Bayesian logistic betting strategy against probability forecasting

Abstract

We propose a betting strategy based on Bayesian logistic regression modeling for the probability forecasting game in the framework of game-theoretic probability by Shafer and Vovk [16]. We prove some results concerning the strong law of large numbers in the probability forecasting game with side information based on our strategy. We also apply our strategy for assessing the quality of probability forecasting by the Japan Meteorological Agency. We find that our strategy beats the agency by exploiting its tendency of avoiding clear-cut forecasts.

Keywords and phrases: exponential family, game-theoretic probability, Japan Meteorological Agency, probability of precipitation, strong law of large numbers.

1 Introduction

In this paper we consider assessing quality of probability forecasting for binary outcomes. A primary example of probability forecasting is the probability of precipitation announced by weather forecasting agencies. The binary outcomes are either “rain” (more precisely, precipitation above certain amount during a specified period at a particular location) or “no rain”. In the United States the National Weather Service started to announce probability of precipitation in 1965 (cf. [6]), whereas the Japan Meteorological Agency started probability forecasting in 1980 for Tokyo area and extended it to the whole Japan in 1986111http://www.jma.go.jp/jma/kishou/intro/gyomu/index2.html (in Japanese). How can we assess the quality of probability forecasting? We propose to assess probability forecasting by setting up a hypothetical betting game against forecasting agencies in the framework of game-theoretic probability by Shafer and Vovk [16].

We can regard the capital process of a betting strategy as a test statistic of a statistical hypothesis ([15], [17]). Our null hypothesis is that given the probability announced by the agency, the outcome is indistinguishable from the Bernoulli trial with success probability . If this hypothesis is true, then the capital process becomes a non-negative martingale and the capital process converges to a finite value almost surely. However if the announced probability is not good, then a clever strategy may be able to beat the forecasting agency in the betting game. In our game we construct a betting strategy based on Bayesian logistic regression modeling, which is a very standard statistical model for analyzing binary responses. We will prove some results on the strong law of large numbers in probability forecasting game with side information based on our betting strategy. We also see that our strategy works well against probability of precipitation announced by the Japan Meteorological Agency.

Organization of this paper is as follows. In Section 2 we formulate the probability forecasting game with side information and derive some basic properties of betting strategies. It also serves as a brief introduction to game-theoretic probability theory. In Section 3 we introduce our betting strategy based on logistic regression model. In Section 4 we prove some properties of our logistic betting strategy in the framework of game-theoretic probability. In Section 5 we give numerical studies of our strategy. In particular we apply our strategy to the data on probability of precipitation announced by the Japan Meteorological Agency. We end the paper with some discussions in Section 6.

2 Formulation of the probability forecasting game and summary of preliminary results

In this section we formulate the probability forecasting game and extend it to include side information. We mostly follow the results in [10].

At the beginning of day (or at the end of day ) an agency (we call it “Forecaster”) announces a probability of certain event in day , such as precipitation in day . Let be the indicator variable for the event, i.e., if the event occurs and otherwise. We suppose that a player “Reality” decides the binary outcome . When Forecaster announces , it also sells a ticket with the price of per ticket. The ticket pays one monetary unit when the event occurs in day , i.e., the value of the ticket at the end of day is . A bettor or gambler, called “Skeptic”, buys tickets with the price of per ticket. Then the payoff to Skeptic in day is . We allow to be negative, so that Skeptic can bet also on the non-occurrence of the event. If the probability announced by the agency is appropriate, it is hard for Skeptic to make money in this game. On the other hand, if the probability is biased in some way, Skeptic may be able to increase his capital denoted by . Hence we can measure the quality of probability forecasting in terms of .

We now give a protocol of the game, following the notational convention of [16].

Binary Probability Forecasting (BPF)

Protocol:

Skeptic announces his initial capital .

FOR :

Forecaster announces .

Skeptic announces .

Reality announces .

.

Collateral Duty: Skeptic must keep non-negative.

Forecaster is supposed to decide its forecast based on all relevant side information available at the time of announcement. We modify the above protocol so that Forecaster also discloses the relevant side information , which is a -dimensional column vector, together with the probability . Furthermore we define auxiliary capital processes and .

Binary Probability Forecasting With Side Information (BPFSI)

Protocol:

.

FOR :

Forecaster announces and .

Skeptic announces .

Reality announces .

.

.

.

Collateral Duty: Skeptic must keep non-negative.

In the protocol, denotes the transpose of , is a scalar, is a -dimensional column vector and is a symmetric matrix.

If and , then . When we study the usual strong law of large numbers in game-theoretic probability, we are interested in the convergence as . Generalizing this case, in the presence of side information, we are interested in the convergence , although the order of may be different from . We call this convergence the usual form of the strong law of large numbers in BPFSI. See Theorem 4.1 in Section 4.1. However, as we prove in Theorem 4.2 of Section 4.2, under mild regularity conditions, we can prove a stronger result

where is close to such as , .

Let

denote the fraction of the capital Skeptic bets on day . Then the capital process is written as

| (1) |

Now suppose that Skeptic himself models Reality’s move as a Bernoulli variable with the success probability . If Skeptic totally trusts Forecaster, then he sets . However if Skeptic does not totally trust Forecaster he may formulate differently from . Furthermore suppose that Skeptic uses the “Kelly criterion” ([12], [9]) to determine so as to maximize the expected value of the logarithm of the capital growth under :

Writing

and differentiating this with respect to , the unique maximizer is obtained as

| (2) |

With this choice of we have

Hence (1) is written as

In the case that Skeptic models the joint probability of Reality’s moves, is given as the conditional probability

In this case

and is written as

| (3) |

For the rest of this section we introduce some terminology of game-theoretic probability. An infinite sequence of Forecaster’s moves and Reality’s moves

is called a path. The set of all paths is called the sample space. A subset is an event. A strategy of Skeptic determines based on a partial path :

denotes the capital process when Skeptic adopts the strategy . We say that Skeptic can weakly force an event by a strategy if is never negative and

For two events , is denoted as , where is the complement of . We say that by a strategy Skeptic can weakly force a conditional event if is never negative and

is interpreted as a set of regularity conditions for the event to hold.

Let and denote the maximum and the minimum eigenvalues of . In this paper we consider the following regularity conditions:

-

i)

.

-

ii)

.

-

iii)

is a bounded set.

Namely we take as

| (4) |

The condition i) makes the meaning of “” precise. The condition ii) means that stays away from being singular. For ii) is trivial and not needed.

3 Logistic betting strategy

In this section we introduce a betting strategy based on logistic modeling of Reality’s moves.

As in the previous section Skeptic models as a Bernoulli variable with the success probability . Furthermore we specify that Skeptic uses the following logistic regression model for the logarithm of the odds ratio:

| (5) |

where is a parameter vector.

In previous studies in game-theoretic probability, many strategies of Skeptic depend only on , , and do not depend on . However obviously it is more reasonable to consider Skeptic’s strategies which depend on . Strategies explicitly depending on are also important from the viewpoint of defensive forecasting ([20], [18]). We again discuss this point in Section 4.3.

We now consider the capital process of (5) for a fixed . Solving for we have

| (6) |

Then

and the capital process is written as

| (7) |

Naturally it is better for Skeptic to choose the value of depending on the moves of other players. In this paper we consider a Bayesian strategy, which specifies a prior distribution for . Bayesian strategies for Binary Probability Forecasting with constant was considered in [10]. Bayesian strategy is basically the same as the universal portfolio by Cover and his coworkers ([3], [4], [5]). In the universal portfolio, a prior is put on the betting ratio itself, where as we put a prior on the parameter of Skeptic’s model. Furthermore differently from [4] we allow continuous side information.

In the Bayesian logistic strategy with the prior density function of , the capital process is written as

is of the form (3) where

In this paper we consider a prior density which is positive in a neighborhood of the origin. We call such “a prior supporting a neighborhood of the origin”.

4 Properties of logistic betting strategy from the viewpoint of game-theoretic probability

In this section we prove game-theoretic properties of our Bayesian logistic strategy.

4.1 Weak forcing of the usual form of the strong law of large numbers

The first theoretical result on our logistic betting strategy is the following theorem.

Theorem 4.1.

In BPFSI, by a Bayesian logistic strategy with a prior supporting a neighborhood of the origin, Skeptic can weakly force

where is given in (4).

The rest of this subsection is devoted to a proof of this theorem. The basic logic of our proof is the same as in Section 3.2 of [16].

We first consider the logarithm of in (7) for a fixed :

For notational simplicity we write

We investigate the behavior of for close the origin. Fix with unit length (i.e. ) and consider , . Note that . We will choose appropriately later in (11).

The derivative of with respect to is written as follows.

| (8) |

Note that and have the same sign and hence each summand in the second term on the right-hand side of (8) is non-negative.

Let

be a function of depending on the parameter . Note . Its derivative is computed as

| (9) |

Hence

where for negative we interpret as . Now in (9) is monotone in with and . Hence

Then for between and we have

| (10) |

Using the upper bound and integrating we obtain

Let . Then

and integrating this for we have (for any and )

For the rest of our proof we arbitrary choose and fix a path , where is given in (4). Various constants (’s, ’s etc.) below may depend on . By iii) there exists such that for all . Also there exist and such that for all . Now suppose that for this . Then for some and for infinitely many we have . Let be a subsequence such that for . The normalized vectors

have an accumulation point , , and hence along a further subsequence we have

By Cauchy-Schwarz, for three vectors , we have

Then we can choose such that for all sufficiently large and for all , , sufficiently close to , we have

We now choose small enough such that

| (11) |

Then

Note that the convergence is uniform for in some neighborhood of . Since our prior puts a positive weight to , along . This completes our proof of Theorem 4.1.

4.2 Weak forcing of a more precise form of the strong law of large numbers

As discussed in Section 2, we can establish a much more precise rate of convergence of the strong law of large numbers based on our Bayesian logistic strategy. Our main theorem of this paper is stated as follows.

Theorem 4.2.

In BPFSI, by a Bayesian logistic strategy with a prior distribution supporting a neighborhood of the origin, Skeptic can weakly force

where is given in (4).

We give a proof of this theorem in the following three subsections.

4.2.1 Bounding the maximum likelihood estimate

We now consider the behavior of in (7), when is maximized with respect to . Let

We call the maximum likelihood estimate, since is of the form of the likelihood function of the logistic regression model. It is easily seen that the maximizer is finite except for a special case that the vectors in lie on a half-space defined by a hyperplane containing the origin. More specifically in Lemma 4.3 we prove that is small when is small.

The maximizing can only be computed at the end of day after seeing all the data . Hence we call a strategy using a “hindsight strategy”, which is the same as the best constant rebalanced portfolio (BCRP) in the terminology of the universal portfolio.

We prove the following lemma.

Lemma 4.3.

Let and , where we assume . Then

For any fixed , there exist , such that and for all sufficiently large . Also in Theorem 4.1 we proved that Skeptic can weakly force . From these results we have the following proposition.

Proposition 4.4.

In the same setting as in Theorem 4.1 Skeptic can weakly force .

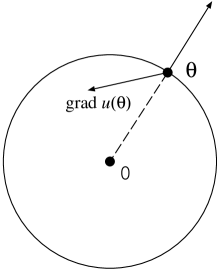

The rest of this subsection is devoted to a proof of Lemma 4.3. Consider the inner product of and the gradient of . If , then the gradient points toward the interior of the ball with radius as shown in Figure 1. If for all with , then .

This can be seen as follows. Suppose . Let be the maximizer of on the sphere (the boundary of the ball). Then at the gradient of is a positive multiple of and this contradicts .

4.2.2 Behavior of the hindsight strategy

We summarize properties of in view of the standard theory of exponential families ([2]) in statistical inference. Define

Note that is the cumulant generating function (potential function) for the logistic regression model, which is an exponential family model with the natural parameter . Hence each and are convex in . Indeed by (9), the Hessian matrix of is given as

which is non-negative definite. The Hessian matrix

of is positive definite if is positive definite, which is the Fisher information matrix in terms of the natural parameter .

Convexity of implies concavity of , where

Hence if the maximum of is attained at a finite value , then the “maximum likelihood estimate” satisfies “the likelihood equation”

or equivalently

| (12) |

The likelihood equation can also be written as

From this it follows that if and only if .

Regard (12) as determining in terms of , i.e., . This is the inverse map of . Differentiating again with respect to we obtain the Jacobi matrix

as the Hessian matrix of . Hence the Jacobi matrix is written as

| (13) |

Now is the Legendre transformation (cf. Chapter 3 of [1]) of :

Differentiating with respect to , by (12) we obtain

| (14) |

By (13) the Hessian matrix of is given by .

We are now ready to prove the following proposition.

Proposition 4.5.

Proof.

As in Proposition 4.5 we have the following corollary.

Corollary 4.6.

In the same setting as in Theorem 4.1 Skeptic can weakly force

4.2.3 Laplace method for evaluating the difference of the hindsight strategy and the logistic strategy

In the last subsection we clarified the behavior of the capital process for the hindsight strategy. Now we employ the standard Laplace method to evaluate the difference of the hindsight strategy and the logistic strategy (Section 5 of [3], Chapter 3.1 of [8]).

Lemma 4.7.

Let be a prior density supporting a neighborhood of the origin and let denote its capital process. For such that ,

| (15) |

Proof.

For close to the origin, expanding around we have

where is on the line segment joining and . Hence

Now by the standard Laplace method we obtain (15). ∎

Finally we give a proof of Theorem 4.2.

4.3 Monotonicity with respect to the forecast probability

Here we consider the case that itself is an element of the vector of the side information and hence is multiplied by a coefficient in (5). For notational convenience we here eliminate from and write (5) as

| (16) |

where denotes the effect of side information other than . Intuitively represents how much trust Skeptic puts in Forecaster. If then Skeptic entirely ignores Forecaster’s and if then Skeptic takes for granted. The value of corresponds to partial trust in . It is somewhat surprising to see that in the case of probability of precipitation announced by the Japan Meteorological Agency in Section 5.2.

We now investigate how in (2) behaves with respect to for given . This is an important question from the viewpoint of defensive forecasting ([20], [18]), because in defensive forecasting we want to obtain for which . For notational simplicity we now omit the subscript and write (6) as

Then

Differentiating this with respect to we obtain

The numerator of can be written as

which is non-positive for . Hence we have the following proposition.

Proposition 4.8.

Under the logistic regression model (16), for the betting ratio is monotone decreasing in .

It is natural that is monotone decreasing in , because if is too high and Skeptic does not believe it, then Skeptic will bet on the non-occurrence .

For the special case of ,

which is bounded and monotone in . For , is unbounded and it can be easily seen that

We can interpret the first limit as follows. Suppose that , i.e. the price of a ticket is 1/1000 of a dollar. In this case Skeptic can buy tickets with one dollar and has the chance of winning dollars. Hence Skeptic may want to buy tickets. Thus it is reasonable that and are inversely proportional when is small.

5 Experiments

In this section we give some numerical studies of our strategy. In Section 5.1 we present some simulation results and in Section 5.2 we apply our strategy against probability forecasting by the Japan Meteorological Agency.

5.1 Some simulation studies

We consider three cases and apply three strategies to these examples. In our simulation studies Reality chooses her moves probabilistically, either by Bernoulli trials or by a Markov chain model.

-

•

Case 1: is a Bernoulli variable with the success probability 0.7 and alternates between and (i.e. and ).

-

•

Case 2: is a Bernoulli variable with the success probability 0.5 and alternates between and .

-

•

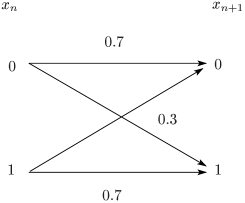

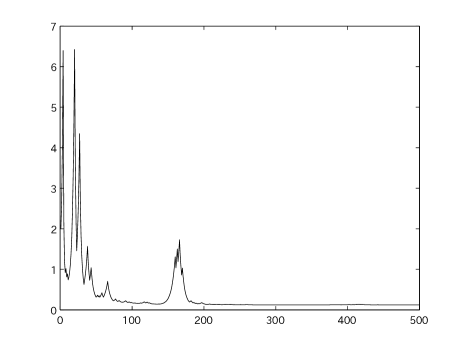

Case 3: and is generated by a Markov chain model with transition probabilities shown in Figure 2.

-

•

Strategy 1: is a scalar and in (5). Assume that the prior density for is given as uniform distribution for [0,1]. The capital process is written as

-

•

Strategy 2: and . Assume independent priors for and , which are uniform distributions over [0,1]. The capital process is written as

-

•

Strategy 3: and . Assume independent priors for , and , which are uniform distributions over [0,1]. The capital process is written as

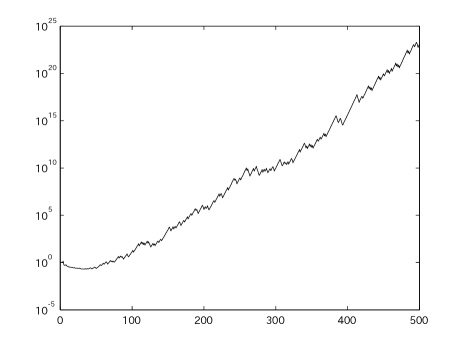

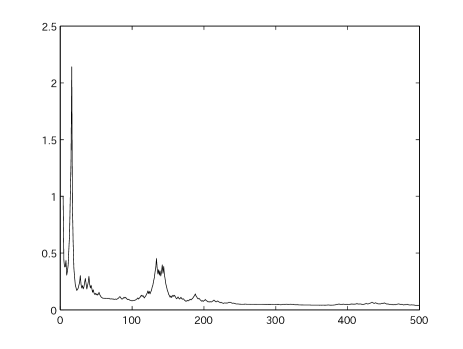

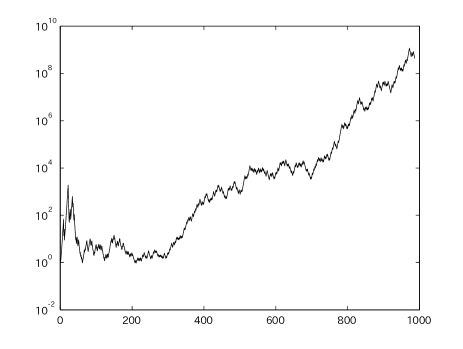

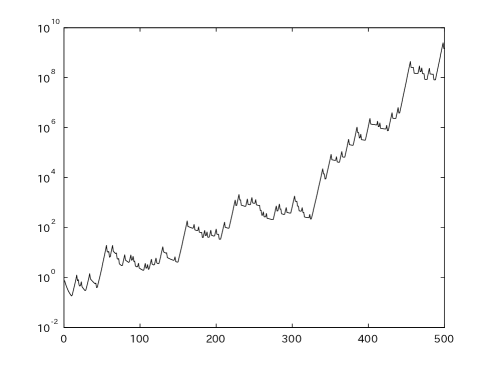

As shown in Figure 4 and Figure 4, we can beat Reality by strategy 1 only in case 1. So we improve our strategy and apply strategy 2 to case 2. We can see from Figure 6 and Figure 6 that strategy 2 can work well in case 2 but still not effective in case 3. Finally, we use strategy 3 in case 3 and observe that it shows a good result for Skeptic in Figure 7.

From these simulations, we see that Skeptic can beat Reality with more flexible strategy utilizing more side information.

5.2 Betting against probability of precipitation by the Japan Meteorological Agency

Now we apply our strategy to probability of precipitation provided by the Japan Meteorological Agency. We collected the forecast probabilities for the Tokyo area from archives of the morning edition of the Mainichi Daily News and the actual weather data on 9:00 and 15:00 of each day for Tokyo area from http://www.weather-eye.com/ for the period of three years from January 1, 2009 to December 31, 2011. We counted a day as rainy if the data on this site records rain on 9:00 or on 15:00 of that day in Tokyo area.

The forecast probability is only announced as multiples of 10% (i.e. ) by JMA. The data are summarized in Table 1. represents the probability of precipitation on day and indicates the actual precipitation. Actual ratio is calculated from the ratio of the number of rainy days to all days for a given value of .

| (%) | Actual Ratio(%) | ||

|---|---|---|---|

| 0 | 1 | 61 | 1.6 |

| 10 | 10 | 324 | 3.0 |

| 20 | 24 | 193 | 11.1 |

| 30 | 36 | 117 | 23.5 |

| 40 | 20 | 26 | 43.5 |

| 50 | 67 | 56 | 54.5 |

| 60 | 38 | 14 | 73.1 |

| 70 | 36 | 7 | 85.7 |

| 80 | 36 | 4 | 90.0 |

| 90 | 22 | 1 | 95.6 |

| 100 | 3 | 0 | 100 |

The distinct feature of the prediction by JMA is that that tends to be closer to 50% than the actual ratio. For example, when JMA announces , the actual ratio is only . Similarly when JMA announces , the actual ratio is . Hence JMA has the tendency of avoiding clear-cut forecasts.

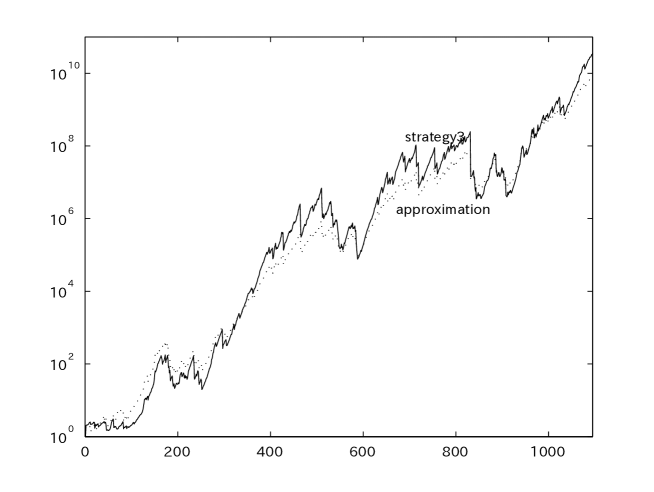

In the hindsight strategy, the value of , which is a coefficient for in strategy 3 is close to 1.5. Hence we modified strategy 3 of the previous section, so that the prior for is uniform between 0 and 2. We also substituted and for and , respectively, because our strategy is not defined for or . Figure 8 shows the behavior of strategy 3 and the approximation . We see that our strategy works very well against JMA by exploiting its tendency of avoiding clear-cut forecasts. It is also of interest that the capital process shows a seasonal fluctuation and it does not perform well for the rainy season (June and July) in Tokyo area.

6 Summary and discussion

In this paper we proposed a Bayesian logistic betting strategy in the binary probability forecasting game with side information (BPFSI). We proved some theoretical results and showed good performance of our strategy against probability forecasting by Japanese Meteorological Agency.

Here we discuss some topics for further investigation.

We considered implications of a single Bayesian logistic betting strategy in BPFSI. We can also take a look at the sequential optimizing strategy (SOS) of [11] in BPFSI. Under the condition , Bayesian strategy and SOS should behave in the same way. However we could not succeed to prove weak forcing of by SOS alone.

For the case of we could employ approaches of [14] to prove results similar to Theorem 4.2. In [14] we also discussed Reality’s strategies. It is of interest to study strategies of Forecaster or Reality in the binary probability forecasting game with side information. Defensive forecasting ([20], [18]) can be considered as a strategy of Forecaster.

We extended the binary probability forecasting game by including side information. In our formulation side information is announced by Forecaster and in our logistic betting strategy is used as regressors in a logistic regression. However Skeptic can use any transformation of in his strategy. In this sense, it might be more natural to formulate the game, where is announced by Skeptic. Binary probability forecasting game is often considered from the viewpoint of prequential probability ([7]) and leads to the notion of randomness of the sequence ([19], [13]). From the viewpoint of prequential probability it might also be natural to consider side information as a part of moves by Skeptic for testing the randomness of .

We assumed multidimensional . However from the viewpoint of game-theoretic probability, we do not lose much generality by restricting to be a scalar, since if Skeptic can weakly force events then he can weakly force . By the same reasoning we can also consider , because if Skeptic can weakly force then he can weakly force . Interpretation and formulation of side information in game-theoretic probability needs further investigation.

References

- [1] V. I. Arnol′d. Mathematical Methods of Classical Mechanics, volume 60 of Graduate Texts in Mathematics. Springer-Verlag, New York, second edition, 1989. Translated from the Russian by K. Vogtmann and A. Weinstein.

- [2] O. Barndorff-Nielsen. Information and Exponential Families. John Wiley & Sons Inc., New York, 1978. Wiley Series in Probability and Mathematical Statistics.

- [3] T. M. Cover. Universal portfolios. Math. Finance, 1(1):1–29, 1991.

- [4] T. M. Cover and E. Ordentlich. Universal portfolios with side information. IEEE Trans. Inform. Theory, 42(2):348–363, 1996.

- [5] T. M. Cover and J. A. Thomas. Elements of Information Theory. Wiley, Hoboken, NJ, second edition, 2006.

- [6] A. P. Dawid. Probability forecasting. In Encyclopedia of Statistical Sciences, volume 7, pages 210–218. Wiley, New York, 1986.

- [7] A. P. Dawid and V. G. Vovk. Prequential probability: principles and properties. Bernoulli, 5(1):125–162, 1999.

- [8] J. L. Jensen. Saddlepoint Approximations. Oxford University Press, Oxford, 1995.

- [9] J. L. Kelly, Jr. A new interpretation of information rate. Bell. System Tech. J., 35:917–926, 1956.

- [10] M. Kumon, A. Takemura, and K. Takeuchi. Capital process and optimality properties of a Bayesian skeptic in coin-tossing games. Stoch. Anal. Appl., 26(6):1161–1180, 2008.

- [11] M. Kumon, A. Takemura, and K. Takeuchi. Sequential optimizing strategy in multi-dimensional bounded forecasting games. Stochastic Process. Appl., 121:155–183, 2011.

- [12] L. C. MacLean, E. O. Thorp, and W. T. Ziemba. The Kelly Capital Growth Investment Criterion: Theory and Practice. World Scientific handbook in financial economic series. World Scientific, 2011.

- [13] K. Miyabe. An optimal superfarthingale and its convergence over a computable topological space, 2011. To appear in Proceedings of Solomonoff 85th Memorial Conference at Melbourne, Australia.

- [14] K. Miyabe and A. Takemura. Convergence of random series and the rate of convergence of the strong law of large numbers in game-theoretic probability. Stochastic Process. Appl., 122(1):1–30, 2012.

- [15] G. Shafer, A. Shen, N. Vereshchagin, and V. Vovk. Test martingales, Bayes factors and -values. Statist. Sci., 26(1):84–101, 2011.

- [16] G. Shafer and V. Vovk. Probability and Finance: It’s Only a Game! Wiley, 2001.

- [17] K. Takeuchi, A. Takemura, and M. Kumon. New procedures for testing whether stock price processes are martingales. Computational Economics, 37(1):67–88, 2010.

- [18] V. Vovk, I. Nouretdinov, A. Takemura, and G. Shafer. Defensive forecasting for linear protocols. In H. S.Jain and E.Tomita, editors, Proceedings of the 16th international conference on algorithmic learning theory, number 3734 in LNAI, pages 459–473, 2005.

- [19] V. Vovk and A. Shen. Prequential randomness and probability. Theoret. Comput. Sci., 411(29-30):2632–2646, 2010.

- [20] V. Vovk, A. Takemura, and G. Shafer. Defensive Forecasting. In R.G.Cowell and Z.Ghahramani, editors, Proceedings of the tenth international workshop on artificial intelligence and statistics, pages 365–372, 2005.