The space of probability distributions on a given sample

space possesses natural geometric properties.

For example, in the case of a smooth parametric family of

probability distributions on the real line, the parameter

space has a Riemannian structure induced by the embedding

of the family into the Hilbert space of square-integrable

functions, and is characterised by the

Fisher-Rao metric. In the nonparametric case the relevant

geometry is determined by the spherical distance function

of Bhattacharyya. In the context of term structure

modelling, we show that minus the derivative of the

discount function with respect to the maturity date gives

rise to a probability density. This follows as a

consequence of the positivity of interest rates.

Therefore, by mapping the density functions associated

with a given family of term structures to Hilbert space,

the resulting

metrical geometry can be used to analyse the relationship

of yield curves to one another. We show that the general

arbitrage-free yield curve dynamics can be represented

as a process taking values in the convex space of smooth

density functions on the positive real line. It follows

that the theory of interest rate dynamics can

be represented by a class of processes in Hilbert space.

We also derive the dynamics for the central moments

associated with the distribution determined by the

yield curve. (26 June 2000)

Keywords: Interest rate models, Heath-Jarrow-Morton

framework,

principal moments analysis, differential

geometry and statistics

1 Introduction

The theory of interest rates has gone through two major

developments in recent decades. Following initial

investigations by Merton (1973) and others, the first decisive

advance

culminated in the work of Vasicek (1977) who was able to give

a fairly general characterisation of the arbitrage-free dynamics

of a family of discount bonds, indexed by their maturity. The

well-known model that bears his name appears as an exact

solution obtained with

specialising assumptions. In the wake of Vasicek’s work were

a number of other specific interest rate models, of varying

degrees of usefulness and tractability, including, for example,

the CIR model (Cox et al. 1985) and its generalisations.

The next significant line of development, following the

general martingale

characterisation of arbitrage-free asset pricing by Harrison

Kreps (1979) and Harrison Pliska (1981), was instigated

with the recognition by Ho Lee (1986) that the initial term

structure

might be specified essentially arbitrarily, a feature that has

important practical implications. This insight was

incorporated into the HJM framework (Heath

et al. 1992), which constituted a major advance in the

subject, providing a general model-independent basis for

the analysis of interest rate dynamics and the pricing of

interest rate derivatives.

Since then there have been numerous further developments. These

include, for example, the infinite dimensional or ‘string-type’

models of Kennedy (1994), Santa-Clara Sornett (1997) and

others, the positive interest rate models of Flesaker

Hughston (1996), the potential approach of Rogers (1997),

the so-called market models (Brace et al. 1996,

1997; Jamshidian 1997), and the geometric analysis of the space

of yield curves undertaken by Björk Svensson (1999).

Nevertheless, no criterion has emerged, based on the

extensive econometric evidence available, that allows in

a rational way for the identification of a clearly

preferred class of

models. On these grounds it makes sense to try to cast the

general interest rate framework into a new form, with the

idea that certain models might thus become recognisable

as more natural on mathematical and economic grounds.

With this end in mind, the

purpose of the present article is to propose a

novel application of information geometry to interest rate

theory. The main results are (i)

the construction of a geometric measure for how ‘different’ two

term structures are from one another; (ii) a characterisation of

the evolutionary trajectory of the term structure as a

measure-valued process; (iii) the derivation of dynamics

for the principal moments of the

term structure; and (iv) a reformulation

of arbitrage-free interest rate dynamics in terms

of a class of processes on Hilbert space.

The paper is organised as follows. In §2 we review the

basic idea

of information geometry and its role

in estimation theory. The geometry of the normal

distribution is considered in detail as an illustration. In §3

a remarkable characterisation of the discount function in terms

of an abstract probability density function is introduced in

Proposition 1. This allows us to apply information geometric

techniques to determine the deviation between different term

structures within a given model. In this connection, in §4

we consider a class of flat rate models as examples.

The material of the first four sections of the paper is

essentially static, i.e., set in the present, whereas in §5

we investigate the dynamics of

the density function that generates the term structure. This is

carried out in such a way that the resulting dynamics is

manifestly arbitrage-free. Our key result here is formula

(5.47), in which we establish that the dynamics of the

term structure can be characterised as a measure-valued process.

This idea is developed further in Proposition 2.

In §6 we introduce an analogue of the classical principal

components analysis for yield curves, and in Propositions 3 and

4 we derive formulae for the evolution of the first two moments

of the term structure density process. Then, making use of the

information geometry developed earlier, in §7 we map the

dynamics developed in §5 to Hilbert space. Our main result

here is Proposition 5, which shows how this can be achieved.

2 Information geometry

Because some of the mathematical

techniques we employ here may not be

familiar to those working in finance, it will be appropriate to

begin with a few background remarks. It has long been known

(see, e.g., Amari 1985; Kass 1989; Murray Rice 1993) that

a useful

approach to statistical inference is to regard a parametric model

as a differentiable manifold equipped with a metric. The

recognition that a parametric family of probability distributions

has a natural geometry associated with it arose in the work of

Mahalanobis (1936), Bhattacharyya (1943) and Rao (1945) over

half of a century ago.

Suppose, for example, that is a continuous random variable

taking values on the real line , and that is

a density function for . Because is nonnegative and has

integral unity, it follows that the square-root

likelihood function

(2.1)

exists for all , and satisfies the normalisation condition

(2.2)

We see that can be regarded

as a unit vector in the Hilbert space

. Now let

denote a

pair of density functions on , and the corresponding Hilbert space elements.

Then the inner product

(2.3)

defines an angle which can be interpreted as the distance between the two probability distributions. More

precisely, if we write for the unit sphere in

, then is the spherical distance

between the points on determined by the vectors

and .

The maximum possible distance, corresponding to nonoverlapping

densities, is given by . This follows from the fact

that and are nonnegative functions,

and thus define points on the positive orthant of .

We remark that an alternative way of expressing (2.3)

is

(2.4)

which makes it apparent that the angle measures

the extent to which the two distributions are distinct.

The spherical distance of Bhattacharyya introduced above is

applicable in a nonparametric context. In the case of a

parametric family of probability distributions we can develop

matters further. Let us write

for the parameterised density function. Here

stands for a set of parameters

. By varying we obtain an

-dimensional submanifold in

determined by the unit vectors .

The parameters are local coordinates

for .

The key point that we require in the

following (cf. Dawid 1977) is that the spherical geometry

of induces a Riemannian geometry on

, for which the metric tensor is

given, in local coordinates, by

(2.5)

By use of definition (2.1), we see that an alternative

expression for is

(2.6)

which shows (cf. Brody Hughston 1998) that the metric

is, apart from the factor of , the Fisher

information matrix, i.e., the covariance matrix of the parametric

gradient of the log-likelihood function (Fisher 1921). We refer

to as the Fisher-Rao metric on the

statistical model .

The significance of the Fisher-Rao metric in estimation theory

is well known. Suppose that is some given function

of the parameters, and that the random variable represented

by the function on is

an unbiased estimator for in the sense that

(2.7)

The variance of the estimator is defined, as usual, by

(2.8)

Then a set of fundamental bounds on , independent

of the choice of the estimator , can be obtained

by applying the operator to (2.7), letting be

arbitrary. By use of (2.1) and

the Schwartz inequality for , we obtain

(2.9)

This matrix inequality is interpreted as saying that if

we subtract the right side from the left, the result is

nonnegative definite. It follows that if the

random variables are unbiased

estimators for the parameters , satisfying

(2.10)

then the covariance matrix of the estimators is bounded by the

inverse Fisher information matrix:

(2.11)

The Riemannian metric (2.5) introduced above can be

used to define a distance measure between two distributions

belonging to a given parametric

family. This measure is invariant in the sense that it is

unaffected by a reparameterisation of the distributions. The

distance is calculated by integrating the infinitesimal line

element along the geodesic connecting the two points in

the statistical manifold , where

(2.12)

The geodesics with respect to a given metric

are the solutions of the differential

equation

(2.13)

for the curve in , subject to

the given boundary conditions at the two end points. Here,

we have written

(2.14)

where , and the inverse

metric , also appearing in (2.11), satisfies

, where

is the Kronecker delta. Note that in

equations (2.13) and (2.14) above, and elsewhere

henceforth in this article, we employ the standard Einstein

summation convention on repeated indices.

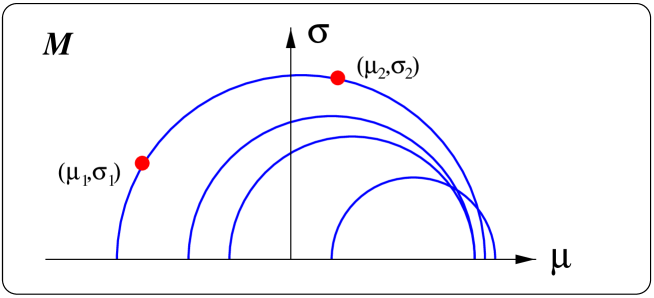

Figure 1: Geodesic curves for normal distributions. The

statistical manifold in this case is the upper

half plane parameterised by and . We have

and . The

shortest path joining the two normal distributions

and

is given by the unique

semi-circular arc through the given two points and centred

on the boundary line .

Let us consider, as an explicit example, the manifold

corresponding

to the normal distributions on

, with mean and standard deviation

. For the parameterised density function we have

(2.15)

A straightforward computation, making use of (2.6),

gives

(2.16)

for the line element, which is defined on the upper half-plane

, . The resulting Riemannian

geometry is that of hyperbolic space, which is a homogeneous

manifold with constant negative curvature. The geometry of this

space has been studied extensively, and has many intriguing

properties. For the distance function in the

case of a pair of normal distributions

,

we obtain

(2.17)

where the function , defined by

(2.18)

lies between 0 and 1. The geodesics, in particular, are given

in general by semi-circular arcs

centred on the boundary line (this line itself is

not part of the manifold ). An exceptional situation

arises when , for which the geodesic is a

straight line given by constant , and we have

(2.19)

We refer the reader to Burbea (1986), where metric and

distance computations have been carried out explicitly for

other families of distributions.

3 Discount bond densities

Our goal now is to make use of the analysis presented in the

previous section to construct a natural metric on the space of

yield curves. In doing so we shall take advantage of a remarkable

‘probabilistic’ characterisation of discount bonds, which we here

proceed to describe.

Let denote the present, and a smooth

family of discount bonds, where is the maturity date

. For positive interest we require

(3.20)

and we assume that as goes to

infinity. A term structure that satisfies these conditions

will be said to be ‘admissible’. These conditions can,

in fact, be relaxed slightly:

need not be strictly smooth, nor strictly decreasing;

but for most of the present discussion we shall

stick with the assumptions indicated.

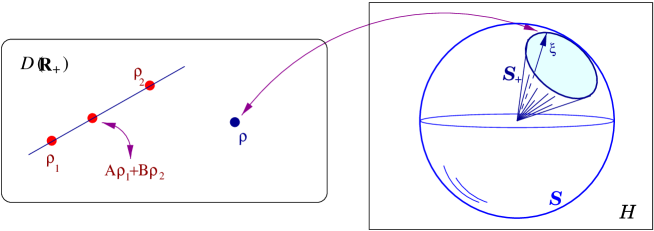

Figure 2: The system of admissible term structures.

A smooth positive interest term structure can be regarded

as a point in , the convex

space consisting of smooth density functions on

. The points of

are in one-to-one correspondence with rays lying in the

positive orthant of the unit sphere

in the Hilbert space .

The interesting point that arises here, of which we shall

make extensive use in the discussions that follow, is that

the discount function can be viewed as a

complementary probability distribution. In other words, we

think of the maturity date as an abstract random variable ,

and for its distribution we write

(3.21)

It should be clear that this can be done if and only if the

positive interest rate conditions given in (3.20) hold.

As a consequence we are able to embody the positive interest

property in a fundamental way in the structure of the theory.

Indeed, this basic economic property is essential if we wish

to treat the yield curve consistently and naturally as a kind

of mathematical object in its own right. Now let us introduce

the function defined by

(3.22)

Clearly, we have and

(3.23)

from which we infer that can be consistently viewed as

a probability density function. It follows from the defining

equation (3.22) that the term structure density

is the product of the instantaneous forward

rate and the discount function itself. Now clearly if

and are admissible term structure

densities, and if and are nonnegative constants satisfying

, then is also an admissible

term structure density. Putting these ingredients together, we

see that the term structure of interest rates can be given the

following general characterisation.

Proposition 1

The system of admissible term structures is isomorphic to the

convex space of smooth density

functions on the positive real line.

At first glance it may seem odd to think of the discount function

in this manner. However, it gives us the advantage of being able to

apply the tools of information geometry in an unexpected way, as

we indicate in what follows.

In particular, there is a one-to-one map from the space

of such term structure densities to

the positive orthant of the unit sphere

in the Hilbert space , as indicated in Figure 2.

Therefore, given two yield

curves we can calculate the distance between them. This can be

carried out either in a nonparametric sense, by use of the

Bhattacharyya spherical distance, or in a parametric sense, by

use of the Fisher-Rao distance. In the former case first we

calculate the corresponding term structure densities

and . These are then mapped to by

taking the square-roots, and their distance is given by

(3.24)

In the parametric case we regard the given parametric family of

yield curves as defining a statistical model , and the distance between the two yield curves

within the given family is then defined by the Fisher-Rao metric.

4 Flat term structures

To provide some illustrations of the principles set

forth in the previous section we consider here properties of

yield curves for which the term structure is flat. Such

yield curves, which are of various types, are on the whole

too simple for use in practical modelling. Nevertheless,

they are of interest as examples, because many of the relevant

computations can be carried out explicitly.

In this connection we begin by introducing a representation of

the discount function as a Laplace transform

(4.25)

for some function . Thus we think of the discount

function as being given by a weighted superposition

of elementary discount functions, each of the form

for some value of . Taking the limit , we

find that must satisfy .

In general the inverse Laplace transform need not

be positive. However, if we restrict our consideration to

nonnegative functions, then can be interpreted as

a density function, and by various

choices of we are led to some interesting

candidates for term structures.

First we consider the case where is

a Dirac -function concentrated at a point, that is,

. A direct substitution gives

,

corresponding to a ‘flat’ term structure with a continuously

compounded rate for each value of the maturity date .

If the density function is given by an exponential

distribution , with parameter

, then one sees that must have dimensions of

time, and a short calculation gives ,

which also corresponds to a flat term structure, in this

case with a simple percentage yield of for all

maturities. We see that the characteristic time-scale

allows us to define an interest rate , which

turns out to be the characteristic interest rate of the

resulting structure, and we can write

for the discount function.

We note that flatness is not a completely unambiguous notion,

because having a uniform continuously compounded yield for all

maturities is not the same thing as having a uniform simple

yield for all maturities. Both define plausible albeit quite

distinct systems of discount bonds. This example illustrates

how by superposing term structures of the elementary form

for various maturities, we can obtain other

reasonable looking and well behaved term structures.

We mention one more example, which contains the

previous two examples as special cases. Consider the

standard gamma distribution, with parameters and

, defined for nonnegative values of by the

density function

(4.26)

In this case, we can verify that the resulting system of

discount bonds is given by

(4.27)

which assumes a more recognisable form if we set

, where again defines a characteristic

time scale, and is a dimensionless number. Then we have

(4.28)

where . The system of discount bonds

arising here can also be interpreted as a flat term structure,

in this case with a constant annualised rate of interest

assuming compounding at the frequency over the life

of each bond ( need not be an integer). It is not

difficult to check that for this reduces to the

case of a flat rate on the basis of a simple yield, whereas

in the limit we recover the case of

a flat rate on the basis of continuous compounding.

Now we shall apply the ideas of statistical geometry to make

comparisons between various term structures of the form

(4.28). For density function in this case we obtain

(4.29)

Here we find it convenient to label the density function

by the flat rate . Note that in the limit

we have

. First consider

the nonparametric separation between

different term structures in this model via spherical distance

of Bhattacharyya given in formula (3.24), where in the

present example we write for

. A direct integration leads to the expression

(4.30)

for the distance when , whereas in the limit

(continuous compounding) we have

(4.31)

It is interesting to observe that the bracketed term in

(4.31) is given by the ratio of the geometric and

arithmetic means of the two rates.

Alternatively, we can view (4.29) as a parametric

family of distributions, parameterised by the flat rate .

Then it is natural to consider the Fisher-Rao distance

between the two term structures characterised by and

. A straightforward calculation then leads to a

simple distance formula given by

(4.32)

where we have assumed .

5 Interest rate dynamics

The formalism we have developed so far is essentially a static

one, set in the present. Now we turn to the problem of developing

a dynamical theory of interest rates. The idea is that, at each

instant of time, the yield curve is characterised by a term

structure density according to the scheme described in the previous

sections. Then, as time passes, the density function evolves

randomly. As a consequence we obtain a measure-valued process.

In particular, we obtain a process on .

Our goal in this section is to determine a set of conditions on

this process necessary and sufficient to ensure that the resulting

interest rate dynamics will be arbitrage-free.

We shall assume the reader is familiar with the general theory

of interest rate dynamics as laid out, for example, in Carverhill

(1994), Rogers (1994), Hughston (1996), Baxter (1997), Musiela

Rutkowski (1997), Brody (2000) or Hunt Kennedy (2000).

For the general discount bond dynamics, let us write

(5.33)

where and are the absolute drift

and absolute volatility processes, respectively, for a bond

with maturity . Here,

is a vector Brownian motion, and is a

vector process, and there is an inner product implied between

and , signified by a dot. We need not

specify the dimensionality of the Brownian motion, which might

be infinite, and indeed in some respects the infinite dimensional

setting is the most natural one.

In fact, it suffices for our purposes merely to

assume that is a one-parameter family of

continuous semi-martingales on the given probability space, with

respect to the given filtration. However, for simplicity of

exposition we shall stick to the case where the relevant

stochastic basis is generated by a multidimensional Brownian

motion. Here, as in Flesaker Hughston (1997a,b), we

regard the discount bond dynamics as the natural

starting position, rather than, say, the instantaneous forward

rate dynamics (Heath et al. 1992), which we need not

consider here directly. We shall assume nevertheless, as in the

HJM framework, that the

processes and are both smooth in the

variable , and that sufficiently strong technical

conditions are in place to ensure that the instantaneous

forward rate processes are semimartingales.

In order to extend the analysis of the previous section it is

convenient to introduce what is sometimes conveniently referred

to as the ‘Musiela parameterisation’, given by

(5.34)

where represents the maturity date of the bond, and

hence is the time left until maturity. Thus is the

value at time of a discount bond that has years left to

mature. This choice of parameterisation has already been shown

to be useful in the geometric analysis of interest rates

(Björk Svensson 1999, Björk Christensen 1999,

Björk Gombani 1999, Björk 2000). We note that

for all

, and that as . It

follows that

(5.35)

is a measure-valued process in the sense that, for each

value of the random function satisfies

and the normalisation condition

(5.36)

Here we have chosen the

notation that makes the dependence more

prominent, to emphasise the fact that, for each value of ,

and conditional on information given up to time ,

is a density function, though we might have

written instead. As a consequence

describes a process on . By

consideration of (5.33) and (5.34) we deduce

for the dynamics of that

where . Differentiating this

expression with respect to and introducing the measure-valued

process according to formula (5.35) we

therefore obtain

(5.39)

A further simplification is then achieved by introducing the

notation

(5.40)

and

(5.41)

which gives us

(5.42)

In the foregoing discussion we have not yet imposed the

arbitrage-free condition. This is given by the drift constraint

(5.43)

where is the process for the market price of risk.

We note that , like , is a vector

process. However, does not depend on the maturity

. The absence of arbitrage ensures the existence of

. For our purposes we do not need to insist that

the bond market is complete: all we require is the existence

of a pricing kernel, or equivalently the existence of a

self-financing

‘natural numeraire’ portfolio with value process such

that is a martingale for each value of

(cf. Flesaker Hughston 1997c). The numeraire process

satisfies

(5.44)

and the corresponding pricing kernel is given by .

As a consequence of the constraint (5.43) we then

have

(5.45)

and therefore, by differentiation of this expression with

respect to , we obtain

(5.46)

Inserting (5.46) in (5.42) we are thus able to

express the dynamics of the density function in the

form

(5.47)

Before proceeding further, let us verify, as a consistency check,

that the dynamics given by (5.47) preserves the

normalisation condition on , given by (5.36).

Integrating the right hand side of (5.47) with respect to

and equating the drift and volatility terms separately to zero

leads to the relations

(5.48)

and

(5.49)

which must hold for all . Condition (5.48) is satisfied

because as and

(5.50)

Condition (5.49) is satisfied because, by definition,

we have

, and the absolute

volatility vanishes both as (a

maturing bond has a definite value and thus has no absolute

volatility), and as (a bond with infinite

maturity has no value, and hence no absolute volatility).

Summing up matters so far, we see that in (5.47) we are

able to cut the standard HJM arbitrage-free interest rate dynamics

in the form of a measure-valued process subject to

the constraints (5.48) and (5.49). At first

glance the role of the short rate in (5.47) seems

anomalous, because it might appear that this has to be specified

separately. However, by virtue of (5.50) we can

incorporate directly into the dynamics of .

In fact, there is another way of expressing (5.47) which

is very suggestive, and ties in naturally with the Hilbert space

approach to dynamics introduced in §7. First

we note that (5.48) can be rewritten in the form

(5.51)

In other words, is minus the expectation of the gradient

of the log-likelihood function. Here the expectation is taken

with respect to itself. Writing for this

abstract expectation, we have

(5.52)

where .

We note that has the interpretation of being a

Brownian motion with respect to the risk-neutral measure

associated with the given pricing kernel. In the risk-neutral

measure, for which the term

involving effectively disappears, the remaining

drift for is determined by the deviation of

from its abstract mean.

Let us now examine more closely the volatility term

appearing in (5.52), with a view to gaining

a better understanding of the significance of the volatility

constraint

(5.49). Because must remain positive

for all values of , the coefficient of

in (5.52) must be of the form

(5.53)

for some bounded process , to ensure that

dies off appropriately for values of such

that approaches zero. As a consequence, we can

write (5.47) in the quasi-lognormal form

where is an exogenously specifiable unconstrained

process. Here, for any process we define

.

The results established above can then be summarised as follows.

Proposition 2

The general admissible term structure evolution based on the

information set generated by a multidimensional Brownian motion

is given by a measure-valued process in

satisfying

(5.57)

where the processes and are

specified exogenously, along with the initial term structure

density .

An advantage of the particular expression (5.57)

given for the dynamics above is that the preservation of the

normalisation condition on is evident by

inspection, because this is equivalent to the relation

(5.58)

An alternative expression for (5.57), which brings

out more explicitly the nonlinearities in the dynamics, is

given by

(5.59)

where as

defined earlier.

6 Principal moment analysis

The characterisation of the yield curve as an abstract probability

density enables us to develop a rigourous analogue of the classical

‘principal component’ analysis often used in the study of yield

curve dynamics. To this end we let be the density process associated with an admissible

family of discount bond prices, and define the moment processes

(6.60)

and

(6.61)

for , along with the central moment processes

(6.62)

It is important to note that in some cases the relevant moments

may not exist. For example, in the case of a continuously

compounded flat yield curve given at by the density

function , we have ,

, , and

for the first four central moments.

On the other hand, in the example of the simple flat term

structure for which we find that none

of the moments exist, on account of the fatness of the tail of

the distribution. In fact, for the flat rate term structures with

compounding frequency the moments exist only up to order

.

The first four moments, if they exist, are the mean, variance,

skewness and kurtosis of the distribution of the abstract

random variable characterising the yield curve, and we refer

to these (and other) moments as the

‘principal moments’ of the given term structure.

At the mean determines a characteristic

time-scale associated with the given term structure, and

its inverse can be thought of as an associated

characteristic yield. The difference then measures the departure of the given

term structure from flatness on a continuously compounded basis.

This is on account of the fact that in the case of an exponential

distribution the variance is given by the square of the mean.

It is legitimate to conjecture that for some purposes the

specification of, e.g., the first three or four moments will be

sufficient to provide an accurate representation of the term

structure. One way of implementing this idea is to introduce the

entropy of the given distribution, defined by

(6.63)

Because has dimensions of inverse time, is

defined only up to an overall additive constant. Therefore, the

difference of the entropies associated with two yield curves has

an invariant significance.

For yield curve calibration we

propose that should be chosen such that is

maximised subject to the constraints of the data available. For

example, if we are given as data only the mean ,

then the maximum entropy term structure is ,

where .

It is also of great interest to study the dynamics of the

principal characteristics in the case of a general admissible

arbitrage-free term structure. We examine here, in particular,

the mean and the variance processes. For this purpose we

introduce a simplified notation for

the variance process, i.e.,

(6.64)

where the mean process is given as in (6.60).

We assume that both and the discount bond volatility

fall off to zero sufficiently rapidly to ensure that

and

for , and

that the integrals and

exist for

.

A straightforward calculation then leads us to the following

conclusion:

Proposition 3

The first principal moment of an admissible,

arbitrage-free term structure satisfies the dynamical law

by use of (5.41). Then,

integrating by parts and using the assumed asymptotic behaviours

for and , we obtain the desired

result.

We note that there is a critical level for the

first principal moment given by

(6.67)

When the drift of

is positive, and the drift increases further as

increases. On the other hand, when ,

the drift of is negative, and the drift decreases

further as decreases. For the variance process, we

have:

Proposition 4

The second principal moment of an admissible,

arbitrage-free term structure satisfies the dynamical law

where we have used (5.41) and (5.54).

As a consequence of the assumed asymptotic behaviour of

and , this becomes

(6.71)

after an integration by parts. For the second term in

(6.69) we have

(6.72)

by Ito’s lemma, and thus

(6.73)

by use of Proposition 3. Combining (6.71) and

(6.73), and using the definition (6.64) we

obtain (6.68).

In this case we recall that the difference

acts as a simple measure of the extent to which the distribution

deviates from the ‘flat’ term structure. As a consequence we see

that the effect of the dynamics here is that the second principal

moment of the term structure tends to increase, i.e., has a

positive drift, providing

is already above the level given by

(6.74)

7 Hilbert space dynamics for term structures

Now that we have examined some of the advantages of expressing

the arbitrage-free interest rate term structure dynamics as a

randomly evolving density function, let us consider how we

transform to the Hilbert space representation for density

functions considered in §2. Denote by the process

for the square-root likelihood function, defined by

as before, and set

. Then the

process for the square-root density can be

written in the form

(7.80)

We recall that the volatility process arising

again in this connection, which is given more explicitly by

the ratio

(7.81)

can be specified exogenously, subject only to the

condition that it has mean zero in the measure ,

which implies that can be written in the form

(5.56).

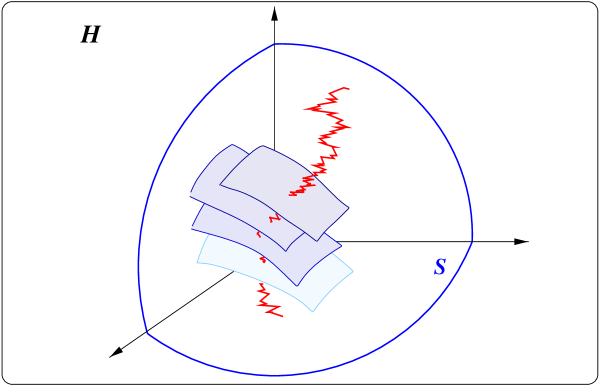

Figure 3: Interest rate dynamics. At each instant of

time the interest rate term structure can be represented as

a point on the positive orthant of the unit sphere

in the Hilbert space . The associated arbitrage-free interest

rate dynamics gives rise to a stochastic trajectory on this

space, which is foliated by hypersurfaces corresponding to

level values of the short-term interest rate.

We would now like to interpret the Hilbert space dynamics in

equation (7.80) more directly in a geometrical fashion.

For this purpose we find

it expedient to introduce an index notation, using Greek

letters to signify Hilbert space operations

(cf. Brody Hughston 1998).

Thus if the function is an element of

, we denote it by

, and if belongs to the

dual Hilbert space we denote this by

. Furthermore, their inner product

is written

(7.82)

There is a preferred symmetric quadratic form

on , given by , which thus establishes

an isomorphism between and , given by

.

Intuitively, one can think of as corresponding

to the delta function , and then we have

(7.83)

There are a number of Hilbert space technicalities

that have to be considered for a complete exposition of the

matter, but that is not our immediate concern.

If belongs to the positive orthant of

then the corresponding indexed quantity

has the interpretation of a ‘state vector’.

In that case we can think of symmetric quadratic forms as

representing certain classes of random variables.

The expectation of the random variable in the

state is

(7.84)

Therefore, a state vector determines a mapping from random

variables to real numbers, through (7.84). For a

normalised state vector we have ,

although for some purposes it is convenient to relax the

normalisation condition. In particular, we notice that the

expectation (7.84) only depends on the direction of

.

Now suppose is a positive function. In that case, the

derivative can be thought of as a linear operator

on , and we have an

endomorphism given by

.

By making use of this, we can now interpret, in the language of

Hilbert space geometry, the first two terms appearing in the

drift in the dynamical equation (7.80).

Let us begin

by noting first that (5.48) can be rewritten in the

form

(7.85)

This allows us to interpret the short term interest rate process

in terms of the mean of the symmetric part of the operator

in the state , i.e.,

(7.86)

where .

Therefore, if we let denote the symmetric

part of the operator , then the abstract

random variable in corresponding to the short rate

is given by .

Similarly we can represent the abstract random variable

for the time left until maturity in by a symmetric

matrix . It is interesting to note that the

random variables for the maturity date and

for the short term interest rate are not

‘compatible’. Two random variables and are said to be

compatible if the expression vanishes for any random variable , where

denotes the anticommutator (Segal 1947).

The lack of compatibility here indicates that the abstract

probability system containing both and

as random variables is not Kolmogorovian.

However, the algebra of random variables generated by

is Kolmogorovian.

Now, let

be an arbitrary element of ,

and let be the corresponding Hilbert space

vector. Then clearly we have

(7.87)

In other words, the first two terms of the drift in (7.80)

can be replaced by the expression , where

(7.88)

where is the Kronecker delta. Clearly,

we have .

With this in mind, let us now proceed to the interpretation of the

volatility process . Again, has the

character of a linear operator acting on , subject to

the constraint . This can be consistently

enforced if there exists a symmetric process

such that

(7.89)

The symmetric operator-valued random process

, whose existence is

thus implied, is ‘primitive’ in the sense that it is

unconstrained and can be specified exogenously. If we write

(7.90)

we obtain

(7.91)

and also

(7.92)

Therefore, putting the various ingredients together, we obtain:

Proposition 5

The dynamics of the Hilbert space vector

that characterises the term structure in an admissible,

arbitrage-free interest rate framework is governed by the

stochastic differential equation

(7.93)

where is given as in

(7.88), and the adapted operator-valued

process is expressible in the form

(7.94)

where is an arbitrary adapted

operator-valued process.

This result shows that the evolution of the yield curve can be viewed

consistently as a process on the positive orthant of the unit

sphere in Hilbert space, and thus gives rise to an entirely new

way of understanding the dynamics of the term structure. The

purpose of the quadratic term in the drift of (7.93) is

to keep the process on the sphere, and in the absence of the

term involving the operator we would have

a general local martingale on the sphere with respect to

the risk-neutral measure, where the martingale property on

is characterised in a standard way by use of the

techniques of stochastic differential geometry (see, e.g., Emery

1989, Ikeda Watanabe 1989, Hughston 1996). The term involving

the operator

splits into a

symmetric and an antisymmetric part. The drift generated by

the antisymmetric part of is generated

by a symmetry of the sphere . The drift generated

by the symmetric part of , on the other

hand, is a negative gradient vector field orthogonal to surfaces

in generated by level values of the short rate .

This term therefore creates a tendency for the vector

to drift towards a lower interest rate, a property of the negative

gradient field which is then counterbalanced by the effects of the

diffusive term.

Acknowledgements

LPH acknowledges the hospitality of the Finance Department of

the Graduate School of Business of the University of Texas at

Austin, where part of this work was carried out. DCB gratefully

acknowledges financial support from The Royal Society.

References

1

2Amari, S. (1985) Differential-Geometric

Methods in Statistics (Springer-Verlag, Berlin).

3

4Bhattacharyya, A. (1943) Proc. 29th Indian Sci.

Cong. 3, 13.

5

6Baxter, M. (1997) General Interest Rate Models, in

Mathematics of Derivative Securities, eds.

Dempster, M. A. H. Pliska, S. R. (Cambridge University

Press, Cambridge).

7

8Björk, T. Svensson, L. (1999) On the existence

of finite dimensional realisations for nonlinear forward rate

models (Preprint, Stockholm School of Economics).

9

10Björk, T. Christensen, B. J. (1999)

Mathematical Finance, 9, 323.

11

12Björk, T. Gombani, A. (1999)

Finance and Stochastics, 3, 413.

13

14Björk, T. (2000)

A Geometric View of Interest Rate Theory.

To appear in Handbook of Mathematical Finance

(Cambridge University Press, Cambridge).

15

16Brace, A., Gatarek, D. Musiela, M. (1996)

The Market Model of Interest Rate Dynamics, in Vasicek

and Beyond: Approach to Building and Applying Interest Rate

Models, ed. Hughston, L. P. (Risk Publications, London).

17

18Brace, A., Gatarek, D. Musiela, M. (1997)

Math. Finance 7, 125.

19

20Brody, D. C. (2000) Mathematical Theory of Finance

(Nihon-Hyoronsya, Tokyo).

21

22Brody, D. C. Hughston, L. P. (1998) Proc.

Roy. Soc. London 454, 2445.

23

24Burbea, J. (1986) Expo. Math. 4, 347.

25

26Carverhill, A. (1994) Stochast. Rep. 53, 227.

27

28Cox, J. C., Ingersoll, J. Ross, S. (1985)

Econometrica 53, 385.

29

30Dawid, A. P. (1977) Ann. Statist. 5, 1249.

31

32Emery, M. (1989) Stochastic Calculus on

Manifolds (Springer-Verlag, Berlin).

33

34Fisher, R. A. (1921) Phil. Trans. Roy. Soc. A

222, 309.

35

36Flesaker, B. Hughston, L. P. (1996) Risk

Magazine 9, 46.

37

38Flesaker, B. Hughston, L. P. (1997a)

Exotic Interest Rate Options, in Exotic Options:

the State of the Art, eds. Clewlow, L. Strickland, C.

(International Thompson Press, London).

39

40Flesaker, B. Hughston, L. P. (1997b)

Dynamic Models of Yield Curve Evolution, in Mathematics of Derivative Securities, eds. Dempster, M. A. H.

Pliska, S. R. (Cambridge University Press, Cambridge).

41

42Flesaker, B. Hughston, L. P. (1997c) Net

Exposure 3, 55.

43

44Harrison, J. M. Kreps, D. M. (1979) J. Econom.

Theory 20, 381.

45

46Harrison, J. M. Pliska, S. R. (1981) Stochast.

Proc. Appl. 11, 215.

47

48Heath, D., Jarrow, R. Morton, A. (1992)

Econometrica 60, 77.

49

50Ho, T. S. Y. Lee, S.B. (1986) J. Finance 41,

1011.

51

52Hughston, L. P. (1996a) Proc. Roy. Soc. London

452, 953.

53

54Hughston, L. P. (1996) Introduction, in

Vasicek and Beyond: Approaches to Building and Applying

Interest Rate Models, ed. Hughston, L. P. (Risk Publications,

London).

55

56Hunt, P. J. Kennedy, J. E. (2000) Financial

Derivatives in Theory and Practice (Wiley, Chichester)

57

58Ikeda, N. Watanabe, S. (1989) Stochastic

Differential Equations and Diffusion Process (North-Holland,

Amsterdam).

59

60Jamshidian, F. (1997) Finance and Stochastics 1,

293.

61

62Kass, R. E. (1989) Statist. Sci. 4, 188.

63

64Kennedy, D. (1994) Math. Finance 4, 247.

65

66Mahalanobis, P. C. (1936) Proc. Nat. Inst. Sci. India

A 2, 49.

67

68Merton, R. C. (1973) Bell. J. Econ. Manag. Sci. 4,

141.

69

70Murray, M. K. Rice, J. W. (1993) Differential

Geometry and Statistics (Chapman Hall, London).

71

72Musiela, M. Rutkowski, M. (1997) Martingale

Methods in Financial Modelling (Springer-Verlag, Berlin).

73

74Nielsen, L. T. (1999) Pricing and Hedging of

Derivative Securities (Oxford University Press, Oxford).

75

76Rao, C. R. (1945) Bull. Calcutta Math. Soc.

37, 81.

77

78Rogers, L. C. G. (1994) Which model of the term

structure of interest rate should one use?, in Mathematical Finance, IMA 65, 63. (Springer-Verlag,

Berlin).

79

80Rogers, L. C. G. (1997) Math. Finance 7, 157.

81

82Santa-Clara, P. Sornette, D. (1997) The dynamics

of the forward interest rate curve with stochastic string

shocks (Preprint, University of California at Los Angeles).