On a non-linear transformation between Brownian martingales

Abstract.

The paper studies a non-linear transformation between Brownian martingales, which is given by the inverse of the pricing operator in the mathematical finance terminology. Subsequently, the solvability of systems of equations corresponding to such transformations is investigated. The latter give rise to novel monotone pathwise couplings of an arbitrary number of certain diffusion processes with varying diffusion coefficients. In the case that there is an uncountable number of these diffusion processes and that the index set is an interval such couplings can be viewed as models for the growth of one-dimensional random surfaces. With this motivation in mind, we derive the appropriate stochastic partial differential equations for the growth of such surfaces.

Key words and phrases:

Diffusion processes, continuous martingales, monotone couplings, nonlinear partial differential equations and systems, stochastic partial differential equations.2000 Mathematics Subject Classification:

60J60, 60G44, 35K551. Introduction

The starting point of the paper is the equation

| (1.1) |

where is a positive real number, , and , are stochastic processes with continuous real-valued paths, is the filtration generated by and is a (deterministic) function. This type of equations is fundamental to the mathematical theory of asset pricing, where the process stands for the price process of an asset in a financial market, for the payoff of a contract on this asset and for the price process of this contract. In this context, one usually assumes that the process is of a particular form (for example, a logarithmic Brownian motion in the classical Black-Scholes model as in [3], [18]) and tries to determine exactly or to obtain estimates on the process . It is standard to model the asset price process by a continuous diffusion process and one assumes that is a martingale, which implies the absence of arbitrage in the market given by and by the Fundamental Theorem of Asset Pricing (see [9], [10], [6], [7] and the references therein). For the rest of the paper, we will call continuous diffusion processes, which are martingales, Brownian martingales.

The starting point of our analysis is the following question asked by David Aldous ([1]): Suppose that is a given Brownian martingale and that the function is given. Can one find a process in the class of Brownian martingales such that (1.1) holds in the sense of equality of probability laws? In other words, can one find a Brownian martingale such that the process , coincides in law with a given Brownian martingale ? The first main result of the paper is that, under certain regularity assumptions on and , the question can be answered in the affirmative. The operation of solving (1.1) for can be viewed as the inverse of the pricing operator, which maps to via (1.1). We remark at this point that, although we allow and to take negative values throughout, one can enforce the nonnegativity of and suggested by the financial interpretation by letting be a Brownian martingale taking only nonnegative values and choosing such that the preimage of the state space of under is a subset of . Similarly, one can ensure that and take values in the desired bounded subintervals of .

In the second part of the paper, we study systems of equations

| (1.2) |

for arbitrary index sets . We provide a necessary and sufficient condition on the family , of Brownian martingales under which it is possible to find a Brownian martingale and functions , of certain regularity satisfying (1.2). Moreover, if is endowed with a partial order , we give a condition for the system (1.2) to be solvable in the specified sense with functions , , which satisfy whenever . Clearly, the result are monotone pathwise couplings of the Brownian martingales , . If is an interval endowed with the usual total order, then by viewing as the time variable and as the space variable, one may regard the process , as a model for the growth of a one-dimensional random surface over time. We show that the growth of the surface can be described by a stochastic partial differential equation (SPDE).

To state our first result rigorously, we introduce some notation. In the context of equation (1.1), we denote the state space of by , which we assume to be a (bounded or unbounded) open interval, and write for the time-dependent generator of the process . Moreover, we let be the space of continuously differentiable functions , whose derivatives are bounded between two positive constants.

Theorem 1.

Suppose that is contained in the range of and that the transition densities , , of exist and possess continuous partial derivatives , , and . Moreover, assume that there are constants such that

| (1.3) |

for all and that for any given and there exists an open neighborhood of and a function such that

Finally, suppose that takes only positive values, its partial derivative is continuous and the estimates

| (1.4) |

hold for some constant . Then, for any , there exists a unique Brownian martingale satisfying the equation (1.1) in law and it solves the stochastic differential equation (SDE)

| (1.5) |

where solves the backward Cauchy problem

| (1.6) |

in the classical sense, the superscript denotes the spatial inverse and is a one-dimensional standard Brownian motion.

Our main result on the solvability of the system (1.2) requires the following definition.

Definition 1.

Let , be a family of Brownian martingales with time-dependent generators and initial values , respectively, and fix the notations , and , . We call the family , consistent if the following conditions hold. For any in , there is a function , which solves the ordinary differential equation (ODE)

| (1.7) |

for all values of such that the pointwise limit

| (1.8) |

exists, belongs to , and one has

| (1.9) |

Hereby, the argument of , is , and the arguments of , , are , .

It turns out that this notion of consistency is necessary and sufficient for the solvability of the system (1.2). For a discussion of the conditions in Definition 1, please see Remarks 1 and 2 following the statement of Theorem 2.

Theorem 2.

Suppose that , is a family of Brownian martingales, which all satisfy the conditions of Theorem 1. In addition, suppose that the diffusion coefficients , of , are continuously differentiable and bounded away from . Then, the system (1.2) is solvable by a Brownian martingale and a family , of functions in if and only if the family , is consistent. Moreover, if this is the case, then there are uncountably infinitely many such solutions and the following are true:

-

(a)

The processes , can be defined on the same probability space to form a weak solution of the degenerate system of SDEs

(1.10) on .

-

(b)

If, in addition, there is a partial order on the set and the functions in Definition 1 are such that implies for all in the state space of , then the processes , can be defined on the same probability space in such a way that, for all in , the inequality holds for all with probability .

-

(c)

If, in the situation of part (b), the set is an interval with the usual total order, the function is continuously differentiable and the function has continuous and bounded partial derivatives , , , and , then there is a version of the growth process , , which is continuously differentiable in , and such that the corresponding derivative solves

(1.11) (1.12) Hereby, is a distribution-valued Gaussian field with correlation function

(1.13)

Remark 1.

Consider first the situation and let be a Brownian martingale with diffusion coefficient and initial value , which satisfies the conditions of Theorem 1. Then, a family of Brownian martingales with diffusion coefficients and initial values , which are consistent with , can be constructed as follows. First, let be a solution of the backward heat equation

with some terminal condition , where is an arbitrary real constant. Next, set

| (1.14) |

Then, the Brownian martingale corresponding to the diffusion coefficient and initial value is consistent with . Indeed, by differentiating the equation once with respect to and once and twice with respect to , one can express the partial derivatives of in terms of the partial derivatives of . Plugging the resulting formulas into the backward heat equation and using , one then easily verifies that the constant function solves the ODE in Definition 1.

In the case that , that is, when is a standard Brownian motion, the backward heat equation simplifies to

| (1.15) |

Next, take to be an arbitrary function in . Then, can be viewed as the cumulative distribution function of an infinite positive measure on . Clearly, for any , the function is given by a cumulative distribution function of the measure , where is the normal density with mean and variance . Consequently, is given by a quantile function of . Thus, we conclude that the Brownian martingale solving

| (1.16) |

is consistent with a Brownian motion started in . We note hereby that, since we can choose the constant above in an arbitrary manner, we can take to be an arbitrary real number.

Finally, in the case that has more than two elements, it suffices to observe that Theorems 1 and 2 imply that the definition of consistency for pairs of Brownian martingales induces a transitive relation on the space of Brownian martingales satisfying the conditions of Theorem 1. Indeed, if , , are Brownian martingales such that and are consistent and and are consistent, then by Theorem 2, there are functions and Brownian martingales , such that

Now, the uniqueness statement of Theorem 1 implies that the processes and coincide in law. Therefore, the process

has the law of , so that and are consistent by Theorem 2. This shows the transitivity of the consistency property for pairs of Brownian martingales and, thus, that the family of processes constructed above is consistent, provided that they all satisfy the conditions of Theorem 1.

Remark 2.

The following is the simplest example of a situation, in which the conditions of Definition 1 hold. Suppose that for every the diffusion coefficient of does not depend on , and that for all in there are constants , such that

and . Then, the family , is consistent. Indeed, choosing and , one can check that the conditions of Definition 1 are satisfied by using the identities and .

Remark 3.

Considering the process in Theorem 2 (c) as given, one can view the SPDE (1.11) for the partial derivative as a degenerate version of the SPDEs studied in [4], [5], with random instead of deterministic coefficients. Indeed, setting in equation (1.1) of [4] and choosing the coefficient there to be the (random) diffusion coefficient in our equation (1.11) and the coefficient there to be the corresponding (random) Itô correction term, one recovers our SPDE (1.11). For other SPDEs with noise, which is white in time and correlated in space, we refer the reader to [15], [16] and the references therein.

The rest of the paper is structured as follows. Section 2 is devoted to the proof of Theorem 1. As it turns out, equation (1.1) can be solved by solving a nonlinear parabolic partial differential equation (PDE). This PDE is similar to the nonlinear PDEs appearing in [19] and can be reduced to a linear PDE by a suitable transformation. This is the content of subsection 2.1. In subsection 2.2, we solve the linear PDE and complete the proof of Theorem 1. In subsection 2.3, we analyze the solvability of equation (1.1) in the degenerate case that for some . In mathematical finance terms, the equation (1.1) for this choice relates the price process of a digital option to its payoff . Alternatively, one can view the process as describing the evolution of the conditional probabilities of the event based on the information about the process available so far. Such processes can be observed in practice as quotes in prediction markets (see [2] for more details). In contrast to the findings of Theorem 1, we find an uncountably infinite family of Brownian martingales solving the equation (1.1) in this case.

In section 3, we give the proof of Theorem 2. For the sake of clarity, we first prove the relevant statements of Theorem 2 in the case that . To this end, we need to solve a system of two nonlinear PDEs, each of the same type as in subsection 2.1. This is the content of subsection 3.1. In subsection 3.2, we show how the arguments extend to the case of general index sets . Finally, in section 4 we give more examples of situations, in which Theorems 1 and 2 apply, by treating Brownian martingales consistent with the Kimura martingale.

2. Proof of Theorem 1

2.1. Reduction to a linear PDE

In this subsection, we show that the problem of solving (1.1) naturally reduces to a backward Cauchy problem for a linear PDE. We start with a proposition.

Proposition 3.

Let the functions and be as in Theorem 1, and suppose that is a Brownian martingale solving (1.1) with this and being a Brownian martingale with time-dependent generator . Moreover, assume that there exists a classical solution of

| (2.1) |

such that , the partial derivative exists and is continuous, and

| (2.2) |

Then, the time-dependent generator of is given by and it holds

| (2.3) |

The proof of the proposition relies on the following lemma.

Lemma 4.

Let the functions and be as in Theorem 1, and suppose that is a classical solution of the PDE (2.1) satisfying and (2.2), whose partial derivative exists and is continuous. Then, the spatial inverse is well-defined, solves the linear backward Cauchy problem

| (2.4) |

in the classical sense and its partial derivative is bounded.

Proof. From the PDE (2.1) it is clear that either everywhere, or everywhere. However, since is strictly increasing, it holds and, hence, the inequality must be true everywhere. Thus, for every , the function is strictly increasing and therefore the spatial inverse is well-defined. Next, we consider the equation . Differentiating this equation with respect to once and with respect to once and twice, we obtain the following set of equations:

| (2.5) | |||

| (2.6) | |||

| (2.7) |

Hereby, the partial derivatives , and exist by the Implicit Function Theorem. Plugging the equations (2.5), (2.6), (2.7) into (2.1), we obtain

| (2.8) |

Simplifying, we conclude that is a classical solution of the problem (2.4) as desired. Moreover, differentiating both sides of the equations in (2.4) with respect to , we deduce that is a classical solution of the problem

| (2.9) |

Hereby, the existence and continuity of the partial derivative follows from the existence and continuity of and the Implicit Function Theorem. Moreover, the existence and continuity of the partial derivative is a consequence of (2.4) and the existence and continuity of and . In addition, by assumption, the function is bounded away from , so that is bounded. Moreover, in view of (2.6), the assumption (2.2) implies

| (2.10) |

Applying the Maximum Principle for linear parabolic PDEs in the form of Theorem 9 in chapter 2 of [8], we conclude that must be bounded everywhere. This finishes the proof of the lemma.

Proof of Proposition 3. By Lemma 4, the spatial inverse is well-defined, solves the PDE (2.4) in the classical sense and has a bounded partial derivative . Defining the process , , we obtain by Itô’s formula:

| (2.11) |

Hereby, the drift terms disappear, since has the time-dependent generator by assumption and is a classical solution of the equation (2.4). Moreover, since is bounded and is a martingale, the process , is also a martingale. Noting that and recalling that is a martingale, we conclude that must hold for all with probability . Clearly, this implies that , with probability . Hence, from equation (2.11), we see that the time-dependent generator of must be given by

| (2.12) |

Finally, by the definition of and the previous considerations, it holds

| (2.13) |

This finishes the proof of the proposition.

The proposition shows that, if a classical solution to the PDE (2.1) with terminal condition exists and possesses a continuous partial derivative , then a solution of the equation (1.1) must have the time-dependent generator . In the next subsection, we show that, under the assumptions of Theorem 1, the desired classical solution of the nonlinear PDE (2.1) exists by solving the linear PDE (2.4), and that the resulting process is indeed a Brownian martingale.

2.2. Solution of the linear PDE

As we have seen in the previous subsection, the crucial step in the solution of the equation (1.1) consists of finding a sufficiently regular solution of the problem (2.4). In the following lemma we show that the latter exists under the assumptions of Theorem 1.

Lemma 5.

Proof. Recalling the notation , , for the transition densities of the process , we define the function by

| (2.15) |

The assumptions on allow us to interchange the order of differentiation and integration to obtain

| (2.16) | |||

| (2.17) |

and to conclude that the functions and are continuous by using the Dominated Convergence Theorem. It follows that

is a consequence of the Kolmogorov backward equation

| (2.18) |

Moreover, by the definition of , we have . In addition, the growth estimate (2.14) follows from another exchange of the order of differentiation and integration

| (2.19) |

and (1.3). Finally, the partial derivative exists and is continuous due to yet another exchange of the order of differentiation and integration

| (2.20) |

and the continuity of the right-hand side in the latter equation, justified by the assumptions on and the Dominated Convergence Theorem.

We are now ready to give the proof of Theorem 1.

Proof of Theorem 1. We first prove that a solution to (1.1) of the described form exists. To this end, we let be a classical solution of the problem (2.4) as in Lemma 5 and set , . Applying Itô’s fomula, we see that

| (2.21) |

Hereby, the drift terms disappear, because has the time-dependent generator and is a classical solution of the PDE in (2.4). Moreover, noting that is a classical solution of the problem (2.9) and applying the Maximum Principle for linear parabolic equations in the form of Theorem 9 in chapter 2 of [8] (note the growth estimate (2.14)), we conclude that is bounded between two positive constants. In particular, the spatial inverse is well-defined and , . Putting these observations together with (2.21), we conclude that is a Brownian martingale with time-dependent generator .

Next, we note that the identities , , imply that the filtration generated by is the same as the filtration generated by . Moreover, we have

| (2.22) |

Hence, since is a martingale in the filtration generated by , it holds

| (2.23) |

as desired.

We now turn to the proof of uniqueness. Differentiating both sides of the equation once with respect to and twice with respect to , we get

| (2.24) | |||

| (2.25) |

Hence,

In addition, the existence and continuity of the partial derivative and the Implicit Function Theorem imply that exists and is continuous. Moreover, the estimate (2.2) is a direct consequence of the growth estimate (2.14). Applying Proposition 3, we conclude that a Brownian martingale solving (1.1) must have the generator . This and the boundedness of the function show that the process , is a martingale in the filtration generated by by an application of Itô’s formula. Therefore, by (1.1)

| (2.26) |

for a process of the same law as . From (2.26) we see that the law of the process , is uniquely determined.

2.3. A degenerate case

We turn now to the degenerate case that the function in equation (1.1) is given by the indicator function for some . To make sure that (1.1) is well-posed, we need to assume that the state space of is the interval and that holds with probability . As before, we write for the time-dependent generator of . In contrast to the non-degenerate case of Theorem 1, there exist uncountably infinitely many Brownian martingales solving (1.1) here.

Proposition 6.

Proof. As in the non-degenerate case, we consider the linear PDE

| (2.28) |

which formally yields

This motivates letting , and setting , . Indeed, then is a Brownian martingale. Moreover,

since the filtration generated by is the same as the filtration generated by , and is a martingale in this filtration. It follows that is a solution of the equation (1.1). Finally, by Theorem 4.2 in chapter 3 of [12], the process obeys the SDE

| (2.29) |

for a standard Brownian motion . This shows that the process , satisfies the SDE in the statement of the proposition. Now, it remains to note that the choice of the constants was arbitrary and the proof is finished.

3. Proof of Theorem 2

3.1. Systems of two equations

For the sake of clarity of exposition and simpler notation, we first give the proof of the relevant statements of Theorem 2 in the case that . To fix notations, we let , be two Brownian martingales with time-dependent generators , and initial values , , respectively. Assuming that and satisfy the conditions of Theorem 1, we seek Brownian martingales and functions such that the system of equations

| (3.1) | |||

| (3.2) |

is satisfied. In the case that , the definition of consistency (Definition 1 in the introduction) simplifies to the following definition.

Definition 2.

Letting and , we say that the Brownian martingales and are consistent if there is a function , which solves the ODE

| (3.3) |

for all values of and such that the pointwise limit

| (3.4) |

exists, belongs to , and it holds

| (3.5) |

Hereby, the argument of , is , and the arguments of , , are , .

We show now that the system (3.1), (3.2) is solvable if and only if the Brownian martingales and are consistent.

Proposition 7.

Suppose that the Brownian martingales , satisfy the assumptions of Theorem 1 and that their diffusion coefficients , are continuously differentiable and bounded away from . Then, there is a Brownian martingale and functions , which solve the system (3.1), (3.2), if and only if and are consistent in the sense of Definition 2. Moreover, if this is the case, then there are uncountably infinitely many such solutions.

Proof. We assume first that and are consistent in the sense of Definition 2. In order to solve the system (3.1), (3.2), it suffices to find a Brownian martingale with a time-dependent generator , as well as functions such that the system of PDEs

| (3.6) | |||

| (3.7) | |||

| (3.8) | |||

| (3.9) | |||

| (3.10) | |||

| (3.11) |

has a classical solution, and . Indeed, then the processes , and , satisfy

| (3.12) | |||

| (3.13) |

for a standard Brownian motion (apply Itô’s formula and (3.6), (3.8), (3.7), (3.9)) and, thus, are Brownian martingales with time-dependent generators , and initial values , , respectively. Since

this gives the desired solution of the system (3.1), (3.2). Note hereby that by our assumptions on and , the solutions to (3.12) and (3.13) are pathwise unique and, therefore, the martingale problems for and are well-posed due to the results of Yamada and Watanabe (see e.g. Proposition 3.20 in [12]).

To solve the system (3.6)-(3.11), we fix an arbitrary function and proceed as in the proof of Theorem 1 to find a Brownian martingale and a function such that the equations (3.6), (3.8), (3.10) and are satisfied. Next, to make sure that equation (3.9) holds, it suffices to choose in such a way that

| (3.14) |

However, recalling the definitions of the functions and in Definition 2 and integrating both sides of the equation (3.14) in , we see that the latter is equivalent to the equation

| (3.15) |

for some function . Moreover, since the functions and take only positive values by assumption, the functions and are strictly increasing for all . It is now easy to check that equation (3.15) will hold if and only if we set with a function satisfying

| (3.16) |

Hereby, we recall from the proof of Theorem 1 that the functions , are strictly increasing, so that the spatial inverses , are well-defined and strictly increasing as well. We note at this point that the just introduced function is determined by the parameters of the problem. On the other hand, we are free to pick a function of our choice and choose it as the function in Definition 2.

Next, we make sure that equation (3.11) holds. To this end, we note that by the definition of the function in Definition 2 and (3.16) we have

| (3.17) |

Thus, to ensure (3.11) it is enough to set . The resulting function belongs to by our assumptions on and . Moreover, one has

| (3.18) |

where the second identity is a consequence of the fact that , solve (3.1) by construction and the third identity is a consequence of and being consistent (see Definition 2).

It remains to check that with the choice of (and, hence, also of ) above, the equation (3.7) is satisfied. We claim that it suffices to show that is a classical solution of the PDE

| (3.19) |

Indeed, differentiating the equation once with respect to and once and twice with respect to , one can express the partial derivatives of in terms of the partial derivatives of and compute

where we have used (3.9) in the first identity. To check that is a classical solution of (3.19), we set and observe that, in view of (3.16), equation (3.19) can be rewritten as

| (3.20) |

Simplifying the left-hand side, we see that this is equivalent to the following ODE for :

| (3.21) |

Hereby, the arguments of and its partial derivatives are , , and the arguments of and its partial derivatives are , , . The key observation is now that, due to the definitions of the functions , and (see (3.16) and Definition 2), we have

Plugging this into (3.21) and recalling from the proof of Theorem 1 that is a classical solution of the problem (2.4), we can simplify the ODE (3.21) to

| (3.22) |

Next, we evaluate the partial derivatives of to

Putting this together with (3.22), we end up with

Finally, recalling that and , we can write the latter equation as

Moreover, since and , this equation simplifies further to

The last equation holds due to the assumption that and are consistent. Thus, we have constructed a solution of the system (3.1), (3.2).

Conversely, suppose that , , form a solution of the system (3.1), (3.2). Then, by the uniqueness result in Theorem 1, the pair has to coincide with the solution of (3.1) constructed in the proof of Theorem 1, and the pair has to coincide with the solution of (3.2) constructed in the proof of Theorem 1. In particular, it must hold

| (3.23) |

One can now proceed as in the first part of the proof to deduce the existence of a function such that is given by (3.16). Plugging this expression for into (3.19) and proceeding as before, one shows that must solve the ODE in Definition 2. Moreover, setting , one easily verifies (3.4) and (3.5) by using (3.15) and , respectively. This shows the consistence of and .

Finally, since the choice of in the construction above was arbitrary among all functions in , we conclude that, if and are consistent, the system (3.1), (3.2) has uncountably infinitely many solutions.

Remark 4.

A careful reading of the proof of Proposition 7 shows that the system (3.1), (3.2) is solvable by a Brownian martingale and functions under the weaker assumption that satisfies the conditions of Theorem 1, the martingale problem for is well-posed and the diffusion coefficients , are continuously differentiable, bounded and bounded away from . The same is true for the statements in the upcoming Corollary 8.

As a consequence of Proposition 7, we obtain the existence of couplings of consistent Brownian martingales.

Corollary 8.

Suppose that the Brownian martingales and satisfy the conditions of Theorem 1, their diffusion coefficients are continuously differentiable and bounded away from , and that , are consistent in the sense of Definition 2. Then, and can be defined on the same probability space to form a weak solution the degenerate system of SDEs

| (3.24) | |||

| (3.25) |

on . If, in addition, the function in Definition 2 is such that for all in the state space of , then the inequality holds for all with probability .

Proof. Applying Proposition 7, we see that there is a probability space, a Brownian martingale defined on this space and functions such that the equations (3.1), (3.2) hold. As we have seen in the course of the proof of Proposition 7, the processes , solve the degenerate system of SDEs (3.24), (3.25). Moreover, under the additional assumption of for all in the state space of , we have

| (3.26) |

with probability , which is the desired monotone coupling.

Remark 5.

In the setting of Remark 1 with , Remark 4 and Corollary 8 show that the degenerate system of SDEs

| (3.27) | |||

| (3.28) |

has a weak solution on for any initial values , . We note hereby that the diffusion coefficient of is continuous, bounded and bounded away from , so that the martingale problem satisfied by is well-posed. Moreover, since the weak solution constructed in the proof of Corollary 8 has the property that, for any , can be written as a deterministic function of , the resulting process is adapted to the filtration generated by the Brownian motion . This shows that the SDE (3.28) has a strong solution for any initial value . We note that if the function

fails to be bounded, the existence of a strong solution does not follow from classical existence theorems such as Theorem 2.9 in chapter 5 of [12]. In addition, in this case , where is uniquely determined by

At this point, Corollary 8 shows that, whenever holds for all , the system (3.27), (3.28) has a weak solution on starting from such that the inequality holds for all with probability .

To demonstrate the possible range of applications of Corollary 8, we give one immediate corollary.

Corollary 9.

Suppose that the Brownian martingales and satisfy the conditions of Theorem 1, their diffusion coefficients are continuously differentiable and bounded away from , and that , are consistent in the sense of Definition 2. Assume further that the inequality holds for all in the state space of . Moreover, for any fixed , let , be the first hitting times of the set before by the respective Brownian martingales (which we set to be equal to if the set is not hit before ). Then, is stochastically dominated by in the sense that it holds

| (3.29) |

for all .

3.2. Systems of any number of equations

We now generalize the constructions of the previous subsection to give a proof of Theorem 2 for a general index set .

Proof of Theorem 2. We assume first that the family , is consistent in the sense of Definition 1 and will construct a solution of the system (1.2) of the desired type. Arguing as in the proof of Proposition 7, we see that it suffices to find a Brownian martingale with a time-dependent generator , as well as functions , in such that the system of PDEs

| (3.30) | |||

| (3.31) | |||

| (3.32) |

has a classical solution and , . To this end, we fix a and a function , and define as the solution of (1.1) for the pair , constructed in the proof of Theorem 1. Then, the equations (3.30), (3.31), (3.32) will hold for . Now, we set for all in . Following the lines of the proof of Proposition 7, one checks that with this choice the equations (3.30), (3.31), (3.32) are satisfied for all due to the consistency of the family , . In addition, since there are uncountably infinitely many choices for the function , there are uncountably infinitely many solutions of the system (1.2).

Conversely, suppose that a Brownian martingale and a family of functions , in solve the system (1.2). Then, by Proposition 7, every pair , must be consistent in the sense of Definition 2. Therefore, the family , is consistent in the sense of Definition 1.

At this point, to show the statements (a) and (b) in the theorem, one only needs to follow the lines of the proof of Corollary 8. To prove statement (c), we apply Theorem 4.2 in [17] to deduce that, under the assumptions in statement (c) in the theorem, there exists a version of the unique strong solution of the system (1.10), which is continuously differentiable in for every , and, for all , the derivative is a strong solution of the equation

| (3.33) |

Rewriting the latter equation in distributional form, we arrive at (1.11).

Remark 6.

A careful reading of the proof of Theorem 2 shows that the system (1.2) has a solution of the desired type and the statements (a), (b), (c) of Theorem 2 hold under the weaker assumption that there is a such that satisfies the conditions of Theorem 1, the martingale problems for , are well-posed and the diffusion coefficients , are continuously differentiable, bounded and bounded away from .

Remark 7.

Let be an interval and define the Brownian martingales , as in the second paragraph of Remark 1, but choosing terminal conditions depending on . Letting be the corresponding quantile functions, we recall from Remark 1 that the family , of Brownian martingales with diffusion coefficients is consistent for any choice of initial values , . In view of Remark 6 and Theorem 2 (a), the degenerate system of SDEs

| (3.34) | |||

| (3.35) |

has a weak solution on for any initial values and , . We recall hereby from Remark 5 that, for every , the martingale problem satisfied by is well-posed. Subsequently, we deduce as in Remark 5 that all processes , are adapted to the filtration generated by the Brownian motion by construction. This shows that the system (3.35) has a strong solution for any initial values , .

Next, define the constants , by

If the functions decrease pointwise in , then the functions satisfy for all in the state space of , whenever . In this case, we can conclude from Theorem 2 (b) that the system (3.35) has a weak solution, for which holds for all with probability , whenever . Finally, if the functions and satisfy the additional regularity assumptions of Theorem 2 (c), then there is a version of the growth process defined there, which satisfies

| (3.36) | |||

| (3.37) |

with being the distribution-valued Gaussian field in part (c) of Theorem 2.

Example 1.

Based on Remark 7, we now give a numeric example of a situation, in which Theorem 2 (c) applies. To this end, we would like to choose the terminal conditions as the functions

| (3.38) |

with varying in . However, the functions do not satisfy the differentiability assumption on of Remark 7. To avoid this problem, we choose a small smoothing parameter and set

| (3.39) |

where is the normal density with mean and variance . A straightforward computation then gives

where is the normal density with mean and variance and is the corresponding cumulative distribution function. Therefore, the corresponding quantile functions , are given as the solutions of

| (3.40) |

Differentiating both sides of this equation with respect to , solving for and simplifying, we end up with the identity

| (3.41) |

where the functions , are given as the solutions of (3.40). We conclude from Remark 7 that the Brownian martingales , corresponding to the diffusion coefficients , and initial values

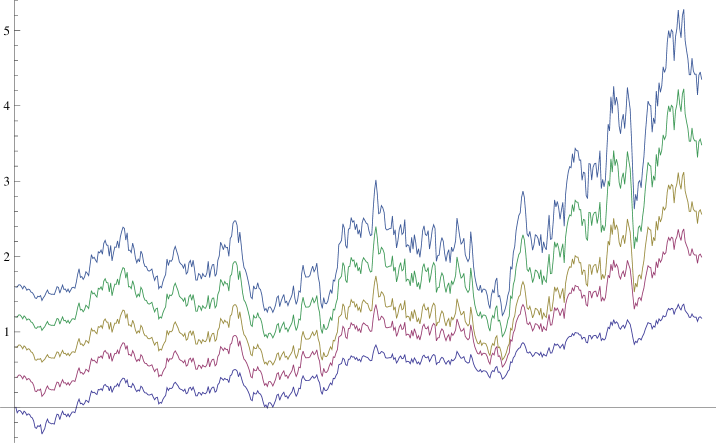

can be defined on the same probability space in such a way that the inequalities are satisfied for all and in with probability . In Figure 1, we demonstrate this fact by plotting sample paths of the Brownian martingales for obtained by using the same sample path of the driving Brownian motion.

4. Additional examples

In this last section we demonstrate the results of Theorem 1, Proposition 6 and Theorem 2 on the example of the Kimura martingale

| (4.1) |

and a time-changed version of it defined below. We recall that the state space of is the open interval and that does not exit from in finite time with probability (see e.g. section 6 in [11]).

4.1. Single equation

First, we fix a function , and seek a Brownian martingale solving (1.1) with given by (4.1). To this end, we recall first that the transition densities of the Kimura martingale can be written down explicitly (see [11], [13]):

, . In particular, the partial derivatives , , and exist and are continuous. In addition, a lengthy but straightforward calculation shows that

| (4.2) |

and that the same is true for the partial derivatives , , and . Therefore, we can apply Theorem 1 to conclude that there exists a unique Brownian martingale , which satisfies (1.1) for these and . Moreover, Theorem 1 and its proof imply that solves the SDE

| (4.3) |

on the time interval , where

| (4.4) |

solves the problem (1.6) with in the classical sense.

To demonstrate an application of Proposition 6, we consider the process obtained from the Kimura martingale by the deterministic time change

| (4.5) |

In other words, is the Brownian martingale given by the solution of the SDE

| (4.6) |

Now, by Proposition 5.22 (d) in chapter 5 of [12], the almost sure limit exists and is given by on a set of probability and by on a set of probability . Letting for some , we see from Proposition 6 that the equation (1.1) with and this choice of has uncountably infinitely many solutions, each of which satisfies an SDE of the form

| (4.7) |

for some constants .

4.2. Systems of equations

In order to give an example of an application of Theorem 2, we start with the Kimura martingale and proceed as in Remark 1 to construct a family of Brownian martingales consistent with . In this particular case, one has

| (4.8) | |||

| (4.9) |

Hence, the backward heat equation of Remark 1 reads

| (4.10) |

Setting and letting be a function in , we see that, for any fixed , it holds with being the appropriate transition density of the diffusion

| (4.11) |

For each , we write for the spatial inverse of and conclude from Remark 1 that the Kimura martingale is consistent with the Brownian martingale solving the SDE

| (4.12) |

Letting be an interval, letting depend on and proceeding as before, we obtain a family of consistent Brownian martingales , . Moreover, the family , , satisfies the conditions described in Remark 6. Indeed, for every , the boundedness, the boundedness away from and the continuity of the diffusion coefficients of shows that the martingale problem satisfied by is well-posed. Therefore, we may apply Theorem 2 (a) in this situation to conclude that the degenerate system of SDEs

has a weak solution on .

If, in addition, the functions are increasing pointwise in , then we can apply Theorem 2 (b) to conclude that there is a weak solution of the latter system of SDEs on such that, for all in , the inequality holds for all with probability .

If, in addition to the above, the function is continuously differentiable and the function has continuous and bounded partial derivatives , , , and , then by Theorem 2 (c) there is a version of the growth process , , , which evolves according to

| (4.13) | |||

| (4.14) |

with being the distribution-valued Gaussian field in Theorem 2, part (c). Note that these equations coincide with the equations in Remark 7 with the difference being that here the functions are given by spatial inverses of convolutions with the heat kernel for the diffusion in (4.11), as opposed to the heat kernel of a standard Brownian motion in Remark 7.

5. Acknowledgement

The author would like to thank David J. Aldous for asking the question about the solvability of equation (1.1), which started this work, and also for his comments throughout the preparation of this work. He is also grateful to Amir Dembo for helpful suggestions.

References

- [1] Aldous, D. (2012). Personal communication.

- [2] Aldous, D. (2012). Using Prediction Market Data to Illustrate Undergraduate Probability. Preprint available at http://www.stat.berkeley.edu/ aldous/Papers/monthly.pdf.

- [3] Black, F., Scholes, M. (1973). The Pricing of Options and Corporate Liabilities. Journal of Political Economy 81 637-654.

- [4] Buckdahn, R., Ma, J. (2001). Stochastic viscosity solutions for nonlinear stochastic partial differential equations. Part I. Stoch. Process Appl. 93 181-204.

- [5] Buckdahn, R., Ma, J. (2001). Stochastic viscosity solutions for nonlinear stochastic partial differential equations. Part II. Stoch. Process Appl. 93 205-228.

- [6] Dybvig, P., Ross, S. (1987). Arbitrage. Eatwell, J., Milgate, M., Newman, P. (eds.) The new Palgrave dictionary of economics 1 100-106. Macmillan, London.

- [7] Delbaen, F., Schachermayer, W. (1994). A general version of the fundamental theorem of asset pricing. Math. Ann. 300 463-520.

- [8] Friedman, A. (1964). Partial differential equations of parabolic type. Prentice-Hall, Inc., Englewood Cliffs, N.J.

- [9] Harrison, M., Kreps, D. (1979). Martingales and arbitrage in multiperiod security markets. J. Econ. Theory 20 381-408.

- [10] Harrison, M., Pliska, S. (1981). Martingales and stochastic integrals in the theory of continuous trading. Stoch. Process Appl. 11 215-260.

- [11] Huillet T. (2011). On the Karlin-Kimura approaches to the Wright-Fisher diffusion with fluctuating selection. J. Stat. Mech. P02016.

- [12] Karatzas I., Shreve S. (1991). Brownian motion and stochastic calculus. 2nd ed. Springer, New York.

- [13] Kimura M. (1954). Process leading to quasi-fixation of genes in natural populations due to random fluctuations of selection intensities. Genetics 39.

- [14] Knight F. B. (1981). Essentials of Brownian motion and diffusion. Mathematical Surveys and Monographs 18. American Mathematical Society.

- [15] Lions, P.-L., Souganidis, P. E. (1998). Fully nonlinear stochastic partial differential equations. C. R. Acad. Sci. Paris 326 1085-1092.

- [16] Lions, P.-L., Souganidis, P. E. (1998). Fully nonlinear stochastic partial differential equations: non-smooth equations and applications. C. R. Acad. Sci. Paris 327 735-741.

- [17] Metivier M. (1983). Pathwise differentiability with respect to a parameter of solutions of stochastic differential equations. Lecture Notes in Control and Inform. Sci. Theory and application of random fields (Bangalore, 1982) 49 188-200.

- [18] Merton, R. C. (1973). Theory of Rational Option Pricing. The Bell Journal of Economics and Management Science 4 141 -183.

- [19] Musiela M., Zariphopoulou, T. (2010). Stochastic partial differential equations and portfolio choice. Contemporary quantitative finance 195-216. Springer, Berlin.