Dynamic Conic Finance: Pricing and Hedging in Market Models with Transaction Costs via Dynamic Coherent Acceptability Indices

This Version: February 10, 2013

Forthcoming in IJTAF)

Abstract

In this paper we present a theoretical framework for determining dynamic ask and bid prices of derivatives using the theory of dynamic coherent acceptability indices in discrete time. We prove a version of the First Fundamental Theorem of Asset Pricing using the dynamic coherent risk measures. We introduce the dynamic ask and bid prices of a derivative contract in markets with transaction costs. Based on these results, we derive a representation theorem for the dynamic bid and ask prices in terms of dynamically consistent sequence of sets of probability measures and risk-neutral measures. To illustrate our results, we compute the ask and bid prices of some path-dependent options using the dynamic Gain-Loss Ratio.

Keywords:

dynamic coherent acceptability index, conic finance, dynamic coherent risk measures, transaction costs, dividend paying securities, swap contracts, no-good-deal bounds, fundamental theorems of asset pricing, dynamic bid and ask, dynamic gain-loss ratio, arbitrage pricing, illiquid market

MSC2010: 91B30, 60G30, 91B06, 62P05

1 Introduction

We develop a framework for narrowing the theoretical spread between ask prices and bid prices of derivative securities in discrete-time market models with transaction costs, using dynamic coherent acceptability indices (DCAIs) that are studied in Bielecki, Cialenco, and Zhang [BCZ11]. Aside from the use of acceptability indices as a tool, our approach is related to the literature studying no-good-deal pricing as a vehicle to narrow the no-arbitrage interval.

We first formulate and prove a no-good-deal version of the fundamental theorem of asset pricing (FTAP) using a family of dynamic coherent risk measures associated with a DCAI. The classic form of FTAP, i.e. the no-arbitrage form of FTAP in frictionless markets, has been established by numerous authors in varying degrees of generality (Harrison and Pliska [HP81], Dalang, Morton, and Willinger [DMW90], Schachermayer [Sch92], Rogers [Rog94], Kabanov and Kramkov [KK94], Jacod and Shiryaev [JS98], Kabanov and Stricker [KS01b]); for continuous time see Delbaen and Schachermayer [DS94, DS96], Cherny [Che07a]). For markets with transaction costs, no-arbitrage versions of the FTAP are proved in Jouini and Kallal [JK95], Kabanov and Stricker [KS01a], Kabanov, Rásonyi, and Striker [KRS02], Schachermayer [Sch04], and Bielecki, Cialenco, and Rodriguez [BCR12]. In Carr, Geman, and Madan [CGM01], the FTAP was formulated and proved in terms of the no strictly acceptable opportunities condition for frictionless markets, and subsequently Pinar, Salih, and Camci [PSC10] proved a version of the FTAP in the context of the Gain-Loss ratio in markets with proportional transaction costs. The no-good-deal version of FTAP has been obtained for markets with transaction costs in the context of static coherent risk measures, and for frictionless markets using discrete-time coherent risk measures by Cherny [Che07b] and [Che07c], respectively.

There is an extensive literature for methods that narrow the theoretical no-arbitrage interval. One of the widely studied approaches is indifference pricing, which is based on utility maximization. Specifically, an indifference price is a price at which an agent receives the same expected utility between trading and not trading. A comprehensive collection of articles related to indifference pricing can be found in Carmona [Car09]. However, it is known that the indifference pricing approach has limitations: numerical implementations and explicit calculations for indifference pricing may not be robust, and the resulting bid and ask prices are not necessarily risk-neutral in practice (see for instance Staum [Sta07]). Alternatively, Cochrane and Saá-Requejo [CSR00] introduced the no-good-deal pricing methodology. In this approach, the arbitrage bounds are narrowed by ruling out deals that are too good—cash flows that have high Sharpe ratios. This strengthens the no-arbitrage argument by assuming that any investor is willing to accept a good-deal. In a subsequent papers by Bernardo and Ledoit [BL00] and Pinar, Salih, and Camci [PSC10] cash flows are considered good deals if their corresponding Gain-Loss ratio is high. The no-good-deal pricing approach has been used in other applications and settings by Carr, Geman, and Madan [CGM01], Jaschke and Kuchler [JK01], Staum [Sta04], Roorda, Schumacher, and Engwerda [RSE05], Björk and Slinko [BS06], Kloppel and Schweitzer [KS07], Arai and Fukasawa [AF11]. The no-good-deal pricing has also been approached via coherent risk measures in Cherny and Madan [CM06] and Cherny [Che07c].

Several authors studied no-good-deal pricing with either discrete-time or continuous time risk measures. In Madan, Pistorius, and Schoutens [MPS11], dynamically consistent bid and ask prices for structured products are derived using nonlinear expectations, and in Bion-Nadal [BN09] and Cherny [Che07b] dynamic bid and ask prices are found via dynamic risk measures.

Cherny and Madan [CM10] proposed the conic finance framework for pricing in incomplete, frictionless markets using static acceptability indices, which are introduced in Cherny and Madan [CM09]. The framework is called conic finance because the derivative prices they introduce depend on the direction of trade—the resulting set of cash flows generated by the prices of the derivative is longer a linear space, it is instead a convex cone. However, as with any static pricing technique, their prices may lack a dynamic consistency property. This drawback renders the static approach inadequate for pricing exotic derivatives such as path-dependent derivatives. In a recent study, Rosazza-Gianin and Sgarra [RGS12] apply the concepts of dynamic acceptability indices and of -expectation to investigate liquidity risk.

Compared to the papers above, our contributions amount to the following:

-

•

Our framework allows for (hedging) cash flows to pay dividends, and be subjected to transaction costs. In particular, we can apply our no-good-deal pricing approach to the pricing of interest rate swaps and credit default swaps in markets with transaction costs.

-

•

We prove a version of the FTAP formulated in terms of a no-good-deal condition. It is important to stress that our no-good-deal condition is dynamically consistent in time.

-

•

We construct the good-deal ask and bid prices of a derivative which are dynamically consistent, in the sense that they are defined in terms of dynamic coherent acceptability indices. This allows us to narrow the no-arbitrage pricing interval.

-

•

We exemplify the proposed general theory with the dynamic Gain-Loss ratio, which is a particular dynamic coherent acceptability index.

This paper is organized as follows. In Section 2, we define the no-arbitrage condition and the no-good-deal condition, and then prove the Fundamental Theorem of Good-Deal Pricing. Next, in Section 3, we define the no-good-deal ask and bid prices, and proceed by proving a representation theorem for them. Finally, in Section 4, we use dynamic Gain-Loss Ratio to compute the good-deal ask and bid prices for some path-dependent, European-style options.

2 Arbitrage and good-deals

We extensively use the results on dynamic acceptability indices that were obtained in [BCZ11]. Thus, we adopt the mathematical set-up that was used therein. In particular, we assume that the underlying probability space is finite, an assumption that indeed is made so to simplify the presentation.

Let be a fixed time horizon, and let . Next, let be the underlying filtered probability space, and assume that , and is of full support. In what follows, we will denote by the set of all -adapted processes.

On this probability space, we consider a market consisting of a savings account and of traded securities satisfying the following properties:

-

•

The savings account can be purchased and sold according to the process

, where is a nonnegative process specifying the risk-free rate. -

•

The securities can be purchased according to the ex-dividend price process

; the associated (cumulative) dividend process is denoted by . -

•

The securities can be sold according to the ex-dividend price process

; the associated (cumulative) dividend process is denoted by .

We assume that the processes introduced above are adapted. Unless stated otherwise, all inequalities and equalities involving vector-valued processes are understood coordinate-wise. In what follows, we shall denote by the backward difference operator: , and we take the convention that .

Remark 2.1.

For any and , the random variable is interpreted as amount of dividend associated with holding a long position in security from time to time . Respectively, the random variable is interpreted as amount of dividend associated with holding a short position in security from time to time .

Let us illustrate the processes introduced above in the context of a Credit Default Swap (CDS) contract.

Example 2.1.

A CDS contract is a contract between two parties, a protection buyer and a protection seller, in which the protection buyer pays periodic fees to the protection seller in exchange for some payment made by the protection seller to the protection buyer if a pre-specified credit event of a reference entity occurs. Let be the nonnegative random variable specifying the time of the credit event of the reference entity. Suppose the CDS contract admits the following specifications: initiation date , expiration date , nominal value $1, and the loss-given-default is given by a nonnegative scalar and is paid at default. Typically, CDS contracts are traded on over-the-counter markets in which dealers quote CDS spreads to investors. Suppose that the CDS spread quoted by the dealer to sell a CDS contract is , and the CDS spread quoted by the dealer to buy a CDS contract is . For the CDS contract specified above, the cumulative dividend processes and are defined as follows

for . In this case, the ex-dividend ask and bid price processes and specify the mark-to-market values of the CDS for the protection seller and protection buyer, respectively, from the perspective of the protection buyer.

From now on, we make the following natural standing assumption.

Assumption (A): and .

2.1 Self-financing trading strategies

A trading strategy is a predictable process , where is interpreted as the number of units of security held from time to time . We take the convention that corresponds to the holdings in the savings account , and .

Definition 2.2.

The wealth process associated with a trading strategy is defined as

Remark 2.3.

(i) It is important to note the difference in the use of bid and ask prices, in the above definition, between the time and the time .

At time , is interpreted as the cost of setting up the portfolio associated with .

For , the wealth process equals the sum of the liquidation value of the portfolio associated with trading strategy before any time transactions and the dividends associated with from time to .

(ii) Also note that, due to the presence of transaction costs, the wealth process may not be linear in its argument, i.e. , and for , and some trading strategies .

This is the major difference from the frictionless setting.

We proceed by introducing the self-financing condition, which is appropriate in the context of this paper.

Definition 2.4.

A trading strategy is self-financing if

| (1) | |||

for all .

The self-financing condition guarantees that no money can flow in or out of the portfolio.

In what follows, we shall work with the discounted processes: for all trading strategies . The next result gives a useful characterization of the self-financing condition in terms of the wealth process. For the proof we refer to Bielecki, Cialenco, and Rodriguez [BCR12].

Lemma 2.5.

A trading strategy is self-financing if and only if the wealth process satisfies the following equality

for .

Thus, the wealth process at time , associated with a self-financing trading strategy , is equal to the sum of setting up the portfolio associated with at time , the liquidation value at time of the portfolio associated with , all purchases and sales before time , and all dividends associated with up to time .

Remark 2.6.

Naturally, if there are no transactions costs, we recover classic definitions of the wealth process and self-financing condition. In the case when the market is frictionless and there are no dividend-paying securities, that is and , see for instance Pliska [Pli97]. If the market is frictionless and there are dividend-paying securities, that is and , see for example Kijima [Kij03].

2.2 Arbitrage

We start with defining the following sets of self-financing trading strategies.

Note that in particular for any

Also, we define

| (2) |

for . We call the set of hedging cash flows initiated at time .

Due to the presence of transaction costs, the sets , generally speaking, are not convex, and for this reason we introduce the following auxiliary sets.

| (3) | ||||

| (4) |

for . We will also refer to as the set of hedging cash flows initiated at time . Moreover, using the fact that the set is a convex cone (see [BCR12]), it is easy to show that the set is also a convex cone.

Let us proceed by defining an arbitrage opportunity in our setting.

Definition 2.7.

An arbitrage opportunity at time for is a cash flow such that for all , and for some .

We say that the no-arbitrage condition holds true at time for if there does not exist an arbitrage opportunity at time for .

Remark 2.8.

Typically, arbitrage is defined as a trading strategy rather than a cash flow. However, in our setting, it is more convenient to work with cash flows, and since each hedging cash flow corresponds to a trading strategy, we take the liberty to define an arbitrage opportunity as a cash flow.

Definition 2.9.

For any fixed , we say that a probability measure is risk-neutral for if , and if for all and all . The set of all risk-neutral measures for will be denoted by

Similarly to the above, we define the set of risk-neutral probabilities, the arbitrage opportunity for set , and no-arbitrage conditions for set . The following two lemmas show that we may formally replace by in Definitions 2.7 and 2.9.

Lemma 2.10.

For any , we have that if and only if , and for all .

Proof.

Fix .

If , then for all .

Hence,

for all and .

Therefore,

for all .

Suppose that , and that for all .

Then, for all and .

Letting proves that .

∎

Lemma 2.11.

For each , the no-arbitrage condition holds true at time for if and only if for each such that , we have .

Proof.

Let us fix .

Assume that is such that . Then, by definition of , there exists and so that . This give us . The no-arbitrage condition holds true at time for , so . Therefore, , which implies .

Suppose that is such that . By assumption, for each such that , we have . From the definition of , this implies that for each , such that , we have . Taking and gives us . ∎

In what follows we shall make use of the following result.

Proposition 2.12.

If , then the no-arbitrage condition holds at time for .

Proof.

We prove by contradiction. Assume that , and that there exists an arbitrage opportunity at time . By the definition of an arbitrage opportunity, , , and for some . Since and , we have that for some . However, this contradicts that . Hence, the no-arbitrage condition holds true at time for . ∎

Next, we introduce some notions that are related to derivatives pricing, and which will be used in Section 3.1. In what follows, for any cash flow we will denote by the discounted cash flow.

Definition 2.13.

Let .

-

•

A set of extended cash flows associated with an -measurable random variable and a process is defined as

-

•

The pricing interval associated with a process and a set of probability measures is defined as

A cash flow in is interpreted as the sum of a position in and a static position of units in the discounted cash flow . In Section 3.1, will have the interpretation of a discounted price of the cash flow .

We will say that is a risk-neutral pricing interval if it is nonempty, and if for each the no-arbitrage condition is satisfied for . That is, is a risk-neutral pricing interval if it is nonempty, and if for each and each such that , we have . If is a risk-neutral pricing interval, we call any a risk-neutral price, the upper no-arbitrage bound, and the lower no-arbitrage bound.

The following lemma gives a necessary condition for to be a risk-neutral pricing interval.

Lemma 2.14.

Let and . If , then is a risk-neutral pricing interval.

Proof.

Fix , , and . Let be a cash flow such that . By definition of , we have that

| (5) |

for some and some -measurable random variable .

2.3 Good-deals

The no-good-deal bound pricing approach was introduced in [CSR00]. This approach assumes that all investors are willing to invest in good deals – trades with high Sharpe ratios – as well as in the arbitrage opportunities, if any. In [Che07b, Che07c], alternative approach to no-good-deal bounds was proposed: these authors suggested using coherent risk measures instead of the Sharpe Ratio. Recently, the notion of conic finance was introduced in [CM10], where a good deal was defined in terms of a family of static coherent risk measures. In the present paper, we extend conic finance to a dynamic setting by defining a good deal in terms of a family of dynamic coherent risk measures (DCAI).

The main tool for building up the theory of Dynamic Conic Finance will be the Dynamic Coherent Acceptability Indices (DCAIs) developed in [BCZ11]. As it was shown in [BCZ11] that any DCAI can be associated with a left-continuous, increasing family of Dynamic Coherent Risk Measures (DCRMs) , and consequently to a family of dynamically consistent sequences of sets of probability measures (see Appendix A for definitions and related results.) In what follows, we fix such a normalized 222A DCAI is said to be normalized if for every and , there exist two portfolios so that and . DCAI , and denote by the corresponding family of DCRMs, and by the corresponding family of dynamically consistent sequences of sets of probability measures.

Definition 2.15.

A good-deal for at time and level is a cash flow such that for some .

Note that a good-deal depends on the family of DCRMs and the level . A cash flow that is a good-deal with respect to a family of DCRMs might not be a good-deal with respect to another family of DCRMs. Also, note that, for a fixed family of DCRMs, a cash flow that is a good-deal at level might not be a good-deal at some other level . Although, since is monotone increasing in , if a cash flow is a good-deal for , then it will also be a good deal for any level . We will also show later that good-deals can be described in terms of the acceptability index associated to family .

Definition 2.16.

We say that the no-good-deal condition (NGD) holds for at time and level if for all and .

We will make the following technical assumption on .

Assumption (B):

For each and , any probability measure is equivalent to , and the set

is closed and convex.

Since is finite and is of full support, the set is bounded. Hence, is compact for all and . In Section 4, we show that a family of densities corresponding to the dynamic Gain-Loss Ratio satisfies this assumption.

Next, we will prove one of the main results of this paper, which is analogous to FTAP.

Theorem 2.17.

The no-good-deal condition (NGD) holds true for at time

and level if and only if .

Proof.

Throughout the proof we fix and .

()

Suppose that .

Since is risk-neutral, it follows that

for all .

Due to Theorem A.5 (Robust Representation of DCRM), we have

for all . Thus, for any , and hence NGD holds true for at time and level .

() Fix and . Let be the set defined in Assumption (B), and let us consider the following set of matrices

Since is compact, by continuity of the mapping

we conclude that is compact in . Also note that, by convexity of and linearity of conditional expectations above w.r.t. , the set is convex.

Let us now define a closed and convex set . We will prove by contradiction that . Towards this end let us assume that . By a version of Hahn-Banach theorem (see Theorem B.3), there exists a linear functional , and such that

| (7) | ||||

| (8) |

for all . From the Riesz representation theorem, there exists such that for all , where for all denotes the Frobenius inner product in . From (8), we have that for all , and therefore, for and .

Since, in view of (7) we have that , we may assume without loss of generality that .

Also in view of (7), we deduce that

for all , where for . Therefore, there exists and an so that

Let us define

Since any is strictly positive and , it follows that

for all . Consequently, taking infimum with respect to and applying Theorem A.5, we get

| (9) |

The set is a convex cone, hence . Thus, in view of (9), the cash flow violates the NGD condition for at time and level , which is a contradiction.

Hence, for all and . Consequently, for each , , the set

is nonempty.

Let us define the following mapping

for any random variable

Since,

we have that . Recall that is compact and hence is closed, and since is continuous, we conclude that is closed.

Now, note that

Therefore, the family of subsets

satisfies the finite intersection property333The family of sets has finite intersection property if is non-empty for any finite .. Since is compact, we have by Lemma B.2 that the set

| (10) |

is nonempty. Hence, there exists an so that for all and . Now, let be a measure corresponding to , so that Using the abstract version of Bayes rule applied to we get

for all . So, in view of Definition 2.9 and Lemma 2.10, we see that Thus, . The theorem is proved. ∎

3 Dynamic ask and bid prices via DCAI

In this section, we derive the dynamic bid and ask prices for a derivative contract via DCAIs. We start by constructing the set of extended cash flows that will be used to derive the good-deal ask and bid prices. Let be a cash flow associated to a derivative contract. For a fixed , , and an -measurable random variable , we define the following sets

| (11) | ||||

| (12) |

where . The pair is interpreted as the set of extended cash flows.

In particular, a cash flow in equals to the sum of a position in the underlying market and a nonnegative static position of units in the discounted cash flow

.

Similarly, a cash flow in equals to the sum of a position in the underlying market444Recall that denotes the set of hedging cash flows initiated at time . and a nonnegative static position of

units in the discounted cash flow .

Similarly to Definition 2.9, we say that a probability measure is risk-neutral for , respectively , if , and for all , respectively for all . Also, we say that the no-good-deal condition holds for , respectively , at time and level , if for all , respectively . We denote by , respectively, , the set of all risk-neutral measures for , respectively .

Remark 3.1.

Note that and are convex cones. Thus, we may replace with or in Theorem 2.17 to prove that NGD holds for , respectively , at time and level if and only if , respectively .

For the sake of brevity, we define the mappings as follows

Next we introduce the main objects of this study – the good-deal ask and bid prices corresponding to a given DCAI :

Definition 3.2.

The discounted good-deal ask and bid prices of a derivative contract , at level , at time are defined as

for all .

Remark 3.3.

We stress that the good-deal prices depend on the choice of DCAI , level , and the set of hedging cash flows . First, we see that, from the monotonicity property of DCAIs (D3), the good-deal ask (bid) price is non-decreasing (non-increasing) in . Secondly, the good-deal ask (bid) price is non-increasing (non-decreasing) in . This is because, as is easily seen, and satisfy

for all .

Remark 3.4.

Remark 3.5.

The discounted good-deal ask price can be interpreted as the minimum amount of cash such that plus the resulting hedging error is acceptable (in the sense of acceptability index ) at least at level . Similarly, the discounted good-deal bid price can be viewed as the maximum amount of cash such that plus the resulting hedging error is -acceptable at least at level .

Remark 3.6.

By Theorem A.6, we have that

for all , , and . Since the cash flows and are discounted, the prices and are also discounted. We took the liberty to denote them by and rather than and (which would agree with earlier notation) to ease exposition.

Proposition 3.7.

For any fixed , , and , the sets

are nonempty for all .

Proof.

The proof will be done by contradiction. Towards this end let us fix , , and .

Suppose that

for all and . By Theorem A.6, we have that

for all and . Since is normalized, there exists such that . Let us define as

Note that, and since , we have that

Next, we see that

for all , , and . From the monotonicity property of , we have that

which contradicts for all . ∎

We close this section with a technical result, which provides a “symmetry” between ask and bid prices, that will be used later.

Lemma 3.8.

For any , , and we have that

Proof.

Using the definitions of and , we have

∎

3.1 Dual representation of good-deal ask and bid prices

We are now in position to prove a representation theorem for the discounted good-deal ask and bid prices. Let us first make the following standing technical assumption

Assumption (C): The mapping is continuous.

In Section 4, we prove that the dynamic Gain-Loss Ratio satisfies this assumption.

We proceed by showing that, for any derivative contract , the prices and have useful representations in terms of the sets and .

Theorem 3.9.

The discounted good-deal ask and bid prices of a derivative contract , at level , at time satisfy

Proof.

In view of Lemma 3.8, it is enough to prove that the theorem holds for . Let , , and . We first show that

Using Theorem A.3 and Lemma B.1, as well as the continuity and monotonicity of the map , we obtain

| (13) |

for all .

Now fix an -measurable random variable , and let be the unique partition that generates . Fix and let . Then for all . Using (13), we have that if and only if

Equivalently,

By property (A2) in Definition A.2 of , it follows that

By Theorem A.5 and property (A6), we deduce that

for any and any nonnegative -measurable random variable . Since is closed under multiplication of nonnegative -measurable random variables, the inequality above is equivalent to

for any and any nonnegative -measurable random variable .

Therefore, by the definition of , we see that

and hence NGD holds for , at time and level . It follows that (see Remark 3.1). Let .

From the definition of , we have that

| (14) |

for all and all nonnegative -measurable random variables . Note that since . Thus, . Because , we may let in (14) to conclude that, if , then there exists such that

Since is arbitrary,

| (15) |

Let us now make a few remarks regarding Theorem 3.9.

Remark 3.10.

If NGD holds false for , at time , at level , then

for all and .

In the next remark, we treat the case in which the markets are frictionless and complete.

Remark 3.11.

If, for , the set of hedging cash flows satisfies the no-arbitrage condition, and is complete (for any , there exists so that ), then it follows from the Fundamental Theorems of Asset Pricing that , for , and . Since , we have that for . By Theorems 2.17 and 3.9, if NGD holds then the good-deal ask and bid prices of a derivative contract , at time and level , satisfy

Notice that, naturally, the good-deal prices no longer depend on the acceptance level .

Remark 3.12.

Let us consider the sets of extended cash flows associated with good-deal prices and :

If is frictionless and complete (and therefore linear), and NGD holds, then as in Remark 3.11, we have that . In this case, the set

is a linear space. Whenever , as in our general case, we have that

is only a convex cone. This is one of the main reasons why we call this approach dynamic conic finance.

3.2 Good-deal forward ask and bid prices

In this section, we define the good-deal forward ask and bid prices, and then prove a representation theorem for them. In this subsection we suppose that the risk-free interest rate is deterministic.

Definition 3.14.

The good-deal ask and bid forward prices, with delivery at time , written at time , of a derivative contract , at level are defined as

| (19) | ||||

| (20) |

for all .

Notice that the cash flow represents an exchange of a cash payment at time for a discounted cash flow that is hedged with . The good-deal forward ask price at level is the minimum amount of cash at time so that is acceptable at level at time .

We now give the representation theorem for the good-deal forward ask and bid prices.

Theorem 3.15.

The good-deal ask and bid forward prices of a derivative contract , with delivery at time , written at time and level , satisfy

Proof.

Remark 3.16.

If is deterministic and the set of hedging cash flows forms a market that is frictionless, complete, and arbitrage-free, then is a singleton, say , and so by Theorem 3.15 we have that . This is compatible with the classic result that states that in a frictionless, complete, and arbitrage-free market the discounted forward price of a derivative contract , with delivery at time , written at time , is given as

where is the discounted risk-neutral spot price given by . Also, from Theorem 3.15, we see that the relationship between the good-deal ask and bid forward prices is classic, in the sense that

4 Pricing with the dynamic Gain-Loss Ratio

In this section, we first prove some auxiliary results that hold for general DCAIs. Then, we particularize these results to the very important special case of DCAI, namely to the dynamic Gain-Loss Ratio (dGLR). Finally, we apply the pricing and hedging results developed in earlier sections using dGLR to path-dependent options. In this section we assume that without loss of generality.

4.1 Characterization of DCAIs

Recall that for every normalized and right-continuous DCAI there exist a family of dynamically consistent sequences of sets of probability measures that is increasing (in ), such that (28) holds (see Appendix A). We say that a family of dynamically consistent sequences of sets of probability measures that is increasing (in ) corresponds to a given normalized and right-continuous DCAI if satisfies (28).

Lemma 4.1.

Suppose that is a normalized and right-continuous DCAI. A family corresponds to if and only if , where 555We will generically denote by a family of dynamically consistent sequences of sets of probability measures that is increasing in .

Proof.

() Let . We fix , , and . Define the set

We may assume that and . Otherwise, it is clear that satisfies (28).

Observe that if , then . So is an upper bound of . If we let , then , and so (28) is satisfied.

Assume . If , then (21) is satisfied because is increasing in .

Next, suppose that and . By Theorem A.3, the mapping

is left-continuous and monotone decreasing. Thus, by left-continuity of , there exists so that . By monotonicity and because satisfies (28), we deduce that . This implies that , which is a contradiction. Hence, we have that (21) holds, and thus . ∎

4.2 Characterization of the dGLR

A performance measures that is very popular among practitioners is the Sharpe Ratio (SR), which was introduced by Sharpe [Sha64]. However, SR is not monotone, and hence not an acceptability index. Moreover, as pointed out by Bernardo and Ledoit [BL00] SR does not respect arbitrage, in the sense that the SR is finite even for cash-flows that exhibit arbitrage opportunities. For this reason, [BL00] proposed the static Gain-Loss Ratio, which is a performance measure that is unbounded for arbitrage opportunities, and, as proved in Cherny and Madan [CM09], is also a static coherent acceptability index. Later, Bielecki et al. [BCZ11] extended the notion of GLR to dynamic setup, and introduced the dynamic Gain-Loss Ratio, defined666By convention, . as follows

| (22) |

It is shown in [BCZ11] that the dGLR satisfies the conditions (D)–(D), and therefore it is a dynamic coherent acceptability index (see Definition A.1).

Remark 4.2.

It is worth to note on the interpretation of the dGLR in the context of arbitrage, which was first noticed in Bernardo and Ledoit [BL00] for the static Gain-Loss Ratio. Observe that

is equivalent to

which is ultimately equivalent to

Therefore, in view of Definition 2.7, a cash flow is an arbitrage opportunity at time if and only if for some . Equivalently, the no-arbitrage condition holds at time if and only if is bounded for all .

In order to apply the general theory developed above, we will find the sets of probability measures that correspond to dGLR. We define a family as

| (23) |

for all , where

Remark 4.3.

-

(i)

For each , the set of densities defined as

is closed and convex. Thus, dGLR satisfies Assumption B.

-

(ii)

For each , the function of defined as

(24) is continuous, and hence dGLR satisfies Assumption C. Indeed, for each we have that

- (iii)

Proposition 4.4.

The family , defined in (23) is an increasing family of dynamically consistent sets of probability measures that corresponds to dGLR.

Proof.

We start by observing that, for each , the set is nonempty since, in particular, we may take in the definition of . Clearly, is increasing in .

For the rest of the proof we fix . We denote by the unique partition of at time that generates . In order to prove our result it suffices to show that is weakly consistent (see Corollary 4.1.1 in [Zha11]), which is

| (25) |

for every , , and . Next, take and suppose that

for some . Applying the tower property of conditional expectations, we deduce that the following implication holds:

Hence, since is arbitrary, we deduce that

for all . Thus, for , we obtain

for all . Therefore,

which proves the weak consistency of .

We now show that the family corresponds to the dGLR. By Lemma 4.1, this is equivalent to show that

| (26) |

for all , and , where for convenience we denoted . In the rest of the proof we fix , and .

4.3 Applications

In this section, using a simple model for ask and bid prices of a stock, and choosing the dGLR as acceptability index, we compute the good-deal ask and bid prices of a European-style Asian option in a market with transaction costs. We compare these good-deal prices with the no-arbitrage bounds. Recall that , defined in (23), is a dynamically consistent family of sets of probability measures that corresponds to the dGLR. We compute the ask and bid prices using the representation result in Theorem 3.9. No-arbitrage price bounds are calculated via using the lower and upper no-arbitrage bounds defined in Section 2.

We suppose that the bid price of the stock is given in Table 1.

The ask price process is assumed to satisfy , where is the transaction costs coefficient. We also define the mid price process as .

We recall that is defined in terms of the reference measure , which we will now assume to be

Example 4.1 (Asian Call Option).

We now compute the ask and bid price of a European-style Asian call option with a strike of 65. According to our two-period model, the derivative contract is defined as

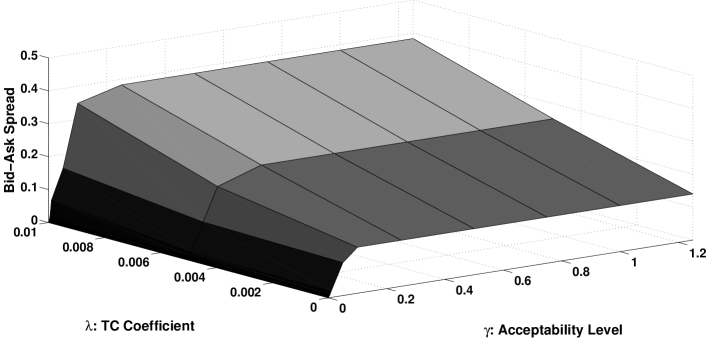

Recall that and denote the good-deal prices computed using the dGLR, whereas and are the upper and lower no-arbitrage bounds, respectively. Our results are presented in Table 2 and Table 3 for different transaction cost coefficients at . The prices displayed in Table 3 correspond to the upper node of the tree, since the prices for the lower node are equal to zero. In Figure 1 we display the “liquidity surface”, which is the plot of good-deal bid-ask spread as a function of the level and transaction costs coefficient at .

| 1.38885 | 1.25003 | 1.48402 | 1.23020 | 1.55003 | 1.16726 | |

|---|---|---|---|---|---|---|

| 0.0001 | 1.34177 | 1.34155 | 1.37681 | 1.37659 | 1.41186 | 1.41163 |

| 0.001 | 1.34274 | 1.34058 | 1.37781 | 1.37560 | 1.41288 | 1.41061 |

| 0.005 | 1.34706 | 1.33628 | 1.38224 | 1.37118 | 1.41742 | 1.40609 |

| 0.01 | 1.35244 | 1.33095 | 1.38776 | 1.36571 | 1.42309 | 1.40047 |

| 0.05 | 1.38885 | 1.28975 | 1.43158 | 1.32344 | 1.46802 | 1.35712 |

| 0.1 | 1.38885 | 1.25003 | 1.48402 | 1.27414 | 1.52322 | 1.30657 |

| 0.25 | 1.38885 | 1.25003 | 1.48402 | 1.23020 | 1.55003 | 1.17523 |

| 0.5 | 1.38885 | 1.25003 | 1.48402 | 1.23020 | 1.55003 | 1.16726 |

| 0.75 | 1.38885 | 1.25003 | 1.48402 | 1.23020 | 1.55003 | 1.16726 |

| 1 | 1.38885 | 1.25003 | 1.48402 | 1.23020 | 1.55003 | 1.16726 |

| 1.25 | 1.38885 | 1.25003 | 1.48402 | 1.23020 | 1.55003 | 1.16726 |

| 5.55541 | 5.00014 | 5.67765 | 5.17512 | 5.79988 | 5.35011 | |

|---|---|---|---|---|---|---|

| 0.0001 | 5.36684 | 5.36648 | 5.50701 | 5.50665 | 5.64718 | 5.64681 |

| 0.001 | 5.36847 | 5.36485 | 5.50866 | 5.50499 | 5.64886 | 5.64513 |

| 0.005 | 5.37568 | 5.35763 | 5.51598 | 5.49767 | 5.65628 | 5.63770 |

| 0.01 | 5.38465 | 5.34864 | 5.52508 | 5.48854 | 5.66551 | 5.62844 |

| 0.05 | 5.45447 | 5.27791 | 5.59591 | 5.41678 | 5.73736 | 5.55566 |

| 0.1 | 5.53722 | 5.19249 | 5.67764 | 5.33012 | 5.79988 | 5.46775 |

| 0.25 | 5.55541 | 5.00014 | 5.67765 | 5.17512 | 5.79988 | 5.35012 |

| 0.5 | 5.55541 | 5.00014 | 5.67765 | 5.17512 | 5.79988 | 5.35011 |

| 0.75 | 5.55541 | 5.00014 | 5.67765 | 5.17512 | 5.79988 | 5.35011 |

| 1 | 5.55541 | 5.00014 | 5.67765 | 5.17512 | 5.79988 | 5.35011 |

| 1.25 | 5.55541 | 5.00014 | 5.67765 | 5.17512 | 5.79988 | 5.35011 |

|

In Figure 1, it is apparent that the good-deal bid-ask spread is increasing both in the acceptance level and in the transaction cost coefficient . The good-deal bid-ask spread naturally increases in because of the representations in Theorem 3.9, and since is increasing in . On the other hand, the good-deal bid-ask spread, as well as the difference between the upper and lower no-arbitrage bounds, increases in since hedging the claim becomes more expensive as the increases.

We also note from Table 2 that both no-arbitrage bounds and the good-deal prices increase in , and that the good-deal ask and bid prices converge to the no-arbitrage bounds at higher values. This is also due to the fact that hedging is more expensive as increases. For example, in case , and approximately converge to and , respectively, at , whereas if this happens at approximately , and in the case it happens at approximately .

Appendix A Dynamic coherent acceptability indices

In this section, we provide some useful background information about acceptability indices and risk measures, as studied in [CM09] and [BCZ11]. Investors are usually concerned with finding satisfactory balance between reward and risk associated with an investment process. Various measures have been developed to quantify this balance. Such measures are typically referred to as performance measures or measures of performance. Cherny and Madan [CM09] originated an effort to provide a mathematical framework to study these measures in a unified way for static models, and Bielecki et al. [BCZ11] followed up with an extension to a dynamic set-up.

A very popular measure of performance is the Sharpe Ratio introduced by [Sha64]. The Sharpe Ratio is expressed as the ratio of expected excess return to standard deviation, and thus in financial applications it measures expected excess return of a portfolio in units of portfolio’s standard deviation. It has been used as a classical tool to rank portfolios according to their “reward-to-risk” characteristics.

Using standard deviation to quantify risk is considered to be the major drawback of Sharpe Ratio because positive returns also contribute to this measure of risk. To eliminate this unwanted feature other ratio-types performance measures that consider the downside risk were proposed, such as Sortino Ratio, [SP94], and Gain Loss Ratio (GLR), [BL00]. Another popular generalization of the Sharpe Ratio is provided by the Risk Adjusted Return on Capital, which is constructed as a ratio of mean excess return to some selected measure of risk.

All the performance measures mentioned above share some common desirable features: they are unit-less, they are increasing functions of reward and decreasing functions of risk; moreover, according to these performance measures diversification of a portfolio improves its performance. This observation prompts a natural desire to study performance measures in a unified mathematical framework. As already mentioned, such a study was recently originated by [CM09]. The study of [CM09] was done in a static, one-time period setup, and the authors coined the term acceptability index as a mathematical terminology for a performance measure. In [BCZ11], this static mathematical framework for studying acceptability indices was elevated to a dynamical, multi-period setup, where cash flows are considered as random processes and acceptability is assessed consistently in time. In particular, they measure the performance of the total cumulative terminal value of the cashflow as seen from the initial time of the investment process, and also all remaining cumulative cashflows between each intermediate time and the terminal time of the investment process.

We proceed by recalling definitions and results from the theory of Dynamic Coherent Acceptability Indices, that were studied in Bielecki et al. [BCZ11].

We first recollect the definition of a dynamic coherent acceptability index.

Definition A.1.

A dynamic coherent acceptability index (DCAI) is a function that satisfies the following properties:

-

(D1)

Adaptiveness. For any and , is -measurable;

-

(D2)

Independence of the past. For any and , if there exists such that for all , then ;

-

(D3)

Monotonicity. For any and , if for all and , then for all ;

-

(D4)

Scale invariance. for all and ;

-

(D5)

Quasi-concavity. If and for some , , , and , then for all ;

-

(D6)

Translation invariance. for every , , , and every -measurable random variable ;

-

(D7)

Dynamic consistency. For any and , if for all , and there exists a non-negative -measurable random variable such that for all , then for all .

Property (D1) is a natural property in a dynamic setup and it assumes that a DCAI is adapted to the same information flow as is any cash flow .

(D2) postulates that in the dynamic context the current measurement of performance of a cash flow only accounts for future payoffs. To decide, at any given point of time, whether one should hold on to a position generating the cash flow , one may want to compare the measurement of the performance of the future payoffs (provided by DCAI at this point of time) to already known past payoffs.

Properties (D3)-(D5) are naturally inherited from the static case.

Translation invariance (D6) implies that if a known dividend is added to at time (today), or at any future time , then all such adjusted cashflows are accepted today at the same level.

Dynamic consistency (D7) is the property in the dynamic setup which relates the values of the index between two consecutive days in a consistent manner. It can be interpreted from financial point of view as follows: if a portfolio has a nonnegative cashflow today, then we accept this portfolio today at least at the same level as we would accept it tomorrow; similarly, if the today’s cashflow is nonpositive the acceptance level today can not be larger than the level of acceptance tomorrow.

For technical reasons, we assume that for every DCAI , and for every and , there exists two portfolios such that and . In this case, we say that the DCAI is normalized. Assuming that is normalized excludes degenerate examples of acceptability indices such as a constant index over all states, times, and portfolios.

Let us proceed by stating with the definition of a dynamic coherent risk measure.

Definition A.2.

Dynamic coherent risk measure (DCRM) is a function that satisfies the following properties:

-

(A1)

Adaptiveness. is -measurable for all and ;

-

(A2)

Independence of the past. If for some , , and and for all , then ;

-

(A3)

Monotonicity. If for some and , and for all and , then for all ;

-

(A4)

Homogeneity. for all , and ;

-

(A5)

Subadditivity. for all , , and ;

-

(A6)

Translation invariance. for every , , -measurable random variable , and all ;

-

(A7)

Dynamic consistency.

for every , and .

We want to mention that our definition of DCRM differs from the definition given in previous studies essentially only by the dynamic consistency property. For sake of completeness, we will present here how property (A7) relates to other forms of dynamic consistency of risk measures (for processes).

-

(A7-I) If , and for some , and , then ;

-

(A7-II) for all times and positions .

-

(A7-III) for all ,

-

(A7-IV) for all ,

-

(A7-V) if , and for some and , then .

Property (A7-I) is the dynamic consistency property for DCRM defined by [Rie04]. Property (A7-II) is the version of the dynamic programming principle (also called recursiveness), introduced by [CDK2006]. Properties (A7-I) and (A7-II) are equivalent, and they are also sometimes called strong dynamic consistency property. To the best of our knowledge, properties (A7-III) and (A7-IV) were first introduced in the context of random processes by [AFP10], and they were called acceptance and rejection consistency, respectively. In the same paper, Acciaio, Föllmer and Penner introduced condition (A7-V) and they called it weakly acceptance consistent.

It is straightforward to show that the dynamic consistency condition (A7) is stronger than (A7-V), and it is weaker than (A7-I) or (A7-II). Also note that since conditions (A7-II) and (A7-III) taken together are equivalent to (A7-II), then, taken together they imply (A7). However, the inverse implication is not necessarily true.

We now recall an important result that provides the representation of a DCAI in terms of a family of DCRMs, and the representation of DCRM in terms of a DCAI. The proof the following theorem can be found in [BCZ11].

Theorem A.3.

-

(i)

If is a normalized, right-continuous, dynamic coherent acceptability index, then there exists a left-continuous and increasing family of dynamic coherent risk measures

, such that(27) -

(ii)

If is a left-continuous and increasing family of dynamic coherent risk measures, then there exists a right-continuous and normalized dynamic coherent acceptability index such that,

We take and .

Next, we recall the definitions of a dynamically consistent sequence of sets of probability measures and an increasing family of sequences of sets of probability measures.

Definition A.4.

-

(i)

A sequence of sets of probability measures absolutely continuous with respect to is called dynamically consistent with respect to the filtration if the sequence is of full-support and the following inequality holds

for all , , and -measurable random variables .

-

(ii)

A family of sequences of sets of probability measures is called increasing if , for all and .

Now, we recall a representation theorem for dynamic coherent risk measures in terms of dynamically consistent set of probabilities. These results, combined with the results from Theorem A.3 about duality between DCAI and DCRM, gives a representation theorem for dynamic coherent acceptability indices.

Theorem A.5 (Robust Representation Theorem for DCRM).

For , a function is a dynamic coherent risk measure if and only if there exists a dynamically consistent family of sets of probabilities such that,

| (28) |

The proof this theorem can be found in [BCZ11].

A direct consequence of Theorem A.3 and Theorem A.5, is the following result, which is proved in [BCZ11].

Theorem A.6.

-

(i)

Assume that is an increasing family of dynamically consistent sequences of sets of probability measures. Then, the function defined as follows,

is a normalized and right-continuous dynamic coherent acceptability index.

-

(ii)

If is a normalized and right-continuous dynamic coherent acceptability index, then there exists a family of dynamically consistent sequences of sets of probability measures such that

Here we adopt the usual convention that and .

Appendix B Technical results

The following lemma is an auxiliary result needed for Theorem 3.9.

Lemma B.1.

For any monotone increasing, continuous function , we have that

for any .

Proof.

Let us define the set . Assume that for some . Then, , and therefore .

Conversely. Suppose that and define . If , then for all , and in particular for . Now assume that . We first argue by contradiction that . If , then . Now, since is continuous, there exists so that . By the definition of the supremum of a set, we have that, for all , there exists so that . Therefore, because is monotonically increasing, . Hence, , which contradicts . We proceed by showing that . Since and is monotonically increasing, we have that . However, , so . ∎

We now recall a well-known characterization of compact sets. For a proof, see Lemma I.5.6 in Dunford and Schwartz [DS58].

Lemma B.2.

A subset of a topological space is compact if and only if every family of closed sets with the finite intersection property has a nonempty intersection.

The following theorem is an application of Hahn-Banach theorem, regarding the separation of hyperplanes.

Theorem B.3.

If and are disjoint closed convex subsets of , and if is compact, then there exists a constant with , and a continuous linear functional , so that

for all and .

Proof.

By Theorem V.2.10 in Dunford and Schwartz [DS58], there exists constants and with , and a continuous linear functional , so that

| (29) |

for all and . We now argue that for all . Suppose there exists and so that . Since is a cone, we have that for all . Thus,

which contradicts (29), and hence . From here, and since is linear and , it follows that . Thus, , and hence . Taking concludes the proof. ∎

References

- [AFP10] Acciaio, B., H. Föllmer and I. Penner (2010): Risk Assessment for Uncertain Cash Flows: Model Ambiguity, Discounting Ambiguity, and the Role of Bubbles. Finance Stoch., 16(4):669–709, 2012.

- [AF11] T. Arai and M. Fukasawa. Convex risk measures for good deal bounds. Preprint, 2011.

- [BCR12] T.R. Bielecki, I. Cialenco, and R. Rodriguez. No-arbitrage pricing theory for dividend-paying securities in discrete-time markets with transaction costs. Preprint, 2012.

- [BCZ11] T.R. Bielecki, I. Cialenco, and Z. Zhang. Dynamic coherent acceptability indices and their applications to finance. forthcoming in Math. Finance, 2011.

- [BL00] A. Bernardo and O. Ledoit. Gain, loss, and asset pricing. J. of Polit. Econ., 108:144–172, 2000.

- [BN09] J. Bion-Nadal. Bid-ask dynamic pricing in financial markets with transaction costs and liquidity risk. Journal of Mathematical Economics, 45(11):738–750, December 2009.

- [BS06] T. Bjork and I. Slinko. Towards a general theory of good-deal bounds. Review of Finance, 10(2):221–260, 2006.

- [Car09] R. Carmona, editor. Indifference pricing. Princeton Series in Financial Engineering. Princeton University Press, Princeton, NJ, 2009. Theory and applications.

- [CGM01] P. Carr, H. Geman, and D.B. Madan. Pricing and hedging in incomplete markets. J. Finan. Econ., 62(1):131–167, 2001.

- [CDK2006] Cheridito, P., F. Delbaen, and M. Kupper. Dynamic Monetary Risk Measures for Bounded Discrete-time Processes. Electron. J. Probab., 11(3): 57-106, 2006.

- [Che07a] A. Cherny. General arbitrage pricing model: I – probability approach. In Catherine Donati-Martin, Michel Émery, Alain Rouault, and Christophe Stricker, editors, Séminaire de Probabilités XL, volume 1899, pages 415–445. Springer Berlin / Heidelberg, 2007.

- [Che07b] A.S. Cherny. Pricing and hedging European options with discrete-time coherent risk. Finance Stoch., 11(4):537–569, 2007.

- [Che07c] A.S. Cherny. Pricing with coherent risk. Theory Probab. Appl., 52(3):506–540, 2007.

- [CM06] A.S. Cherny and D.B. Madan. Pricing and hedging in incomplete markets with coherent risk, 2006.

- [CM09] A.S. Cherny and D.B. Madan. New measures for performance evaluation. Rev. Finan. Stud., 22(7):2571–2606, 2009.

- [CM10] A. Cherny and D.B. Madan. Markets as a counterparty: An introduction to conic finance. Int. J. Theor. Appl. Finance, 13(08):1149–1177, 2010.

- [CSR00] J. Cochrane and J. Saa-Requejo. Beyond arbitrage: Good deal asset price bounds in incomplete markets. Journal of Policital Economy, 108:79–119, 2000.

- [DMW90] R.C. Dalang, A. Morton, and W. Willinger. Equivalent martingale measures and no-arbitrage in stochastic securities market models. Stochastics Stochastics Rep., 29(2):185–201, 1990.

- [DS58] N. Dunford and J.T. Schwartz. Linear Operators. I. General Theory. Interscience Publishers, New York, NY, USA, 1958.

- [DS94] F. Delbaen and W. Schachermayer. A general version of the fundamental theorem of asset pricing. Math. Ann., 300:463–520, 1994.

- [DS96] F. Delbaen and W. Schachermayer. The fundamental theorem of asset pricing for unbounded stochastic processes. Mathematische Annalen, 312:215–250, 1996.

- [HP81] J.M. Harrison and S.R. Pliska. Martingales and stochastic integrals in the theory of continuous trading. Stochastic Process. Appl., 11(3):215–260, 1981.

- [JK95] E. Jouini and H. Kallal. Martingales and arbitrage in securities markets with transaction costs. J. of Econ. Theory, 66(1):178–197, 1995.

- [JK01] S. Jaschke and U. Kuchler. Coherent risk measures and good-deal bounds. Finance Stoch., 5(2):181–200, 2001.

- [JS98] J. Jacod and A.N. Shiryaev. Local martingales and the fundamental asset pricing theorems in the discrete-time case. Finance Stoch., 2(3):259–273, 1998.

- [Kij03] M. Kijima. Stochastic processes with applications to finance. Chapman & Hall/CRC, Boca Raton, FL, 2003.

- [KK94] Y.M. Kabanov and D.O. Kramkov. No-arbitrage and equivalent martingale measures: an elementary proof of the Harrison–Pliska theorem. Theory Probab. Appl., 39(3):523–527, 1994.

- [KRS02] Y.M. Kabanov, M. Rásonyi, and C. Stricker. No-arbitrage criteria for financial markets with efficient friction. Finance Stoch., 6(3):371–382, 2002.

- [KS01a] Y.M. Kabanov and C. Stricker. The Harrison–Pliska arbitrage pricing theorem under transaction costs. J. Math.Econom., 35(2):185–196, 2001.

- [KS01b] Y.M. Kabanov and C. Stricker. A teachers’ note on no-arbitrage criteria. In Séminaire de Probabilités, XXXV, volume 1755 of Lecture Notes in Math., pages 149–152. Springer Berlin, 2001.

- [KS07] S. Klöppel and M. Schweitzer. Dynamic utility-based good deal bounds. Statistics and Decisions, 25:285 309, 2007.

- [MPS11] D.B. Madan, M. Pistorius, and W. Schoutens. The valuation of structured products using Markov chain models. Quantitative Finance, 2011.

- [MS11a] D.B. Madan and W. Schoutens. Conic coconuts: the pricing of contingent capital notes using conic finance. Mathematics and Financial Economics, 4(2):87–106, 2011.

- [MS11b] D.B Madan and W. Schoutens. Structured products equilibria in conic two price markets. Preprint, 2011.

- [Pli97] S.R. Pliska. Introduction to Mathematical Finance: Discrete Time Models. Blackwell Publishers, first edition, 1997.

- [PSC10] M.Ç. Pinar, A. Salih, and A. Camci. Expected gain-loss pricing and hedging of contingent claims in incomplete markets by linear programming. European Journal of Operational Research, 201(3):770–785, 2010.

- [RGS12] E. Rosazza Gianin and E. Sgarra. Acceptability indexes via -expectations: an application to liquidity risk. Preprint, 2012.

- [Rie04] F. Riedel (2004): Dynamic Coherent Risk Measures. Stochastic Process. Appl., 112(2): 185–200, 2004.

- [Rog94] L.C.G. Rogers. Equivalent martingale measures and no-arbitrage. Stochastics Stochastics Rep., 51(1-2):41–49, 1994.

- [RSE05] B. Roorda, J.M. Schumacher, and J. Engwerda. Coherent acceptability measures in multiperiod models. Math. Finance, 15(4):589–612, 2005.

- [Sch92] W. Schachermayer. A Hilbert space proof of the fundamental theorem of asset pricing in finite discrete time. Insurance Math. Econom., 11(4):249–257, 1992.

- [Sch04] W. Schachermayer. The fundamental theorem of asset pricing under proportional transaction costs in finite discrete time. Math. Finance, 14(1):19–48, 2004.

- [Sha64] W.F. Sharpe. Capital asset prices: A theory of market equilibrium under conditions of risk. Journal of Finance, 19:425–442, 1964.

- [SP94] F. A. Sortino and L. N. Price (1994): Performance Measurement in a Downside Risk Framework. The Journal of Investing, 3(3), 59–64.

- [Sta04] J. Staum. Fundamental theorems of asset pricing for good deal bounds. Mathematical Finance, 14(2):141–161, 2004.

- [Sta07] J. Staum. Incomplete markets. In J. R. Birge and V. Linetsky, editors, Handbooks in Operations Research and Management Science, volume 15, pages 511–563. Elsevier, 2007.

- [Zha11] Z. Zhang. Dynamic Coherent Acceptability Indices and their Application in Finance. PhD thesis, Illinois Institute of Technology, 2011.