pageheadfootsecnumdepth3\setkomafontpagenumber\setkomafontcaptionlabel \deffootnote[1em]1em1em\thefootnotemark \setvruler[10pt][1][1][4][1][0pt][0pt][-28pt][]

Likelihood inference for Archimedean copulas

Marius Hofert111RiskLab, Department of Mathematics, ETH Zurich, 8092 Zurich, Switzerland, marius.hofert@math.ethz.ch. The author (Willis Research Fellow) thanks Willis Re for financial support while this work was being completed., Martin Mächler222Seminar für Statistik, ETH Zurich, 8092 Zurich, Switzerland, maechler@stat.math.ethz.ch, Alexander J. McNeil333Department of Actuarial Mathematics and Statistics, Heriot-Watt University, Edinburgh, EH14 4AS, Scotland, A.J.McNeil@hw.ac.uk

2024-02-29

Abstract

Explicit functional forms for the generator derivatives of well-known one-parameter Archimedean copulas are derived. These derivatives are essential for likelihood inference as they appear in the copula density, conditional distribution functions, or the Kendall distribution function. They are also required for several asymmetric extensions of Archimedean copulas such as Khoudraji-transformed Archimedean copulas. Access to the generator derivatives makes maximum-likelihood estimation for Archimedean copulas feasible in terms of both precision and run time, even in large dimensions. It is shown by simulation that the root mean squared error is decreasing in the dimension. This decrease is of the same order as the decrease in sample size. Furthermore, confidence intervals for the parameter vector are derived. Moreover, extensions to multi-parameter Archimedean families are given. All presented methods are implemented in the open-source R package nacopula and can thus easily be accessed and studied.

Keywords Archimedean copulas, maximum-likelihood estimation, confidence intervals, multi-parameter families. \minisecMSC2010 62H12, 62F10, 62H99, 65C60.

1 Introduction

The well-known class of Archimedean copulas consists of copulas of the form

with generator . In practical applications, belongs to a parametric family whose parameter vector needs to be estimated.

There are several known approaches for estimating parametric Archimedean copula families; see Hofert et al. (2011) for an overview and a comparison of some estimators.

In the work at hand, we consider a (semi-)parametric estimation approach based on the likelihood. There are two significant obstacles to overcome. The first one is to derive tractable algebraic expressions for the generator derivatives and thus the copula density. The second is to evaluate these expressions efficiently in terms of both precision and run time.

Although the density of an Archimedean copula has an explicit form in theory, accessing the required derivatives is known to be challenging, especially in large dimensions. For example, Berg and Aas (2009) mention that for Archimedean copulas it is not straightforward to derive the density in general for all parametric families. For the Gumbel family, they say that one has to resort to a computer algebra system, such as Mathematica or the function D in R, to derive the -dimensional density. Note that computations based on computer algebra systems often fail already in low dimensions. Even if a theoretical formula can be computed, the numerical evaluation of such (typically lengthy) formulas is prone to errors since they are not given in a numerically tractable form. This often requires to work with a large number of significant digits which is typically far too slow to be applied in large-scale simulation studies (for example, to access the quality of goodness-of-fit testing procedures). Furthermore, as we will point out below, results obtained by computer algebra systems can be unreliable.

Generator derivatives for some important Archimedean families can be found in Shi (1995), Barbe et al. (1996), and Wu et al. (2007), however, in recursive form. In this work, we derive explicit formulas for the generator derivatives of well-known Archimedean families in any dimension. These derivatives are interesting in their own right, for example, for accessing densities, for building conditional distribution functions, or for evaluating the Kendall distribution function. They can also be used to explicitly compute densities of asymmetric extensions of Archimedean copulas such as Khoudraji-transformed Archimedean copulas.

We then tackle the problem of maximum-likelihood estimation for Archimedean copulas for these families. Focus is put on large, say ten to one hundred, dimensions since they are the most relevant in practice; see Embrechts and Hofert (2011). Note that the considered Gumbel family is also an extreme value copula, for which densities in general are rarely known. Hofert et al. (2011) show the excellent performance of the maximum-likelihood estimator as measured by both precision and run time in a large-scale comparison with various other estimators up to dimension one hundred. Furthermore, to add transparency, all the algorithms used in this paper are implemented in the open source R package nacopula, so that the interested reader can study the non-trivial details of the numerical implementation and the numerous tests conducted in more detail. In the work at hand, we also consider examples of multi-parameter Archimedean families. In contrast to method-of-moments-like estimation procedures such as the one based on Kendall’s tau, maximum-likelihood estimation is not limited to the one-parameter case. Furthermore, we address the problem of computing initial intervals for the optimization of the log-likelihood for the multi-parameter Archimedean families considered. Additionally, we show how confidence intervals for the copula parameter vector can be constructed.

The paper is organized as follows. In Section 2, we briefly recall the notion of Archimedean copulas and the families considered. Section 3 presents explicit functional forms of the generator derivatives of these families and the corresponding copula densities are derived. In Section 4, the root mean squared error is investigated as a function of the dimension. Section 5 presents methods for constructing confidence intervals for the copula parameter vector. In Section 6 we address extensions to multi-parameter Archimedean families, including a strategy for computing initial intervals and two examples of two-parameter families. Finally, Section 7 concludes.

2 Archimedean copulas

Definition 2.1

An (Archimedean) generator is a continuous, decreasing function which satisfies , , and which is strictly decreasing on . A -dimensional copula is called Archimedean if it permits the representation

| (1) |

for some generator with inverse , where .

McNeil and Nešlehová (2009) show that a generator defines an Archimedean copula if and only if is -monotone, meaning that is continuous on , admits derivatives up to the order satisfying for all , , and is decreasing and convex on .

According to McNeil and Nešlehová (2009), an Archimedean copula admits a density if and only if exists and is absolutely continuous on . In this case, is given by

| (2) |

where .

We mainly assume to be completely monotone, meaning that is continuous on and for all , , so that is the Laplace-Stieltjes transform of a distribution function on the positive real line, that is, ; see Bernstein’s Theorem in Feller (1971, p. 439). The class of all such generators is denoted by and it is clear that a generates an Archimedean copula in any dimensions and that its density exists.

There are several well-known parametric generator families; see Nelsen (2007, pp. 116), also referred to as Archimedean families. Among the most widely used in applications are those of Ali-Mikhail-Haq (“A”), Clayton (“C”), Frank (“F”), Gumbel (“G”), and Joe (“J”); see Table 1. We consider these families as working examples throughout this work. Detailed information about the corresponding distribution functions is given in Hofert (2011b) and references therein. Note that these one-parameter families can be extended to allow for more parameters, for example, via outer power transformations. Furthermore, there are Archimedean families which are naturally given by more than a single parameter. Examples for both cases are given in Section 6.

| Family | Parameter | ||

|---|---|---|---|

| A | |||

| C | |||

| F | |||

| G | |||

| J |

Table 2 summarizes properties concerning Kendall’s tau and the tail-dependence coefficients; see Joe (1997, p. 91), Joe and Hu (1996), and Nelsen (2007, p. 214) for the investigated Archimedean families. Here, denotes the Debye function of order one. Note that these properties are often of interest in order to choose a suitable model which is then estimated. The construction of initial intervals in Section 6.1 for the optimization of the likelihood is based on Kendall’s tau.

| Family | |||

|---|---|---|---|

| A | 0 | 0 | |

| C | 0 | ||

| F | 0 | 0 | |

| G | 0 | ||

| J | 0 |

3 Maximum-likelihood estimation for Archimedean copulas

3.1 The pseudo maximum-likelihood estimator

Assume that we have given realizations , , of independent and identically distributed (“i.i.d.”) random vectors , , from a joint distribution function with Archimedean copula generated by and corresponding density . The generator is assumed to belong to a parametric family with parameter vector , , and the true but unknown vector is (similarly, and ). As usual, random vectors or random variables are denoted by upper-case letters, their realizations by lower-case letters.

Before estimating , the first step is usually to estimate the marginal distribution functions. In a second step, one then estimates . This two-step approach is typically much easier to accomplish than estimating the parameters of the marginal distribution functions and the copula parameter vector simultaneously. Estimating the marginal distribution functions can be done either parametrically or non-parametrically. Based on maximum-likelihood estimation, the former approach is suggested by Joe and Xu (1996) and is known as inference functions for margins. The latter approach is known as pseudo maximum-likelihood estimation and is suggested by Genest et al. (1995); see Kim et al. (2007) for a comparison of maximum-likelihood estimation, the method of inference functions for margins, and pseudo maximum-likelihood estimation.

Following pseudo maximum-likelihood estimation, the marginal distribution functions are estimated by their empirical distribution functions , , leading to the so-called pseudo-observations , , where

| (3) |

Here, for each , denotes the rank of among all , . The asymptotically negligible scaling factor of is used to force the variates to fall inside the open unit hypercube to avoid problems with density evaluation at the boundaries of . As usual, the pseudo-observations are interpreted as realizations of a random sample from (despite known issues of this interpretation such as the fact that the pseudo-observations are neither realizations of perfectly independent random vectors nor that the components are perfectly following a univariate standard uniform distribution) based on which the copula parameter vector is estimated.

3.2 Likelihood theory

Maximum-likelihood estimation is based on the following theory. Given realizations , , of a random sample , , from the copula (in practice, is taken as , , in (3)), the likelihood and log-likelihood are defined by

respectively, where

Here, the subscript of is used to stress the dependence of on . The maximum-likelihood estimator can thus be found by solving the optimization problem

This optimization is typically done numerically.

Assuming the derivatives to exist, the score function is defined as

and the Fisher information is

for .

Under regularity conditions (see Cox and Hinkley (1974, p. 281), Rohatgi (1976, pp. 384), Serfling (1980, pp. 144), Newey and McFadden (1994, p. 2146), Schervish (1995, p. 421), Lehmann and Casella (1998, p. 449), van der Vaart (2000, pp. 51), Bickel and Doksum (2000, p. 386), or Davison (2003, p. 118)), the following result holds.

Theorem 3.1

-

(1)

(Strong) consistency of maximum-likelihood estimators:

-

(2)

Asymptotic normality of maximum-likelihood estimators:

where denotes the identity matrix in .

3.3 Generator derivatives and copula density

Applying maximum-likelihood estimation requires an efficient strategy for evaluating the (log-)density of the parametric Archimedean copula family to be estimated. The most important part is to know how to access the generator derivatives. As mentioned in the introduction, this requires to know both a tractable algebraic form of the derivatives and a procedure to numerically evaluate the formulas in an efficient way in terms of precision and run time.

As mentioned in the introduction, it is often stated that a computer algebra system can be used to access a generator’s derivatives. Such an approach has typically two major flaws:

-

(1)

It is not trivial and sometimes not possible for a computer algebra system to find derivatives of higher order;

-

(2)

Even if formulas are obtained, they are usually not provided in a form which is both numerically stable and sufficiently fast to evaluate.

We experienced these flaws when we tried to access the 50th derivative of a Gumbel generator with parameter at . On a MacBook Pro running Max OS X 10.6.6, we aborted Mathematica 8 after ten minutes without obtaining a result. Maple 14 lead to the values 10 628, -29 800, and others (without warning) when computing several times. Note the chaotic behavior of this deterministic problem; the values should of course be equal and positive! MATLAB 7.11.0 did return the correct value of (roughly) 1057, but failed to access (aborted after ten minutes). Let us stress that carelessly using such programs in simulations may lead to wrong results. Apart from numerical issues, the formulas for the derivatives obtained from computer algebra systems can become quite large and thus rather slow to evaluate. They are therefore not suitable in large-scale simulation studies, for example, for goodness-of-fit tests (or simulations of their performance) involving a parametric bootstrap.

In the following theorem we derive explicit formulas for the generator derivatives for all Archimedean families given in Table 1.

Theorem 3.2

-

(1)

For the family of Ali-Mikhail-Haq,

where denotes the polylogarithm of order at .

-

(2)

For the family of Clayton,

where denotes the falling factorial.

-

(3)

For the family of Frank,

-

(4)

For the family of Gumbel,

where

and and denote the Stirling numbers of the first kind and the second kind, respectively.

-

(5)

For the family of Joe,

where

-

Proof

-

(1)

The generator of the Archimedean family of Ali-Mikhail-Haq is of the form , , with probability mass function as given in Table 1. This implies that from which the statement easily follows from the definition of the polylogarithm as .

-

(2)

The result for Clayton is straightforward to obtain by taking the derivatives.

-

(3)

Similar to (1).

-

(4)

Now consider Gumbel’s family. Writing the generator in terms of the exponential series and differentiating the summands, leads to , where . Since for , , one obtains . Note that is the th exponential polynomial and equals ; see Boyadzhiev (2009). With and noting that the summand for is zero, we obtain . Interchanging the order of summation leads to from which the result about directly follows. For the last equality in the statement about note that from which the result follows.

-

(5)

For Joe’s family, , , where . Letting , this equals . The operator is investigated in Boyadzhiev (2009). It follows from the results there that . Thus, . Resubstituting leads to the result as stated.

∎

-

(1)

With the notation as in Theorem 3.2, we obtain the following representations for the densities of the Archimedean families of Ali-Mikhail-Haq, Clayton, Frank, Gumbel, and Joe.

Corollary 3.3

-

(1)

For the family of Ali-Mikhail-Haq,

where .

-

(2)

For the family of Clayton,

-

(3)

For the family of Frank,

where .

-

(4)

For the family of Gumbel,

-

(5)

For the family of Joe,

where .

Remark 3.4

-

(1)

Recursive formulas for the generator derivatives for some Archimedean families were presented by Barbe et al. (1996) and Wu et al. (2007). In contrast, Theorem 3.2 provides explicit formulas. As seen from Corollary 3.3, this allows us to explicitly compute the densities of the corresponding well-known and widely used Archimedean families, even in large dimensions. Furthermore, it allows us to compute conditional distribution functions based on these families and important statistical quantities such as the Kendall distribution function, which is of interest, for example, in goodness-of-fit testing; see Genest et al. (2006), Genest et al. (2009), or Hering and Hofert (2011). Among others, note that extreme value copulas rarely have an explicit form of the density, the important Gumbel family can now be added to this list.

-

(2)

The derivatives presented in Theorem 3.2 also play an important role in asymmetric extensions of Archimedean copulas. For example, consider a Khoudraji-transformed Archimedean copula , given by

where denotes an Archimedean copula generated by , denotes the independence copula, and , , are parameters. Given the generator derivatives, the density of a Khoudraji-transformed Archimedean copula is given by

This makes maximum likelihood estimation for these copulas feasible; see Hofert and Vrins (2011) for an application.

-

(3)

As pointed out by Hofert (2010b, pp. 117), new Archimedean copulas are often constructed with simple transformations of the generators addressed in Theorem 3.2. The results in Theorem 3.2 might therefore carry over to other Archimedean families. In fact, one example for such a transformation is the outer power transformation addressed in Section 6.

-

(4)

For an Archimedean generator with unknown derivatives but known , Hofert et al. (2011) suggested to approximate via

where , , are realizations of i.i.d. random variables following . In the conducted simulation study, this approximation turned out to be quite accurate. Furthermore, it is typically straightforward to implement. However, such a Monte Carlo approach is of course slower than having a direct formula for the generator derivatives at hand.

4 Sample size vs dimension

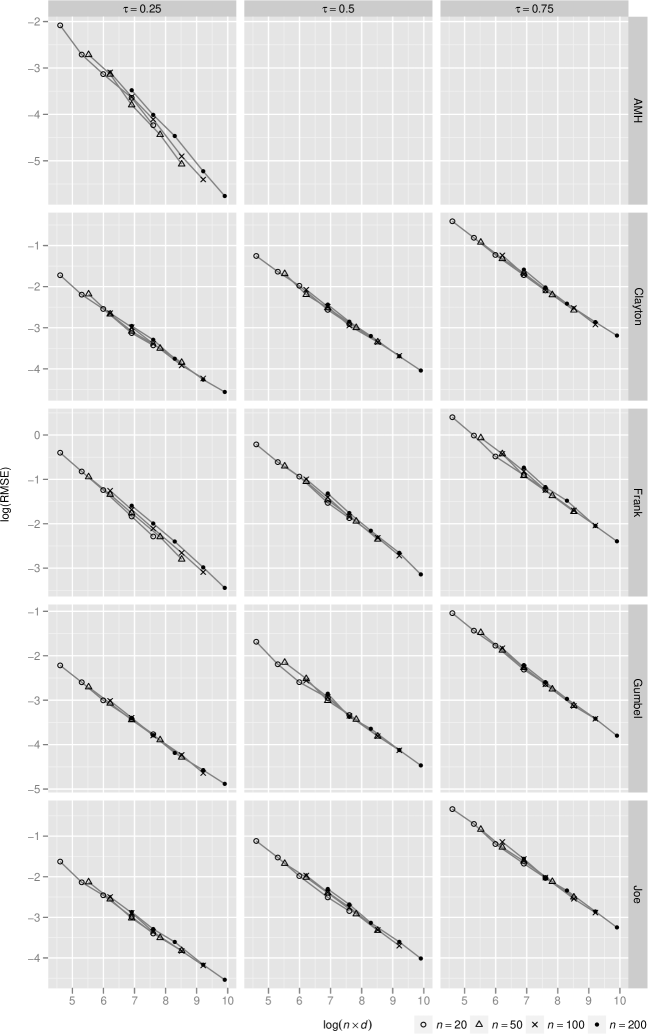

The results of Hofert et al. (2011) indicate that the root mean squared error (“RMSE”) is decreasing in the dimension for all other parameters (Archimedean family, dependence level measured by Kendall’s tau, and sample size) fixed. This may be intuitive for exchangeable copulas since the curse of dimensionality is circumvented by symmetry. In this section we briefly investigate how the RMSE decreases in the dimension. Figure 1 shows a clear picture. For fixed Archimedean family (Ali-Mikhail-Haq (“AMH”), Clayton, Frank, Gumbel, and Joe), dependence level measured by Kendall’s tau (), and sample size (), the RMSE (estimated based on replications) is decreasing in the dimension (). As the log-log plot further reveals, the decrease of the RMSE in the dimension is of the same order as in the sample size , that is, the mean squared error (“MSE”) satisfies

Although this behavior in the sample size is well-known, the behavior in the dimension is rather impressive since it contradicts the findings of Weiß (2010), for example. In the latter work, conclusions are drawn based on simulations only involving small dimensions. In small dimensions, however, numerical problems are often not (regarded) as severe as in larger dimensions. Sometimes, they are simply not solved correctly. However, according to our experience, we believe that the larger the dimension of interest is, the more involved numerical issues typically are. This will certainly become more important in the future as applications are often high-dimensional.

\setcapwidth

\setcapwidth

0.78

5 Constructing confidence intervals

In this section, we describe different ways of how to obtain confidence intervals for the copula parameter vector .

5.1 Fisher information

It follows from Theorem 3.1 (2) that

This result remains valid if is replace by a consistent estimator . Therefore, an asymptotic confidence region for is given by

where denotes the -quantile of the chi-square distribution with degrees of freedom. In the one-parameter case, an asymptotic confidence interval for is given by

where denotes the -quantile of the standard normal distribution function.

For the estimator , there are several options, described in what follows. Assuming the derivatives to exist, the observed information is defined as

Under regularity conditions (see the references in Section 3.2), the Fisher information satisfies

that is, the Fisher information is the negative Hessian of the score function. From this and the definition of the Fisher information, the following choices for naturally arise (see also Newey and McFadden (1994, pp. 2157) including conditions for consistency):

| (4) | ||||

| (5) | ||||

| (6) |

The expected information is often difficult to obtain. Furthermore, Efron and Hinkley (1978) argue for in favor of . The estimator is found much less in the literature, a reference being Newey and McFadden (1994, p. 2157). The reason why we state it here is that there are cases where the second-order partial derivatives are (much) more complicated to access than the first-order ones based on the score function.

The following proposition provides the score functions for the one-parameter Archimedean families given in Table 1.

Proposition 5.1

-

(1)

For the family of Ali-Mikhail-Haq,

where .

-

(2)

For the family of Clayton,

-

(3)

For the family of Frank,

-

(4)

For the family of Gumbel,

where and with .

-

(5)

For the family of Joe,

where and with .

-

Proof

The proof is quite tedious but straightforward to obtain from Corollary 3.3. ∎

5.2 Likelihood-based confidence intervals

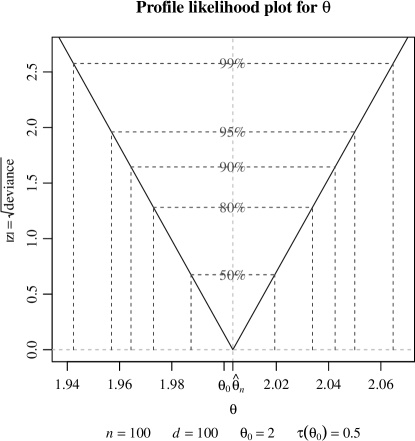

Confidence regions or confidence intervals can also be constructed solely based on the likelihood function (without requiring its derivatives). For this, the likelihood ratio statistic is used, defined as

As Davison (2003, p. 126) notes, the likelihood ratio statistic asymptotically follows a chi-square distribution, meaning that

Based on this result, an asymptotic confidence region for is given by

| (7) |

If only a sub-vector of components of are of interest ( and are referred to as parameters of interest and nuisance parameters, respectively), an asymptotic confidence region for follows from a similar argument to before, based on the profile log-likelihood

where is the maximum-likelihood estimator of given . Under regularity conditions, the generalized likelihood ratio statistic

satisfies

An asymptotic confidence region for is thus given by

where

This will be used in Section 6 to construct confidence intervals for multi-parameter families.

Example 5.2

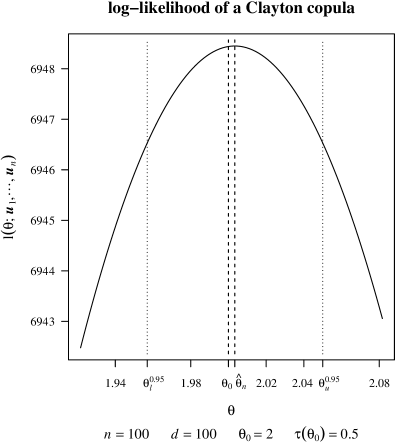

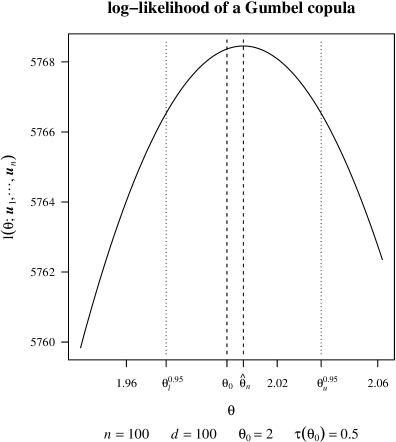

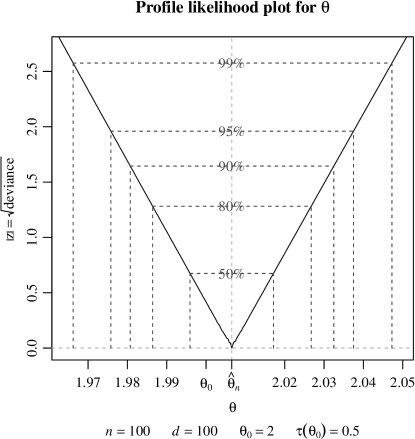

The left-hand side of Figure 2 shows the log-likelihood of a Clayton copula based on a 100-dimensional sample of size with parameter such that the corresponding bivariate population version of Kendall’s tau equals . The maximum-likelihood estimator is denoted by and the lower and upper endpoints of the likelihood-based 0.95 confidence interval by and , respectively. The right-hand side of Figure 2 shows the profile likelihood plot for the same sample. Similarly for Figure 3 which shows the log-likelihood and profile likelihood plot for the 100-dimensional Gumbel family with parameter such that Kendall’s tau equals .

\setcapwidth

\setcapwidth

\setcapwidth

\setcapwidth

5.3 A simulation study to access the coverage probability

In this section, we compare the different approaches for obtaining (asymptotic) confidence regions and intervals. For this, we conduct a simulation study to access the coverage probability. The methods for obtaining confidence intervals based on the Fisher information are denoted by “” for (4), “” for (5), and “” for (6); the likelihood-based approach (7) by “”.

As can be seen from Proposition 5.1, already the score functions can be quite complicated. In order to be able to investigate the method based on the observed information, we only consider the Clayton family, for which

with , that is, for which can be easily computed. Our simulation study is based on the sample sizes in the dimensions for the dependencies . For each of these setups and each of the methods , , , and , we determine the proportion of cases among replications for which the true parameter is contained in the computed confidence interval. Since the expected information is not known explicitly, we evaluate it by a Monte Carlo simulation based on samples of size .

Table 3 shows the results of the conducted simulation study. Overall, all methods work comparably well. Note that from a computational point of view, is preferred to if the latter has to be evaluated based on a Monte Carlo simulation. Furthermore, is typically difficult to evaluate, due to the complicated second order derivatives; the tractable Clayton family is certainly an exception. Even may be (numerically) challenging for some families, as Proposition 5.1 indicates. The likelihood based approach has several advantages. First, it is typically even simpler to evaluate than . Second, it may lead to asymmetric confidence intervals. Finally, by using a re-parameterization, it allows one to construct confidence intervals for quantities such as Kendall’s tau or the tail-dependence coefficients (otherwise often obtained from the Delta Method based on the approximate normal distribution).

| Coverage probabilities for Clayton (in %) | Method for obtaining confidence intervals | ||||||

|---|---|---|---|---|---|---|---|

6 Multi-parameter families

The one-parameter generators of Ali-Mikhail-Haq, Clayton, Frank, Gumbel, and Joe can easily be extended to allow for more parameters, for example, by so-called outer power transformations or even more general generator transformations; see Hofert (2010a), Hofert (2010b), or Hofert (2011a). In this section, we investigate an outer power Clayton copula and the Archimedean GIG family and apply maximum-likelihood estimation for estimating the copula parameters. Both of these families are available via the R package nacopula so that the interested reader can easily follow our calculations. The computations carried out in this section were run on a Mac mini under Mac OS X Version 10.6.6 with a 2.66 GHz Intel Core 2 Duo processor and 4 GB 1067 MHz DDR3 memory. The R version used is 2.12.1.

6.1 Finding initial intervals

Maximizing the log-likelihood is typically achieved by a numerical routine. These algorithms often require an initial interval (or an initial value, which can be derived from the former). This interval should be sufficiently large in order to contain the optimum, but also sufficiently small in order to find the optimum fast. Furthermore, one should be able to compute an initial interval in a small amount of time in comparison to the actual log-likelihood evaluations required for maximizing the log-likelihood.

For Archimedean families with , the measure of concordance Kendall’s tau is a function in which always maps to the unit interval; see, for example, Hofert (2010b, pp. 59). It thus provides an intuitive “distance” in terms of concordance. For one-parameter families, one can thus typically choose an initial interval of the form

where is suitably chosen with intuitive interpretation as “distance in concordance” and and denote lower and upper admissible Kendall’s tau for the families considered (in Example 5.2 we used this technique to find an interval on which the log-likelihood is plotted; we took as the correct value , and used and for Clayton’s and Gumbel’s family, respectively). If the dimension is not too large, one can take the mean of pairwise sample versions of Kendall’s tau as estimator of Kendall’s tau; see Berg (2009), Kojadinovic and Yan (2010), and Savu and Trede (2010) for this estimator. Another option is a multivariate version of Kendall’s tau; see Jaworski et al. (2010, pp. 217). A fast way, especially in large dimensions, is to utilize the explicit diagonal maximum-likelihood estimator

for Gumbel’s family, see Hofert et al. (2011), and estimate Kendall’s tau by , where denotes Kendall’s tau for Gumbel’s family as a function in the parameter. Since the optimization for one-parameter families is typically not too time-consuming, one can also just maximize the log-likelihood on a reasonably large, fixed interval, for example , where and are suitably chosen constants in the range of ; see Hofert et al. (2011).

For multi-parameter Archimedean families, the log-likelihood is typically even more challenging to evaluate. An initial interval therefore also serves the purpose of reducing the parameter space to an area where the log-likelihood can be evaluate without numerical problems. The idea we present here to construct initial intervals for multi-parameter families is again based on Kendall’s tau. In a first step, we estimate Kendall’s tau by . To this end we apply the pairwise Kendall’s tau estimator, which, due to the rather complicated log-likelihood evaluations does not take too much run time for the ten-dimensional examples considered below; another option would be to randomly select sub-columns of the data and apply the pairwise Kendall’s tau estimator to this sub-data in order to reduce run time. Based on this estimator of Kendall’s tau, we then construct an initial rectangle by three points. These points are determined via and , that is, via certain positive numbers and (sufficiently small to ensure that and are in the range of admissible Kendall’s tau). They allow for an intuitive interpretation as “distance in (terms of) concordance” and are independent of the parameterization of the family (since they measure distances in Kendall’s tau and not in the underlying copula parameters). Now note that is not uniquely defined for two- or more-parameter families. It is, however, if one fixes all but one parameter. By starting with one corner of the initial rectangle to be constructed and applying monotonicity properties of as a function in its parameters, one can thus construct an initial rectangle around the estimate of . More details are given in Sections 6.2 and 6.3 for the two-parameter Archimedean families investigated.

6.2 Outer power copulas

If , so is for all , since the composition of a completely monotone function with a non-negative function that has a completely monotone derivative is again completely monotone; see Feller (1971, p. 441). The copula family generated by is referred to as outer power family.

The generator derivatives of can be accessed with a formula about derivatives of compositions which dates back at least to Schlömilch (1846). According to this formula,

Via (2) and the form of given in Theorem 3.2 (4) one can thus easily derive the density of an outer power copula.

For sampling , Hofert (2011a) derived the stochastic representation

Note that can easily be sampled via the R package nacopula for all given in Table 1.

We consider the case where is Clayton’s generator, so we obtain the two-parameter outer power Clayton copula with generator . This copula, which generalizes the Clayton family, was successfully applied in Hofert and Scherer (2011) in the context of pricing collateralized debt obligations. For this copula, Kendall’s tau and the tail-dependence coefficients are given explicitly by

| (8) |

Note the possibility to have upper tail dependence for this copula, which is not possible for a Clayton copula.

The following algorithm describes a procedure for finding an initial interval for outer power Clayton copulas. The algorithm can easily be adapted to other outer power copulas, given that the base family (the family generated by ) is positively ordered in its parameter and admits a sufficiently large range of Kendall’s tau.

Algorithm 6.1

| (1) | Choose , and . |

| (2) | Let the smallest be denoted by . |

| (3) | Solve with respect to . |

| (4) | Solve with respect to . |

| (5) | Solve with respect to . |

| (6) | Return the initial interval . |

The idea behind Algorithm 6.1 is to construct an initial rectangle by three points. First, the lower-right endpoint of the rectangle is constructed. Since is an increasing function in both and , the largest and the smallest , that is, , are chosen such that Kendall’s tau equals plus a small “distance in concordance” to ensure that is indeed an upper bound for . The truncation done by is to obtain an admissible Kendall’s tau range. Second, the lower-left endpoint is found. The monotonicity of justifies determining the minimal value for such that , where is suitably chosen, similar to . In the third and final step, the upper-left endpoint of the initial rectangle is determined. The maximal value for is determined in a similar fashion to the first step. Note that all equations can be solved explicitly due to the explicit form of Kendall’s tau as given in (8).

To access the performance of the maximum-likelihood estimator, we generate times realizations of i.i.d. random vectors following -dimensional outer power Clayton copulas. For demonstration purposes, we consider . Furthermore, we consider three setups of dependencies: resulting in a Kendall’s tau of 0.25; with corresponding Kendall’s tau equal to 0.5; and with Kendall’s tau equal to 0.75. For finding initial intervals, Algorithm 6.1 is applied with , , and . The results are summarized in Table 4, where “RMSE” denotes the root mean squared error as before and “MUT” denotes the mean user time (in seconds).

| Bias | RMSE | Bias | RMSE | MUT | |||||

|---|---|---|---|---|---|---|---|---|---|

| 100 | |||||||||

| 100 | |||||||||

| 100 | |||||||||

| 500 | |||||||||

| 500 | |||||||||

| 500 | |||||||||

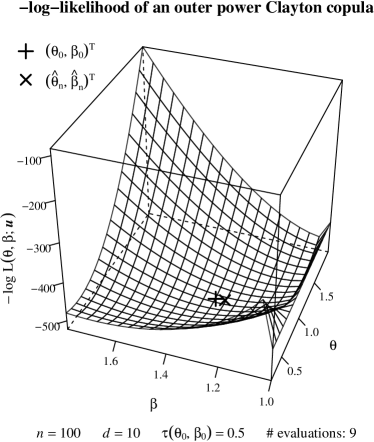

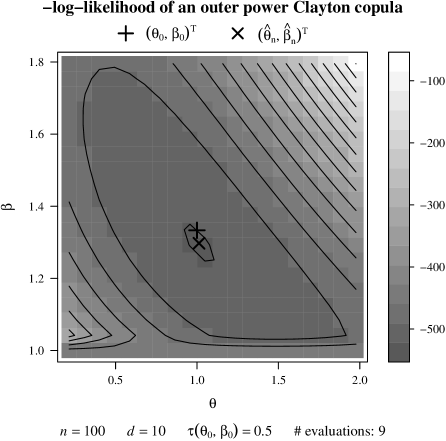

Figure 4 shows a wire-frame plot (left) of the negative log-likelihood of a sample of size for the setup () and the corresponding level plot (right). Both plots have the initial interval determined by Algorithm 6.1 as domain and show both the true value and the optimum as determined by the optimizer.

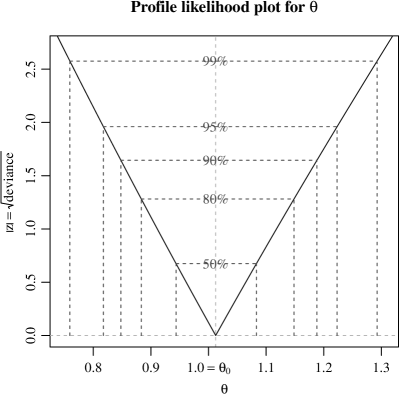

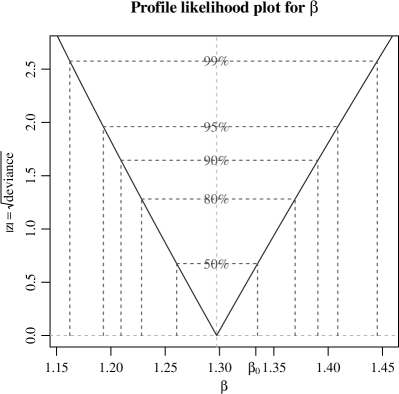

Figure 5 shows profile likelihood plots for the two parameters and .

\setcapwidth

\setcapwidth

6.3 The GIG family

An Archimedean family which naturally allows for two parameters can be constructed as follows. We start with the density of a generalized inverse Gaussian distribution , given by

Here, with: , , if ; , if ; and , , if ; see McNeil et al. (2005, p. 497). The function denotes the modified Bessel function of the third kind with parameter . It is decreasing in and symmetric about zero in . Furthermore, it is increasing in if . Another important property is

| (9) |

Note that for a , the generator generates the same Archimedean copula as for all . Letting and leads to a comparably simple form of the generator of an Archimedean GIG copula with parameter vector , given by

| (10) |

If we let

one obtains from (9) that for every and . Since can be written as , one obtains as limiting case a distribution for if , that is, a Clayton copula with parameter .

The density of is given by

so that with . The GIG distribution can easily be sampled with the R package Runuran. For numerically computing , note that for all and (see Paris (1984)), so that is an initial interval for searching for all .

Kendall’s tau and the coefficients of tail dependence of a GIG copula are given by

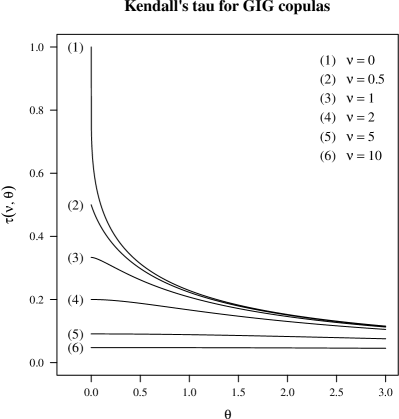

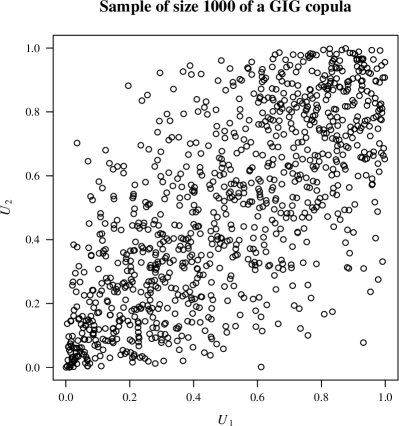

where , , , and . For computing the tail dependence coefficients, consider for the limits and , and use (valid for ) in the latter case. A numerically stable evaluation of the integral formula for Kendall’s tau for small based on the Clayton limit is given in the R package nacopula. Note that as numerical results indicate, Kendall’s tau is decreasing in both and if ; see Figure 6 (left). If , the limit for Kendall’s tau as is which equals Kendall’s tau for Clayton’s family with parameter . Figure 6 (right) shows a scatter plot of 1000 bivariate vectors of random variates following a GIG family with with corresponding Kendall’s tau equal to 0.5.

\setcapwidth

\setcapwidth

One advantage of the GIG family is that the generator derivatives take on a comparably simple form, which can be represented as

This can be easily derived by differentiating under the integral sign and interpreting the resulting integrand as the density of a distribution which integrates to one. Via (2), one then easily finds the form of the log-density of a GIG family, given by

The following algorithm describes a procedure for finding an initial interval for GIG copulas with . The idea behind this algorithm is similarly to those of Algorithm 6.1. However, it takes into account that is decreasing in both parameters and and thus first determines the upper-left, then the lower-left, and finally the lower-right endpoint of the initial rectangle. As before, denotes an estimator of Kendall’s tau, taken as the pairwise Kendall’s tau estimator. Note that for , the range of Kendall’s tau as a function in is ; see Figure 6 (left). Furthermore, for sufficiently small, the range of Kendall’s tau as a function in is .

Algorithm 6.2

| (1) | Choose , and . |

| (2) | Let the smallest be denoted by . |

| (3) | Solve with respect to . |

| (4) | Solve with respect to . |

| (5) | Solve with respect to . |

| (6) | Return the initial interval . |

We generate times realizations of i.i.d. random vectors in dimensions following GIG copulas with parameters resulting in a Kendall’s tau of 0.25, with corresponding Kendall’s tau equal to 0.5, and with Kendall’s tau equal to 0.75 (the choice of is made solely to the larger run time for this family). For finding initial intervals, Algorithm 6.2 is applied with and . The results are summarized in Table 5. Note that especially under weak concordance, the GIG family requires a larger sample size in order for the bias to be small.

| Bias | RMSE | Bias | RMSE | MUT | |||||

|---|---|---|---|---|---|---|---|---|---|

| 100 | |||||||||

| 100 | |||||||||

| 100 | |||||||||

| 500 | |||||||||

| 500 | |||||||||

| 500 | |||||||||

7 Conclusion

We presented explicit functional forms for the generator derivatives of well-known Archimedean copulas. These explicit formulas are of interest for several reasons. Apart from being able to express various important quantities such as conditional distributions or the Kendall distribution function explicitly, the generator derivatives allow us to apply maximum-likelihood estimation for estimating the parameter vectors of various Archimedean copulas, even in large dimensions such as . The excellent performance in terms of both precision and run time of maximum likelihood estimation was shown in Hofert et al. (2011) in a large-scale comparison with various other estimators up to dimension . In the present work, we presented the theoretical details and showed that maximum-likelihood estimation is also feasible for multi-parameter Archimedean families. Furthermore, we showed that the mean squared error MSE is decreasing in the dimension and that this decrease is of the same order as the decrease in the sample size , that is, . We also constructed initial intervals for the likelihood optimization. Moreover, we obtained likelihood-based confidence intervals for the parameter vector and compared them to information-based confidence intervals for the Clayton family where the Fisher information is comparably easy to compute. A transparent implementation of the presented results is given in the open source R package nacopula, so that the interested reader can easily follow our calculations.

Acknowledgements

The authors would like to thank Khristo Boyadzhiev (Ohio Northern University) for introducing us to and guiding us through the fascinating world of exponential polynomials.

References

- Barbe et al. (1996) P. Barbe, C. Genest, K. Ghoudi, and B. Rémillard. On Kendall’s Process. Journal of Multivariate Analysis, 58:197–229, 1996.

- Berg (2009) D. Berg. Copula goodness-of-fit testing: an overview and power comparison. The European Journal of Finance, 2009. URL http://www.informaworld.com/10.1080/13518470802697428.

- Berg and Aas (2009) D. Berg and K. Aas. Models for construction of multivariate dependence – A comparison study. The European Journal of Finance, 15(7):639–659, 2009.

- Bickel and Doksum (2000) P. J. Bickel and K. A. Doksum. Copula Theory and Its Applications. Prentice Hall, 2 edition, 2000.

- Boyadzhiev (2009) K. N. Boyadzhiev. Exponential Polynomials, Stirling Numbers, and Evaluation of Some Gamma Integrals. Abstract and Applied Analysis, 2009, 2009.

- Cox and Hinkley (1974) D. R. Cox and D. V. Hinkley. Theoretical Statistics. Chapman and Hall, 1974.

- Davison (2003) A. C. Davison. Statistical Models. Cambridge Series in Statistical and Probabilistic Mathematics, 2003.

- Efron and Hinkley (1978) B. Efron and D. V. Hinkley. Assessing the accuracy of the maximum likelihood estimator: Observed versus expected Fisher information. Biometrika, 65(3):457–487, 1978.

- Embrechts and Hofert (2011) P. Embrechts and M. Hofert. On Archimedean copulas and a non-parametric estimation method. TEST, 2011. 10.1007/s11749-011-0252-4. in press.

- Feller (1971) W. Feller. An Introduction to Probability Theory and Its Applications, volume 2. Wiley, 2 edition, 1971.

- Genest et al. (1995) C. Genest, K. Ghoudi, and L.-P. Rivest. A semiparametric estimation procedure of dependence parameters in multivariate families of distributions. Biometrika, 82(3):543–552, 1995.

- Genest et al. (2006) C. Genest, J. F. Quessy, and B. Rémillard. Goodness-of-fit procedures for copula models based on the probability integral transformation. Scandinavian Journal of Statistics, 33:337–366, 2006.

- Genest et al. (2009) C. Genest, B. Rémillard, and D. Beaudoin. Goodness-of-fit tests for copulas: A review and a power study. Insurance: Mathematics and Economics, 44:199–213, 2009.

- Hering and Hofert (2011) C. Hering and M. Hofert. Goodness-of-fit tests for Archimedean copulas in large dimensions. 2011. submitted.

- Hofert (2010a) M. Hofert. Construction and sampling of nested Archimedean copulas. In F. Durante, W. Härdle, P. Jaworski, and T. Rychlik, editors, Copula Theory and Its Applications, Proceedings of the Workshop held in Warsaw 25-26 September 2009, pages 147–160. Springer, 2010a. 10.1007/978-3-642-12465-5_7.

- Hofert (2010b) M. Hofert. Sampling Nested Archimedean Copulas with Applications to CDO Pricing. Südwestdeutscher Verlag für Hochschulschriften AG & Co. KG, 2010b. ISBN 978-3-8381-1656-3. PhD thesis.

- Hofert (2011a) M. Hofert. Efficiently sampling nested Archimedean copulas. Computational Statistics & Data Analysis, 55:57–70, 2011a. 10.1016/j.csda.2010.04.025.

- Hofert (2011b) M. Hofert. A stochastic representation and sampling algorithm for nested Archimedean copulas. Journal of Statistical Computation and Simulation, 2011b. 10.1080/00949655.2011.574632. in press.

- Hofert and Scherer (2011) M. Hofert and M. Scherer. CDO pricing with nested Archimedean copulas. Quantitative Finance, 11(5):775–787, 2011. 10.1080/14697680903508479.

- Hofert and Vrins (2011) M. Hofert and F. Vrins. Sibuya copulas. 2011. in progress, early version: http://arxiv.org/pdf/1008.2292.

- Hofert et al. (2011) M. Hofert, M. Mächler, and A. J. McNeil. Estimators for Archimedean copulas in high dimensions: A comparison. 2011. in progress.

- Jaworski et al. (2010) P. Jaworski, F. Durante, W. K. Härdle, and T. Rychlik, editors. Copula Theory and Its Applications, volume 198 of Lecture Notes in Statistics – Proceedings. Springer, 2010.

- Joe (1997) H. Joe. Multivariate Models and Dependence Concepts. Chapman & Hall/CRC, 1997.

- Joe and Hu (1996) H. Joe and T. Hu. Multivariate Distributions from Mixtures of Max-Infinitely Divisible Distributions. Journal of Multivariate Analysis, 57:240–265, 1996.

- Joe and Xu (1996) H. Joe and J. J. Xu. The Estimation Method of Inference Functions for Margins for Multivariate Models. Technical Report no. 166, Department of Statistics, University of British Columbia, 1996.

- Kim et al. (2007) G. Kim, M. J. Silvapulle, and P. Silvapulle. Comparison of semiparametric and parametric methods for estimating copulas. Computational Statistics & Data Analysis, 51:2836–2850, 2007.

- Kojadinovic and Yan (2010) I. Kojadinovic and J. Yan. Modeling Multivariate Distributions with Continuous Margins Using the copula R Package. Journal of Statistical Software, 34(9):1–20, 2010.

- Lehmann and Casella (1998) E. L. Lehmann and G. Casella. Theory of Point Estimation. Springer, 2 edition, 1998.

- McNeil and Nešlehová (2009) A. J. McNeil and J. Nešlehová. Multivariate Archimedean copulas, -monotone functions and -norm symmetric distributions. The Annals of Statistics, 37(5b):3059–3097, 2009.

- McNeil et al. (2005) A. J. McNeil, R. Frey, and P. Embrechts. Quantitative Risk Management: Concepts, Techniques, Tools. Princeton University Press, 2005.

- Nelsen (2007) R. B. Nelsen. An Introduction to Copulas. Springer, 2007.

- Newey and McFadden (1994) W. K. Newey and D. McFadden. Large sample estimation and hypothesis testing. In R. F. Engle and D. L. McFadden, editors, Handbook of Econometrics, pages 2111–2245. Elsevier North Holland, 1994.

- Paris (1984) R. B. Paris. An inequality for the Bessel function . SIAM Journal on Mathematical Analysis, 15(1):203–205, 1984.

- Rohatgi (1976) V. K. Rohatgi. An introduction to probability theory and mathematical statistics. Wiley, 1976.

- Savu and Trede (2010) C. Savu and M. Trede. Hierarchies of Archimedean copulas. Quantitative Finance, 10(3):295–304, 2010.

- Schervish (1995) M. J. Schervish. Theory of Statistics. Springer, 1995.

- Schlömilch (1846) O. Schlömilch. Allgemeine Sätze für eine Theorie der höheren Differential-Quotienten. Archiv der Mathematik und Physik, 7:204–214, 1846.

- Serfling (1980) R. J. Serfling. Approximation Theorems Of Mathematical Statistics . Wiley-Interscience, 1980.

- Shi (1995) D. Shi. Fisher information for a multivariate extreme value distribution. Biometrika, 82(3):644–649, 1995.

- van der Vaart (2000) A. W. van der Vaart. Asymptotic Statistics. Cambridge University Press, 2000.

- Weiß (2010) G. N. F. Weiß. Copula parameter estimation: numerical considerations and implications for risk management. The Journal of Risk, 13(1):17–53, 2010.

- Wu et al. (2007) F. Wu, E. A. Valdez, and M. Sherris. Simulating Exchangeable Multivariate Archimedean Copulas and its Applications. Communications in Statistics – Simulation and Computation, 36(5):1019–1034, 2007.