BEHAVIOR OF AN ALMOST SEMICONTINUOUS POISSON PROCESS

ON A MARKOV CHAIN UPON ATTAINMENT OF A LEVEL11footnotemark: 1footnotetext: Translated from

Ukrains’kyi Matematychnyi Zhurnal,

Vol. 62, No. 1, pp. 81–89, January,

2010. Original article submitted April 4, 2008;

revision submitted February 19, 2009.

This reprint differs from the original in

pagination and typographic detail.

Ievgen Karnaukh

footnotetext: Kyiv National University of Trade

and Economics, Kyiv, Ukraine.ievgen.karnaukh@gmail.com UDC 519.21

We consider the almost

semi-continuous processes defined on a finite Markov chain.

The representation of the moment generating functions

for the absolute maximum after achievement positive level and for

the recovery time are obtained. Modified processes with two-step

rate of negative jumps are investigated.

In the present paper, we continue the investigations of almost

semicontinuous processes defined on finite

Markov chains originated in [1, 2].

In the first section, we consider analogs of the functionals

studied in [3]

(Sec. 6.3) for the scalar case.

In the second section, we study overjump functionals for a

modified almost semi-

continuous process playing the role of an analog of a modified

semicontinuous process with drift whose variations

depend on the attained level (see, e.g., [4],

Chap. VII and [5]; for the scalar case,

see [6]).

Let be a finite irreducible Markov chain with the set of

states

and an infinitesimal matrix .

A process is defined as follows: ; for

, ,

the increments coincide with the increments of the process

where and are

Poisson processes with the rates and ,

respectively. and are independent positive random variables. Moreover,

have exponential distributions with parameters , whereas have absolutely continuous distributions with finite expectations .

In this case, is an almost lower semicontinuous process on a Markov chain

(see [1, p. 562]) with cumulant

(1)

where , , ,

,

and

, .

By

we denote the extrema of the process . The

overjump functionals are specified as follows:

Let be an exponentially distributed random variable

with parameter

independent of . The distributions of extrema and the

corresponding atomic probabilities are defined as follows:

, , and .

Further, we denote and

.

Thus, for , we can write (see [2])

(2)

Since

we conclude that the spectra of the matrices

and are formed by positive elements.

The following assertion for overjump functionals

is obtained from [2, p. 48]:

Note that and the matrices

and satisfies the equations

respectively.

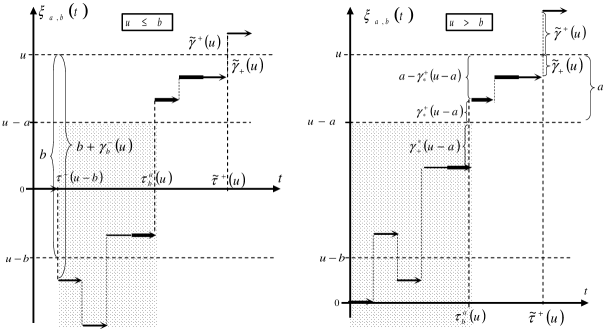

2 Red period

In the present section, we consider functionals connected with the behavior of

upon attainment of a

positive level. Denote

It is worth noting that the process can be regarded

as a surplus risk process with stochastic function

of premiums (the values of premiums are exponentially

distributed) in a Markov environment and the functionals

, , can be regarded as the total

deficit after ruin, recovery time, and ”red period”, respectively

(see [7]).

In view of the fact that, under the condition , the functional is

stochastically equivalent to , we find

In exactly the same way as in the proof of Theorem 5.1

in [8],

for the moment generating function of the time to recovery, we deduce

Combining this relation with (2),

we obtain (7).

By using the strict Markov property, we get

In deducing this equality, we have used the fact that, under the condition , the functional is stochastically equivalent

to the time of attainment of the level .

In the matrix form, we can write

By using (2) and (5), we establish equality (8).

∎

3 Modified Process

In the present section, in addition to the results obtained for the overjump functionals, we use the relations for

two-limit functionals. By

we denote the time of exit from the interval .

Further, we consider the events specifying the times of exit

through the upper and lower boundaries of the interval:

and the corresponding overjumps

It follows from the results presented in [1, p.559] that

(9)

Note that the representations for and

were obtained in [1]

for almost upper semicontinuous processes.

In this case, one can use the fact that if

is an almost upper semicontinuous process, then

is an almost lower semicontinuous process.

We now determine the modified process , . Assume that the rates of exponentially

distributed negative jumps

depend on the threshold levels

and (see [6]). In the risk theory, this

process has the following interpretation: As soon as the reserve

of an insurance company attains a certain level,

the company may decrease the value of the premium to attract

additional clients. Therefore, the distribution of

the values of premiums contains a parameter

,

if the reserve of the company is equal to

. Assume that takes only two values

and equal to

the initial and lowered values of the premium,

respectively, and in

addition, that the transition between these values

occurs on passing through an inert zone .

The increments of the process coincide with

the increments of the process

(with intensities ) between the last crossing of the level

from below and the next crossing of the level from above.

The increments of coincide with (with intensities

) between the last crossing of the level

from above and the subsequent crossing of the level from below.

In the notation of moment generating functions we use the symbol ,

which corresponds to the process . Further, if , then

where .

Figure 1: Modified Risk Process

By , we denote the overjump functionals for the modified

process (see Figure 1). We also denote

Then the Gerber–Shiu function can be defined as follows (see [9])

where ,

is a nonnegative function (penalty). If the parameter

is regarded as the force of interest, then

can be regarded as a discounted expected penalty at the time to ruin.

Assume that the process describes the price

of a stock whose variations have the form of random jumps.

We now consider a perpetual American put option with strike price .

The payoff at time is equal to .

For the scalar case, the optimal strategy is as follows

where exercise boundary

: . Assume that the market is risk neutral.

Then the price of an option is defined as the expected discounted payoff

or, in view of the fact that , as follows

Therefore,

with

can also be regarded as the price of perpetual American

put option [10, p.12].

Theorem 2.

For the modified process

1) if , then

(10)

2) if , then

(11)

where

(12)

Proof.

Relation (10) is an analog of the

result obtained in [6].

By using the formula of total probability and

the strict Markov property, for , we find

(13)

This yields relation (11). Relation (12)

is obtained from (11) as a result of the integral transform.

∎

In the scalar case the matrix relations become

somewhat simpler. If we set , then

is the ruin probability for the modified process.

Corollary 1.

For the scalar modified process

1) if , then

(14)

2) if then

(15)

where

Example. Assume that, for the scalar risk process, the premiums

have exponential distributions with parameter , whereas the claims

obey the Erlang distribution(2):

It is necessary to determine the corresponding ruin probability for .

where the quantities , and are independent of and ; and

are positive roots of the Lundberg equation for the processes and

, respectively. By using (5) and (14), we conclude

(for ):

(16)

where , and are independent of and .

Assume that , , , , and

. Then and . The corresponding Lundberg roots are ,

and , .

In addition, the distribution of the absolute maximum of the process and

the probability of exit of the process from the interval

through the lower boundary are given by the formulas

For ,

by using (16), we arrive at the following expression for the ruin

probability

References

[1]

Karnaukh, E.V. Two-limit problems for almost semicontinuous

processes defined on a Markov chain. (Ukrainian, English)//Ukr. Mat.

Zh. 59, No. 4 (2007), 555-565, translation in Ukr. Math. J. 59, No.

4 (2007), 620-632, arXiv:0909.1420v1[math.PR].

[2]

Karnaukh, E.V. Overshoot functionals for almost semicontinuous

processes defined on a Markov chain // Teor. Imovir. ta Matem.

Statyst., No.76 (2007), 45-52, translation in Theor. Probability and

Math. Statist. No. 76 (2008), 49-57, arXiv:0909.3690v1[mathPR].

[3]

Gusak D.V., Boundary value problems for

processes with independent increments in the risk theory[in Ukrainian],

Institute of Mathematics,

Ukrainian National Academy of Sciences, Kyiv, 2007.

[4]

Asmussen S., Ruin Probabilities,

World Scientific,

Singapore,

2000.

[5]

Jasiulewicz H., Probability of ruin with variable premium

rate in a Markovian environment, Insurance: Mathematics and

Economics 29 (2001),

291–296.

[6]

Bratiychuk M.S., Derfla D., On a modification of the

classical risk process, Insurance: Mathematics and Economics

41 (2007), 156–162.

[7]

Rolsky T., Shmidly H., Shmidt V., Teugels J., Stochastic

Processes for Insurance and Finance, Wiley, New York,

1999.

[8]

Gusak D.V., Boundary problems for processes with

independent increments on Markov chains and for

semi-Markov processes, Institute of Mathematics, Ukrainian National Academy

of Sciences, Kyiv, 1998.

[9]

Gerber H.U., Shiu S.W., On the time value of ruin, North

American Actuarial Journal 2 (1998), N 1, 48–78.

[10]

Gerber H.U., Shiu S.W., From ruin theory to pricing reset

guarantees and perpetual put optoins, Insurance: Mathematics and

Economics 24 (1999),

3–14.