Losing money with a high Sharpe ratio

Abstract

A simple example shows that losing all money is compatible with a very high Sharpe ratio (as computed after losing all money). However, the only way that the Sharpe ratio can be high while losing money is that there is a period in which all or almost all money is lost. This note explores the best achievable Sharpe and Sortino ratios for investors who lose money but whose one-period returns are bounded below (or both below and above) by a known constant.

1 Introduction

Sharpe ratio [2, 3] has become a “gold standard” for measuring performance of hedge funds and other institutional investors (this note uses the generic term “portfolio”). It is sometimes argued that it is applicable only to i.i.d. Gaussian returns, but we will follow a common practice of ignoring such assumptions. For simplicity we assume that the benchmark return (such as the risk-free rate) is zero.

The (ex post) Sharpe ratio of a sequence of returns is defined as , where

(None of our results will be affected if we replace, assuming , by , as in [3], (6).) Intuitively, the Sharpe ratio is the return per unit of risk.

Another way of measuring the performance of a portfolio whose sequence of returns is is to see how this sequence of returns would have affected an initial investment of 1 assuming no capital inflows and outflows after the initial investment. The final capital resulting from this sequence of returns is . We are interested in conditions under which the following anomaly is possible: the Sharpe ratio is large while . (More generally, if we did not assume zero benchmark returns, we would replace by the condition that in the absence of capital inflows and outflows the returns underperform the benchmark portfolio.)

Suppose the return is over periods, and then it is in the th period. As , and . Therefore, making large enough, we can make the Sharpe ratio as large as we want, despite losing all the money over the periods.

If we want the sequence of returns to be i.i.d., let the return in each period be with probability and with probability , for a large enough . With probability one the Sharpe ratio will tend to a large number as , despite all money being regularly lost. Of course, in this example the returns are far from being Gaussian (strictly speaking, returns cannot be Gaussian unless they are constant, since they are bounded from below by ).

2 Upper bound on the Sharpe ratio for losers

The examples of the previous section are somewhat unrealistic in that there is a period in which the portfolio loses almost all its money. In this section we show that only in this way a high Sharpe ratio can become compatible with losing money.

For each , define

| (1) |

where ranges over the positive integers and over . In other words, is the best achievable Sharpe ratio for sequences of returns that lose money, assuming that none of the returns falls below .

It is not difficult to show that , and in the previous section we saw that . In this section we are interested in the behaviour of for the intermediate values of , .

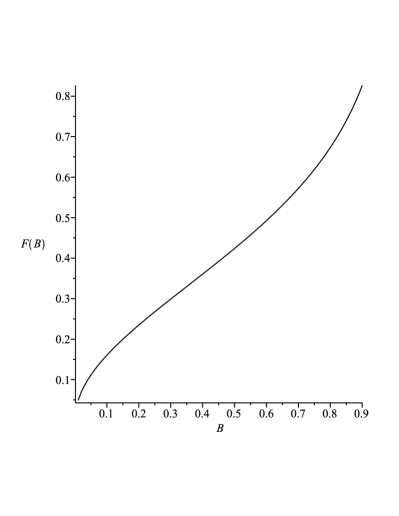

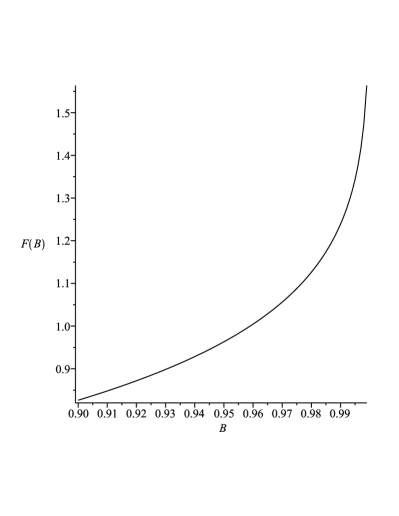

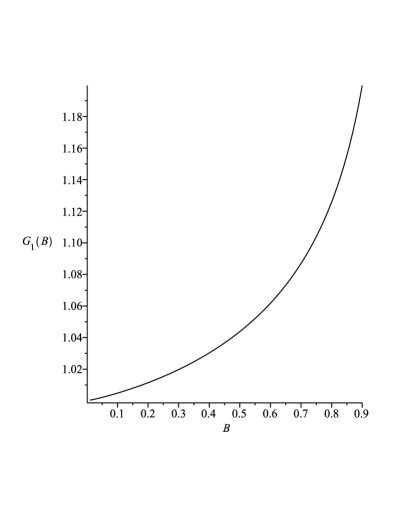

Figure 1 shows the graph of over and over . Over the interval the slope of is roughly 1. We can see that even for a relatively large value of , the Sharpe ratio of a losing portfolio never exceeds 0.5; according to Table 1, (much less than the conventional threshold of 1 for a good Sharpe ratio [1]).

| 0.1 | 0.160 | 10.49 | 0.041 | 0.8 | 0.673 | 6.37 | 0.446 |

|---|---|---|---|---|---|---|---|

| 0.2 | 0.235 | 10.00 | 0.085 | 0.9 | 0.826 | 5.42 | 0.553 |

| 0.3 | 0.299 | 9.50 | 0.132 | 0.99 | 1.239 | 3.90 | 0.743 |

| 0.4 | 0.361 | 8.97 | 0.182 | 0.999 | 1.564 | 3.35 | 0.824 |

| 0.5 | 0.424 | 8.40 | 0.236 | 0.9999 | 1.836 | 3.10 | 0.867 |

| 0.6 | 0.493 | 7.80 | 0.296 | 0.99999 | 2.075 | 2.96 | 0.893 |

| 0.7 | 0.572 | 7.13 | 0.365 | 0.999999 | 2.289 | 2.88 | 0.911 |

Table 1 gives approximate numerical values of for selected . These approximate values are attained for sequences of returns involving only two levels of returns: and another level . The table also lists the value of and the fraction of returns equal to at which the given approximate value of is attained.

| 0.1 | 0.050 | 0.525 | 0.4 | 0.210 | 0.603 |

|---|---|---|---|---|---|

| 0.2 | 0.101 | 0.550 | 0.5 | 0.271 | 0.631 |

| 0.3 | 0.154 | 0.576 | 0.6 | 0.340 | 0.661 |

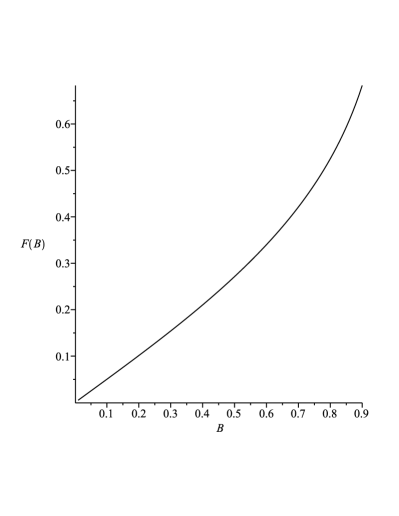

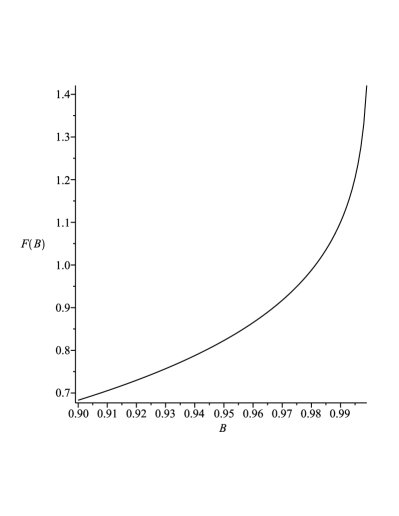

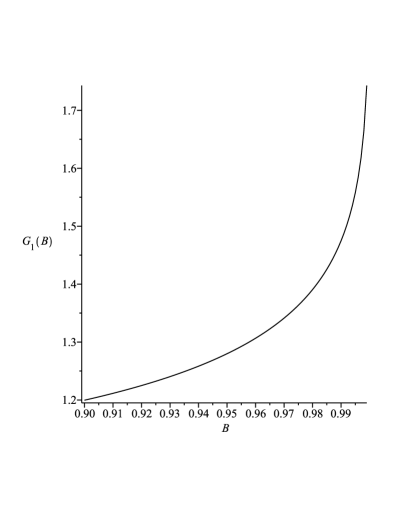

A striking feature of Table 1 is the values of : they exceed even for . The value of corresponding to in Table 1 means that the portfolio increases its value 11-fold in one period. Figure 2 is analogous to Figure 1 but imposes the upper bound of on the absolute values of one-period returns. Namely, it plots the graph of the function which is defined by the same formula (1) as but with now ranging over . An abridged analogue of Table 1 for is given as Table 2; the latter does not give the value of as it is equal to in all the entries. Not surprisingly are not so different from in Table 2, especially for smaller .

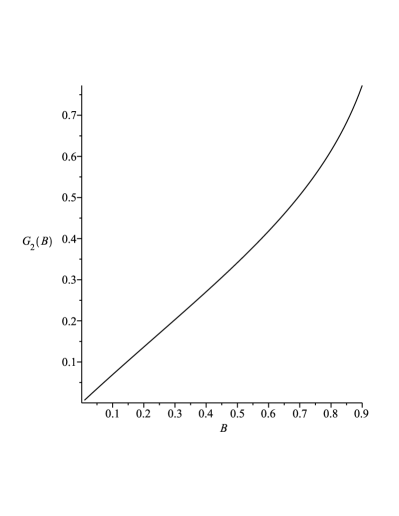

The analogues of Figures 1 and 2 for the Sortino ratio are Figures 3 (one-sided) and 4 (two-sided). The function of Figure 3 is defined, in analogy with (1), by

| (2) |

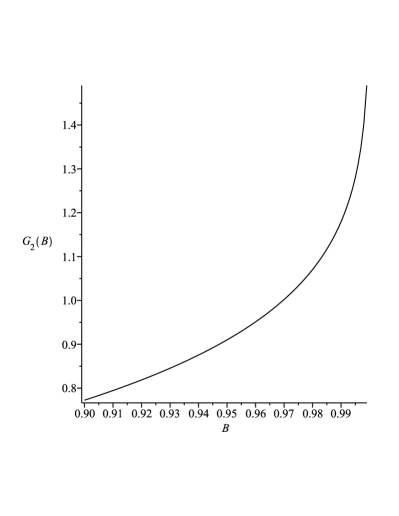

where ranges over the positive integers and over . The function of Figure 4 is defined as the right-hand side of (2) but with ranging over .

| 0.1 | 1.005 | 0.011 | 0.1 | 0.069 | 0.525 |

|---|---|---|---|---|---|

| 0.2 | 1.011 | 0.026 | 0.2 | 0.136 | 0.550 |

| 0.3 | 1.020 | 0.045 | 0.3 | 0.203 | 0.576 |

| 0.4 | 1.030 | 0.069 | 0.4 | 0.271 | 0.603 |

| 0.5 | 1.044 | 0.099 | 0.5 | 0.341 | 0.631 |

| 0.6 | 1.062 | 0.137 | 0.6 | 0.418 | 0.661 |

The values of and for selected are shown in Table 3, on the left and on the right. The meaning of is the same as in Tables 1 and 2. We do not give the values of ; they are huge on the left-hand side of the table and equal to on the right-hand side. The left-hand side suggests that , and this can be verified analytically.

3 Discussion

Figures 1–4 can be regarded as a sanity check for the Sharpe and Sortino ratio. Not surprisingly, they survive it, despite the theoretical possibility of having a high Sharpe and, a fortiori, Sortino ratio while losing money. In the case of the Sharpe ratio, such an abnormal behaviour can happen only when some one-period returns are very close to . In the case of the Sortino ratio, such an abnormal behaviour can happen only when some one-period returns are very close to or when some one-period returns are huge.

Acknowledgements

I am grateful to Boris Afanasiev for his advice and to Wouter Koolen for useful comments. All computations for this note were done in Maple.

References

- [1] Investopedia. Understanding the Sharpe ratio, July 2010.

- [2] William F. Sharpe. Mutual fund performance. Journal of Business, 39:119–138, 1966.

- [3] William F. Sharpe. The Sharpe ratio. Journal of Portfolio Management, 49:49–58, 1994.

- [4] Frank A. Sortino and Lee N. Price. Performance measurement in a downside risk framework. Journal of Investing, 3:59–64, 1994.

- [5] Frank A. Sortino and Robert van der Meer. Downside risk. Journal of Portfolio Management, 17:27–31, 1991.