Representation Theory for Risk On Markowitz-Tversky-Kahneman Topology111I thank Mario Ghossub for bringing my attention to related work on preference based loss aversion estimation. Research support of the Institute for Innovation and Technology Management is gratefully acknowledged.

Abstract

We introduce a representation theory for risk operations on locally compact groups in a partition of unity on a topological manifold for Markowitz-Tversky-Kahneman (MTK) reference points. We identify (1) risk torsion induced by the flip rate for risk averse and risk seeking behaviour, and (2) a structure constant or coupling of that torsion in the paracompact manifold. The risk torsion operator extends by continuity to prudence and maxmin expected utility (MEU) operators, as well as other behavioural operators introduced by the Italian school. In our erstwhile chaotic dynamical system, induced by behavioural rotations of probability domains, the loss aversion index is an unobserved gauge transformation; and reference points are hyperbolic on the utility hypersurface characterized by the special unitary group . We identify conditions for existence of harmonic utility functions on paracompact MTK manifolds induced by transformation groups. And we use those mathematical objects to estimate: (1) loss aversion index from infinitesimal tangent vectors; and (2) value function from a classic Dirichlet problem for first exit time of Brownian motion from regular points on the boundary of MTK base topology.

Keywords: representation theory, topological groups, utility hypersurface, risk torsion, chaos, loss aversion

JEL Classification Codes: C62, C65, D81

2000 Mathematics Subject Classification: 54H15, 37CXX

1 Introduction

We fill a gap in the literature on decision theory by introducing a representation theory for the Lie algebra of decision making under risk and uncertainty on locally compact groups in a topological manifold . This approach is motivated by (Markowitz, 1952, Fig. 5, pg. 154) who, in extending Friedman and Savage (1948) utility theory, stated “[g]enerally people avoid symmetric bets. This implies that the curve falls faster to the left of the origin than it rises to the right of the origin”. In fact, (Markowitz, 1952, pg. 155) plainly states: “the utility function has three inflection points. The middle inflection point is defined to be the “customary” level of wealth. The curve is monotonially increasing but bounded; it is first concave, then convex, then concave, and finally convex”. Thus, he posited a utility function of wealth around the origin such that and “ is customary wealth”, id., at 155–a de facto reference point for gains or losses in wealth. Each of the subject inflection points are critical points for risk dynamics. (Kahneman and Tversky, 1979, pg. 277) also introduced a reference point hypothesis. Theirs is based on “perception and judgment”, and they “hypothesize that the value function for changes of wealth is normally concave above the reference point for and often convex below it ” [emphasis added], id., at 278. See also, (Tversky and Kahneman, 1992, pg. 303).

The aforementioned seminal papers support examination of risk dynamics for transformation groups in a neighbourhood of the origin [or critical points] which, by definition, are included in a topological manifold. For example, the basis sets for Markowitz (1952) topology are

while that for Kahneman and Tversky (1979); Tversky and Kahneman (1992) are given by

A refined topology has basis set . So for index . We prove that the Gauss curvature associated to a reference point on the topological manifold of a utility hypersurface is hyperbolic, i.e. consistent with Friedman-Savage-Markowitz utility, and typically characterized by the quantum group . Moreover, we introduce the concept of risk torsion and a corresponding gauge transformation for risk torsion. And extend it to the literature on prudence spawned by Sandmo (1970). The latter typically involves precautionary savings as a buffer against uncertain future income streams. These theoretical results provide a microfoundational bottom-up approach to results reported under rubric of decision field theory and quantum decision theory. See e.g. Busemeyer and Diederich (2002); Lambert-Mogiliansky et al. (2009); Busemeyer et al. (2011); Yukalov and Sornette (2010); Yukalov and Sornette (2011).

Other independently important results derived from our approach are value function and loss aversion index estimates. The latter being a solution to a gauge transformation for transformation groups in a Hardy space. That result is consistent with (Köbberling and Wakker, 2005, pg. 127) who argued that loss aversion is a psychological risk attribute unrelated to probability weighting and curvature of value functions in loss gain domains. Among other things, a recent paper by (Ghossub, 2012, pg. 5) proposed a preference based estimation procedure for loss aversion, motivated by a probability weighting operator introduced in (Bernard and Ghossoub, 2010, pg. 281), and extended it to objects other than lotteries. Our estimate for loss aversion index differs from those papers because it is based on the distribution of elements of the infinitesimal tangent vector in a Lie group germ. Thus, eliminating some of the differentiability problems at the kink in Köbberling and Wakker (2005), and providing a preference indued loss aversion estimator. Further, we identify harmonic utility in Hardy spaces, and exploit the mean value property induced by the first exit times of Brownian motion through regular points on the boundary of a domain in MTK basis topology. Those results are summarized in Proposition 3.14.

Intuitively, our theory is based on the fact that analysis on a local utility surface extends globally if the topological manifold for that surface is paracompact. In Proposition 2.2 we proffer a partition of unity of probability weighting functions where each partition has a local coordinate system. The second axiom of countability and paracompactness criterion allows us to extend the analysis globally. See e.g., (Warner, 1983, pp. 8-10). Furthermore, Lie group theory is based on infinitesimal generators on a topological manifold, and Lie algebras extend to linear algebra. See (Nathanson, 1979, pg. 5). So our results have practical importance for analysis of behavioural data. The main results of the paper are summarized in Lemmas 3.3 (risk coupling), 3.4 (risk torsion), and 3.11 (harmonic utility). The rest of the paper proceeds as follows. In subsection 2.2 we describe the Euclidean motions induced by risk operations. In section 3 we introduce the concept of risk torsion, and characterize the representation of the Lie algebra of risk. We conclude in section 4 with perspectives on avenues for further research.

2 The Model

In this section we provide preliminaries on definitions and other pedantic used to develop the model in the sequel.

2.1 Preliminaries

Definition 2.1 (Group).

(Clark, 1971, pp. 17-18)

A group is a set with an operation or mapping called a group product which associates each ordered pair with an element in such a way that:

-

(1)

for any elements , we have

-

(2)

there is a unique element such that for any

-

(3)

for each there exist , called the inverse, such that

Remark 2.1.

When is omitted from the definition we have a semi-group.

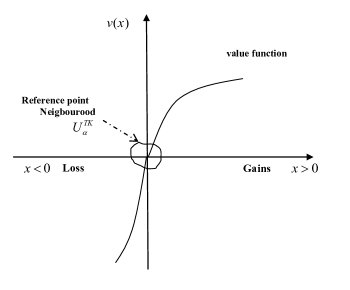

Definition 2.2 (Markowitz-Tversky-Kahneman reference point nbd topology).

A Markowitz-Tversky-Kahneman reference point neihbourood for a typical value function is depicted in Figure 1 on page 1.

Definition 2.3 (Compact set).

See (Dugundji, 1966, pg. 222) A set is compact if every covering has a countable sub-cover.

Definition 2.4 (Paracompact spaces).

(Dugundji, 1966, pg. 162) A Hausdorf space is paracompact of each open covering of has an open neighbourhood-finite refinement.

Definition 2.5 (Topological Manifold).

(Michor, 1997, pg. 1)

A topological manifold is a separable metrizable space which is locally homeomorphic to . So for any open neighbourhood of a point there is a homeomorphism . The pair is called a chart on . A family of charts such that is a cover of is called an atlas.

Remark 2.2.

(Chevalley, 1946, pg. 68) provides a useful but more lengthy axiomatic definition of a manifold.

For example, and are charts on some choice space manifold . Whereas and are covers of .

Definition 2.6 (Partition of unity).

(Warner, 1983, pg. 8) A partition of unity on is a collection of weighting functions on such that

- (a)

-

The collection of supports is locally finite.

- (b)

-

for all , and for all and .

Theorem 2.1 (Existence of partition of unity on manifolds).

(Warner, 1983, pg. 10) Let be a differentiable manifold and be an open cover of . Then there exists a countable partition of unity , subordinate to the cover , i.e. , and supp compact.

Remark 2.3.

We state here that part of the theorem that pertains to paracompactness of . However, it can be extended to non-compact support for .

Theorem 2.1 basically allows us extend the analysis in a reference point neighbourhood to global probability weighting functions and value function analysis. We state this formally with the following:

Proposition 2.2 (Partition of probability weighting functions).

Let be a reference point for a real valued value function and be a neighbourhood (nbd) of . So that . Let be the corresponding probability attached to the reference point. Let be a nbd of for some . Then there exist some local probability weighting function with compact support, such that supp and . So that .

To implement Proposition 2.2, we summarize the (Tversky and Kahneman, 1992, pg. 300) topology. Let be an outcome space that includes a neutral outcome or reference point which we assign . So that all other elements of are gains or losses relative to that point. An uncertain prospect is a mapping were is a sample space or finite set of states of nature. Thus, is a stochastic choice. Rank in monotonic increasing order. So that a prospect is a sequence of pairs where is a discrete partition of indexed by . In other words, the prospect is a rank ordered configuration, i.e. sample function of a random field, of outcomes in . Let be a refinement of the neighbourhood topology in Definition 2.2. Next, we introduce the notion of attached spaces, and proceed to apply it to the implementation at hand.

Definition 2.7 (Attaching weighted probability space to outcome space).

(Dugundji, 1966, pg. 127). Let be a classic probability space with sample space , -field of Borel measurable subsets of given by , and probability measure on . For a sample element , define where is a neighbourhood base in consequence or outcome space, and is an act, i.e., stochastic choice. Let be a measurable neighbourhood base such that , where is a probability distribution that corresponds to . Thus, and are two disjoint abstract spaces. Let be the free union of and . Define an equivalence relation by , where is a probability weighting function. The quotient space is said to be attached to by the composite function which is written . The composite function is called the attaching map.

Remark 2.4.

The interested reader is referred to (Willard, 1970, §9) for a taxonomy of examples of construction of new spaces from old in the context of quotient topology.

Let be a mapping into a reference point neighbourhood, and be a weighting function such that , where is an induced neighbourhood base cover for probability weighting assigned to uncertain events . Such mappings are permitted due to the smallness of the neighbourhoods being considered. From the outset we note that according to Prelec (1998); Luce (2001). In that way is a covering of the probabilistic manifold, i.e. we assign so that and . For example, . In other words, by Definition 2.7, is attached to by and the attached space is a covering of the prospect .

Definition 2.8 (Lie product).

(Guggenheimer, 1977, pg. 105)

The Lie product of two infinitesimal vectors and belonging to curves and , respectively, is the infinitesimal vector of . The substraction is understood to bee in thee sense of vector addition in .

Definition 2.9 (Lie algebra).

(Guggenheimer, 1977, pg. 106)

The Lie algebra of a Lie group germ is the algebra of infinitesimal vectors defined by the Lie product.

Definition 2.10 (Lie group).

(Guggenheimer, 1977, pg. 103)

A Lie group is a group which is also a differentiable manifold. A Lie group germ is a neighbourhood of the unit element of a Lie group. Thus, it is possible to construct a compact Lie group from coverings of Lie group germs. Let G be a Lie group germ in a neighbourhood V of the origin e in such that the pair of vectors is mapped (x,y) f(x,y) subject to the following axioms.

-

(L1)

f(x,y) is defined for all x V, y V

-

(L2)

f(x,y) C2()

-

(L3)

If f(x,y) V and f(y,z) V, then f(f(x,y),z) = f(x, f(y,z))

-

(L4)

f(e,y) = y and f(x,e) = x

The Lie algebra (G) on this transformation group is given by [a,b] such that

2.2 Rotation of behavioral operator over probability domains.

Let be a fixed point probability that separates loss and gain domains. See Kahneman and Tversky (1979) and Tversky and Kahneman (1992). Let and be loss and gain probability domains as indicated. So that the entire domain is . Let be a probability weighting function (PWF), and be an equivalent martingale measure.

Definition 2.11 (Behavioural matrix operator).

The confidence index from loss to gain domain is a real valued mapping defined by the kernel function

| (2.1) | ||||

| (2.2) | ||||

| We note that that kernel can be transformed even further so that it is singular at the fixed point as follows: | ||||

| (2.3) | ||||

In particular, for and is a behavioural matrix operator.

The kernel accommodates any Lebesgue integrable PWF compared to any linear probability scheme. See e.g., Prelec (1998) and Luce (2001) for axioms on PWF, and Machina (1982) for linear probability schemes. Evidently, is an averaging operator induced by , and it suggests that the Newtonian potential or logarithmic potential on loss-gain probability domains are admissible kernels. The estimation characteristics of these kernels are outside the scope of this paper. The interested reader is referred to the exposition in Stein (2010). Let be a partially ordered index set on probability domains, and and be subsets of for indexed loss and indexed gain probabilities, respectively. So that

| (2.4) |

For example, for and if the index gives rise to a matrix operator . The “adjoint matrix“ . So transforms gain domain into loss domain–implying fear of loss, or risk aversion, for prior probability . While is an Euclidean motion that transforms loss domain into hope of gain from risk seeking for prior gain probability .

Definition 2.12 (Behavioural operator on loss gain probability domains).

Let be a behavioral operator constructed as in (2.2). Then the adjoint behavioural operator is a rotation and reversal operation represented by .

Thus, captures Yaari (1987) “reversal of the roles of probabilities and payments”, ie, the preference reversal phenomenon in gambles first reported by Lichtenstein and Slovic (1973). Moreover, and are generated (in part) by prior probability beliefs consistent with Gilboa and Schmeidler (1989). The “axis of spin” induced by this behavioural rotation is perpendicular to the plane in which and operates as follows.

2.2.1 Ergodic behaviour

Consider the composite behavioural operator and its adjoint which is skew symmetric.

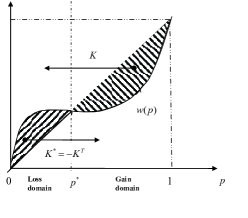

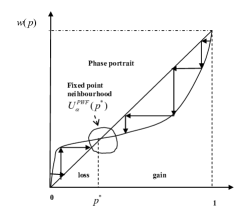

What does. By definition, takes a vector valued function in gain domain (through ) that is transformed into [fear of] loss domain, and sends it back from a reduced part of loss domain (through ) where it is transformed into [hope of] gain domain. In other words, is a contraction mapping of loss domain. A subject who continues to have hope of gain in the face of repeated losses in that cycle will be eventually ruined. By the same token, an operator is a contraction mapping of gain domain. In this case, a subject who fears loss of her gains will eventually stop before she looses it all. Thus, the composite behavior of and is ergodic because it sends vector valued functions back and forth across loss-gain probability domains in a “3-cycle” while reducing the respective domain in each cycle. These phenomena are depicted on page 2. There, Figure 2 depicts the behavioural operations that transform probability domains. Figure 3 depicts the corresponding phase portrait and a fixed point neighbourood basis set. In what follows, we introduce a behavioural ergodic theory by analyzing . The analysis for is similar so it is omitted. Let

| (2.5) | ||||

| Define the range of by | ||||

| (2.6) | ||||

| (2.7) | ||||

| (2.8) | ||||

Thus, reduces , i.e. it reduces the domain of , and is skew symmetric by construction.

Lemma 2.3 (Graph of confidence).

Let be the domain of , and respectively. Furthermore, construct the operator . We claim (i) that is a bounded linear operator, and (ii) that for the graph is closed.

Proof.

See Appendix A ∎

Proposition 2.4 (Ergodic confidence).

Let , and . Define the reduced space . And let be a Banach-space, i.e. normed linear space, that contains . Let be a probability space, such that and is a probability measure and -field of Borel measureable subsets, on , respectively. We claim that is measure preserving, and that the orbit or trajectory of induces an ergodic component of confidence.

Proof.

See Appendix B ∎

Remark 2.5.

One of the prerequisites for an ergpdic theory is the existence of a Krylov-Bogulyubov type invariant probability measure. See (Jost, 2005, pg. 139). Using entropy and information, (Cadogan, 2012, Thm. 3.2) introduced canonical harmonic probability weighting functions with inverted S-shape in loss-gain probability domains. So that the phase portrait in Figure Figure 3 on page 3, based on an inverted S-shaped probability weighting function, is an admissible representation of the underlying chaotic behavioural dynamical system.

Remark 2.6.

Let be the set of all probabilities for which . The maximal of such set is called the ergodic basin of . See (Jost, 2005, pg. 141).

2.2.2 Axis of spin induced by rotation

Let be a [vector valued] curve in the domain of (or of ) with respect to a parameter such that and are unit vectors along the coordinate axes; and and be parametric curves. The “axes of spin” for is perpendicular to and . If and are in the same plane and inclined at an angle between them, then is a vector perpendicular to the plane. The corresponding unit vector is given by

| (2.9) |

Definition 2.13 (Spin vector).

(Wardle, 2008, pp. 16-17)

The spin vector of x(t) G, where t is a parameter, is defined as

where , for the angle between x and ; and .

Remark 2.7.

The direction of the “spin vector” determines whether an agent is risk averse or risk seeking at that instant in our model.

Definition 2.14 (Curvature).

(Wardle, 2008, pg. 18)

The curvature is given by

where is the unit tangent vector relative to arc-length as parameter, and is the derivative of with respect to . In the context of a vector we have

Definition 2.15 (Binormal).

(Wardle, 2008, pg. 18) The unit normal vector drawn at a point on a curve in the direction of the vector is called the binormal at . Specifically,

or

Definition 2.16 (Torsion).

(Wardle, 2008, pg. 19) The rate of turn of the binormal with respect to arc length at a point of a curve is called the torsion represented by the triple scalar product

which can also be written as

Remark 2.8.

(Struik, 1961, pg. 15) defines torsion as the rate of change of the osculating plane. The latter being the plane subtended by two consecutive tangent lines. For our purposes, torsion is roughly equal to the rate of change of Arrow-Pratt risk measure.

3 Lie algebra of risk operators

We define our risk operator as follows.

Definition 3.1 (Logarithmic differential operator).

A logarithmic differential operator is defined for all functions in the domain of such that

This definition is general enough to handle and is undefined for .

Definition 3.2 (Arrow-Pratt risk operator).

Let be a compact choice space, and be a twice differentiable continuous utility function. Let be the differential operator so that and . Then the Arrow-Pratt risk operator for the risk measure is given by

In the sequel we use , and for risk averse and risk seeking operations respectively.

Let be an open space of choice vectors, i.e., n-dimensional basket of goods; be a compact group in ; x,y G; and be a vector valued utility function. By Definition 2.5, is a topological manifold, i.e. a topological group. Assume that is a Lie group germ induced by . For example could be a local budget set for income level , price vector , and consumption bundle . Let Ara = be the operator for Arrow-Pratt risk aversion (ra) described in Definition 3.2. The corresponding infinitesimal vectors for are and , which stem from the expansion

| (3.1) |

This gives rise to the following relationship between group operations in and vector addition of infinitesimal vectors:

Theorem 3.1 (Infinitesimal vectors of group product).

(Guggenheimer, 1977, pg. 104)

Let be curves in , with infinitesimal vectors and . The curve is differentiable and it has infinitesimal vector .

Second order Taylor expansion222See (Taylor and Mann, 1983, pp. 207-208). of and (3.1) around the origin suggest that:

| (3.2) | ||||

| (3.3) |

| (3.4) | ||||

| The typical element of the squared term in (3.3) is of the form | ||||

| (3.5) | ||||

| (3.6) | ||||

So that for differentiable curves x(t) and y(t), with parameter t, i.e., one parameter group of motions, the Lie group structure for risk associated to u(x,y), i.e., the infinitesimal generator of risk, is determined by:

| (3.7) | |||

| (3.8) | |||

| (3.9) |

Here k, k are the k-th elements of the infinitesimal tangent vector and , and is the structure constant for second order terms in the Taylor expansion of x(t) and y(t); and is 333(Belinfante et al., 1966, pp. 14-15).. After applying Theorem 3.1; multiplying and dividing terms inside the brackets in (3.9) by , and differentiating, the differential of constant terms vanish since

| (3.10) |

So we can rewrite (3.9) as

| (3.11) | ||||

| (3.12) | ||||

| (3.13) | ||||

| For risk seeking (rs), the sign of the Arrow-Pratt operator changes according to the spin vector in Definition 2.13. So we leave the same for convenience but define | ||||

| (3.14) | ||||

| (3.15) | ||||

Subtract (3.15) from (3.13) to get the -th element of the Lie product vector in Definition 2.8

| (3.16) | ||||

| (3.17) | ||||

| (3.18) | ||||

| (3.19) |

where the quantity

| (3.20) |

is the structure constant for the risk operations on our topological group . This gives rise to the following

Definition 3.3 (Commutator).

Let . The commutator of and is defined by . The commutator is the element that induces commutation between and so that

Definition 3.4 (Structure constant or coupling constant).

The structure constant characterizes the strength of the interaction between risk averse and risk seeking behavior.

Theorem 3.2 (Infinitesimal vector of commutator curve).

(Guggenheimer, 1977, pg. 106)

is the infinitesimal vector of the commutator curve .

The quantities

| (3.21) |

has the following interpretation. are the k-th element of the tangent vector and and 2 is the k-th coefficient of the second order terms which reflect the rate of spin of the tangent vectors. That is, in the context of Definition 2.16 is a torsion type constant. However, examination of (3.13), (3.15) and Definition 2.13 suggests that, in the context of our model, reflects the rate at which agents “flip” between risk aversion and risk seeking in decision making. It is, in effect, risk torsion444(Pratt, 1964, pg. 127) distinguished his risk measure from the curvature in Definition 2.14. By the same token, “risk torsion” is distinguished from the torsion in Definition 2.16..

Lemma 3.3 (Coupling risk aversion and risk seeking torsion).

The structure constant associated with risk operations reflects the coupling between risk aversion and risk seeking torsion behavior in decision making.

3.1 Prudence risk torsion

Lemma 3.3 is related to the concept of prudence, introduced by Sandmo (1970) in the context of a two period model of consumption and investment, characterized by a utility function where are consumption in periods and . There, Sandmo is interested in comparing a subject’s response to income and capital risk in a two period model with interest rate is .

Definition 3.5 (Prudence).

(Sandmo, 1970, pg. 353) A subject is prudent if in the face of income risk [s]he engages in precautionay savings as a buffer against future consumption.

(Sandmo, 1970, pg. 359) condition for prudence rests on the relationship:

| (3.22) |

This implies the existence of . In fact, (Sandmo, 1970, pg. 354, eq. 2) suggests and (Kimball, 1990, pg. 60, eq. 9) states that for a utility function prudence is defined by the operation

| (3.23) | ||||

| which, in the context of Definition 3.2, is a risk operation | ||||

| (3.24) | ||||

(Sandmo, 1970, pg. 354) described a subject’s risk attitudes towards present [known] and future [uncertain] consumption thusly:

Diagramatically it means that, starting at any point in the indifference map [for ], the risk aversion function decreases with movements in the NW direction [] and increases with movement in the SE direction []. We shall refer to this assumption as the hypothesis of decreasing temporal risk aversion.

[Emphasis added]. In the context of Lemma 3.3, that description implies a coupling between the directions of the two risk operations. To see this, for some measure on consider the integral operator

| (3.25) | ||||

| (3.26) | ||||

| (3.27) |

by virtue of (3.24). We note that could be any one of several functional integration operators characterized by a -measure in the literature on decision making under risk and uncertainty. For example, includes but is not limited to Von Neumann and Morgenstern (1953)(VNM utility functional); Gilboa and Schmeidler (1989)(maximin expected utility (MEU)); Klibanoff et al. (2005) (smooth ambiguity); Maccheroni et al. (2006) (variational model of that captures ambiguity); Chateauneuf and Faro (2009) (operator representation of confidence preferences) or Machina (1982)(local utility functional). Let be the coupling action for risk averse and risk seeking prudence operations. Thus we can rewrite (3.19) as

| (3.28) |

We summarize the foregoing with the following

Lemma 3.4 (Prudence risk torsion).

Let be a differential operator, be Arrow-Pratt risk aversion operator, and be the corresponding risk seeking operator. Furthermore, let be an integral operator. Define the prudence operation for risk aversion by , assuming that the expressed functions are in the domains of the respective operators. Then the prudence risk torsion operator is given by

3.2 Risk operator representation

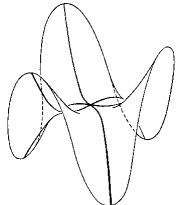

Perhaps most important, the risk averse operation in (3.13) and risk seeking operation in (3.15) have different signs at a given point . In that case, the risk torsion operator in (3.16) has positive and negative eigenvalues and it belongs to the quantum group . This is a characteristic of Gauss curvature K(x0) associated with a hyperbolic point x0 on the utility hypersurface near the reference point or identity (e) in . See (Guggenheimer, 1977, pg. 213) and (Struik, 1961, pp. 77-79). A three dimensional sketch of a hyperbolic point is depicted in Figure 4. See (Struik, 1961, pg. 83). There it can be seen that the curvature of surface area in a neighbourood of the saddle depends on the cross section or “spin”.

Theorem 3.5 (Lie algebra of risk operators).

Let be a compact group on a differentiable manifold X of choice vectors in n, and be a mapping of a compact group onto itself. Let u be a vector valued von Neuman-Morgenstern utility function defined on X, and be choice vectors in . Define risk operators such that for risk aversion Ara = (risk seeking Ars = ) on the class of functions where is the domain of . Then the Lie algebra for the risk associated to u is the special linear group of skew symmetric matrices.

Theorem 3.6 (Risk torsion quantum group).

Let u be a vector valued von Neuman-Morgenstern utility function defined on X, and be a risk torsion operator. Then has representation in the quantum group .

Assumption 3.7.

See (Von Neumann and

Morgenstern, 1953, Appendix).

Subjects have von Neuman Morgenstern utility.

Under von Newman Morgenstern (VNM) utility framework, Arrow-Pratt risk measure is positive for risk aversion, negative for risk seeking, and the absolute value of the measure is unchanged. So . This relation has the following consequence for

| (3.29) |

| By definition of group operations in the identity element is the matrix , and the “tangent matrix” is characterized by some matrix analog to (3.1). We write | ||||

| (3.31) | ||||

| So that is consistent with the idea that the identity element of must correspond to the origin in accord with Definition 2.1. Now | ||||

| (3.32) | ||||

| After differentiating the left hand side and setting , the Lie group germ structure is | ||||

| (3.33) | ||||

| Let | ||||

| (3.34) | ||||

| According to Definition 2.12 the adjoint behavioural operator is now | ||||

| (3.35) | ||||

| If , i.e. belongs to the group of orthogonal matrices so , then (3.32), (3.33) and (3.35) reduces to | ||||

| (3.36) | ||||

In which case, we have skew symmetric or antisymmetric risk operation

| (3.37) |

Thus, the risk operation in (3.35) is functionally equivalent to the risk torsion operations in (3.13) and (3.15). This suggests that our behavioural operator in (2.2) is well defined. More on point, the matrix representation of the skew symmetric risk operators belongs to the orthonormal group with Lie algebra . Thus, the Lie algebra (G) of the Lie group G is the algebra of skew symmetric555This result jibes well with (Kahneman and Tversky, 1979, pg. 268) experiment where they reported: “[T]he preference between negative prospects is the mirror image of the preference between positive prospects. Thus, the reflection of prospects around 0 reverses the preference order. We label this pattern the reflection effect”. So the risk operator is well defined. matrices. The foregoing is a special case of the important

Theorem 3.8 (Ado’s theorem).

(Nathanson, 1979, pg. 202)

Every finite dimensional Lie algebra of characteristic zero has a finite dimensional representation.

Remark 3.1.

A field has characteristic if for any and implies . For example, if the “additive identity” element of the field is , it is the number of times we must add the identity to get . See (Clark, 1971, pg. 69). The theorem basically says, for example, that a finite dimensional Lie algebra with characteristic has a representation in the matrix group .

This gives rise to the following

Theorem 3.9 (Lie algebra of risk operation on Abelian group).

The Lie algebra induced by risk operations on VNM utility with support on the abelian group is that of the antisymmetric or skew symmetric matrices .

The infinitesimal vectors characterized by (3.37) and our choice of and in (3.4) and (3.6) on page 3.6 require that

| (3.38) | ||||

| (3.39) | ||||

| (3.40) | ||||

| (3.41) | ||||

| (3.42) |

So the vector elements are on a circle.

The story is different for the structure constant

| (3.43) | ||||

| (3.44) | ||||

| (3.45) | ||||

| (3.46) | ||||

| (3.47) |

There are two scenarios implied by (3.46)

-

Sc1

If , then the vectors lie in an annulus.

-

Sc2

If , then the vectors are complex valued.

In Sc2 above, and or are complex valued666This subsumes the case when sgn sgn in the circle (3.47). Thus, the Hardy spaces in the unit disk are admissible for our class of infinitesimal vectors where

| (3.48) |

Here, is a holomorphic function, i.e. complex valued function of complex variable(s) that is complex differentiable at every point in its domain. This class of functions also include analytic functions. So the Abelian groups implied by our structure constant are in a Hardy space. Thus, we state the following

Lemma 3.10 (Abelian groups supported by risk operations).

The Abelian [transformation] groups supported by risk operations are in the class of holomorphic functions in Hardy spaces .

Lemma 3.11 (Harmonic utility functions).

The class of utility functions that support risk operations on Abelian transformation groups in Hardy spaces is harmonic. Specifically, for infinitesimal vectors and where are vector elements, , unit disk , and we have the Laplacian with solution .

According to Lemma 3.11, for , we have that the imaginary part is an admissible harmonic utility specification for slow varying function . The interested reader is referred to the monograph by Folland and Stein (1982) for ramifications of this result which is beyond the scope of this paper.

Assumption 3.12.

The story is different for prospect theory which posits a loss aversion index for risk seeking over losses. So the Arrow-Pratt risk operator is asymmetrically skewed. In that case, in concert with (3.13) and (3.15) we posit:

| (3.49) | ||||

| (3.50) | ||||

| (3.51) | ||||

| (3.52) |

So the commutator in (3.50) is inflated by . In this case is a gauge transformation in (3.52) because it has no effect on the commutativity of the underlying vectors.

Definition 3.6 (Loss aversion gauge).

(Köbberling and Wakker, 2005, pg. 125) Loss aversion is a psychological gauge transformation which governs the rate of exchange between gain and loss units.

This implies that our vectors lie in Hardy spaces when and in an annulus or torus otherwise. The foregoing gives rise to the following estimates for loss aversion, and Tversky and Kahneman (1992) value function.

3.3 Estimates of loss aversion index and value function

Proposition 3.13 (Estimate of loss aversion index).

Let be an indicator function, be a reference point ndb in Definition 2.2. Let be a unit disk, and be infinitesimal vectors in the Hardy space such that . Let be a value function with components on loss -gain domain with loss aversion index . Then the loss aversion index has estimate

Proposition 3.14 (Dirichlet estimate of value function).

Let be a domain, and be a bounded function for regular points on the boundary of that domain . Let such that

-

1.

in

-

2.

for all

Then

where is the expectation operator for Brownian motion starting at , is Brownian motion with respet to some probability space , and the first exit time from the domain is

Proof.

See (Øksendal, 2003, pp. 177-178). ∎

The latter proposition essentially says that for Brownian motion starting at an interior point , our estimate of the value function is its average over the distribution of its values at those points were it potentially first exits the boundary of . The results presented here fall under rubric of potential theory. One of the problems posed by (Köbberling and Wakker, 2005, pg. 121) is how to estimate the loss aversion index at the kink at depicted in the MTK neighbourhood in Figure 1 on page 1. Proposition 3.13 provides estimates for loss aversion based on elements of a tangent vector in the Lie group germ inside a Hardy space on a disk with radius normalized to 1. This approach explains the range of loss aversion index reported in (Abdellaoui and Paraschiv, 2007, pg. 1662).

We claim that Proposition 3.14 above also allows us to obtain an estimate for loss aversion by imposing suitable boundary value conditions while circumventing the problem of existence of differentials at . For example, Itô (1950) provides analytics for Brownian motion in a Lie group germ consistent wit Definition 2.10. Further, Harrison and Shepp (1981) provide analytics for skew Brownian motion induced by asymmetric probabilities for initial steps of a random walk, and local time around the origin where

| (3.53) |

is Brownian motion, is local time at the origin, , and is -adapted. Thus, it is possible to obtain separate estimates for the value function, on loss and gain domains, based on asymmetric probabilities and the path properties of skew Brownian motion dynamics near the origin in the domain . See also, (Harrison and Shepp, 1981, pg. 310). In order not to overload the paper we do not address that proposed estimation scheme here and leave it for another day.

4 Conclusion

The behavioural operators and risk torsion concepts introduced in this paper provide a foundation for behavioural chaos in dynamical systems, and a mechanism for providing estimates for loss aversion and value functions. Moreover, it suggests that loss aversion index and value function estimation can be extended to potential theory. We believe that the research paradigms suggested here would yield fruitful results that further our understanding of the data generating process for decision making under risk and uncertainty.

Appendix of Proofs

Appendix A Proof of Lemma 2.3

Proof.

-

(i).

That is a bounded operator follows from the facts that the fixed point induces singularity in and . Also, by construction is a contraction mapping so it is bounded. The analytic proof of those facts suggests that we let be a sequence of operators induced by an appropriate corresponding sequence of and , and –the spectrum of . Thus, we write , where . Singularity implies and for , we have . Thus, is bounded.

-

(ii).

Let and . So for . For that operation to be meaningful we must have . But . According to the Open Mapping Closed Graph Theorem, see (Yosida, 1980, pg. 73), the boundedness of guarantees that the graph is closed.

∎

Appendix B Proof of Proposition 2.4

Proof.

Let . Then for . But . Since is arbitrary, then by our reduced space hypothesis, maps arbitrary points in its domain back into that domain. So that . Whereupon from our probability space on Banach space hypothesis, for some measureable set we have the set function and . In which case is measure preserving. Now by Lemma 2.3, is a closed graph on . By the method of induction, is also a graph for each . In which case the evolution of the graphs is a dynamical system, see (Devaney, 1989, pg. 2), that traces the trajectory or orbit of . Now we construct a sum of N graphs and take their “time average” to get

| (B.1) | ||||

| According to Birchoff-Khinchin Ergodic Theorem, (Gikhman and Skorokhod, 1969, pg. 127), since is measure preserving on , we have | ||||

| (B.2) | ||||

| Furthermore, is -invariant and integrable, i.e. | ||||

| (B.3) | ||||

| (B.4) | ||||

| (B.5) | ||||

| Moreover, | ||||

| (B.6) | ||||

So the “time average” in (B.5) is equal to the “space average” in (B.6). Whence induces an ergodic component of confidence . ∎

References

- Abdellaoui and Paraschiv (2007) Abdellaoui, M., B. H. and C. Paraschiv (2007, Oct). Loss Aversion Under Prospect Theory: A Parameter Free Measurement. Management Science 53(10), 1659–1674.

- Belinfante et al. (1966) Belinfante, J. G., B. Kolman, and H. A. Smith (1966, Jan.). An Introduction to Lie Groups and Lie Algebras, with Applications. SIAM Review 8(1), 11–46.

- Bernard and Ghossoub (2010) Bernard, C. and M. Ghossoub (2010). Static portfolio choice under cumulative prospect theory. Mathematics and Financial Economics 2, 277–306.

- Busemeyer and Diederich (2002) Busemeyer, J. R. and A. Diederich (2002). Survey of Decision Field Theory. Mathematical Social Sciences 43, 345–370.

- Busemeyer et al. (2011) Busemeyer, J. R., E. M. Pothos, R. Franco, and J. S. Trueblood (2011). A Quantum Theoretical Explanation for Probability Judgment Errors. Psychological Review 118(2), 193–218.

- Cadogan (2012) Cadogan, G. (2012, Jan). The Source of Uncertainty for Probabilistic Preferences Over Gambles . Working Paper. Available at SSRN eLibrary http://ssrn.com/paper=1971954.

- Chateauneuf and Faro (2009) Chateauneuf, A. and J. H. Faro (2009). Ambiguity through confidence functions. Journal of Mathematical Economics 45(9-10), 535 – 558.

- Chevalley (1946) Chevalley, C. (1946). Theory of Lie Groups, Volume I. Princeton, NJ: Princeton University Press. Third printing 1957.

- Clark (1971) Clark, A. (1971). Elements of Abstract Algebra. Belmont, CA: Wadsworth Publishing Co. Dover unabridged reprint 1984.

- Devaney (1989) Devaney, R. L. (1989). An Introduction To Chaotic Dynamical Systems (2nd ed.). Studies in Nonlinearity. Reading, MA: Addison-Wesley Publishing Co., Inc.

- Dugundji (1966) Dugundji, J. (1966). Topology. Allyn and Bacon Series in Advanced Mathematics. Boston, MA: Allyn and Bacon, Inc.

- Folland and Stein (1982) Folland, G. B. and E. M. Stein (1982). Hardy Spaces on Homogenous Groups. Princeton Matheematical Notes. Princeton, NJ: Princeton University Press.

- Friedman and Savage (1948) Friedman, M. and L. J. Savage (1948, Aug). The Utility Analysis of Choice Involving Risk. Journal of Political Economy 56(4), 279–304.

- Ghossub (2012) Ghossub, M. (2012, Mar). Towards a Purely Behavioral Definition of Loss Aversion. SSRN eJournal. Available at http://ssrn.com/abstract=2028146.

- Gikhman and Skorokhod (1969) Gikhman, I. I. and A. V. Skorokhod (1969). Introduction to The Theory of Random Processes. Phildelphia, PA: W. B. Saunders, Co. Dover reprint 1996.

- Gilboa and Schmeidler (1989) Gilboa, I. and D. Schmeidler (1989). Maxmin Expected Utility with Non-unique Prior. Journal of Mathematical Economics 18(2), 141–153.

- Guggenheimer (1977) Guggenheimer, H. W. (1977). Differential Geometry. Mineola, New York: Dover Publications, Inc.

- Harrison and Shepp (1981) Harrison, J. M. and L. A. Shepp (1981). On Skew Brownian Motion. Annals of Probability 9(2), 309–313.

- Itô (1950) Itô (1950). Brownian Motion in a Lie Group. Proceedings of the Japan Academy 26(8), 4–10. Available at http://projecteuclid.org/DPubS?service=UI&version=1.0&verb=Display&handle=euclid.pja/1195571633.

- Jost (2005) Jost, J. (2005). Dynamical Systems: Examples of Complex Behavior. Universitext. New York, NY: Springer.

- Kahneman and Tversky (1979) Kahneman, D. and A. Tversky (1979). Prospect theory: An analysis of decisions under risk. Econometrica 47(2), 263–291.

- Kimball (1990) Kimball, M. S. (1990, Jan.). Precautionary Saving in the Small and in the Large. Econometrica 58(1), pp. 53–73.

- Klibanoff et al. (2005) Klibanoff, P., M. Marinacci, and S. Mukerji (2005). A Smooth Model of Decision Making under Ambiguity. Econometrica 73(6), 1849–1892.

- Köbberling and Wakker (2005) Köbberling, V. and P. Wakker (2005). An index of loss aversion. Journal of Economic Theory 112, 119–131.

- Lambert-Mogiliansky et al. (2009) Lambert-Mogiliansky, A., S. Zamir, and H. Zwirn (2009). Type indeterminacy: A model of the KT(Kahneman Tversky)-man. Journal of Mathematical Psychology 53(5), 349 – 361. Special Issue: Quantum Cognition.

- Lichtenstein and Slovic (1973) Lichtenstein, S. and P. Slovic (1973, Nov.). Response-induced reversals of preference in gambling: An extended replication in Las Vegas. Journal of Experimental Psychology 101(1), 16–20.

- Luce (2001) Luce, R. D. (2001). Reduction invariance and Prelec’s weighting functions. Journal of Mathematical Psychology 45, 167–179.

- Maccheroni et al. (2006) Maccheroni, F., M. Marinacci, and A. Rustichini (2006). Ambiguity Aversion, Robustness, and the Variational Representation of Preferences. Econometrica 74(6), 1447–1498.

- Machina (1982) Machina, M. (1982, March). ”Expected Utility” Analysis without the Independence Axiom. Econometrica 50(2), 277–323.

- Markowitz (1952) Markowitz, H. (1952, April). The Utility of Wealth. Journal of Political Economy 40(2), 151–158.

- Michor (1997) Michor, P. W. (1997). Foundations of Differential Geometry. Lecture Notes. Institut für Mathematik der Universität Wien.

- Nathanson (1979) Nathanson, J. (1979). Lie Algebras (Unabridged correction of 1962 John Wiley & Sons. ed.). Mineola, NY: Dover Publications, Inc. Dover reprint.

- Øksendal (2003) Øksendal, B. (2003). Stochastic Differential Equations: An IntroductionWith Applications (6th ed.). Universitext. New York: Springer-Verlag.

- Pratt (1964) Pratt, J. W. (1964, Jan.-Apr.). Risk Aversion in the Small and in the Large. Econometrica 32(1/2), 122–134.

- Prelec (1998) Prelec, D. (1998). The probability weighting function. Econometrica 60, 497–528.

- Sandmo (1970) Sandmo, A. (1970, Jul.). The Effect of Uncertainty on Saving Decisions. Review of Economic Studies 37(3), pp. 353–360.

- Stein (2010) Stein, E. M. (2010). Some geometrical concepts arising in harmonic analysis. In N. Alon, J. Bourgain, A. Connes, M. Gromov, and V. Milman (Eds.), Visions in Mathematics, Modern Birkh user Classics, pp. 434–453. Birkh user Basel. See also, GAFA Geom. funct. anal., Special Volume 2000.

- Struik (1961) Struik, D. J. (1961). Lectures in Classical Differential Geometry (2nd ed.). Reading, MA: Addison-Weseley Publishing Co., Inc. Dover reprint 1988.

- Taylor and Mann (1983) Taylor, A. E. and W. R. Mann (1983). Advanced Calculus (3rd ed.). New York, NY: John Wiley & Sons, Inc.

- Tversky and Kahneman (1992) Tversky, A. and D. Kahneman (1992). Advances in prospect theory: Cumulative representation of uncertainty. Journal of Risk and Uncertainty 5, 297–323.

- Von Neumann and Morgenstern (1953) Von Neumann, J. and O. Morgenstern (1953). Theory of Games and Economic Behavior (3rd ed.). Princeton University Press.

- Wardle (2008) Wardle, K. L. (2008). Differential Geometry (Unabridged 1965 ed.). Mineola, NY: Dover Publications, Inc. Dover reprint.

- Warner (1983) Warner, F. (1983). Foundations of Differentiable Manifolds and Lie Groups. Glenview, IL: Scott, Foresman and Company.

- Willard (1970) Willard, S. (1970). General Topology. Reading, MA: Addison-Wesley.

- Yaari (1987) Yaari, M. (1987, Jan.). The duality theory of choice under risk. Econometrica 55(1), 95–115.

- Yosida (1980) Yosida, K. (1980). Functional Analysis (6th ed.). New York: Springer-verlag.

- Yukalov and Sornette (2011) Yukalov, V. and D. Sornette (2011). Decision theory with prospect interference and entanglement. Theory and Decision 70, 283–328.

- Yukalov and Sornette (2010) Yukalov, V. I. and D. Sornette (2010). Mathematical Structure of Quantum Decision Theory. Advances in Complex Systems, 13(5), 659–698.