Multi-agent based analysis of financial data

Abstract

In this work the system of agents is applied to establish a model of the nonlinear distributed signal processing. The evolution of the system of the agents - by the prediction time scale diversified trend followers, has been studied for the stochastic time-varying environments represented by the real currency-exchange time series. The time varying population and its statistical characteristics have been analyzed in the non-interacting and interacting cases. The outputs of our analysis are presented in the form of the mean life-times, mean utilities and corresponding distributions. They show that populations are susceptible to the strength and form of inter-agent interaction. We believe that our results will be useful for the development of the robust adaptive prediction systems.

pacs:

89.65.Gh, 89.65.Gh, 05.10.-a, 05.65.+bI Introduction

The agent-based models are distributed computational models which claim to treat complex problems by turning them into a multitude of the subtasks which can be efficiently solved by means of the elementary specialized autonomous entities called agents. There are well known examples of the agent-based and multi-agent models which claim to simulate complex economic Palmer94 ; Shimokawa2007 and social Multi2009 phenomena which are beyond traditional analysis in economics. Here we discuss entirely different approach and problem. We apply agent-based modeling to investigate time series data Cao2010 that have an economic origin. In such case a final answer relevant for the investigator of the population may be extracted in a way that pieces of the output information belonging to individual agents are synthesized to form the statistical output of interest.

I.1 Model of non-interacting entities, population of scale-dependent trend-followers

Trend following (TF) is an investment strategy that aims to analyze and benefit from market trend mechanism. TF strategy which focuses on the price moves both up and down is based on assumption of time continuation of the moves. Many variations of this basic framework exist, but here we focus on the consequences of the minimalist, less CPU time demanding approach. Our multi-agent system is built to describe the scale-selection process. We assumed the constant population of agents, where th agent is characterized by its individual operating time scale (), which specifies the time window relevant for decisions. As new agent is born, its is chosen randomly within given bounds but it does not vary during the agent’s lifespan. The elementary TF agents we deal with are perceiving trend by comparing actual price with preceding time-shifted , where denotes index of tick quotation. The actual agent’s sell-buy trade decision is encoded by the variable as it follows:

| (3) |

In the elementary variant of the model the decisions of TF agents are made independently. We analyzed tick-by-tick sequences of the currency exchange rate quotations. By each simulation, population of agents proceeds over the middle price records from chosen data file. We treated obtained by the standard transformation from the ask and bid tick by tick quotations. The information from environment is discretized by the following scheme

| (6) |

At each iteration, the deviation of prediction made for steps forward is measured by the recurrently given utility . To construct the series of , it remains to specify initial utility . The life of the agent begins at the moment of the death of its predecessor labeled by the same index (i). The agent’s life continues until the utility drops to zero bound .

II Results

II.1 The scale-formation process of independent TF agents

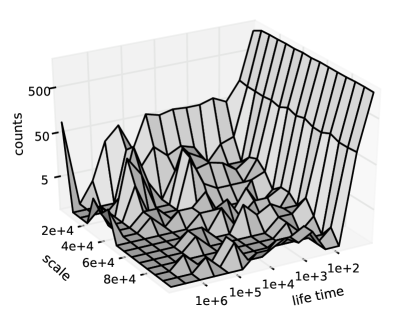

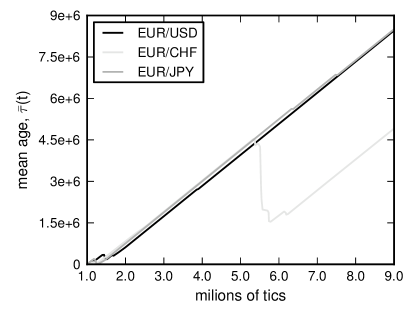

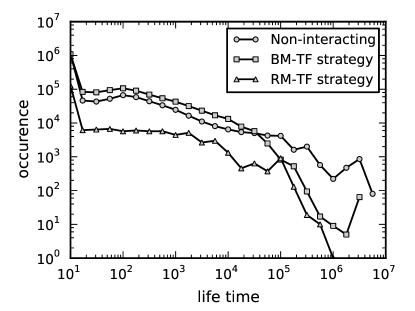

We realize that the question of the population size is apparently irrelevant for the independent (non-communication, non-interacting) TF agents, however it starts to be important when the aspects of evolution and inter-agent interaction (information exchange) are taken into account. The numerical analysis of the population of independent TF agents has been done for , , . At the moment of birth, the scale has been drawn randomly uniformly within the bounds , . The approach has been applied to treat the six year record of the EUR/USD exchange rate (period 2004-2009). We have been interested in probability distributions as functions life-time and scales (see Fig.1).

Apart from the excessive simplicity of the TF mechanism, we found that several agents survived after the complete data record had been browsed. Then, what follows from it is that TF strategies may provide adequate ground for some basic prediction models. We extended simulation to include USD/CHF, USD/JPY records. Similar, but not identical distributions have been obtained for these data. We can state that TF agents provide a better prediction (for ) if they focus on the small, i.e. scales. The statement is general and covers all aforementioned foreign exchange records. Next question we claim to answer is ”How the distribution of life-time and will be affected, when the prediction is made for more than one step forward ()?”. Let’s compare previous results for with those obtained for . The results depicted in Fig.1 appear to imply that no general statement regarding life-time can be made. There is, however, some qualitative difference which might be noticed, that functional relation between life-times and seems to be less readily seen for than it is in the case of . As , the results become more currency specific. One may conclude that in general, the increase in leads to the inhibition of preferential scales.

II.1.1 Populations of agents - instant averages and transient characteristics

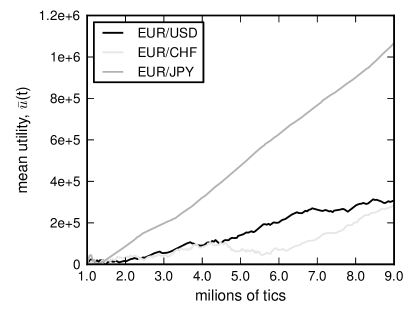

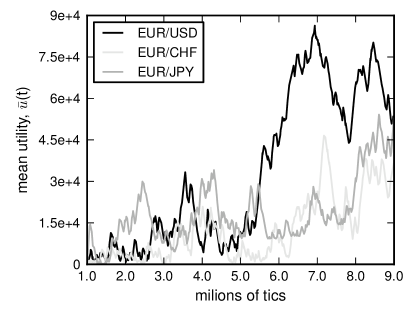

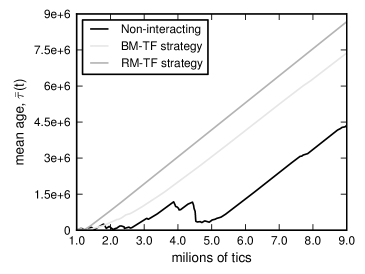

The agents are predicting, gaining or losing pieces of their utilities, some agents are dying and some new agents are being born. To shed light on the population dynamics we calculated transient characteristics including temporal development of two instantaneous population averages: mean utility and mean actual age , where represents actual age of agent at tick . As can be seen from Fig.2, the mean utility is growing faster when the predictions are made for smaller number of steps forward (). Within the EUR/USD record, after the initial transient ticks, the accumulated reaches values around , , , for the predictions steps forward, respectively. However, if is measured for other currencies, the comparatively slower growth has been observed as increases. The value may be used as well to define the prediction accuracy by means of the formula . The calculation of leads - (for ), - (as ) and - (as ticks). The monitoring of and revealed stages of the continuous growth interrupted by the bursts consisting of several sudden small drops. These events could be interpreted in terms of the population biology as massive extinctions. The extinctions may be also be perceived as an expulsion of TF agents from certain scales and determination of temporary stableness at some another specific scales. The observation of the subsequent renewal of the regime with less fluctuating and result in epochs of the temporarily sustainable generations.

II.2 The information exchange between agents

Until now we have studied idealized population of elementary agents where each member acts independently of others. It seems interesting to extend our study to strategies which are based on the inter-agent interaction. The experience from the design of the complex systems is that interaction may lead to the emergence of the unexpected phenomena. Our hypothesis is that under certain conditions the interactions of agents may extenuate undesired data effects (like those which cause massive extinctions), or may improve the quality of the predictions. Within the next subsections we discuss several models of interaction which extend picture of the TF agent in a very natural way.

II.2.1 Superior - merchant agents with exceptional information access.

The elementary evolutionary belief we are implementing lies in the fact that exceptional access to information resources may to enhance the performance of decisions. In this respect, we want to supplement population by better informed decision makers. We have introduced and tested effect of agents we shall call merchants or M agents. They are designed to receive information about the pure expected TF decisions or to provide information to assist TF decisions modified by the recommendation process. The information M-agent can get from TF agent is always reduced to the instant pair. The comparative process within the population yields decision output of M agent. More concretely, we studied information processing where M agent decides in accordance with a decision of TF agent attaining highest instant utility within TF population. Similar strategies, such as weighted averaging according utility, have been tested as well, however, their contribution does not differ in principal from the results obtained for the above defined strategy of M agent.

II.2.2 BM-TF strategy: TF agent born by the M agent.

Originally, the non-interacting agents were born with scale drawn uniformly randomly. The evolutionary feature we analyzed is that agents are born at the proximity to the scale actually occupied by the M agent. The diversity which prevents from getting stuck is achieved by the mutation process where shift with respect to the scale of M agent is modelled by the Gaussian distribution, with the mean localized at the scale of M agent (the dispersion is set to be equal to 3000).

II.2.3 RM-TF strategy: decisions of TF agents regarding recommendations of M agents.

As mentioned above, the main motivation for the use of multi-agent data analysis represents an information inter-agent exchange which may induce self-organized behavior and emergence of the qualitative unexpected changes in the information treatment. More specifically, by means of correlated decisions we claim to induce self-improvement and stability of the TF population. With this aim we implemented information exchange where agents are comparing their predictions with recommendations concerned in the unique central variable . The information in the form of is transmitted by the M agents which are endowed with an exceptional authority to affect subordinated TF agents by the recommendation process. As a consequence, each TF agent justifies its preliminary decision (calculated according Eq.(3) within the scheme of independent agents) with . The approval scheme for subordinated TF agent yields decision model

| (9) |

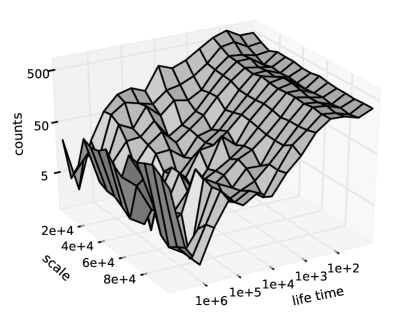

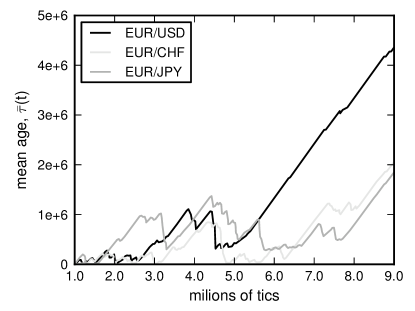

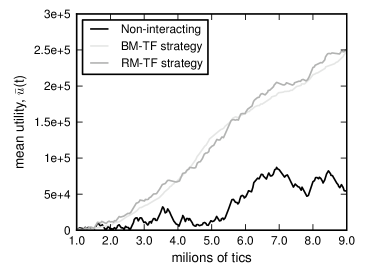

The formula gives rise to the newly defined passive state which stems from disagreement of agents. The proposed here RM-TF strategy closes the information feedback loop since the M agent has access to decisions of subordinated TF community. The results of simulation are presented in Fig.3. They show the influence of the interaction effect on the stability of population.

II.3 The statistical consequences of interaction

| distribution of life-times | range | effective index |

| non-interacting | -0.50 | |

| BM-TF | -0.30 | |

| RM-TF | -0.40 | |

| distribution of deathrates | range | effective index |

| non-interacting | -0.73 | |

| BM-TF | -0.83 | |

| RM-TF | -0.50 |

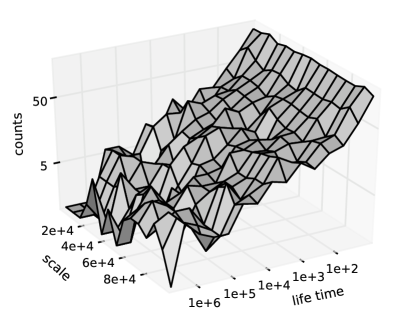

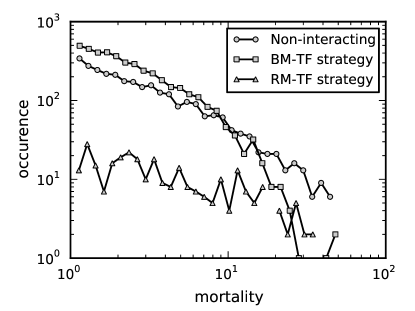

We compared characteristics of non-interacting population with those obtained by means of the combined BM-TF, RM-TF strategies (see Fig.3). These findings imply statistical stabilization effect of the interaction. The transient epochs monitored by means of and clearly indicate that massive extinctions of the non-interacting TF population may be remarkably reduced upon the implementation of the BM-TF, RM-TF types of the information exchange. From the point of view of the universal features of the distributions and their hypothetical power-law form (see Fig.4), we observed a remarkable effect of the combined strategies on the distributions of the life-times. The population of TF agents gains nearly critical properties (see e.g. Honga2007 ) indicated by the power-law form with the indices (log-log slopes or exponents) listed in table 1. The dynamics of given system have been found to be similar to those of complex systems, conventionally studied in physics of critical phenomena. In contrast, we uncover that inter-agent RM-TF type interaction ruins the power-law form pertinent to currency data. However, this finding most typical for EUR/USD differs for other currencies. Of course, artificially suggested forms of interaction seem to be very far from the interaction of the real market agents, therefore, there may appear loose of the power-law form.

III Conclusions

We studied model of data analysis based on the system of autonomous agents. The model has been tested for several selected currencies in the case of the non-interacting (independent) and interacting agents. The modelling of the non-interacting agents uncovered specific periods of the extinctions of agents (and belonging scales) interrupted by the relatively calm periods. It has been demonstrated that specific inter-agent interaction may stabilize population of agents and inhibit in part criticality which is typical for financial market data.

References

- (1) Palmer, R.G., Arthur, W.B., Holland, J.H., LeBaron, B., Tayler, P.: Artificial economic life: a simple model of a stockmarket. Physica D 75, 264–274 (1994)

- (2) Shimokawa T., Suzuki K., Misawa T.: An agent based approach to financial stylized facts. Physica A 379, 207-225 (2007)

- (3) David, N., Sichman, J.S.: Multi-agent Based simulation IX, International Workshop, MABS 2008, Springer Verlag Berlin Heidelberg (2009)

- (4) Cao L., Yu P.S., Zhang Ch., Zhao Y.: Domain Driven Data Mining. Springer, New York (2010)

- (5) Honga B.H., Leeb K.E., Leeb J.W.: Power law of quiet time distribution in the Korean stock-market. Physica A 377, 576–582 (2007)