On Bayesian quantile regression curve fitting via auxiliary variables

Abstract

Quantile regression has received increased attention in the statistics community in recent years. This article adapts an auxiliary variable method, commonly used in Bayesian variable selection for mean regression models, to the fitting of quantile regression curves. We focus on the fitting of regression splines, with unknown number and location of knots. We provide an efficient algorithm with Metropolis-Hastings updates whose tuning is fully automated. The method is tested on simulated and real examples and its extension to additive models is described. Finally we propose a simple postprocessing procedure to deal with the problem of the crossing of multiple separately estimated quantile curves.

Keywords: Quantile regression; Curve fitting; Gibbs sampling; Splines; Additive models; Automatic tuning; Noncrossing curves.

1 Introduction

Quantile regression has been recognized in recent years as a robust statistical procedure that offers a powerful alternative to the ordinary mean regression, especially when the data contains large outliers or when the response variable has a skewed or multimodal conditional distribution. Given a fixed probability , , let the model corresponding to the -th quantile regression curve be given by

where are independent draws from a noise distribution whose -th quantile is , i.e. . Under this model the -th quantile of the conditional distribution of given is given by some smooth function . If the distribution of the noise is left unspecified then the estimation of is typically carried out by solving the minimization problem, for a given class of curves,

| (1) |

where the so-called ”check function” is given by if and otherwise (see [Koenker and Bassett (1978]). To define a likelihood function, one usually assumes that the noise distribution is an asymetric Laplace distribution so that the maximum likelihood estimate corresponds to the solution of the minimization problem (see [Koenker and Machado (1999]). See e.g. ?) or ?) for a review on quantile regression and ?) for quantile regression with longitudinal data. References on Bayesian treatments of the subject include ?) for inference on a single quantile, ?) for quantile regression with a random walk Metropolis-Hastings algorithm and ?) for quantile regression with a reversible jump MCMC sampler (RJMCMC, [Green (1995]). More recently ?) considers additive mixed regression models and inference with either MCMC sampling or the integrated nested Laplace approximation (INLA, [Rue et al. (2009]) and ?) proposed quantile regression with a Gibbs sampler.

In this article, we are interested in the case where the curve is modeled with spline functions of a given degree, , so that,

| (2) |

where and where represent the locations of knot points (see [Hastie and Tibshirani (1990]). Typically, the degree is set to equal 3, since cubic splines are known to approximate locally smooth functions arbitrarily well. ?) provides a Bayesian inference on this model, where the number of knots and their location are automatically selected. Their method relies on a RJMCMC algorithm which, under the prior specifications they use, needs to compute an approximation of the ratio of marginal likelihoods. For fitting of quantile smoothing splines see ?) and ?) and for a Bayesian inference with natural cubic splines see ?).

We propose here an alternative strategy that avoids the use of the RJMCMC sampler which can often be difficult to tune (see [Fan and Sisson (2011] for a review) and that does not rely on approximations to simplify computations. Recognising that a Bayesian variable selection technique (e.g. [George and McCulloch (1993]) can be used for inference on a curve (e.g. [Smith and Kohn (1996], [Fan et al. (2010]) we use an auxiliary variable approach which makes possible, under appropriate prior specifications, a Metropolis-Hastings within Gibbs sampler. The proposed MCMC sampler is easy to implement and fully automated. In particular it incorporates an algorithm which automatically tunes the scaling parameters used in our Random-walk Metropolis-Hastings algorithm.

In Section 2 we present the model and the prior specifications, then we describe how inference is carried out with a MCMC sampler. We apply the method on several datasets in Section 3. In Section 4 we consider quantile curve regression for additive models. Finally, in Section 5, we discuss the problem of crossing quantile curves and propose a simple postprocessing procedure to reweight the MCMC samples from separately estimated quantile curves.

2 Quantile regression with splines

For some , and given paired observations , we are interested in fitting the -th quantile regression model

| (3) |

where are independent draws from the asymetric Laplace distribution

| (4) |

for an unknown scale parameter . Under this model the -th quantile of the conditional distribution of given is . The asymetric Laplace distribution has been adopted in many papers, see for example ?), ?), ?), ?), ?) or ?) . Under the asymmetric Laplace distribution, given , the function maximizing the likelihood corresponding to model (3) is also the solution of the minimization problem in Equation (1). The scale parameter that takes into account the variability of the observations is considered as a nuisance parameter.

We consider hereafter that the curve is modeled with spline functions of a given degree , in the form of Equation (2). Under this representation, fitting the curve consists of estimating the number of knots , the knot locations , and the corresponding regression coefficients , and , . If , , where represents the (known) maximum number of potential knots, model (3) can be written as the linear model

| (5) |

where , , , with design matrix

| (6) |

where and where denotes the unit vector of size .

2.1 The model and prior assumptions

We adopt an auxiliary variable approach for the spline regression model by introducing a vector of binary indicator variables ,

where denotes the spline coefficients in model (5), and the intervals are defined on the range of the ’s. Each interval contains at most one knot with unknown location . In practice, such intervals can be defined by either using prior information on regions where a knot is suspected or, in the absence of such prior information, an equal partition of the range may be adopted. We denote the vector by and consider the Uniform distributions on the interval as the prior distribution on . Each possible value for gives a model of the form (5). Let denotes the matrix constructed with the columns of corresponding to non-zero entries in , and let denotes the vector of corresponding regression coefficients.

A desirable feature of the asymetric Laplace distribution is that it can be decomposed as a scale mixture of normals (see e.g. [Tsionas (2003], [Yue and Rue (2011] or [Kozumi and Kobayashi (2011])

where denotes the exponential distribution with mean . If , denote the variable associated with each , the conditional distribution of given , the diagonal matrix with entries , , is

| (7) |

Conditional on we use the following decomposition of the joint prior distribution of the unknown parameters

where we set

| (8) |

This conditional prior for , related to -priors ([Zellner (1986]), has the advantage of conjugacy in the case of normal errors, in which case the regression and variance parameters can be analytically integrated out.

Different choices for the parameter have been proposed in the literature for mean regression problems. The case , where is the sample size, corresponds to the unit information prior which was used by ?), a default choice that works well in practice in Bayesian variable selection problems with large sample sizes. ?) recommend values of in the range for the problems they considered. Here including an adaptive scale parameter , and treating it as another parameter was more satisfactory than using a fixed one. Thus we include a hyper-prior for , following e.g. ?), we use a diffuse prior with a mode at

See ?) for more discussion about the choice of a prior distribution on the parameter .

For the variance parameter, we use the standard uninformative prior . Finally, we need to define the prior distribution for , we consider the decomposition of this prior given by

where is the number of non-zero entries in , i.e. the number of knots that are used in the corresponding model. We use for this term a Poisson distribution with mean that is right-truncated at a specified maximum value, . We assume also that, given this quantity, all possible configurations for have equal probabilities, so that

The parameters and can be integrated out of the full joint posterior distribution and we get

| (9) |

where

and where

Details of the marginal posterior are given in Appendix A.

2.2 Inference on the posterior distribution

An MCMC sampler is used for the inference on the model. Based on the posterior distribution (9), for each iteration of the MCMC update, , perform the following successive updates for , , and :

-

•

Update . This update involves two types of moves; with probability 0.5 we propose an add/delete step, otherwise a swap step is proposed. Specifically, the two move steps involve

-

–

add/delete: randomly select a and propose to change its value;

-

–

swap: randomly select two values and , and propose to exchange their values.

In both cases, proposed moves from current value to proposed value are accepted with the usual Metropolis-Hastings acceptance probability

where is the probability of proposing the new value given the current value .

-

–

-

•

Update . For each , we differentiate the cases when and when :

-

–

if then is updated according to its prior distribution, i.e. a Uniform distribution on ;

-

–

if , is updated to a new value , according to the posterior distribution

An independence Metropolis-Hastings step can be used for this last type of updating, using the prior on as a proposal, with the corresponding acceptance probability given by

-

–

-

•

Update . Each has conditional posterior distribution

We use a Random-walk Metropolis-Hastings proposal to update each . We consider as proposal distribution a normal distribution with mean and variance . We sample , then the proposed value is accepted with probability

The tuning parameters are optimally obtained automatically, prior to starting the main part of MCMC, see Appendix B.

-

•

Update . The parameter has conditional distribution

We use a Random-walk Metropolis-Hastings proposal to update . We sample then accept the proposed value with acceptance probability

The tuning parameter is also obtained via the algorithm in Appendix B.

Note that when the sample size is large, the number of parameters in the Update step becomes large and correspondingly manual tuning of the scale parameters in the Gaussian Random-Walk Metropolis-Hastings sampler becomes infeasible. One strategy to automate the sampler is to use a slice sampler (see [Neal (2003]). But the additional evaluations of the posterior function makes this algorithm much more computationally intensive. In this article we use the algorithm of ?) that automatically tunes the scaling parameters and obtains an optimal over all acceptance rate of ([Roberts and Rosenthal (2001]) for these univariate updates. See Appendix B for a description of the algorithm used for tuning.

Once a converged MCMC sample is obtained it is possible to estimate the curve by a Bayesian model averaging approach (BMA). The posterior expectation for given , , and is

| (10) |

Thus an estimate for can be obtained by

Another possibility to estimate the curve is to use the maximum a posteriori (MAP) estimate for

then calculate the corresponding curve estimate via

3 Examples

3.1 Simulation studies

We carry out simulations to compare the use of the method described in this paper with the method COBS proposed by ?). COBS estimates both constrained and unconstrained quantile curves using B-spline smoothing and is available as an R package. Here we use the unconstrained case as a fully automated procedure, where both the smoothing parameter and the selection of knots is carried out according to either the AIC or the BIC criterion.

We consider simulated datasets that correspond to the three examples described bellow, these examples are adapted from some well known examples in the curve fitting literature, see e.g. ?), ?) and ?).

- Example 1:

-

Here the curve takes the form

where denotes the value at of the normal density with mean and variance . data points are sampled from the Uniform distribution . The noise is added to the data, they corresponds to a Gamma distribution with shape parameter 1 and rate parameter 4 that is translated by - (so that the median of this noise distribution is approximatively 0).

- Example 2:

-

Here the curve takes the form

and is evaluated at regularly spaced grid points. This function is first rescaled so that the support is on the unit interval. The noise added to the data is simulated in the same way as in the first example.

- Example 3:

-

In this example the curve is given by,

and the data points correspond to regularly spaced grid points. As in the previous example the function is rescaled on the unit interval for and the same distribution for noise is used for the data.

To compare the different methods we use the mean squared error (MSE) as a measure of goodness of fit, given by

where is the true median regression function and is the estimated function. Since the COBS algorithm computes the median curve with quadratic (or linear) splines we consider hereafter the case .

For the prior specifications of each example, we set and for the truncated Poisson prior. Results are largely insensitive to values of around this range and the maximum number of knots allowed is chosen to be large enough to not affect the simulation results here. For these examples we consider the situation where there is no prior information on the knot locations and chose the intervals to correspond to the ranges given by every sorted values. We found that was sufficient to provide a good fit in each of the three examples. We use a B-spline basis to formulate the matrix, as in ?), to avoid numerical instability (see e.g. [Ruppert et al. (2003]).

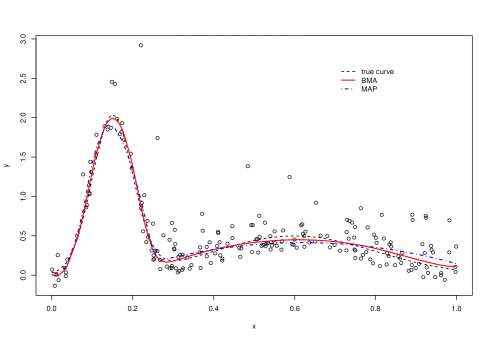

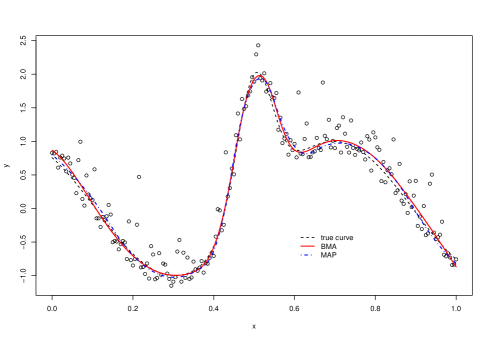

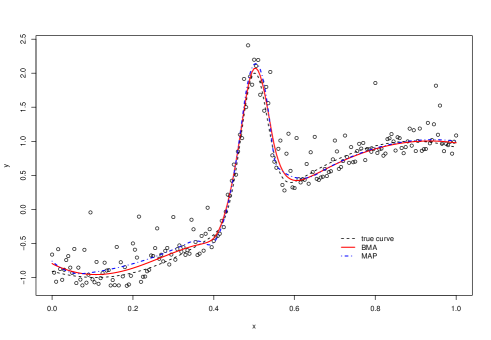

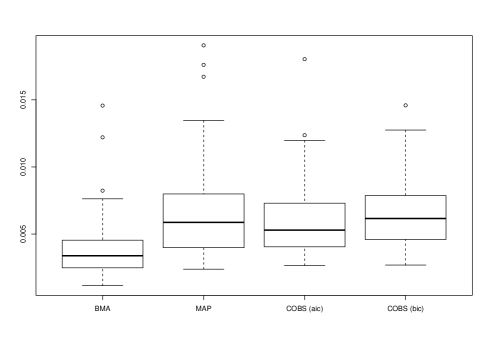

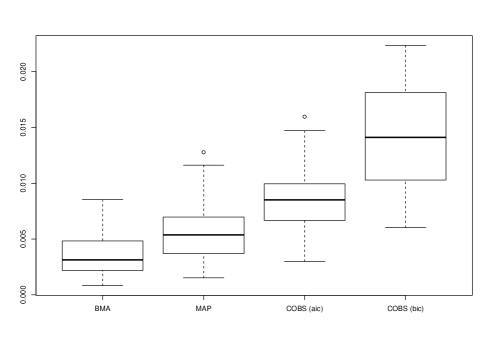

The computation of all three examples started with an arbitrary set of initial values generated from the prior distributions. We first ran the algorithm 500 iterations for adaptive tuning then fixing the scaling parameters of the Random-Walk Metropolis Hastings algorithm at the final value of the tuning run, we then ran a burn-in of 500 iterations, followed by 1,500 recorded iterations. Each iteration involves an update of 20 update steps for each update step. To assess convergence, we monitored the trace plots of each model parameters as well as posterior values. We also ran much longer chains of 10,000 iterations and found the results to be similar in terms of MSE calculations. See Figure 1 for the fitted functions of the three examples using our method with the BMA estimate and with the MAP estimate.

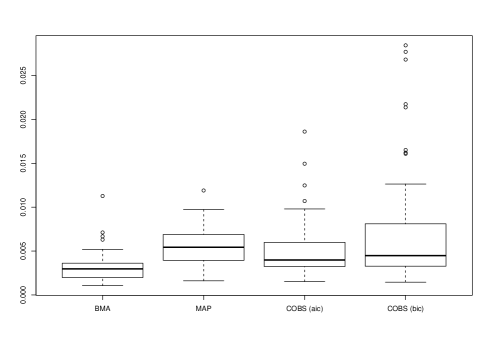

For each of the three examples the BMA, MAP and COBS (with the AIC or the BIC criterion) estimates are calculated over 50 randomly generated datasets. The mean and standard deviation of the MSEs are presented in Table 1, the corresponding boxplots are given in Figure 2. On the whole the method presented in this paper performs well compared to COBS, especially on the datasets corresponding to Example 3. On the three types of datasets that are considered here, the BMA estimates seem to be more accurate than the MAP estimates.

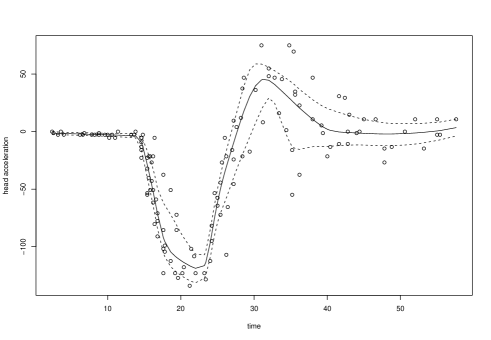

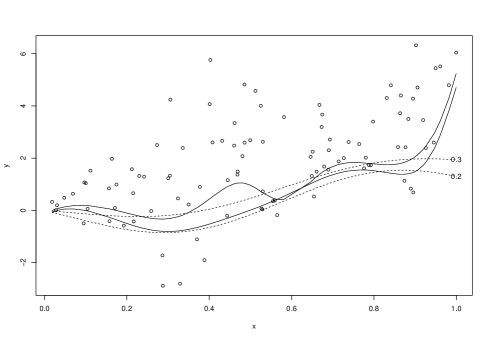

3.2 Motorcycle data set

We consider a reference dataset, the motorcycle data, studied in the context of quantile regression for example in ?) or in ?). These data are analyzed in ?) and contain experimental measurements of the acceleration of the head of a test dummy (expressed in , acceleration due to gravity) as a function of time in the first moments after an impact (the time is expressed in ). The dataset is challenging for quantile regression as the the values and the variability of the response vary dramatically with the independent variable.

We fit to these data the quantile regression curves corresponding to and . The prior settings are esentially the same as the ones already described in the simulation studies, except here we set and for the truncated Poisson prior. For the MCMC computation of the curves we started with an arbitrary set of initial values generated from the prior distributions. Again we used the first 500 iterations for adaptive tuning then we ran a burn-in of 500 iterations followed by 3,500 recorded iterations, where each iteration involves an update of 20 update steps for each update step.

We give in Figure 3 the quantile curves corresponding to linear splines . The results appear quite satisfactory as the quantile curves are not crossing each other, even in the region beyond 50 millisecond where the data are sparse. The changes in the variability of the acceleration over time has been captured well by the fitted conditional quantile curves, as they are very close to each other for the first few milliseconds then diverge after the crash.

4 Quantile regression for additive models

4.1 Introduction

When several potential predictors for the response variable are of interest, a standard procedure to avoid the so-called “curse of dimensionality” is to use an additive model ([Hastie and Tibshirani (1990]) where the response is modeled as a sum of functions of the predictors. In the context of quantile regression, if denotes the real-valued response variable and if now denotes a vector of predictors, the -th quantile of the conditional distribution of given is modeled as

| (11) |

See ?) for an inference on the additive quantile regression model by a kernel-weighted local linear fitting and see ?) for a Bayesian inference with either a MCMC algorithm or using INLA.

If we use spline functions to model the different curves it is still possible to use the linear model (5) with the difference that the design matrix is now made up of the columns of the individual design matrices corresponding to (6), with a single intercept term for identifiability. Thus inference on the additive quantile regression model can be performed via the same methodology and algorithm described in the previous sections. We consider below the study of a real dataset that involves additive quantile regression.

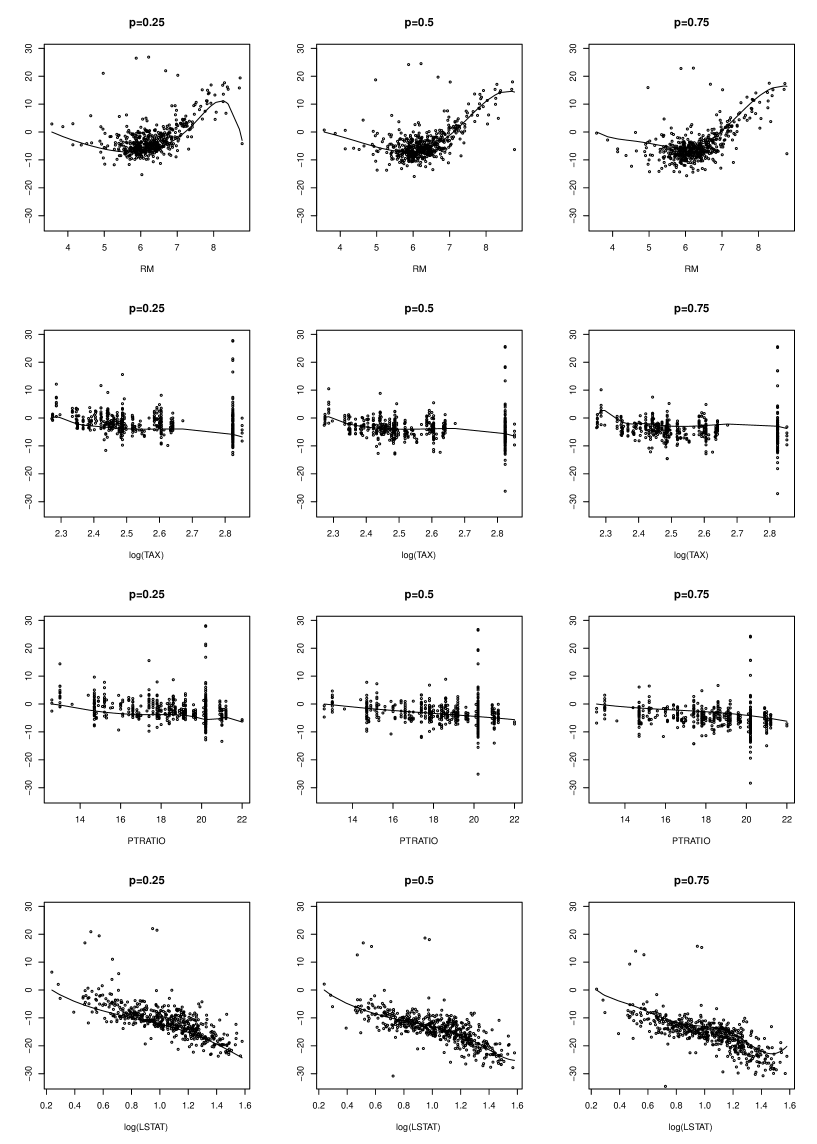

4.2 Analysis of the Boston housing dataset

We revisit the so-called Boston house price data available in the R package MASS.

This dataset has been originally studied in ?).

The full dataset consists of the median value of owner-occupied homes in 506 census tracts in the Boston Standard Metropolitan Statistical Area in 1970

along with 13 various sociodemographic variables.

This dataset has been analyzed in many statistical papers including ?), who used an additive model for mean regression,

and ?), who proposed an additive quantile regression model by a kernel-weighted local linear fitting. As in these two references we consider

the median values of the owner-occupied homes (in $1000s) as the dependent variable and four covariates given by

RM = average number of rooms per house in the area,

TAX = full property tax rate ($/$10,000),

PTRATIO = pupil/teacher ratio by town school distric,

LSTAT = the percentage of the population having lower economic status in the area.

As noticed in ?) these data are suitable for a quantile regression analysis since the response is a median price in a given area and the variables RM and LSTAT are highly skewed. More precisely we consider the additive model where the -th quantile of the conditional distribution of the response is given by

We fit to these data the -th quantile regression curves corresponding to cubic splines () at the quantile levels and . For the prior settings we took and for the truncated Poisson prior. For each predictor we set the intervals to be 10 equally sized partition sets over the range of the variable. Excluding the possibility of knots in the first and the last intervals, we get for each variable. For the MCMC computation of the curves we started with a random set of initial values generated from the prior distributions. We first ran the algorithm 500 iterations for adaptive tuning then we ran a burn-in of 500 iterations, followed by 4,000 recorded iterations, where each iteration involves an update of 20 update steps for each update step. We present in Figure 4 the different estimated curves. We plotted on the same graphs the datapoints corresponding to the original data minus the effect of all the other variables and the constant term. The fact that the values of TAX are not well dispersed over their range and the presence of a few outliers in the dataset did not seem to be a problem for our method.

Our results appear consistent with the results provided in the quoted previous analyses. Briefly, the variables RM and LSTAT appear as the most important covariates. If the contribution of LSTAT look similar for the three quantiles levels, the contribution of RM looks slightly more important for the upper quantile level . The variable TAX has a contribution relatively more important for the lower quantile level . Finally the Figure 4 suggests a linear contribution of the variable PTRATIO, especially for and for .

5 Noncrossing quantile regression curves

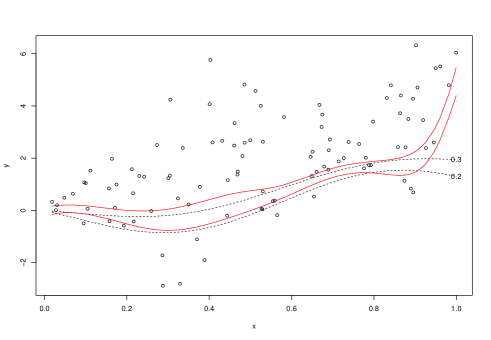

One known problem when using quantile regression for multiple percentiles is that the quantile curves that are estimated separately can cross, which is impossible. See for example the Figure 5 (a) where, partly due to the relatively small size of the dataset and the complex conditional distribution of the response variable, the two estimated quantile curves for and are crossing around the value .

The treatment of noncrossing quantile regression curves is difficult and several attempts to circumvent this problem have been proposed in different settings, see e.g. the references in ?) and in ?) or, for a more recent development in this area, see e.g. ?). In particular, ?) proposed a solution to this problem by considering a generalization of the criterion (1) to the case of simultaneous inference on several quantile curves. For clarity we suppose hereafter that we are interested in the fitting of two quantile curves corresponding to quantile levels and , with . ?) gave a solution to the minimization under the constraint of the expression

| (12) |

plus a penalty term corresponding to smoothing. An alternative approach described in ?) uses a so-called “substitution likelihood” that does not correspond to the distribution of the data given the unknown curves but yields a valid uncertainty. The substitution likelihood that they considered corresponds to the multinomial weights

| (13) |

where represents the number of datapoints below the curve , where represents the number of datapoints between the two curves and where is the number of datapoints above the curve . They gave conditions on the prior for the “pseudo-posterior” to be proper and proposed a MCMC algorithm for (pseudo-)posterior computation in the case of linear quantiles.

Here we propose a new method to postprocess the MCMC samples obtained from separate quantile regression curve fitting. We denote by the full set of unknown parameters for the -th quantile regression curve model (7). Let , , be the parameters corresponding to the quantile regression curve for the quantile levels and respectively, . We consider a new substitution likelihood of the form

| (14) |

where and denotes the two likelihood functions for quantile levels and given by the conditional distribution (7). The indicator function takes the value one if for all and zero otherwise, here the function is evaluated according to Equation (2) with parameters . It is not hard to see that the maximizer of this substitution likelihood is the maximizer of (12). Moreover, if we take independent priors and on the two sets of parameters, then the corresponding quasi-posterior is simply

| (15) | |||||

Given samples from the distribution an importance sampling argument can be used to reweight the samples according to this quasi-posterior.

In practice, MCMC samples obtained from separate posterior explorations of and of can be combined to form the new estimate of the the curve by

| (16) |

When the constraint above excludes too many samples this estimator will be unreliable, in this case more MCMC samples will be required. A computationally cheap way to obtain more samples is to consider all combinations of the two MCMC samples.

Figure 5 (b) shows the corrected curves from the estimator in (16), using all the possible combinations of the two MCMC samples, each of size 2,000. To evaluate the curves we use here the plug-in estimator (10) for . Finally the constraint on the curves is checked at every observed values of .

The strength of the above approach is that it is very easy to apply, and can be used on any posterior samples from separate quantile curves. An obvious draw back is that in some cases, when for example and are very close, the number of samples satisfying the constraint can be extremely low.

6 Conclusion

In this article, we have provided a procedure for Bayesian inference on quantile curve fitting. We focused on the use of regression splines with unknown number of knots and location to obtain smooth curves. We have seen that, within an auxiliary variable framework, a scale mixture of normals representation for the asymmetric Laplace distribution together with appropriate prior specifications makes it possible to integrate out the regression and the variance parameters analytically. This facilitates a simple Metropolis- Hastings within Gibbs sampler for simulation from the posterior distribution of interest. The proposed algorithm is fully automated with the inclusion of an automatic tuning step, which optimally tunes the Random-Walk Metropolis-Hastings scaling parameters. We have shown that our method performs well on several types of datasets. We have also shown that the proposed framework can be trivially extended to inference on additive models. Finally we have proposed and discussed a simple and general procedure that postprocesses MCMC samples to obtain noncrossing quantile regression curves.

References

- Bondell et al. (2010 Bondell, H. D., B. J. Reich, and H. Wang (2010). Noncrossing quantile regression curve estimation. Biometrika 97(4), 825–838.

- Chen and Yu (2009 Chen, C. and K. Yu (2009). Automatic Bayesian quantile regression curve fitting. Statistics and Computing 19, 271–281.

- Denison et al. (1998 Denison, D. G. T., B. K. Mallick, and A. F. M. Smith (1998). Automatic Bayesian curve fitting. Journal of Royal Statistical Society, Series B 60, 330 – 350.

- DiMatteo et al. (2001 DiMatteo, I., C. R. Genovese, and R. E. Kass (2001). Bayesian curve-fitting with free-knot splines. Biometrika 88(4), 1055–1071.

- Dunson and Taylor (2005 Dunson, D. B. and J. A. Taylor (2005). Approximate Bayesian inference for quantiles. J. Nonparametr. Stat. 17(3), 385–400.

- Fan et al. (2010 Fan, Y., J.-L. Dortet-Bernadet, and S. A. Sisson (2010). On Bayesian curve fitting via auxiliary variables. J. Comput. Graph. Statist. 19(3), 626–644.

- Fan and Sisson (2011 Fan, Y. and S. A. Sisson (2011). Handbook of Markov Chain Monte Carlo, Chapter Reversible Jump Markov chain Monte Carlo. Chapman and Hall/CRC Press.

- Garthwaite et al. (2010 Garthwaite, P. H., Y. Fan, and S. A. Sisson (2010). Adaptive optimal scaling of metropolis-hastings algorithms using the robbins-monro process. Technical report, University of New South Wales.

- George and McCulloch (1993 George, E. I. and R. E. McCulloch (1993). Variable selection via gibbs sampling. Journal of American Statistical Association 88, 881 – 889.

- Geraci and Bottai (2007 Geraci, M. and M. Bottai (2007). Quantile regression for longitudinal data using the asymmetric Laplace distribution. Biostatistics 8(1), 140–154.

- Green (1995 Green, P. J. (1995). Reversible jump MCMC computation and Bayesian model determination. Biometrika 82, 711–732.

- Harrison and Rubinfeld (1978 Harrison, D. J. and D. L. Rubinfeld (1978). Hedonic housing prices and the demand for clean air. Journal of Environmental Economics and Management 5(1), 81–102.

- Hastie and Tibshirani (1990 Hastie, T. J. and R. J. Tibshirani (1990). Generalised additive models. Chapman and Hall, London.

- He and Ng (1999 He, X. and P. Ng (1999). Cobs: Qualitatively constrained smoothing via linear programming. Computational Statistics 14(3), 315–337.

- Koenker (2005 Koenker, R. (2005). Quantile regression, Volume 38 of Econometric Society Monographs. Cambridge: Cambridge University Press.

- Koenker and Bassett (1978 Koenker, R. and J. Bassett, Gilbert (1978). Regression quantiles. Econometrica 46(1), 33–50.

- Koenker and Machado (1999 Koenker, R. and J. A. F. Machado (1999). Goodness of fit and related inference processes for quantile regression. Journal of the American Statistical Association 94(448), pp. 1296–1310.

- Koenker et al. (1994 Koenker, R., P. Ng, and S. Portnoy (1994). Quantile smoothing splines. Biometrika 81(4), 673–680.

- Kozumi and Kobayashi (2011 Kozumi, H. and G. Kobayashi (2011). Gibbs sampling methods for Bayesian quantile regression. Journal of Statistical Computation and Simulation 81(11), 1565–1578.

- Leslie et al. (2007 Leslie, D., R. Kohn, and D. Nott (2007). A general approach to heteroscedastic linear regression. Statistics and Computing 17, 131–146.

- Liang et al. (2008 Liang, F., R. Paulo, G. Molina, M. A. Clyde, and J. O. Berger (2008, March). Mixtures of g priors for Bayesian variable selection. Journal of the American Statistical Association 103, 410–423.

- Neal (2003 Neal, R. M. (2003). Slice sampling. Annals of Statistics 31(3), 705 – 767.

- Opsomer and Ruppert (1998 Opsomer, J. D. and D. Ruppert (1998). A fully automated bandwidth selection method for fitting additive models. Journal of the American Statistical Association 93(442), pp. 605–619.

- Reich et al. (2011 Reich, B. J., M. Fuentes, and D. B. Dunson (2011). Bayesian spatial quantile regression. Journal of the American Statistical Association 106(493), 6–20.

- Roberts and Rosenthal (2001 Roberts, G. O. and J. S. Rosenthal (2001). Optimal scaling for various Metropolis-Hastings algorithms. Statistical Science 16, 351–367.

- Rue et al. (2009 Rue, H., S. Martino, and N. Chopin (2009). Approximate Bayesian inference for latent gaussian models by using integrated nested laplace approximations. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 71(2), 319–392.

- Ruppert et al. (2003 Ruppert, D., M. P. Wand, and R. J. Carroll (2003). Semiparametric regression. Cambridge University Press.

- Silverman (1985 Silverman, B. W. (1985). Some aspects of the spline smoothing approach to non-parametric regression curve fitting. Journal of the Royal Statistical Society. Series B (Methodological) 47(1), pp. 1–52.

- Smith and Kohn (1996 Smith, M. and R. Kohn (1996). Nonparametric regression using Bayesian variable selection. Journal of Econometrics 75, 317–343.

- Thompson et al. (2010 Thompson, P., Y. Cai, R. Moyeed, D. Reeve, and J. Stander (2010). Bayesian nonparametric quantile regression using splines. Computational Statistics and Data Analysis 54(4), 1138 – 1150.

- Tsionas (2003 Tsionas, E. G. (2003). Bayesian quantile inference. J. Stat. Comput. Simul. 73(9), 659–674.

- Yu (2002 Yu, K. (2002). Quantile regression using RJMCMC algorithm. Comput. Statist. Data Anal. 40(2), 303–315.

- Yu and Lu (2004 Yu, K. and Z. Lu (2004). Local linear additive quantile regression. Scandinavian Journal of Statistics 31(3), pp. 333–346.

- Yu et al. (2003 Yu, K., Z. Lu, and J. Stander (2003). Quantile regression: applications and current research areas. The Statistician 52(3), 331–350.

- Yu and Moyeed (2001 Yu, K. and R. A. Moyeed (2001). Bayesian quantile regression. Statist. Probab. Lett. 54(4), 437–447.

- Yue and Rue (2011 Yue, Y. R. and H. Rue (2011). Bayesian inference for additive mixed quantile regression models. Computational Statistics and Data Analysis 55(1), 84 – 96.

- Zellner (1986 Zellner, A. (1986). On assessing prior distributions and Bayesian regression analysis with -prior distributions. In Bayesian inference and decision techniques, Volume 6 of Stud. Bayesian Econometrics Statist., pp. 233–243. Amsterdam: North-Holland.

Appendix A

The marginal posterior

Appendix B

Automatic tuning algorithm

Here we provide the algorithm to optimally search for the tuning parameters , and . The algorithm runs within the main MCMC algorithm given in Section 2.2. Tuning will only apply to the Update and Update steps. For the update of each of the parameters and do:

Initialisation:

For the iteration of the algorithm initialise the scaling parameter , where corresponds to and when updating the parameters , and respectively.

Set and initialise . The value of corresponds to the optimal acceptance probability for a univariate Random-Walk Metropolis-Hastings algorithm ([Roberts and

Rosenthal (2001]).

Tuning: Set ; update the parameters according to either Update or update , and obtain the corresponding acceptance probability as in Section 2.2.

update scaling: if set , else set

where and .

restart the algorithm: If , and either or , restart the algorithm, setting and . Note we do not restart the algorithm again if the total number of restarts exceeds 5.

Increment loop: Set . Go back to the beginning unless exceeds some prespecified number of iterations .

It is easy to monitor the changes in in order to determine the number of tuning iterations to achieve stability. In practice, we run the first iterations of the algorithm in Section 2.2 with automatic tuning, and then start the main part of MCMC as usual with the scaling parameters fixed at the value .