Communication-Efficient Algorithms for

Statistical Optimization

\nameYuchen Zhang1\emailyuczhang@eecs.berkeley.edu

\nameJohn C. Duchi1\emailjduchi@eecs.berkeley.edu

\nameMartin J. Wainwright1,2\emailwainwrig@berkeley.edu

\addr1Department of Electrical Engineering and

Computer Science

2Department of Statistics

University of California, Berkeley

Berkeley, CA 94720-1776 USA

Abstract

We analyze two communication-efficient algorithms for distributed

optimization in statistical settings involving large-scale data

sets. The first algorithm is a standard averaging method that

distributes the data samples evenly to

machines, performs separate minimization on each subset, and then

averages the estimates. We provide a sharp analysis of this average

mixture algorithm, showing that under a reasonable set of conditions,

the combined parameter achieves mean-squared error (MSE) that decays

as . Whenever

, this guarantee matches the best

possible rate achievable by a centralized algorithm having access to

all samples. The second algorithm is a novel method,

based on an appropriate form of bootstrap subsampling. Requiring only

a single round of communication, it has mean-squared error that decays

as , and so

is more robust to the amount of parallelization. In addition, we show

that a stochastic gradient-based method attains mean-squared error

decaying as , easing computation at the expense of a potentially

slower MSE rate. We also provide an experimental evaluation of our

methods, investigating their performance both on simulated data and on

a large-scale regression problem from the internet search domain. In

particular, we show that our methods can be used to efficiently solve

an advertisement prediction problem from the Chinese SoSo Search

Engine, which involves logistic regression with samples and covariates.

Many procedures for statistical estimation are based on a form of

(regularized) empirical risk minimization, meaning that a parameter of

interest is estimated by minimizing an objective function defined by

the average of a loss function over the data. Given the current

explosion in the size and amount of data available in statistical

studies, a central challenge is to design efficient algorithms for

solving large-scale problem instances. In a centralized setting,

there are many procedures for solving empirical risk minimization

problems, among them standard convex programming approaches

(e.g. Boyd and Vandenberghe, 2004) as well as stochastic approximation and

optimization algorithms (Robbins and Monro, 1951; Hazan et al., 2006; Nemirovski et al., 2009). When the size of the dataset becomes extremely

large, however, it may be infeasible to store all of the data on a

single computer, or at least to keep the data in memory. Accordingly,

the focus of this paper is the study of some distributed and

communication-efficient procedures for empirical risk minimization.

Recent years have witnessed a flurry of research on distributed

approaches to solving very large-scale statistical optimization

problems. Although we cannot survey the literature adequately—the

papers Nedić and Ozdaglar (2009); Ram et al. (2010); Johansson et al. (2009); Duchi et al. (2012a); Dekel et al. (2012); Agarwal and Duchi (2011); Recht et al. (2011); Duchi et al. (2012b)

and references therein contain a sample of relevant work—we touch on

a few important themes here. It can be difficult within a purely

optimization-theoretic setting to show explicit benefits arising from

distributed computation. In statistical settings, however, distributed

computation can lead to gains in computational efficiency, as shown by a

number of authors (Agarwal and Duchi, 2011; Dekel et al., 2012; Recht et al., 2011; Duchi et al., 2012b). Within the family of distributed algorithms, there

can be significant differences in communication complexity: different

computers must be synchronized, and when the dimensionality of the

data is high, communication can be prohibitively expensive. It is thus

interesting to study distributed estimation algorithms that require

fairly limited synchronization and communication while still enjoying

the greater statistical accuracy that is usually associated

with a larger dataset.

With this context, perhaps the simplest algorithm for distributed

statistical estimation is what we term the average mixture

(Avgm) algorithm. It is an appealingly simple method: given

different machines and a dataset of size ,

first assign to each machine a (distinct) dataset of size , then have each machine compute the

empirical minimizer on its fraction of the data, and

finally average all the parameter estimates across the

machines. This approach has been studied for some classification and

estimation problems by Mann et al. (2009)

and McDonald et al. (2010), as well as for certain stochastic

approximation methods by Zinkevich et al. (2010). Given an empirical

risk minimization algorithm that works on one machine, the procedure

is straightforward to implement and is extremely communication

efficient, requiring only a single round of communication. It is also

relatively robust to possible failures in a subset of machines and/or

differences in speeds, since there is no repeated synchronization.

When the local estimators are all unbiased, it is clear that the the

Avgm procedure will yield an estimate that is essentially as good as

that of an estimator based on all samples. However,

many estimators used in practice are biased, and so it is natural to

ask whether the method has any guarantees in a more general setting.

To the best of our knowledge, however, no work has shown rigorously

that the Avgm procedure generally has greater

efficiency than the naive approach of using samples on a single machine.

This paper makes three main contributions. First, in

Section 3, we provide a sharp analysis of the

Avgm algorithm, showing that under a reasonable set of conditions on

the population risk, it can indeed achieve substantially better rates

than the naive approach. More concretely, we provide bounds on the

mean-squared error (MSE) that decay as . Whenever the number of machines

is less than the number of samples per machine,

this guarantee matches the best possible rate achievable by a

centralized algorithm having access to all samples. In the special case of optimizing log likelihoods,

the pre-factor in our bound involves the trace of the Fisher

information, a quantity well-known to control the fundamental limits

of statistical estimation. We also show how the result extends to

stochastic programming approaches, exhibiting a stochastic

gradient-descent based procedure that also attains convergence rates

scaling as , but with slightly worse

dependence on different problem-specific parameters.

Our second contribution is to develop a novel extension of simple

averaging. It is based on an appropriate form of

resampling (Efron and Tibshirani, 1993; Hall, 1992; Politis et al., 1999), which we refer to

as the subsampled average mixture (Savgm) approach. At a high

level, the Savgm algorithm distributes samples evenly among

processors or computers as before, but instead of simply

returning the empirical minimizer, each processor further subsamples

its own dataset in order to estimate the bias of its own estimate, and

returns a subsample-corrected estimate. We establish that the

Savgm algorithm has mean-squared error decaying as

. As long as

, the subsampled method again matches the

centralized gold standard in the first-order term, and has a

second-order term smaller than the standard averaging approach.

Our third contribution is to perform a detailed empirical evaluation

of both the Avgm and Savgm procedures, which we present in

Sections 4 and 5. Using

simulated data from normal and non-normal regression models, we

explore the conditions under which the Savgm algorithm yields better

performance than the Avgm algorithm; in addition, we study the

performance of both methods relative to an oracle baseline that uses

all samples. We also study the sensitivity of the

algorithms to the number of splits of the data, and in the

Savgm case, we investigate the sensitivity of the method to the

amount of resampling. These simulations show that both Avgm and

Savgm have favorable performance, even when compared to the

unattainable “gold standard” procedure that has access to all

samples. In Section 5, we

complement our simulation experiments with a large logistic regression

experiment that arises from the problem of predicting whether a user

of a search engine will click on an advertisement. This experiment is

large enough—involving

samples in dimensions with a storage size of

approximately 55 gigabytes—that it is difficult to solve efficiently

on one machine. Consequently, a distributed approach is essential to

take full advantage of this data set. Our experiments on this

problem show that Savgm—with the resampling and correction

it provides—gives substantial performance benefits over naive

solutions as well as the averaging algorithm Avgm.

2 Background and problem set-up

We begin by setting up our decision-theoretic framework for empirical

risk minimization, after which we describe our algorithms and the

assumptions we require for our main theoretical results.

2.1 Empirical risk minimization

Let

be a collection of real-valued and convex loss functions, each defined

on a set containing the convex set . Let

be a probability distribution over the sample space

. Assuming that each function is -integrable, the population risk is given by

(1)

Our goal is to estimate the parameter vector minimizing the population

risk, namely the quantity

(2)

which we assume to be unique. In practice, the population distribution

is unknown to us, but we have access to a collection

of samples from the distribution . Empirical

risk minimization is based on estimating by solving the

optimization problem

(3)

Throughout the paper, we impose some regularity conditions on the

parameter space, the risk function , and the instantaneous

loss functions .

These conditions are standard in classical statistical analysis of

-estimators (e.g. Lehmann and Casella, 1998; Keener, 2010). Our first

assumption deals with the relationship of the parameter space to the

optimal parameter .

Assumption A (Parameters)

The parameter space is a compact convex

set, with and

-radius .

In addition, the risk function is required to have some amount of

curvature. We formalize this notion in terms of the Hessian of

:

Assumption B (Local strong convexity)

The population risk is twice differentiable, and there exists a

parameter such that .

Here denotes the

Hessian matrix of the population objective evaluated at

, and we use to denote the positive semidefinite

ordering (i.e., means that is positive

semidefinite.) This local condition is milder than a global strong

convexity condition and is required to hold only for the population

risk evaluated at . It is worth observing that

some type of curvature of the risk is required for any method to

consistently estimate the parameters .

2.2 Averaging methods

Consider a data set consisting of

samples, drawn i.i.d. according to the distribution

. In the distributed setting, we divide this

-sample data set evenly and uniformly at random among a

total of processors. (For simplicity, we have assumed the

total number of samples is a multiple of .) For , we let denote the data set assigned

to processor ; by construction, it is a collection of

samples drawn i.i.d. according to , and the samples in

subsets and are independent for . In addition, for each processor we define the (local)

empirical distribution and empirical objective

via

(4)

With this notation, the Avgm algorithm is very simple to

describe:

Average mixture algorithm

(1)

For each , processor uses

its local dataset to compute the local empirical

minimizer

(5)

(2)

These local estimates are then averaged

together—that is, we compute

(6)

The subsampled average mixture (Savgm) algorithm is based on an

additional level of sampling on top of the first, involving a fixed

subsampling rate . It consists of

the following additional steps:

Subsampled average mixture algorithm

(1)

Each processor draws a subset of size

by sampling uniformly at random without

replacement from its local data set .

(2)

Each processor computes both the local empirical

minimizers from equation (5)

and the empirical minimizer

(7)

(3)

In addition to the previous

average (6), the Savgm algorithm computes the

bootstrap average , and then returns the weighted

combination

(8)

The intuition for the weighted estimator (8) is

similar to that for standard bias correction procedures using the bootstrap or

subsampling (Efron and Tibshirani, 1993; Hall, 1992; Politis et al., 1999). Roughly speaking, if is the bias of the first estimator, then we may

approximate by the subsampled estimate of bias . Then, we use the fact that

to argue that . The re-normalization

enforces that the

relative “weights” of and sum to 1.

The goal of this paper is to understand under what

conditions—and in what sense—the

estimators (6) and (8)

approach the oracle performance, by which we mean the error of

a centralized risk minimization procedure that is given access to all

samples.

Notation:

Before continuing, we define the remainder of our notation. We use

to denote the usual Euclidean norm . The -operator norm of a

matrix is its maximum singular value,

defined by

A convex function is -strongly convex on a set if for arbitrary we have

(If is not differentiable, we may replace with any

subgradient of .) We let denote the Kronecker product,

and for a pair of vectors , we define the outer product . For a three-times differentiable function ,

we denote the third derivative tensor by , so that for

each the operator is linear and satisfies the relation

We denote the indicator function of an event by ,

which is 1 if is true and 0 otherwise.

3 Theoretical results

Having described the Avgm and Savgm algorithms, we now turn to

statements of our main theorems on their statistical properties, along

with some consequences and comparison to past work.

3.1 Smoothness conditions

In addition to our previously stated assumptions on the population

risk, we require regularity conditions on the empirical risk

functions. It is simplest to state these in terms of the functions

, and we note that, as with

Assumption B, we require these to hold

only locally around the optimal point , in particular

within some Euclidean ball of

radius .

Assumption C (Smoothness)

There are finite constants such that the first and

the second partial derivatives of exist and satisfy the bounds

In addition, for any , the Hessian

matrix is

-Lipschitz continuous, meaning that

(9)

We require that and

for some finite constant .

It is an important insight of our analysis that some type of

smoothness condition on the Hessian matrix, as in the Lipschitz

condition (9), is essential in order for simple

averaging methods to work. This necessity is illustrated by the

following example:

Example 1 (Necessity of Hessian conditions)

Let be a Bernoulli variable with parameter , and

consider the loss function

(10)

where is the indicator of the

event . The associated population risk is

. Since , the

population risk is strongly convex and smooth, but it has

discontinuous second derivative. The unique minimizer of the

population risk is , and by an asymptotic expansion

given in Appendix A, it can be

shown that .

Consequently, the bias of is ,

and the Avgm algorithm using

observations must suffer mean squared error .

The previous example establishes the necessity of a smoothness

condition. However, in a certain sense, it is a pathological case:

both the smoothness condition given in

Assumption C and the local strong convexity

condition given in Assumption B are

relatively innocuous for practical problems. For instance, both

conditions will hold for standard forms of regression, such as linear

and logistic, as long as the population data covariance matrix

is not rank deficient and the data has suitable moments. Moreover, in

the linear regression case, one has .

3.2 Bounds for simple averaging

We now turn to our first theorem that provides guarantees on the

statistical error associated with the Avgm procedure. We recall

that denotes the minimizer of the population objective

function , and that for each , we

use to denote a dataset of independent samples.

For each , we use to denote a minimizer

of the empirical risk for the dataset , and we define the

averaged vector . The following result bounds the mean-squared error

between this averaged estimate and the minimizer of the

population risk.

Theorem 1

Under Assumptions A

through C, the mean-squared error is upper

bounded as

(11)

where is a numerical constant.

A slightly weaker corollary of

Theorem 1 makes it easier to parse. In

particular, note that

(12)

where step (i) follows from the inequality , valid for any matrix and vector ; and

step (ii) follows from Assumption B.

In addition, Assumption C implies

, and

putting together the pieces, we have established the following.

This upper bound shows that the leading term decays proportionally to

, with the pre-factor depending inversely on

the strong convexity constant and growing

proportionally with the bound on the loss gradient.

Although easily interpretable, the upper bound (13)

can be loose, since it is based on the relatively weak series of

bounds (12).

The leading term in our original upper

bound (11) involves the product of the gradient

with the inverse Hessian. In many

statistical settings, including the problem of linear regression, the

effect of this matrix-vector multiplication is to perform some type of

standardization. When the loss is actually the negative log-likelihood

for a parametric family of models

, we can make this intuition precise. In

particular, under suitable regularity conditions (e.g. Lehmann and Casella, 1998, Chapter

6), we can define the Fisher information matrix

Recalling that is the total number of samples

available, let us define the neighborhood . Then under our assumptions, the

Hájek-Le Cam minimax theorem (van der Vaart, 1998, Theorem 8.11) guarantees

for any estimator based on

samples that

In addition to the conditions of Theorem 1,

suppose that the loss functions are the

negative log-likelihood for a

parametric family . Then the mean-squared error is upper bounded as

where is a numerical constant.

Proof:

Rewriting the log-likelihood in the notation of

Theorem 1, we have and

all we need to note is that

Now apply the linearity of the trace and use the fact that

.

Except for the factor of two in the bound,

Corollary 3 shows that

Theorem 1 essentially achieves the best

possible result. The important aspect of our bound, however, is that

we obtain this convergence rate without calculating an estimate on all

samples: instead, we calculate

independent estimators, and then average them to attain the

convergence guarantee. We remark that an inspection of our proof shows

that, at the expense of worse constants on higher order terms, we can

reduce the factor of on the leading term in

Theorem 1 to for

any constant ; as made clear by

Corollary 3, this is

unimprovable, even by constant factors.

As noted in the introduction, our bounds are certainly to be expected

for unbiased estimators, since in such cases averaging

independent solutions reduces the variance by . In this

sense, our results are similar to classical distributional convergence

results in -estimation: for smooth enough problems, -estimators

behave asymptotically like averages (van der Vaart, 1998; Lehmann and Casella, 1998),

and averaging multiple independent realizations reduces their

variance. However, it is often desirable to use biased estimators,

and such bias introduces difficulty in the analysis, which we explore

more in the next section. We also note that in contrast to classical

asymptotic results, our results are applicable to finite samples and

give explicit upper bounds on the mean-squared error. Lastly, our

results are not tied to a specific model, which allows for fairly

general sampling distributions.

3.3 Bounds for subsampled mixture averaging

When the number of machines is relatively small,

Theorem 1 and

Corollary 2 show that the convergence rate

of the Avgm algorithm is mainly determined by the first term in the

bound (11), which is at most

. In contrast, when

the number of processors grows, the second term in the

bound (11), in spite of being

, may have non-negligible effect. This issue is

exacerbated when the local strong convexity parameter

of the risk is close to zero or the Lipschitz continuity

constant of is large. This concern motivated our

development of the subsampled average mixture (Savgm) algorithm, to

which we now return.

Due to the additional randomness introduced by the subsampling in

Savgm, its analysis requires an additional smoothness condition. In

particular, recalling the Euclidean -neighborhood of

the optimum , we require that the loss function is

(locally) smooth through its third derivatives.

Assumption D (Strong smoothness)

For each , the third derivatives

of are -Lipschitz continuous,

meaning that

where for some constant

.

It is easy to verify that

Assumption D holds for least-squares

regression with . It also holds for

various types of non-linear regression problems (e.g., logistic,

multinomial etc.) as long as the covariates have finite eighth

moments.

With this set-up, our second theorem establishes that

bootstrap sampling yields improved performance:

Theorem 4

Under Assumptions A

through D, the output of the bootstrap

Savgm algorithm has mean-squared error bounded as

(14)

for a numerical constant .

Comparing the conclusions of Theorem 4 to those

of Theorem 1, we see that the the

term in the bound (11) has

been eliminated. The reason for this elimination is that subsampling

at a rate reduces the bias of the Savgm algorithm to

, whereas in contrast, the bias of the

Avgm algorithm induces terms of order .

Theorem 4 suggests that the performance of the

Savgm algorithm is affected by the subsampling rate ; in

order to minimize the upper bound (14) in the regime

, the optimal choice is of the form

where . Roughly, as the number of machines becomes

larger, we may increase , since we enjoy averaging affects

from the Savgm algorithm.

Let us consider the relative effects of having larger numbers of

machines for both the Avgm and Savgm algorithms, which

provides some guidance to selecting in practice. We

define to be the asymptotic variance. Then to

obtain the optimal convergence rate of , we

must have

(15)

in Theorem 1. Applying the bound of

Theorem 4, we find that to obtain the same rate

we require

Now suppose that we replace with as in the previous paragraph. Under the conditions

and , we then find that

(16)

Comparing inequalities (15)

and (16), we see that in both cases

may grow polynomially with the global sample size while

still guaranteeing optimal convergence rates. On one hand, this

asymptotic growth is faster in the subsampled

case (16); on the other hand, the dependence

on the dimension of the problem is more stringent than the

standard averaging case (15). As the local

strong convexity constant of the population risk

shrinks, both methods allow less splitting of the data, meaning that

the sample size per machine must be larger. This limitation is

intuitive, since lower curvature for the population risk means that

the local empirical risks associated with each machine will inherit

lower curvature as well, and this effect will be exacerbated with a

small local sample size per machine. Averaging methods are, of

course, not a panacea: the allowed number of partitions does

not grow linearly in either case, so blindly increasing the number of

machines proportionally to the total sample size will

not lead to a useful estimate.

In practice, an optimal choice of may not be apparent, which

may necessitate cross validation or another type of model

evaluation. We leave as intriguing open questions whether computing

multiple subsamples at each machine can yield improved performance or

reduce the variance of the Savgm procedure, and whether using

estimates based on resampling the data with replacement, as opposed to

without replacement as considered here, can yield improved

performance.

3.4 Time complexity

In practice, the exact empirical minimizers assumed in

Theorems 1 and 4 may be

unavailable. Instead, we need to use a finite number of iterations of

some optimization algorithm in order to obtain reasonable

approximations to the exact minimizers. In this section, we sketch an

argument that shows that both the Avgm algorithm and the

Savgm algorithm can use such approximate empirical minimizers, and

as long as the optimization error is sufficiently small, the resulting

averaged estimate achieves the same order-optimal statistical error.

Here we provide the arguments only for the Avgm algorithm; the

arguments for the Savgm algorithm are analogous.

More precisely, suppose that each processor runs a finite number of

iterations of some optimization algorithm, thereby obtaining the

vector as an approximate minimizer of the objective

function . Thus, the vector can be viewed as an

approximate form of , and we let denote the average

of these approximate minimizers, which corresponds to the output of

the approximate Avgm algorithm. With this notation, we have

(17)

where step (i) follows by triangle inequality and the elementary bound

; step (ii) follows by Jensen’s

inequality. Consequently, suppose that processor runs

enough iterations to obtain an approximate minimizer such

that

(18)

When this condition holds, the

bound (17) shows that the

average of the approximate minimizers shares the same

convergence rates provided by Theorem 1.

But how long does it take to compute an approximate minimizer

satisfying condition (18)?

Assuming processing one sample requires one unit of time, we claim

that this computation can be performed in time . In particular, the following two-stage

strategy, involving a combination of stochastic gradient descent (see

the following subsection for more details) and standard gradient

descent, has this complexity:

(1)

As shown in the proof of

Theorem 1, with high probability, the

empirical risk is strongly convex in a ball

of constant radius around

. Consequently, performing stochastic gradient descent

on for iterations

yields an approximate minimizer that falls within

with high probability (e.g. Nemirovski et al., 2009, Proposition

2.1). Note that the radius for local

strong convexity is a property of the population risk we

use as a prior knowledge.

(2)

This initial estimate can be further improved by a few iterations

of standard gradient descent. Under local strong convexity of the objective

function, gradient descent is known to converge at a geometric

rate (see, e.g. Nocedal and Wright, 2006; Boyd and Vandenberghe, 2004), so

iterations will reduce the error to order

. In our case, we have , and

since each iteration of standard gradient descent requires

units of time, a total of time units

are sufficient to obtain a final estimate satisfying

condition (18).

Overall, we conclude that the speed-up of the Avgm

relative to the naive approach of processing all samples on one processor, is at least of order

.

3.5 Stochastic gradient descent with averaging

The previous strategy involved a combination of stochastic gradient

descent and standard gradient descent. In many settings, it may be

appealing to use only a stochastic gradient algorithm, due to their

ease of their implementation and limited computational requirements.

In this section, we describe an extension of

Theorem 1 to the case in which each machine

computes an approximate minimizer using only stochastic gradient descent.

Stochastic gradient algorithms have a lengthy history in

statistics, optimization, and machine learning (Robbins and Monro, 1951; Polyak and Juditsky, 1992; Nemirovski et al., 2009; Rakhlin et al., 2012). Let us begin by briefly

reviewing the basic form of stochastic gradient descent (SGD).

Stochastic gradient descent algorithms iteratively update a parameter

vector over time based on randomly sampled gradient

information. Specifically, at iteration , a sample is

drawn at random from the distribution (or, in the case of

a finite set of data , a

sample is chosen from the data set). The method then

performs the following two steps:

(19)

Here is a stepsize, and the first update

in (19) is a gradient descent step with respect to the

random gradient . The method then projects the

intermediate point back onto the constraint set

(if there is a constraint set). The convergence of SGD methods

of the form (19) has been well-studied, and we refer the

reader to the papers by Polyak and Juditsky (1992), Nemirovski et al. (2009), and

Rakhlin et al. (2012) for deeper investigations.

To prove convergence of our stochastic gradient-based averaging

algorithms, we require the following smoothness and strong convexity

condition, which is an alternative to the

Assumptions B

and C used previously.

Assumption E (Smoothness and Strong Convexity II)

There exists a function such that

and .

There are finite constants and such

that

In addition, the population function is -strongly

convex over the space , meaning that

(20)

Assumption E does not require as many

moments as does Assumption C, but it does

require each moment bound to hold globally, that is, over the entire

space , rather than only in a neighborhood of the

optimal point . Similarly, the necessary curvature—in the

form of the lower bound on the Hessian matrix —is

also required to hold globally, rather than only locally. Nonetheless,

Assumption E holds for many common

problems; for instance, it holds for any linear regression problem in

which the covariates have finite fourth moments and the domain

is compact.

The averaged stochastic gradient algorithm

(SGDavgm) is based on the following two steps:

(1)

Given some constant , each machine performs

iterations of stochastic gradient

descent (19) on its local dataset of

samples using the stepsize ,

then outputs the resulting local parameter .

(2)

The algorithm computes the average .

The following result characterizes the mean-squared error of this

procedure in terms of the constants

Theorem 5

Under Assumptions A

and E, the output of

the Savgm algorithm has mean-squared error upper bounded as

(21)

Theorem 5 shows that the averaged stochastic gradient descent

procedure attains the optimal convergence rate

as a function of the total

number of observations . The constant and

problem-dependent factors

are somewhat worse than those in the earlier results we presented in

Theorems 1 and 4, but the

practical implementability of such a procedure may in some circumstances

outweigh those differences. We also note that the second term of order

may be reduced to for

any by assuming the existence of th moments in

Assumption E; we show this in passing after our

proof of the theorem in Appendix D. It is not clear whether

a bootstrap correction is possible for the stochastic-gradient based

estimator; such a correction could be significant, because the term arising from the bias in the stochastic gradient estimator may

be non-trivial. We leave this question to future work.

4 Performance on synthetic data

In this section, we report the results of simulation studies comparing the

Avgm, Savgm, and SGDavgm methods, as well as a trivial method using only a

fraction of the data available on a single machine. For each of our simulated

experiments, we use a fixed total number of samples , but we vary the number of parallel splits of the data

(and consequently, the local dataset sizes )

and the dimensionality of the problem solved.

For our experiments, we simulate data from one of three regression models:

(22a)

(22b)

(22c)

where , and is a function to be

specified. Specifically, the data generation procedure is as follows.

For each individual simulation, we choose fixed vector

with entries distributed uniformly in (and similarly

for ), and we set . The

models (22a)

through (22c) provide points on a

curve from correctly-specified to grossly mis-specified models, so

models (22b)

and (22c) help us understand the

effects of subsampling in the Savgm algorithm. (In contrast, the

standard least-squares estimator is unbiased for

model (22a).) The noise variable

is always chosen as a standard Gaussian variate

, independent from sample to sample.

In our simulation experiments we use the least-squares loss

The goal in each experiment is to

estimate the vector minimizing . For each simulation, we generate

samples according to either the

model (22a)

or (22c). For each , we estimate using a parallel method with data split into

independent sets of size ,

specifically

(i)

The Avgm method

(ii)

The Savgm method with several settings of the subsampling

ratio

(iii)

The SGDavgm method with stepsize , which gave good performance.

In addition to (i)–(iii), we also estimate with

(iv)

The empirical minimizer of a single split of the data of size

(v)

The empirical minimizer on the full dataset (the oracle solution).

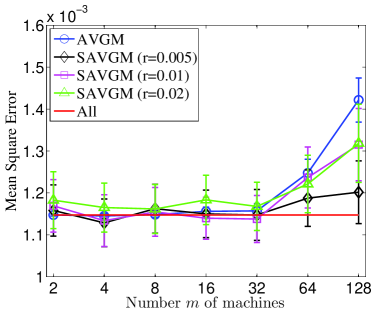

(a)

(b)

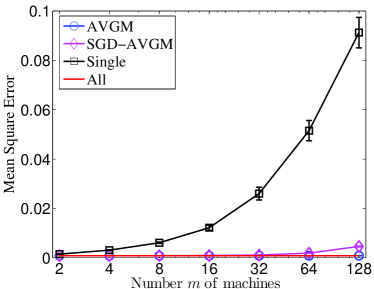

Figure 1: The error

versus number of machines, with standard errors across twenty simulations,

for solving least squares with data generated according to the normal

model (22a). The oracle

least-squares estimate using all samples is given by the

line “All,” while the line “Single” gives the performance of the naive

estimator using only samples.

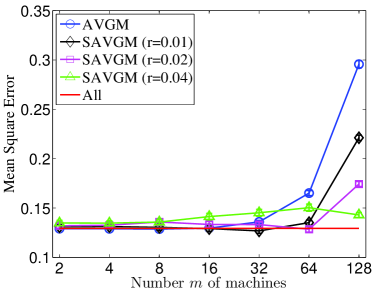

(a)

(b)

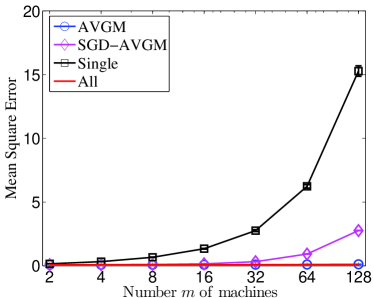

Figure 2: Comparison of Avgm and

SGDavgm methods as in Figure 1 plotted on logarithmic

scale. The plot shows , where

is the oracle least-squares estimator using all data

samples.

4.1 Averaging methods

For our first set of experiments, we study the performance of the averaging

methods (Avgm and Savgm), showing their scaling as the number of splits of

data—the number of machines —grows for fixed and

dimensions and . We use the standard regression

model (22a) to generate the data, and throughout we

let denote the estimate returned by the method under

consideration (so in the Avgm case, for example, this is the vector

). The data samples consist of pairs , where and is the target value. To sample each

vector, we choose five distinct indices in uniformly at

random, and the entries of at those indices are distributed as . For the model (22a), the population optimal

vector is .

In Figure 1, we plot the error of the inferred parameter vector for

the true parameters versus the number of splits ,

or equivalently, the number of separate machines available for use. We

also plot standard errors (across twenty experiments) for each

curve. As a baseline in each plot, we plot as a red line the

squared error of

the centralized “gold standard,” obtained by applying a batch method

to all samples.

From the plots in Figure 1, we can make a few observations. The

Avgm algorithm enjoys excellent performance, as predicted by our theoretical

results, especially compared to the naive solution using only a fraction

of the data. In particular, if is obtained by the

batch method, then Avgm is almost as good as the full-batch baseline even

for as large as , though there is some evident degradation in

solution quality. The SGDavgm (stochastic-gradient with averaging) solution

also yields much higher accuracy than the naive solution, but its performance

degrades more quickly than the Avgm method’s as grows. In higher

dimensions, both the Avgm and SGDavgm procedures have somewhat worse

performance; again, this is not unexpected since in high dimensions the strong

convexity condition is satisfied with lower probability in local datasets.

We present a comparison between the Avgm method and the

SGDavgm method with somewhat more distinguishing power in

Figure 2. For these plots, we compute the gap

between the Avgm mean-squared-error and the unparallel baseline MSE,

which is the accuracy lost due to parallelization or distributing the

inference procedure across multiple machines.

Figure 2 shows that the mean-squared error

grows polynomially with the number of machines , which is

consistent with our theoretical

results. From Corollary 3, we

expect the Avgm method to suffer (lower-order) penalties

proportional to as grows, while

Theorem 5 suggests the somewhat faster growth we see

for the SGDavgm method in Figure 2. Thus,

we see that the improved run-time performance of the

SGDavgm method—requiring only a single pass through the data on

each machine, touching each datum only once—comes at the expense of

some loss of accuracy, as measured by mean-squared error.

4.2 Subsampling correction

(a)

(b)

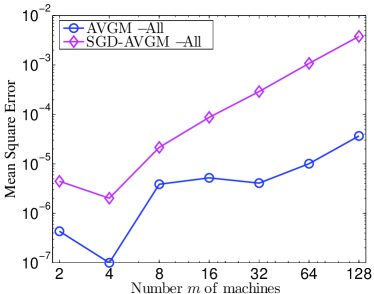

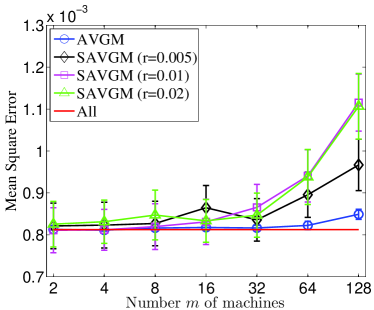

Figure 3: The error plotted against the number of machines for the

Avgm and Savgm methods, with standard errors across twenty

simulations, using the normal regression

model (22a). The oracle estimator is

denoted by the line “All.”

(a)

(b)

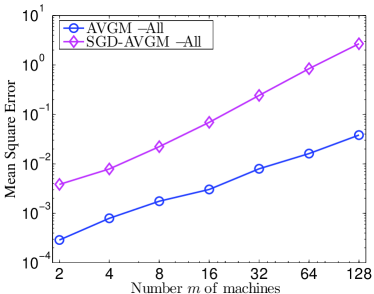

Figure 4: The error plotted against the number of machines for the

Avgm and Savgm methods, with standard errors across twenty

simulations, using the non-normal regression

model (22c). The oracle estimator is

denoted by the line “All.”

We now turn to developing an understanding of the Savgm algorithm in

comparison to the standard average mixture algorithm, developing

intuition for the benefits and drawbacks of the method. Before

describing the results, we remark that for the standard regression

model (22a), the least-squares solution is

unbiased for , so we expect subsampled averaging to yield

little (if any) improvement. The Savgm method is essentially aimed

at correcting the bias of the estimator , and de-biasing an

unbiased estimator only increases its variance. However, for the

mis-specified models (22b)

and (22c) we expect to see some

performance gains. In our experiments, we use multiple sub-sampling

rates to study their effects, choosing

, where we recall that the output

of the Savgm algorithm is the vector .

We begin with experiments in which the data is generated as in the

previous section. That is, to generate a feature vector , choose five distinct indices in uniformly

at random, and the entries of at those indices are distributed as

. In Figure 3, we plot the results

of simulations comparing Avgm and Savgm with data generated from

the normal regression model (22a). Both

algorithms have have low error rates, but the Avgm method is

slightly better than the Savgm method for both values of the

dimension and all and sub-sampling rates . As expected,

in this case the Savgm method does not offer improvement over Avgm,

since the estimators are unbiased. (In Figure 3(a),

we note that the standard error is in fact very small, since the

mean-squared error is only of order .)

To understand settings in which subsampling for bias correction helps, in

Figure 4, we plot mean-square error curves for the

least-squares regression problem when the vector is sampled according to

the non-normal regression model (22c). In

this case, the least-squares estimator is biased for (which, as

before, we estimate by solving a larger regression problem using data samples). Figure 4 shows that both the

Avgm and Savgm method still enjoy good performance; in some cases, the

Savgm method even beats the oracle least-squares estimator for

that uses all samples. Since the Avgm estimate is biased in

this case, its error curve increases roughly quadratically with ,

which agrees with our theoretical predictions in

Theorem 1. In contrast, we see that the

Savgm algorithm enjoys somewhat more stable performance, with increasing

benefit as the number of machines increases. For example, in case of

, if we choose for , choose for and for , then

Savgm has performance comparable with the oracle method that uses all

samples. Moreover, we see that all the values of —at

least for the reasonably small values we use in the experiment—provide

performance improvements over a non-subsampled distributed estimator.

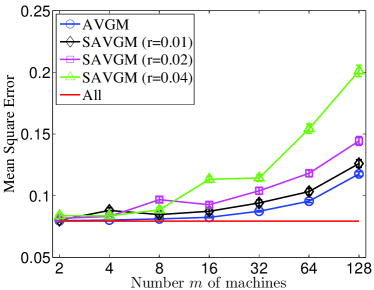

For our final simulation, we plot results comparing Savgm with Avgm in

model (22b), which is mis-specified but still

a normal model. We use a simpler data generating mechanism, specifically, we

draw from a standard -dimensional

normal, and is chosen uniformly in ; in this case, the population

minimizer has the closed form .

Figure 5 shows the results for dimensions and performed over experiments (the standard errors are too

small to see). Since the model (22b) is not

that badly mis-specified, the performance of the Savgm method improves

upon that of the Avgm method only for relatively large values of ,

however, the performance of the Savgm is always at least as good as

that of Avgm.

Figure 5: The error plotted against the number of machines for

the Avgm and Savgm methods using regression

model (22b).

5 Experiments with advertising data

Table 1: Features used in online advertisement prediction problem.

Feature Name

Dimension

Description

Query

20000

Word tokens appearing in the query.

Gender

3

Gender of the user

Keyword

20000

Word tokens appearing in the purchase keywords.

Title

20000

Word tokens appearing in the ad title.

Advertiser

39191

Advertiser’s ID

AdID

641707

Advertisement’s ID.

Age

6

Age of the user

UserFreq

25

Number of appearances of the same user.

Position

3

Position of advertisement on search page.

Depth

3

Number of ads in the session.

QueryFreq

25

Number of occurrences of the same query.

AdFreq

25

Number of occurrences of the same ad.

QueryLength

20

Number of words in the query.

TitleLength

30

Number of words in the ad title.

DespLength

50

Number of words in the ad description.

QueryCtr

150

Average click-through-rate for query.

UserCtr

150

Average click-through-rate for user.

AdvrCtr

150

Average click-through-rate for advertiser.

WordCtr

150

Average click-through-rate for keyword advertised.

UserAdFreq

20

Number of times this user sees an ad.

UserQueryFreq

20

Number of times this user performs a search.

Predicting whether a user of a search engine will click on an

advertisement presented to him or her is of central importance to the

business of several internet companies, and in this section, we

present experiments studying the performance of the Avgm and

Savgm methods for this task. We use a large dataset from the

Tencent search engine, soso.com (Sun, 2012), which contains

641,707 distinct advertisement items with data samples.

Each sample consists of a so-called impression, which in the

terminology of the information retrieval literature (e.g., see the

book by Manning et al. (2008)), is a list containing a user-issued

search, the advertisement presented to the user in response to the

search, and a label indicating whether the user

clicked on the advertisement. The ads in our dataset were presented

to 23,669,283 distinct users.

Transforming an impression into a useable set of regressors is

non-trivial, but the Tencent dataset provides a standard encoding. We

list the features present in the data in Table 1,

along with some description of their meaning. Each text-based

feature—that is, those made up of words, which are Query, Keyword,

and Title—is given a “bag-of-words”

encoding (Manning et al., 2008). This encoding assigns each of 20,000

possible words an index, and if the word appears in the query (or

Keyword or Title feature), the corresponding index in the vector

is set to 1. Words that do not appear are encoded with a zero.

Real-valued features, corresponding to the bottom fifteen features in

Table 1 beginning with “Age”, are binned into a

fixed number of intervals , each of which is assigned an index in

. (Note that the intervals and number thereof vary per feature, and

the dimension of the features listed in Table 1

corresponds to the number of intervals). When a feature falls into a

particular bin, the corresponding entry of is assigned a 1, and

otherwise the entries of corresponding to the feature are 0. Each

feature has one additional value for “unknown.” The remaining

categorical features—gender, advertiser, and advertisement ID

(AdID)—are also given encodings, where only one index of

corresponding to the feature may be non-zero (which indicates the

particular gender, advertiser, or AdID). This combination of encodings

yields a binary-valued covariate vector with dimensions. Note also that the features incorporate

information about the user, advertisement, and query issued, encoding

information about their interactions into the model.

Our goal is to predict the probability of a user clicking a given

advertisement as a function of the covariates in

Table 1. To do so, we use a logistic

regression model to estimate the probability of a click response

where is the unknown regression vector. We use

the negative logarithm of as the loss, incorporating a ridge

regularization penalty. This combination yields instantaneous loss

(23)

In all our experiments, we assume that the population negative log-likelihood

risk has local strong convexity as suggested by

Assumption B. In practice, we use a small

regularization parameter to ensure fast

convergence for the local sub-problems.

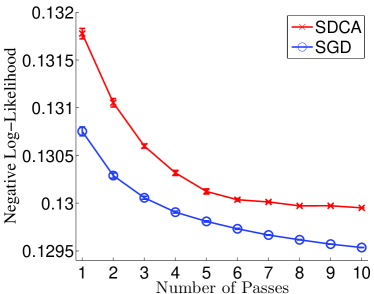

Figure 6: The negative log-likelihood of the output of

the Avgm, Savgm, and stochastic methods on the held-out dataset for the

click-through prediction task. (a) Performance of the Avgm and

Savgm methods versus the number of splits of the

data. (b) Performance of SDCA and SGD baselines as a function of number of

passes through the entire dataset.

For this problem, we cannot evaluate the mean-squared error

, as we do not know the true optimal

parameter . Consequently, we evaluate the performance of an

estimate using log-loss on a held-out dataset. Specifically,

we perform a five-fold validation experiment, where we shuffle the data and

partition it into five equal-sized subsets. For each of our five experiments,

we hold out one partition to use as the test set, using the remaining data as

the training set for inference. When studying the Avgm or

Savgm method, we compute the local estimate via a trust-region

Newton-based method (Nocedal and Wright, 2006) implemented by LIBSVM (Chang and Lin, 2011).

The dataset is too large to fit in the memory of most computers: in total,

four splits of the data require 55 gigabytes. Consequently, it is difficult

to provide an oracle training comparison using the full

samples. Instead, for each experiment, we perform 10 passes of stochastic dual

coordinate ascent (SDCA) (Shalev-Shwartz and Zhang, 2012) and 10 passes of stochastic gradient descent (SGD) through the

dataset to get two rough baselines of the

performance attained by the empirical minimizer for the entire training

dataset. Figure 6(b) shows the hold-out set log-loss after

each of the sequential passes through the training data finishes. Note that

although the SDCA enjoys faster convergence rate on the regularized empirical risk (Shalev-Shwartz and Zhang, 2012),

the plot shows that the SGD has better generalization performance.

In Figure 6(a), we show the average hold-out set log-loss

(with standard errors) of the estimator provided by the

Avgm method versus number of splits of the data , and we also plot

the log-loss of the Savgm method using subsampling ratios of . The plot shows that for small , both Avgm and

Savgm enjoy good performance, comparable to or better than (our proxy for)

the oracle solution using all samples. As the number of

machines grows, however, the de-biasing provided by the subsampled

bootstrap method yields substantial improvements over the standard

Avgm method. In addition, even with splits of the dataset,

the Savgm method gives better hold-out set performance than performing two

passes of stochastic gradient on the entire dataset of samples; with

, Savgm enjoys performance as strong as looping through the

data four times with stochastic gradient descent. This is striking, since

doing even one pass through the data with stochastic gradient descent gives

minimax optimal convergence rates (Polyak and Juditsky, 1992; Agarwal et al., 2012). In

ranking applications, rather than measuring negative log-likelihood, one may

wish to use a direct measure of prediction error; to that end,

Figure 7 shows plots of the area-under-the-curve (AUC)

measure for the

Avgm and Savgm methods; AUC is a well-known measure of prediction error

for bipartite ranking (Manning et al., 2008). Broadly, this plot shows

a similar story to that in Figure 6.

\psfrag{AVGM}{{Avgm}}\psfrag{BAVGM $r=0.1$}{{Savgm}\ $(r=.1)$}\psfrag{BAVGM $r=0.25$}{{Savgm}\ $(r=.25)$}\includegraphics[width=216.81pt]{Images/soso_comparison_auc}Figure 7: The area-under-the-curve (AUC) measure of

ranking error for the output of the Avgm and Savgm methods for the

click-through prediction task.\psfrag{BAVGM $m=128$}{\small{{Savgm}\ $(m=128)$}}\includegraphics[width=195.12767pt]{Images/soso_r_compare}Figure 8:

The log-loss on held-out data for the Savgm method applied with

parallel splits of the data, plotted versus the

sub-sampling rate .

It is instructive and important to understand the sensitivity of the

Savgm method to the value of the

resampling parameter . We explore this question

in Figure 8 using splits, where we plot

the log-loss of the Savgm estimator on the held-out data set versus the

subsampling ratio . We choose because more data splits

provide more variable performance in . For the soso.com ad

prediction data set, the choice achieves the best performance,

but Figure 8 suggests that mis-specifying the ratio is not

terribly detrimental. Indeed, while the performance of Savgm degrades

to that of the Avgm method, a wide range of settings

of give

improved performance, and there does not appear to be a phase transition

to poor performance.

6 Discussion

Large scale statistical inference problems are challenging, and the

difficulty of solving them will only grow as data becomes more

abundant: the amount of data we collect is growing much faster than

the speed or storage capabilities of our computers. Our Avgm, Savgm,

and SGDavgm methods provide strategies for efficiently solving such

large-scale risk minimization problems, enjoying performance

comparable to an oracle method that is able to access the entire large

dataset. We believe there are several interesting questions that

remain open after this work. First, nonparametric estimation problems,

which often suffer superlinear scaling in the size of the data, may

provide an interesting avenue for further study of decomposition-based

methods. Our own recent work has addressed aspects of this challenge

in the context of kernel methods for non-parametric

regression (Zhang et al., 2013). More generally, an understanding

of the interplay between statistical efficiency and communication

could provide an avenue for further research, and it may also be

interesting to study the effects of subsampled or bootstrap-based

estimators in other distributed environments.

Acknowledgments

We thank Joel Tropp for some informative discussions on and references for

matrix concentration and moment inequalities. We also thank Ohad Shamir for

pointing out a mistake in the statements of results related to Theorem 1, and

the editor and reviewers for their helpful comments and feedback. JCD was

supported by the Department of Defence under the NDSEG Fellowship Program and

by a Facebook PhD fellowship. This work was partially funded by Office of

Naval Research MURI grant N00014-11-1-0688 to MJW.

A The necessity of smoothness

Here we show that some version of the smoothness conditions presented

in Assumption C are necessary for averaging

methods to attain better mean-squared error than using only the

samples on a single processor. Given the loss

function (10), let to be the count of 0

samples. Using as shorthand for , we see by

inspection that the empirical minimizer is

For simplicity, we may assume that is odd. In this case, we

obtain that

by the symmetry of the binomial. Adding and subtracting from the term

within the braces, noting that , we

have the equality

If is distributed normally with mean and variance

, then an asymptotic expansion of the binomial

distribution yields

the final equality following from standard calculations, since .

Although Theorem 1 is in terms of bounds on

order moments, we prove a somewhat more general result in

terms of a set of moment

conditions given by

for . (Recall the definition of prior to

Assumption C). Doing so allows sharper

control if higher moment bounds are available. The reader should

recall throughout our arguments that we have assumed

. Throughout the

proof, we use and to indicate the local empirical

objective and empirical minimizer of machine (which have the same

distribution as those of the other processors), and we recall the

notation for the indicator function of the event

.

Before beginning the proof of Theorem 1

proper, we begin with a simple inequality that relates the error term

to an average of the errors , each of which we can bound in turn. Specifically, a bit of

algebra gives us that

(24)

Here we used the definition of the averaged vector and the

fact that for , the vectors and are

statistically independent, they are functions of independent

samples. The upper bound (24) illuminates the

path for the remainder of our proof: we bound each of

and . Intuitively, since our objective is locally

strongly convex by Assumption B, the

empirical minimizing vector is a nearly unbiased estimator

for , which allows us to prove the convergence rates in the

theorem.

We begin by defining three events—which we (later) show hold with

high probability—that guarantee the closeness of and

. In rough terms, when these events hold, the function

behaves similarly to the population risk around the point

; since is locally strongly convex, the minimizer

of will be close to . Recall that

Assumption C guarantees the existence of a

ball of radius such that

for all and any , where

. In

addition, Assumption B guarantees that

. Now, choosing the

potentially smaller radius , we can define the three “good”

events

(25)

We then have the following lemma:

Lemma 6

Under the events , , and previously

defined (25), we have

The proof of Lemma 6 relies on some standard

optimization guarantees relating gradients to minimizers of functions

(e.g. Boyd and Vandenberghe (2004), Chapter 9), although some care is required

since smoothness and strong convexity hold only locally in our

problem. As the argument is somewhat technical, we defer it to

Appendix E.

Our approach from here is to give bounds on and by careful

Taylor expansions, which allows us to bound via our initial

expansion (24). We begin by noting that

whenever the events , , and hold, then

, and moreover, by a Taylor series

expansion of between and , we have

where for

some . By adding and subtracting terms,

we have

(26)

Since , we can define

the inverse Hessian matrix , and setting , we multiply both sides of the Taylor

expansion (26) by to

obtain the relation

(27)

Thus, if we define the matrices and

, equality (27) can be re-written

as

(28)

Note that equation (28) holds when the

conditions of Lemma 6 hold, and otherwise we may

simply assert only that .

Roughly, we expect the final two terms in the error

expansion (28) to be of smaller order

than the first term, since we hope that and additionally that the Hessian differences decrease

to zero at a sufficiently fast rate. We now formalize this intuition.

Inspecting the Taylor expansion (28), we

see that there are several terms of a form similar to ;

using the smoothness Assumption C, we can

convert these terms into higher order terms involving only . Thus, to effectively control the

expansions (27)

and (28), we must show that higher order

terms of the form , for , decrease quickly enough in .

Control of :

Recalling the events (25), we define and then observe that

where we have used the bound

for all , from

Assumption A. Our goal is to prove

that and

that . We move forward with a

two lemmas that lay the groundwork for proving these two facts:

Lemma 7

Under Assumption C, there exist constants

and (dependent only on the moments and

respectively) such that

As an immediate consequence of Lemma 7, we

see that the events and defined

by (25) occur with reasonably high probability. Indeed,

recalling that ,

Boole’s law and the union bound imply

(30)

for some universal constants , where in the

second-to-last line we have invoked the moment bound in

Assumption C. Consequently, we find that

In summary, we have proved the following lemma:

Lemma 8

Let Assumptions B

and C hold. For any

with , we have

where the order statements hold as .

Now recall the matrix defined following

equation (27). The following result controls

the moments of its operator norm:

Lemma 9

For , we have

.

Proof:

We begin by using Jensen’s inequality and

Assumption C to see that

Now we apply the Cauchy-Schwarz inequality and

Lemma 8, thereby obtaining

Lemma 8 allows us to control the first term

from our initial bound (24) almost

immediately. Indeed, using our last Taylor

expansion (28)

and the definition of

the event , we have

where we have applied the inequality . Again

using this same inequality, then applying Cauchy-Schwarz and

Lemmas 8

and 9, we see that

where we have used the fact that to apply Lemma 9.

Combining these results, we obtain the upper bound

(31)

which completes the first part of our proof of

Theorem 1.

Control of :

It remains to consider the term

from our initial error inequality (24). When

the events (25) occur, we know that all derivatives

exist, so we may recursively apply our

expansion (28) of to find that

(32)

where we have introduced as shorthand for the vector on the right hand side.

Thus, with a bit of algebraic manipulation we

obtain the relation

(33)

Now note that thus

Thus, by re-substituting the appropriate quantities

in (33) and applying the

triangle inequality, we have

(34)

Since by assumption, we have

for any , where

step (i) follows from

the inequality (30).

Hölder’s inequality also yields that

Recalling Lemmas 7

and 9, we have

,

and we similarly have . Lastly, we have for

, whence we find that

for any such ,

We can similarly

apply Lemma 8 to the last

remaining term in the inequality (34) to obtain that

for any ,

Applying these two bounds, we find that

(35)

for any such that

and .

In the remainder of the proof, we show that part of the

bound (35) still consists only of

higher-order terms, leaving us with an expression not involving . To that end, note that

by three applications of Hölder’s inequality, the fact that , and Lemmas 7, 8

and 9.

Coupled with our bound (35), we

use the fact that

to obtain

(36)

We focus on bounding the remaining

expectation. We have

the following series of inequalities:

Here step (i) follows from Jensen’s inequality and the fact that

; step (ii) uses the

Cauchy-Schwarz inequality; and step (iii) follows from the fact that

. We have already bounded the first two

terms in the product in our proofs; in particular,

Lemma 7 guarantees that

, while

for some numerical constant (recall

Lemma 9). Summarizing our bounds on

and , we have

(37)

From Assumption C we know that and , and hence we can further simplify the

bound (37) to obtain

for some numerical constant , where we have applied our earlier

inequality (36).

Noting that we may (without loss of

generality) take , then applying this inequality with the

bound (31) on

we previously proved to our decomposition (24)

completes the proof.

Our proof of Theorem 4 begins with a simple inequality

that mimics our first inequality (24) in the proof of

Theorem 1. Recall the definitions of the averaged

vector and subsampled averaged vector . Let

denote the minimizer of the (an arbitrary) empirical risk

, and denote the minimizer of the resampled empirical risk

(from the same samples as ). Then we have

(38)

Thus, parallel to our proof of Theorem 1, it

suffices to bound the two terms in the

decomposition (38)

separately. Specifically, we prove the following two lemmas.

In conjunction, Lemmas 10 and 11

coupled with the decomposition (38)

yield the desired claim. Indeed, applying each

of the lemmas to the decomposition (38), we see

that

The remainder of our argument is devoted to establishing

Lemmas 10 and 11.

Before providing their proofs (in

Appendices C.3

and C.4 respectively), we require some

further set-up and auxiliary results. Throughout the rest of the

proof, we use the notation

for some random variables and to mean that there exists a random

variable such that and .111 Formally, in our proof this will mean that

there exist random vectors , , and that are measurable with

respect to the -field ,

where and .

The symbol may

indicate different random variables throughout a proof and is notational

shorthand for a moment-based big-O notation. We also remark that

if we have , we

have , since .

For shorthand, we also say

that if , which implies that if then

, since

C.1 Optimization Error Expansion

In this section, we derive a sharper asymptotic expansion of the optimization

errors .

Recall our definition of the Kronecker product , where for vectors

we have . With this notation, we have the

following expansion of .

In these lemmas,

denotes a vector for which for a numerical

constant .

We prove Lemma 12 in

Appendix G. The lemma requires

careful moment control over the expansion , leading

to some technical difficulty, but is similar in spirit to the results leading

to Theorem 1.

An immediately analogous result to

Lemma 12

follows for our sub-sampled estimators. Since we use

samples to compute , the second

level estimator, we find

Now that we have given Taylor expansions that describe the behavior of

and , we can prove

Lemmas 10 and 11 (though, as

noted earlier, we defer the proof of Lemma 11 to

Appendix C.4). The key insight is that expectations

of terms involving are nearly the same as expectations

of terms involving , except that some corrections for

the sampling ratio are necessary.

We begin by noting that

(42)

In Lemmas 12

and 13, we

derived expansions for each of the right hand side terms, and since

Lemmas 12

and 13 coupled with the

rewritten

correction (42) yield

(43)

Here the remainder terms follow because of the

term on .

To prove the claim in the lemma, it suffices to show that

(44)

and

(45)

Indeed, these two claims combined with the

expansion (43) yield the

bound (39) in Lemma 10

immediately.

We first consider the difference (44).

To make things notationally simpler, we define functions and via and . If we let be the original samples and

be the subsampled

dataset, we must show

Since the are sampled without replacement (i.e. from directly), and and , we find that for

, and thus

In particular, we see that the

equality (44) holds:

The statement (45) follows from

analogous arguments.

The proof of Lemma 11 follows from that of

Lemmas 12

and 13. We first claim

that

(46)

The proofs of both claims similar, so we focus on proving the second

statement. Using the inequality and

Lemma 13, we see

that

(47)

We now bound the first two terms in

inequality (47). Applying

the Cauchy-Schwarz inequality and Lemma 7, the

first term can be upper bounded as

where the order notation subsumes the logarithmic factor in the

dimension. Since is linear, the second term in the

inequality (47) may be bounded

completely analogously as it involves the outer product .

Recalling the

bound (47), we have thus shown that

or . The proof of the first equality in

equation (46) is entirely analogous.

We now apply the equalities (46) to obtain the

result of the lemma. We have

Using the inequality

for any ,

we have

for any . Taking and , we obtain

, so applying the triangle inequality,

we have

(48)

Since is a sub-sampled version of , algebraic manipulations yield

(49)

Combining equations (48)

and (49), we obtain the

desired bound (40).

We begin by recalling that if denotes the output

of performing stochastic gradient on one machine, then

from the inequality (24) we have the upper bound

To prove the error bound (21), it thus suffices to

prove the inequalities

(50a)

(50b)

Before proving the theorem, we introduce some notation and a few

preliminary results. Let be the gradient of the sample in stochastic

gradient descent, where we consider running SGD on a single

machine. We also let

denote the projection of the point onto the domain .

We now state a known result, which gives sharp rates on the

convergence of the iterates in stochastic gradient

descent.

Assume that for all . Choosing

for some , for any we have

With these ingredients, we can now turn to the proof of

Theorem 5. Lemma 14 gives

the inequality (50a), so it remains to prove

that has the smaller

bound (50b) on its bias. To that end, recall the

neighborhood in

Assumption E, and note that

since when , we have .

Consequently, an application of the triangle inequality gives

By the definition of the projection and the fact that , we additionally have

Thus, by applying Hölder’s inequality (with the

conjugate choices ) and

Assumption E, we have

(51)

the inequality (51) following from an

application of Markov’s inequality. By applying

Lemma 14, we finally obtain

(52)

Now we turn to controlling the rate at which goes to zero. Let be

shorthand for the loss evaluated on the data point. By

defining

a bit of algebra yields

Since belongs to the -field of , the Hessian is (conditionally)

independent of and

(53)

If , then Taylor’s theorem implies that is the

Lagrange remainder

where for

some .

Applying Assumption E and

Hölder’s inequality, we find that

since is conditionally independent of ,

On the other hand, when , we have

the following sequence of inequalities:

Here step (i) follows from Hölder’s inequality (again applied with

the conjugates ); step (ii) follows from

Jensen’s inequality, since ;

and step (iii) follows from Markov’s inequality, as in the

bounds (51)

and (52). Combining our two bounds

on , we find that

(54)

By combining the expansion (53) with the

bound (54), we find that

Using the earlier

bound (52), this inequality

then yields

We now complete the proof via an inductive argument using our immediately

preceding bounds. Our reasoning follows a similar induction given

by Rakhlin et al. (2012).

First, note that by strong convexity and

our condition that , we

have

whenever . Define ; then for we obtain

(55)

For shorthand, we define two intermediate variables

Inequality (55) then implies the inductive

relation . Now we show that

by defining , we have

. Indeed, it is clear that .

Using the inductive hypothesis, we then have

We first prove that under the conditions given in the lemma statement,

the function is -strongly convex over

the ball around . Indeed, fix ,

then use the triangle inequality to conclude that

Here we used Assumption C on the first term

and the fact that the event holds on the second. By our

choice of , this

final term is bounded by . In particular, we have

which proves that is -strongly convex

on the ball .

In order to prove the conclusion of the lemma, we argue

that since is (locally) strongly convex, if the function has small

gradient at the point , it must be the case that the

minimizer of is near . Then we

can employ reasoning similar to standard analyses of optimality for

globally strongly convex functions (e.g. Boyd and Vandenberghe (2004), Chapter 9).

By definition of (the local) strong convexity on the set , for any

, we have

Rewriting this inequality, we find that

Dividing each side by , then noting that we may

set for any , we have

Of course, by assumption, so

we find that for any we have the strict inequality

the last inequality following from the definition of . Since this

holds for any , if , we may set , which would yield a contradiction. Thus, we have

, and by our earlier

inequalities,

Dividing by completes the proof.

F Moment bounds

In this appendix, we state two useful moment bounds, showing how they

combine to provide a proof of Lemma 7.

The two lemmas are a vector and a non-commutative matrix variant of

the classical Rosenthal inequalities. We begin with the case of

independent random vectors:

Let be independent and symmetrically

distributed Hermitian matrices. Then

Equipped with these two auxiliary results, we turn to our proof

Lemma 7. To prove the first

bound (29a), let and note

that by Jensen’s inequality, we have

Again applying Jensen’s inequality, . Thus by recalling the definition

and applying the inequality

The proof of the bound (29b) requires a very

slightly more delicate argument involving symmetrization step.

Define matrices . If are i.i.d. Rademacher variables independent of , then

for any integer in the interval , a standard

symmetrization argument (e.g. Ledoux and Talagrand, 1991, Lemma 6.3) implies

that

(56)

Now we may apply Lemma 16, since the

matrices are Hermitian and symmetrically

distributed; by expanding the

definition of the , we find that

Since the are i.i.d., we have

by Jensen’s inequality, since

for semidefinite .

Finally, noting that

The proof follows from a slightly more careful application of the Taylor

expansion (26). The starting point in our

proof is to recall the success events (25) and the joint

event . We begin by

arguing that we may focus on the case where holds. Let denote

the right hand side of the equality (41)

except for the remainder term. By

Assumption C, we follow

the bound (30) (with )

to find that

so we can focus on the case where the joint event

does occur.

Defining for notational

convenience, on we have that for some , with

,

Now, we recall the definition , the

Hessian of the risk at the optimal point, and solve for the error

to see that

(57)

on the event .

As we did in the proof of Theorem 1, specifically

in deriving the recursive equality (32), we may

apply the expansion (28) of to obtain a clean asymptotic expansion of

using (57). Recall the

definition for

shorthand here (as in the expansion (28),

though we no longer require ).

First, we claim that

(58)

To prove the above expression, we add and subtract (and drop for simplicity).

We must control

To begin, recall that . By Assumption D, on

the event we have that is -Lipschitz, so defining , we have

by Hölder’s inequality and Lemma 8. The

remaining term we must control is the derivative difference

. Define the random vector-valued function

, and let denote its th

coordinate. Then by definition we have

Therefore, by the Cauchy-Schwarz inequality and the fact that

,