Error estimates for binomial approximations of game put options

Abstract.

A game or Israeli option is an American style option where both the writer and the holder have the right to terminate the contract before the expiration time. As [9] shows the fair price for this option can be expressed as the value of a Dynkin game. In general, there are no explicit formulas for fair prices of American and game options and approximations are used for their computations. The paper [17] provides error estimates for binomial approximation of American put options and here we extend the approach of [17] in order to obtain error estimates for binomial approximations of game put options which is more complicated as it requires us to deal with two free boundaries corresponding to the writer and to the holder of the game option.

Key words and phrases:

game options, put options, binomial approximations, Dynkin games2000 Mathematics Subject Classification:

Primary 91B28: Secondary: 60G40, 91B301. Introduction

A put option on a stock can be interpreted as a contract between a holder and a writer which allows the former to claim from the latter at an exercise time the amount where is a fixed amount called the option’s strike, is the stock price at time and . In the American options case its holder has the right to choose any exercise time before the contract matures while in the game options case the contract writer also has the right to terminate it at any time before its maturity but then he is required to pay a cancellation fee in addition to the payoff above.

The fair price of American options and of game options is defined as the minimal amount the writer needs to construct a self-financing portfolio which covers his obligation to pay according to the option’s contract. It is well known that in the American options case the fair price can be obtained as a value of an appropriate optimal stopping problem while for game options we have to deal with an optimal stopping (Dynkin) game (see [9]). In general, both for American options and, even more so, for game options with finite maturity explicit formulas for their price are not available and approximation methods come into the picture while estimates of their errors become important. One of most easily implemented methods is the binomial approximation of stock prices modelled by the geometric Brownian motion and [17] provided corresponding error estimates for American put options. In the present paper we extend this approach in order to provide error estimates of binomial approximations for game put options. We observe that for perpetual game options some explicit formulas can be obtained (see [15]) but the finite maturity case studied here seems to be more realistic.

Approximating the Brownian motion by appropriately normalized sums of Bernoulli random variables the paper [17] provided (error) estimates const and const for the difference between the price of an American put option and the price of its corresponding th binomial model approximation. Using again the binomial approximation of the Brownian motion as above we construct in this paper two approximating procedures such that the difference between the price of a game put option and its th approximation in the first procedure is between const and const and in the second procedure is between const and const. The error estimates here are somewhat worse than in the case of American put options which is due to the lack of a smooth fit on the boundary of the writer’s stopping region which causes substantial difficulties in the study of regularity of payoff functions.

We observe that specific properties of game put options had to be used in order to obtain error estimates with the above precision. For instance, when payoffs are path dependent (and not only dependent on the present value of the stock) [10] provides error estimates of similar binomial approximations only of order . Since price functions of game options can be represented as solutions of doubly reflected backward stochastic differential equations the results of [4] are also related to game options approximations. Nevertheless, approximations in [4] are not by binomial models, where computations can be done by means of the effective dynamical programming algorithm (see [10]), but by time discretizations, and so relevant probability space and -algebras remain infinite which prevents effective computations. Furthermore, error estimates in [4] applied to our situation are of order , i.e. they are worse than for binomial approximations which we construct here for the specific case of game put options.

Our exposition proceeds as follows. In Section 2 we provide basic results concerning game put option price functions, introduce our approximation processes and formulate our main result Theorem 2.1. In Section 3 we show that the price function can be represented as a solution of a variational inequality problem closely related to the Stefan problem (see [11]). We then use this representation to study regularity properties of the price function near the free boundary of the option’s holder exercise region. In Section 4 we study the price function near the boundary of the exercise region of the writer. We use the information about this region from [14] in order to represent the price function as an explicit solution of the heat equation. This representation enables us to understand better the behavior of the price function near the boundary. We estimate also the rate of decay of the price function when the initial stock price tends to infinity. Section 5 is devoted to the proof of Theorem 2.1. Finally, in Section 6 we exhibit some computations of the price functions and of the free boundaries.

2. Preliminaries and main results

The Black–Scholes (BS) model of a financial market consists of two assets among which one is nonrisky and the other one is risky. A nonrisky asset is called a bond and its price at time is given by the formula where is interpreted as the interest rate. A risky asset is called a stock and its price at time is determined by a geometric Brownian motion

| (2.1) |

where is called volatility and is a standard Brownian motion defined on a complete probability space . If we write also for . The fair price of an American put option at time with a strike (price) and a maturity (horizon) time can now be written as a function of time and the current stock price having the form (see, for instance, [13]),

| (2.2) |

where denotes the set of all stopping times of the Brownian filtration with values in the interval and is the expectation with respect to the measure . If we set , and then we can rewrite (2.2) in the form

| (2.3) |

Relying on [9] (see also [15], [16] and [14]) we can also write the fair price of a game put option at time with a strike price , a maturity time and a constant penalty as a function of time and the current stock price in the form

| (2.4) |

where and is the indicator of an event . Using the functions and as above we can rewrite this formula in the form

| (2.5) |

It follows also (see [18], [9], [14], [16]) that the saddle point (optimal) stopping times for the game value expressions (2.4) and (2.5) are given by

| (2.6) | |||

Next, we introduce our binomial approximations of the Brownian motion

where are independent indentically distributed (i.i.d.) random variables taking on values 1 and -1 with probability and denotes the integral part of a number . It is convenient to view as defined on the sequence space by the formula if . Then will be defined on the probability space where is the product measure and is generated by cylinder sets.

Now set which is the price of the American put option with a maturity and a strike provided the initial stock price is . It is easy to see that if the penalty then it does not make sense for the writer to cancel the corresponding game put option (see Lemma 3.1 in [16]), and so in this case the prices of American and game options are the same, i.e. . Since approximations of American options were studied in [17] we assume in this paper that . Observe that is continuous in and it is strictly decreasing to 0 as increases to , and so for each there exists a unique such that . Furthermore, we can define to be the minimal such that and set . In order to define two sequences of functions and which will approximate we set , and introduce stopping times

| (2.7) |

where if the infimum above is taken over the empty set and we set . Introduce a filtration where is the trivial -algebra and is generated by . Denote by the set of all stopping times with respect to the filtration taking on value in the set . Then, clearly, . Now, for we define

| (2.8) |

and for we set

| (2.9) |

The second approximation function is defined for all by

| (2.10) |

Setting we formulate now our main result.

2.1 Theorem.

For each there exists such that for all ,

| (2.11) |

Observe that appearing in Theorem 2.1 is defined via and which can be obtained only knowing precise price function of the American put option with the initial stock price equal . But from the computational point of view we can obtain only approximately using, for instance, the algorithm from [17]. One of the ways to overcome this difficulty is to proceed as follows. Let denotes the -th binomial approximation of obtained in [17] which uniformly in satisfies

| (2.12) |

for some . Denote by the minimal such that taking if this inequality does not hold true for all . Set which unlike can be computed employing [17]. It is well known that exists (see, for instance, [17]) and, clearly, this derivative is nonpositive. In fact, it is possible to show that

| (2.13) |

This together with (2.12) yields that

| (2.14) |

From the definitions (2.8)–(2.10) it follows that for each there exists independent of such that

| (2.15) |

Now we obtain from Theorem 2.1 together with (2.14) and (2.15) the following

2.2 Corollary.

For each there exists such that for all ,

| (2.16) |

In the following sections we will analyze regularity properties of the price function of game put options and will complete the proof of Theorem 2.1 in Section 5 providing some computations in Section 6. The general strategy of the proof resembles that of [17] but the study of the price function of game put options is more complicated than in the American options case, in particular, because of appearance of two exercise boundaries (holder’s and writer’s) having different properties. Our proof will be based on regularity properties of solutions of parabolic partial diferential equations with free boundary and of the corresponding variational inequalities and we will rely also on some prior results from [17], [15] and [14].

3. Price function near the holder’s exercise boundary

3.1. Some previous results

3.1 Proposition.

(i) There exists an increasing function such that

and for all satisfying

.

(ii) There exists such that for every there is a so that for and for we have for all .

(iii) Furthermore,

for all

In particular, is of class , i.e. continuously differentiable once with respect to and twice with respect to , and so, in fact, it is a smooth function there.

(iv) Finally, is convex and strictly decreasing in and nonincreasing in .

Next, we introduce an operator which acts on Borel functions on by

| (3.1) |

Clearly, can be viewed as a discretization of the differential operator . We will rely on the following results from [17] concerning the operator .

3.2 Proposition.

For each Borel function on there exists a martingale with respect to the filtration such that and for every ,

| (3.2) |

3.3 Proposition.

Let and . Assume that is a function on . Then

| (3.3) |

where

We will need also the following result concerning the free boundary of the holder exercise region of our game put option which in the case of American options appears as Proposition 1 in [17] and it can be proved for game options in the same way.

3.4 Proposition.

Let and let then .

We also observe that it follows from the Berry-Esseen estimate (see [19]) that for some constant independent of and ,

| (3.4) |

We will also rely on the following standard bounds on derivatives of solutions of 2nd order parabolic equations with constant coefficients (see, for instance, [3] and [5]).

3.5 Proposition.

Let and let be a solution in of the following parabolic equation

Suppose that for all and that there exists such that for all . Then for every and there exists such that

| (3.5) |

3.2. Price function and variational inequalities

Next, we will show that the price function of the game put option can be represented as a solution of a variational inequality (v.i.) problem which is a generalization of the Stefan problem (see [11] ,VIII). This will enable us to derive certain regularity properties of this price function which we will use later on. Details of some of the proofs concerning the solutions of the v.i. problem below which are similar to the proofs in the case of the Stefan problem will not be given here. For the corresponding results in the American put option case we refer the reader to [13], [17] and to references there.

Let be such that and set

| (3.6) |

Using the maximum principle, properties of price functions of American and game put options and the fact that after time the price functions of the game and American option are the same we obtain that for every the time derivative is strictly negative and we can find satisfying such that for some constant ,

| (3.7) |

Relying on Proposition 3.1(iii) we also observe that for all ,

| (3.8) | |||

Let be such that . Introduce the domain and for all in the closure of define the functions

| (3.9) |

We obtain that

| (3.10) |

and from the definition of it follows that for any ,

| (3.11) | |||

Since and are bounded we obtain that the integrability properties of the first and second order derivatives of and are the same in . Now set

| (3.12) |

| (3.13) |

It follows from (3.8) and (3.9)–(3.10) that on the set ,

| (3.14) |

and on the set we obtain

| (3.15) |

Hence we arrive at the following (see [11]).

3.6 Lemma.

The function is the unique solution of the following variational inequality

problem.

v.i. Problem 1: Find such that

(i)

(ii) a.s for every .

(iii) for .

(iv) for .

(v) for .

Proof.

We shall prove uniqueness, the fact that is a solution to v.i. Problem 1 follows from (3.9)-(3.15). Assume that and are two solutions of v.i. Problem 1. Since (property (i)) we can use the property (ii) of and replace by . Since both of them are solutions we obtain that

| (3.16) |

Define the parabolic boundary as the boundary of without the interval and let . Note that is zero on the parabolic boundary and the sum of the two inequalities (3.16) is

| (3.17) |

Integrating both sides of (3.17) on we obtain four terms on the left side. For the first term we have

Integration by parts of the second term and the fact that on the parabolic boundary yields

| (3.18) |

For the third term note that and that for every , and so

The last term satisfies since . We conclude that the left side of (3.17) can not be negative and so it must be zero. Since all terms in the left hand side of (3.17) are non-negative and their sum is equal to 0 we obtain that , and so almost everywhere (a.e.). Hence, a.e., and so there is only one continuous solution. ∎

Denote parts of the boundary of by

and set

| (3.19) |

Thus, is a parabolic boundary of . For every we define following functions.

-

(1)

A smooth function on such that for and for where satisfies and for .

-

(2)

A smooth function satisfying

-

(3)

with defined in (3.12).

-

(4)

A smooth function such that and for some ,

Set which is a Lipschitz continuous function and for every constant there is such that whenever and . Let be a function on satisfying

and, moreover, relying on Chapter 3 in [5] we can choose so that

-

(1)

for some (in fact for each ) and we refer the reader to Chapter 3 in [5] for the definition of and for conditions yielding that a function defined only on the boundary can be extended to a function from .

-

(2)

at the points and .

By the theory of semi-linear parabolic equations (see [5]) there exist a function for some such that

| (3.20) |

In particular are continuous on .

Let . By differentiating with respect to the equation (3.20) and taking into account (3.12), (3.20) and the properties of we obtain that

We see that in the function is a solution to a parabolic equation and since we can use the maximum principle

| (3.22) |

Therefore in order to bound the function we only need to bound its values on the parabolic boundary. First, we estimate the left hand side of (3.22). For we have that , and so . In view of (3.7), (3.10) and the definition of above there exists such that for every ,

On the interval we have and since we see that . Since on this interval we obtain

Hence, on . We obtain next that,

It follows that

Next, we estimate the right hand side of (3.22). On we have that

where is a constant independent of , and so

We conclude that there are some constants and such that for every ,

| (3.23) |

Since and for we deduce that and because is uniformly bounded it follows that is also uniformly bounded. By the properties of we see that

| (3.24) |

Let be an upper subrectangle of where is the same as in the definition of the function in (4). From the definition we have in and since is nonnegative, we obtain that , and so

This means that on the function satisfies the parabolic equation

For and we also have that

Next, let be a function on such that

and all of its first and second order derivatives are bounded there. Such a function exists since we can choose a smooth function on the remaining part of the parabolic boundary of which extends as a smooth function to the whole , and then use Theorem 12 from Chapter 3 in [11]. For each we define in the domain where . Then for every . Fix , then by Proposition 4.5 from Section 4.1 of [11] we obtain that for every where a constant is independent of . Since we assume that for it follows that (for every ). Let , then by Theorem in chapter 3 of [5] we obtain that for every (and in fact every ) and there is a constant independent of such that

In particular, we get

| (3.25) |

Considering again the whole region we have

Hence,

Since all terms in the right hand side are uniformly bounded there is a constant independent of such that for every . Now we see that in the equation

all terms in the right hand side are uniformly bounded and therefore the term in the left is uniformly bounded, as well.

We summarize this in the following lemma.

3.7 Lemma.

There are constants such that for every ,

We now obtain the following (see [11]).

3.8 Proposition.

For any and , as weakly in . Furthermore, uniformly on and also uniformly in for each . The function is the unique solution of v.i. Problem 1.

Next, we analyze properties of second order derivatives starting with the following result.

3.9 Lemma.

There is a constant such that for any ,

Proof.

Set and . Multiply the equation (3.2) by to obtain

Integrating this equation over and recalling that and are non-negative we obtain that for any ,

| (3.26) |

By (3.20) and (3.23) we estimate the third term in (3.26),

For the second term in (3.26) we see that

Since and the function is uniformly bounded in we see in view of (3.25) that is uniformly bounded near the boundary and while for some constant independent of . Thus, we conclude from (3.26) that

for some independent of . Integrating the last equation over we obtain

Since the function is uniformly bounded it follows that there is independent of such that

∎

We will now deal with the properties of the function .

3.10 Lemma.

There is a constant such that for any and every ,

Proof.

Set and . Multiplying (3.2) by the function we have

and an integration with respect to over yields

| (3.27) |

Fix some . Since we see that

From (3.25) it follows that for some constant independent of , and so we obtain

| (3.28) | |||

Now we deal with the last term in (3.27). Since and we obtain that

We plug this inequality into (3.28) and obtain

Integrate the last inequality with respect to over the interval to obtain

Next, integrating in over the interval for some and taking into account that by the property (2) of we obtain that

| (3.29) | |||

Now, by (3.23), (3.24) and Lemma 3.9 together with the Cauchy–Schwarz inequality we estimate the right hand side of (3.29) by a constant independent of . Hence,

and Lemma 3.10 follows. ∎

As a corollary of previous results we obtain

3.11 Proposition.

Let and . Define . Then

| (3.30) |

where by definition is the set of all the functions in with an weak second order derivatives. Also there exists such that for every ,

| (3.31) |

Proof.

From Lemma 3.10, Lemma 3.9 and Lemma 3.7 we obtain that are uniformly bounded in and so they have a weak limit . Since uniformly we must have that , and so . Since is the solution of (3.15) we can apply Proposition 3.5 and using the fact that the constant in (3.5) doesn’t depend on we can obtain in a similar way that for a fixed there is a constant such that for every ,

From (3.11) we can deduce the same result for the function . ∎

3.12 Corollary.

For each the function is Holder continuous with a Holder exponent .

Proof.

For every Proposition 3.11 gives us that . Hence, the result is a consequence of the Sobolev inequality. ∎

3.13 Corollary.

For every the functions and as functions of are continuous in the closed interval .

Proof.

3.14 Corollary.

Let and . Define and . Then

| (3.32) |

and there exists such that for every ,

| (3.33) |

4. Price function near the writer’s exercise boundary

4.1. Regularity properties of price function

Let be the price function of the put game option (see Section 2). We begin this section by showing that near the writer’s exercise region the function is continuous. Let

| (4.1) |

which is a non homogeneous in time Markov process in where and . Let

| (4.2) |

which is the infinitesimal generator of when considered on the space of all functions. This is a parabolic operator with bounded smooth coefficients in the domain

| (4.3) |

where . Let and be the probability and the corresponding expectation for the Markov process starting at the point . We will first show that for any ,

| (4.4) |

where and for any closed set we set to be the arrival time at the set for a Markov process under consideration which is here. Indeed, choosing an appropriate nonnegative function on the boundary and relying on Chapter 3 in [5] we can choose which solves the equation in and equals 1 on the boundary part for while decaying smoothly to when grows to . Then

and so

Next let and . Recall that the price of a put game option with an expiration time and a constant penalty can be written in the form

where and for any bounded Borel functions and we write

Set

| (4.5) |

where . Let and be the two saddle points (see [9]) corresponding to the optimal stopping games with values and , respectively, and so

| (4.6) | |||

Then

4.1 Lemma.

For all and , .

Proof.

We have

Indeed, the first inequality above follows by the saddle point property. The second inequality holds true since is nonincreasing in the time variable, for and . The third inequality is satisfied since the process is a continuous supermartingale in with respect to (see [8]). For the other direction we have

where we use the submartingale property of in . ∎

Now for any bounded Borel functions and set

From the time homogeneity of the process we obtain that

| (4.7) |

4.2 Proposition.

There is a constant such that for any ,

Proof.

The left hand side of the above inequality follows from (iii) and (iv) of Proposition 3.1. For the right hand side, let be such that and and let . By (see [17]) the price function of an American put option has a bounded derivative with respect to in , i.e. This together with Proposition 3.1(ii) yields

| (4.8) |

Next, by Lemma 4.1 and the saddle point property,

| (4.9) |

By Lemma 4.1, (4.7) and the saddle point property,

| (4.10) | |||

Now, (4.5), (4.8), (4.9) and (4.10) yields that

Passing to the limit as we obtain the result. ∎

4.3 Corollary.

For every , , and so .

Proof.

Next, we deal with functions , and so it is natural to consider the domain for some positive (which is, essentially, the same domain after the space coordinate change) and let

| (4.11) |

Let be a function solving the equation with A defined by (3.6) and satisfying the boundary conditions

| (4.12) |

Since these boundary conditions are continuous then (see [5]) they are satisfied by a unique solution in of the above equation. Let be a function on such that

| (4.13) |

Thus, and it satisfies the same parabolic equation in as and . Its boundary values are

| (4.14) |

From the continuity of on we see that it is bounded there and since is also bounded there we obtain the same result for the function as for . Hence,

| (4.15) |

4.2. Integrability of and

Now we will analyze the function . Let be the diffusion process in the plane whose infinitesimal generator is equal to on the space of functions. For each define . Let be the parabolic boundary of . For every which is sufficiently small we can find a smooth function with compact support on the plane such that in it is equal to . By the Dynkin formula we obtain that for every ,

| (4.16) |

where denotes the arrival time to by the process . Note that since for we can replace by in the above formula and since for we obtain that . It follows that for every ,

| (4.17) |

Now fix and a continuous path . Let where is such that . The sequence of times is non decreasing with respect to and so it has a limit . Let be an accumulation point in , i.e. for some subsequence . Define and note that this function is continuous on and it is if and only if . Since for each we conclude that and since it follows that Hence, . By the definition is continuous except at the point but because for every we can ignore paths that reach the point , and so

| (4.18) |

4.4 Corollary.

For every ,

where , and .

Proof.

Let and assume that . Then it is not difficult to understand that

and so is nonincreasing in for every which implies that

| (4.19) |

It is also easy to see that for and ,

and so

| (4.20) |

4.5 Lemma.

The functions and are in .

4.3. Integrability of and

We continue this section by analyzing the function solving the equation with the boundary conditions given by (4.12). Let be the set of all functions which have one derivative in and two derivatives in both uniformly continuous in .

4.6 Lemma.

There exist a function such that

| (4.21) |

Proof.

Recall that for and note that the functions and as function of belong to the space Set

Then since it is a linear combination of functions from this space. We also have

Thus, we obtain

| (4.22) |

Since

it follows that

| (4.23) |

∎

Next, define . From Lemma 4.6 we obtain that is bounded in and so it belongs to for every . Set and observe that

We conclude that the function is the unique solution of the following problem (see [1]).

4.7 Theorem.

Let then for any there exists a unique function such that

(i) ,

(ii) ,

(iii) for every ,

(iv) .

From assertions (i) and (ii) of Theorem 4.7 we obtain that the functions and are both in for every and since we obtain the following.

4.8 Corollary.

For every the functions and belong to the space .

We can now summarize most of the results of this section as follows.

4.9 Proposition.

Let and define

Then the function is continuous at every point in the domain , and there exist two functions and on such that

| (4.24) |

| (4.25) |

and both functions are solutions of the parabolic equation . Furthermore, is continuous in and it satisfies

| (4.26) | |||

and

| (4.27) |

Finally, and for every ,

| (4.28) |

The same decomposition of with the same properties holds true in the domain .

Proof.

Taking the same functions and as in (4.13) we see that (4.25) is actually the same as (4.15) and the fact that both and are solution of is clear from their definitions. Next we see that (4.26) is the same as (4.14), that (4.27) is the same as Lemma 4.5 and that (4.28) is, in fact, Corollary 4.8. Observe that we did not use in this section the fact that so all the proofs are also applicable to the case and the domain . ∎

From (4.24), (4.27), (4.28) and estimating via other derivatives in view of the equation (3.8) we obtain the following.

4.10 Corollary.

Let and

| (4.29) |

Then

| (4.30) |

4.4. Price function when initial stock price is large

Let and be as above. Recall that in the domain the function satisfies the equation , it is continuous in the closure of and for . Define

| (4.31) |

where is given by (4.29) and set . It follows from Proposition 4.9 that

-

(1)

,

-

(2)

for every ,

-

(3)

is continuous,

-

(4)

for every ,

-

(5)

is bounded (since is).

Since a bounded solution of the heat equation in is unique (see [3]) then for every ,

| (4.32) |

and so

Differentiating we obtain polynomials such that for all ,

If is large enough and then is a polynomial in and and it is bounded on . Since for any we can set deriving that for any and ,

For some . Hence, the following results hold true.

4.11 Corollary.

For any positive integers and ,

4.12 Corollary.

Let and . Then

5. Proof of main theorem

We split the proof into two cases for and for .

5.1. Case

We begin by proving the upper bound in (2.11). Since the option holder can exercise at time 0 it is clear from the definition of in (2.5) that for every . Furthermore, by Proposition 3.1(iv) for each fixed the function as a function of is nonincreasing. Therefore, when . From the definition (2.7) of the stopping time it is not difficult to see that in the present case when ,

and so

| (5.1) |

Hence for every we obtain,

| (5.2) | |||

By Proposition 3.2,

| (5.3) |

where, as before, . Taking the sup with respect to all in the inequality (5.2) and using the fact that we obtain that

| (5.4) |

Thus, in order to bound from the above it suffices to find an upper bound of the right hand in (5.4).

Next, we split the domain into three parts

| (5.5) | |||

In order to estimate the right hand side of (5.4) we split it into three parts according to the domains C, S and B, i.e.

| (5.6) | |||

By Proposition 3.1(ii) after the time the prices of the American and game put options coincide which enables us to conclude that for and that the sets , and are the same as the corresponding parts of the domains , and introduced in [17] for the case of American put options. Therefore, we can use the following results from Sections 4.2 and 4.3 in [17].

5.1 Proposition.

There exists a constant such that for every ,

| (5.7) |

where , and

| (5.8) |

Observe also that in the domain S, and so we can use there Lemma 2 from Section 4 of [17].

5.2 Lemma.

For every we have , and so

Thus, for an upper bound of the right side of (5.4) we can ignore the second term in the right hand side of (5.6) and estimate only two remaining terms starting with the first term in the right hand side of (5.6).

5.3 Proposition.

There is a constant such that for all ,

| (5.9) |

Proof.

We have

| (5.10) | |||

Proposition 5.1 provides a bound for the second term in the right hand side of (5.10), and so it remains to deal only with the first term there. Note that if and then

where the equalities above are just definitions of and . Observe also that since and then by the definition of the stopping times the process does not exceed . By Proposition 3.3,

| (5.11) |

Relying on the same computation as in Section 4 of [17] we see that for and ,

| (5.12) |

Thus, for ,

From (3.4) we see that there is a constant independent of and such that

Hence, for ,

Define

where is the free boundary of the option holder and was introduced at the beginning of Section 3. Observe that for every and any ,

Summing up the above estimates we obtain

| (5.13) | |||

where the term comes from the first term of the sum which can be estimated easily using the fact that and are bounded for small .

Let and note that where and are defined in Corollaries 3.14 and 4.10 which imply that . Hence,

| (5.14) |

Next, we estimate the first integral in brackets in the right hand side of (5.13). Let and split the integral in question as follows

| (5.15) | |||

From Corollary 3.14 we know that the function is in where

(for an appropriate in the definition of ). Therefore we can use the Cauchy-Schwarz inequality to obtain

| (5.16) | |||

Now we are left with the second integral in the right hand side of (5.15). We will show that there is a constant such that,

| (5.17) |

Recall that , and so

Observe that the functions and are all bounded for small . Indeed, while is bounded in the domain of integration in (5.17) for small in view of (4.13), (4.15), (4.24) and (4.25). Next, is bounded by Theorem 8.1 from [14]. Finally, is bounded since in the domain in question and its first derivatives are bounded and satisfies the equation (see (3.8)). Therefore, we can write

| (5.18) |

for some constant independent of . Recall that for by Proposition 4.9, where and belong to . Hence, expressing and via and we can estimate the integral (5.18) containing and by means of the Cauchy-Schwarz inequality as it was done in (5.16). Replacing these integrals by we obtain

By (4.19) and (4.20) the functions and do not change signs in , and so it follows that

| (5.19) | |||

By Proposition 4.9, is bounded on , and so the contribution of the first integral in the right hand side of (5.19) is bounded by a constant and it remains to estimate only the second integral there.

Next, we will need a more explicit representation of the function . Let

| (5.20) |

Then in the domain ,

Define

| (5.21) |

and let

In the domain the function satisfies the heat equation

If we let

| (5.22) |

then from the boundary values of we obtain

Note that is a bounded continuous function on the boundaries of . Hence, by Chapter 14 of [3] we can represent in the form

| (5.23) |

where is the fundamental solution and the functions are bounded continuous on the interval . From the definition of we see that

Since is bounded then for some constant independent of ,

From the representation (5.23) of we obtain that

| (5.24) | |||

Observe that as long as we keep or away from the function is smooth and it has bounded derivatives with bounds depending on the range of and their distance from zero. Next, if satisfies

then

Since we see that stays away from on the entire interval . It follows from the above that the function

has bounded derivatives with respect to with bounds independent of in the region . We conclude that the first integral in the right hand side of (5.24) is bounded from above by a constant independent of and it remains to estimate the second integral there.

Set

We see that if

then

In this case can be zero when but this can happen only for a that which is at least apart from . Thus, the function is smooth with a bounded uniformly continuous derivative with respect to though this bound may depend on . Nevertheless, we still have the following

We see that in the second term in the right hand side can take on the value for but then is at least apart from and now the separation constant does not depend on . Thus, we can bound the second term there from above by a constant and it remains to estimate the first term which we do as follows

where is a constant independent of . Analyzing the integral with respect to in the second term in the right hand side above by considering different possible values of we conclude that this integral is bounded by a constant independent of . Next we observe that is also bounded by a constant independent of too. Hence, we obtain

for a constant independent of . Set and note that and . We proceed by changing variables arriving at

for some constants independent of and (5.17) follows. Combining (5.17) and (5.16) we obtain from (5.15) that

| (5.25) |

Finally, Proposition 5.1 follows from (5.25), (5.13) and (5.14). ∎

Next, we turn our attention to the domain B. First, we will prove the following result.

5.4 Lemma.

There exists a constant such that for all ,

| (5.26) |

Proof.

Let and be the set of all points such that and , respectively. We split (5.26) according to these two regions, namely,

By Proposition 5.1 we have that for a constant independent of ,

Thus, it remains to estimate only the first term in the right hand side. Let where and . For large enough we can find such a because is continuous and . We know from Corollary 3.14 that . Since is dense in this space we can approximate by functions to get equality (3.3) of Proposition 3.3 for , as well. Since in the domain we obtain

It follows that

where . Hence,

Here , and the term is the contribution of which holds true from by the definition of the operator and boundedness of and for small . From Corollary 3.14 we see that there exists a constant such that

| (5.27) |

This together with (3.4), the Cauchy-Schwarz inequality and the inequality , which is satisfied when and , yields that

By combining the results of Lemma 5.2 , Proposition 5.3 and Lemma 5.4 together with (5.6) we obtain that the upper bound for some constant independent of and of .

Next, we will obtain a lower bound for the approximation error when . Set

| (5.28) |

By Proposition 5.3,

| (5.29) | |||

Set and let be defined by (5.28) with there replaced by the free boundary for the American put option (see Section 2.2 in [17]). Define also and . We will rely on the following estimate from Section 4.5 in [17].

5.5 Lemma.

5.6 Remark.

Note that for , and so and .

From now on we assume that is large enough so that . From the definition of we have

| (5.31) |

Hence, if we prove that for some constant independent of ,

| (5.32) |

then by (5.31) and (5.29) we could conclude that

| (5.33) |

We split the left hand side of (5.32) into three parts

| (5.34) | |||

This equality is true since on the set . We begin with the last term. First note that on the set we have, in particular, and so by Remark 5.6. In the case we have and and so from Lemma 5.5 we derive that

Next, we deal with the first term in the right hand side of (5.34) where . This means that before time the process is stopped near the boundary and

By the definition, . Thus, we have

If then so we can assume that

| (5.35) |

To continue we need the following lemma.

5.7 Lemma.

There is a constant independent of such that for every point satisfying and ,

Proof.

The function is Lipschitz continuous when and (see [14]), and so

for some independent of . If then and we are done. Now assume that where .

Using (5.35) and the above lemma we obtain

| (5.36) | |||

Hence, we are done with the first term in the right hand side of (5.34) and it remains to estimate the second one. Since the process is stopped near the writer’s boundary. Namely, we have

Since when , and is Lipschitz continuous (see Theorem 8.1 of [14]) we obtain that

for some independent of . Hence,

| (5.37) |

It follows that there exists independent of such that for every ,

| (5.38) |

Next, we will derive a lower bound for the second approximation function defined by (2.10), still assuming that . According to (5.29) in order to obtain

| (5.39) |

it suffices to show that

| (5.40) |

We have

| (5.41) | |||

Indeed, the first inequality is true since is defined as the sup on and we chose a specific one, i.e. . The equality is true due to the same reason that (5.34) holds true. We see that the first term in the right hand side of (5.41) is the same as the first term in (5.34) and by (5.36) it is less then for some constant . The second term is nonpositive because for every we have and so we can just remove it from the equation. The last term is the same as the last term of (5.34) and from Lemma (5.5) we obtain that this term is less or equal than for an appropriate . These arguments yield (5.40) and hence (5.39), as well. For the upper bound we already know that and from the definition of and it is not hard to see that . It follows from above that there exist such that for every ,

| (5.42) |

5.2. Case

We begin with the upper bound on . We will show first that

| (5.43) |

The proof is similar to the proof of (5.4), we just have to show that for every ,

| (5.44) |

On the set this inequality is clear since For the case observe that because we must have

By Theorem 8.1 in [14] the right derivative at satisfies for any , and so for each provided is small enough. Assume , then . Hence, taking we have

Put then for and sufficiently large ,

Hence, we obtain (5.44) which yields also (5.41). To bound the right hand side of (5.43) we split it similarly to the case (see (5.6)) according to the three different regions C, B and S. Since our process starts at , if for some then this must happen after the time , and so we can use (5.8). The part that belongs to the region S is non positive so we can ignore it, and so we will be left only with the region C.

5.8 Lemma.

For the discrete process such that we have

Proof.

It suffices to show that

| (5.45) |

for some independent of since after time we come back to the American option case. This is done in the same way as in Proposition 5.3, and so we provide only a sketch of the proof. Let then similarly to the proof of Proposition 5.3 we obtain

| (5.46) |

Let and split the integral in (5.46) into two parts

| (5.47) | |||

Let then by Corollary 4.12 we see that , and so we obtain similarly to (5.16) that for some constant ,

| (5.48) |

In the first integral in the right hand side of (5.47) we do the same procedure as in (5.13)-(5.17) relying on Proposition 4.9 and deriving that for some constant ,

| (5.49) |

Combining (5.46)–(5.49) we obtain (5.45) and complete the proof of the lemma. ∎

An estimate for the lower bound of when is done similarly to the case . As in that case we use the stopping time from (5.28) and from the above we see that (5.29) is true also for the case under consideration. We consider again defined before Lemma 5.5 and similarly to (5.30) obtain that

| (5.50) | |||

In order to estimate (5.50) for we only need to split it into two parts, one for and the other one for . This it true in view of the fact that if we begin with and then we must have , and so we are back to the American option case and can use Lemma 5.5 for this case. If then the process is stopped near the seller’s boundary and similarly to (5.37) we can use the Lipschitz property of to obtain,

From here we can proceed similarly to the case of and obtain the lower bound for proving (2.11) for . ∎

Next, we turn to the second approximation function , still in the case of . For the upper bound we use Lemma 5.7 as in the case and proceed similarly to the proof of the upper bound for the first approximation function . The proof of the lower bound is similar to the case and we obtain the result observing that if then for any . ∎

6. Computations

In this section we exhibit computations of price functions and free boundaries of game and American put options. All graphs of functions related to game put options were plotted using the approximation function (see (2.10)). The graphs for the American put options were computed using the approximation function from [17].

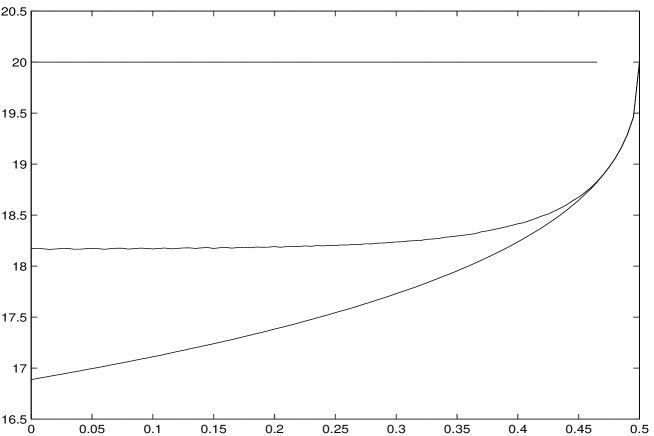

Figure 1 shows both free boundaries of the holder and of the writer of a game put option and also the free boundary of the holder of an American put option corresponding to the option parameters . Here is the strike of the option, is the interest rate, is the volatility, is the time to maturity and is the writer’s cancelation penalty in the case of game option.

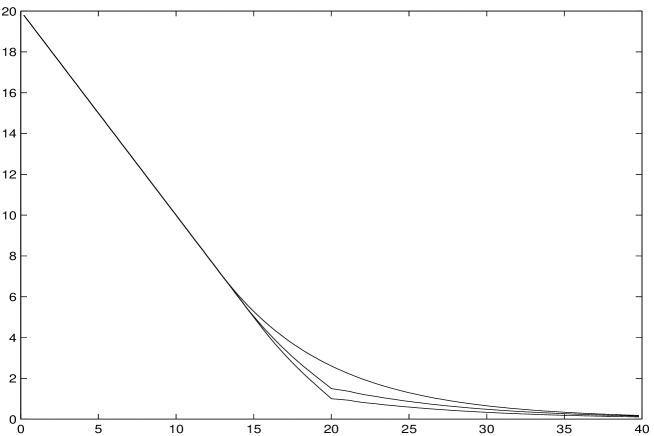

In Figure 2 we plot the graphs of an American put option price function and of a game put option price functions with and while other parameters are . To see what is what here we recall that prices of game options do not exceed prices of corresponding American options and higher penalties increase prices.

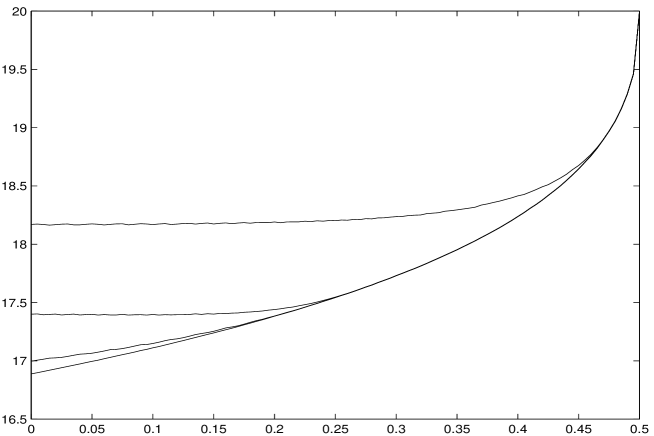

Figure 3 shows the holder’s free boundary for American and game put options where we use the same parameters as in Figure 1 adding also plots of free boundaries for the game put options with penalty values and .

References

- [1] Bensoussan, G. and Friedman, V. (1977): Nonzero-sum stochastic differential games with stopping times and free boundary problems, Trans. AMS 231, 275-327.

- [2] Bensoussan, G. and Lions, J. L. (1982): Application of Variational Inequalities in Stochastic Control, North-Holland, Amsterdam.

- [3] Cannon, J. R. (1984): The One-Dimensional Heat Equation, Addison-Wesley.

- [4] Chassagneux, J. F. (2009): A discrete-time approximation for doubly reflected BSDEs, Adv. Appl. Probab. 41, 101-130.

- [5] Friedman, A. (1964): Partial Differential Equation of Parabolic Type Englewood Cliffs, N.J.:Prentice-Hall.

- [6] Friedman, A. (1982) Variational Principles and Free-Boundary Problems, Wiley, New York.

- [7] Ikeda, N. and Watanabe, S. (1989): Stochastic Differential Equations and Diffusion Processes, 2nd. ed. North–Holland/Kodansha.

- [8] Iron, Yo. and Kifer, Yu. (2011): Hedging of swing game options in contninuous time, Stochastics. 83, 365-404.

- [9] Kifer, Y. (2000): Game options, Finance and Stoch. 4, 443–463.

- [10] Kifer, Y. (2006): Error estimate for binomial approximation of game options, Annals of Appl. Probab. 16, 984-1033.

- [11] Kinderlehrer, D. and Stampacchia, G. (1980): An Introduction to Variational Inequalities and Their Applications, Academic Press, New York.

- [12] Karatzas, I. and Shreve, S. (1991): Brownian Motion and Stochastic Calculus, 2nd ed., Springer–Verlag, New York.

- [13] Karatzas, I. and Shreve, S. (1998): Methods of Mathematical Finance, Springer–Verlag, New York.

- [14] Kunita, H. and Seko, S. Game call options and their exercise regions, Tech. Report, NANZAN-TR-2004-06.

- [15] Kyprianou, A. E. (2004): Some calculations for Israeli options, Finance and Stoch. 8, 73-86.

- [16] Kühn, C. and Kyprianou, A. E. (2007): Callable puts as composite exotic options, Math. Finance 17, 487–502.

- [17] Lamberton, D. (1998): Error estimate for the binomial approximation of American put option, Annals of Appl. Probab. 8, 206-233.

- [18] Lepeltier, J. P. and Maingueneau, J. P. (1984): Le jeu de Dynkin en theorie generale sans l’hypothese de Mokobodski, Stochastics 13, 24–44.

- [19] Shiryaev, A (1984): Probability, Springer, New York.