=0

Large Portfolio Asymptotics for Loss From Default

Abstract.

We prove a law of large numbers for the loss from default and use it for approximating the distribution of the loss from default in large, potentially heterogenous portfolios. The density of the limiting measure is shown to solve a non-linear stochastic PDE, and certain moments of the limiting measure are shown to satisfy an infinite system of SDEs. The solution to this system leads to the distribution of the limiting portfolio loss, which we propose as an approximation to the loss distribution for a large portfolio. Numerical tests illustrate the accuracy of the approximation, and highlight its computational advantages over a direct Monte Carlo simulation of the original stochastic system.

Mathematical Finance, forthcoming

1. Introduction

Reduced-form point process models of correlated default timing are widely used to measure portfolio credit risk and to value securities exposed to correlated default risk. Computing the distribution of the loss from default in these models tends to be difficult, however, especially in bottom-up formulations with many names. Semi-analytical transform methods have limited scope. Monte Carlo simulation is much more broadly applicable but can be slow for the large portfolios and longer time horizons common in practice.

This paper develops an approximation to the distribution of the loss from default in large portfolios that may have a heterogenous structure. The approximation is valid for a class of reduced-form models in which a name defaults at a stochastic intensity that is influenced by an idiosyncratic risk factor process, a systematic risk factor process common to all names in the pool, and the portfolio loss rate. It is based on a law of large numbers for the portfolio loss rate. The limiting portfolio loss is not deterministic but follows a stochastic process driven by , indicating that the exposure to the systematic risk cannot be diversified. We show that the density of the limiting measure, if it exists, satisfies a nonlinear stochastic partial differential equation (SPDE) driven by . We develop a numerical method for solving this equation. The method is based on the observation that certain moments of the limiting measure satisfy an infinite system of SDEs. These SDEs are driven by the systematic risk factor ; a truncated system can be solved using a discretization scheme, for example. The solution to the SDE system leads to the solution to the SPDE through an inverse moment problem. It also leads to the distribution of the limiting portfolio loss, which we propose as an approximation to the distribution of the loss from default for a large portfolio. Estimators of portfolio value at risk and other risk measures are immediate from the limiting loss distribution.

Numerical tests illustrate the accuracy and computational efficiency of the approximation for large but finite portfolios. We find a substantial reduction in computational effort over the alternative of direct Monte Carlo simulation of the high-dimensional original stochastic system. The accuracy of the approximation mainly depends on the portfolio size and the sensitivity to the systematic risk factor. For a given sensitivity, the accuracy increases with , as expected. The higher the sensitivity to the systematic risk, the higher the variance of the loss distribution and the more accurate is the approximation for fixed . The approximation is remarkably accurate in the tail of the loss distribution. This renders it particularly suitable for the estimation of risk measures for the large pools of loans commonly held by banks.

Large portfolio approximations were first studied by \citeasnounvasicek. In Vasicek’s static model of a homogenous pool, firms default independently of one another conditional on a normally distributed random variable representing a systematic risk factor. Because the losses from defaults are conditionally i.i.d., the classical law of large numbers ensures the convergence of the portfolio loss rate to its conditional mean, from which the limiting loss distribution is immediate. \citeasnounschloegl-okane examine alternative distributions of the systematic factor, and \citeasnounlucas-etal and \citeasnounGordy03arisk-factor study the limiting loss in a heterogenous portfolio. \citeasnounhambly analyze a dynamic extension of Vasicek’s homogeneous pool model in which the systematic risk factor follows a Brownian motion. They obtain an SPDE driven by that Brownian motion for the density of the limiting measure, which they solve using a finite element method. The conditional independence of defaults can also be exploited to analyze the tail behavior of the losses in large, not necessarily homogenous, portfolios using large deviations arguments; see \citeasnounddd and \citeasnounglasserman-kang.

The analysis in this paper differs from that in the aforementioned articles in several important respects. We study a class of dynamic point process models of correlated default timing in which a firm defaults at a stochastic intensity process. The intensity is influenced by an idiosyncratic risk factor process following a square-root diffusion, a systematic risk factor process following a diffusion with arbitrary coefficient functions, and the portfolio loss rate. To address the heterogeneity of a portfolio, the intensity parameters of each name are allowed to be different. The choice for dependence of the intensity on idiosyncratic and systematic risk factor processes is motivated by the empirical findings of \citeasnounduffie-saita-wang. The choice for dependence of the intensity on the portfolio loss is motivated by the empirical results of \citeasnounazizpour-giesecke-schwenkler, who find that defaults have a statistically significant feedback effect on the surviving firms. The self-exciting behavior of defaults violates the conditional independence property that is exploited in the aforementioned articles. It complicates the asymptotic analysis and induces an integral term in the drift of the SPDE governing the density of the limiting measure. The exposure to the systematic risk leads to the noise term in the SPDE, which is given by an Itô integral against the Brownian motion driving the systematic risk diffusion. The solution to the SPDE governs the distribution of the limiting loss at all future horizons, facilitating the computation of the “loss surface.” This dynamic perspective is absent in the static formulations considered in most of the aforementioned articles.

The law of large numbers (LLN) proved in this paper significantly extends an earlier result in \citeasnounGieseckeSpiliopoulosSowers2011, which assumes Ornstein-Uhlenbeck dynamics for the systematic risk factor and the sensitivity of the intensity to the systematic risk to vanish in the large-portfolio limit. The LLN developed here allows for general diffusion dynamics for the systematic risk factor. Moreover, the exposure of an intensity to this diffusion is not required to vanish, generating a much richer, non-deterministic limiting behavior governed by an SPDE rather than a PDE. The treatment of these features requires additional arguments. Our main result (Theorem 3.1) develops the stochastic evolution equation that the limiting empirical measure satisfies. If the limiting empirical measure admits a density, then an integration by parts argument shows that the density satisfies an SPDE. The filtered martingale problem is used to identify the limit and prove the LLN. A major difficulty in the identification of the limit is the solution of a coupled system of SDEs, which we address using fixed-point arguments. In contrast to \citeasnounGieseckeSpiliopoulosSowers2011, this system does not easily decouple in the more general setting considered here. The analysis of the fixed-point arguments is complicated due to the square-root singularity.

CMZ prove a LLN for a related system, taking an intensity as a function of an idiosyncratic risk factor, a systematic risk factor, and the portfolio loss rate. The risk factors follow diffusion processes whose coefficients may depend on the portfolio loss. In that formulation, the impact of a default on the dynamics of the surviving firms is permanent. In our work, an intensity depends on the path of the portfolio loss. Therefore, the impact of a default on the surviving firms may be transient and fade away with time. There is a recovery effect. Other interacting particle systems with permanent default impact are analyzed by \citeasnoundaipra-etal and \citeasnoundaipra-tolotti, who take an intensity as a function of the portfolio loss rate. In a model with local interaction, \citeasnoungiesecke-weber take the intensity of a name as a function of the state of the names in a specified neighborhood of that name. These papers prove LLNs for the portfolio loss and develop Gaussian approximations to the portfolio loss distribution based on central limit theorems. The interacting particle system which we propose and study includes firm-specific sources of default risk and addresses an additional source of default clustering, namely the exposure of a firm to a systematic risk factor process. This exposure generates a random limiting behavior.

There are several other related articles. \citeasnoundavis-rod develop large portfolio approximations based on a law of large numbers and a central limit theorem in a stochastic network setting, in which firms default independently of one another conditional on the realization of a systematic factor governed by a finite state Markov chain. \citeasnounsircar-zari examine large portfolio asymptotics for utility indifference valuation of securities exposed to the losses in the pool. Our formulation addresses the dependence of the intensity on a systematic diffusion factor and the portfolio loss. It allows for self-exciting effects that violate the conditional independence assumption. Gaussian and large deviation approximations to the distribution of portfolio losses for an affine point process system with features similar to those of our, not necessarily affine, system are provided by \citeasnounzhang-etal. Their asymptotic analysis is based on a “large horizon” rather than a “large portfolio” regime considered here and in the aforementioned articles. The scope of their approximations differs from that of ours.

The rest of the paper is organized as follows. Section 2 describes a class of point process models of correlated default timing in a pool of names. Section 3 states our main result, Theorem 3.1, a law of large numbers for the loss rate in the pool. Section 4 provides further insights into the limiting behavior of the loss for the special case of a homogenous pool. Section 5 develops, implements and tests a moment method for the numerical solution of the SPDE. Numerical results illustrate the method and demonstrate the accuracy of the approximation of the portfolio loss by the limiting loss. Section 6 discusses the extension of our results to more general intensity dynamics. Sections 7 and 8 are devoted to the proof of Theorem 3.1. Appendices provide auxiliary results.

2. Model and Assumptions

We provide a dynamic point process model of correlated default timing in a portfolio of names. We assume that is an underlying probability space on which all random variables are defined. Let be a countable collection of independent standard Brownian motions. Let be an i.i.d. collection of standard exponential random variables which are independent of the ’s. Finally, let be a standard Brownian motion which is independent of the ’s and ’s. Each will represent a source of risk which is idiosyncratic to a specific name. Each will represent a normalized default time for a specific name. The process will drive a systematic risk factor process to which all names are exposed. Define and , where contains the -null sets.

Fix , and consider the following system:

| (1) | ||||

Here, is the indicator function. The initial condition of is fixed. The are constant parameters, for each and . We discuss their meaning below. The description of is equivalent to a more standard construction. In particular, define

| (2) |

Then and consequently

| (3) |

The process represents the loss rate in a portfolio of names, assuming a loss given default of one unit. The process represents the intensity, or conditional event rate, of the -th name in the pool. More precisely, is the density of the Doob-Meyer compensator to the default indicator ; see (6). The results in Section 3 of \citeasnounGieseckeSpiliopoulosSowers2011 imply that the system (1) has a unique solution such that for every , and . Thus, the model is well-posed.

The jump-diffusion intensity model (1) is empirically motivated. It addresses several channels of default clustering. An intensity is driven by an idiosyncratic source of risk represented by a Brownian motion , and a source of systematic risk common to all firms–the diffusion process . Movements in cause correlated changes in firms’ intensities and thus provide a channel for default clustering emphasized by \citeasnounddk for corporate defaults in the U.S. The sensitivity of to changes in is measured by the parameter . The second channel for default clustering is modeled through the feedback (“contagion”) term . A default causes a jump of size in the intensity , where . Due to the mean-reversion of , the impact of a default fades away with time, exponentially with rate . \citeasnounazizpour-giesecke-schwenkler have found self-exciting effects of this type to be an important channel for the clustering of defaults in the U.S., over and above any clustering caused by the exposure of firms to systematic risk factors. \citeasnoungiesecke-schwenkler develop and analyze likelihood estimators of the parameters of point process models such as (1).

We allow for a heterogeneous pool; the intensity dynamics of each name can be different. We capture these different dynamics by defining the “types”

| (4) |

the ’s take values in parameter space . In order to expect regular macroscopic behavior of as , the ’s and the ’s should have enough regularity as . For each , define

these are elements of and respectively111As usual, if is a topological space, is the collection of Borel probability measures on ..

We require three main conditions. These conditions are in force throughout the paper, even though this may not always be stated explicitly. Firstly, we assume that the types of (4) and the initial distributions (the ’s) are sufficiently regular.

Condition 2.1.

and exist (in and , respectively).

We also require that the ’s and ’s all (uniformly in ) have compact support. We could relax this requirement, at the cost of a much more careful error analysis.

Condition 2.2.

There is a such that the ’s, ’s, ’s, ’s, ’s, and ’s are all bounded by for all and .

Regarding the systematic risk process , we assume

Condition 2.3.

The functions and that govern the systematic risk diffusion are such that the corresponding SDE has a unique strong solution. Moreover, there is a function such that and for every we have

| (5) |

The Novikov condition (5) may not be necessary. Lemma 8.2 is the key step for the proof of a law of large numbers for the loss rate in the system (1), which is stated as Theorem 3.1 below. Its proof is based on a fixed point argument and uses Girsanov’s theorem; this is where (5) is required.222If condition (5) is required to hold only for some , then the statement of Theorem 3.1 below will hold for instead of .

Our basic formulation significantly extends that of \citeasnounGieseckeSpiliopoulosSowers2011. First, we allow the systematic risk to follow a general diffusion process with coefficients satisfying Condition 2.3 rather than a simple Ornstein-Uhlenbeck process. Second, we no longer require the exposure to the systematic risk, , to vanish in the limit as . This implies a richer, non-deterministic limiting behavior. The analysis of this behavior is more challenging and requires new arguments.

Section 6 discusses further extensions of our basic formulation, including stochastic position losses and more general intensity dynamics.

3. Law of Large Numbers

We develop a law of large numbers for the portfolio loss rate in the system (1). To this end, we need to understand a system which contains a bit more information than the loss rate . For each and , define

| (6) |

(where is as in (2)). In other words, if and only if the -th name is still alive at time ; otherwise . Thus is nonincreasing and right-continuous. It is easy to see that

is a martingale. Define . For each , define for all and . For each , define

in other words we keep track of the empirical distribution of the type and intensity for those assets which are still “alive”. We note that

We want to understand the dynamics of for large (this will then imply the “typical” behavior for ). To understand what our main result is, let’s first set up a topological framework to understand convergence of . Let be the collection of sub-probability measures (i.e., defective probability measures) on ; i.e., consists of those Borel measures on such that . We can topologize in the usual way (by projecting onto the one-point compactification of ; see \citeasnoun[Ch. 9.5]MR90g:00004). In particular, fix a point that is not in and define . Give the standard topology; open sets are those which are open subsets of (with its original topology) or complements in of closed subsets of (again, in the original topology of ). Define a bijection from to (the collection of Borel probability measures on ) by setting

for all . We can define the Skorohod topology on , and define a corresponding metric on by requiring to be an isometry. This makes a Polish space. Thus, is an element333If is a Polish space, then is the collection of maps from into which are right-continuous and which have left-hand limits. The space can be topologized by the Skorohod metric, which we will denote by ; see \citeasnounMR88a:60130. of .

The main result of this paper is Theorem 3.1, essentially a law of large numbers for as . For where and , define the operators

| (7) | ||||

Also define

The generator corresponds to the diffusive part of the intensity with killing rate , and is the macroscopic effect of contagion on the surviving intensities at any given time. Operators and are related to the exogenous systematic risk .

For every and , define

Theorem 3.1.

We have that converges in distribution to in . The evolution of is given by the measure evolution equation

Suppose there is a solution of the nonlinear SPDE

| (8) |

where denote adjoint operators, with initial condition

Then

Remark 3.2.

The proof of Theorem 3.1 is given in Sections 7 and 8. Lemma 8.4 provides an alternative characterization of the limit . Auxiliary results are given in the appendices.

Remark 3.3.

Equation (8) is a stochastic partial integral differential equation (SPIDE) in the half line that degenerates at the boundary . Due to Lemma 8.2 below, (8) can be viewed as a linear SPDE in the half line that degenerates at the boundary. Indeed, by Lemma 8.2, there is a unique pair taking values in satisfying the coupled system (29)-(30). Noting that , we see that the SPDE (8) can be written as

| (9) |

Notice also that by Remark 4.1, is bounded for all . Linear SPDEs in the half line that degenerate at the boundary are treated, under alternative assumptions, by \citeasnounKryLot1998, \citeasnounKim2009, \citeasnounLot2001 and \citeasnounKim2008.

4. Homogeneous Pool

We develop further insights into the SPDE governing the limit density (if it exists) in the case that the portfolio is homogenous. Let where . For a homogenous pool, for all and . In this case, we write for the solution of the SPDE (8), suppressing the dependence on the fixed .

4.1. Limiting Portfolio Loss

The SPDE takes the form

| (10) | ||||

where the adjoint operators are given by

| (11) |

Define the limiting portfolio loss by

| (12) |

this is a random quantity since depends on the systematic risk . For large , Theorem 3.1 suggests the “large-portfolio approximation”

| (13) |

4.2. Justification of Boundary Conditions

Note that and for all and . Assuming that is continuous in , this gives , for otherwise the integral diverges.

The boundary condition of is implied by the intensities being positive almost surely. For the deterministic case of , it is sufficient to stipulate Feller’s condition of , see \citeasnounFellerTwoSingularDiffusionProblems. For the case of , let us assume that . Then, Feller’s condition is again sufficient to imply . Let the flux be where . This follows from the fact that the stay non-negative almost surely by Lemma in \citeasnounGieseckeSpiliopoulosSowers2011 and therefore, according to the empirical measure , only leave by defaulting. In the asymptotic case described by the SPDE, defaults occur via the sink term . Then, probability mass only leaves via the sink term and does not flow across the boundaries at and . Integrating (10) over and using the aforementioned flux condition along with the boundary condition at , we have that

which is only satisfied by .

This discussion provides a justification for the choice of the boundary conditions for a homogeneous pool. The treatment of a heterogeneous pool is analogous.

4.3. Alternative Representation of Limiting Loss

As we shall see below, if the density has sufficiently fast decay at and at , then one can justify an alternative representation of the limiting loss (12). By integration by parts, we have

| (14) | |||||

Now, observe that

This implies that

| (15) |

Recall the boundary conditions . Then, if we assume that for any , and decay fast at infinity, in the sense that , the integration by parts formula (14) and equation (15) imply

| (16) |

A particularly interesting consequence of (16) is summarized in the following remark.

Remark 4.1.

Moreover, (16) implies for the rate of change

Finally, we mention that one can view as a pair satisfying

5. Numerical method and results

We develop and implement a method for the numerical solution of the SPDE (10) governing the limiting portfolio loss (12) in a homogenous pool. We obtain the distribution of the limiting loss , which we propose as an approximation to the loss when is large. Numerical results illustrate the method, as well as the accuracy and computational efficiency of the approximation.

5.1. Numerical Approaches in the Deterministic Case

In the case of , (10) becomes a deterministic, quasi-linear PDE. For completeness, we outline some numerical methods for this case.

5.1.1. No Feedback

If in addition , the default times are independent and we have the analytic solution where and satisfy

where , , , , and .

5.1.2. Finite Difference

For the deterministic case where , a finite difference scheme can efficiently solve the PDE. We devise a scheme which is implicit in the differential operators and explicit in the integral operator. A predictor-corrector iteration is employed to increase accuracy for the integral term. This finite difference scheme is second-order accurate. Let be the time-step for the scheme. Also, denote and let for be predictor steps. Formally,

where and .

5.2. Method of Moments

We provide a method for the numerical solution of the SPDE (10) that applies in the case that . Suppose that the boundary conditions for the SPDE are and , as justified in Section 4.2 above. (Note that the latter boundary condition also implies .) Furthermore, suppose that for each , is integrable on , almost surely. A sufficient condition is that the solution decays exponentially in ; that is, there exist constants such that almost surely for , . (We note that it was shown in Remark 4.1 that and exist.) Then, the moments exist almost surely. They follow the SDE system

| (18) | ||||

To find , multiply (10) by and integrate by parts over . Also, use the boundary conditions at and . Note that the limiting loss . A standard discretization scheme can be used to numerically solve the system (18).444Since the solution of the SPDE is nonnegative, the moments should also be nonnegative. However, due to the time discretization, the moments may become negative when simulated. This can cause instability in the numerical scheme. To avoid these problems, one could immediately set a moment to zero if it ever goes negative. In particular, instability in the higher moments may occur for large due to the exponential growth term . To reduce this instability, one could solve the transformed moments . The SDEs for will not have the exponential growth term anymore. Note also that .

Moment methods have previously been applied to deterministic PDEs such as the Boltzmann equation, see \citeasnounBoltzmann, for example. The moment SDE system in our case is not closed since the -th equation introduces the -th moment. So, in practice one must perform a truncation at some level where we let (that is, we use the first moments). In the asymptotic time limit of the case where , the sensitivity of to is of the order . The sensitivity in the more general case is more difficult to analyze. Numerical results, reported below, indicate that the convergence in terms of the number of moments is very rapid.

We remark that plays a pivotal role in the truncated version of system (18). If and appropriate choices are made for the coefficient functions and of the systematic risk, the truncated system satisfies the global Lipschitz condition and we have the standard existence and uniqueness results. If , the truncated system is only locally Lipschitz and therefore there exists a unique solution up to a stopping time .

In addition, the moments can be inverted to yield . However, although a distribution uniquely determines its moments, the converse may not be true. See \citeasnounInverseMoment for some numerical methods for moment inversion.

There is an alternative approach to viewing the moment system. The system (18) is driven by a single diffusion, which suggests there should be a canonical form where only one SDE has a diffusion term and the other SDEs only have drift terms. Define for and . Then

The moment and the “canonical” moments solve a system of random ODEs. They depend on the path of the systematic risk . A skeleton of can be generated exactly (without discretization bias) using the methods of \citeasnounBeskos, \citeasnounchen, or \citeasnounsmelov.

5.3. Behavior of Limiting Loss Distribution

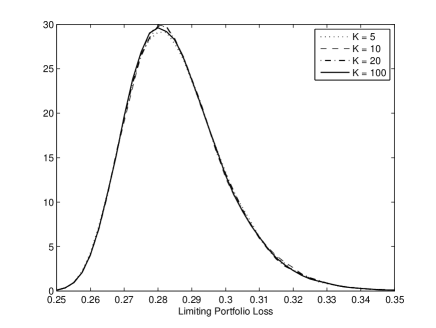

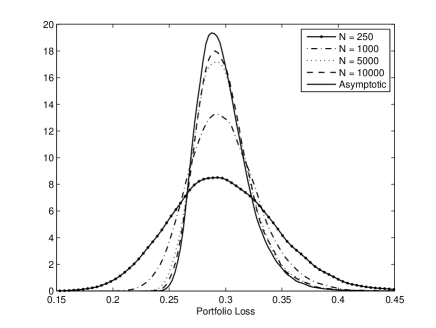

We provide some numerical results. Here and below, we choose the systematic risk process to be the CIR process where , , , and . We choose the initial condition . The moment system (18) is solved using an Euler scheme with time-step of . Figure 1 shows the rapid convergence of the moment system solution. Even using as few as six moments (), one can achieve a very accurate distribution for the limiting loss . Also, it is noteworthy that in the deterministic case of , the moment method is faster for the same accuracy than the finite difference approach outlined in Section 5.1.2.

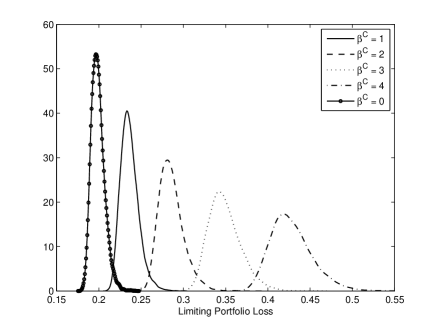

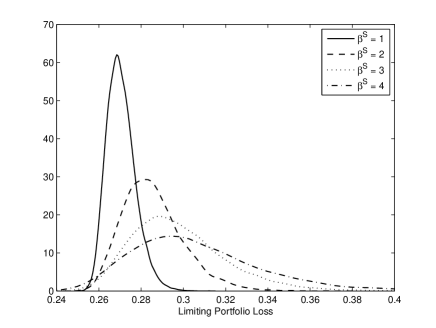

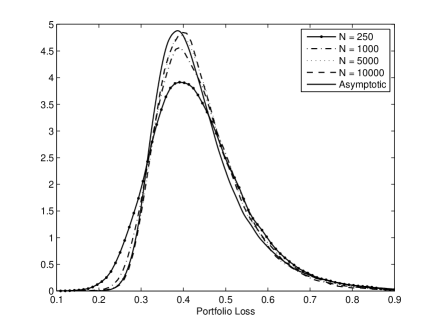

We report some salient features of the limiting loss distribution. Figure 2 shows the effect of the feedback sensitivity parameter on the distribution of . As increases, the mean of the losses increases and a heavy tail develops on the right (indicating a greater probability of extreme losses). Larger also causes a wider or more spread-out distribution, indicating a higher variance. An important ramification is that greater connectivity between firms, modeled here through a nonlinear term, can increase the volatility of their ensemble behavior. Similarly, increasing the systematic risk sensitivity parameter causes heavy tails on the right, see Figure 3. A hypothesis is that the initial losses can be sparked by the systematic risk factor (whose influence is determined by the parameter ) and then are later magnified by the contagion risk factor (determined by the parameter ). This has significant economic implications for the spread of risk through macro credit markets. The joint presence and interaction of systematic and contagion risk greatly magnifies the likelihood of extreme default events.

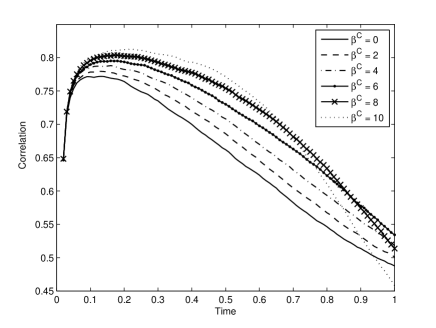

To shed more light on this issue, we calculate the Spearman correlation between and . Figure 4 shows that the correlation over a short time increases with the parameter while holding fixed. This indicates that the larger the exposure of firms in the pool to contagion effects, the more susceptible the system is to shocks from the systematic risk. This relationship is demonstrated in Figure 2 by the loss distribution’s heavy right tails for large . Our finding quantifies the central feature of the model: the complex interaction between systematic risk and contagion. The system becomes increasingly vulnerable to stresses from the systematic risk as the contagion channel in the system becomes stronger.

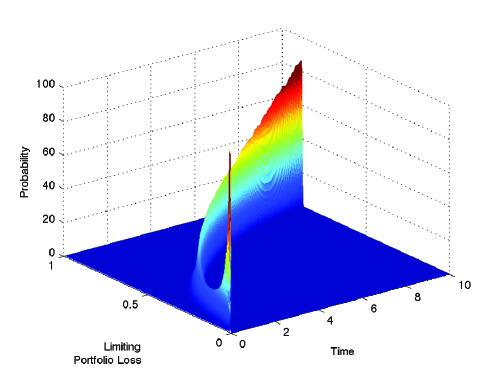

Another interesting observation is that the loss distribution can demonstrate non-monotonic behavior in time; for example, the distribution of losses may widen and then later tighten. Figure 5 shows the evolution of the distribution of over time , demonstrating this non-monotonicity. It is noteworthy that our numerical method yields the limiting loss distribution for all horizons simultaneously; this is useful for some applications, including the analysis of portfolio risk measures such as value at risk.

5.4. Accuracy of Large-Portfolio Approximation

We analyze the accuracy of the approximation (13). To this end, we estimate the distribution of the loss in a pool of names by Monte Carlo simulation of the default times . The simulation uses a time-scaling method, which is based on a discretization of the intensities on a time grid where for some . Intensities are simulated on using a truncated Euler scheme so that they remain nonnegative. Firm defaults (as well as jumps in intensity due to defaults) occur at the grid points according to a discretized version of (2):

-

•

Generate independent for each firm ,

-

•

For

-

(1)

,

-

(2)

If and , then ,

-

(3)

,

-

(1)

-

•

end.

The increments can be simulated using an Euler scheme similar to the one described above or by an exact scheme. For the results presented here, we again choose to be a CIR process with the same parameters as stated earlier. The CIR process is simulated using an Euler scheme (truncated at zero as shown above). We choose a time-step of .

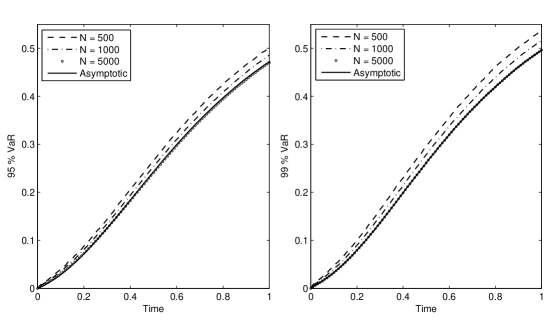

Convergence of the distribution of to that of the limiting loss tends be more rapid when is larger. When the variance of the losses is very small (i.e., the limiting losses are close to a deterministic solution), the convergence rate is slower. Convergence is most rapid in the tails of the loss distribution. Figures 6 and 7 show the convergence of the distribution of to that of for two different parameter cases. Convergence is relatively slow, but does indicate that the asymptotic solution is applicable for a portfolio consisting of several thousand names, a portfolio size not unusual in practice. Figure 8 compares the value at risk (VaR) of and at the 95 and 99 percent levels. The limiting VaR is surprisingly accurate even for moderately sized portfolios or several thousand firms. If is relatively small, then the VaR of tends to understate the VaR of . This is because fluctuations of due to the idiosyncratic noise terms in the intensity processes have not completely averaged out for small .

We evaluate the computational efficiency of the approximation. The parameter case is , and . A discrete time-step of is used. Monte Carlo samples are produced. The table below indicates computation times for , for each of several . The computation time for using is 6.25 seconds. (Here and below, the computation times are based on a Matlab implementation on a computer running Mac OS X with a GHz dual-core processor.) In general, the computational effort will be of an order greater for the generation of , where is the number of firms in the pool and is the truncation level of the moment method.

| Portfolio Size | Computation time |

|---|---|

| 13.58 seconds | |

| 22.12 seconds | |

| 236.24 seconds | |

| 441.80 seconds | |

| 1048.80 seconds |

5.5. Comparison of Method of Moments and Explicit Finite Difference

An alternate approach to the method of moments is a direct finite difference of the SPDE. An implicit method such as Crank-Nicholson cannot be used since the term must be non-anticipating. We therefore use explicit finite difference, which has the disadvantages of only first-order accuracy in time and conditional stability.

We provide the explicit finite difference scheme in the case of the general diffusion . The time-step is denoted and the mesh-size by . Let , and , for and . Then, the explicit finite difference scheme is

with boundary condition and . For , the criterion for conditional stability for a deterministic diffusion PDE with constant coefficients leads us to propose the approximate criterion for stability of the above numerical scheme, where . Numerical studies confirm that this condition for stability is a good approximation. Note that the time-step must become very small as the effect of systematic risk (i.e., the stochastic terms in the SPDE proportional to the parameter ) increases. For a general diffusion coefficient , we expect instability to generally increase if with high probability (and to decrease if with high probability).

Accuracy of explicit finite difference and the method of moments is comparable since we also use a first-order accurate scheme, the Euler method, for the SDE moment system. However, the great advantage of the SDE moment system is its extremely low computational cost in comparison with explicit finite difference of the SPDE. If one chooses a mesh with points for a finite difference scheme, then the finite difference scheme has an order of complexity of at least coupled SDEs whereas the method of moments can achieve highly accurate results with as little as half a dozen SDEs. As an example comparison, if the finite difference scheme has a mesh ranging from to with a mesh-size of , the finite difference scheme has at least the order of complexity of coupled SDEs. Furthermore, the explicit finite difference scheme is only conditionally stable. This means that even if one is satisfied with a time error of , one may have to choose a much smaller time-step to avoid instability. For instance, if , , and , our approximate criterion indicates must be less than . Given a desired accuracy in time of , we estimate the ratio of the computational cost of the explicit finite difference to that of the method of moments for the case of to be

| (19) |

As a concrete example, we report computational times for computing the loss at for the case of , and . The systematic risk is just a Brownian motion (i.e., and ); we can then compare the observed numerical instability with our approximate criterion for stability. The finite difference method uses a mesh-size of and while the method of moments is truncated at level . This parameter case was chosen to demonstrate the instability of the explicit finite difference scheme when becomes reasonably large and the mesh includes large values. Computational times are reported for Monte Carlo trials.

| Time Step | Method of Moments | Explicit Finite Difference |

|---|---|---|

| 2.4890 seconds | Unstable | |

| 25.7241 seconds | Unstable | |

| 254.6494 seconds | Unstable | |

| 2561.9614 seconds | 8512.3172 seconds |

The approximate criterion for stability gives , which matches well with the numerical results. In this example, we used a rather large number of moments (, to match the number of mesh points in the finite difference scheme). As we remarked earlier, the computational advantage of the method of moments over finite difference increases substantially if we take a small number of moments since highly accurate results are still achievable even using only a few moments.

6. Extensions

6.1. Extending the model

We can extend the system (1) to the case of more general coefficient functions for the intensity as well as stochastic position losses. Fix and . Let be a family of i.i.d. random variables with support . The variable represents the loss rate at default of the -th name in a pool of size . Consider the following system:

| (20) | ||||

where the coefficient functions , , and satisfy suitable regularity conditions guaranteeing the existence of a unique nonnegative solution .

Define the operators

Then, following the arguments applied to the system (1), we can show that the SPDE governing the limiting density takes the following form:

for and , where and .

Naturally, one expects that, for large and for every , .

6.2. Extending the Moment Method

The moment SDE system can be extended to the case of general coefficient functions as well as the non-homogeneous parameter case. By Theorem 3.1, in the non-homogeneous case the SPDE takes the form

The SDE moment system for the non-homogeneous case follows:

where . The SDE moment system is coupled across the parameter space . For numerical implementation, the parameter space must be discretized.

For the case of intensity processes with general coefficients , , and , we have an SPDE of the form stated in Section 6.1. A general moment method can be applied to this class of SPDEs, provided that we prescribe , , and such that the processes stay positive almost surely. Also, assume , , and are analytic on . Then, the generalized moment

solves a moment system similar (albeit more complicated) to (18).

7. Tightness and Identification of the Limit

We start by discussing relative compactness of the sequence .

Lemma 7.1.

The sequence is relatively compact in .

Proof.

The proof follows exactly as in Section 6 of \citeasnounGieseckeSpiliopoulosSowers2011. We omit the details. ∎

Next, we want to use the martingale problem (see \citeasnounMR88a:60130) to identify the limit of ’s.

Let be the collection of elements in of the form

| (21) |

for some , some , some and some . Then separates \citeasnounMR88a:60130. It thus suffices to show convergence of the martingale problem for functions of the form (21).

Let’s fix and understand exactly what happens to when one of the firms defaults. Suppose that the -th firm defaults at time and that none of the other names defaults at time (defaults occur simultaneously with probability zero). Then

Note furthermore that the default at time means that , so . Hence

| (22) |

where

for all , and .

For convenience, let’s define

for all . This is the generator of the systematic risk.

We now identify the limiting martingale problem for . For where and , recall the definitions of the operators in (7).

For of the form (21) we define the following operators.

and

| (23) | |||||

Moreover, we define the following processes

| (24) | ||||

and

| (25) |

where

is the Brownian martingale and is the martingale

With these definitions we have the following lemma.

Lemma 7.2.

For any and any we have that

Moreover, for any , the following limits hold

Proof.

For where , define

Then is the generator of the idiosyncratic part of the intensity.

We start by writing that

where is a martingale and

To proceed, let’s simplify . For each , , and , define

| (26) |

Then

where is the constant from Condition 2.2.

Define for . Setting

we have that

Moreover, by Lemma 3.4 in \citeasnounGieseckeSpiliopoulosSowers2011 we have that for any and any , there is a constant such that . This and Condition 2.2 imply that

Collecting things together, we get the statements of the lemma. ∎

We in particular note the macroscopic effect of the contagion.

Remark 7.3.

The key step in quantifying the coarse-grained effect of contagion was (26). Namely, we average the combination of the jump rate and the exposure to contagion across the pool.

8. Proof of Theorem 3.1

Let be the -law of ; i.e.,

for all . Thus for all . For , define for all .

Also for , define the quantity

| (27) |

Let .

Proposition 8.1.

We have that converges (in the topology of ) to the solution of the (filtered) martingale problem for by (27) and such that . In particular, and for all and and , we have that is a square integrable martingale with respect to both and . Namely,

| (28) |

Lastly, .

Proof.

The family is relatively compact (as a -valued random variable) by Lemma 7.1. Hence is also relatively compact. Let be an accumulation point of one of its convergent subsequences. Then, will converge in distribution to . This and Lemma 7.2 imply that the process will satisfy (28). Uniqueness of this martingale problem can also be shown as in \citeasnounGieseckeSpiliopoulosSowers2011.

Of course, we also have that for any ,

which implies the claimed initial condition. The rest of the statements are easily seen to be true. ∎

We next want to identify . This will take a couple of steps.

For notational convenience we shall write

The next lemma is essential for the characterization of the limit. Its proof is deferred to Appendix A.

Lemma 8.2.

Remark 8.3.

For notational convenience we do not write the dependence of and on but this is always assumed.

Lemma 8.4.

We have that , where for all and , is given by

Proof.

To proceed, define

On the one hand, we have that

On the other hand, by Lemma 8.2 we have

| (31) |

Thus, we have that

Thus

and hence satisfies the martingale problem generated by . Of course we also have that . By uniqueness, the claim follows.∎

Now we collect our results to prove the law of large numbers given in Theorem 3.1.

Proof of Theorem 3.1.

In Lemma 8.4 we proved that, for any , the limiting measure satisfies the measure evolution equation

From this expression it is immediately derived by integration by parts that, if there exists a solution to the nonlinear SPDE (8), then the density of should satisfy (8). This concludes the proof of the theorem. ∎

Appendix A Proof of Lemma 8.2

In this section we prove Lemma 8.2. The proof uses a fixed point theorem argument. For notational convenience we sometimes drop the superscript and from the notation of and simply write .

The square root singularity imposes some technical difficulties in the proof. For this purpose we introduce in Subsection A.1 an auxiliary function that will be used later on and study its properties. In Subsection A.2 we study existence and uniqueness and properties of satisfying (30) with a given .

In Subsection A.3 we prove the lemma under the additional condition that is bounded. Then, in Subsection A.4 we prove the lemma using Girsanov’s theorem for the process.

A.1. An auxiliary function

Let and define

for all . We note that is even, so is also even. Taking derivatives, we have that

for all . Since , is non-increasing. For ,

so in fact is nonnegative on and it vanishes on . Thus is nondecreasing and reaches its maximum at . Since , we in fact have that

for all . Since is non-increasing on and for , we have that for all , so . Since is even, we in fact must have that for all . Hence

for all . We finally note that

| (32) |

and that for all .

A.2. The uncoupled linear case

Let be a -predictable, nondecreasing, bounded and right-continuous process such that . Consider the SDE

| (33) | ||||

Then, as in Lemmas 3.1 and 3.2 of \citeasnounGieseckeSpiliopoulosSowers2011, we get that (33) has a unique nonnegative solution such that for all and .

A.3. Proof assuming that is bounded

In this subsection we prove Lemma 8.2 assuming that is bounded. The proof uses a fixed point theorem argument.

The main condition of this subsection is that there exists a such that

| (34) |

Let and be the set of valued, adapted, continuous processes such that

The space endowed with the norm is a Banach space.

Let us consider now a nonnegative process . Set

| (35) |

and consider (33) with in place of . We are going to prove that the map defined by through (33)-(35) with is a contraction on equipped with the norm

locally in which can also be extended to any arbitrary .

We collect in the following lemma some important properties of as defined though (35).

Lemma A.1.

Let a nonnegative process be given and let be the constant from Condition 2.2. The map , as a function of , is continuous, non-decreasing, positive, bounded uniformly in by and satisfies .

Proof.

All the statements are obvious. ∎

Fix and write for notational convenience and . The process satisfies

Next, we apply Itô formula to defined in Subsection A.1 with , getting

| (36) | |||||

For notational convenience we define the quantity for any given couple of stochastic processes .

Lemma A.2.

Proof.

By the definition of from (35) we get

Recall the trivial inequality . Since , we get that

The latter, Hölder inequality and Fubini’s Theorem imply

This concludes the proof of the lemma. ∎

Lemma A.3.

Proof.

The proof of this lemma follows by bounding each term on the right hand side of (36) separately using the bound from Lemma A.2 and the bounds for the first and second order derivatives of , i.e. and (32) respectively. In particular we have the following.

Taking expected value in (36) we obtain

| (38) | |||||

Let us now bound each term on the right hand side of (38).

Due to the boundedness condition on we have for the first and second term

| (39) |

Regarding the third term we recall the properties of outlined in Lemma A.1 and that for all and . Then, approximating by simple processes, we get that that there exists a constant such that

The latter display and Lemma A.2 imply that

| (40) |

Relation (32) gives for the fourth term

| (41) |

Relation (32) and the condition give for the fifth term

| (42) |

Lemma A.4.

For any , there exists a positive such that

Moreover, is continuous, increasing in and satisfies .

Proof.

Applying to and using Gronwall’s Lemma we obtain

where the constants are as in Lemma A.3. Taking we obtain

where for some constant . This concludes the proof of the lemma. ∎

We collect the previous results for the proof of Lemma 8.2 in the case of a bounded drift .

Proof.

Using Lemma A.4, a standard Picard iteration procedure shows that there exists a fixed point of , i.e. , for such that .

Let us show that this fixed point is necessarily unique. Indeed, suppose that are both fixed points. Then, Lemma A.4 implies that

By integrating, and using the condition for , we immediately obtain that

Therefore, for every and we should have almost surely. This gives uniqueness.

For the general case, we only have to subdivide the interval into a finite number of small intervals. Thus, there is a unique fixed point to the equation for all . Notice that the equation can be trivially written as the pair of the coupled equations (29)-(30). Clearly is nonnegative since is nonnegative. This concludes the proof of the lemma. ∎

A.4. Proof of Lemma 8.2

In this section we prove Lemma 8.2. By Lemma A.5 we know that the statement of Lemma 8.2 is true if is bounded. Our strategy is to apply this result for the case and then to generalize using Girsanov’s Theorem.

Recall the map defined by through (33)-(35). For notational convenience we shall write for to emphasize the fact that we are considering (33)-(35) with . We keep the notation for the case of a general .

Let be such that and define the quantity

For given we define iteratively the sequence

We shall prove that the sequence is a Cauchy sequence in probability uniformly in . In particular we have the following lemma.

Lemma A.6.

Assume that there is a such that and let be such that . For every , there exists such that for all

for every and for some constant independent of .

Proof.

As we saw in the proof of Lemma A.5, it is enough to consider the equation . Let be two solutions of the equation .

By Girsanov’s Theorem on the absolute continuous change of measure in the space of trajectories, Hölder and Chebychev inequality, we have the following

where satisfy and .

Then Lemma A.4 implies that can be made arbitrarily small by choosing large enough. This together with the boundedness of conclude the proof of the lemma. ∎

Now we are in position to prove Lemma 8.2.

Appendix B Some auxiliary results

In this section we prove some auxiliary lemmata that were needed in various places in the paper. These results are of independent interest.

Lemma B.1.

If is an integrable measurable random variable, then .

Proof.

Notice that where

Since is an -adapted Brownian motion, we get that is independent of . Therefore, we have

∎

Lemma B.2.

Consider a càdlàg and -adapted process such that for every . Then we have

Proof.

Given an arbitrary , i.e. , consider the quantity

It is easy to see that satisfies the SDE

Therefore, on the one hand we have

On the other hand,

Thus we arrive at the equality

Since this statement is true for every , we are done. ∎

References

- [1] \harvarditem[Ang et al.]Ang, Gorenflo, Le \harvardand Trong2002InverseMoment Ang, Dang Dinh, Rudolf Gorenflo, Vy Khoi Le \harvardand Dang Duc Trong \harvardyearleft2002\harvardyearright, Moment theory and some inverse problems in potential theory and heat conduction, Lecture Notes in Mathematics, Springer-Verlag, Berlin.

- [2] \harvarditem[Azizpour et al.]Azizpour, Giesecke \harvardand Schwenkler2010azizpour-giesecke-schwenkler Azizpour, Shahriar, Kay Giesecke \harvardand Gustavo Schwenkler \harvardyearleft2010\harvardyearright, Exploring the sources of default clustering. Working Paper, Stanford University.

- [3] \harvarditemBeskos \harvardand Roberts2005Beskos Beskos, Alexander \harvardand Gareth Roberts \harvardyearleft2005\harvardyearright, ‘Exact simulation of diffusions’, Annals of Applied Probability 15(4), 2422–2444.

- [4] \harvarditem[Bush et al.]Bush, Hambly, Haworth, Jin \harvardand Reisinger2011hambly Bush, Nick, Ben Hambly, Helen Haworth, Lei Jin \harvardand Christoph Reisinger \harvardyearleft2011\harvardyearright, Stochastic evolution equations in portfolio credit modelling. SIAM Journal on Financial Mathematics, forthcoming.

- [5] \harvarditemChen2009chen Chen, Nan \harvardyearleft2009\harvardyearright, Localization and exact simulation of Brownian motion driven stochastic differential equations. Working Paper, Chinese University of Hong Kong.

- [6] \harvarditem[Cvitanić et al.]Cvitanić, Ma \harvardand Zhang2011CMZ Cvitanić, Jakša, Jin Ma \harvardand Jianfeng Zhang \harvardyearleft2011\harvardyearright, Law of large numbers for self-exciting correlated defaults. Working Paper, University of Southern California.

- [7] \harvarditemDai Pra \harvardand Tolotti2009daipra-tolotti Dai Pra, Paolo \harvardand Marco Tolotti \harvardyearleft2009\harvardyearright, ‘Heterogeneous credit portfolios and the dynamics of the aggregate losses’, Stochastic Processes and their Applications 119, 2913–2944.

- [8] \harvarditem[Dai Pra et al.]Dai Pra, Runggaldier, Sartori \harvardand Tolotti2009daipra-etal Dai Pra, Paolo, Wolfgang Runggaldier, Elena Sartori \harvardand Marco Tolotti \harvardyearleft2009\harvardyearright, ‘Large portfolio losses: A dynamic contagion model’, The Annals of Applied Probability 19, 347–394.

- [9] \harvarditem[Das et al.]Das, Duffie, Kapadia \harvardand Saita2007ddk Das, Sanjiv, Darrell Duffie, Nikunj Kapadia \harvardand Leandro Saita \harvardyearleft2007\harvardyearright, ‘Common failings: How corporate defaults are correlated’, Journal of Finance 62, 93–117.

- [10] \harvarditemDavis \harvardand Rodriguez2007davis-rod Davis, Mark \harvardand Juan Carlos Esparragoza Rodriguez \harvardyearleft2007\harvardyearright, ‘Large portfolio credit risk modelling’, International Journal of Theoretical and Applied Finance 10, 653–678.

- [11] \harvarditem[Dembo et al.]Dembo, Deuschel \harvardand Duffie2004ddd Dembo, Amir, Jean-Dominique Deuschel \harvardand Darrell Duffie \harvardyearleft2004\harvardyearright, ‘Large portfolio losses’, Finance and Stochastics 8, 3–16.

- [12] \harvarditem[Duffie et al.]Duffie, Saita \harvardand Wang2006duffie-saita-wang Duffie, Darrell, Leandro Saita \harvardand Ke Wang \harvardyearleft2006\harvardyearright, ‘Multi-period corporate default prediction with stochastic covariates’, Journal of Financial Economics 83(3), 635–665.

- [13] \harvarditemEthier \harvardand Kurtz1986MR88a:60130 Ethier, Stewart N. \harvardand Thomas G. Kurtz \harvardyearleft1986\harvardyearright, Markov Processes: Characterization and Convergence, John Wiley & Sons Inc., New York.

- [14] \harvarditemFeller1951FellerTwoSingularDiffusionProblems Feller, William \harvardyearleft1951\harvardyearright, ‘Two singular diffusion problems’, Annals of Mathematics 54(1).

- [15] \harvarditemGiesecke \harvardand Smelov2010smelov Giesecke, Kay \harvardand Dmitry Smelov \harvardyearleft2010\harvardyearright, Exact simulation of jump-diffusions. Working Paper, Stanford University.

- [16] \harvarditem[Giesecke et al.]Giesecke, Spiliopoulos \harvardand Sowers2011GieseckeSpiliopoulosSowers2011 Giesecke, Kay, Konstantinos Spiliopoulos \harvardand Richard Sowers \harvardyearleft2011\harvardyearright, Default clustering in large portfolios: Typical and atypical events. Working Paper, Stanford University.

- [17] \harvarditemGiesecke \harvardand Weber2006giesecke-weber Giesecke, Kay \harvardand Stefan Weber \harvardyearleft2006\harvardyearright, ‘Credit contagion and aggregate losses’, Journal of Economic Dynamics and Control 30, 741–767.

- [18] \harvarditem[Glasserman et al.]Glasserman, Kang \harvardand Shahabuddin2007glasserman-kang Glasserman, Paul, Wanmo Kang \harvardand Perwez Shahabuddin \harvardyearleft2007\harvardyearright, ‘Large deviations in multifactor portfolio credit risk’, Mathematical Finance 17(3), 345–379.

- [19] \harvarditemGordy2003Gordy03arisk-factor Gordy, Michael B. \harvardyearleft2003\harvardyearright, ‘A risk-factor model foundation for ratings-based bank capital rules’, Journal of Financial Intermediation 12, 199–232.

- [20] \harvarditemKim2008Kim2008 Kim, Kyeong-Hun \harvardyearleft2008\harvardyearright, ‘-theory of parabolic SPDEs degenerating on the boundary of ’, Journal of Theoretical Probability 21(1), 169–192.

- [21] \harvarditemKim2009Kim2009 Kim, Kyeong-Hun \harvardyearleft2009\harvardyearright, ‘Sobolev space theory of SPDEs with continuous or measurable leading coefficients’, Stochastic Processes and their Applications 119(1), 16–44.

- [22] \harvarditemKrylov \harvardand Lototsky1998KryLot1998 Krylov, Nicolai \harvardand Sergey Lototsky \harvardyearleft1998\harvardyearright, ‘A Sobolev space theory of SPDEs with constant coefficients on a half line’, SIAM Journal of Mathematical Analysis 30(2), 298–325.

- [23] \harvarditemLototsky2001Lot2001 Lototsky, Sergey \harvardyearleft2001\harvardyearright, ‘Linear stochastic parabolic equations degenerating on the boundary of a domain’, Electronic Journal of Probability 6(24), 1–14.

- [24] \harvarditem[Lucas et al.]Lucas, Klaassen, Spreij \harvardand Straetmans2001lucas-etal Lucas, Andre, Pieter Klaassen, Peter Spreij \harvardand Stefan Straetmans \harvardyearleft2001\harvardyearright, ‘An analytic approach to credit risk of large corporate bond and loan portfolios’, Journal of Banking and Finance 25, 1635–1664.

- [25] \harvarditemRoyden1988MR90g:00004 Royden, Halsey \harvardyearleft1988\harvardyearright, Real analysis, third edn, Macmillan Publishing Company, New York.

- [26] \harvarditemSchloegl \harvardand O’Kane2005schloegl-okane Schloegl, Lutz \harvardand Dominic O’Kane \harvardyearleft2005\harvardyearright, ‘A note on the large homogeneous portfolio approximation with the student-t copula’, Finance and Stochastics 9(4), 577–584.

- [27] \harvarditemSircar \harvardand Zariphopoulou2010sircar-zari Sircar, Ronnie \harvardand Thaleia Zariphopoulou \harvardyearleft2010\harvardyearright, ‘Utility valuation of credit derivatives and application to CDOs’, Quantitative Finance 10(2), 195–208.

- [28] \harvarditemVasicek1991vasicek Vasicek, Oldrich \harvardyearleft1991\harvardyearright, Limiting loan loss probability distribution. Technical Report, KMV Corporation.

- [29] \harvarditemVincenti \harvardand Kruger1965Boltzmann Vincenti, Walter G. \harvardand Charles H. Kruger \harvardyearleft1965\harvardyearright, Introduction to Physical Gas Dynamics, John Wiley & Sons, New York.

- [30] \harvarditem[Zhang et al.]Zhang, Blanchet, Giesecke \harvardand Glynn2011zhang-etal Zhang, Xiaowei, Jose Blanchet, Kay Giesecke \harvardand Peter Glynn \harvardyearleft2011\harvardyearright, Affine point processes: Asymptotic analysis and efficient rare-event simulation. Working Paper, Stanford University.

- [31]