UMR n 7351 CNRS UNSA

Université de Nice - Sophia Antipolis

06108 Nice Cedex 02 France

Tel.: +33-04-92-07-62-56

salima@unice.fr

Parametric estimation of hidden stochastic model by contrast minimization and deconvolution: application to the Stochastic Volatility Model

Abstract

We study a new parametric approach for particular hidden stochastic models such as the Stochastic Volatility model. This method is based on contrast minimization and deconvolution.

After proving consistency and asymptotic normality of the estimation leading to asymptotic confidence intervals, we provide a thorough numerical study, which compares most of the classical methods that are used in practice (Quasi Maximum Likelihood estimator, Simulated Expectation Maximization Likelihood estimator and Bayesian estimators). We prove that our estimator clearly outperforms the Maximum Likelihood Estimator in term of computing time, but also most of the other methods. We also show that this contrast method is the most robust with respect to non Gaussianity of the error and also does not need any tuning parameter.

Keywords: Contrast function, Deconvolution, Parametric inference, Stochastic volatility.

1 Introduction

This paper is concerned with the particular hidden stochastic model:

| (1) |

where and are two independent sequences of independent and identically distributed (i.i.d) centered random variables with variance and . It is assumed that the variance is known. The terminology hidden comes from the unobservable character of the process since the only available observations are .

The dynamics of the process is described by a measurable function which depends on an unknown parameter and by a sequence of i.i.d centered random variables with unknown variance . We denote by the vector of parameters governing the process and suppose that the model is correctly specified: that is, belongs to the parameter space , with .

Inference in hidden Markov models is a real challenge and has been studied by many authors (see [CMR05a], [DdFG01], [RRT00]). K.C. Chanda provided in [Cha95] an asymptotically normal estimator for the vector of parameters by using modified Yule Walker equation but it assumes that the function is linear in and , so the model (1) is reduced to an autoregressive model with measurement error.

Recently, in [DMOvH11], the authors propose an efficient estimator of the vector of parameters for nonlinear function . They prove that their Maximisation Likelihood Estimator (MLE) is consistent and asymptotically normal. The main difficulty with their approach comes from the unobservable character of the process making the calculus of the exact likelihood intractable in practice: the likelihood is only available in the form of a multiple integral, so exact likelihood methods require simulations and have therefore an intensive computational cost. In many case, the MLE has to be approximated. A popular approach to approximate the MLE consists in using Monte Carlo Markov Chain (MCMC) simulation techniques. Thanks to the development of these methods, the MLE has known a huge progress and Bayesian estimations have received more attention (see [SR93]). Another method for performing the MLE consists in using the Expectation-Maximization (EM) algorithm proposed by Dempster et al. in 1977 (see [DLR77]). Nevertheless, since is unobservable, this method requires to introduce a MCMC in the Expectation step. Although these methods are used in practice, they are expensive from a computational point of view.

Some authors have proposed Sequential Monte Carlo algorithms (SMC) known as Particles Filtering methods which allow to approximate the likelikood. The computational cost is reduced by a recursive construction. We refer to the book of [DdFG01] and [CMR05a] for a complete review of these methods.

Particle Markov Chain Monte Carlo (PMCMC) is another method for estimating the model (1). This method combines Particles filtering methods and MCMC methods to estimate the vector of parameters . From a computational point of view, this approach is expensive and we refer the reader to [ADH10] for more details. In [PHH10], they propose an adaptive PMCMC method to estimate ecological hidden stochastic models.

We propose here an approach based on M-estimation: It consists in the optimisation of a well-chosen contrast function (see [VdV98] chapter p.41 for a partial review) and deconvolution strategy. The deconvolution problem is encountered in many statistical situations where the observations are collected with random errors. In this approach, a method for estimating the parameter has been proposed by F. Comte and M. Taupin (see [CT01]). Their procedure of estimation is based on a modified least squared minimization. In the same perspective, J. Dedecker, A. Samson and M-L. Taupin in [DST11] propose also the same procedure of estimation based on a weighted least squared estimation: Their assumptions on the process are less restrictive than those proposed by F. Comte and M. Taupin and they provide consistent estimation of the parameter with a parametric rate of convergence in a very general framework. Their general estimator is based on the introduction of a kernel deconvolution density and depends on the choice of a weight function.

The approach proposed here is different: it is not based on a weighted least squared estimation so that the choice of the weight function is not encountered in this paper. Moreover, it allows to estimate both the parameters and . Our principle of estimation relies on the Nadaraya-Watson strategy and is proposed by F. Comte et al. in [CL11] in a non parametric case to estimate the function as a ratio of an estimate of and an estimate of , where represents the invariant density of the . We propose to adapt their approach in a parametric context and suppose that the form of the stationary density is known up to some unknown parameter . Our work is purely parametric but we go further in this direction by proposing an analytical expression of the asymptotic variance matrix which allows to construct confidence interval. Furthermore, this approach is much less greedy from a computational point of view than the MLE and its implementation is straighforward.

Applications: Applications include epidemiology, meterology, neuroscience, ecology (see [IBAK11]) and finance (see [JPS09]). For example, our approach can be applied to the five ecological state space models described in [PHH10]. Although the scope of our method is general, we have chosen to focus on the so-called discrete time Stochastic Volatility model (SV) introduced by Taylor in 1982 (see [Tay05]). We also investigate the behavior of our method on the simpler autoregressive process AR(1) with measurement noise which has been widely studied and on which our method can be more easily understood and compared with other ones. Our procedure allows to estimate the parameters of a large class of discrete Stochastic Volatility models (ARCH-E model, Vasicek model, Merton model..), which is a real challenge in financial application.

(i) Gaussian Autoregressive AR(1) with measurement noise: It has the following form:

| (2) |

where and are two centered Gaussian random variables with variance assumed to be known and assumed to be unknown. Additionally, we assume that which implies the stationary and ergodic property of the process (see [DDL+07]).

(ii) SV model: It is directly connected to the type of diffusion process used in asset-pricing theory ( see [MT90]):

| (3) |

where and are two centered Gaussian random variables with variance assumed to be known and equal to one and assumed to be unknown. The variables represent the returns and is the log-volatility process.

By applying a log-transformation and , the SV model is a particular version of (1). We assume that and we refer the reader to [GCJL00] for the mixing properties of stochastic volatility models.

Most of the computational problems stem from the assumptions that the innovation of the returns are Gaussian which translates into a logarithmic chi-square distribution when the model (12) is transformed in a linear state space model. Many authors have ignored it in their implementation and many authors use some mixture of Gaussian to approximate the log-chi-square density. For example, in the Quasi-Maximum Likelihood (QML) method implemented by Jacquier, Polson and Rossi in [JPR02] and in the Simulated Expectation-Maximization Likelihood estimator proposed (SIEMLE) by Kim, Shephard, and Chib in [KS94] they used a mixture of Gaussian distribution to approximate the log-chi-square distribution. Harvey [HRS94] used the Kalman filter to estimate the likelihood of the transform state space model, hence the model was also assumed to be Gaussian.

Organization of the paper: The first purpose of the paper is to present our estimator and its statistical properties in Section 1.1: Under weak assumptions, we show that it is a consistent and asymptotically normal estimator.

The second purpose of this paper consists in comparing our contrast estimator with different estimations: the QML, the SIEMLE and Bayesian estimators. Section 2 contains the numerical study: In Section 2.4 we give the parameter estimates and the comparison with others ones for simulation data and Section 2.6 contains the study on real data. We compare our contrast estimator with other ones on the SP500 and FTSE index. From a computational point of view, we show that the implementation of our estimator is straightforward and it is faster than the SIEMLE (see Table [2] in Section 2.5.1). Besides, we show that our estimator outperforms the QML and Bayesian estimators.

Notations: We denote by: the Fourier transform of the function and with . We write the norm of on the space of functions . By property of the Fourier transform, we have and . The vector of the partial derivatives of with respect to (w.r.t) is denoted by and the Hessian matrix of w.r.t is denoted by . The Euclidean norm matrix, that is, the square root of the sum of the squares of all its elements will be written by . We denote by the pair and is a given realisation of .

In the following, and denote respectively the probability , the expected value , the variance and the covariance when the true parameter is . Additionally, we write (resp. ) the empirical expectation (resp. theoretical), that is: for any stochastic variable : (resp. ).

1.1 Procedure: Contrast estimator

Hereafter, we propose explicit estimators of the parameter . This estimator called the contrast estimator is based on minimization of suitable functions of the observations usually called “contrasts functions”. We refer the reader to [VdV98] for a general account on this notion. Furthermore, in this part, we use the contrast function proposed by [CLR10], that is:

| (4) |

with the number of observations and:

where the function and are given by:

| (5) |

with the invariant density of .

Some assumptions. As our procedure relies on the Fourier deconvolution strategy, in order to construct our estimator, we assume that the density of the noise , denoted by , is fully known and belongs to , and for all . Furthermore, we assume that the function belongs to . The function must be integrable.

For the statistical study, the key assumption is that the process is stationary and ergodic (see [GCJL00] for a definition).

Remark 1.

In this paper we consider the situation in which the observation noise variance is known. This assumption which is not in general the case in practice is necessary for the identifiability of the model and so is a standard assumption for state-space models given in (1).

There is some restrictions on the distribution of the observation and process errors in the Nadaraya-Watson approach. It is known that the rate of convergence for estimating the function is related to the rate of decrease of . In particular, the smoother , the slower the rate of convergence for estimating is (The Gaussian, log-chi squared or Cauchy distributions are super-smooth. The Laplace distribution is ordinary smooth). This rate of convergence can be improved by assuming some additional regularity conditions on . There is a good discussion about this subject in [CLR10] and [DST11].

The procedure Let us explain the choice of the contrast function and how the strategy of deconvolution works. Obviously, as the model (1) shows, the are not i.i.d. However, by assumption, they are stationary ergodic, so the convergence of to as tends to the infinity is provided by the Ergodic Theorem. Moreover, the limit of the contrast function can be explicitly computed:

By Eq.(1) and under the independence assumptions of the noise and , we have:

Using Fubini’s Theorem and Eq.(1), we obtain:

| (6) | |||||

Then,

| (7) | |||||

| (8) |

Under the uniqueness assumption (CT) given just later this quantity is minimal when =. Hence, the associated minimum-contrast estimators is defined as any solution of:

| (9) |

Remark 2.

One can see in the deconvolution strategy described in Eq.(6) that temporal correlation in the observation or latent process errors can be authorized. The procedure still be applicable but the covariance matrix for the CLT has not an analytic expression in this case since the use of the Fourier deconvolution approach does not work.

We refer the reader to [DDL+07] for the proof that if is an ergodic process then the process , which is the sum of an ergodic process with an i.i.d. noise, is again stationary ergodic. Furthermore, by the definition of an ergodic process, if is an ergodic process then the couple inherits the property (see [GCJL00]).

1.2 Asymptotic properties of the Contrast estimator

Our proof holds under the following assumptions. For the reader convenience, we denote by (E) (resp. (C) and (T)) the assumptions which serve us for the existence (resp. Consistency and Central Limit Theorem). If the same assumption is needed for two results, for example for the existence and the consistency, it is denoted by (EC).

(ECT): The parameter space is a compact subset of and is an element of the interior of .

(C): (Local dominance): .

(CT): The application admits an unique minimum and its Hessian matrix denoted by is non-singular in .

(T): (Regularity): We assume that the function is twice continuously differentiable w.r.t for any and measurable w.r.t for all in . Additionally, each coordinate of and each coordinate of belong to and each coordinate of and have to be integrable as well.

(Moment condition): For some and for :

(Hessian Local dominance): For some neighbourhood of and for :

Let us introduce the matrix:

where and

Theorem 1.1.

Under our assumptions, let be the minimum-contrast estimator defined by (9). Then:

The following corollary gives an expression of the matrix and of Theorem 1.1 for the practical implementation:

Corollary 1.

Under our assumptions, the matrix is given by:

where:

and, the covariance terms are given by:

where and the differential is taken at point .

Furthermore, the Hessian matrix is given by:

Let us now state the strategy of the proof, the full proof is given in Appendix B. Clearly, the proof of Theorem 1.1 relies on M-estimators properties and on the deconvolution strategy. The existence of our estimator follows from regularity properties of the function and compactness argument of the parameter space, it is explained in Appendix B.1. The key of the proof consists in proving the asymptotic properties of our estimator. This is done by splitting the proof into two parts: we first give the consistency result in Appendix B.2 and then give the asymptotic normality in Appendix B.3. Let us introduce the principal arguments:

The main idea for proving the consistency of a M-estimator comes from the following observation: if converges to in probability, and if the true parameter solves the limit minimization problem, then, the limit of the argminimum is . By using an argument of uniform convergence in probability and by compactness of the parameter space, we show that the argminimum of the limit is the limit of the argminimum. A standard method to prove the uniform convergence is to use the Uniform Law of Large Numbers (see Lemma 1 in Appendix A). Combining these arguments with the dominance argument (C) give the consistency of our estimator, and then, the first part of Theorem 1.1.

The asymptotic normality follows essentially from Central Limit Theorem for a mixing process (see [Jon04]). Thanks to the consistency, the proof is based on a moment condition of the Jacobian vector of the function and on a local dominance condition of its Hessian matrix.

To refer to likelihood results, one can see these assumptions as a moment condition of the score function and a local dominance condition of the Hessian.

2 Applications

2.1 Contrast estimator for the Gaussian AR(1) model with measurement noise:

Consider the following autoregressive process AR(1) with measurement noise:

| (10) |

The noises and are supposed to be centered Gaussian randoms with variance respectively and . We assume that is known. Here, the unknown vector of parameters is and for stationary and ergodic properties of the process , we assume that the parameter satisfies (see [DDL+07]). The functions and are defined by:

where . The vector of parameter belongs to the compact subset given by with where , , and are positive real constants. We consider this subset since by stationary of , the parameter and by construction the function is well defined for with which is implied by . The contrast estimator defined in (1.1) has the following form:

| (11) |

2.2 Contrast estimator for the SV model:

We consider the following SV model:

| (12) |

The noises and are two centered Gaussian random variables with standard variance assumed to be known and . We assume that and we refer the reader to [GCJL00] for the mixing properties of this model.

By applying a log-transformation and , the log-transform SV model is given by:

| (13) |

The Fourier transform of the noise is given by:

where and = . Here, represents the gamma function given by:

The vector of parameters belongs to the compact subset given by with , and positive real constants.

Our contrast estimator (1.1) is given by:

| (14) |

with .

2.3 Comparison with the others methods

2.3.1 QML Estimator

For the SV model, the QML estimator, proposed independently by Harvey et al.(1994) (see [HRS94]) is based on the log-transform model given in (13). Making as if the were Gaussian in the log-transform of the SV model, the Kalman filter [Kal60] can be applied in order to obtain the quasi likelihood function of where is the sample data length. For the AR(1) and the log-transform of the SV model, the log-likelihood is given by:

where is the one-step ahead prediction error for , and is the corresponding mean square error. More precisely, the two quantities are given by:

where is the one-step ahead prediction for and is the one-step ahead error variance for .

Hence, the associated estimator of is defined as a solution of:

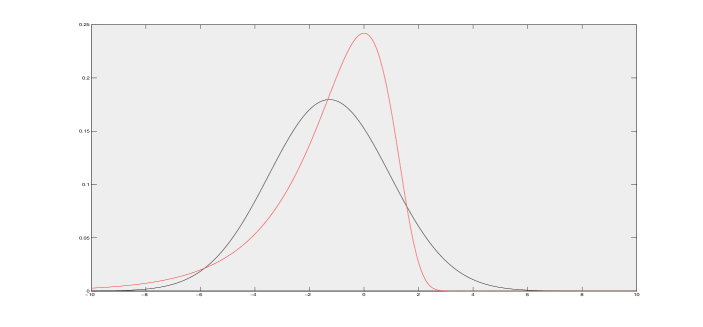

Note that this procedure can be inefficient: the method does not rely on the exact likelihood of the and approximating the true log-chi-square density by a normal density can be rather inappropriate (see Figure [1] below).

2.3.2 Particle filters estimators: Bootstrap, APF and KSAPF

For the particle filters, the vector of parameters is supposed random obeying the prior distribution assumed to be known. We propose to use the Kitagawa and al.’s approach (see [DdFG01] chapter 10 p.189) in which the parameters are supposed time-varying: where is a centered Gaussian random with a variance matrix supposed to be known. Now, we consider the augmented state vector where is the hidden state variable and the unknown vector of parameters. In this paragraph, we use the terminology of the particle filtering method, that is: we call particle a random variable. The sequential particle estimation of the vector consists in a combined estimation of and . For initialisation the distribution of 111 To avoid confusions between the true value and the initial value in the Bayesian algorithms, we start the algorithms with . conditionally to is given by the stationary density .

For the comparison with our contrast estimator (1.1), we use the three methods: the Bootstrap filter, the Auxiliary Particle filter (APF) and the Kernel Smoothing Auxiliary Particle filter (KSAPF). We refer the reader to [DdFG01], [PS99] and [LW01] for a complete revue of these methods.

Remark 3.

Let us underline some particularity of the combined state and parameters estimation: For the Bootstrap and APF estimator, an important issue concerns the choice of the parameter variance since the parameter is itself unobservable. If one can choose an optimal variance the APF estimator could be a very good estimator since with arbitrary variance the results are acceptable (see Table [4]). In practice, Q is chosen by an empirical optimization. The KSAPF is an enhanced version of the APF and depends on a smooth factor (see [LW01]). Therefore, the choice of is another problem in practice.

A common approach to estimate the vector of parameters is to maximize the likelihood. Nevertheless, for state space models, the main difficulty with the Maximum Likelihood Estimator (MLE) comes from the unobservable character of the state making the calculus of the likelihood untractable in practice: the likelihood is only available in the form of a multiple integral, so exact likelihood methods require simulations and have therefore an intensive computational cost. In many cases, the MLE has to be approximated. A popular approach to approximate it consists in using MCMC simulation techniques (see [SR93] and [CMR05b]). Another approach to approximate the likelihood consists in using particles filtering algorithms. Recently, in [RMC09] the authors propose an approach of Integrated Nested Laplace Approximations to obtain approximations of the likelihood.

In [CJP11] the authors propose a sequential algorithm which allows an efficient approximation of the complete distribution . Their approach is an extension of the Iterated Batch Importance Sampling (IBIS) proposed in [Cho02]. In [ADH10] the authors develop a general algorithm which is a MCMC algorithm that uses the particles filter to approximate the intractable density combined with a MCMC step that samples from . They show that their PMCMC algorithm admits as stationary density the distribution of interest . There exist others methods and we refer the reader to [JDD08], [PDS11] for more details.

2.4 A simulation study

For the AR(1) and SV model, we sample the trajectory of the with the parameters and . Conditionally to the trajectory, we sample the variables for where represents the number of observations. We take and for the two models. This means that we consider the following model:

with . In this case, the Fourier transform of is given by: with (see Appendix C.2).

For the three methods, we take a number of particles equal to . Note that for the Bayesian procedure (Bootstrap, APF and KSAPF), we need a prior on , and this only at the first step. The prior for is taken to be the Uniform law and conditionally to the distribution of is the stationary law:

We take for the KSAPF and for the APF and Bootstrap filter.

Remark 4.

Note that, in practice, there is no constraint on the parameters for the contrast function contrary to the particle filters where we take the stationary law for and the Uniform law around the true parameters. Hence, we bias favourably the particle filters.

2.5 Numerical Results

In the numerical section we compare the different estimations: the QML estimator defined in Section 2.3.1, the Bayesian estimators defined in Section 2.3.2 and our contrast estimator defined in Section 1.1. For the comparison of the computing time, we also compare our contrast estimator with the SIEMLE proposed by Kim, Shepard and Chib (see Appendix D.1 and [KS94] for more general details).

2.5.1 Computing time

From a theoretical point of view, the MLE is asymptotically efficient. However, in practice since the states are unobservable and the SV model is non Gaussian, the likelihood is untractable. We have to use numerical methods to approximate it. In this section, we illustrate the SIEMLE which consists in approximating the likelihood and applying the Expectation-Maximisation algorithm introduced by Dempster [DLR77] to find the parameter .

To illustrate the SIEMLE for the SV model, we run an estimator with a number of observations equal to . Although the estimation is good the computing time is very long compared with the others methods (see Tables [1] and [2]). This result illustrates the numerical complexity of the SIEMLE (see Appendix D.1). Therefore, in the following, we only compare our contrast estimator with the QML and Bayesian estimators. The results are illustrated by Figure [1]. We can see that our contrast estimator is the fastest for the Gaussian AR(1) model. The QML is the most rapid for the SV model since it assumes that the measurement errors are Gaussian but we show in Figures [2], [3] and [4] that it is a biased estimator with large mean square error. For our algorithm, for the Gaussian AR(1) model, the function has an explicit expression but for the SV model, the function is approximated numerically since the Fourier transform of the function has not an explicit form. This explains why our algorithm is slower on the SV model than on the Gaussian AR(1) model.222We use a quadrature method implemented in Matlab to approximate the Fourier transform of . One can also use the FFT method and we expect that the contrast estimator will be more rapid in this case. In spite of this approximation, our contrast estimator is fast and its implementation is straightforward.

| n | SV | AR(1) | ||||

|---|---|---|---|---|---|---|

| CPU | MSE | CPU | MSE | |||

| Contrast | 200 | 4.2695 | 0.0425 | 0.032146 | 0.0411 | |

| 300 | 5.1015 | 0.0453 | 0.022588 | 0.0398 | ||

| 400 | 7.0502 | 0.0239 | 0.028062 | 0.0374 | ||

| 500 | 6.9109 | 0.0175 | 0.026517 | 0.0306 | ||

| 750 | 11.8555 | 0.0117 | 0.031353 | 0.0218 | ||

| 1000 | 20.4074 | 0.0078 | 0.056931 | 0.0133 | ||

| 1500 | 29.3910 | 0.0061 | 0.08432 | 0.0091 | ||

| Bootstrap filter | 200 | 41.4780 | 0.0275 | 85.65 | 0.0225 | |

| 300 | 57.5201 | 0.0261 | 103.7212 | 0.0211 | ||

| 400 | 67.9421 | 0.0248 | 155.0456 | 0.0199 | ||

| 500 | 107.9450 | 0.0228 | 169.5578 | 0.0187 | ||

| 750 | 138.0307 | 0.0186 | 241.1891 | 0.0154 | ||

| 1000 | 192.2166 | 0.0174 | 318.5656 | 0.0133 | ||

| 1500 | 158.3680 | 0.0166 | 388.7098 | 0.0122 | ||

| APF | 200 | 19.4471 | 0.0209 | 49.6784 | 0.0138 | |

| 300 | 39.2457 | 0.0182 | 69.3421 | 0.0125 | ||

| 400 | 46.9590 | 0.0123 | 86.9111 | 0.0118 | ||

| 500 | 54.5811 | 0.0189 | 108.9087 | 0.0112 | ||

| 750 | 91.5288 | 0.0171 | 166.3432 | 0.0100 | ||

| 1000 | 105.1695 | 0.0163 | 189.5432 | 0.0087 | ||

| 1500 | 122.1278 | 0.0159 | 326.7654 | 0.0074 | ||

| KSAPF | 200 | 32.8328 | 0.0131 | 55.039200 | 0.0121 | |

| 300 | 47.4919 | 0.0129 | 90.691115 | 0.0116 | ||

| 400 | 58.3216 | 0.0118 | 107.767974 | 0.110 | ||

| 500 | 66.3554 | 0.0114 | 127.565273 | 0.102 | ||

| 750 | 76.4818 | 0.0103 | 173.311428 | 0.0086 | ||

| 1000 | 93.8846 | 0.0093 | 246.09729 | 0.0073 | ||

| 1500 | 151.7971 | 0.0084 | 376.8976 | 0.0068 | ||

| QML | 200 | 0.0268 | 0.172 | 0.0283 | 0.0444 | |

| 300 | 0.0201 | 0.164 | 0.0312 | 0.0331 | ||

| 400 | 0.0532 | 0.153 | 0.0386 | 0.0336 | ||

| 500 | 0.0675 | 0.146 | 0.0476 | 0.0327 | ||

| 750 | 0.1046 | 0.132 | 0.0631 | 0.0311 | ||

| 1000 | 0.0702 | 0.118 | 0.0712 | 0.0278 | ||

| 1500 | 0.2148 | 0.110 | 0.0854 | 0.0253 |

| CPU (sec) | ||||

|---|---|---|---|---|

| 0.7 | 0.3 | 0.667 | 0.2892 | 74300 |

2.5.2 Parameter estimates

For the AR(1) Gaussian model, we run estimates for each method (QML, APF, KSAPF and Bootsrap filter) and for the SV model. The number of observations is equal to for the two models.

In order to compare with others the performance of our estimator, we compute for each method the Mean Square Error (MSE) defined by:

| (15) |

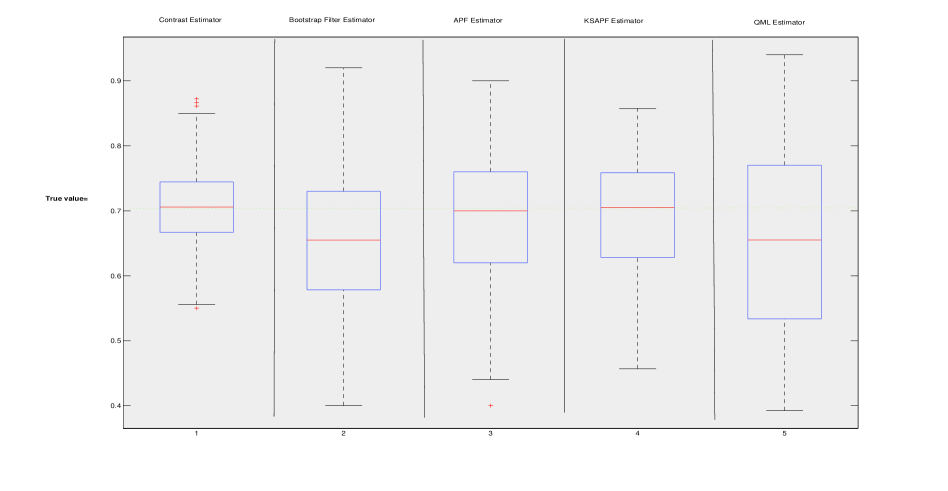

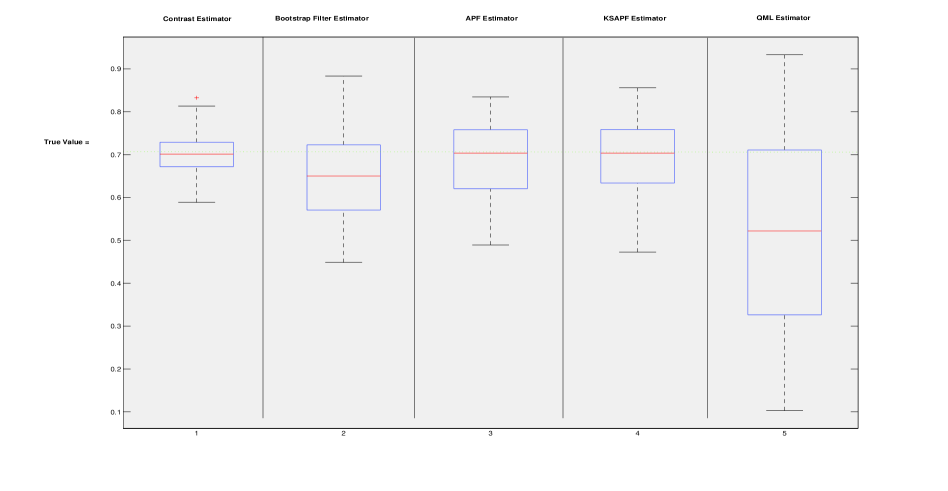

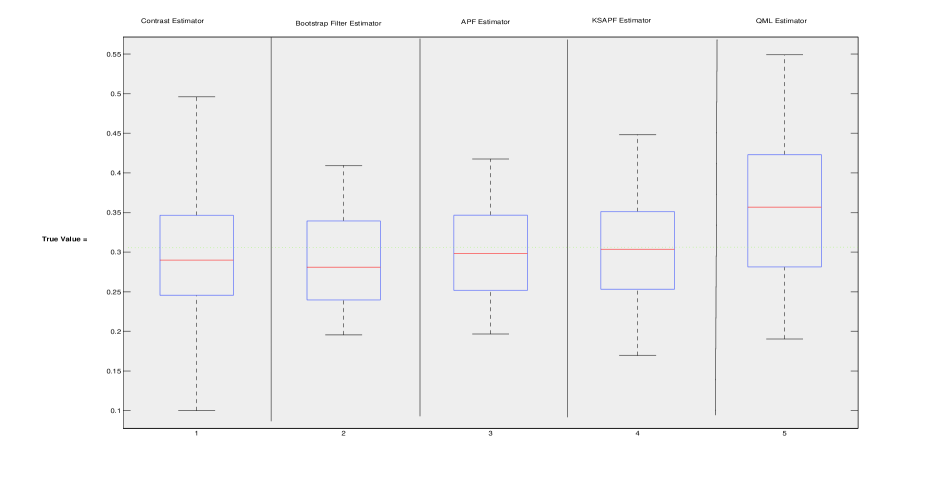

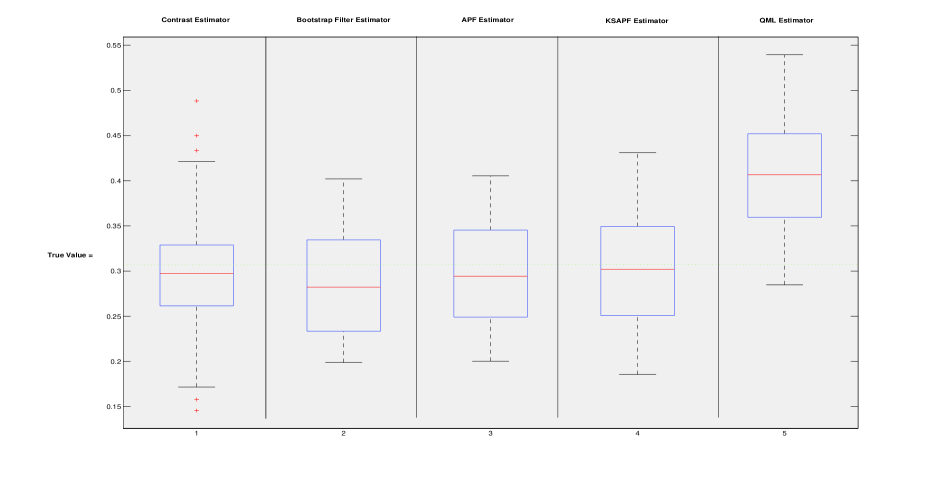

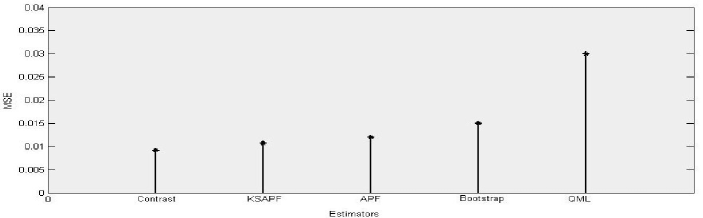

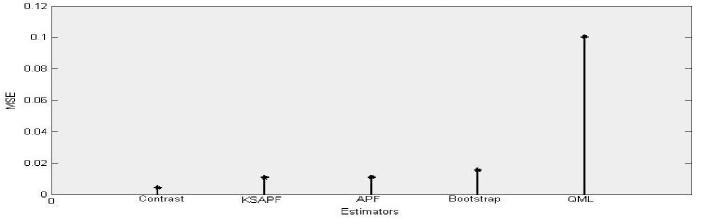

We illustrate by boxplots the different estimates (see Figures [2] and [3]). We also illustrate in Figure [4] the MSE for each estimator computed by equation(15). We can see that, for the parameter , the QML estimator is better for the Gaussian AR(1) model than for the SV model (see Figure [2]). Indeed, the Gaussianity assumption is wrong for the SV model. Moreover, the estimate of by QML is very bad for the two models (see Figure [3]) and its corresponding boxplots have the largest dispersion meaning that the QML method is not very stable. The Bootstrap, APF and KSAPF have also a large dispersion of their boxplots, in particular for the parameter (see Figure [2]). Besides, the Booststrap filter is less efficient than the APF and KSAPF. For the Gaussian and SV model, the boxplots of our contrast estimator show that our estimator is the most stable with respect to and we obtain similar results for . The MSE is better for the SV model and the smallest for our contrast estimator.

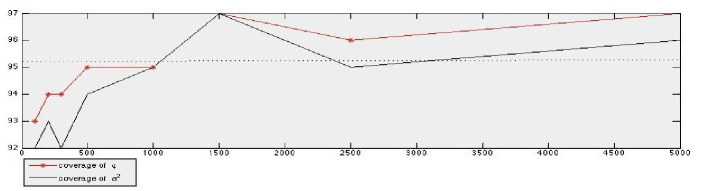

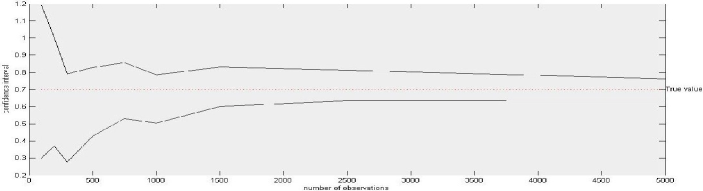

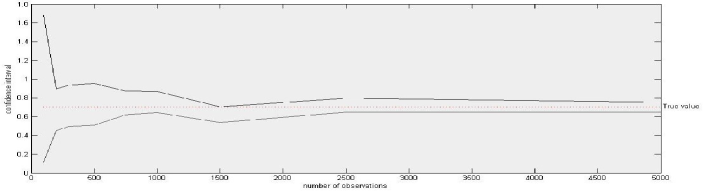

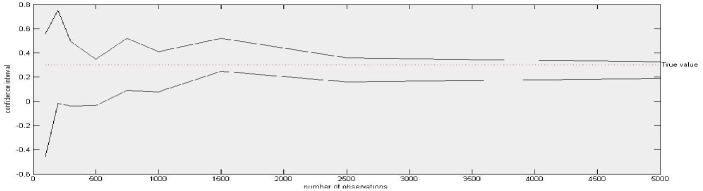

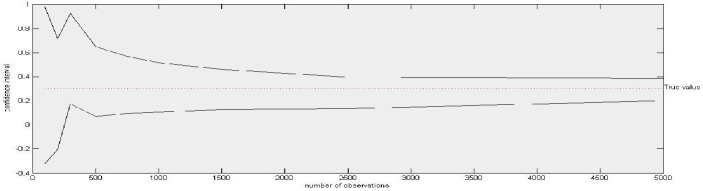

2.5.3 Confidence Interval of the contrast estimator

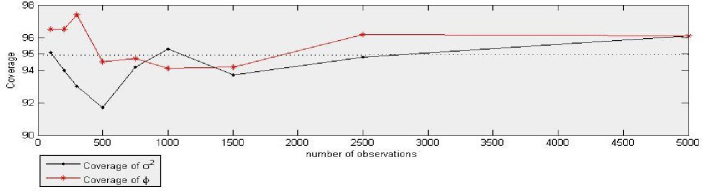

To illustrate the statistical properties of our contrast estimator, we compute for each model the confidence intervals computed with the confidence level equal to for estimator and the coverages for with respect to the number of observations. The coverage corresponds to the number of times for which the true parameter belongs to the confidence interval. The results are illustrated by the Figures [5]-[6] and [7]: for the Gaussian and SV models, the coverage converges to for a small number of observations. As expected, the confidence interval decreases with the number of observations,. Note that of course a MLE confidence interval would be smaller since the MLE is efficient but the corresponding computing time would be huge.

2.6 Application to Real Data

The data consist of daily observations on FTSE stock price index and SP500 stock price index. The series taken in boursorama.com are closing prices from January, 3, 2004 to January, 2, 2007 for the FTSE and SP500 leaving a sample of observations for the two series.

The daily prices are transformed into compounded rates returns centered around their sample mean for self-normalization (see [MS98] and [GHR96]) . We want to model those data by the SV model defined in (13) leading to :

Those data are represented on Figure [8].

2.6.1 Parameter Estimates

In the empirical analysis, we compare the QML, the Bootstrap filter, the APF and the KSAPF estimators. The last one is our contrast estimator. The variance of the measurement noise is , that is is equal to (see Section 2.4). Table [3] summarises the parameter estimates and the computing time for the five methods. For initialization of the Bayesian procedure, we take the Uniform law for the parameters and the stationary law for the log-volatility process , i.e, .

The estimates of are in full accordance with results reported in previous studies of SV models. This parameter is in general close to 1 which implies persistent logarithmic volatility data. We compute the corresponding confidence intervals at level (see Table [4]). For the SP500 and the FTSE, note that the Bootstrap filter and the QML are not in the confidence interval for the two parameters and . These results are consistent with the simulations where we showed that both methods were biased for the SV model (see Section 2.5.2). Note also that as expected the computing time for the QML is the shortest because it assumes Gaussianity which is probably not the case here. Except of QML, the contrast is the fastest method. The results are presented in Table [3] below.

| Index | FTSE | SP500 | ||||

| CPU | CPU | |||||

| Contrast | 0.69 | 0.27 | 26 | 0.78 | 0.13 | 38 |

| Bootstrap filter | 0.91 | 0.15 | 204 | 0.830 | 0.247 | 214 |

| APF | 0.693 | 0.29 | 169 | 0.734 | 0.108 | 182 |

| KSAPF | 0.697 | 0.29 | 152 | 0.80 | 0.12 | 175 |

| QML | 0.649 | 0.08 | 0.07 | 0.895 | 0.257 | 0.1 |

| Index | Confidence Interval | |

|---|---|---|

| FTSE | [ 0.6627 ; 0.7173] | [0.1771 ; 0.3629] |

| SP500 | [ 0.7086 ; 0.8514] | [ 0.0278 ; 0.2322] |

2.7 Summary and Conclusions

In this paper we propose a new method to estimate an hidden stochastic model on the form (1). This method is based on the deconvolution strategy and leads to a consistent and asymptotically normal estimator. We empirically study the performance of our estimator for the Gaussian AR(1) model and SV model and we are able to construct a confidence interval (see Figures [6] and [7]). As the boxplots [2] and [3] show, only the Contrast, the APF, and the KSAPF estimators are comparable. Indeed the QML and the Bootstrap Filter estimators are biased and their MSE are bad, and in particular, the QML method is the worst estimator (see Figure [4]). One can see that the QML estimator proposed by Harvey et al. is not suitable for the SV model because the approximation of the log-chi-square density by the Gaussian density is not robust (see Figure [1]). Furthermore, if we compare the MSE of the three Sequential Bayesian estimation, the KSAPF estimator is the best method. From a Bayesian point of view, it is known that the Bootstrap filter is less efficient than the APF and KSAPF filter since by using the density transition as the importance density, the propagation step of the particles will be made without taking care the observations (see [DdFG01]).

Among the three estimators (Contrast, APF, and KSAPF) which give good results our estimator outperforms the others in a MSE aspect (see Figure [4]). Moreover, as we already mentioned, in the combined state and parameters estimation the difficulties are the choice of , and the prior law since the results depend on these choices. In the numerical section, we have used the stationary law for the variable and this choice yields good results but we expect that the behavior of the Bayesian estimation will be worse for another prior. The implementation of the contrast estimator is the easiest and it leads to confidence intervals with a larger variance than the SIEMLE but at a smaller computing cost, in particular for the AR(1) Gaussian model (see Table [1]). Furthermore, the contrast estimator does not require an arbitrary choice of parameter in practice.

Appendix A M-Estimator

Definition 1.

Geometrical ergodic process

Denote by the transition kernel at step of a (discrete-time) stationary Markov chain which started at at time . That is, . Let denote the stationary law of and let be any measurable function. We call mixing coefficients the coefficients defined by, for each :

where . We say that a process is geometrically ergodic if the decreasing of the sequence of the mixing coefficients is geometrical, that is:

The following results are the main tools for the proof of Theorem 1.1.

Consider the following quantities:

where is real function from with value in .

Lemma 1.

Uniform Law of Large Numbers (ULLN)(see [NM94] for the proof.)

Let be an ergodic stationary process and suppose that:

-

1.

is continuous in for all and measurable in for all in the compact subset .

-

2.

There exists a function (called the dominating function) such that for all and . Then:

Moreover, is a continuous function of .

Proposition 1 (Proposition 7.8 p. 472 in [Hay00]. The proof is in [New87] Theorem 4.1.5.).

Suppose that:

-

1.

is in the interior of .

-

2.

is twice continuously differentiable in for any .

-

3.

The Hessian matrix of the application is non-singular.

-

4.

in law as n , with a positive definite matrix.

-

5.

Local dominance on the Hessian: for some neighbourhood of :

so that, for any consistent estimator of we have: in probability as n .

Then, is asymptotically normal with asymptotic covariance matrix given by:

where the differential is taken at point .

Proposition 2 (The proof is in [Jon04]).

Let be an ergodic stationary Markov chain and let g: a borelian function. Suppose that is geometrically ergodic and for some . Then, when ,

where

Appendix B Proofs of Theorem 1.1

For the reader convenience we split the proof of Theorem 1.1 into three parts: in Subsection B.1, we give the proof of the existence of our contrast estimator defined in (1.1). In Subsection B.2, we prove the consistency, that is, the first part of Theorem 1.1. Then, we prove the asymptotic normality of our estimator in Subsection B.3, that is, the second part of Theorem 1.1. The Section B.4 is devoted to Corollary 1. Finally, in Section C we prove that Theorem 1.1 applies for the AR(1) and SV models.

B.1 Proof of the existence and measurability of the M-Estimator

By assumption, the function is continuous. Moreover, and then are continuous w.r.t . In particular, the function is continuous w.r.t . Hence, the function is continuous w.r.t belonging to the compact subset . So, there exists belongs to such that:

B.2 Proof of the Consistency

By assumption is continuous w.r.t for any and measurable w.r.t for all which implies the continuity and the measurability of the function on the compact subset . Furthermore, the local dominance assumption (C) implies that is finite. Indeed,

As is continuous on the compact subset , is finite. Therefore, is finite if is finite. Lemma ULLN 1 gives us the uniform convergence in probability of the contrast function: for any :

Combining the uniform convergence with Theorem 2.1 p. 2121 chapter 36 in [HH97] yields the weak (convergence in probability) consistency of the estimator.∎

Remark 5.

In most applications, we do not know the bounds for the true parameter. So the compactness assumption is sometimes restrictive, one can replace the compactness assumption by: is an element of the interior of a convex parameter space . Then, under our assumptions except the compactness, the estimator is also consistent. The proof is the same and the existence is proved by using convex optimization arguments. One can refer to [Hay00] for this discussion.

B.3 Proof of the asymptotic normality

The proof is based on the following Lemma:

Lemma 2.

Suppose that the conditions of the consistency hold. Suppose further that:

-

1.

geometrically ergodic.

-

2.

(Moment condition): for some and for each

.

-

3.

(Hessian Local condition): For some neighbourhood of and for :

Proof.

It just remains to check that the conditions (2) and (3) of Lemma 2 hold under our assumptions (T) .

Moment condition: As the function is twice continuously differentiable w.r.t , for all , the application is twice continuously differentiable for all and its first derivatives are given by:

By assumption, for each , , therefore one can apply the Lebesgue Derivation Theorem and Fubini’s Theorem to obtain :

| (16) |

Then, for some :

| (17) | |||||

where and are two positive constants. By assumption, the function is twice continuously differentiable w.r.t . Hence, is continuous on the compact subset and the first term of equation (17) is finite. The second term is finite by the moment assumption (T).

Hessian Local dominance: For , , the Lebesgue Derivation Theorem gives:

and, for some neighbourhood of :

The first term of the above equation is finite by continuity and by compactness argument. And, the second term is finite by the Hessian local dominance assumption (T).∎

B.4 Proof of Corollary 1

By replacing by its expression (16), we have:

Furthermore, by Eq.(1) and by independence of the centered noise and , we have:

Using Fubini’s Theorem and Eq.(1) we obtain:

| (18) | |||||

Hence,

where

By using Eq.(18) and the stationary property of the , one can replace the second term of the above equation by:

Furthermore, by using Eq.(1) we obtain:

| (19) | |||||

| (20) | |||||

| (21) |

By independence of the centered noise, the term (19), (20) and (21) are equal to zero. Now, if we use Fubini’s Theorem we have:

| (22) |

Hence, the covariance matrix is given by:

Finally, we obtain: with and .

Expression of the Hessian matrix : We have:

| (23) |

For all in , the application is twice differentiable w.r.t on the compact subset . And for :

and for :

Appendix C Proof of the Applications

C.1 The Gaussian AR(1) model with measurement noise

C.1.1 Contrast Function

We have:

So that:

and the Fourier Transform of is given by:

As is a centered Gaussian noise with variance , we have:

Define:

Then:

where . We deduce that the function is given by:

Then, the contrast estimator defined in (1.1) is given by:

C.1.2 Checking assumptions of Theorem 1.1

Mixing properties. If , the process is geometrically ergodic. For further details, we refer to [DDL+07].

Regularity conditions:

It remains to prove that the assumptions of Theorem 1.1 hold. It is easy to see that the only difficulty is to check the moment condition and the local dominance (C)-(T) and the uniqueness assumption (CT). The others assumptions are easily to verify since the function is regular in belonging to .

(CT): The limit contrast function given by:

is differentiable for all in and if and only if is equal to . More precisely its first derivatives are given by:

and

The partial derivatives of w.r.t are given by:

For the reader convenience let us introduce the following notations:

| (24) | |||

| (25) |

We rewrite:

where the function defines the normal probability density of a centered random variable with variance . Now, we can use Corollary 1 to compute the Hessian matrix :

| (26) |

with . By replacing the terms and at the point we obtain:

| (27) |

which has a positive determinant equal to at the true value . Hence, is non-singular. Furthermore, the strict convexity of the function gives that is a minimum.

(C): (Local dominance): We have:

The multivariate normal density of the pair denoted is given by:

with:

By definition of the parameter space and as all moments of the pair exist, the quantity is finite.

Moment condition (T): We recall that:

The Fourier transforms of the first derivatives are:

and

We can compute the function :

with and and The Fourier transform of the function is given by:

| (28) | |||||

with and By the same arguments, we obtain:

| (29) |

with and

Hence, for some , is finite if:

which is satisfied by the existence of all moments of the pair . One can check that the Hessian local assumption (T) is also satisfied by the same arguments.

C.1.3 Explicit form of the Covariance matrix

Lemma 3.

The matrix in the Gaussian AR(1) model is given by:

with

and

where:

and is the symmetric matrix multiplied by a factor and its coefficients are given by:

with , , , and:

The covariance terms are given by:

with:

where:

Moreover .

Remark 6.

In practice, for the computing of the covariance matrix that appears in Corollary 1, we have truncated the infinite sum ().

Proof.

Calculus of

For all , the function is two times differentiable w.r.t on the compact subset . More precisely, note that since , it follows from the definition of the subset that . So that for all in the function is differentiable and:

with:

| (30) |

Calculus of : Recall that we have:

And the moments of a centered Gaussian random variable with variance are given by:

We define by a polynomial function of ordinary degree. We are interested in the calculus of where . We have:

where .

Denote by the constant . We obtain:

where . The polynomials are given by:

Lastly, by replacing the terms , , and by their expressions given in Eq.(24) at the point , we obtain:

Calculus of :

We have:

| (31) | |||||

The density of is . Then, is equal to:

with and .

Then, we obtain:

In the following, we set . Now, we can compute the moments:

In a similar manner, we have:

and

By replacing all the terms of Eq.(31) we obtain:

| (32) | |||||

and

| (33) | |||||

and

| (34) |

Calculus of : We want to compute:

Since we have already computed the terms of the matrix , it remains to compute the terms of the covariance matrix given by:

For all , the pair has a multivariate normal density where is given by:

The density of the couple is:

We start by computing:

We have:

For all , we define:

We can rewrite:

So, by Fubini’s Theorem, we obtain:

where . Thus, . We obtain:

| (35) |

where . Additionally, we have:

| (36) |

Now, we are interested in . In a similar manner, we obtain:

| (37) |

where . We use the fact that the moments of a random variable are:

By replacing in equation (C.1.3), we have:

| (38) |

For all , the matrix is given by:

Finally, by replacing the terms , , and , the matrix is equal to:

where .

Asymptotic behaviour of the covariance matrix : By the stationary assumption , the limits of the following terms are:

and

Therefore,

We obtain:

We conclude that the covariance between the two vectors vanishes when the lag between the two observations and goes to the infinity.

Calculus of : The Hessian matrix is given in Eq. (27).

∎

C.2 The SV model

C.2.1 Contrast function

The -norm and the Fourier transform of the function are the same as the Gaussian AR(1) model. The only difference is the law of the measurement noise which is a log-chi-square for the log-transform SV model.

Consider the random variable where such that is centered. The random variable is a standard Gaussian random. The Fourier transform of is given by:

By a change of variable , one has:

and the expression (14) of the contrast function follows with .

C.2.2 Checking assumption of Theorem 1.1

Regularity conditions: The proof is essentially the same as for the Gaussian case since the functions and are the same. We need only to check the assumptions (C) and (T). These assumptions are satisfied since Fan (see [Fan91]) showed that the noises have a Fourier transform which satisfies :

which means that is super-smooth in its terminology. Furthermore, by the compactness of the parameter space and as the functions , and for , the functions , have the following form where and are two constants well defined in the parameter space with , we obtain:

C.2.3 Expression of the Covariance matrix:

As, the functions and are the same for the two models, the expressions of the matrix and are given in Lemma 3. We need only to use an estimator of since we can just approximate . A natural and consistent estimator of is given by:

| (39) |

Remark 7.

In some models, the covariance matrix cannot be explicitly computable. We refer the reader to [Hay00] chapter 6 Section 6.6 p.408 for this case.

Appendix D EM algorithm

We first refer to [DLR77] for general details on the EM algorithm. The EM algorithm is an iterative procedure for maximizing the log-likelihood . Suppose that after the iteration, the estimate for is given by . Since the objective is to maximize , we want to compute an updated such that:

Hidden variables can be introduced for making the ML estimation tractable. Denote the hidden random variables and a given realization by . The total probability can be written as:

Hence,

| (40) | |||||

| (41) | |||||

In going from Eq.(40) to Eq.(41) we use the Jensen inequality: for constants with . And in going from Eq.(41) to Eq.(D) we use the fact that . Hence,

The function is bounded by the log-likelihood function and they are equal when . Consequently, any which increases will increases . The EM algorithm selects such that is maximized. We denote this updated value . Thus,

| (43) | |||||

D.1 Simulated Expectation Maximization Estimator

Here, we describe the SIEMLE proposed by Kim, Shepard and Chib [KS94] for the SV model, these authors retain the linear log-transform model given in (13). However, instead of approximating the log-chi-square distribution of with a Gaussian distribution, they approximate by a mixture of seven Gaussian. The distribution of the noise is given by:

where denotes the Gaussian distribution of with mean and variance , and is a Gaussian distribution conditional to an indicator variable at time and the variables are the given weights attached to each component and such that . Note that, most importantly, given the indicator variable at each time , the log-transform model is Gaussian. That is:

Then, conditionally to the indicator variable , the SV model becomes a Gaussian state-space model and the Kalman filter can be used in the SIEMLE in order to compute the log-likelihood function given by:

with and . The quantities and are computed by the Kalman filter.

Hence, if we consider that the missing data for the EM correspond to the indicator variables , then according to Eq.(43) and since do not depend on , the Maximization step is:

where the expectation is according to . Nevertheless, for the SV model, the problem with the EM algorithm is that the density is unknown. The main idea consists in introducing a Gibbs algorithm to obtain draws from the law . Hence, the objective function is approximated by:

Then, the simulated EM algorithm for the SV model is as follows: Let be a threshold to stop the algorithm and a given arbitrary value of the parameter. While

-

1.

Apply the Gibbs sampler as follows:

The Gibbs Sampler: Choose arbitrary starting values , and let .

-

(a)

Sample .

-

(b)

Sample .

-

(c)

Set and goto (a).

-

(a)

-

2.

.

Step (a): to sample the vector from its full conditional density, we sample each independently. We have:

and for And the step (b) of the Gibbs sampler is conducted by the Kalman filter since the model is Gaussian.

Acknowledgements 1.

I thank my co-director Patricia Reynaud-Bouret for her idea about this paper and for her help and generosity. I thank also my director Frédéric Patras for his supervisory throughout this paper. I thank him for his careful reading of the paper and his large comments. I would like to thank F. Comte, A. Samson, N. Chopin, M. Miniconi and F. Pelgrin for their suggestions and their interest about this framework.

I thank also the referees for careful reading and constructive suggestions which were helpful in improving substantially this paper.

References

- [ADH10] Christophe Andrieu, Arnaud Doucet, and Roman Holenstein. Particle Markov chain Monte Carlo methods. J. R. Stat. Soc. Ser. B Stat. Methodol., 72(3):269–342, 2010.

- [Cha95] Kamal C. Chanda. Large sample analysis of autoregressive moving-average models with errors in variables. J. Time Ser. Anal., 16(1):1–15, 1995.

- [Cho02] Nicolas Chopin. A sequential particle filter method for static models. Biometrika, 89(3):539–551, 2002.

- [CJP11] Nicolas Chopin, Pierre E. Jacob, and Omiros Papaspiliopoulos. : an efficient algorithm for sequential analysis of state-space models. Preprint in arxiv.org/abs/1101.1528, 2011.

- [CL11] F. Comte and C. Lacour. Data-driven density estimation in the presence of additive noise with unknown distribution. J. R. Stat. Soc. Ser. B Stat. Methodol., 73(4):601–627, 2011.

- [CLR10] F. Comte, C. Lacour, and Y. Rozenholc. Adaptive estimation of the dynamics of a discrete time stochastic volatility model. J. Econometrics, 154(1):59–73, 2010.

- [CMR05a] Olivier Cappé, Eric Moulines, and Tobias Rydén. Inference in hidden Markov models. Springer Series in Statistics. Springer, New York, 2005. With Randal Douc’s contributions to Chapter 9 and Christian P. Robert’s to Chapters 6, 7 and 13, With Chapter 14 by Gersende Fort, Philippe Soulier and Moulines, and Chapter 15 by Stéphane Boucheron and Elisabeth Gassiat.

- [CMR05b] Olivier Cappé, Eric Moulines, and Tobias Rydén. Inference in hidden Markov models. Springer Series in Statistics. Springer, New York, 2005. With Randal Douc’s contributions to Chapter 9 and Christian P. Robert’s to Chapters 6, 7 and 13, With Chapter 14 by Gersende Fort, Philippe Soulier and Moulines, and Chapter 15 by Stéphane Boucheron and Elisabeth Gassiat.

- [CT01] F. Comte and M.-L. Taupin. Semiparametric estimation in the (auto)-regressive -mixing model with errors-in-variables. Math. Methods Statist., 10(2):121–160, 2001.

- [DdFG01] Arnaud Doucet, Nando de Freitas, and Neil Gordon, editors. Sequential Monte Carlo methods in practice. Statistics for Engineering and Information Science. Springer-Verlag, New York, 2001.

- [DDL+07] Jérôme Dedecker, Paul Doukhan, Gabriel Lang, José Rafael León R., Sana Louhichi, and Clémentine Prieur. Weak dependence: with examples and applications, volume 190 of Lecture Notes in Statistics. Springer, New York, 2007.

- [DLR77] A. P. Dempster, N. M. Laird, and D. B. Rubin. Maximum likelihood from incomplete data via the EM algorithm. J. Roy. Statist. Soc. Ser. B, 39(1):1–38, 1977. With discussion.

- [DMOvH11] Randal Douc, Eric Moulines, Jimmy Olsson, and Ramon van Handel. Consistency of the maximum likelihood estimator for general hidden Markov models. Ann. Statist., 39(1):474–513, 2011.

- [DST11] Jerome Dedecker, Adeline Samson, and Marie Luce Taupin. Estimation in autoregressive model with measurement noise. Preprint: hal-00591114, 2011.

- [Fan91] Jianqing Fan. Asymptotic normality for deconvolution kernel density estimators. Sankhyā Ser. A, 53(1):97–110, 1991.

- [GCJL00] Valentine Genon-Catalot, Thierry Jeantheau, and Catherine Larédo. Stochastic volatility models as hidden Markov models and statistical applications. Bernoulli, 6(6):1051–1079, 2000.

- [GHR96] Eric Ghysels, Andrew C. Harvey, and Eric Renault. Stochastic volatility. In Statistical methods in finance, volume 14 of Handbook of Statist., pages 119–191. North-Holland, Amsterdam, 1996.

- [Hay00] Fumio Hayashi, editor. Econometrics. Princeton University Press, Princeton NJ, 2000.

- [HH97] Bruce E. Hansen and Joel L. Horowitz. Handbook of econometrics, vol. 4 robert f. engle and daniel l. mcfadden, editors elsevier science b. v., 1994. Econometric Theory, 13(01):119–132, February 1997.

- [HRS94] Andrew Harvey, Esther Ruiz, and Neil Shephard. Multivariate stochastic variance models. Review of Economic Studies, 61(2):247–64, April 1994.

- [IBAK11] Edward L. Ionides, Anindya Bhadra, Yves Atchadé, and Aaron King. Iterated filtering. Ann. Statist., 39(3):1776–1802, 2011.

- [JDD08] Adam M. Johansen, Arnaud Doucet, and Manuel Davy. Particle methods for maximum likelihood estimation in latent variable models. Stat. Comput., 18(1):47–57, 2008.

- [Jon04] Galin L. Jones. On the Markov chain central limit theorem. Probab. Surv., 1:299–320, 2004.

- [JPR02] Eric Jacquier, Nicholas G. Polson, and Peter E. Rossi. Bayesian analysis of stochastic volatility models. J. Bus. Econom. Statist., 20(1):69–87, 2002. Twentieth anniversary commemorative issue.

- [JPS09] Michael S. Johannes, Nicholas G. Polson, and Jonathan R. Stroud. Optimal filtering of jump diffusions: Extracting latent states from asset prices. Review of Financial Studies, 22(7):2559–2599, July 2009.

- [Kal60] R. E. Kalman. A new approach to linear filtering and prediction problems. 1960.

- [KS94] Sangjoon Kim and Neil Shephard. Stochastic volatility: likelihood inference and comparison with arch models. Economics Papers 3., Economics Group, Nuffield College, University of Oxford, November 1994.

- [LW01] J. Liu and M. West. Combined parameter and state estimation in simulation-based filtering. in arnaud doucet, nando de freitas, and neil gordon, editors. Sequential Monte Carlo Methods in Practice, 2001.

- [MS98] R. J. Mathieu and P. C. Schotman. An empirical application of stochastic volatility models. Review of Economic Studies, 13(4):333–360, 1998.

- [MT90] Angelo Melino and Stuart M. Turnbull. Pricing foreign currency options with stochastic volatility. Journal of Econometrics, 45(1-2):239–265, 1990.

- [New87] Whitney K. Newey. Advanced econometrics by takeshi amemiya, harvard university press, 1986. Econometric Theory, 3(01):153–158, February 1987.

- [NM94] Whitney K. Newey and Daniel McFadden. Large sample estimation and hypothesis testing. In Handbook of econometrics, Vol. IV, volume 2 of Handbooks in Econom., pages 2111–2245. North-Holland, Amsterdam, 1994.

- [PDS11] George Poyiadjis, Arnaud Doucet, and Sumeetpal S. Singh. Particle approximations of the score and observed information matrix in state space models with application to parameter estimation. Biometrika, 98(1):65–80, 2011.

- [PHH10] Gareth W. Peters, Geoffrey R. Hosack, and Keith R. Hayes. Ecological non-linear state space model selection via adaptive particle markov chain monte carlo (adpmcmc). Preprint:arXIv-1005.2238v1, 2010.

- [PS99] Michael K. Pitt and Neil Shephard. Filtering via simulation: auxiliary particle filters. J. Amer. Statist. Assoc., 94(446):590–599, 1999.

- [RMC09] Håvard Rue, Sara Martino, and Nicolas Chopin. Approximate Bayesian inference for latent Gaussian models by using integrated nested Laplace approximations. J. R. Stat. Soc. Ser. B Stat. Methodol., 71(2):319–392, 2009.

- [RRT00] Christian P. Robert, Tobias Rydén, and D. M. Titterington. Bayesian inference in hidden Markov models through the reversible jump Markov chain Monte Carlo method. J. R. Stat. Soc. Ser. B Stat. Methodol., 62(1):57–75, 2000.

- [SR93] A. F. M. Smith and G. O. Roberts. Bayesian computation via the Gibbs sampler and related Markov chain Monte Carlo methods. J. Roy. Statist. Soc. Ser. B, 55(1):3–23, 1993.

- [Tay05] Sj Taylor. Financial returns modelled by the product of two stochastic processes, a study of daily sugar prices., volume 1, pages 203–226. Oxford University Press, 2005.

- [VdV98] A. W. Van der Vaart. Asymptotic statistics, volume 3 of Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press, Cambridge, 1998.