∎

11email: g.damico@unich.it 22institutetext: Dipartimento di Scienze Economiche e Aziendali, Università degli studi di Cagliari, 09123 Cagliari, Italy

22email: fpetroni@unica.it 33institutetext: Dipartimento di Ingegneria Meccanica, Energetica e Gestionale, Università degli studi dell’Aquila, 67100 L’Aquila, Italy

33email: flavioprattico@gmail.com

Performability analysis of the second order semi-Markov chains: an application to wind energy production

Abstract

In this paper a general second order semi-Markov reward model is presented. Equations for the higher order moments of the reward process are presented for the first time and applied to wind energy production. The application is executed by considering a database, freely available from the web, that includes wind speed data taken from L.S.I. - Lastem station (Italy) and sampled every 10 minutes. We compute the expectation and the variance of the total energy produced by using the commercial blade Aircon HAWT - 10 kW.

Keywords:

semi-Markov chains reward process wind speed1 Introduction

Discrete time homogeneous semi-Markov chains have been recognized as a flexible and efficient tool in the modelling of stochastic systems. Recent results and applications are retrievable in barb04 ; jans07 ; dami12a . The idea to link rewards to the occupancy of a semi-Markov state led to the construction of semi-Markov reward processes. These processes have been studied in howa71 and since then many developments and applications have been discussed. Non-homogeneous semi-Markov reward processes were defined in dedo86 . A method of computing the distribution of performability in a semi-Markov reward process was discussed in ciar90 . The asymptotic behaviour of a time homogeneous semi-Markov reward process was studied in solt98 . More recent developments includes the derivations of higher order moments of the homogeneous semi-Markov reward process with initial backward (sten06 ) and for the non-homogeneous case (sten07 ), both the papers presented applications in the field of disability insurance. In papa07 the reward paths in non-homogeneous semi-Markov systems in discrete time are examined with stochastic selection of the transition probabilities. The mean entrance probabilities and the mean rewards in the course of time are evaluated. This paper has been further generalized in papa12 . Finally in the paper by dami13b duration dependent non-homogeneous semi-Markov chains were proposed in a disability insurance model.

In this paper we generalize some of the previous contributions by defining and analyzing the second order semi-Markov reward process in state and duration and giving relations for computing the higher order moments of this process. Moreover, we propose to employ a matrix notation that makes calculations easier and also provides a compact form for equations of moments of the reward process. The second order semi-Markov model in state and duration constitutes a generalization of the semi-Markov chain model because it allows the transition probabilities to vary depending on the last two visited states of the system and on the sojourn time lenght between these states.

The second order semi-Markov model in state and duration was proposed in dami12 were it was applied in the modeling of wind speed. In that paper first and

second order semi-Markov models were proposed with the aim of generating reliable synthetic wind speed data. There, it was shown that all the semi-Markov models perform better

than the Markov chain model in reproducing the statistical properties of wind speed data. In particular, the model recognized as being more suitable is the second order semi-Markov

chain in state and duration. This model has been further investigated in dami13 where classical reliability measures were computed with application

to wind energy production. Continuing the effort in the searching of models ever more able to describe wind speed data, in this paper we apply the theoretical results concerning moments of the reward process to provide methods for computing the accumulated energy produced by a blade in a bounded time interval. The expected total energy produced gives important information on the feasibility of the investment in a wind farm and the riskiness of the investment can be measured in terms of variance, skewness, and kurtosis of the reward process. Finally notice that the technological characteristics of different blades are captured by the permanence reward and consequently we are able to choose among different blades to be installed at a given location.

The paper is divided in this way: first, the second order semi-Markov model in state and duration is presented. Second, the reward structure is introduced and the equations

of the higher order moments of the reward process are determined. Finally, the proposed approach is applied to compute moments of the total energy produced by a commercial blade

applied to real wind speed data.

2 The second order semi-Markov chain in state and duration

In this section we give a short description of the second order semi-Markov chain in state and duration, see dami12 and dami13 for additional results.

Let us consider a finite set of states in which the system can be into and a complete probability space on which we define the following random variables:

| (1) |

They denote the state occupied at the -th transition and the time of the -th transition, respectively. To be more concrete, by we denote the wind speed at the -th transition and by the time of the -th transition of the wind speed.

We assume that

| (2) | ||||

Relation asserts that, the knowledge of the values suffices to give the conditional distribution of the couple whatever the values of the past variables might be. Therefore to make probabilistic forecasting we need the knowledge of the last two visited states and the duration time of the transition between them. For this reason we called this model a second order semi-Markov chains in state and duration.

It should be remarked that in the paper by limn03 were defined nth order semi-Markov chains in continuous time. Anyway the dependence was only on past states and not on durations.

The conditional probabilities

are stored in a matrix of functions named the second order kernel (in state and duration). The element represents the probability that next wind speed will be in speed at time given that the current wind speed is and the previous wind speed state was and the duration in wind speed before of reaching wind speed was equal to units of time.

From the knowledge of the kernel we can define the cumulated second order kernel probabilities:

| (3) | ||||

The process is a second order Markov chain with state space and transition probability matrix . We shall refer to it as the embedded Markov chain.

Define the unconditional waiting time distribution function in states coming from state with duration as

| (4) |

The conditional cumulative distribution functions of the waiting time in each state, given the state subsequently occupied is defined as

| (5) | ||||

Define by . We define the second order (in state and duration) semi-Markov chain as .

For this model ordinary transition probability functions and transition probabilities with initial and final backward recurrence times were defined and computed in dami12 and reliability measures applied to wind energy production were presented in dami13 .

3 The second order semi-Markov reward model in state and duration

In this section, following the line of research in sten07 , we determine recursive equations for higher order moments of the second order semi-Markov reward chain in state and duration.

Let denote the accumulated discounted reward during the time interval defined by the following relation,

| (6) |

where: is the backward recurrence time process, is the sojourn time in state before the transition and with is the one period deterministic discount factor.

The reward measures the performance of the system at time . In our model the actual performance is a function of the current state occupied by the system; it depends on the last two visited states ; it is duration dependent in the current state because it is a function of the backward process and finally it depends on the sojourn time in the past states being dependent on . Our reward model is more general than those considered in sten07 because in that paper the authors considered a first order semi-Markov chain and the permanence reward do depend only on the couple .

Let also denote by the random variable, which has the distribution the same with the conditional distribution for the random variable given that

and let denote by .

In order to propose a matrix representation that simplifies calculations and provides a compact form for next equations we need to introduce the adopted notation and products.

Definition 1

Given two matrices and , their Hadamard matrix product gives the matrix whose generic element is given by:

Definition 2

Let be a matrix and be a vector, their matrix product gives the vector whose elements, for all are expressed by

The first order moment of the reward process is computed in the following Theorem.

Theorem 3.1

The first order moment of the second order semi-Markov chain in state and duration satisfies the following matrix equation:

| (7) | ||||

where

is and is ,

and is the unitary row vector.

Proof: Let consider the random variable . The time of next transition can be greater of or not. Consequently it results that:

| (8) |

In the case we have that

| (9) |

and this event occurs with probability

| (10) | ||||

Then it results that

| (11) |

The elements are stored in the matrix of dimension according to the following rule:

The elements are stored in the matrix of dimension according to the rule:

Consequently the right hand side of can be expressed in matrix form as follows:

| (12) |

In the second case, when , if we consider the next visited state and the time of next transition we have:

| (13) |

The event occurs with probability

| (14) | ||||

Notice that the random variable is independent of the distribution of the joint random variable because the accumulation process has the Markov property at transition times and consequently once the state and the are known its behaviour doesn’t depends on the distribution of . Then by taking the expectation in we get

| (15) | ||||

The elements are stored in the matrix of dimension according to the rule:

Then become the elements of the vector where is the unitary row vector.

Having defined these matrices it is simple to realize that is a vector and

This argument, applied also to the second term on the r.h.s. of equation , allows to represent in matrix form as:

| (16) |

A substitution of and in concludes the proof.

By using similar techniques it is possible to get recursive equations for the higher order moments of the reward process.

Corollary 1

The higher order moments of the reward process satisfy the following equation:

| (17) | ||||

Proof:

| (18) | ||||

In the case we have that

| (19) |

and this event occurs with probability , see (LABEL:tre). Consequently it results that

| (20) |

In the opposite case, when , we have that

| (21) | ||||

The event occurs with probability .

Then, by using the already mentioned independence between and the joint random variable , by taking the expectation in we get:

| (22) | ||||

If we substitute and in and we represent the resulting expression in matrix form we obtain the equation .

Remark 1

If and we have that

then the second order semi-Markov reward chain model in state and duration collapses in a standard semi-Markov reward chain model and we recover exactly the results by sten07 .

Remark 2

The adopted matrix notation for the moments of the second order semi-Markov reward chain in state and duration permits the computation of the moments with no more difficulties as compared to those necessary for the standard semi-Markov chain reward model.

4 Application to wind energy production

In two previous papers dami12 ; dami13 we showed that wind speed can be well described by a second order semi-Markov process. Given these results we try to verify here if the reward model, described in the previous section, is able to well describe the production of energy by a wind turbine. The data used in this analysis are freely available from . The database is composed of about 230000 wind speed measures ranging from 0 to 16 with a sample frequency of 10 minutes. More accurate information about our database can be found in dami12 ; dami13 .

The state space of wind speed has been discretized into 8 states chosen to cover all the wind speed distribution. The state space is numerically represented by the set . From the discretized trajectory of the wind speed process

we have to estimate the probabilities and . The quantity is the censored sojourn time in the last wind speed state . First of all we introduce the following counting processes:

| (23) |

Formula expresses the number of transitions from the state to the state with a sojourn time which are preceded by a transition from the state into the state with sojourn time equal to .

| (24) |

Formula expresses the number of transitions from the state to the state which are preceded by a transition from the state into the state with sojourn time equal to .

| (25) |

Formula expresses the number of transitions from the state into the state with sojourn time equal to .

The transition probabilities of the embedded Markov chain

can be estimated by

| (26) |

The estimation of the conditional waiting time distributions is executed by considering the corresponding probability mass functions

which can be estimated by

| (27) |

If then . If then .

Starting from estimators and it is possible to obtain estimators of all the quantities of interest through a plug-in procedure.

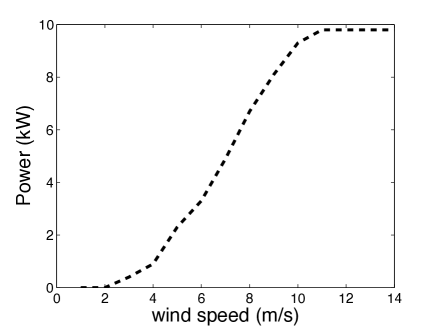

To have a realistic energy production we choose a commercial wind turbine, a 10 kW Aircon HAWT with a power curve given in Figure 1.

The power curve of a wind turbine represents how it produces energy as a function of the wind speed. In this case we have no production of energy in the interval 0-2 , the wind turbine produces energy linearly from 3 to 10 , then, with increasing wind speed the production remains constant until the limit of wind speed in which the wind turbine is stopped for structural reason. Note that the power curve is a graphical representation of the rewards . In this application the rewards depend only on the present wind speed and is settled to be zero.

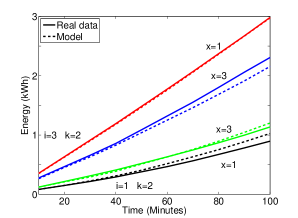

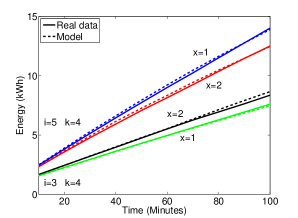

In Figure 2 we compare the average cumulated energy produced by real data and the expected value as calculated using formula where . The comparison is made by varying the sojourn time and the starting state. Particularly, the cumulated energy is plotted for two different initial states i maintaining constant the current state k for two different sojourn times x. Left and right panel of the figure have different values for the current speed state.

It is possible to note that all the cumulated energies plotted above depend strongly on the initial and current states and that there is also a great dependence on the sojourn time . In fact, the expected value has different values also if only the sojourn time is changed keeping constant initial states and final state . For example, from Figure 2 left panel it is possible to see that

while

This reveals that it is important to dispose of a model that is able to distinguish between these different situations which are determined only from a different duration of permanence in the initial state before making a transition to the current state . Models based on Markov chains or classical semi-Markov chain are unable to capture this important effect that our second order semi-Markov chain in state and duration reproduces according to the real data.

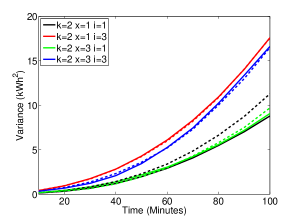

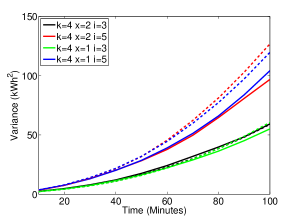

In Figure 3 we compare the second central moment of the reward process again for real data and as obtained from the model calculated according to equation .

Also in this case it is possible to recognize that the model describes well real data behavior especially when the dependence from current states, past states and sojourn times is concerned. In this case the dependence is less evident but still present.

5 Conclusion

The purposes of this paper is to provide theoretical methods for computing the moments of a second order semi-Markov reward process in state and duration. The model is then used also to provide theoretical methods for computing the cumulated energy produced by a blade in a temporal interval . We have reached this aim by modeling wind speed as a second order semi-Markov process. All the equations for the reward process are then derived under this hypothesis. Our model is tested against real data on wind speed freely available from the web. We have shown that the proposed model is able to reproduce well the behavior of real data as far as energy production from wind speed is concerned. In particular, we have shown that the cumulated energy produced by a commercial blade does depend on the initial state i, the current state k and on the sojourn times x. These results confirm the second order semi-Markov hypothesis.

References

- (1) Barbu, V., Boussemart, M. and Limnios, N. (2004). Discrete time semi-Markov model for reliability and survival analysis. Communications in Statistics: Theory and Methods, 33, 2833-2868.

- (2) Janssen J, Manca R (2007) Semi-Markov risk models for finance insurance and reliability. Springer.

- (3) G. D’Amico, F. Petroni, A semi-Markov model for price returns, Physica A (2012) 4867-4876.

- (4) Howard RA (1971) Dynamic probabilistic systems: semi-Markov and decision processes, vol II. Dover.

- (5) De Dominicis R. and R.Manca, Some new results on the transient behavior of semi-Markov reward processes. Methods Oper Res, 54: 387-397

- (6) G. Ciardo, M.A. Raymonf, B. Sericola, K.S. Trivedi, Performability analysis using semi-Markov reward processes, IEEE Transactions on Computers (10), (1990), 1251-1264.

- (7) A.R. Soltani, K. Khorshidian, Reward Processes for semi-Markov processes: asymptotic behaviour, J. Appl. Prob. , (1998), 833-842.

- (8) F. Stenberg, R. Manca, D. Silvestrov, Semi Markov reward models for disability insurance. Theory Stoch Proces (28), no. 3-4: 239-254.

- (9) F. Stenberg, R. Manca, D. Silvestrov, An algorithmic approach to discrete time non-homogeneous backward semi-Markov reward processes with an application to disability insurance. Methodology and Computing in Applied Probability (2007) 497-519.

- (10) A.A. Papadopoulou, G. Tsaklidis, Some Reward Paths in Semi-Markov Models with Stochastic Selection of the Transition Probabilities. Methodology and Computing in Applied Probability (3) (2007) 399-411.

- (11) A.A. Papadopoulou, G. Tsaklidis, S. McClean, L. Garg, On the moments and the Distribution of the Cost of a semi-Markov Model for Healthcare Systems. Methodology and Computing in Applied Probability (3) (2012) 717-737.

- (12) G. D’Amico, Guillen M. and R. Manca, Semi-Markov Disability Insurance Models To appear in Communications in Statistics - Theory and Methods 2013.

- (13) G. D’Amico, Petroni F. and F. Prattico, First and second order semi-Markov chains for wind speed modeling, Physica A: Statistical Mechanics and its Applications, 392(5), 1194-1201.

- (14) G. D’Amico, Petroni F. and F. Prattico, Reliability measures of second order semi-Markov chain with application to wind energy production Journal of Renewable Energy, Volume 2013, Article ID 368940.

- (15) N. Limnios, G. Oprişan. An introduction to Semi-Markov Processes with Application to Reliability, In D.N. Shanbhag and C.R. Rao, eds., Handbook of Statistics, 21, (2003), 515-556.