Super-exponential bubbles in lab experiments: evidence for anchoring over-optimistic expectations on price

Abstract

We analyze a controlled price formation experiment in the laboratory that shows evidence for bubbles. We calibrate two models that demonstrate with high statistical significance that these laboratory bubbles have a tendency to grow faster than exponential due to positive feedback. We show that the positive feedback operates by traders continuously upgrading their over-optimistic expectations of future returns based on past prices rather than on realized returns.

Keywords: rational expectations; financial bubbles; speculation; anchoring; laboratory experiments; behavioral model; super-exponential growth; positive feedback; behavioral expectations

JEL: C92; D84; G12

Highlights:

-

•

We offer an interpretation of lab experiments that exhibit financial bubbles.

-

•

We show that bubbles in controlled experiments can grow faster than exponential.

-

•

We find traders anchor expectations more on price than on returns in these bubbles.

1 Introduction

Bubbles, defined as significant persistent deviations from fundamental value, express one of the most paradoxical behaviors of real financial markets. Here, we analyze the dynamics of bubbles in a laboratory market (Hommes et al. (2008)) and focus on the regimes of strong deviations from the known fundamental values, which we refer to as the bubble regimes. Because this data is from a controlled environment, we can exclude exogenous influences such as news or private information. We show that a model with exponential growth, corresponding to a constant rate of returns, cannot account for the observed transient explosive price increases. Models that incorporate positive feedback leading to faster-than-exponential growth are found to better describe the data.

Research on financial bubbles has a rich literature (see e.g. Kaizoji and Sornette (2010) for a recent review) aiming at explaining the origin of bubbles, their persistence and other properties. The theoretical literature has classified different type of bubbles. For instance, Blanchard (1979) and Blanchard and Watson (1982) introduced rational expectation (RE) bubbles, i.e., bubbles that appear in the presence of rational investors who are willing to earn the large returns offered during the duration of the bubble as a remuneration for the risk that the bubble ends in a crash. Tirole (1982) argued that heterogeneous beliefs among traders is necessary for bubbles to develop. de Long et al. (1990) demonstrated that introducing noise traders in a universe of rational speculators can amplify the size and duration of bubbles. Brock and Hommes (1998) showed that endogenous switching between heterogeneous expectations rules, driven by their recent relative performance, generates bubble and crash dynamics of asset prices. Abreu and Brunnermeier (2003) explained the persistence of bubbles by the heterogeneous diagnostics of rational agents concerning the start time of the bubble, which leads to a lack of synchronization of their shorting of the underlying asset, and therefore prevents them from stopping the bubble to blossom. Lux and Sornette (2002) showed that the multiplicative stochastic process proposed by Blanchard and Watson (1982), together with the no-arbitrage condition, predicts a tail exponent of the distribution of returns smaller than , which is incompatible with empirical observations. Johansen et al. (1999) and Johansen et al. (2000) thus extended the Blanchard-Watson (1982) model of RE bubbles by proposing models for the crash hazard rate that exhibit critical bifurcation points reflecting the imitation and herding behavior of the noise traders. Gallegati et al. (2011) presented a model of bubbles and crashes, where crashes occur after a period of financial distress. Hommes (2006) reviewed behavioral models of bubbles with fundamentalists trading against chartists.

Jarrow et al. (2007), Jarrow et al. (2010) and Jarrow et al. (2011) developed local martingale models of bubbles within the arbitrage-free martingale pricing technology that underlies option pricing theory, based on the assumption that bubbles come together with (or are defined by) a volatility growing faster than linearly with the underlying price. But Andersen and Sornette (2004), among others, have shown that some (and perhaps most) bubbles are not associated with an increase in volatility. In particular,Bates (1991) documented that the famous worldwide October 1987 crash occurred at a minimum of the implied volatility, at least in the US. Gürkaynak (2008) surveyed econometric tests of asset price bubbles and showed that the econometric detection of asset price bubbles cannot be achieved with a satisfactory degree of certainty: for each paper that finds evidence of bubbles, there is another one that fits the data equally well without allowing for a bubble.

The present paper represents the first detailed quantitative calibration of simple models with positive feedback that unambiguously demonstrates the existence of positive feedback mechanisms and super-exponential bubbles in the price formation process. It thus provides support within controlled laboratory set-ups for the empirical evidence presented by Sornette et al. on historical financial bubbles (see Jiang et al. (2010) and Kaizoji and Sornette (2010)111An extended version is available at http://arxiv.org/abs/0812.2449 and references therein for an overview).

2 Material and methods

In the experiment of Hommes et al. (2008), participants (“traders”) were asked to forecast the price of a single asset in every turn. The price of the asset evolves with the equation,

| (1) |

where the market price at time is given as an average of the traders discounted price expectations; is the interest rate, is the estimate of trader for the price for period based on information up to time and is the dividend. Hence, today’s price is simply the average of the current value of the traders’ expectations for tomorrow . Note that the traders have to make a two period forecast; for their forecast , only the prices up to time are available.

Traders are given the parameters above (but not the price forming Equation 1 itself) and are rewarded according to their prediction accuracy222The reward is proportional to the quadratic scoring rule . The fundamental/equilibrium price (which traders could calculate) is 333. In our analysis, we focus on the realized price and not on the traders’ individual estimates .

Notwithstanding the existence of a clearly defined market price formula, this experiment is remarkable in reporting realized prices that are quite loosely tied to the fundamental value, because traders are rewarded more by correctly foreseeing the other traders’ forecasts than by correctly calculating the fundamental price . Moreover, traders are allowed to estimate the asset value in a large price range between and (where the upper bound is more than the fundamental value ).

3 Theory/calculation

3.1 Rational Bubble

Hommes et al. (2008) discussed the rational bubble

| (2) |

where is a positive constant. This process fulfills the “self-confirming” nature of rational expectations if the assumed interest rate equals the interest rate from Equation 1 and equals the fundamental value of 444For a rational bubble, we have . . In fact, Hommes et al. (2008) found that traders do use an interest rate significantly larger than in four of the six groups and hence their expectations are no longer rational (see section 4). Furthermore, the growth rate is not constant, but is increasing as we will see later.

Todd and Gigerenzer (2000) argued that “decision-making agents in the real world must arrive at their inferences using realistic amounts of time, information, and computational resources. [..] The most important aspects of an agent’s environment are often created by the other agents it interacts with.” Moreover, Tversky and Kahneman (1974) presented three heuristics that are employed in making judgments under uncertainty. For our purposes, the heuristic that is relevant to interpret the groups’ behaviors is the “adjustment from an anchor, which is usually employed in numerical prediction when a relevant value is available. These heuristics are highly economical and usually effective, but they lead to systematic and predictable errors.” (Emphasis is ours).

In the rest of this section, we are presenting two models in which traders anchor their forecasts on (1) price or (2) return. Both models have in common that they can generate price growth that is significantly faster than exponential (as observed in the data) and generalize the rational bubble of Equation 2.

3.2 Anchoring on Price

Generalizing the constant growth generated by Equation 2, we specify a model which allows faster or slower than exponential growth. The growth rate can be explained by the excess price (which is the difference between the observed price and the fundamental price ) plus a constant:

| (3) |

and would imply faster than exponential growth i.e. the growth rate grows itself. For , we recover the exponential growth (equivalent to the rational bubble Equation 2 with ). We will see below that is typically significantly larger than zero, indicating faster than exponential growth and positive feedback on the price.

One justification for the functional form (Equation 3) is that anchoring on price is commonly used in technical trading. One of many patterns used are support and resistance levels which is nothing else but anchoring on price. Although in violation with the efficient markets hypothesis, Lo et al. (2000) studied technical trading rules and found “practical value” for such technical rules.

3.3 Anchoring on Return

Alternatively, we check if the growth rate can be explained by the excess log-return following the following process

| (4) |

The conditions that and implies again faster than exponential growth of the excess price and positive feedback from past returns. This model can be interpreted as a second order iteration or adaptive form of the exponential growth.

4 Results

In this section, we estimate the parameters of the two processes and check for the statistical significance of and that express a positive feedback of price (Equation 3) or of return (Equation 4) onto future returns. In particular, we are interested in the lower 95% confidence interval for the null hypothesis that and are zero, to check for significant deviations that can confirm or not that price growth is indeed significantly faster than exponential (which is the situation corresponding to and greater than zero). As the two models can be run over a multitude of different start and end points, we present the results in graphical form instead of tables to provide better insight.

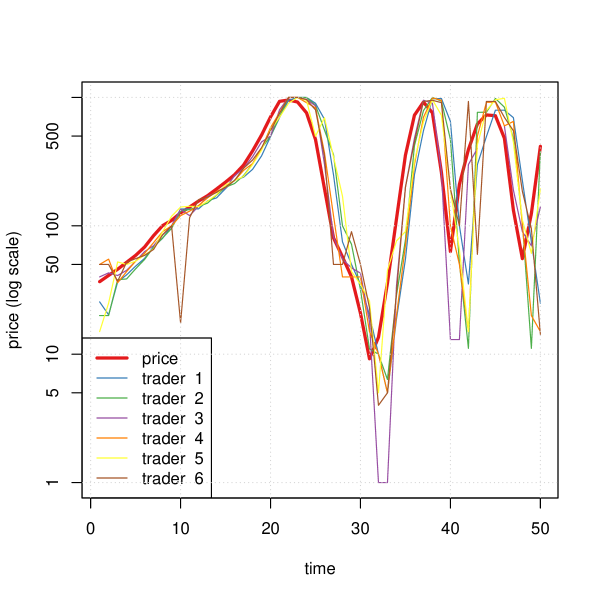

Hommes et al. (2008) identified bubbles in five out of the six groups. Group one shows a somehow erratic price trajectory and no bubbles. Groups five and six show some tendency towards bubbles, but the time horizon is too short for our analysis to get significant results. Moreover, Hommes et al. (2008) found that the bubble in group five is compatible with the hypothesis of a rational bubble (Equation 2). Hence, we focus on group number two, three and four.

| Group | Time window | Description | Classification |

|---|---|---|---|

| 1 | NA | erratic price trajectory | — |

| 2 | 7 – 26 | speculative bubble | anchoring on price |

| 3 | 7 – 29 | speculative bubble | anchoring on price |

| 4 | 7 – 21 | speculative bubble | anchoring on price |

| 5 | 29 – 37 | rational bubble | — |

| 6 | 23 – 29 | speculative bubble | (too short for analysis) |

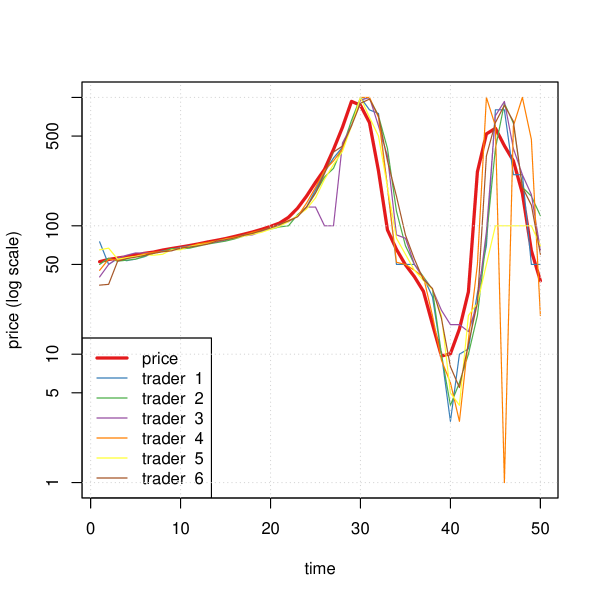

4.1 Group 2

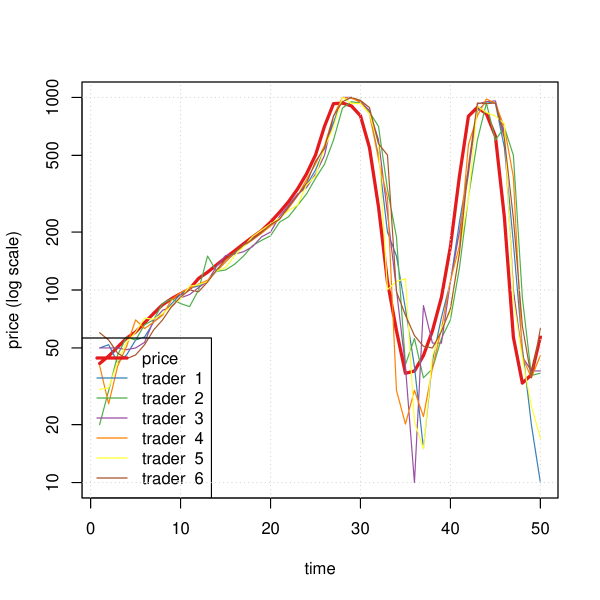

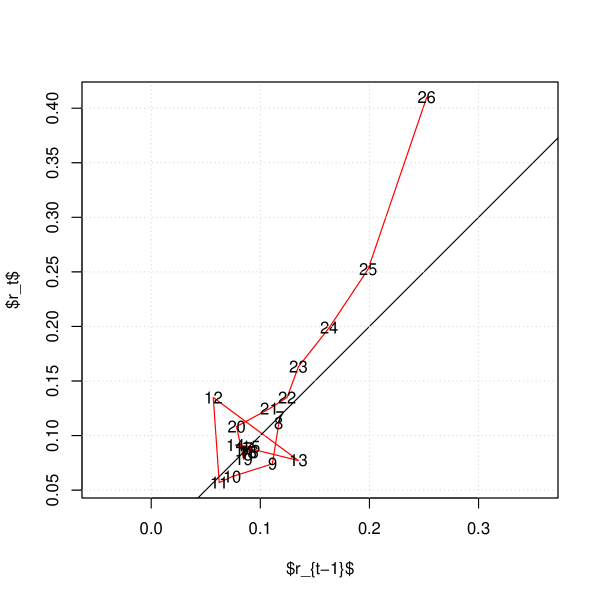

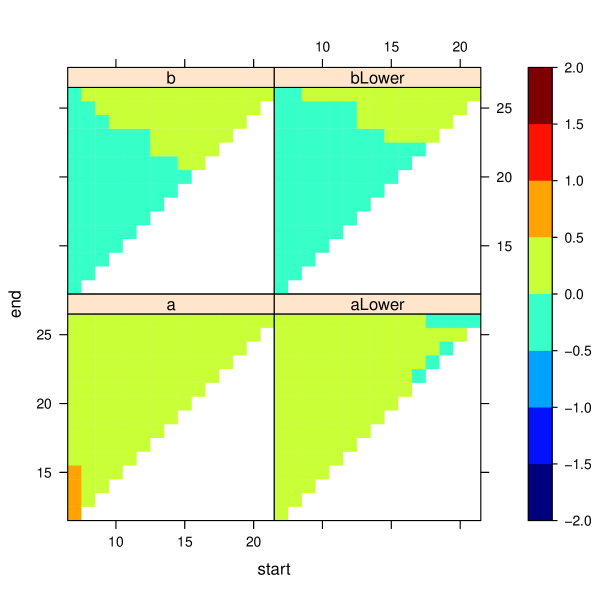

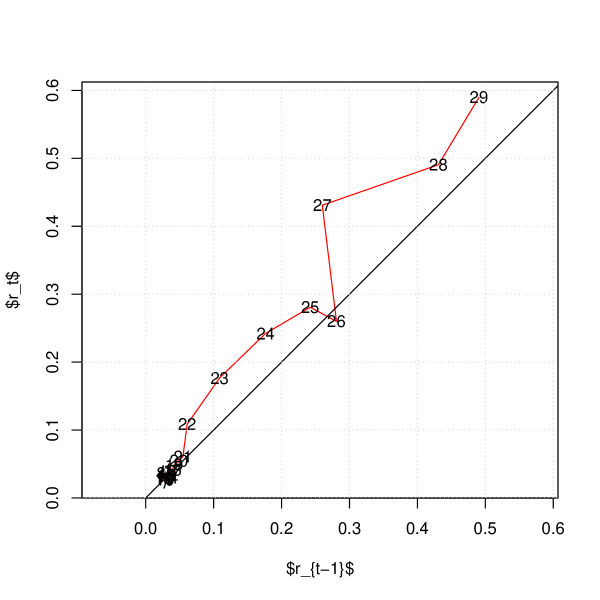

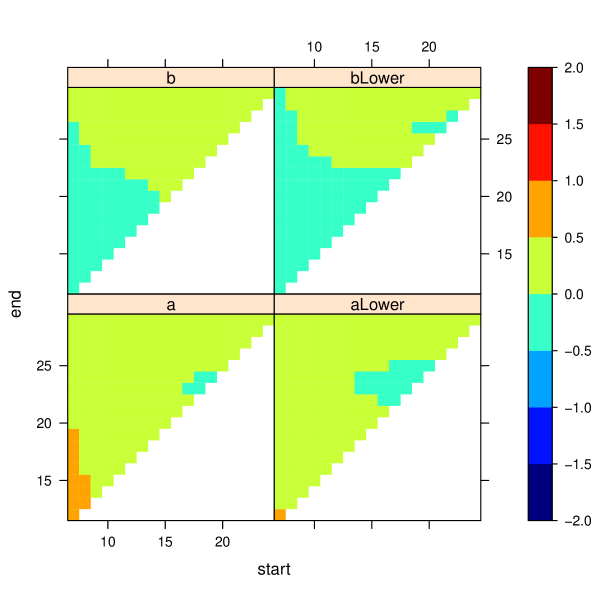

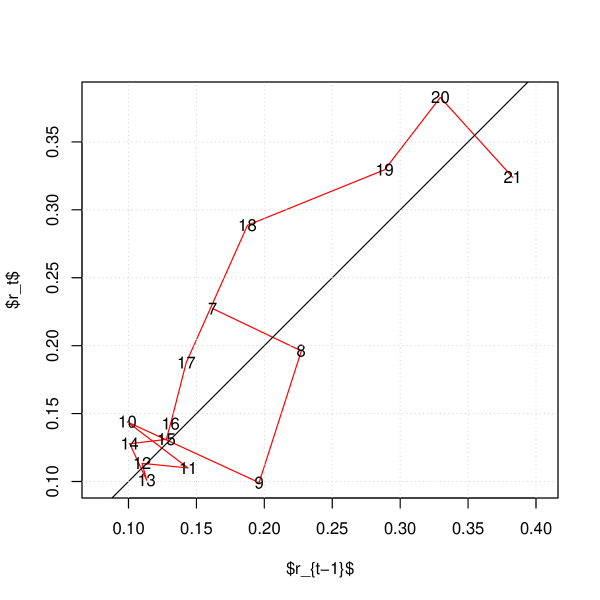

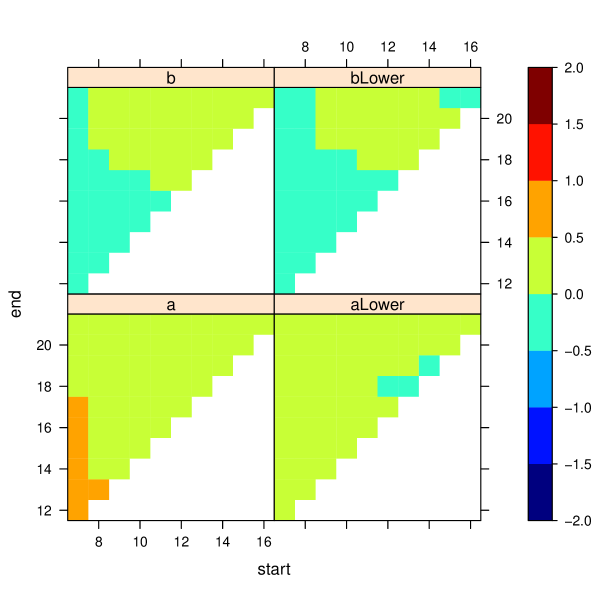

The bubble period identified by Hommes et al. (2008) runs from 7 – 26. Figure 1 shows that the price becomes larger than the fundamental value at . Checking the returns vs. past returns in Figure 2, we see that the bubble initially grows approximately exponentially () as confirmed by the positions of the points along the diagonal. Later, at around , the returns become monotonous increasing (i.e. prices become faster than exponential growth) and are plotted above the diagonal. This is also confirmed by Figure 3 where, for low starting and ending values of the analyzing time window, the parameters estimated for Equation 3 are not distinguishable from exponential growth since the parameter is not significantly different from zero. However, towards the middle and the end of the bubble, the growth rate accelerates ( becomes significantly larger then zero) before the bubble finally bursts. The parameter is positive over the whole analysis window (lower left panel) and almost always significantly larger than zero (lower right panel). The upper panels shows that (for low start and ending values) is not significant different from zero, but, later in the bubble, becomes positive (top left panel) and even significant positive (upper right panel).

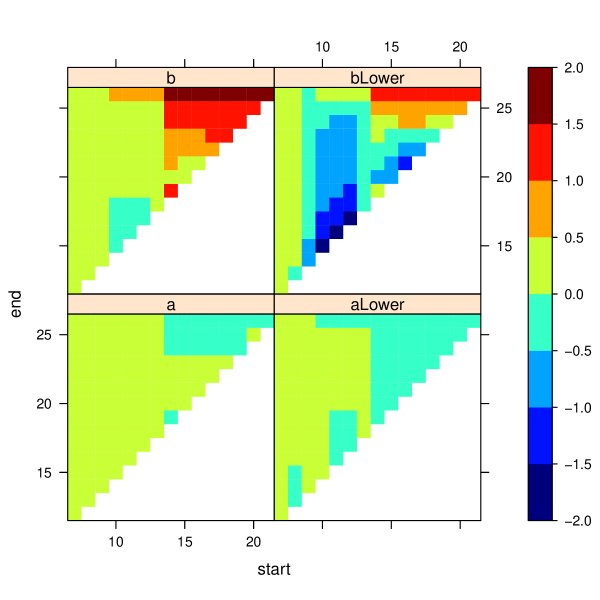

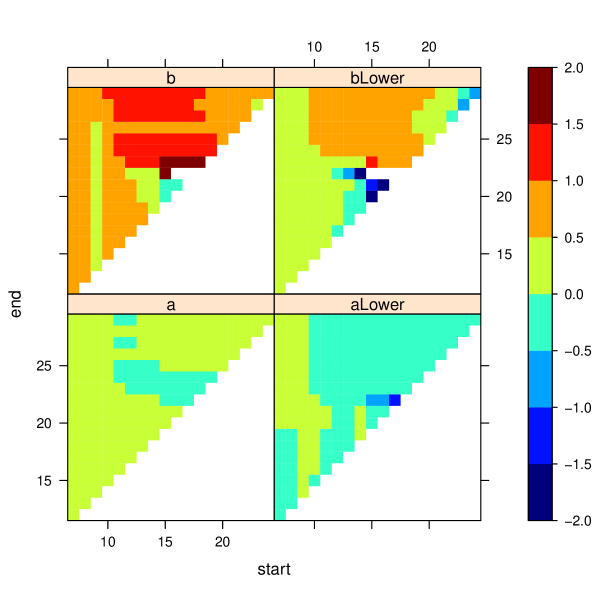

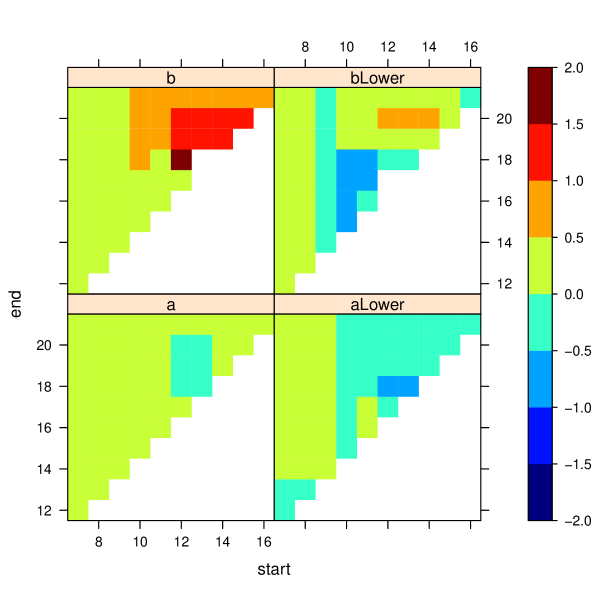

Checking for the existence of feedback from past returns in Figure 4, we find that Equation 4 describes less accurately the experimental results; although the parameters and are both positive (left panels), the time windows where the parameters are both significantly positive (right panels) is relatively small (only for starting values and ).

Hence, in summary, the bubble in group 2 does not only grow significantly faster then exponential in the end phase, but traders seem to anchor their expectations more on price rather than on return.

4.2 Group 3

Group 3 (over the time horizon from 7 – 29) is the longest bubble among the six groups. From Figure 5 (which is plotted on scale), the bubble seems to grow initially only exponentially (visible as a straight line in the plot), which is also confirmed by Figure 6, which shows that the growth rate is initially constant. At around , growth accelerates. This observation is also confirmed by the analysis of Equation 3, where is significant for almost all analysis windows. But, the positive feedback of the price on the growth rate embodied by becomes only significant in the later phase of the bubble. Analyzing this group for the possible existence of anchoring on return (Equation 4) in Figure 8, we find that the results are less clear cut: although and are positive, is not significantly different form zero for starting values after . Hence, we conclude that Equation 4 does not appropriately describe the price and traders tend to anchor their expectations on price rather than on return.

4.3 Group 4

As can be seen from Figure 9, the bubble formed over the time window 7 – 29 is briefly disrupted by the intervention of trader number 6555The prediction of trader number six at time point seems to be off by an order of magnitude as he has misplaced the decimal.. This can also be seen in Figure 6 where we plot the returns. Between and , we have more or less a cobweb and then, starting with , the growth rate increases and a bubble is formed. For anchoring on price, we see in Figure 11 very strong evidence for faster then exponential growth; and are both significantly positive. Again, for very early and small analysis windows, only is positive, indicating exponential growth in the initial phase of the bubble. The analysis for Equation 4 in Figure 12 is less clear, but the signal for jointly positive and is relatively small (only for two smallest starting values), indicating that traders prefer to anchor their predictions on price and not on return.

5 Discussion

It is remarkable that we find many time windows where we can clearly reject the hypothesis of exponential growth and find evidence for faster than exponential growth. This is even more remarkable when taking into account that the data suffers some limitations which make detection of faster than exponential growth more difficult.

- Price ceiling:

-

Although the price is allowed to fluctuate over a relatively large range, it is capped at a maximum value of . Because traders know and can anticipate this, we would expect traders to level off their price expectation much before reaching this upper bound. This turns out not to be the case.

- Stable equilibrium price:

-

The pricing formula Equation 1 assumes a fundamental value of and thus biases the price towards this value. Even if all traders give an estimate of , the realized market price from Equation 1 would be , i.e. the price is artificially deflated by almost 45 monetary units.

- Mis-trades:

-

There seems to be a few instances where trades’ estimates are off by an order magnitude (i.e. some traders seem to fail to place the decimal point at the correct digit at some times).

- Short data horizon:

-

Although the experiments run over a time horizon of time-steps; the bubbles appear in much shorter time, leaving relatively few points to estimate tight confidence intervals.

Heemeijer et al. (2009) ran a comparable experiment with a slightly different price forming mechanisms and focusing on the traders’ individual price forecasts. Further, agents’ predictions had to lie in a relatively narrow range (0 – 100) allowing relatively small deviations from the fundamental price compared to the data that we have analyzed here. In contrast to Heemeijer et al. (2009) who analyzed the data along the dimensions of trend following, fundamentalism and obstinacy, we focus on non-linear feedback of realized price and return on the price growth rate. Anufriev and Hommes (2012) have fitted a heuristics switching model to a positive feedback asset pricing experiment in the presence of a fundamental robot trader, whose trading drives the price back towards its fundamental value. As a consequence, long lasting bubbles do not arise in that setting, but rather asset prices oscillate around the fundamental and individuals switch between different simple forecasting heuristics such as adaptive expectations and trend following rules.

Tirole (1982) noted that “[..] speculation relies on inconsistent plans and is ruled out by rational expectations.” However, in the experiments of Hommes et al. (2008) that we analyze here, traders are rewarded, not on the basis of how well they predict the fundamental value of the assets they buy but rather, on the accuracy of their prediction of the realized price itself, similarly to real financial markets. Traders also do not need to invest their wealth into an asset, they do not worry about price fluctuations or care about supply & demand, which lead them to “ride the bubble” (see Abreu and Brunnermeier (2003), de Long et al. (1990) and De Long et al. (1990)). They rather give a forecast as in a Keynesian beauty contest Keynes (1936), where traders need to synchronize their beliefs. Such self-confirming predictions can easily lead to herding, in particular in situations where the fundamental value is not directly observable or when strong disagreement on the fundamentals between the traders occurs, such as in the dot-com bubbles, see Shiller (2005) for instance.

6 Conclusions

There have been many reports of super-exponential behavior in financial markets in a literature inspired by the dynamics of positive feedback leading to finite-time singularities in natural and physical systems (see for instance Johansen and Sornette (2001) and Sornette (2004) and references therein). However, the challenge has been and is still to confirm with more and more statistical evidence that the very noisy financial returns do contain a significant positive feedback component during some bubbles regimes. In the present paper, by analyzing a controlled experiments in the laboratory, we have the luxury of working with a low noise data set. With this advantage, we have presented the first detailed quantitative calibration of simple models with positive feedback that unambiguously demonstrate the existence of positive feedback mechanisms in the price formation process of controlled experimental financial markets.

Appendix

Faster than exponential growth means that there is a positive feedback loop, or as Andreassen and Kraus (1990) noted that “[..] subjects were more likely [..] to buy as prices rose [..]”. The table down-below illustrates the difference between constant growth and positive feedback. Note that the prices in the two bubbles can be indistinguishable in the early phase of the bubble.

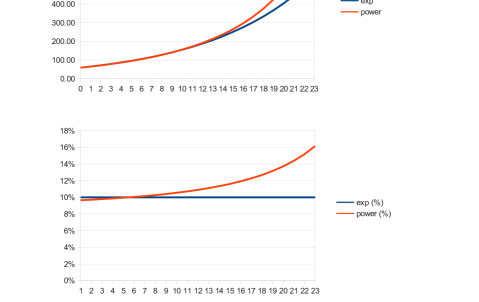

| % | % | |||

| 0 | 60.00 | – | 60.00 | – |

| 1 | 66.00 | 10% | 65.79 | 10% |

| 2 | 72.60 | 10% | 72.19 | 10% |

| 3 | 79.86 | 10% | 79.26 | 10% |

| 4 | 87.85 | 10% | 87.08 | 10% |

| 5 | 96.63 | 10% | 95.74 | 10% |

| 6 | 106.29 | 10% | 105.36 | 10% |

| 7 | 116.92 | 10% | 116.06 | 10% |

| 8 | 128.62 | 10% | 127.99 | 10% |

| 9 | 141.48 | 10% | 141.30 | 10% |

| 10 | 155.62 | 10% | 156.21 | 11% |

| 11 | 171.19 | 10% | 172.95 | 11% |

| 12 | 188.31 | 10% | 191.80 | 11% |

| 13 | 207.14 | 10% | 213.11 | 11% |

| 14 | 227.85 | 10% | 237.30 | 11% |

| 15 | 250.63 | 10% | 264.87 | 12% |

| 16 | 275.70 | 10% | 296.45 | 12% |

| 17 | 303.27 | 10% | 332.86 | 12% |

| 18 | 333.60 | 10% | 375.09 | 13% |

| 19 | 366.95 | 10% | 424.48 | 13% |

| 20 | 403.65 | 10% | 482.74 | 14% |

| 21 | 444.01 | 10% | 552.22 | 14% |

| 22 | 488.42 | 10% | 636.09 | 15% |

| 23 | 537.26 | 10% | 738.87 | 16% |

References

- Abreu and Brunnermeier (2003) D. Abreu and M. K. Brunnermeier. Bubbles and Crashes. Econometrica, 71(1):173–204, 2003. doi: 10.1111/1468-0262.00393. URL http://dx.doi.org/10.1111/1468-0262.00393.

- Andersen and Sornette (2004) J. V. Andersen and D. Sornette. Fearless versus fearful speculative financial bubbles. Physica A: Statistical Mechanics and its Applications, 337(3-4):565–585, June 2004. ISSN 03784371. doi: 10.1016/j.physa.2004.01.054. URL http://dx.doi.org/10.1016/j.physa.2004.01.054.

- Andreassen and Kraus (1990) P. B. Andreassen and S. J. Kraus. Judgmental extrapolation and the salience of change. J. Forecast., 9(4):347–372, 1990. doi: 10.1002/for.3980090405. URL http://dx.doi.org/10.1002/for.3980090405.

- Anufriev and Hommes (2012) M. Anufriev and C. Hommes. Evolutionary selection of individual expectations and aggregate outcomes (forthcoming). American Economic Journal: Micro, 2012. URL http://dare.uva.nl/record/333825.

- Bates (1991) D. S. Bates. The Crash of ’87: Was It Expected? The Evidence from Options Markets. The Journal of Finance, 46(3):1009–1044, July 1991. ISSN 00221082. doi: 10.2307/2328552. URL http://dx.doi.org/10.2307/2328552.

- Blanchard (1979) O. J. Blanchard. Speculative bubbles, crashes and rational expectations. Economics Letters, 3(4):387–389, Jan. 1979. ISSN 01651765. doi: 10.1016/0165-1765(79)90017-X. URL http://dx.doi.org/10.1016/0165-1765(79)90017-X.

- Blanchard and Watson (1982) O. J. Blanchard and M. W. Watson. Bubbles, Rational Expectations,and Financial Markets. 1982.

- Brock and Hommes (1998) W. A. Brock and C. H. Hommes. Heterogeneous beliefs and routes to chaos in a simple asset pricing model. Journal of Economic Dynamics and Control, 22(8-9):1235–1274, July 1998. ISSN 01651889. doi: 10.1016/S0165-1889(98)00011-6. URL http://dx.doi.org/10.1016/S0165-1889(98)00011-6.

- de Long et al. (1990) J. B. de Long, A. Shleifer, L. H. Summers, and R. J. Waldmann. Positive Feedback Investment Strategies and Destabilizing Rational Speculation. The Journal of Finance, 45(2):379–395, June 1990. ISSN 00221082. doi: 10.2307/2328662. URL http://dx.doi.org/10.2307/2328662.

- De Long et al. (1990) J. B. De Long, A. Shleifer, L. H. Summers, and R. J. Waldmann. Noise Trader Risk in Financial Markets. The Journal of Political Economy, 98(4):703–738, 1990. ISSN 00223808. doi: 10.2307/2937765. URL http://dx.doi.org/10.2307/2937765.

- Gallegati et al. (2011) M. Gallegati, A. Palestrini, and J. B. Rosser. The period of financial distress in speculative markets: Interacting heterogeneous agents and financial constraints. Macroeconomic Dynamics, 15(01):60–79, 2011. doi: 10.1017/S1365100509090531. URL http://dx.doi.org/10.1017/S1365100509090531.

- Gürkaynak (2008) R. S. Gürkaynak. Econometric tests of asset price bubbles: Taking stock. Journal of Economic Surveys, 22(1):166–186, Feb. 2008. ISSN 0950-0804. doi: 10.1111/j.1467-6419.2007.00530.x. URL http://dx.doi.org/10.1111/j.1467-6419.2007.00530.x.

- Heemeijer et al. (2009) P. Heemeijer, C. Hommes, J. Sonnemans, and J. Tuinstra. Price stability and volatility in markets with positive and negative expectations feedback: An experimental investigation. Journal of Economic Dynamics and Control, 33(5):1052–1072, May 2009. ISSN 01651889. doi: 10.1016/j.jedc.2008.09.009. URL http://dx.doi.org/10.1016/j.jedc.2008.09.009.

- Hommes et al. (2008) C. Hommes, J. Sonnemans, J. Tuinstra, and H. van de Velden. Expectations and bubbles in asset pricing experiments. Journal of Economic Behavior & Organization, 67(1):116–133, July 2008. ISSN 01672681. doi: 10.1016/j.jebo.2007.06.006. URL http://dx.doi.org/10.1016/j.jebo.2007.06.006.

- Hommes (2006) C. H. Hommes. Chapter 23 Heterogeneous Agent Models in Economics and Finance, volume 2, pages 1109–1186. Elsevier, 2006. ISBN 9780444512536. doi: 10.1016/S1574-0021(05)02023-X. URL http://dx.doi.org/10.1016/S1574-0021(05)02023-X.

- Jarrow et al. (2007) R. A. Jarrow, P. Protter, and K. Shimbo. Asset Price Bubbles in Complete Markets Advances in Mathematical Finance. In M. C. Fu, R. A. Jarrow, J.-Y. J. Yen, and R. J. Elliott, editors, Advances in Mathematical Finance, Applied and Numerical Harmonic Analysis, chapter 7, pages 97–121. Birkhäuser Boston, Boston, MA, 2007. ISBN 978-0-8176-4544-1. doi: 10.1007/978-0-8176-4545-8“˙7. URL http://dx.doi.org/10.1007/978-0-8176-4545-8_7.

- Jarrow et al. (2010) R. A. Jarrow, P. Protter, and K. Shimbo. Asset price bubbles in incomplete markets. Mathematical Finance, 20(2):145–185, 2010. ISSN 0960-1627. doi: 10.1111/j.1467-9965.2010.00394.x. URL http://dx.doi.org/10.1111/j.1467-9965.2010.00394.x.

- Jarrow et al. (2011) R. A. Jarrow, Y. Kchia, and P. Protter. How to Detect an Asset Bubble. SIAM Journal on Financial Mathematics, 2:839–865, June 2011. URL http://ssrn.com/abstract=1621728.

- Jiang et al. (2010) Z.-Q. Jiang, W.-X. Zhou, D. Sornette, R. Woodard, K. Bastiaensen, and P. Cauwels. Bubble diagnosis and prediction of the 2005–2007 and 2008–2009 Chinese stock market bubbles. Journal of Economic Behavior & Organization, 74(3):149–162, June 2010. ISSN 01672681. doi: 10.1016/j.jebo.2010.02.007. URL http://dx.doi.org/10.1016/j.jebo.2010.02.007.

- Johansen and Sornette (2001) A. Johansen and D. Sornette. Finite-time singularity in the dynamics of the world population, economic and financial indices. Physica A: Statistical Mechanics and its Applications, 294(3-4):465–502, May 2001. ISSN 03784371. doi: 10.1016/S0378-4371(01)00105-4. URL http://arxiv.org/pdf/cond-mat/0002075.

- Johansen et al. (1999) A. Johansen, D. Sornette, and O. Ledoit. Predicting Financial Crashes using discrete scale invariance. Journal of Risk 1, No. 4:5–32, 1999.

- Johansen et al. (2000) A. Johansen, O. Ledoit, and D. Sornette. Crashes as critical points. Int. J. Theoret. Appl. Financ., 3:219–255, 2000.

- Kaizoji and Sornette (2010) T. Kaizoji and D. Sornette. Bubbles and Crashes. John Wiley & Sons, Ltd, 2010. doi: 10.1002/9780470061602.eqf01018. URL http://dx.doi.org/10.1002/9780470061602.eqf01018.

- Keynes (1936) J. M. Keynes. The General Theory of Employment, Interest, and Money. Prometheus Books, 1936. ISBN 1573921394. URL http://www.worldcat.org/isbn/1573921394.

- Lo et al. (2000) A. W. Lo, H. Mamaysky, and J. Wang. Foundations of Technical Analysis: Computational Algorithms, Statistical Inference, and Empirical Implementation. The Journal of Finance, 55(4):1705–1770, 2000. doi: 10.1111/0022-1082.00265. URL http://dx.doi.org/10.1111/0022-1082.00265.

- Lux and Sornette (2002) T. Lux and D. Sornette. On Rational Bubbles and Fat Tails. Journal of Money, Credit and Banking, 34(3):589–610, 2002. ISSN 00222879. doi: 10.2307/3270733. URL http://dx.doi.org/10.2307/3270733.

- Shiller (2005) R. J. Shiller. Irrational Exuberance: (Second Edition). Princeton University Press, 2 edition, Feb. 2005. ISBN 0691123357. URL http://www.worldcat.org/isbn/0691123357.

- Sornette (2004) D. Sornette. Why Stock Markets Crash: Critical Events in Complex Financial Systems. Princeton University Press, Feb. 2004. ISBN 0691118507. URL http://www.worldcat.org/isbn/0691118507.

- Tirole (1982) J. Tirole. On the Possibility of Speculation under Rational Expectations. Econometrica, 50(5):1163–1181, Sept. 1982. ISSN 00129682. doi: 10.2307/1911868. URL http://dx.doi.org/10.2307/1911868.

- Todd and Gigerenzer (2000) P. M. Todd and G. Gigerenzer. Precis of Simple heuristics that make us smart. Behavioral and Brain Sciences, 23(05):727–741, 2000. doi: null. URL http://dx.doi.org/null.

- Tversky and Kahneman (1974) A. Tversky and D. Kahneman. Judgment under Uncertainty: Heuristics and Biases. Science, 185(4157):1124–1131, Sept. 1974. ISSN 1095-9203. doi: 10.1126/science.185.4157.1124. URL http://dx.doi.org/10.1126/science.185.4157.1124.