Abstract

The short-time asymptotic behavior of option prices for a variety of models with jumps has received much attention in recent years. In the present work, a novel second-order approximation for ATM option prices under the CGMY Lévy model is derived and, then, extended to a model with an additional independent Brownian component. Our method of proof is based on an integral representation of the option price involving the tail probability of the log-return process under the share measure and a suitable change of probability measure under which the process becomes stable. This approach is sufficiently efficient to produce the third-order asymptotic behavior of the option prices and, moreover, is expected to apply to many other popular classes of Lévy processes which satisfy the fundamental property of being stable under a suitable change of probability measure. Our results shed new light on the connection between both the volatility of the continuous component and the jump parameters and the behavior of ATM option prices near expiration. In the case of an additional Brownian component, the second-order term, in time-, is of the form , with the coefficient depending only on the overall jump intensity parameter and the tail-heaviness parameter . This extends the known result that the leading term is , where is the volatility of the continuous component. In contrast, under a pure-jump CGMY model, the dependence on the two parameters and is already reflected in the leading term, which is of the form . Information on the relative frequency of negative and positive jumps appears only in the second-order term, which is shown to be of the form and whose order of decay turns out to be independent of . The third-order asymptotic behavior of the option prices as well as the asymptotic behavior of the corresponding Black-Scholes implied volatilities are also addressed. Our numerical results show that first-order term typically exhibits extremely poor performance and that the second-order term significantly improves the approximation’s accuracy.

AMS 2000 subject classifications: 60G51, 60F99, 91G20, 91G60.

Keywords and phrases: Exponential Lévy models; CGMY and tempered stable models; short-time asymptotics; option pricing; implied volatility.

1 Introduction

It is generally recognized that the standard option pricing model of Black-Scholes is inconsistent with options data, while remaining a widely used model in practice because of its simplicity. Exponential Lévy models generalize the classical Black-Scholes setup by allowing jumps in stock prices while preserving the independence and stationarity of returns. There are several reasons for introducing jumps in financial modeling. First of all, asset prices do jump, and some risks simply cannot be handled within continuous-paths models. Second, historical asset prices exhibit distributions with so-called stylized features, such as heavy tails, high kurtosis, volatility clustering and leverage effects, which are hard to replicate within purely-continuous frameworks. Finally, market prices of vanilla options exhibit skewed implied volatilities (relative to changes in the strikes), in contrast to the classical Black-Scholes model which predicts a flat implied volatility smile. Moreover, the fact that the implied volatiliy smile and skewness phenomenon becomes much more pronounced for short maturities is a clear indication of the presence of jumps.

One of the first applications of jump processes in financial modeling is due to Mandelbrot [26], who suggested a pure-jump stable Lévy process to model power-like tails and self-similar behavior in cotton price returns.

Merton [28] and Press [31] subsequently considered option pricing and hedging problems under an exponential compound Poisson process with Gaussian jumps and an additive independent non-zero Brownian component. A similar exponential compound Poisson jump-diffusion model was more recently studied in Kou [22], where the jump sizes are distributed according to an asymmetric Laplace law. For infinite activity exponential Lévy models, Barndorff-Nielsen [1] introduced the normal inverse Gaussian (NIG) model, while the extension to the generalized hyperbolic class was studied by Eberlein, Keller and Prause [10]. Madan and Seneta [25] introduced the symmetric variance gamma (VG) model while its asymmetric extension was later studied by Madan and Milne [24] and Madan, Carr and Chang [23]. Both models are built on Brownian subordination; the main difference being that the log-return process in the NIG model is an infinite variation process with stable like () behavior of small jumps, while in the VG model, the log-price is of finite variation with infinite but relatively low activity of small jumps. The class of “tempered stable” processes was first introduced by Koponen [21] and further developed by Carr, Geman, Madan and Yor [5], who introduced the terminology CGMY. The CGMY model is a particular case of the more general KoBoL class of [4] and was also previously proposed for financial modeling in [7] and [27]. Nowadays, the CGMY model is considered to be a prototype of the general class of models with jumps and enjoys widespread applicability.

Stemming in part from its importance for model calibration and testing, small-time asymptotics of option prices have received a lot of attention in recent years (see, e.g., [2], [3], [11], [12], [13], [16], [17], [18], [19], [20], [30], [32], [38]). We shall review here only the studies most closely related to ours, focusing in particular on the at-the-money (ATM) case. Carr and Wu [9] first analyzed, partially via heuristic arguments, the first order asymptotic behavior of an Itô semimartingale with jumps. Concretely, ATM option prices of pure-jump models of bounded variation decrease at the rate , while they are just under the presence of a Brownian component. By considering a stable pure-jump component, [9] also showed that, in general, the rate could be , for some . Muhle-Karbe and Nutz [29] formally showed that, under the presence of a continuous-time component, the leading term of ATM option prices is of order , for a relatively general class of Itô models, while for a more general type of Itô processes with -stable-like small jumps, the leading term is (see also [13, Proposition 4.2], [15, Theorem 3.7], and [38, Proposition 5] for related results in exponential Lévy models). However, none of the these papers obtained second or higher order asymptotics for the ATM option prices, which are arguably more relevant for calibration purposes, given that the most liquid options are of this type.

In the present paper, we study the small-time behavior for at-the-money (ATM) call (or equivalently, put) option prices

|

|

|

(1.1) |

under the exponential Lévy model

|

|

|

(1.2) |

where is the superposition of a CGMY Lévy process and of an independent Brownian motion ; i.e.,

|

|

|

(1.3) |

where is a standard Brownian motion independent of .

Here, as usual, is the positive part of . The first order asymptotic behavior of (1.1) in short-time under the model (1.3) takes the form:

|

|

|

(1.4) |

where is a symmetric stable random variable with under . When , () and, thus, (see [38] and [32]).

When and , the characteristic function of is explicitly given (see [13] and [38]) by

|

|

|

In that case, (see (25.6) in [37]),

|

|

|

(1.5) |

Interestingly enough, under the presence of a continuous component, the first-order asymptotic term only reflects information on the continuous-time volatility, in sharp contrast with the pure-jump case where the leading term depends on the overall jumps-intensity parameter and the index , which in turn controls the tail-heaviness of the distributions.

Below, we also obtain a second order correction term for the approximation (1.4).

The derivation of the second-order results builds on two facts. First, as in [13], we make use of the following representation of Carr and Madan [6]:

|

|

|

(1.6) |

where is the martingale probability measure obtained when one takes the stock as the numéraire (i.e., ) and is an independent mean-one exponential random variable under . The measure is sometimes called the share measure (see [6]). Notice that under , also admits a decomposition similar to (1.3),

|

|

|

(1.7) |

where is a Wiener process and is also a CGMY process, independent of . Second, we change probability measures from to a probability measure , under which is a stable Lévy process and is still a standard Brownian motion independent of . We show that the second-order asymptotic behavior of the ATM call option price (1.1) in short-time is then of the form

|

|

|

in the pure-jump CGMY case (), while in the case of a non-zero independent Brownian component (),

|

|

|

for different constants and that we will determine explicitly. To wit, we found that, under the presence of a nonzero Gaussian component, the second-order term depends only on the overall jump intensity parameter and the tail-heaviness parameter . The parameters and (which control the relative frequency of negative and positive jumps) do not appear until the next order term. However, for a pure-jump case, the parameters and are already present in the second-order term. The above asymptotic behaviors should also be compared to the corresponding behavior under the standard Black-Scholes model, where it is known that (see, e.g., [18, Corollary 3.4])

|

|

|

Our method of proof is sharp enough to produce the third-order asymptotic behavior of the option prices (see Remark 3.4 and 4.4 below) and, moreover, is expected to apply to other popular classes of Lévy processes, which satisfy the fundamental property of being stable under a suitable change of probability measure such as tempered stable processes in the sense of Rosiński [35] (this will be presented elsewhere). Finally, the asymptotic behavior of the corresponding Black-Scholes implied volatilities are also addressed.

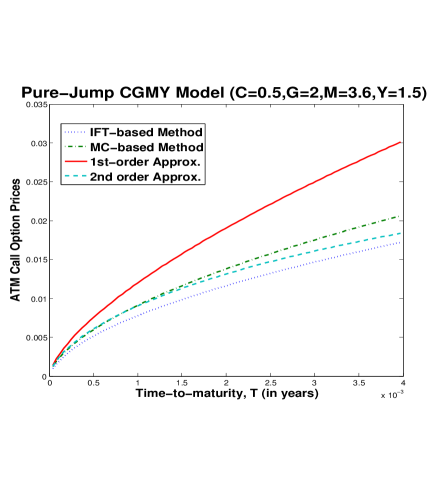

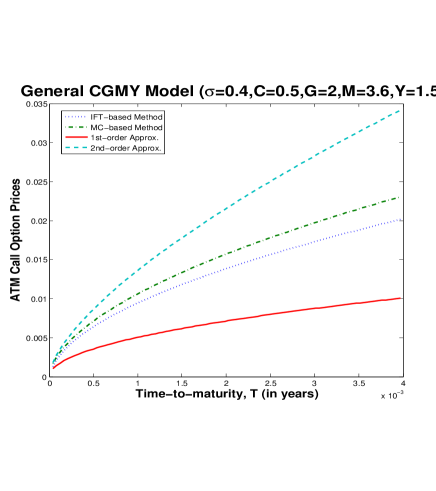

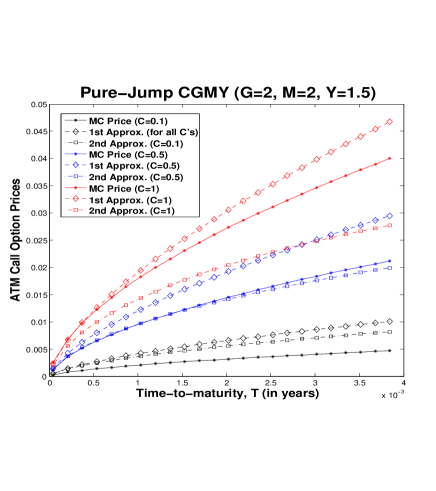

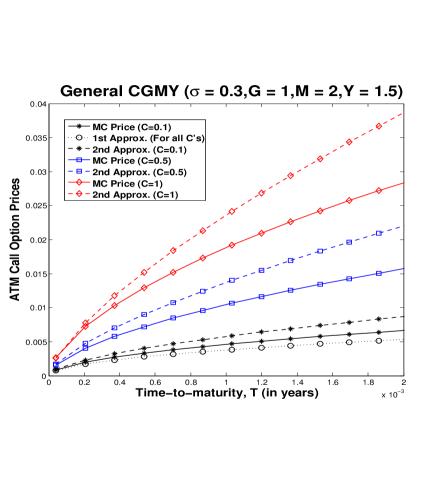

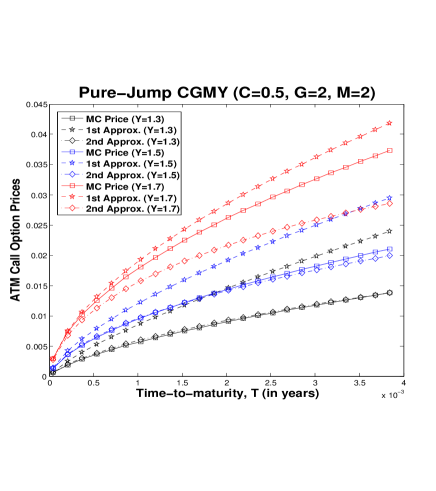

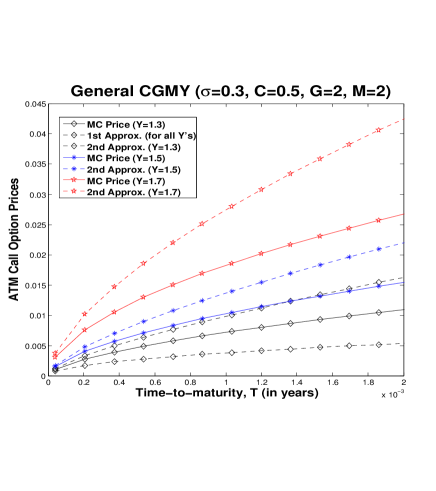

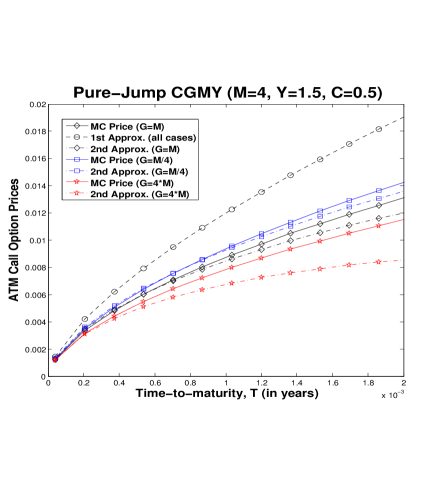

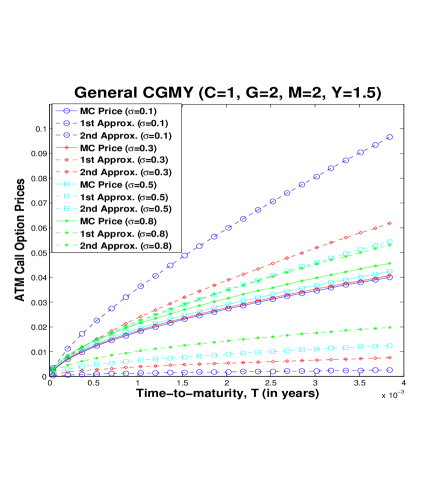

The present paper is organized as follows. Section 2 contains preliminary results on the CGMY model, some probability measure transformations, and asymptotic results for stable Lévy processes which will be needed throughout the paper. Section 3 establishes the second-order asymptotics of the call option price under the pure-jump CGMY model (). Section 4 establishes the second-order asymptotics of the call-option price under the CGMY model with an additional independent non-zero Brownian component (). In Section 5, we assess the performance of our asymptotic expansions through a detailed numerical analysis. The proofs of our main results are deferred to the Appendices.

Appendix B Proofs of Section 4: CGMY model with Brownian component

Proof of Proposition 4.1.

From (1.6), note that

|

|

|

|

Now for any and ,

|

|

|

|

|

|

|

|

(B.1) |

Clearly the first term in (B.1) is integrable on . To estimate the second term, applying the change of probability measure (2.13) and using the self-similarity property (2.12) of , we obtain

|

|

|

Pick and such that , then by Hölder’s inequality and (2.26),

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

since as given in (2.16), . If , then by (2.23), for any and ,

|

|

|

and thus,

|

|

|

which is integrable on . On the other hand, if ,

|

|

|

|

|

|

|

|

and thus

|

|

|

which is also integrable on . Therefore, by the dominated convergence theorem,

|

|

|

The proof is now complete. ∎

For simplicity, we fix .

Recalling that under and using (1.6), the self-similarity of , and the change of variable , it follows that

|

|

|

|

Next, by changing the probability measure to and using that , , and the change of variable in the first integral above, we get

|

|

|

|

|

|

|

|

(B.2) |

|

|

|

|

|

|

|

|

The last term above is clearly as , while the second term above can be shown to be asymptotically equivalent to by arguments analogous to those of (A.20).

Thus, we only need to analyze the term in (B.2) that we denote and that can be written as follows in light of the self-similarity property of and :

|

|

|

|

(B.3) |

where we had denoted . To analyze the asymptotic behavior of , we decompose it into the following three terms:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(B.4) |

We analyze each of three terms above in the following three steps:

Step 1.

We first analyze the behavior of . Since and are independent,

|

|

|

|

|

|

|

|

|

|

|

|

(B.5) |

Using that the distribution of is symmetric under (hence, ), is then decomposed as:

|

|

|

|

|

|

|

|

(B.6) |

Let us first consider . By (2.24), it follows that, for any and ,

|

|

|

(B.7) |

for some (see Appendix C for the verification of this claim).

Moreover, for any fixed ,

|

|

|

Using (2.25),

|

|

|

for small enough and all . Therefore, by the dominated convergence theorem and, in light of (2.25), we get:

|

|

|

|

|

|

|

|

|

|

|

|

(B.8) |

For , note that

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Next, change variable back to :

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(B.9) |

For and , set

|

|

|

By (A.12), there exists such that for any and ,

|

|

|

(B.10) |

Hence,

|

|

|

|

|

|

|

|

|

|

|

|

(B.11) |

as , since . Similarly, using and Lemma 2.1, for any and , we have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(B.12) |

Therefore,

|

|

|

(B.13) |

For , since and are identically distributed, we proceed in the proof as follows:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(B.14) |

which is again independent of and integrable on when multiplied by . Moreover,

|

|

|

|

|

|

|

|

|

|

|

|

Hence, by the dominated convergence theorem,

|

|

|

|

|

|

|

|

(B.15) |

as since , for . Similarly, since , it follows from (B.14) that

|

|

|

Therefore,

|

|

|

(B.16) |

Combining (B.8), (B.11), (B.13), (B.15) and (B.16), we obtain

|

|

|

(B.17) |

Step 2.

Next, we analyze the asymptotic behavior of . Using the independence of and ,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(B.18) |

By (2.23) and the symmetry of ,

|

|

|

which, when multiplied by , becomes integrable on . Hence, by (2.24) and the dominated convergence theorem,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(B.19) |

To find the asymptotic behavior of the first integral in (B.18), we decompose it as:

|

|

|

|

|

|

|

|

|

|

|

|

(B.20) |

For , note that for any and ,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

which is independent of . Since , for , by the dominated convergence theorem,

|

|

|

|

|

|

|

|

(B.21) |

We further decompose the second term in (B.20) as:

|

|

|

|

|

|

|

|

|

|

|

|

(B.22) |

Since , for , it is easy to see that

|

|

|

(B.23) |

Moreover,

|

|

|

|

|

|

|

|

|

|

|

|

Hence by (B.12) and the dominated convergence theorem,

|

|

|

|

(B.24) |

as . Combining (B.19), (B.21), (B.23) and (B.24), we obtain

|

|

|

(B.25) |

Step 3.

We finally analyze the behavior of . Note that

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(B.26) |

We first investigate the asymptotic of by decomposing it as:

|

|

|

|

|

|

|

|

(B.27) |

By (2.23), it is easy to see that , for any and .

Hence, by (2.24) and the dominated convergence theorem,

|

|

|

(B.28) |

Also, can be further decomposed as:

|

|

|

For any , and , let .

It is easily seen that

|

|

|

|

|

|

|

|

|

|

|

|

(B.29) |

Moreover,

|

|

|

(B.30) |

Hence, for any and , and since , for ,

|

|

|

|

|

|

|

|

(B.31) |

Since both control functions in (B.29) and (B.30) are independent of , combining (B.28) and (B.31), and by the dominated convergence theorem,

|

|

|

(B.32) |

Next, we decompose the quantity defined in (B.26) as:

|

|

|

|

|

|

|

|

|

|

|

|

(B.33) |

Note that is the same as in (B.6), and thus the corresponding integral has an asymptotic behavior similar to (B.8):

|

|

|

(B.34) |

Next, we further decompose as:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Note that for ,

|

|

|

while for ,

|

|

|

Using the estimates (B.10) and (B.14), a proof as in getting (B.11) and (B.15) gives

|

|

|

(B.35) |

Combining (B.32), (B.34) and (B.35), we have

|

|

|

(B.36) |

Finally, from (B.4), (B.17), (B.25) and (B.36), and since , for , we obtain (4.3), therefore finishing the proof. ∎

Proof of Proposition 4.5.

When the diffusion component exists, [38, Proposition 5] implies that as . In particular, as and, thus, (A.22) above still holds. Let , then as , and (A.22) can be written as

|

|

|

(B.37) |

By comparing (4.4)-(4.5) and (B.37), we have

|

|

|

and, therefore,

|

|

|

The proof is now complete. ∎