Convergence of a Particle-based Approximation of the Block Online Expectation Maximization Algorithm

Abstract

Online variants of the Expectation Maximization (EM) algorithm have recently been proposed to perform parameter inference with large data sets or data streams, in independent latent models and in hidden Markov models. Nevertheless, the convergence properties of these algorithms remain an open problem at least in the hidden Markov case. This contribution deals with a new online EM algorithm which updates the parameter at some deterministic times. Some convergence results have been derived even in general latent models such as hidden Markov models. These properties rely on the assumption that some intermediate quantities are available in closed form or can be approximated by Monte Carlo methods when the Monte Carlo error vanishes rapidly enough. In this paper, we propose an algorithm which approximates these quantities using Sequential Monte Carlo methods. The convergence of this algorithm and of an averaged version is established and their performance is illustrated through Monte Carlo experiments.

This extended version of the paper “Convergence of a Particle-based Approximation of the Block Online Expectation Maximization Algorithm“, by S. Le Corff and G. Fort, provides detailed proofs which have been omitted in the submitted paper since they are very close to existing results. These additional proofs are postponed to Appendix B.

1 Introduction

The Expectation Maximization (EM) algorithm is a well-known iterative algorithm to solve maximum likelihood estimation in incomplete data models, see [14]. Each iteration is decomposed into two steps: in the E-step the conditional expectation of the complete log-likelihood (log of the joint distribution of the hidden states and the observations) given the observations is computed; and the M-step updates the parameter estimate. The EM algorithm is mostly practicable if the model belongs to the curved exponential family, see [29, Section ] and [6, Section ], so that we assume below that our model belongs to this family. Under mild regularity conditions, this algorithm is known to converge to the stationary points of the log-likelihood of the observations, see [36]. However, the original EM algorithm cannot be used to perform online estimation or when the inference task relies on large data sets. Each iteration requires the whole data set and each piece of data needs to be stored and scanned to produce a new parameter estimate. Online variants of the EM algorithm were first proposed for independent and identically distributed (i.i.d.) observations: [5] proposed to replace the original E-step by a stochastic approximation using the new observation. Solutions have also been proposed in hidden Markov models (HMM): [4] provides an algorithm for finite state-space HMM which relies on recursive computations of the filtering distributions combined with a stochastic approximation step. Note that, since the state-space is finite, deterministic approximations of these distributions are available. This algorithm has been extended to the case of general state-space models, the approximations of the filtering distributions being handled with Sequential Monte Carlo (SMC) algorithms, see [3], [10] and [25]. Unfortunately, it is quite challenging to address the asymptotic behavior of these algorithms (in the HMM case) since the recursive computation of the filtering distributions relies on approximations which are really difficult to control.

In [23], another online variant of the EM algorithm in HMM is proposed, called the Block Online EM (BOEM) algorithm. In this case, the data stream is decomposed into blocks of increasing sizes. Within each block, the parameter estimate is kept fixed and the update occurs at the end of the block. This update is based on a single scan of the observations, so that it is not required to store any block of observations. [23] provides results on the convergence and on the convergence rates of the BOEM algorithms. These analyses are established when the E-step (computed on each block) is available in closed form and when it can be approximated using Monte Carlo methods, under an assumption on the -error of the Monte Carlo approximation.

In this paper, we consider the case when the E-step of the BOEM algorithm is computed with SMC approximations: the filtering distributions are approximated using a set of random weighted particles, see [6] and [8]. The Monte Carlo approximation is based on an online variant of the Forward Filtering Backward Smoothing algorithm (FFBS) proposed in [4] and [10]. This method is appealing for two reasons: first, it can be implemented forwards in time i.e. within a block, each observation is scanned once and never stored and the approximation computed on each block does not require a backward step - this is crucial in our online estimation framework. Secondly, recent work on SMC approximations provides -mean control of the Monte Carlo error, see e.g. [19] and [9]. This control, combined with the results in [23], sparks off the convergence results and the convergence rates provided in this contribution.

The paper is organized as follows: our new algorithm called the Particle Block Online EM algorithm (P-BOEM) is derived in Section 2 together with an averaged version. Section 3 is devoted to practical applications: the P-BOEM algorithm is used to perform parameter inference in stochastic volatility models and in the more challenging framework of the Simultaneous Localization And Mapping problem (SLAM). The convergence properties and the convergence rates of the P-BOEM algorithms are given in Section 4.

2 The Particle Block Online EM algorithms

In Section 2.1, we fix notation that will be used throughout this paper. We then derive our online algorithms in Sections 2.2 and 2.3. We finally detail, in Section 2.4, the SMC procedure that makes our algorithm a true online algorithm.

2.1 Notations and Model assumptions

A hidden Markov model on is defined by an initial distribution on and two families of transition kernels. In this paper, the transition kernels are parametrized by , where is a compact set. In the sequel, the initial distribution on is assumed to be known and fixed. The parameter is estimated online in the maximum likelihood sense using a sequence of observations . Online maximum likelihood parameter inference algorithms were proposed either with a gradient approach or an EM approach. In the case of finite state-spaces HMM, [26] proposed a recursive maximum likelihood procedure. The asymptotic properties of this algorithm have recently been addressed in [34]. This algorithm has been adapted to general state-spaces HMM with SMC methods (see [18]). The main drawback of gradient methods is the necessity to scale the gradient components. As an alternative to performing online inference in HMM, online EM based algorithms have been proposed for finite state-spaces (see [4]) or general state-spaces HMM (see [3], [10] and [23]). [10] proposed a SMC method giving encouraging experimental results. Nevertheless, it relies on a combination of stochastic approximations and SMC computations so that its analysis is quite challenging. In [23], the convergence of an online EM based algorithm is established. This algorithm requires either the exact computation of intermediate quantities (available explicitly only in finite state-spaces HMM or in linear Gaussian models) or the use of Monte Carlo methods to approximate these quantities. We propose to apply this algorithm to general models where these quantities are replaced by SMC approximations. We prove that the Monte Carlo error is controlled in such a way that the convergence properties of [23] hold for the P-BOEM algorithms.

We now detail the model assumptions. Consider a family of transition kernels on , where is a general state-space equipped with a countably generated -field , and is a finite measure on . Let be a family of transition kernels on , where is a general space endowed with a countably generated -field and is a measure on . Let be the observation process defined on and taking values in . The batch EM algorithm is an offline maximum likelihood procedure which iteratively produces parameter estimates using the complete data log-likelihood (log of the joint distribution of the observations and the states) and a fixed set of observations, see [14]. In the HMM context presented above, given observations , the missing data and a parameter , the complete data log-likelihood may be written as (up to the initial distribution which is assumed to be known)

| (1) |

where we use as a shorthand notation for the sequence , . Each iteration of the batch EM algorithm is decomposed into two steps. The E-step computes, for all an expectation of the complete data log-likelihood under the conditional probability of the hidden states given the observations and the current parameter estimate . In the HMM context, due to the additive form of the complete data log-likelihood (1), the E-step is decomposed into expectations under the conditional probabilities where

| (2) |

for any bounded function , any , any and any sequence . Then, given the current value of the parameter , the E-step amounts to computing the quantity

| (3) |

for any . The M-step sets the new parameter estimate as a maximum of this expectation over .

The computation of for any is usually intractable except in the case of complete data likelihood belonging to the curved exponential family, see [29, Section ] and [6, Section ]. Therefore, in the sequel, the following assumption is assumed to hold:

-

A1

-

(a)

There exist continuous functions , and s.t.

where denotes the scalar product on .

-

(b)

There exists an open subset of that contains the convex hull of .

-

(c)

There exists a continuous function s.t. for any ,

-

(a)

Under AA1, the quantity defined by (3) becomes

| (4) |

so that the definition of the function requires the computation of an expectation independently of .

The M-step of the batch EM iteration amounts to computing

This batch EM algorithm is designed for a fixed set of observations. A natural extension of this algorithm to the online context is to define a sequence of parameter estimates by

Unfortunately, the computation of requires the whole set of observations to be stored and scanned for each estimation. For large data sets the computation cost of the E-step makes it intractable in this case. To overcome this difficulty, several online variants of the batch EM algorithm have been proposed, based on a recursive approximation of the function (see [3], [10] and [23]). In this paper, we focus on the Block Online EM (BOEM) algorithm, see [23].

2.2 Particle Block Online EM (P-BOEM)

The BOEM algorithm, introduced in [23], is an online variant of the EM algorithm. The observations are processed sequentially per block and the parameter estimate is updated at the end of each block. Let be a sequence of positive integers denoting the length of the blocks and set

| (5) |

are the deterministic times at which the parameter updates occur. Define, for all integers and and all ,

| (6) |

The quantity corresponds to the intermediate quantity in (4) with the observations .

The BOEM algorithm iteratively defines a sequence of parameter estimates as follows: given the current parameter estimate ,

-

(i)

compute the quantity ,

-

(ii)

compute a candidate for the new value of the parameter: ,

To make the exposition easier, we assume that the initial distribution is the same on each block. The dependence of on is thus dropped from the notation for better clarity.

The quantity is available in closed form only in the case of linear Gaussian models and HMM with finite state-spaces. In HMM with general state-spaces cannot be computed explicitly and we propose to compute an approximation of using SMC algorithms thus yielding the Particle-BOEM (P-BOEM) algorithm. Different methods can be used to compute these approximations (see e.g. [9], [10] and [16]). We will discuss in Section 2.4 below some SMC approximations that use the data sequentially.

-

Denote by the SMC approximation of computed with particles. The P-BOEM algorithm iteratively defines a sequence of parameter estimates as follows: given the current parameter estimate ,

-

(i)

compute the quantity ,

-

(ii)

compute a candidate for the new value of the parameter:

-

(i)

We give in Algorithm 1 lines to an algorithmic description of the P-BOEM algorithm. Note that the idea of processing the observations by blocks is proposed in [30] to fit a normal mixture model. The incremental EM algorithm discussed in [30] is an alternative to the batch EM algorithm for very large data sets. Contrary to our framework, in the algorithm proposed by [30], the number of observations is fixed and the same observations are scanned several times.

2.3 Averaged Particle Block Online EM

Following the same lines as in [23], we propose to replace the P-BOEM sequence by an averaged sequence. This new sequence can be computed recursively, simultaneously with the P-BOEM sequence, and does not require additional storage of the data. The proposed averaged P-BOEM algorithm is defined as follows (see also lines and of Algorithm 1): the step (ii) of the P-BOEM algorithm presented above is followed by

-

(iv)

compute the quantity

(7) -

(v)

define

(8)

We set so that

| (9) |

we will prove in Section 4.4 that the rate of convergence of the averaged sequence , computed from the averaged statistics , is better than the non-averaged one. We will also observe this property in Section 3 by comparing the variability of the P-BOEM and the averaged P-BOEM sequences in numerical applications.

2.4 The SMC approximation step

As the P-BOEM algorithm is an online algorithm, the SMC algorithm should use the data sequentially: no backward pass is allowed to browse all the data at the end of the block. Hence, the approximation is computed recursively within each block, each observation being used once and never stored. These SMC algorithms will be referred to as forward only SMC. We detail below a forward only SMC algorithm for the computation of which has been proposed by [4] (see also [10]).

For notational convenience, the dependence on is omitted. For block , the algorithm below has to be applied with , and .

The key property is to observe that

| (10) |

where is the filtering distribution at time , and the functions , , satisfy the equations

| (11) |

where denotes the backward smoothing kernel at time

| (12) |

By convention, and . A proof of the equalities (10) to (12) can be found in [4] and [10]. Therefore, a careful reading of Eqs (10) to (12) shows that, for an iterative particle approximation of , it is sufficient to update from time to

-

(i)

weighted samples used to approximate the filtering distribution .

-

(ii)

the intermediate quantities , approximating the function at point , .

We describe below such an algorithm. An algorithmic description is also provided in Appendix A, Algorithm 2.

Given instrumental Markov transition kernels on and adjustment multipliers , the procedure goes as follows:

-

(i)

line in Algorithm 2: sample independently particles with the same distribution .

-

(ii)

line in Algorithm 2: at each time step , pairs of indices and particles are sampled independently (conditionally to , and ) from the instrumental distribution:

(13) on the product space . For any and any , denotes the index of the selected particle at time used to produce .

-

(iii)

line in Algorithm 2: once the new particles have been sampled, their importance weights are computed.

-

(iv)

lines in Algorithm 2: update the intermediate quantities .

If, for all , and if the kernels are chosen such that , lines - in Algorithm 2 are known as the Bootstrap filter. Other choices of and can be made, see e.g. [6].

3 Applications to Bayesian inverse problems in Hidden Markov Models

3.1 Stochastic volatility model

Consider the following stochastic volatility model:

where and and are two sequences of i.i.d. standard Gaussian r.v., independent from .

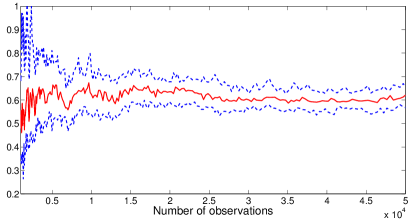

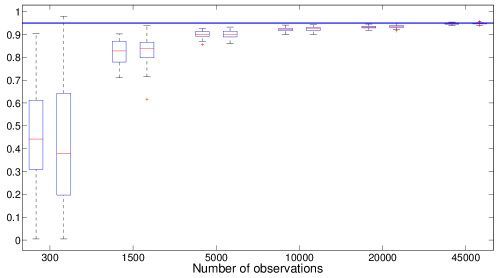

We illustrate the convergence of the P-BOEM algorithms and discuss the choice of some design parameters such as the pair (). Data are sampled using , and ; we estimate by applying the P-BOEM algorithm and its averaged version. All runs are started from , and .

Figure 1 displays the estimation of the three parameters as a function of the number of observations, over independent Monte Carlo runs. The block-size sequence is of the form . For the SMC step, we choose ; particles are sampled as described in Algorithm 2 (see Appendix A) with the bootstrap filter. For each parameter, Figure 1 displays the empirical median (bold line) and upper and lower quartiles (dotted line). The averaging procedure is started after observations. Both algorithms converge to the true values of the parameters and, once the averaging procedure is started, the variance of the estimation decreases (estimation of and ). The estimation of shows that, if the averaging procedure is started with too few observations, the estimation can be slowed down.

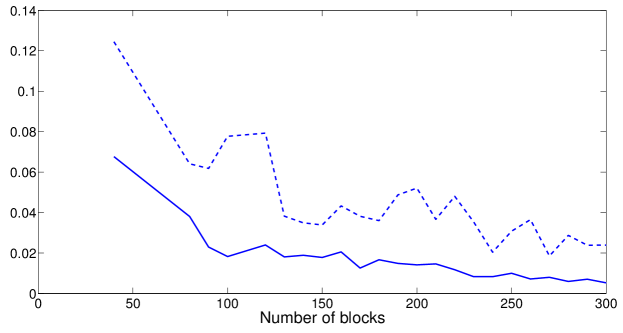

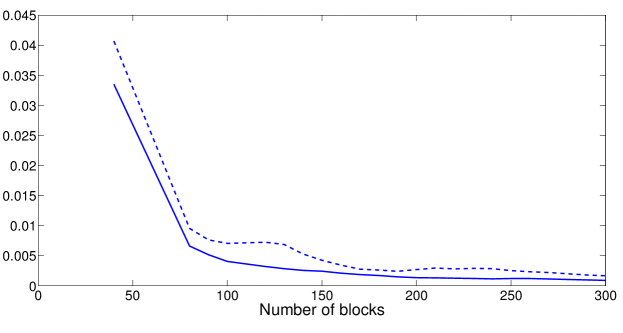

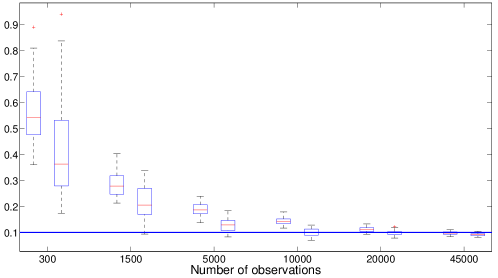

We now discuss the role of the pairs . Roughly speaking (see section 4 for a rigorous decomposition), controls the rate of convergence of to ; and controls the error between and its SMC approximation. We will show in Section 4 that are part of some sufficient conditions for the P-BOEM algorithms to converge. We thus choose increasing sequences . The role of has been illustrated in [23, Section ]. Hence, in this illustration, we fix and discuss the role of . Figure 2 compares the algorithms when applied with and or . The empirical variance (over independent Monte Carlo runs) of the estimation of is displayed, as a function of the number of blocks. First, Figure 2 illustrates the variance decrease provided by the averaged procedure, whatever the block size sequence. Moreover, increasing the number of particles per block improves the variance of the estimation given by the P-BOEM algorithm while the impact on the variance of the averaged estimation is less important. On average, the variance is reduced by a factor of for the P-BOEM algorithm and by a factor of for its averaged version when the number of particles goes from to . These practical considerations illustrate the theoretical results derived in Section 4.4.

Finally, we discuss the role of the initial distribution . In all the applications above, we have the same distribution at the beginning of each block. We could choose a different distribution for each block such as, e.g., the filtering distribution at the end of the previous block. We have observed that this particular choice of leads to the same behavior for both algorithms.

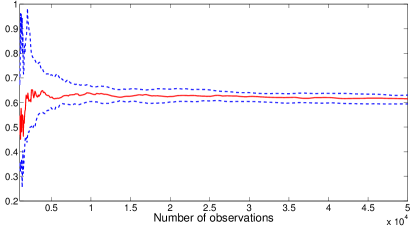

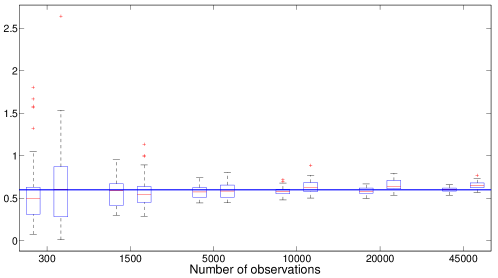

To end this section, the P-BOEM algorithm is compared to the Online EM algorithm outlined in [4] and [10]. These algorithms rely on a combination of stochastic approximation and SMC methods. According to classical results on stochastic approximation, it is expected that the rate of convergence of the Online EM algorithm behaves like , where is the so called step-size sequence. Hence, in the Online EM algorithm is chosen such that and the block-size sequence in the P-BOEM algorithm such that . The number of particles used in the Online EM algorithm is fixed and chosen so that the computational costs of both algorithms are similar. Provided that in the P-BOEM algorithm, this leads to a choice of particles for the Online EM algorithm. We report in Figure 3, the estimation of and for a Polyak-Ruppert averaged Online EM algorithm (see [33]) and the averaged P-BOEM algorithm as a function of the number of observations. The averaging procedure is started after about observations. As noted in [23, Section ] for a constant sequence this figure shows that both algorithms behave similarly. For the estimation of and , the variance is smaller for the P-BOEM algorithm and the convergence is faster for the P-BOEM algorithm in the case of . Conclusions are different for the estimation of : the variance is smaller for the P-BOEM algorithm but the Online EM algorithm converges a bit faster. The main advantage of the P-BOEM algorithm is that it relies on approximations which can be controlled in such a way that we are able to show that the limiting points of the P-BOEM algorithms are the stationary points of the limiting normalized log-likelihood of the observations.

3.2 Simultaneous Localization And Mapping

The Simultaneous Localization And Mapping (SLAM) problem arises when a mobile device wants to build a map of an unknown environment and, at the same time, has to estimate its position in this map. The common statistical approach for the SLAM problem is to introduce a state-space model. Many solutions have been proposed depending on the assumptions made on the transition and observation models, and on the map (see e.g. [2], [28] and [32]). In [28] and [25], it is proposed to see the SLAM as an inference problem in HMM: the localization of the robot is the hidden state with Markovian dynamic, and the map is seen as an unknown parameter. Therefore, the mapping problem is answered by solving the inference task, and the localization problem is answered by approximating the conditional distribution of the hidden states given the observations.

In this application, we consider a statistical model for a landmark-based SLAM problem for a bicycle manoeuvring on a plane surface.

Let be the robot position, where and are the robot’s cartesian coordinates and its orientation. At each time step, deterministic controls are sent to the robot so that it explores a given part of the environment. Controls are denoted by where stands for the robot’s heading direction and its velocity. The robot position at time , given its previous position at time and the noisy controls , can be written as

| (14) |

where is a -dimensional Gaussian distribution with mean and known covariance matrix . In this contribution we use the kinematic model of the front wheel of a bicycle (see e.g. [1]) where the function in (14) is given by

where is the time period between two successive positions and is the robot wheelbase.

The -dimensional environment is represented by a set of landmarks , being the position of the th landmark. The total number of landmarks and the association between observations and landmarks are assumed to be known.

At time , the robot observes the distance and the angular position of all landmarks in its neighborhood; let be the set of observed landmarks at time . It is assumed that the observations are independent and satisfy

where is defined by

and the noise vectors are i.i.d Gaussian . is assumed to be known.

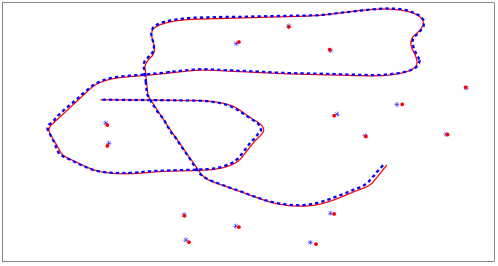

The model presented in this Section does not take into account all the issues arising in the SLAM problem (such as the association process which is assumed to be known and the known covariance matrices). The aim is to prove that the BOEM algorithm and its averaged version have satisfying behavior even in the challenging framework described above. The observation and motion models are highly nonlinear and we show that the BOEM algorithm remains stable in this experiment. Several solutions have been proposed to solve the association problem (see e.g. [2] for a solution based on the likelihood of the observations) and could be adapted to our case. We want to estimate by applying the P-BOEM algorithms. In this paper, we use simulated data. landmarks are drawn in a square of size . The robot path is sampled with a given set of controls. Using the true positions of all landmarks in the map and the true path of the robot (see the dots and the bold line on Figure 4), observations are sampled by setting: where , and . We choose where , and .

In this model, the transition denoted by does not depend on the map (see (14)) and the marginal likelihood is such that the complete data likelihood does not belong to the curved exponential family:

| (15) |

Hence, in order to apply Algorithm 1, at the beginning of each block, is approximated by a function depending on the current parameter estimate so that the resulting approximated model belongs to the curved exponential family (see [25]). As can be seen from (15), approximating the function by its first-order Taylor expansion at leads to a quadratic approximation of . This approach is commonly used in the SLAM framework to use the properties of linear Gaussian models (see e.g. [2]).

As the landmarks are not observed all the time, we choose a slowly increasing sequence so that the number of updates is not too small (in this experiment, we have updates for a total number of observations of ). As the total number of observations is not so large (the largest block is of length ), the number of particles is chosen to be constant on each block: for all , . For the SMC step, we apply Algorithm 2 with the bootstrap filter.

For each run the estimated path (equal to the weighted mean of the particles) and the estimated map at the end of the loop () are stored. Figure 4 represents the mean estimated path and the mean map over independent Monte Carlo runs. It highlights the good performance of the P-BOEM algorithm in a more complex framework.

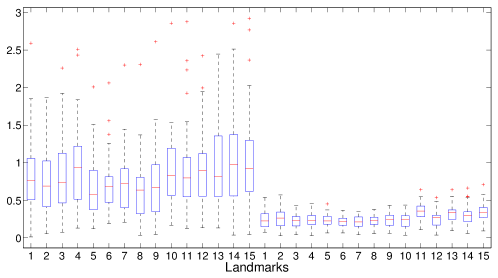

We also compare our algorithm to the marginal SLAM algorithm proposed by [28]. In this algorithm, the map is also modeled as a parameter to learn in a HMM model; SMC methods are used to estimate the map in the maximum likelihood sense. The Marginal SLAM algorithm is a gradient-based approach for solving the recursive maximum likelihood procedure. Note that, in the case of i.i.d. observations, [35] proposed to update the parameter estimate each time a new observation is available using a stochastic gradient approach. Figure 5 illustrates the estimation of the position of each landmark. The P-BOEM algorithm is applied using the same parameters as above and the marginal SLAM algorithm uses a sequence of step-size . We use the averaged version of the P-BOEM algorithm and a Polyak-Ruppert based averaging procedure for the marginal SLAM algorithm (see [33]). For each landmark the last estimation (at the end of the loop) of the position is stored for each of the independent Monte Carlo runs. Figure 5 displays the distance between the estimated position and the true position for each landmark. In this experiment, the P-BOEM based SLAM algorithm outperforms the marginal SLAM algorithm.

4 Convergence of the Particle Block Online EM algorithms

In this section, we analyze the limiting points of the P-BOEM algorithm. We prove in Theorem 4.3 that the P-BOEM algorithm has the same limit points as a so-called limiting EM algorithm, which defines a sequence by where is the a.s. limit (defined by (6)). As discussed in [23, Section 4.3.], the set of limit points of the limiting EM algorithm is the set of stationary points of the contrast function , defined as the a.s. limit of the normalized log-likelihood of the observations, when . The convergence result below on the P-BOEM algorithm requires two sets of assumptions: conditions AA2 to AA5 are the same as in [23] and imply the convergence of the BOEM algorithm; assumptions AA6 and AA7 are introduced to control the Monte Carlo error.

4.1 Assumptions

Consider the following assumptions

-

A2

There exist and s.t. for any and any , . Set

Define, for all ,

| (16) |

For any sequence of r.v. on , let

| (17) |

be -fields associated to . We also define the mixing coefficients by, see [7],

| (18) |

where for any -algebras and ,

| (19) |

For and a -valued random variable measurable w.r.t. the -algebra , set

-

A3

-()

-

A4

-

(a)

is a stationary sequence such that there exist and satisfying, for any , , where is defined in (18).

-

(b)

.

-

(a)

-

A5

There exist and such that for all , .

Assumptions AA2 to AA5 are the same as in [23]. AA2, referred to as the strong mixing condition, is used to prove the uniform forgetting property of the initial condition of the filter, see e.g. [11] and [12]. This assumption is easy to check in finite state-space HMM or when the state-space is compact when the Markov kernel is sufficiently regular. As noted in [23], it can fail to hold in quite general situations. Nevertheless, the exponential forgetting property needed to ensure the convergence results could be checked under weaker assumptions (see [15] for a Doeblin assumption). However, it would imply quite technical supplementary results out of the scope of this paper. Examples of observation sequences satisfying AA4 include, for example, stationary -irreducible and positive recurrent Markov chains which are geometrically ergodic (see e.g. [31] for Markov chains theory).

4.2 -error of the SMC approximation

4.3 Asymptotic behavior of the Particle Block Online EM algorithms

Following [23], we address the convergence of the P-BOEM algorithm as the convergence of a perturbed version of the limiting EM recursion. The following result, which is proved in [23, Theorem 4.1.], shows that when is large, the BOEM statistic is an approximation of a deterministic quantity ; the limiting EM algorithm is the iterative procedure defined by where

| (20) |

the mapping is given by AA1.

Theorem 4.2.

The asymptotic behavior of the limiting EM algorithm is addressed in [23, Section ]: the main ingredient is that the map admits a positive and continuous Lyapunov function w.r.t. the set

| (22) |

i.e. (i) for any and, (ii) for any compact subset of , . This Lyapunov function is equal to , where the contrast function is the (deterministic) limit of the normalized log-likelihood of the observations when (see [24, Theorem ]).

Theorem 4.3 establishes the convergence of the P-BOEM algorithm to the set defined by (22). The proof of Theorem 4.3 is an application of [23, Theorem ]. An additional assumption on the number of particles per block is required to check [23, A] (note indeed that AA8 below and Proposition 4.1 imply the condition in [23] about the -control of the error).

-

A8

There exist and (where is given by AA5) such that, for all , .

Theorem 4.3.

The assumption on made in Theorem 4.3 is in common use to prove the convergence of EM based procedures or stochastic approximation algorithms. It is used in [36] to find the limit points of the classical EM algorithm. See also [13] and [20] for the stability of the Monte Carlo EM algorithm and of a stochastic approximation of the EM algorithm. If is sufficiently regular, Sard’s theorem states that has Lebesgue measure and hence has an empty interior.

Under the assumptions of Theorem 4.3, it can be proved that, along any converging P-BOEM sequence to in , the averaged P-BOEM statistics defined by (7) (see also (9)) converge to , see Proposition 5.2. Since is continuous, the averaged P-BOEM sequence converges to . Since , , showing that the averaged P-BOEM algorithm has the same limit points as the P-BOEM algorithm.

4.4 Rate of convergence of the Particle Block Online EM algorithms

In this section, we consider a converging P-BOEM sequence with limiting point . It can be shown, as in [24, Proposition ], that the convergence of the sequence is equivalent to the convergence of the sufficient statistics : along any P-BOEM sequence converging to , this sequence of sufficient statistics converges to . Let be the limiting EM map defined on the space of sufficient statistics by

| (23) |

To that goal consider the following assumption.

-

A9

-

(a)

and are twice continuously differentiable on and .

-

(b)

where denotes the spectral radius.

-

(a)

We will use the following notation: for any sequence of random variables , write if ; and if

Theorem 4.4.

Eq. (24) shows that the error has a -norm decreasing as . This result is obtained by assuming , with , which implies that the SMC error and the BOEM error are balanced. Unfortunately, such a rate is obtained after a total number of observations ; therefore, as discussed in [23], it is quite sub-optimal. Eq (25) shows that the rate of convergence equal to the square root of the total number of observations up to block , can be reached by using the averaged P-BOEM algorithm: the -norm of the error has a rate of convergence proportional to . Here again, note that since is chosen as in AA8 the SMC error and the BOEM error are balanced.

5 Proofs

For a function , define .

5.1 Proof of Proposition 4.1

For any , define the -algebra by

| (26) |

We use as a shorthand notation for . Under AA2 and AA6, Propositions B.., B.. and B.. in Appendix B of [22] can be applied so that

| (27) |

where

By the Hölder inequality applied with and ,

By AA2, AA3-(), AA4(a) and AA7-(), we have

Using similar arguments for yields , which concludes the proof.

5.2 -controls

Proposition 5.1.

Proof.

Proposition 5.2.

Proof.

By (7), can be written as

| (28) |

By Theorem 4.2, is continuous so, by the Cesaro Lemma, the second term in the right-hand side of (28) converges to -a.s., on the set . By Proposition 5.1, there exists a constant such that for any ,

Hence, by AA5, AA8 and the Borel-Cantelli Lemma,

The proof is concluded by applying the Cesaro Lemma. ∎

Appendix A Detailed SMC algorithm

In this section, we give a detailed description of the SMC algorithm used to compute sequentially the quantities , . This is the algorithm proposed by [4] and [10].

At each time step, the weighted samples are produced using sequential importance sampling and sampling importance resampling steps. In Algorithm 2, the instrumental proposition kernel used to select and propagate the particles is (see (13) and [16, 17, 27] for further details on this SMC step).

It is readily seen from the description below that the observations are processed sequentially.

Appendix B -controls of SMC approximations

In this section, we give further details on the control on each block (see (27)):

is defined by (6) (we recall that, being fixed, it is dropped from the notations) and is the SMC approximation of based on particles computed as described in Section 2.4.

The following results are technical lemmas taken from [16] (stated here for a better clarity) or extensions of the controls derived in [19].

Hereafter, “time ” corresponds to time in the block . Therefore, even if it is not explicit in the notations (in order to make them simpler), the following quantities depend upon the observations .

Denote by the filtering distribution at time , and let

be the backward kernel smoothing kernel at time . For all and for all bounded measurable function on , define recursively backward in time, according to

| (29) |

starting from . By convention, .

For , let be the weighted samples obtained as described in Section 2.4 (see also Algorithm 2 in Appendix A); it approximates the filtering distribution . Denote by this approximation. For , an approximation of the backward kernel can be obtained

and inserting this expression into (29) gives the following particle approximation of the fixed-interval smoothing distribution

| (30) |

with .

Lemma B.1.

For all and all bounded measurable function on , define the kernel by

| (33) |

by convention, . Let and be two kernels on defined for all by

| (34) | ||||

| (35) |

Note that

| (36) |

Lemma B.2.

Proof.

By definition of ,

We write

where we used the convention

We have for all ,

Therefore, for all ,

∎

Proposition B.3.

For any , we recall the definition of given by (26)

where are the weighted samples obtained by Algorithm 2 in Appendix A, with input variables , , .

Lemma B.4.

Proof.

By definition of the weighted particles,

∎

Lemma B.5.

Assume AA2 and AA6. Let be the weighted samples obtained by Algorithm 2 in Appendix A, with input variables , , .

-

(i)

For any and any measurable function on , the random variables are:

-

(a)

conditionally independent and identically distributed given ,

-

(b)

centered conditionally to .

-

(a)

- (ii)

-

(iii)

For all and any ,

Proof.

The proofs of Propositions B.6 and B.7 follow the same lines as [19, Propositions -]. The upper bounds given here provide an explicit dependence on the observations.

Proposition B.6.

Proof.

By Lemma B.5(i) and since is -measurable for all , is a martingale difference. Since , Burkholder’s inequality (see [21, Theorem 2.10, page 23]) states the existence of a constant depending only on such that:

Hence,

which implies, using the convexity inequality ,

Since and are -measurable,

By Lemma B.5(i), using again the Burkholder and convexity inequalities, there exists s.t.

The proof is concluded by (43). ∎

Proposition B.7.

Proof.

References

- [1] T. Bailey, J. Nieto, J. Guivant, M. Stevens, and E. Nebot. Consistency of the EKF-SLAM algorithm. In IEEE International Conference on Intelligent Robots and Systems, pages 3562–3568, 2006.

- [2] W. Burgard, D. Fox, and S. Thrun. Probabilistic robotics. Cambridge, MA:MIT Press, 2005.

- [3] O. Cappé. Online sequential Monte Carlo EM algorithm. In IEEE Workshop on Statistical Signal Processing (SSP), pages 37–40, 2009.

- [4] O. Cappé. Online EM algorithm for Hidden Markov Models. To appear in J. Comput. Graph. Statist., 2011.

- [5] O. Cappé and E. Moulines. Online Expectation Maximization algorithm for latent data models. J. Roy. Statist. Soc. B, 71(3):593–613, 2009.

- [6] O. Cappé, E. Moulines, and T. Rydén. Inference in Hidden Markov Models. Springer. New York, 2005.

- [7] J. Davidson. Stochastic Limit Theory: An Introduction for Econometricians. Oxford University Press, 1994.

- [8] P. Del Moral. Feynman-Kac Formulae. Genealogical and Interacting Particle Systems with Applications. Springer. New York, 2004.

- [9] P. Del Moral, A. Doucet, and S.S. Singh. A Backward Particle Interpretation of Feynman-Kac Formulae. ESAIM M2AN, 44(5):947–975, 2010.

- [10] P. Del Moral, A. Doucet, and S.S. Singh. Forward smoothing using sequential Monte Carlo. Technical report, arXiv:1012.5390v1, 2010.

- [11] P. Del Moral and A. Guionnet. Large deviations for interacting particle systems: applications to non-linear filtering. Stoch. Proc. App., 78:69–95, 1998.

- [12] P. Del Moral, M. Ledoux, and L. Miclo. On contraction properties of Markov kernels. Probab. Theory Related Fields, 126(3):395–420, 2003.

- [13] B. Delyon, M. Lavielle, and E. Moulines. Convergence of a stochastic approximation version of the EM algorithm. Ann. Statist., 27(1), 1999.

- [14] A. P. Dempster, N. M. Laird, and D. B. Rubin. Maximum likelihood from incomplete data via the EM algorithm. J. Roy. Statist. Soc. B, 39(1):1–38 (with discussion), 1977.

- [15] R. Douc, G. Fort, E. Moulines, and P. Priouret. Forgetting the initial distribution for hidden Markov models. Stochastic Processes and their Applications, 119(4):1235–1256, 2009.

- [16] R. Douc, A. Garivier, E. Moulines, and J. Olsson. Sequential Monte Carlo smoothing for general state space hidden Markov models. To appear in Ann. Appl. Probab., 4 2010.

- [17] A. Doucet, N. De Freitas, and N. Gordon, editors. Sequential Monte Carlo Methods in Practice. Springer, New York, 2001.

- [18] A. Doucet, G. Poyiadjis, and S.S. Singh. Particle approximations of the score and observed information matrix in state-space models with application to parameter estimation. Biometrika, 98(1):65–80, 2010.

- [19] C. Dubarry and S. Le Corff. Non-asymptotic deviation inequalities for smoothed additive functionals in non-linear state-space models. Technical report, arXiv:1012.4183v1, 2011.

- [20] G. Fort and E. Moulines. Convergence of the Monte Carlo Expectation Maximization for curved exponential families. Ann. Statist., 31(4):1220–1259, 2003.

- [21] P. Hall and C. C. Heyde. Martingale Limit Theory and its Application. Academic Press, New York, London, 1980.

- [22] S. Le Corff and G. Fort. Convergence of a particle-based approximation of the Block Online Expectation Maximization algorithm. Technical report, arXiv, 2011.

- [23] S. Le Corff and G. Fort. Online Expectation Maximization based algorithms for inference in Hidden Markov Models. Technical report, arXiv:1108.3968v1, 2011.

- [24] S. Le Corff and G. Fort. Supplement paper to "Online Expectation Maximization based algorithms for inference in Hidden Markov Models". Technical report, arXiv:1108.4130v1, 2011.

- [25] S. Le Corff, G. Fort, and E. Moulines. Online EM algorithm to solve the SLAM problem. In IEEE Workshop on Statistical Signal Processing (SSP), 2011.

- [26] F. Le Gland and L. Mevel. Recursive estimation in HMMs. In Proc. IEEE Conf. Decis. Control, pages 3468–3473, 1997.

- [27] J.S. Liu. Monte Carlo Strategies in Scientific Computing. Springer, New York, 2001.

- [28] Ruben Martinez-Cantin. Active Map Learning for Robots: Insights into Statistical Consistency. PhD thesis, University of Zaragoza, 2008.

- [29] G. J. McLachlan and T. Krishnan. The EM Algorithm and Extensions. Wiley. New York, 1997.

- [30] G. J. McLachlan and S. K. NG. On the choice of the number of blocks with the incremental EM algorithm for the fitting of normal mixtures. Statistics and Computing, 13(1):45–55, 2003.

- [31] S. P. Meyn and R. L. Tweedie. Markov Chains and Stochastic Stability. Springer, London, 1993.

- [32] M. Montemerlo, S. Thrun, D. Koller, and B. Wegbreit. FastSLAM 2.0: An improved particle filtering algorithm for simultaneous localization and mapping that provably converges. In Proceedings of the Sixteenth IJCAI, Mexico, 2003.

- [33] B. T. Polyak. A new method of stochastic approximation type. Autom. Remote Control, 51:98–107, 1990.

- [34] Vladislav B. Tadić. Analyticity, convergence, and convergence rate of recursive maximum-likelihood estimation in hidden Markov models. IEEE Trans. Inf. Theor., 56:6406–6432, December 2010.

- [35] D. M. Titterington. Recursive parameter estimation using incomplete data. J. Roy. Statist. Soc. B, 46(2):257–267, 1984.

- [36] C. F. J. Wu. On the convergence properties of the EM algorithm. Ann. Statist., 11:95–103, 1983.