integrals in function spaces: financial applications. Computational Econ., 1994, 7, 277–285.

- [21] Engle, R. F., Autoregressive conditional heteroskedasticity with estimates of the variance of United Kingdom inflation. Econometrica, 1982, 50, 987–1007.

- [22] Fama, E. F., The behavior of stock market prices. J. Bus., 1965, 84, 34–105.

- [23] Friedrich, R., Peinke, J. and Renner, C., How to quantify deterministic and random influences on the statistics of the foreign exchange market. Phys. Rev. Lett., 2000, 84, 5224–5227.

- [24] Fouque, J. P., Papanicolaou, G. and Sircar, K. R., Derivatives in Financial Markets with Stochastic Volatility, 2000 (Cambridge: Cambridge University Press).

- [25] Ghashgaie, S., Breymann, W., Peinke, J., Talkner, P. and Dodge, Y., Turbulent cascades in foreign exchange markets. Nature, 1996, 381, 767–770.

- [26] Iacus, S. M., Simulation and Inference for Stochastic Differential Equations, 2008 (New York: Springer).

- [27] Jorion, P., Value at Risk: The New Benchmark for Managing Financial Risk, 2007 (New York: McGraw-Hill).

- [28] Mandelbrot, B., The variation of certain speculative prices. J. Bus., 1963, 36, 394–419.

- [29] Mandelbrot, B., Fractals and Scaling in Finance: Discontinuity, Concentration and Risk, 1997 (New York: Springer).

- [30] Mantegna, R. N. and Stanley, H. E., An Introduction to Econophysics: Correlations and Complexity in Finance, 2004 (Cambridge: Cambridge University Press).

- [31] McCauley, J. L., Dynamics of Markets: Econophysics and Finance, 2004 (Cambridge: Cambridge University Press).

- [32] McCauley, J. L. and Gunaratne, G. H., An empirical model of volatility of returns and option pricing. Physica A, 2003, 329, 178–198.

- [33] McCauley, J. L., Gunaratne, G. H. and Bassler, K. E., Hurst exponents, Markov processes, and fractional Brownian motion. Physica A, 2007a, 379, 1–9.

- [34] McCauley, J. L., Gunaratne, G. H. and Bassler, K. E., Martingale option pricing. Physica A, 2007b, 380, 351–356.

- [35] Merton, R., Theory of rational option pricing. Bell J. Econ., 1973, 4, 141–183.

- [36] McNeil, A. J., Frey, R. and Embrechts, P., Quantitative Risk Management: Concepts, Techniques and Tools, 2005 (Princeton: Princeton University Press).

- [37] Montagna, G., Nicrosini, O. and Moreni, N., A path integral way to option pricing. Physica A, 2002, 310, 450–466.

- [38] Vellekoop, M. H. and Nieuwenhuis, J. W., On option pricing models in the presence of heavy tails. Quant. Finance, 2007 7, 563–573.