Optimal Investment Under Transaction Costs

Abstract

We investigate how and when to diversify capital over assets, i.e., the portfolio selection problem, from a signal processing perspective. To this end, we first construct portfolios that achieve the optimal expected growth in i.i.d. discrete-time two-asset markets under proportional transaction costs. We then extend our analysis to cover markets having more than two stocks. The market is modeled by a sequence of price relative vectors with arbitrary discrete distributions, which can also be used to approximate a wide class of continuous distributions. To achieve the optimal growth, we use threshold portfolios, where we introduce a recursive update to calculate the expected wealth. We then demonstrate that under the threshold rebalancing framework, the achievable set of portfolios elegantly form an irreducible Markov chain under mild technical conditions. We evaluate the corresponding stationary distribution of this Markov chain, which provides a natural and efficient method to calculate the cumulative expected wealth. Subsequently, the corresponding parameters are optimized yielding the growth optimal portfolio under proportional transaction costs in i.i.d. discrete-time two-asset markets. As a widely known financial problem, we next solve optimal portfolio selection in discrete-time markets constructed by sampling continuous-time Brownian markets. For the case that the underlying discrete distributions of the price relative vectors are unknown, we provide a maximum likelihood estimator that is also incorporated in the optimization framework in our simulations.

I Introduction

The problem of how and when an investor should diversify capital over various assets, whose future returns are yet to be realized, is extensively studied in various different fields from financial engineering [1, 2], signal processing [3, 4, 5, 6, 7], machine learning [8, 9] to information theory [10]. Naturally this is one of the most important financial applications due to the amount of money involved. However, the current financial crisis demonstrated that there is a significant room for improvement in this field by sound signal processing methods [6, 7], which is the main goal of this paper. In this paper, we investigate how and when to diversify capital over assets, i.e., the portfolio selection problem, from a signal processing perspective and provide portfolio selection strategies that maximize the expected cumulative wealth in discrete-time markets under proportional transaction costs.

In particular, we study an investment problem in markets that allow trading at discrete periods, where the discrete period is arbitrary, e.g., it can be seconds, minutes or days [11]. Furthermore the market levies transaction fees for both selling and buying an asset proportional to the volume of trading at each transaction, which accurately models a broad range of financial markets [11, 12]. In our discussions, we first consider markets with two assets, i.e., two-asset markets. We emphasize that the two-stock markets are extensively studied in financial literature and are shown to accurately model a wide range of financial applications [11] such as the well-known “Stock and Bond Market” [11]. We then extend our analysis to markets having more than two assets, i.e., -stock markets, where is arbitrary. Following the extensive literature [10, 13, 1, 2, 5, 11], the market is modeled by a sequence of price relative vectors, say , , where each entry of , i.e., , is the ratio of the closing price to the opening price of the th stock per investment period. Hence, each entry of quantifies the gain (or the loss) of that asset at each investment period. The sequence of price relative vectors is assumed to have an i.i.d. “discrete” distribution [1, 2, 5, 11], however, the discrete distributions on the vector of price relatives are arbitrary. In this sense, the corresponding discrete distributions can approximate a wide class of continuous distributions on the price relatives that satisfy certain regularity conditions by appropriately increasing the size of the discrete sample space. We first assume that we know the discrete distributions on the price relative vectors and then extend our analysis to cover when the underlying distributions are unknown. We emphasize that the i.i.d. assumption on the sequence of price relative vectors is shown to hold in most realistic markets [11, 14]. The detailed market model is provided in Section IV. At each investment period, the diversification of the capital over the assets is represented by a portfolio vector , where for each entry , , and is the ratio of the capital invested in the th asset at investment period . As an example if we invest using , we earn (or loose) at the investment period after is revealed. Given that we start with one dollars, after an investment period of days, we have the wealth growth . Under this general market model, we provide algorithms that maximize the expected growth over any period by using “threshold rebalanced portfolios” (TRP)s, which are shown to yield optimal growth in general i.i.d. discrete-time markets [14].

Under mild assumptions on the sequence of price relatives and without any transaction costs, Cover et. al [10] showed that the portfolio that achieves the maximal growth is a constant rebalanced portfolio (CRP) in i.i.d. discrete-time markets. A CRP is a portfolio investment strategy where the fraction of wealth invested in each stock is kept constant at each investment period. A problem extensively studied in this framework is to find sequential portfolios that asymptotically achieve the wealth of the best CRP tuned to the underlying sequence of price relatives. This amounts to finding a daily trading strategy that has the ability to perform as well as the best asset diversified, constantly rebalanced portfolio. Several sequential algorithms are introduced that achieve the performance of the best CRP either with different convergence rates or performance on historical data sets [8, 10, 9, 15]. Even under transaction costs, sequential algorithms are introduced that achieve the performance of the best CRP [12]. Nevertheless, we emphasize that keeping a CRP may require extensive trading due to possible rebalancing at each investment period deeming CRPs, or even the best CRP, ineffective in realistic markets even under mild transaction costs [13].

In continuous-time markets, however, it has been shown that under transaction costs, the optimal portfolios that achieve the maximal wealth are certain class of “no-trade zone” portfolios [16, 17, 18]. In simple terms, a no-trade zone portfolio has a compact closed set such that the rebalancing occurs if the current portfolio breaches this set, otherwise no rebalancing occurs. Clearly, such a no-trade zone portfolio may avoid hefty transaction costs since it can limit excessive rebalancing by defining appropriate no-trade zones. Analogous to continuous time markets, it has been shown in [14] that in two-asset i.i.d. markets under proportional transaction costs, compact no-trade zone portfolios are optimal such that they achieve the maximal growth under mild assumptions on the sequence of price relatives. In two-asset markets, the compact no trade zone is represented by thresholds, e.g., if at investment period , the portfolio is given by , where , then rebalancing occurs if , given the thresholds , , where . Similarly, the interval can be represented using a target portfolio and a region around it, i.e., , where such that and . Extension of TRPs to markets having more than two stocks is straightforward and explained in Section III-B.

However, how to construct the no-trade zone portfolio, i.e., selecting the thresholds that achieve the maximal growth, has not yet been solved except in elementary scenarios [14]. We emphasize that a sequential universal algorithm that asymptotically achieves the performance of the best TRP specifically tuned to the underlying sequence of price relatives is introduced in [19]. This algorithm leverages Bayesian type weighting from [10] inspired from universal source coding and requires no statistical assumptions on the sequence of price relatives. In similar lines, various different universal sequential algorithms are introduced that achieve the performance of the best algorithm in different competition classes in [20, 13, 21, 3, 4, 22]. However, we emphasize that the performance guarantees in [19] (and in [20, 13, 3, 4]) on the performance, although without any stochastic assumptions, is given for the worst case sequence and only optimal in the asymptotic. For any finite investment period, the corresponding order terms in the upper bounds may not be negligible in financial markets, although they may be neglected in source coding applications (where these algorithms are inspired from). We demonstrate that our algorithm readily outperforms these universal algorithms over historical data [10], where similar observations are reported in [23, 21].

Our main contributions are as follows. We first consider two-asset markets and recursively evaluate the expected achieved wealth of a threshold portfolio for any and over any investment period. We then extend this analysis to markets having more than two-stocks. We next demonstrate that under the threshold rebalancing framework, the achievable set of portfolios form an irreducible Markov chain under mild technical conditions. We evaluate the corresponding stationary distribution of this Markov chain, which provides a natural and efficient method to calculate the cumulative expected wealth. Subsequently, the corresponding parameters are optimized using a brute force approach yielding the growth optimal investment portfolio under proportional transaction costs in i.i.d. discrete-time two-asset markets. We note that for the case with the irreducible Markov chain, which covers practically all scenarios in the realistic markets, the optimization of the parameters is offline and carried out only once. However, for the case with recursive calculations, the algorithm has an exponential computational complexity in terms of the number of states. However, in our simulations, we observe that a reduced complexity form of the recursive algorithm that keeps only a constant number of states by appropriately pruning certain states provides nearly identical results with the “optimal” algorithm. Furthermore, as a well studied problem, we also solve optimal portfolio selection in discrete-time markets constructed by sampling continuous-time Brownian markets [11]. When the underlying discrete distributions of the price relative vectors are unknown, we provide a maximum likelihood estimator to estimate the corresponding distributions that is incorporated in the optimization framework in the Simulations section. For all these approaches, we also provide the corresponding complexity bounds.

The organization of the paper is as follows. In Section II, we briefly describe our discrete-time stock market model with discrete price relatives and symmetric proportional transaction costs. In Section III, we start to investigate TRPs, where we first introduce a recursive update in Section III-A for a market having two-stocks. Generalization of the iterative algorithm to the -asset market case is provided in Section III-B. We then show that the TRP framework can be analyzed using finite state Markov chains in Section III-C and Section III-D. The special Brownian market is analyzed in Section III-E. The maximum likelihood estimator is derived in Section IV. We simulate the performance of our algorithms in Section V and the paper concludes with certain remarks in Section VI.

II Problem Description

We consider discrete-time stock markets under transaction costs. We first consider a market with two stocks and then extend the analysis to markets having more than two stocks. We model the market using a sequence of price relative vectors . A vector of price relatives in a market with assets represents the change in the prices of the assets over investment period , i.e., for the th stock is the ratio of the closing to the opening price of the th stock over period . For a market having two assets, we have . We assume that the price relative sequences and are independent and identically distributed (i.i.d.) over with possibly different discrete sample spaces and , i.e., and , respectively [14]. For technical reasons, in our derivations, we assume that the sample space is for both and where is the cardinality of the set . The probability mass function (pmf) of is and the probability mass function of is . We define and for and the probability mass vectors and , respectively. Here, we first assume that the corresponding probability mass vectors and are known. We then extend our analysis where and are unknown and sequentially estimated using a maximum likelihood estimator in Section IV.

An allocation of wealth over two stocks is represented by the portfolio vector , where and represents the proportion of wealth invested in the first and second stocks, respectively, for each investment period . In two stock markets, the portfolio vector is completely characterized by the proportion of the total wealth invested in the first stock. For notational clarity, we use to represent throughout the paper.

We denote a threshold rebalancing portfolio with an initial and target portfolio and a threshold by TRP(,). At each market period , an investor rebalances the asset allocation only if the portfolio leaves the interval . When , the investor buys and sells stocks so that the asset allocation is rebalanced to the initial allocation, i.e., , and he/she has to pay transaction fees. We emphasize that the rebalancing can be made directly to the closest boundary instead of to as suggested in [14], however, we rebalance to for notational simplicity and our derivations hold for that case also. We model transaction cost paid when rebalancing the asset allocation by a fixed proportional cost [12, 14, 13]. For instance, if the investor buys or sells dollars of stocks, then he/she pays dollars of transaction fees. Although we assume a symmetric transaction cost ratio, all the results can be carried over to markets with asymmetric costs [13, 14]. Let denote the achieved wealth at investment period and assume, without loss of generality, that the initial wealth of the investor is 1 dollars. For example, if the portfolio does not leave the interval and the allocation of wealth is not rebalanced for investment periods, then the current proportion of wealth invested in the first stock is given by and achieved wealth is given by If the portfolio leaves the interval at period , i.e., , then the investor rebalances the asset distribution to the initial distribution and pays approximately dollars for transaction costs [12]. In the next section, we first evaluate the expected achieved wealth so that we can optimize and .

III Threshold Rebalanced Portfolios

In this section, we first investigate TRPs in discrete-time two-asset markets under proportional transaction costs. We initially calculate the expected achieved wealth at a given investment period by an iterative algorithm. Then, we present an upper bound on the complexity of the algorithm. We also calculate the expected achieved wealth of markets having more than two assets, i.e., -asset markets for an arbitrary . We then provide the necessary and sufficient conditions such that the achievable portfolios are finite such that the complexity of the algorithm does not grow at any period. We also show that the portfolio sequence converges to a stationary distribution and derive the expected achieved wealth. Based on the calculation of the expected achieved wealth, we optimize and using a brute-force search. Finally, with these derivations, we consider the well-known discrete-time two-asset Brownian market with proportional transaction costs and investigate the asymptotic expected achieved wealth.

III-A An Iterative Algorithm

In this section, we calculate the expected wealth growth of a TRP with an iterative algorithm and find an upper bound on the complexity of the algorithm. To accomplish this, we first define the set of achievable portfolios at each investment period since the iterative calculation of the expected achieved wealth is based on the achievable portfolio set. We next introduce the portfolio transition sets and the transition probabilities of achievable portfolios at successive investment periods in order to find the probability of each portfolio state iteratively and to calculate .

We define the set of achievable portfolios at each investment period as follows. Since the sample space of the price relative sequences and is finite, i.e., , the set of achievable portfolios at period can only have finitely many elements. We define the set of achievable portfolios at period as , where is the size of the set for . As illustrated in Fig. 1, for each achievable portfolio , there is a certain set of portfolios in that are connected to , by definition of . At a given investment period , the set of achievable portfolios is given by

We let, without loss of generality, for each . Note that in Fig. 1, the size of the set of achievable portfolios at each period may grow in the next period depending on the set of price relative vectors. We next define the transition probabilities as for and and the set of achievable portfolios that are connected to , i.e., the portfolio transition set, as for . Hence, the probability of each portfolio state is given by

| (1) |

for . Therefore, we can calculate the probability of achievable portfolios iteratively. Using these iterative equations, we next iteratively calculate the expected achieved wealth at each period as follows.

By definition of and using the law of total expectation [24], the expected achieved wealth at investment period can be written as

| (2) |

To get in (2) iteratively, we evaluate for each from for . To achieve this, we first find the transition probabilities (not the state probabilities) between the achievable portfolios.

We define the set of price relative vectors that connect to as where

for and . We consider the price relative vectors that connect to separately since, in this case, there are two cases depending on whether the portfolio leaves the interval or not. We define as , where is the set of price relative vectors that connect to such that the portfolio does not leave the interval at period , i.e.,

and is the set of price relative vectors that connect to such that the portfolio leaves the interval at period and is rebalanced to , i.e.,

Then, the transition probabilities are given by

| (3) |

for and so that we can calculate iteratively for each by (1). Since we have recursive equations for the state probabilities, we next perform the iterative calculation of the expected achieved wealth based on the achievable portfolio sets and the transition probabilities.

Given the recursive formulation for the state probabilities, we can

evaluate the term

for from

for

iteratively to calculate by

(2) as follows. To evaluate

, we need to

consider two cases separately based on the value of .

In the first case, we see that if the portfolio , where , then the portfolio does not leave the interval at period . Hence, no transaction cost is paid so that we can express as a summation of the conditional expectations for all by the law of total expectation [24] as

| (4) |

where (4) follows from Bayes’ theorem [24]. We note that given and , the price relative vector can take values from and so that (4) can be written as a summation of the conditional expectations for all [24] after replacing

| (5) |

Now, given that , and , we observe that and

| (6) |

and by using (6) in (5), we have

Therefore, we can write from as

| (7) |

for , where we use .

In the second case, if the portfolio , then there are two sets of price relative vectors that connect to , i.e., and . Depending on the value of the price vector, the portfolio may be rebalanced to . If , then the portfolio is not rebalanced and no transaction fee is paid. If , then the portfolio is rebalanced and transaction cost is paid. We can find from as a summation of the conditional expectations for all [24] as

| (8) |

We note that given and , the price relative vector can take values from or , and which yields in (8) that

If , then it follows that

| (9) |

If , then transaction cost is paid which results

| (10) |

Hence, we can write (8) after using (9) and (10) as

| (11) | |||

Thus, we can write from as

| (12) | |||

which yields the recursive expressions for iteratively for each with (7) and (12).

Hence, we can calculate for the case where the portfolio for by (7) and for the case where the portfolio by (12). Therefore, we can evaluate iteratively by (2). Since, we have the recursive formulation, we can optimize and by a brute force search as shown in the Simulations section. For this recursive evaluation, we have to find the set of achievable portfolios at each investment period to compute by (2). Hence, we next analyze the number of calculations required to evaluate the expected achieved wealth .

III-A1 Complexity Analysis of the Iterative Algorithm

We next investigate the number of achievable portfolios at a given market period to determine the complexity of the iterative algorithm. We show that the set of achievable portfolios at period is equivalent to the set of achievable portfolios when the portfolio does not leave the interval for investment periods. We first demonstrate that if the portfolio never leaves the interval for periods, then is given by , where with a sample space where . Then, we argue that the number of achievable portfolios at period , , is equal to the number of different values that the sum can take when the portfolio does not leave the interval for investment periods. We point out that since the price relative sequences and are elements of the same sample space with and by using this, we find an upper bound on the number of achievable portfolios.

Lemma III.1

The number of achievable portfolios at period , , is equal to the number of different values that the sum can take when the portfolio does not leave the interval for investment periods and is bounded by , i.e., .

Proof:

The proof is in the Appendix A. ∎

Remark III.1

Note that the complexity of calculating is bounded by since at each period , we calculate as a summation of terms, i.e., and .

In the next section, we extend the given iterative algorithm to calculate the expected achieved wealth in a market with -assets, where is an arbitrary number determined by the investor.

III-B Generalization of the Iterative Algorithm to the -asset Market Case

In this section, we generalize the iterative method introduced in Section III-A to a market with assets where . We model the market as a sequence of i.i.d. price relative vectors , where and the p.m.f. of is . For -asset case, the portfolio vector is given by , , , target portfolio vector is defined as and the threshold vector is given by . Along these lines, TRP rebalances the wealth allocation to only when . In this case, if the wealth allocation is not rebalanced for investment periods, then the proportion of wealth invested in the th asset becomes and achieved wealth is given by We define the set of achievable portfolios at period as

where . In accordance with the definitions given in two-asset market case, the definitions of the portfolio transition sets and the transition probabilities of achievable portfolios follows. Then similar to the iterative algorithm introduced in Section III-A, (7) and (12), we can evaluate for from for iteratively to calculate . Therefore for the -asset market case, by using

the expected achieved wealth can be evaluated iteratively.

In the next section, we show that the set of all achievable portfolios, , is finite under mild technical conditions.

III-C Finitely Many Achievable Portfolios

In this section, we investigate the cardinality of the set of achievable portfolios and demonstrate that is finite under certain conditions in the following theorem, Theorem III.1. This result is significant since when is finite, we can derive a recursive update with a constant complexity, i.e., the number of states does not grow, to calculate the expected achieved wealth at any investment period. We demonstrate that the portfolio sequence forms a Markov chain with a finite state space and converges to a stationary distribution. Then, we can investigate the limiting behavior of the expected achieved wealth using this update to optimize and . Before providing the main theorem, we first state a couple of lemmas that are used in the derivation of the main result of this section.

We first point out that in Lemma III.1, we showed that the number of achievable portfolios at period is equal to the number of different values that the sum can take when the portfolio does not leave the interval for investment periods. Then, we observed that the cardinality of the set is equal to the number of different values that the sum can take for any when the portfolio never leaves the interval . We next show that the portfolio does not leave the interval for periods if and only if the sum for , where and . Moreover, we also prove that the number of achievable portfolios is equal to the cardinality of the set where we define the set as

, . Note that is the set of positive elements of the set and any value that the sum can take is an element of . Hence, if we can demonstrate that the set is finite under certain conditions, then it yields the cardinality of the set since is finite if and only if is finite.

In the following lemma, we prove that the portfolio does not leave the interval for periods if and only if the sum for .

Lemma III.2

The portfolio does not leave the interval for investment periods if and only if the sum for .

Proof:

The proof is in the Appendix B. ∎

In the following lemma, we demonstrate that if the condition is satisfied for each , then for any element , there exists an -period market scenario where the portfolio does not leave the interval for investment periods and such that for some and . It follows that the set of different values that the sum can take for any when the portfolio never leaves the interval for investment periods is equivalent to the set . Hence, we show that the cardinality of the set of achievable portfolios is equal to the cardinality of the set . After this lemma, we present conditions under which the set is finite so that the set of achievable portfolios is also finite.

Lemma III.3

If for , then any element of can be written as a sum for some where and for .

Proof:

In Lemma III.1, we showed that for any investment period , the number of different portfolio values that can take is equal to the number of different values that the sum can take where for . Since this is true for any investment period , it follows that the number of all achievable portfolios is equal to the number of different values that the sum can take for any such that .

Here, we show that if , then there exists a sequence for some such that and for . Let . Then, it can be written as for some and , . We define for and construct a sequence for some such that and for each as follows. We choose such that , let and decrease by 1. We see that since . Next, we choose such that , let and increase by 1. Then, it follows that since . At any time , if

-

•

, we choose such that , let and increase by 1. Note that since , and . Now assume that there exists no such that , i.e., for . If we let where and for , then we get that where . We observe that for since , and .

-

•

, we choose such that , let and decrease by 1. Note that since , and . Assume that there exists no such that , i.e., for . If we let where and for , then we get that where . We see that for since , and .

Therefore, we can write for some where and for . ∎

Hence, we showed that if the condition is satisfied for each , then any element of the set can be written as a sum for some when the portfolio does not leave the interval for investment periods. It follows that the set of different values that the sum can take for any when the portfolio does not leave the interval for investment periods is equivalent to the set . Thus, the number of achievable portfolios is equal to the cardinality of the set . In the following theorem, we demonstrate that if for and the set has a minimum positive element, then is finite. Hence, the set of achievable portfolios is also finite under these conditions. Otherwise, we show that the set contains infinitely many elements so that the set of achievable portfolios is also infinite. Thus, we show that the set of achievable portfolios is finite if and only if the minimum positive element of the set exists.

Theorem III.1

If for and the set has a minimum positive element, i.e., if

exists, then the set of achievable portfolio is finite. If such a minimum positive element does not exist, then is countably infinite.

In Theorem III.1 we present a necessary and sufficient condition for the achievable portfolios to be finite. We emphasize that the required condition, i.e., for , is a necessary required technical condition which assures that the TRP thresholds are large enough to prohibit constant rebalancings at each investment period. In this sense, this condition does not limit the generality of the TRP framework.

By Theorem III.1, we establish the conditions for a unique stationary distribution of the achievable portfolios. With the existence of a unique stationary distribution, in the next section, we provide the asymptotic behavior of the expected wealth growth by presenting the growth rate.

Proof:

For any investment period , we showed in Lemma III.1 that the number of different portfolio values that can take is equal to the number of different values that the sum can take where the sum for . In the Lemma III.3, we showed that the set of different values that the sum can take where the sum for is equivalent to the set . We let be the set of values that the sum can take for any , i.e., . Now, assume that the minimum positive element exists. We next illustrate that the sum for any sequence can be written as for some , i.e., .

Assume that there exists a sequence such that the sum for any . If we divide the real line into intervals of length , then should lie in one of the intervals, i.e., there exists such that so that we can write where . By definition of , an integer multiple of any element of is also an element of so that since . Moreover, for any two elements of , their difference is also an element of so that since and . However, this contradicts to the fact that is the minimum positive element of since and . Hence, it follows that any element of can be written as for some . Note that there are finitely many elements in since any element can be written as for some and . Since , it follows that the set of achievable portfolios is finite.

To show that if does not exist then contains infinitely many elements, we assume that does not exist. Since every finite set of real numbers has a minimum, there are either countably infinitely many positive elements in the set or none. We know that there exists so that there are positive numbers in . Therefore, there are infinitely many elements in . Now assume that there exists that can be written as a sum for some where and . Then, by Lemma III.3, it follows that and since there exists no positive minimum element of , there exists such that so that . In this way, we can construct a decreasing sequence such that for each . Note that for any , is also element of by Lemma III.3 so that there are countably infinite elements in . Hence, it follows that has countably infinitely many elements. ∎

We showed that if for and the minimum positive element of the set exists, then the set of achievable portfolios, , is finite. If the minimum positive element of the set does not exist, then the set is countably infinite so that the number of achievable portfolios is also countably infinite. Hence, the set of achievable portfolios is finite if and only if the minimum positive element of the set exists. However, Theorem III.1 does not specify the exact number of achievable portfolios. In the following corollary, we demonstrate that the number of achievable portfolios is if the set of achievable portfolios is finite.

Corollary III.1

If for and exists, then the number of achievable portfolios is111Here, is the largest integer less than or equal to .

Proof:

Assume that exists and there exists such that can be written as a sum for some and such that for . Note that such a exists, e.g., where since . Then, by Lemma III.3, it follows that . Since is the minimum positive element of , it follows that and . Hence, by Lemma III.3, we get that can be written as a sum for some and where for . We note that is an element of the set of different values that the sum can take for any and for such that the portfolio does not leave the interval . We showed in Theorem III.1 that any element of can be written as for some so that the number of elements in is . Hence, it follows that there are exactly achievable portfolios since Lemma III.3 implies that the set is equivalent to the set of different values that the sum can take for any and for such that the sum for each and the cardinality of the latter set is equal to the number of achievable portfolios. ∎

In Theorem III.1, we introduce conditions on the cardinality of the set of all achievable portfolio states, , and showed that if for all and the minimum positive element of the set exists, then is finite. This result is significant when we analyze the asymptotic behavior of the expected achieved wealth, i.e., in the following, we demonstrate that when is finite, the portfolio sequence converges to a stationary distribution. Hence, we can determine the limiting behavior of the expected achieved wealth so that we can optimize and . To accomplish this, specifically, we first present a recursive update to evaluate . We then maximize over and with a brute-force search, i.e., we calculate for different pairs and find the one that yields the maximum.

III-D Finite State Markov Chain for Threshold Portfolios

If we assume that for all and exists, then the set of all achievable portfolios is finite. By Corollary 1, it follows that there are exactly achievable portfolios. We let and, without loss of generality, . We define the probability mass vector of the portfolio sequence as where . The portfolio sequence forms a homogeneous Markov chain with a finite state space since the transition probabilities between states are independent of period . We see that is irreducible since each state communicates with other states so that all states are null-persistent since is finite [24]. Then, it follows that there exists a unique stationary distribution vector , i.e., . To calculate , we first observe that the set of portfolios that are connected to , , and the set of price relative vectors that connect to , , are independent of investment period since the price relative sequences are i.i.d. for and . Hence, we write and for . We next note that the state transition probabilities are also independent of investment period and write for , and . Therefore, we can write as

| (13) |

where if . Now, by using the definition of and (13), we get for each , where is the state transition matrix, i.e., .

We next determine the limiting behavior of the expected achieved wealth to optimize and as follows. In Section III-A, we showed that can be calculated iteratively by (2), (7) and (12). If we define the vector where , then we can calculate as the sum of the entries of by (2), i.e., , where is the vector of ones. Hence, by definition of , we can write where the matrix is given by

| (14) | |||

where and we ignore rebalancing for presentation purposes. From (7) and (12), does not depend on period since there are finitely many portfolio states, i.e., is constant. If we take rebalancing into account, then only the first row of the matrix changes and the other rows remain the same where

is the set of price relative vectors that connect to without crossing the threshold boundaries and is the set of price relative vectors that connect to by crossing the threshold boundaries for . Note that we can find the matrix by using the set of achievable portfolios and the probability mass vectors and of the price relative sequences.

Here, we analyze as as follows. We assume that the matrix is diagonalizable with the eigenvalues and, without loss of generality, , which is the case for a wide range of transaction costs [24]. Then, there exists a nonsingular matrix such that where is the diagonal matrix with entries . We observe that the matrix has nonnegative entries. Therefore, it follows from Perron-Frobenius Theorem [25] that the matrix has a unique largest eigenvalue and any other eigenvalue is strictly smaller than in absolute value, i.e., for . Then, the recursion on yields , and after some algebra, the expected achieved wealth is given by

where and . Then, it follows that

since for . Hence, we can optimize and as

To maximize , we evaluate it for different values of pairs and find the pair that maximizes , i.e., by a brute-force search in the Simulations section.

In the next section, we investigate the well-studied two-asset Brownian market model with transaction costs.

III-E Two Stock Brownian Markets

In this section, we consider the well-known two-asset Brownian market, where stock price signals are generated from a standard Brownian motion [14, 16, 17]. Portfolio selection problem in continuous time two-asset Brownian markets with proportional transaction costs was investigated in [17], where the growth optimal investment strategy is shown to be a threshold portfolio. Here, as usually done in the financial literature [16], we first convert the continuous time Brownian market by sampling to a discrete-time market [14]. Then, we calculate the expected achieved wealth and optimize and to find the best portfolio rebalancing strategy for a discrete-time Brownian market with transaction costs. Note that although, the growth optimal investment in discrete-time two-asset Brownian markets with proportional transaction costs was investigated in [14], the expected achieved wealth and the optimal threshold interval has not been calculated yet.

To model the Brownian two-asset market, we use the price relative vector with and where is constant and is a random variable with . This price relative vector is obtained by sampling the stock price processes of the continuous time two-asset Brownian market [14, 17]. We emphasize that this sampling results a discrete-time market identical to the binomial model popular in asset pricing [14]. We first present the set of achievable portfolios and the transition probabilities between portfolio states.

Since the price of the first stock is the same over investment periods, the portfolio leaves the interval if either the money in the second stock grows over a certain limit or falls below a certain limit. If the portfolio does not leave the interval for investment periods, then the money in the first stock is dollars and the money in the second stock is for some so that the portfolio is . Note that if and only if , where 222Here, is the largest integer greater or equal to the . and . Hence, the set of achievable portfolios is given by

where and and . We see that the portfolio is rebalanced to only if it is in the state and or if it is in the state and . Therefore, the transition probabilities are given by

where is the probability that the portfolio given that for any period . We now calculate using the recursions in Section III-D as follows. The sets of price relative vectors that connect portfolio states are given by

Hence, we can calculate the matrix defined in (14) as

where we ignore rebalancing. If we take rebalancing into account, then and Then, by the recursions in Section III-D, is given by . Moreover, we maximize where is the largest eigenvalue of the matrix . Here, we optimize and with a brute-force search, i.e., we find for different pairs and find the one that achieves the maximum.

IV Maximum Likelihood Estimators of The Probability Mass Vectors

In this section, we sequentially estimate the probability mass vectors and corresponding to and , respectively, using a maximum likelihood estimator (MLE). In general, these vectors may not be known or change in time, hence, could be estimated at each investment period prior to calculation of . The maximum likelihood estimator for a pmf on a finite set is well-known [24], but we provide the corresponding derivations here for completeness. We consider, without loss of generality, the price relative sequence and assume that its realizations are given by for and estimate . Similar derivations follow for the price relative sequence and . Note that as demonstrated in the Simulations section, the corresponding estimation can be carried out over a finite length window to emphasize the most recent data. We define the realization vector and the probability mass function as for and the parameter vector . Then, the MLE of the probability mass vector is given by . Since the price relative sequence is i.i.d., it follows that since is the indicator function. If we change the order of the product operators, then we obtain where , i.e., the number of realizations that are equal to for . Note that . Hence, we can write since is a monotone increasing function. If we define the vector , where for , then we see that for and . Since and are probability vectors, i.e., their entries are nonnegative and sum to one, it follows that and if and only if , i.e., their relative entropy is nonnegative [26]. Therefore, we get that where the equality is reached if and only if . Hence, it follows that so that we estimate the probability mass vector with at each investment period where is the proportion of realizations up to period that are equal to for .

V Simulations

In this section, we demonstrate the performance of TRPs with several different examples. We first analyze the performance of TRPs in a discrete-time two-asset Brownian market introduced in Section III-E. As the next example, we apply TRPs to historical data from [27, 13] collected from the New York Stock Exchange over a 22-year period and compare the results to those obtained from other investment strategies [13, 27, 19, 20]. We show that the performance of the TRP algorithm is significantly better than the portfolio investment strategies from [13, 27, 19, 20] in historical data sets as expected from Section III.

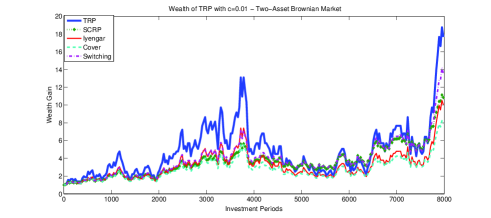

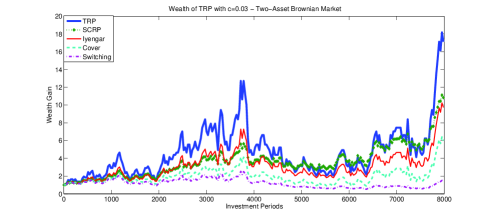

As the first scenario, we apply TRPs to a discrete-time two-asset Brownian market. Under this well studied market in the financial literature [11], the price relative vector is given by , where , and with equal probabilities and we set [14]. Here, the sample spaces of the price relative sequences and are and , respectively, and , where , , . Hence, the probability mass vectors of the price relative sequences and are given by and , respectively. Based on this data, we evaluate the growth rate for different pairs to find the best TRP that maximizes the growth rate using the approach introduced in Section III-E, i.e., we form the matrix and evaluate the corresponding maximum eigenvalues to find the pair that achieves the largest maximum eigenvalue since this pair also maximizes the growth rate. Then, we invest 1 dollars in a randomly generated two-asset Brownian market using: the TRP, labeled as, “TRP”, i.e., TRP(,) with calculated pair, the SCRP algorithm with the target portfolio vector , labeled as “SCRP”, as suggested in [13], the Iyengar’s algorithm, labeled as “Iyengar”, the Cover’s algorithm, labeled as “Cover”, and the switching portfolio, labeled as “Switching”, with parameters suggested in [20]. In Fig. 2, we plot the wealth achieved by each algorithm for transaction costs and , where is the proportion paid when rebalancing, i.e, is a commission. As expected from the derivations in Section III, we observe that, in both cases, the performance of the TRP algorithm is significantly better than the other algorithms under transaction costs.

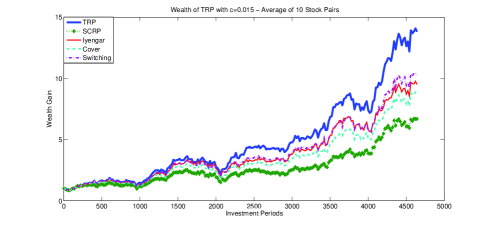

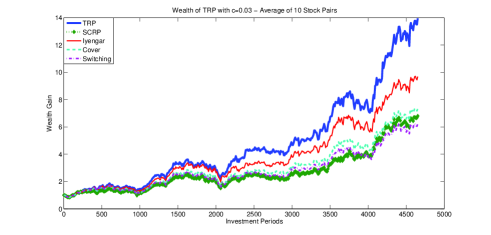

We next present results that illustrate the average performance of TRPs on a number of stock pairs from the historical data sets [27] to avoid any bias to particular stock pairs. In this set of simulations, we first randomly select pairs of stocks from the historical data that includes 34 stocks (where the Kin Ark stock is excluded). The data includes the price relative sequences of 34 stock pairs for 5651 investment periods (days). Since the brute force algorithm introduced in Section III-A requires the sample spaces of the price relative sequences, for each randomly selected stock pair, we proceed as follows. We first calculate the sample spaces and the probability mass vectors of the price relative sequences from the first 1000-day realizations of and , where the sample spaces are simply constructed by quantizing the observed realizations into bins. We observed that the performance of the TRP is not effected by the number of bins provided that there are an adequate number of bins to approximate the continuous valued price relatives. Then, we optimize and using the MLE introduced in Section IV and the brute force algorithm from Section III, and invest using this TRP for the next 1000 periods, i.e., from period 1001 to period 2000. We then update pair using the first -day realizations of the price relative vectors and invest using the best TRP for the next 1000 periods. We repeat this process through all available data. Hence, we invest on each stock pairs using TRP for 4651 periods where we update pair at each 1000 periods. In Fig. 3a and Fig. 3b, we present the average performances of the TRP algorithm, the SCRP algorithm, the Cover’s algorithm, the Iyengar’s algorithm and the switching portfolio, under a mild transaction cost and a hefty transaction cost , respectively. In Fig. 3, we present the wealth gain for each algorithm, where the results are averaged over randomly selected 10 independent stock pairs. We observe that although the performance of the algorithms other than the TRP degrade with increasing transaction cost, the performance of the TRP, using the MLE, is not significantly effected since it can avoid excessive rebalancings. We further observe from these simulations that the average performance of the TRP is better than the average performance of the other portfolio investment strategies commonly used in the literature.

VI Conclusion

We studied growth optimal investment in i.i.d. discrete-time markets under proportional transaction costs. Under this market model, we studied threshold portfolios that are shown to yield the optimal growth. We first introduced a recursive update to calculate the expected growth for a two-asset market and then extend our results to markets having more than two assets. We next demonstrated that under the threshold rebalancing framework, the achievable set of portfolios form an irreducible Markov chain under mild technical conditions. We evaluated the corresponding stationary distribution of this Markov chain, which provides a natural and efficient method to calculate the cumulative expected wealth. Subsequently, the corresponding parameters are optimized using a brute force approach yielding the growth optimal investment portfolio under proportional transaction costs in i.i.d. discrete-time two-asset markets. We also solved the optimal portfolio selection in discrete-time markets constructed by sampling continuous-time Brownian markets. For the case that the underlying discrete distributions of the price relative vectors are unknown, we provide a maximum likelihood estimator. We observed in our simulations, which include simulations using the historical data sets from [27], that the introduced TRP algorithm significantly improves the achieved wealth under both mild and hefty transaction costs as predicted from our derivations.

A) Proof of Lemma III.1: We analyze the cardinality of the set of achievable portfolios at period , , as follows. If we assume that an investor invests with a TRP(,) for investment periods and the sequence of price relative vectors are given by and the portfolio sequence is given by , then we see that the portfolio could leave the interval at any period depending on the realizations of the price relative vector. We define an -period market scenario as a sequence of portfolios . We can find the number of achievable portfolios at period as the number of different values that the last element of -period market scenarios can take. Here, we partition the set of -period market scenarios according to the last time the portfolio leaves the interval and show that any achievable portfolio at period can be achieved by an -period market scenario where the portfolio does no leave the interval for periods as follows. If we define the set as the set of -period market scenarios, i.e.,

where is the set of -period market scenarios where the portfolio leaves the interval last time at period , , and is the set of -period market scenarios where the portfolio does not leave the interval for investment periods. We point out that ’s are disjoint, i.e., for and their union gives the set of all -period market scenarios, i.e., so that they form a partition for . We see that the set of achievable portfolios at period is the set of last elements of -period market scenarios, i.e., . We next show that the last element of any -period market scenario from for is also a last element of an -period market scenario from . Therefore, we demonstrate that any element of the set is achievable by a market scenario from and .

Assume that for some so that , i.e., the portfolio is rebalanced to last time at period . Note that can also be achieved by an -period market scenario where the portfolio never leaves the interval , for and for so that . Hence, it follows that the set of achievable portfolios at period is the set of achievable portfolios by -period market scenarios from . We next find the number of different values that can take where the portfolio does not leave the interval for investment periods.

When the portfolio never leaves the interval for investment periods, is given by

. If we write the reciprocal of as

then we observe that the number of different values that the portfolio can take is the same as the number of different values that the sum can take. Since the price relative sequences and are elements of the same sample space with , it follows that . Since the number of different values that the sum can take is equal to and , it follows that the number of achievable portfolios at period is bounded by , i.e., and the proof follows.

B) Proof of Lemma III.2:If the portfolio does not leave the interval for investment periods, then for and it is not adjusted to at these periods so that

for each . Taking the reciprocal of , we get that

Noting that and taking the logarithm of each side, it follows that

i.e., for . Now, if the portfolio leaves the interval first time at period for some , then we get that or

so that we get

or

i.e., .

References

- [1] Harry Markowitz, “Portfolio selection,” The Journal of Finance, vol. 7, no. 1, pp. 77–91, March 1952.

- [2] Harry Markowitz, “Foundations of portfolio theory,” The Journal of Finance, vol. 46, no. 2, pp. 469–477, June 1991.

- [3] A. J. Bean and A. C. Singer, “Factor graphs for universal portfolios,” in 2009 Conference Record of the Forty-Third Asilomar Conference on Signals, Systems and Computers, 2009, pp. 1375 – 1379.

- [4] A. J. Bean and A. C. Singer, “Factor graph switching portfolios under transaction costs,” in IEEE International Conference on Acoustics Speech and Signal Processing, 2011, pp. 5748–5751.

- [5] Mustafa U. Torun, Ali N. Akansu, and Marco Avellaneda, “Portfolio risk in multiple frequencies,” IEEE Signal Processing Magazine, vol. 28, no. 5, pp. 61–71, September 2011.

- [6] IEEE Signal Processing Magazine, “Special issue on signal processing for financial applications,” December 2011.

- [7] IEEE Journal of Selected Topics in Signal Processing, “Special issue on signal processing methods in finance and electronic trading,” March 2012.

- [8] D. P. Helmbold, R. E. Schapire, Y. Singer, and M. K. Warmuth, “On-line portfolio selection using multiplicative updates,” Mathematical Finance, vol. 8, pp. 325–347, 1998.

- [9] V. Vovk and C. Watkins, “Universal portfolio selection,” in Proceedings of the COLT, 1998, pp. 12–23.

- [10] T. Cover and E. Ordentlich, “Universal portfolios with side-information,” IEEE Transactions on Information Theory, vol. 42, no. 2, pp. 348–363, 1996.

- [11] D. Luenberger, Investment Science, Oxford University Press, 1998.

- [12] A. Blum and A. Kalai, “Universal portfolios with and without transaction costs,” Machine Learning, pp. 309–313, 1997.

- [13] S. S Kozat and A. C. Singer, “Universal semiconstant rebalanced portfolios,” Mathematical Finance, vol. 21, no. 2, pp. 293–311, 2011.

- [14] G. Iyengar, “Discrete time growth optimal investment with costs,” http://www.ieor.columbia.edu/gi10/Papers/stochastic.pdf.

- [15] A. Kalai and S. Vempala, “Efficient algorithms for universal portfolios,” in IEEE Symposium on Foundations of Computer Science, 2000, pp. 486–491.

- [16] M. H. A. Davis and A. R. Norman, “Portfolio selection with transaction costs,” Mathematics of Operations Research, vol. 15, no. 4, pp. 676–713, 1990.

- [17] M.I. Taksar, M. J. Klass, and D. Assaf, “Diffusion model for optimal portfolio selection in the presence of brokerage fees,” Mathematics of Operations Research, vol. 13, no. 2, pp. 277– 294, 1988.

- [18] M. W. Brandt, P. Santa-Clara, and R. I. Valkanov, “Parametric portfolio policies: Exploiting characteristics in the cross section of equity returns,” EFA 2005 Moscow Meetings Paper, 2005.

- [19] G. N. Iyengar, “Universal investment in market with transaction costs,” Mathematical Finance, vol. 15, no. 2, pp. 359 371, 2005.

- [20] S. S. Kozat and A. C. Singer, “Switching strategies for sequential decision problems with multiplicative loss with application to portfolios,” IEEE Transactions on Signal Processing, vol. 57, pp. 2192–2208, 2009.

- [21] S. S. Kozat, A. C. Singer, and A. J. Bean, “A tree-weighting approach to sequential decision problems with multiplicative loss,” Signal Processing, vol. 92, no. 4, pp. 890–905, 2011.

- [22] S. S. Kozat and A. C. Singer, “Universal switching portfolios under transaction costs,” in IEEE International Conference on Acoustics, Speech and Signal Processing, 2008, pp. 5404 – 5407.

- [23] A. Borodin, R. El-Yaniv, and V. Govan, “Can we learn to beat the best stock,” Journal of Artificial Intelligence Research, vol. 21, pp. 579–594, 2004.

- [24] H. Stark and J. W. Woods, Probability And Random Processes With Applications To Signal Processing, Prentice-Hall, 2001.

- [25] C. D. Meyer, Matrix Analysis and Applied Linear Algebra, SIAM, 2001.

- [26] T. Cover and J. A. Thomas, Elements of Information Theory, Wiley Series, 1991.

- [27] T. Cover, “Universal portfolios,” Mathematical Finance, vol. 1, no. 1, pp. 1–29, 1991.