THE NUMERICAL GENERALIZED LEAST-SQUARES ESTIMATOR OF AN UNKNOWN CONSTANT MEAN OF RANDOM FIELD

Abstract.

We constraint on computer the best linear unbiased generalized statistics of random field for the best linear unbiased generalized statistics of an unknown constant mean of random field and derive the numerical generalized least-squares estimator of an unknown constant mean of random field. We derive the third constraint of spatial statistics and show that the classic generalized least-squares estimator of an unknown constant mean of the field is only an asymptotic disjunction of the numerical one.

1. The best linear unbiased generalized statistics

Remark. To simplify notation we use Einstein summation convention then

where

are given vectors and

where

is given matrix.

Let us consider the random field with an unknown constant mean and variance its estimation statistics and the variance of the difference , where , as covariance

and the linear estimation statistics (weighted variable) at then

| (1) | |||||

where is given

vector of correlations and

is given (symmetric) matrix of correlations (see Appendix A).

The unbiasedness constraint

(the first constraint on the estimation statistics)

equal to

| (2) |

gives the first equation

The minimization constraint (the second constraint on the estimation statistics – the statistics is the best)

| (3) |

where (1)

produces equations in unknowns the kriging weights and a Lagrange parameter

this system of equations if multiplied by

and substituted into

since variance of the (estimation) statistics is minimized

| (4) | |||||

gives

| (5) |

the constraints (2) and (3) produce equations in unknowns

| (6) |

2. The classic best linear unbiased generalized statistics of an unknown constant mean of the field

Remark. When we consider an independent set of the random variables with an unknown constant mean and variance the best linear unbiased ordinary (estimation) statistics of the field has the asymptotic property

| (7) |

whilst for spatial dependence between random variables (the best linear unbiased generalized statistics) we get (see Appendix B)

| (8) |

Due to different asymptotic limits between (7) and (8) the ordinary least-squares estimator of an unknown constant mean of the field, the best linear unbiased estimator of an unknown constant mean of the field, can not be so easy generalized (like it was in past).

Let us constraint the best linear unbiased generalized (estimation) statistics of the random field , when for finite and the vector of correlations simplifies to

| (9) |

then from (2)

| (10) |

it holds (5)

| (11) |

for the co-ordinate independent statistics of an unknown constant mean of the field with the constraint on (11)

| (12) |

given by constrained from (11)

| (13) |

and from (9) the system of equations (6)

equivalent to

and

where

with the solution

| (14) |

and

| (15) |

of the classic best linear unbiased generalized statistics for finite and of an unknown constant mean of the field

| (16) |

where

with constrained minimized variance of the best linear unbiased generalized (estimation) statistics (4) as its variance (from(10) and (13))

then (from(14))

with the classic generalized least-squares estimator for finite and of an unknown constant mean of the field

| (17) |

based on observation seen as outcome of .

3. The numerical best linear unbiased generalized statistics of an unknown constant mean of the field

To remove the asymptotic limit of the classic best linear unbiased generalized statistics for finite and of an unknown constant mean of the field with the constraint (12)

the best linear unbiased generalized (estimation) statistic of the field at finite

given by the kriging algorithm (6) for

the negative correlation function with the parameter

| (18) |

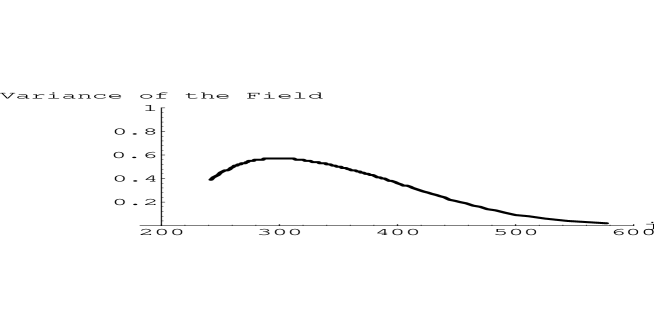

was constrained (from (5)) on computer (139 times) for the numerical best linear unbiased generalized statistics for finite at finite of an unknown constant mean of the field with the third constraint of spatial statistics

| (19) |

equivalent to

| (20) |

with constrained minimized variance of the best linear unbiased generalized (estimation) statistics (4) as its variance (see Fig. 1).

Our aim was to derive for the negative correlation function (18) with the parameter the numerical generalized least-squares estimator of an unknown constant mean of the field in fact the proper best linear unbiased (generalized) estimator of an unknown constant mean of the field

given at finite by numerical approximation to root of the equation (20). This (co-ordinate dependent) generalized least-squares estimator was compared to the (co-ordinate independent) classic generalized least-squares estimator of an unknown constant mean of the field (17)

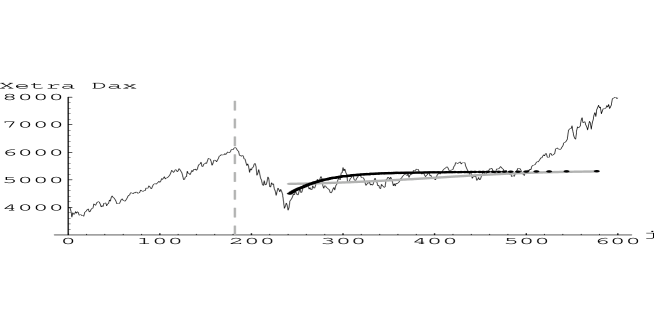

based on the same observation an initial amplification of long-lived asymmetric index profile recorded by close quotes of Xetra Dax Index shown in Fig. 2 then

with the same correlation function (18).

Since the classic best linear unbiased generalized statistics for finite and of an unknown constant mean of the field with the constraint

is an asymptotic disjunction for of the numerical best linear unbiased generalized statistics for finite at finite of an unknown constant mean of the field with the constraint

then the correct classic generalized least-squares estimator of an unknown constant mean of the field is an asymptotic disjunction for of the numerical generalized least-squares estimator of an unknowm constant mean of the field (see Fig. 2).

4. Summary

It was shown that the (estimation) statistics of the field with an unknown constant mean and variance

that assumes – the unbiasedness constraint (2)

that assumes – the minimization constraint (3)

given by the kriging system of equations (6)

is the best linear unbiased generalized (estimation) statistics of random field with minimized variance of the statistics

| (21) |

and (minimized)

| (22) |

with the asymptotic property (Appendix B)

and

constrained once again from (22) on computer – the third constraint of spatial statistics

is the numerical best linear unbiased generalized statistics for finite at finite of an unknown constant mean of the field with the numerical generalized least-squares estimator of an unknown constant mean of the field and its asymptotic disjunction for the classic generalized least-squares estimator of an unknown constant mean of the field.

References

- [1] E. H. Isaaks and R. M. Srivastava, An Introduction to Applied Geostatistics, New York: Oxford Univ. Press (1989).

Appendix A The sign of the terms

Appendix B The asymptotic property of the best linear unbiased generalized statistics of random field

From the minimization constraint (3)

we get

where

substituted into (2)

gives

for (9)

then the Lagrange parameter simplifies to

from the unbiasedness condition (2) it also holds

then the minimized variance of the estimation statistics (4)

simplifies to

and (5)

simplifies to

since

and

we get the asymptotic property of the best linear unbiased generalized statistics of random field

and