Default and Systemic Risk in Equilibrium

Abstract

We develop a finite horizon continuous time market model, where risk averse investors maximize utility from terminal wealth by dynamically investing in a risk-free money market account, a stock written on a default-free dividend process, and a defaultable bond, whose prices are determined via equilibrium. We analyze the endogenous interaction arising between the stock and the defaultable bond via the interplay between equilibrium behavior of investors, risk preferences and cyclicality properties of the default intensity. We find that the equilibrium price of the stock experiences a jump at default, despite that the default event has no causal impact on the dividend process. We characterize the direction of the jump in terms of a relation between investor preferences and the cyclicality properties of the default intensity. We conduct a similar analysis for the market price of risk and for the investor wealth process, and determine how heterogeneity of preferences affects the exposure to default carried by different investors.

1 Introduction

The default of a systemically important entity can have an impact on the rest of the economy through a number of different mechanisms. For instance, firms that have exposures to the defaulted entity through market transactions, can experience a deterioration in fundamentals driving the value of their assets. Under adverse circumstances this can lead to a domino effect, where the default of one firm causes financial distress on entities with which the firm had business relations. This distress can propagate through the financial system causing a cascading failure, leading in the worst case to the collapse of a significant portion of the system (the recent credit crisis being a clear example). In the context of interbank lending, Giesecke and Weber (2006) propose a reduced form contagion model, while Amini et al. (2010) and Amini et al. (2011) use tools from random graph theory to analyze short term counterparty credit exposures. Dynamic contagion models are considered in Dai Pra et al. (2009), and more recently in Cvitanić et al. (2010) and Giesecke et al. (2011).

Alternatively, there may be a purely informational effect, where the default of one firm triggers the market participants to update their perception of the state of the economy. For example, Collin-Dufresne et al. (2003) show that the unexpected default of an individual firm can lead to a market-wide increase in credit spreads, and demonstrate via calibration that the risk premium due to contagion risk may be considerable.

A third possibility is that the sudden shock associated with the default event leads to a re-allocation of wealth as the economy returns to equilibrium. This may in turn cause rapid price changes due to linkages that stem from the equality between supply and demand. The aim of the present paper is to study this mechanism in a continuous time financial model, including default risk, where prices are determined endogenously in equilibrium.

While models of economic equilibrium have been studied for a long time, it is only recently that fully dynamic stochastic models of equilibrium have received significant attention. Dumas (1988) considers a dynamic equilibrium model with two investors, and characterizes the equilibrium behavior of the wealth allocation and risk-free rate, assuming that the stock returns are specified exogenously. Chabakauri (2010) considers a similar economy, but allows for the possibility of portfolio constraints, and analyzes cyclicality properties of market price of risk and stock return volatilities. Bhamra and Uppal (2009) consider a continuous time economy populated by two power utility agents with heterogenous beliefs and preferences, and give closed form expressions for consumption policies, portfolio policies, and asset prices. The same model as in Bhamra and Uppal (2009) is considered by Cvitanic et al. (2011) and Cvitanic and Malamud (2011a), who extend the results by Bhamra and Uppal to the case of an arbitrary number of agents, including an asymptotic analysis for large time horizons. Cvitanic and Malamud (2011b) provide decompositions into myopic and non-myopic components for market price of risk, stock volatility, and hedging strategies. In the same economic model, Wang (1996) studies how investor preferences affect the term structure of interest rates.

The literature on dynamic equilibrium models, including the papers mentioned above, has been concerned primarily with models where equilibrium prices have continuous paths. This means that dramatic and sudden changes, such as crisis events or major defaults, are absent—and indeed these papers have focused on other economic phenomena. An exception is Hasler (2011), which considers a Lucas economy with multiple defaults, where the default intensities are constant.

In the present paper we study a finite horizon continuous time model, where rational investors maximize utility from terminal wealth. Three securities are liquidly and dynamically traded: a money market represented by a locally risk-free security, i.e. investors can borrow from or lend to each other without default, a stock representing shares of the aggregate endowment, and a defaultable bond which represents the corporate bond index (for example, the Dow Jones corporate bond index). We assume a constant recovery model, in which case the default of the bond index is interpreted as the default of one (or more) of the index bonds, which reduces the total payment of the index. The intensity of the defaultable bond may, but need not, depend on the dividend process.

As we demonstrate in the present paper, introducing a defaultable security in the economy leads to new insights regarding the behavior of securities prices, market price of risk, and wealth allocation. For instance, we find that the equilibrium price of the stock typically jumps when default occurs, despite the fact that the underlying dividend process is entirely unaffected by the default event. Moreover, the direction of the jump (up or down) depends in a non-trivial way on the interplay between investor preferences and the cyclicality properties of the default intensity. In particular, we show that upward jumps in the stock price are possible if, roughly speaking, the default intensity is sufficiently counter-cyclical. The precise statement is given in Theorem 2. We also show that a similar analysis, with similar conclusions, can be carried out for the wealth processes of individual investors, see Section 5. In this connection, we investigate how heterogeneity of preferences affects the exposure to the default carried by the different investors.

Due to the possibility of default, there are two sources of risk in our model: diffusion risk and jump risk. Using techniques from the theory of filtration expansions, which has a long and successful history in credit risk modeling, we are able to guarantee market completeness, even in the presence of jumps, see also Bielecki et al. (2006a) and Bielecki et al. (2006b) for a detailed analysis of market completeness and replication strategies in reduced form models of credit risk. This allows us to identify a unique market price of risk process, corresponding to diffusion risk, and default risk premium process, corresponding to jump risk. It turns out that the two quantities are intimately linked, see Proposition 2. By means of a quite delicate mathematical analysis, these quantities are studied in the case of constant interest rate and default intensity.

The most natural interpretation of the phenomena we study is as a form of systemic risk, arising in an economy consisting of securities carrying both market and default risk. While systemic risk effects generated from equilibrium models have been studied, for instance in Allen and Gale (2000) and Freixas et al. (2000), these papers use static discrete time models, exclusive of default, where the focus is on characterizing optimal risk sharing across banks with different credit profiles, or belonging to different geographical sectors. Differently from most research efforts, our model exhibits an endogenous interaction between the stock and the defaultable bond, which arises via the interplay between equilibrium behavior of the investors and their risk preferences.

The rest of the paper is organized as follows. Section 2 introduces the economic model. Section 3 analyzes the market price of risk in equilibrium along with its behavior at the default event. Section 4 characterizes the behavior of the equilibrium stock price at default via a relation between cyclicality properties of short rate and default intensity, and investor preferences. Section 5 performs a similar analysis for the wealth process of a risk-averse agent, and, in the case of a power utility investor, provides monotonicity relations between the size of the jump and the level of risk aversion. Section 6 concludes the paper. The proofs of the necessary lemmas are deferred to the appendix.

2 The Model

2.1 The Probabilistic Model

Let be a complete probability space, supporting a standard Brownian motion . Let be the augmented filtration generated by , which satisfies the usual hypotheses of completeness and right continuity. We use a standard construction (also called Cox construction) of the default time , based on doubly stochastic point processes, using a given nonnegative adapted intensity process . To this end, we assume the existence of an exponentially distributed random variable defined on the probability space , independent of the process . The default time is then defined as

The market filtration , which describes the information available to investors, is given by

That is, it contains all information in , together with the knowledge of whether has occurred or not, and has been made right-continuous. It is a well-known result (see e.g. Bielecki and Rutkowski (2001), Section 6.5 for details) that the process

is a -martingale under . In other words, is the default intensity (or hazard rate) of .

An important consequence of the previous construction is that Hypothesis (H) holds, i.e. every martingale remains a martingale, see Bielecki and Rutkowski (2001). It then follows from a result by Kusuoka (Theorem 5 in Appendix A) that every square integrable martingale may be represented as a stochastic integral with respect to and .

2.2 The market model

We consider a market model, which is an extension of the standard setting in Cvitanić and Malamud (2010). We assume that there is an underlying dividend process with dynamics

| (1) |

It is assumed that and are such that a strictly positive, strong solution exists. We also assume that and are infinitely differentiable on , and that .

There are two risky assets in the economy, a stock which carries market risk, and a defaultable bond which carries default risk. At terminal time , the stock pays a terminal dividend , while the defaultable bond pays a terminal dividend . The latter is given by

Here is a constant recovery value paid at time in case default happens at or before . We assume that is deterministic, although many calculations would still be valid as long as is -measurable. Neither the stock, nor the defaultable bond generates any intermediate dividends. We also assume the existence of a locally risk free money-market account with interest rate . Finally, we assume that the default intensity and interest rate are of the form

for deterministic functions and . The same assumption has also been used by Cvitanić and Malamud (2010) for the interest rate.

In our model, both the stock and the defaultable bond are positive net supply assets. In contrast, the zero money-market account is assumed to be available in zero net supply.

The market price at time of the stock is denoted by , and that of the defaultable bond by . These processes are determined in equilibrium, and their dynamics is of the form

The existence of such representations follows from Theorem 5 together with the fact that in equilibrium, both and are semimartingales with absolutely continuous finite variation parts. Furthermore, we conjecture that the matrix

will be invertible in equilibrium. This immediately implies that the market is complete, via application of Theorem 5. It is then well known, see e.g. Cvitanić and Zapatero (2004), that there exists a unique state-price density process

The time price of a payoff received at time is given by .

2.3 The investors

There are a finite number of investors, indexed by , who optimize expected utility from final consumption. They are all assumed to have identical beliefs given by the historical probability , but can have different utility functions . These are assumed to be twice continuously differentiable, strictly concave, and satisfy Inada conditions at zero and infinity:

Two important measures of risk aversion, which will be used extensively in this paper, are the coefficients of absolute and relative risk aversion, both defined in Pratt (1964). The coefficient of absolute risk aversion is defined as

| (2) |

Pratt related this measure to the agent’s risk behavior by showing that an agent with utility is more risk averse than an agent with utility if and only if for all . The coefficient of relative risk aversion is defined as

| (3) |

The :th investor chooses a dynamic portfolio strategy , a predictable and -integrable process, where is the proportion of wealth invested in the stock at time , and is the proportion of wealth invested in the defaultable bond. The remaining wealth is invested in the money market account to make the strategy self-financing. The investor must choose his strategy so that the corresponding wealth process, given by

| (4) |

stays strictly positive for . The portfolio strategy is chosen to maximize the expected utility

Market completeness allows one to use standard duality methods (see Cvitanić and Malamud (2010)) to show that the optimal final wealth in equilibrium is given by

| (5) |

where the number is the solution to the budget constraint equation,

Moreover, the wealth at times is given by

| (6) |

2.4 The equilibrium

We employ the usual notion of equilibrium:

Definition 1

The market is said to be in equilibrium if each investor behaves optimally and all the securities markets clear.

Again by market completeness, standard equilibrium theory, see Constantinides (1982), shows that security prices coincide with those in an artificial economy populated by a single, representative investor. We denote the corresponding utility function by , and assume that is twice continuously differentiable, strictly concave, and satisfies Inada conditions at zero and infinity. The state-price density is then given by

| (7) |

Furthermore,

where is the Radon-Nikodym density process corresponding to the (unique) risk-neutral measure ,

Using Equation (7), the definition of and , and Lemma 4 in Appendix A, we can separate the state price density into a pre- and post-default component. More precisely, we have

where

| (8) |

Remark. Assume that the intensity is deterministic and, for simplicity, that . We then have

indicating that the pre-default state price density is the weighted average of the state price density in an economy where default will surely happen, and the state price density in a default-free economy. The weights are, respectively, the probability that default will, or will not, take place before , given that it has not occurred up to time .

3 Equilibrium market price of risk

In this section we derive expressions for the market price of (diffusion and default) risk, as well as the risk premium of the stock. The risk premium is defined as the excess growth rate of the asset above the risk-free rate, namely .

By Theorem 5 the density process associated with the risk-neutral measure has the representation

for some predictable processes and . An application of Girsanov’s theorem shows that

are local martingales, and in particular is Brownian motion. Note that we can write

so that the risk-neutral default intensity is given by . The quantity is called the default risk premium, and is called the market price of risk. We fix this notation from now on.

Proposition 1

The market price of risk is given by

where is the volatility of , and is the volatility of . The default risk premium is given by

The risk premium associated with the stock, or the equity risk premium, is given by

Proof. The assertions concerning and follow from Lemma 5 and the definition of and , since . Let us establish the expression for the risk premium. The relations between and , respectively and , together with the -dynamics of the stock price yield

The drift term equals since the discounted stock price is a martingale under . The proof follows by substituting the expressions for and into the above equation (the latter follows from Lemma 5.)

Remark. The risk premium can alternatively be expressed in terms of the risk-neutral default intensity , using that . The result is

It is clear from the definition of and that we always have . The contribution to the equity risk premium coming from default risk therefore has the same sign as . This quantity is minus the size of the jump in the stock price, were default to happen at time . In particular, if the stock price jumps down at default, then the investors require a premium for holding the stock, as they want to be compensated for the loss incurred upon default. On the other hand, if the stock jumps up at default, then it becomes an attractive security to hold, and therefore the investors are willing to pay a premium for holding it. We will study the sign of the jump in more detail in Section 4; suffice it to say here that positive price jumps, while atypical, are indeed possible.

There is an interesting relationship between the sensitivity of with respect to changes in the level of the dividend process, and the market price of diffusion risk. To state the result, first observe that the Markovian structure allows us to write

for some measurable function . We now have

Proposition 2

The function is differentiable, and the derivative is given by

Proof. As for , the Markovian structure allows us to write for and measurable functions . As in the proof of Theorem 1 below, we may apply Theorem 6.1 in Janson and Tysk (2006) to obtain the smoothness of , and hence of since by Proposition 1. Differentiating this relation yields

Now, the volatility of a positive adapted semimartingale of the form is given by , as can be seen from Itô’s formula. By Proposition 1, is equal to minus the volatility of , which yields the result.

Observe that is the size of the jump in , if default were to occur at time . Proposition 2 shows in particular that if this quantity is positive, the default risk premium moves in the opposite direction to the dividend: an increase in the dividend process is accompanied by a decrease in the default risk premium, and vice versa. This appears to suggest that, upon default, a risk averse investor who sees an upward jump in the market price of risk, prefers to shift wealth from the risky stock to a default-free bond, giving a sure payoff of at maturity. If, on the other hand, is negative, the default risk premium moves in the same direction as the dividend.

We proceed to study how the market price of risk behaves at default. As we have just seen, this also provides information about the sensitivity of the default risk premium to changes in . The following result unfortunately requires us to assume constant interest rate and constant default intensity—already in this case the analysis is non-trivial (in particular it is much more delicate than for the jump in the stock price.) Extending it to more general and is an interesting problem that we leave for future research.

Theorem 1

Assume that the interest rate and default intensity are constant. If the representative investor has a strictly decreasing absolute risk aversion, then the market price of risk has a nonnegative jump at .

The rest of this section is devoted to proving Theorem 1. First, let us introduce some notation. For each , define the function

Using, for instance, Theorem 6.1 in Janson and Tysk (2006), we deduce that satisfies the PDE

where the subscripts denote partial derivatives. Standard results then imply that has the same degree of smoothness as and on , see e.g. Theorem 10 in Chapter 3 of Friedman (2008). Since we assume that and are infinitely differentiable, the same holds for .

Proof of Theorem 1. Due to Lemma 1 below, the theorem will be proved once we establish that the quantity

is decreasing in . This is done in two stages: Lemma 2 gives the result when is bounded, and Lemma 3 then extends this to unbounded .

Lemma 1

Assume that the interest rate and default intensity are constant. If

for all , then on .

Proof. It follows from (8) and the assumption of constant and that

and

The volatility of a positive adapted semimartingale of the form is given by , as can be seen from Itô’s formula. By Proposition 1 and the above expressions for and it then follows that

and

A calculation using that and are strictly positive reveals that if and only if

The result now follows.

Lemma 2

Assume that the conditions of Theorem 1 are satisfied. Assume also that there is a constant such that and for all . Then

is strictly decreasing in .

Proof. Define . It can be readily verified that satisfies the terminal value problem

Now define , and differentiate the above equation with respect to to see that satisfies the nonlinear PDE

with terminal condition

Let us pick , and define . We want to prove that . The function satisfies the terminal value problem

| (12) | ||||

where

Notice that , as we are assuming that the coefficient of absolute risk aversion is strictly decreasing. Moreover, the coefficients and are smooth due to the smoothness of , , and . The latter functions are smooth since they are the derivatives of the logarithm of the infinitely differentiable functions and .

Now, let be the solution to the SDE

The smoothness of and implies that a unique strong solution exists up to an explosion time, but since and for all , we have and there, so no explosion can occur. Indeed, holds for , almost surely.

Next, define a process by

Itô’s formula and the fact that satisfies (12) show that

and since remains in a compact set and , and are continuous, the integrand in front of is bounded. Therefore is a martingale, and its final value is due to the boundary condition of . We deduce that for every almost surely, and hence that , as desired.

Lemma 3

Proof. Fix . The goal is to show that . For each , let and be infinitely differentiable and coincide with , respectively , on , while being zero outside the interval . Denote by the solution to

and define . An application of Lemma 2 shows that

for each . It thus suffices to prove that and pointwise. The latter follows from the former using interior Schauder estimates, for instance by applying the corollary of Theorem 15 in Chapter 3 of Friedman (2008) on each subdomain , (using the PDE representation of , and noticing that on each subdomain the coefficients of the parabolic operator associated to are Hölder continuous, and is bounded away from zero for all sufficiently large .)

To prove that , first note that and by the Markov property. Since is bounded, the desired convergence follows from the Bounded Convergence Theorem if almost surely, with . But this is clear: pathwise uniqueness and the construction of and imply that and coincide on the event

so . Since , almost surely, and the proof is finished.

4 Equilibrium stock price

In this section we are interested in how the market price of the stock changes when default occurs. If , there may be a jump in the stock price at . Under certain cyclicality assumptions on the default intensity and the interest rate, it turns out that the sign of the jump must be negative. On the other hand, in specific circumstances it can happen that the jump is positive. The following results gives the precise conditions. The proofs rely on a number of lemmas, which are stated and proved in Appendix B.

Theorem 2

Assume that the interest rate is counter-cyclical, and that the representative investor has strictly decreasing absolute risk aversion, as well as relative risk aversion bounded by one. Define

| (13) |

Then the following hold.

-

(i)

If is strictly increasing in for every , the stock price has a strictly positive jump at .

-

(ii)

If is strictly decreasing in for every , the stock price has a strictly negative jump at .

Proof. Equations (8), (10) and (LABEL:eq:Sprepost2) show that the jump in the stock price is given by

| (14) |

where

Using that and , elementary manipulations yields

on , where denotes -conditional covariance, and is defined in (13). It suffices to analyze the two covariances, since both and are strictly positive. Let us fix . By the Markov property of (and using that and ), we may without loss of generality assume that (and think of as ), as long as the starting point is allowed to be arbitrary.

By conditioning on , we find

and

where , and is given in (13). Since is counter-cyclical, is decreasing by Lemma 6, and hence is also decreasing. Moreover, the function has a derivative , which is strictly greater than zero if and only if

This is indeed the case since the relative risk aversion is less than or equal to one. Thus is strictly increasing.

Under the assumption of , is strictly increasing, so the first covariance is strictly positive, while the second is strictly negative. This uses the fact that for positive, strictly increasing functions and , and any non-constant random variable , , while if is strictly decreasing, .

Under the assumption of that is strictly decreasing, the situation reverses and the jump becomes strictly negative.

We also provide the following result, which shows that the stock price jump will be negative under more general conditions than those of Theorem 2.

Theorem 3

Assume that the interest rate is counter-cyclical and the default intensity pro-cyclical. If the representative agent has strictly decreasing absolute risk aversion, then the stock price has a strictly negative jump at .

Proof. Let , , and be as in the proof of Theorem 2. From Equation (14) we see that a sufficient condition for having a strictly negative jump is that for all . As in the proof of Theorem 2 it suffices to consider .

By Lemma 8 and the cyclicality of and , we have

Therefore, with and , we obtain by conditioning on that

Here is again given by (13). The derivative of is

| (15) |

which is strictly negative since the absolute risk aversion is assumed to be strictly decreasing. Therefore is strictly decreasing. Moreover, by Lemma 8 and the cyclicality of and , the functions and are decreasing. They are also strictly positive. Hence

for . Observing that has no atoms and , Lemma 9 then yields that , as desired.

Naively one might expect the jump in the stock price always to be negative, for the following reason. The default event leads to an instantaneous drop in the aggregate wealth in the economy. If the representative investor has a decreasing absolute risk aversion, this should lead to a reduced demand for the risky asset (after default, the stock is the only risky asset). This in turn forces the stock price down so that market clearing is maintained.

Such an argument supposes that the stock price jump is exclusively a wealth effect. However, when the default intensity is stochastic, there is also a “non-myopic” effect originating from expected future co-movements of the default intensity and the dividend process. Specifically, if the default intensity is highly counter-cyclical, and the current (pre-default) value of the dividend process is low, then even a moderate expected future dividend increase is coupled with a dramatic future reduction in the default intensity. The representative investor, in anticipation of the reduced risk of default, may then wish to shift wealth to the defaultable bond. This causes a downward pressure on the stock price, pushing it below what would be its fundamental value, were there no defaultable bond in the economy. When the default occurs, this downward pressure vanishes, and the stock price jumps up.

Of course, the same reasoning could be used for very high values of the dividend process to argue that the jump would be negative in these cases. Consistent with this observation, we have found that the function appearing in Theorem 2 becomes decreasing for large values of , even in examples where is highly counter-cyclical. In such cases the price jump will still be (mostly) positive on simulated paths, if the probability is sufficiently small that ever reaches the high levels where the function is decreasing.

We end this section with a numerical case study to support the argument just made. Specifically, we assume that the dividend process in Equation (1) is a geometric Brownian motion, i.e. and . Using time reversal of diffusions, see Lemma 10 in Appendix B, we may write

where the process satisfies the SDE

| (16) |

with

| (17) |

We set , , , , and use a strongly counter-cyclical default intensity given by . Further, we choose a logarithmic utility function given by . Under these choices of parameters, we estimated via Monte-Carlo simulation that at the default time the stock experiences a positive jump of size 0.001.

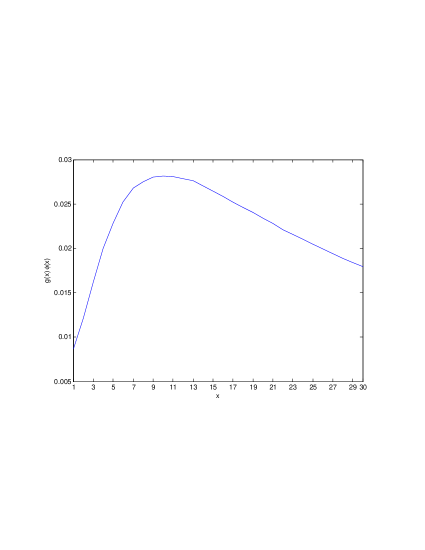

We estimate via Monte-Carlo simulations using (16) and (17), and report the behavior of in Figure 1. We see that this function is initially increasing, and it only starts decreasing for sufficiently large values of (). However, the probability that the geometric Brownian motion with negative drift reaches those values before time , given that it starts at , is extremely low.

5 Wealth processes

The jump in an individual agent’s wealth can be analyzed using the same techniques as for the stock price. Starting from Equations (5) and (6), and using Lemma 4 in Appendix A, the wealth of the :th investor can be decomposed into a pre- and post-default term. The result is

where

The jump in wealth is then on . The following result shows that the condition of Theorem 3 is also sufficient to ensure a negative jump in wealth. Unfortunately, the structure of the final value of the wealth process prevents us from obtaining a simple condition to guarantee a positive jump. (The reason is that, in contrast to the stock, cannot be expressed as times an -measurable random variable.)

Theorem 4

Assume that the interest rate is counter-cyclical and the default intensity pro-cyclical. If the representative agent has strictly decreasing absolute risk aversion, then every agent’s wealth process has a strictly negative jump at .

Proof. We consider the :th investor, so let us fix . The proof follows along the same lines as that of Theorem 3. The jump in wealth is

| (18) |

where

and . As in the proof of Theorem 3, it suffices to prove that . To make the notation less cluttered we write , , . As before, . Since both and are decreasing, is increasing. Hence

The cyclicality of and implies, via Lemma 8, that

Therefore, with and , we obtain by conditioning on that

Now, the cyclicality of and together with Lemma 6 shows that and are decreasing. Since also is strictly positive, is strictly decreasing, and is increasing, we have

for . The positivity of now follows by Lemma 9, since and has no atoms.

5.1 Jump sizes under power utility

We now investigate how the size of the jump is affected by the risk aversion of the agents. For this, we assume that all agents in the economy have power utility with relative risk aversion . That is,

which should be interpreted as when . We then have

The following result gives a condition under which a more risk averse investor will suffer a smaller jump in wealth than one who is less risk averse.

Proposition 3

Assume that the interest rate is counter-cyclical and the default intensity pro-cyclical, and that the representative agent has strictly decreasing absolute risk aversion. Consider two agents and with . If

| (19) |

for all , then

If is constant, the statement remains true also in the case where both inequalities are reversed.

Proof. Let , , , be as in the proof of Theorem 4. If jumps at , we have

and this is negative by Theorem 4 (this is the only place where the counter-cyclicality of is needed.) Hence

and this is nonpositive if and only if . As in the proof of Theorem 2 it is enough to consider . Let us define and . The assumption of power utility implies that

and hence, with and ,

The result follows once we prove that the first difference inside the parentheses is nonnegative, i.e.,

| (20) |

where by conditioning on we may replace by . Since , we have . Moreover, since and are both decreasing (the latter due to Lemma 6 and the pro-cyclicality of ), we have that

Thus, it is enough to apply Lemma 8 to establish (20), which completes the proof for non-constant . The last assertion is readily deduced upon noting that equality holds in (20) if is constant.

As a corollary we obtain that in an economy populated exclusively by investors with power utilities and logarithmic utilities, those with logarithmic utilities will suffer the smallest relative jump in wealth.

Corollary 1

Assume that the interest rate is counter-cyclical and the default intensity constant, and that the representative agent has strictly decreasing absolute risk aversion. Consider two agents and . If , i.e. the :th investor has log-utility, then

5.2 Measures of Systemic Risk

Based on the analysis done in the previous sections, we suggest two measures to quantify the amount of systemic risk at time in our economy. These are given by

Here corresponds to the drop in the stock price, and to the drop in the wealth of the :th investor, if default were to happen at time . Note that the measures are positive if the drop is positive (the jump is downward). The measure measures the impact a default would have on the stock, under the scenario that a default is imminent. The measure, , instead, quantifies the impact that default would have on the aggregate wealth of the economy, under the same scenario. Both measures can be interpreted as the number of dollars lost by the stock (respectively by the portfolio of the “average” investor in the economy) for each dollar lost by the corporate bond at time , in case default occurs at . Notice that the two measures convey different information. While depends on the interplay between cyclicality properties of the default intensity and interest rate, and the risk aversion of the representative investor, also accounts for the aggregate level of risk aversion in the economy. We postpone the characterization of the dependence of these measures on the market and default risk parameters of our model for future research.

6 Conclusions

We have developed a novel framework where a stock and a defaultable bond interact endogenously through equilibrium mechanisms. Our market consists of a money market account, a stock, and a defaultable bond, which are related to each other only through an underlying dividend process, whose dynamics is unaffected by the default event. The price processes of the stock and of the defaultable bond are determined endogenously in equilibrium. We analyzed in detail the impact of the default event on the stock price, market price of risk, default risk premium, and investor wealth processes, as well as the relations between them. We found that the equilibrium price of the stock typically jumps at default. As the default event has no casual impact on the dividend process, this results in a form of endogenous interaction between the stock and the defaultable bond. We have characterized the direction of the jump of the stock price at default in terms of investor preferences and cyclicality properties of the default intensity, showing that upwards jumps are possible when the default intensity is sufficiently counter-cyclical. Under the assumption of pro-cyclical default intensity and counter-cyclical interest rate, we have shown that the wealth process of the representative investor jumps down upon default, and that power utility investors will suffer a smaller relative jump in wealth if they are more risk averse. Based on the analysis done in the paper, we have suggested two possible measures to quantify systemic risk. In the future, we would like to extend our results to an economy consisting of multiple defaultable securities, and analyze how default correlations and cyclicality properties of the model parameters impact the price of the securities and the aggregate wealth in the economy.

Acknowledgments

A significant portion of the research reported in this paper was done while the authors were visiting the Swiss Institute of Finance at EPFL. The authors are grateful to them for the hospitality and the useful conversations on this topic. We would also like to thank Jakša Cvitanić, Jeremy Staum, and Robert Jarrow for useful conversations and feedback provided.

Appendix A Results relating to filtration expansion

Theorem 5 (Martingale representation in )

For every square integrable martingale there are predictable processes and , such that

and

Proof. This follows from Theorem 2.3 in Kusuoka (1999), since every martingale remains a martingale.

The following result is crucial in that it allows us to reduce -conditional expectations to -conditional expectations. This type of result is classical in credit risk modeling.

Lemma 4

Let , where and are integrable -measurable random variables. Then

Proof. First note that

Since Hypothesis (H) holds between and , any martingale satisfies . Apply this with , whose final value is since is -measurable, to get . Next, use the identity

which holds for -measurable and integrable , with . The claim now follows after some rearrangement.

Lemma 5

Let be a semimartingale, where and are continuous. Then

| (21) |

If is a strictly positive with representation

then . If in addition and have representations

then .

Proof. The expression (21) follows from Itô’s formula. Concerning the expression for , note that the continuity of and implies that

for some continuous process . Since , the result follows. Finally, combining (21) with the assumed representation for and yields

where is a stochastic integral with respect to and only. The expression for now follows, since and .

Appendix B Results relating to stochastic ordering and correlations

Lemma 6

Let satisfy with a fixed starting point , where we assume that

-

(i)

and are infinitely differentiable;

-

(ii)

is does not explode;

-

(iii)

for each , admits a density with continuous second derivatives.

Let be an nondecreasing (nonincreasing) function of . Then

is nondecreasing (nonincreasing) in .

Proof. The proof is based on time reversal of diffusions. Let . Then and , so

We wish to apply Theorem 2.1 in Haussmann and Pardoux (1986) to obtain the dynamics of the time-reversed process . The smoothness of and the local Lipschitz property of and (which is guaranteed by their smoothness), together with condition , imply that the assumptions of that theorem are satisfied; see Haussmann and Pardoux (1986), Remark 2.2 and Section 3. This yields

| (22) |

where

| (23) |

and is Brownian motion. The smoothness of , and implies that and are continuously differentiable on the interior of the support of , and hence locally Lipschitz there. By localization we may assume they are globally Lipschitz, so that standard comparison theorems (see for instance Ikeda and Watanabe (1977)) become available. Specifically, if lie in the support of , and denotes the solution to (22) started from , we have and hence if is nondecreasing. The case of nonincreasing is deduced in the same manner.

Lemma 7

Let be as in Lemma 6. Suppose and are all nondecreasing (resp. all nonincreasing), nonnegative functions, and let . Then

is nondecreasing (resp. nonincreasing), and we have

Proof. We treat the nondecreasing case, the other one being similar. Consider again the time-reversed process , and define time points , and functions , . Then , and we have

The nondecreasing property of can now be deduced as in the proof of Lemma 6. Concerning the inequality, we are done if we can prove that

for any (take to recover the desired inequality.) This is achieved by induction similarly as in the proof of Lemma A.4 in Cvitanić and Malamud (2010). Suppose the inequality holds for , , etc. Then by the Markov property of and the induction hypothesis,

where and . These functions are nondecreasing by the first part of the lemma, so an application of the induction hypothesis with yields

as desired. It remains to establish the case ; but this follows immediately from Lemma A.3 in Cvitanić and Malamud (2010).

Lemma 8

Let be as in Lemma 6. Let and be nondecreasing (resp. nonincreasing) functions. Then

Proof. Approximate and from below using functions of the form , then apply Lemma 7 and monotone convergence.

Lemma 9

Let , , , and be measurable functions and define

If and are nonnegative for all and , then

| (24) |

for every random variable for which the left side is well-defined. If and for , and has no atoms, the inequality is strict.

Proof. Let be an independent copy of . The left side of (24) then equals

and since and are exchangeable, it is also equal to

Adding the two expressions yields

which is nonnegative due to the assumptions on and . The statement concerning strict inequality is immediate.

Lemma 10

Assume that the dividend process is a geometric Brownian motion, i.e. , . Then

| (25) |

where the process satisfies the SDE , with

| (26) |

Proof. Define . Then and . Therefore, Eq. (25) holds. The smoothness of the transition density of given by

along with the local Lipschitz property of and , and the fact that the geometric Brownian motion is nonexplosive, allow applying Theorem 2.1 in Haussmann and Pardoux (1986). Using Eq. (23), we obtain the expressions in Eq. (26).

References

- Allen and Gale (2000) F. Allen and D. Gale. Systemic risk, interbank relations and liquidity provision by the central bank. Journal of Political Economy, 108(1):1–33, 2000.

- Amini et al. (2010) H. Amini, R. Cont, and A. Minca. Resilience to contagion in financial networks. Working Paper, Columbia University, 2010.

- Amini et al. (2011) H. Amini, R. Cont, , and A. Minca. Stress testing the resilience of financial networks. International Journal of Theoretical and applied finance, 14, 2011.

- Bhamra and Uppal (2009) H.S. Bhamra and R. Uppal. The effect of introducing a non-redundant derivative on the volatility of stock-market returns when agents differ in risk aversion. Review of Financial Studies, 22(6):2303–2330, 2009.

- Bielecki and Rutkowski (2001) T. Bielecki and M. Rutkowski. Credit Risk: Modeling, Valuation, and Hedging. Springer Finance, 2001.

- Bielecki et al. (2006a) T. Bielecki, M. Jeanblanc, and M. Rutkowski. Replication of contingent claims in a reduced-form credit risk model with discontinuous asset prices. Stochastic Models, 22:661–687, 2006a.

- Bielecki et al. (2006b) T. Bielecki, M. Jeanblanc, and M. Rutkowski. Completeness of a general semimartingale market under constrained trading. In M. do Rosario Grossinho, Editor, Stochastic Finance, Lisbon, Springer, pages 83–106, 2006b.

- Chabakauri (2010) G. Chabakauri. Asset pricing with heterogeneous investors and portfolio constraints. Working Paper, London School of Economics, 2010.

- Collin-Dufresne et al. (2003) P. Collin-Dufresne, R. Goldstein, and J. Helwege. Is credit-event risk priced? modeling contagion risk via the updating of beliefs. Working Paper, Columbia University, 2003.

- Constantinides (1982) G. Constantinides. Intertemporal asset pricing with heterogeneous consumers and without demand aggregation. Journal of Business, 55:253–267, 1982.

- Cvitanić and Malamud (2010) J. Cvitanić and S. Malamud. Equilibrium asset pricing and portfolio choice with heterogeneous prefrences. Working Paper, Swiss Finance Institute, EPFL, 2010.

- Cvitanic and Malamud (2011a) J. Cvitanic and S. Malamud. Relative extinction of heterogenous agents (contributions), article 4. The B.E. Journal of Theoretical Economics, 10(1), 2011a.

- Cvitanic and Malamud (2011b) J. Cvitanic and S. Malamud. Equilibrium asset pricing and portfolio choice with heterogeneous preferences. Working Paper, California Institute of Technology and EPFL, 2011b.

- Cvitanić and Zapatero (2004) J. Cvitanić and F. Zapatero. Introduction to the Economics and Mathematics of Financial Markets. MIT Press, 2004.

- Cvitanić et al. (2010) J. Cvitanić, J. Ma, and J. Zhang. Law of large numbers for self-exciting correlated defaults. Preprint available at http://www.hss.caltech.edu/~cvitanic/PAPERS/cmz2011.pdf, 2010.

- Cvitanic et al. (2011) J. Cvitanic, E. Jouini, S. Malamud, and C. Napp. Financial markets equilibrium with heterogeneous agents. Review of Finance. Forthcoming., 2011.

- Dai Pra et al. (2009) P. Dai Pra, W. Runggaldier, E. Sartori, and M. Tolotti. Large portfolio losses; a dynamic contagion model. The Annals of Applied Probability, 19(1):347–394, 2009.

- Dumas (1988) B. Dumas. Two-person dynamic equilibrium in the capital market. Review of Financial Studies, 2(2):157–188, 1988.

- Freixas et al. (2000) X. Freixas, M. Parigi, and J. Rochet. Systemic risk, interbank relations and liquidity provision by the central bank. Journal of Money Credit and Banking, 32(3):661–638, 2000.

- Friedman (2008) A. Friedman. Partial Differential Equations of Parabolic Type. Dover, 2008.

- Giesecke and Weber (2006) K. Giesecke and S. Weber. Credit contagion and aggregate losses. Journal of Economic Dynamics and Control, 30:741–767, 2006.

- Giesecke et al. (2011) K. Giesecke, K. Spiliopoulos, and R. Sowers. Default clustering in large portfolios: Typical and atypical events. Working Paper, Stanford University, 2011.

- Hasler (2011) M. Hasler. Reduced form default in a pure-exchange economy. Preprint, 2011.

- Haussmann and Pardoux (1986) H.G. Haussmann and E. Pardoux. Time reversal of diffusions. Annals of Probability, 14(4):1188–1205, 1986.

- Ikeda and Watanabe (1977) N. Ikeda and S. Watanabe. A comparison theorem for solutions of stochastic differential equations and applications. Osaka J. Math, 14:619–633, 1977.

- Janson and Tysk (2006) S. Janson and J. Tysk. Feynman-Kac formulas for Black-Scholes-type operators. Bull. London Math. Soc., 38:269–282, 2006.

- Kusuoka (1999) S. Kusuoka. A remark on default risk models. Adv. Math. Econ., 1, 1999.

- Pratt (1964) J. Pratt. Risk aversion in the small and in the large. Econometrica, 32:122–136, 1964.

- Wang (1996) J. Wang. The term structure of interest rates in a pure exchange economy with heterogenous investors. Journal of Financial Economics, 41:75–110, 1996.