Efficient implementation of Markov chain Monte Carlo when using an unbiased likelihood estimator

Efficient implementation of Markov chain Monte Carlo when using an unbiased likelihood estimator

Abstract

When an unbiased estimator of the likelihood is used within a Metropolis–Hastings chain, it is necessary to trade off the number of Monte Carlo samples used to construct this estimator against the asymptotic variances of averages computed under this chain. Many Monte Carlo samples will typically result in Metropolis–Hastings averages with lower asymptotic variances than the corresponding Metropolis–Hastings averages using fewer samples. However, the computing time required to construct the likelihood estimator increases with the number of Monte Carlo samples. Under the assumption that the distribution of the additive noise introduced by the log-likelihood estimator is Gaussian with variance inversely proportional to the number of Monte Carlo samples and independent of the parameter value at which it is evaluated, we provide guidelines on the number of samples to select. We demonstrate our results by considering a stochastic volatility model applied to stock index returns.

Keywords: Intractable likelihood, Metropolis-Hastings algorithm, Particle filter, Sequential Monte Carlo, State-space model.

1 Introduction

The use of unbiased estimators within the Metropolis–Hastings algorithm was initiated by Lin et al. (2000), with a surge of interest in these ideas since their introduction in Bayesian statistics by Beaumont (2003). In a Bayesian context, an unbiased likelihood estimator is commonly constructed using importance sampling as in Beaumont (2003) or particle filters as in Andrieu et al. (2010). Andrieu & Roberts (2009) call this method the pseudo-marginal algorithm, and establish some of its theoretical properties.

Apart from the choice of proposals inherent to any Metropolis–Hastings algorithm, the main practical issue with the pseudo-marginal algorithm is the choice of the number, , of Monte Carlo samples or particles used to estimate the likelihood. For any fixed , the transition kernel of the pseudo-marginal algorithm leaves the posterior distribution of interest invariant. Using many Monte Carlo samples usually results in pseudo-marginal averages with asymptotic variances lower than the corresponding averages using fewer samples, as established by Andrieu & Vihola (2014) for likelihood estimators based on importance sampling. Empirical evidence suggests this result also holds when the likelihood is estimated by particle filters. However, the computing cost of constructing the likelihood estimator increases with . We aim to select so as to minimize the computational resources necessary to achieve a specified asymptotic variance for a particular pseudo-marginal average. This quantity, which is referred to as the computing time, is typically proportional to times the asymptotic variance of this average, which is itself a function of . Assuming that the distribution of the additive noise introduced by the log-likelihood estimator is Gaussian, with a variance inversely proportional to and independent of the parameter value at which it is evaluated, this minimization was carried out in Pitt et al. (2012) and in Sherlock et al. (2013). However, Pitt et al. (2012) assume that the Metropolis–Hastings proposal is the posterior density, whereas Sherlock et al. (2013) relax the Gaussian noise assumption, but restrict themselves to an isotropic normal random walk proposal and assume that the posterior density factorizes into independent and identically distributed components and .

Our article addresses a similar problem but considers general proposal and target densities and relaxes the Gaussian noise assumption. In this more general setting, we cannot minimize the computing time, and instead minimize explicit upper bounds on it. Quantitative results are presented under a Gaussian assumption. In this scenario, our guidelines are that should be chosen such that the standard deviation of the log-likelihood estimator should be around when the Metropolis–Hastings algorithm using the exact likelihood is efficient and around when it is inefficient. In most practical scenarios, the efficiency of the Metropolis–Hastings algorithm using the exact likelihood is unknown as it cannot be implemented. In these cases, our results suggest selecting a standard deviation around .

2 Metropolis–Hastings method using an estimated likelihood

We briefly review how an unbiased likelihood estimator may be used within a Metropolis–Hastings scheme in a Bayesian context. Let be the observations and the parameters of interest. The likelihood of the observations is denoted by and the prior for admits a density with respect to Lebesgue measure so the posterior density of interest is . We slightly abuse notation by using the same symbols for distributions and densities.

The Metropolis–Hastings scheme to sample from simulates a Markov chain according to the transition kernel

| (1) |

where

| (2) |

with . This Markov chain cannot be simulated if is intractable.

Assume is intractable, but we have access to a non-negative unbiased estimator of , where represents all the auxiliary random variables used to obtain this estimator. In this case, we introduce the joint density on , where

| (3) |

This joint density admits the correct marginal density , because is unbiased. The pseudo-marginal algorithm is a Metropolis–Hastings scheme targeting (3) with proposal density , yielding the acceptance probability

| (4) |

for a proposal . In practice, we only record instead of . We follow Andrieu & Roberts (2009) and Pitt et al. (2012) and analyze this scheme using additive noise, , in the log-likelihood estimator, rather than . In this parameterization, the target density on becomes

| (5) |

where is the density of when and the transformation is applied.

To sample from , we could use the scheme previously described to sample from and then set . We can equivalently use the transition kernel

| (6) | ||||

where

| (7) |

is (4) expressed in the new parameterization. Henceforth, we make the following assumption.

Assumption 1.

The noise density is independent of and is denoted by .

Under this assumption, the target density (5) factorizes as , where

| (8) |

Assumption 1 allows us to analyze in detail the performance of the pseudo-marginal algorithm. This simplifying assumption is not satisfied in practical scenarios. However, in the stationary regime, we are concerned with the noise density at values of the parameter which arise from the target density and the marginal density of the proposals at stationarity . If the noise density does not vary significantly in regions of high probability mass of these densities, then we expect this assumption to be a reasonable approximation. In Section 4, we examine experimentally how the noise density varies against draws from and .

3 Main results

3.1 Outline

This section presents the main contributions of the paper. All the proofs are in Appendix 1 and in the Supplementary Material. We minimize upper bounds on the computing time of the pseudo-marginal algorithm, as discussed in Section 1. This requires establishing upper bounds on the asymptotic variance of an ergodic average under the kernel given in (6). To obtain these bounds, we introduce a new Markov kernel , where

| (9) | ||||

and

| (10) | ||||

| (11) |

As and are reversible with respect to and the acceptance probability (10) is always smaller than (7), an application of the theorem in Peskun (1973) ensures that the variance of an ergodic average under is greater than or equal to the variance under . We obtain an exact expression for the variance under the bounding kernel and simpler upper bounds by exploiting a non-standard representation of this variance, the factor form of the acceptance probability (10) and the spectral properties of an auxiliary Markov kernel.

3.2 Inefficiency of Metropolis–Hastings type chains

This section recalls and establishes various results on the integrated autocorrelation time of Markov chains, henceforth referred to as the inefficiency. In particular, we present a novel representation of the inefficiency of Metropolis–Hastings type chains, which is the basic component of the proof of our main result.

Consider a Markov kernel on the measurable space , where is the Borel -algebra on . For any measurable real-valued function , measurable set and probability measure , we use the standard notation: , and for , , with . We introduce the Hilbert spaces

equipped with the inner product . A -invariant and -irreducible Markov chain is said to be ergodic; see Tierney (1994) for the definition of -irreducibility. The next result follows directly from Kipnis & Varadhan (1986) and Theorem 4 and Corollary 6 in Häggström & Rosenthal (2007).

Proposition 1.

Suppose is a -reversible and ergodic Markov kernel. Let be a stationary Markov chain evolving according to and let be such that where . Write for the autocorrelation at lag of and for the associated inefficiency. Then,

-

(i)

there exists a probability measure on such that the autocorrelation and inefficiency satisfy the spectral representations

(12) -

(ii)

if , then as

(13) in distribution, where denotes the normal distribution with mean and variance .

When estimating , equation (13) implies that we need approximately samples from the Markov chain to obtain an estimator of the same precision as an average of independent draws from .

We consider henceforth a -reversible kernel given by

where the proposal kernel is selected such that , is the acceptance probability and we assume there does not exist an such that . We refer to as a Metropolis–Hastings type kernel since it is structurally similar to the Metropolis–Hastings kernel, but we do not require to be the Metropolis–Hastings acceptance probability. This generalization is required when studying the kernel as the acceptance probability in (10) is not the Metropolis–Hastings acceptance probability.

Let be a Markov chain evolving according to . We now establish a non-standard expression for derived from the associated jump chain representation of . In this representation, corresponds to the sequence of accepted proposals and the associated sojourn times, that is etc., with . Some properties of this jump chain are now stated; see Lemma 1 in Douc & Robert (2011).

Lemma 1.

Let be -irreducible. Then for any and is a Markov chain with a -reversible transition kernel , where

| (14) |

with

| (15) |

and denotes the geometric distribution with parameter .

The next proposition gives the relationship between and .

Proposition 2.

Assume that and are ergodic, that and that . Then ,

| (16) |

and .

Lemma 1 and Proposition 2 are used in Section 3.3 to establish a representation of the inefficiency for the kernel .

We conclude this section by establishing some results on the positivity of the Metropolis–Hastings kernel and its associated jump kernel. Recall that a -invariant Markov kernel is positive if for any . If is reversible, then positivity is equivalent to for all , where is the spectral measure, and it implies that ; see, for example, Geyer (1992). The positivity of the jump kernel associated with a Metropolis-Hastings kernel is useful here as several bounds on the inefficiency established subsequently require the spectral measure of to be supported on . We now give sufficient conditions ensuring this property by extending Lemma 3.1 of Baxendale (2005). This complements results of Rudolf & Ullrich (2013).

Proposition 3.

Assume is the Metropolis–Hastings acceptance probability and . If is -irreducible, then and are both positive if one of the following two conditions is satisfied:

-

(i)

is a -reversible kernel with , is absolutely continuous with respect to , and there exists such that , where is a measure on

-

(ii)

and there exists such that , where is a measure on

Remark 1.

Condition (i) is satisfied for an independent proposal by taking , and It is also satisfied for autoregressive positively correlated proposals with normal or Student-t innovations. Condition (ii) holds if is a symmetric random walk proposal whose increments are multivariate normal or Student-t.

3.3 Inefficiency of the bounding chain

This section applies the results of Section 3.2 to establish an exact expression for . The next lemma shows that is an upper bound on .

Lemma 2.

The kernel is -reversible and for any .

In practice, we are only interested in functions . To simplify notation, we write in this case, instead of introducing the function satisfying for all and writing . Proposition 2 shows that it is possible to express as a function of the inefficiency of its jump kernel , which is particularly useful as admits a simple structure.

Lemma 3.

Assume is -irreducible. The jump kernel associated with is

| (17) |

where

| (18) |

The kernel is reversible with respect to and the kernel is positive and reversible with respect to , where

If is ergodic, , and is ergodic, then , , and

| (19) |

Additionally, ensures that is geometrically ergodic and .

The following theorem provides an expression for which decouples the contributions of the parameter and the noise components. The proof exploits the relationships between and , and and the spectral representation (12) of . This spectral representation admits a simple structure due to the product form (17) of .

Theorem 1.

Let . Assume that , , are ergodic with . Then, and

| (20) |

Remark 2.

Theorem 1 requires and to be ergodic. The following proposition, generalizing Theorem 2.2 of Roberts & Tweedie (1996), provides sufficient conditions ensuring this.

Proposition 4.

Suppose is bounded away from and on compact sets, and there exist and such that, for every ,

| (21) |

Then and are ergodic.

3.4 Bounds on the relative inefficiency of the pseudo-marginal chain

For any kernel , we define the relative inefficiency , which measures the inefficiency of compared to that of . This section provides tractable upper bounds for . From Lemma 2, , but the expression of that follows from Theorem 1 is intricate and depends on the autocorrelation sequence , as well as other terms. The next corollary provides upper bounds on that depend only on . To simplify the notation, we write .

Corollary 1.

Under the assumptions of Theorem 1,

-

1.

, where

(22) -

2.

if, in addition, , then , where

(23)

Remark 3.

The bounds above are tight in two cases. First, if , then , , . Second, if , then .

We now provide upper bounds on and lower bounds on in terms of .

Corollary 2.

Under the assumptions of Theorem 1,

-

1.

, where

(24) -

2.

, where

(25) -

3.

if is positive, then , where

(26) -

4.

, where

(27) and as .

Proposition 3 gives sufficient conditions for to be positive. Section 3.5 discusses these bounds in more detail.

3.5 Optimizing the computing time under a Gaussian assumption

This section provides quantitative guidelines on how to select the standard deviation of the noise density, under the following assumption.

Assumption 2.

The noise density is , where is a univariate normal density with mean and variance .

Assumption 2 ensures that as required by the unbiasedness of the likelihood estimator. Consider a time series , where the likelihood estimator of is computed through a particle filter with particles. Theorem 1 of an unpublished technical report (arXiv:1307.0181) by Bérard et al. shows that, under regularity assumptions, the log-likelihood error is distributed according to a normal density with mean and variance as , for . Hence, in this important scenario, the noise distribution satisfies approximately the form specified in Assumption 2 for large and the variance is asymptotically inversely proportional to the number of samples. This assumption is also made in Pitt et al. (2012), where it is justified experimentally. Section 4 below provides additional experimental results.

The next result is Lemma 4 in Pitt et al. (2012) and follows from Assumption 2, equation (8) and Remark 2. We now make the dependence on explicit in our notation.

Corollary 3.

Under Assumption 2, ,

where and is the standard Gaussian cumulative distribution function. Additionally, .

The terms , and , appearing in the bounds of Corollaries 1 and 2, do not admit analytic expressions, but can be computed numerically. We note that is finite, and thus by Lemma 3 is also finite. Consequently, for specific values of and , these bounds can be calculated.

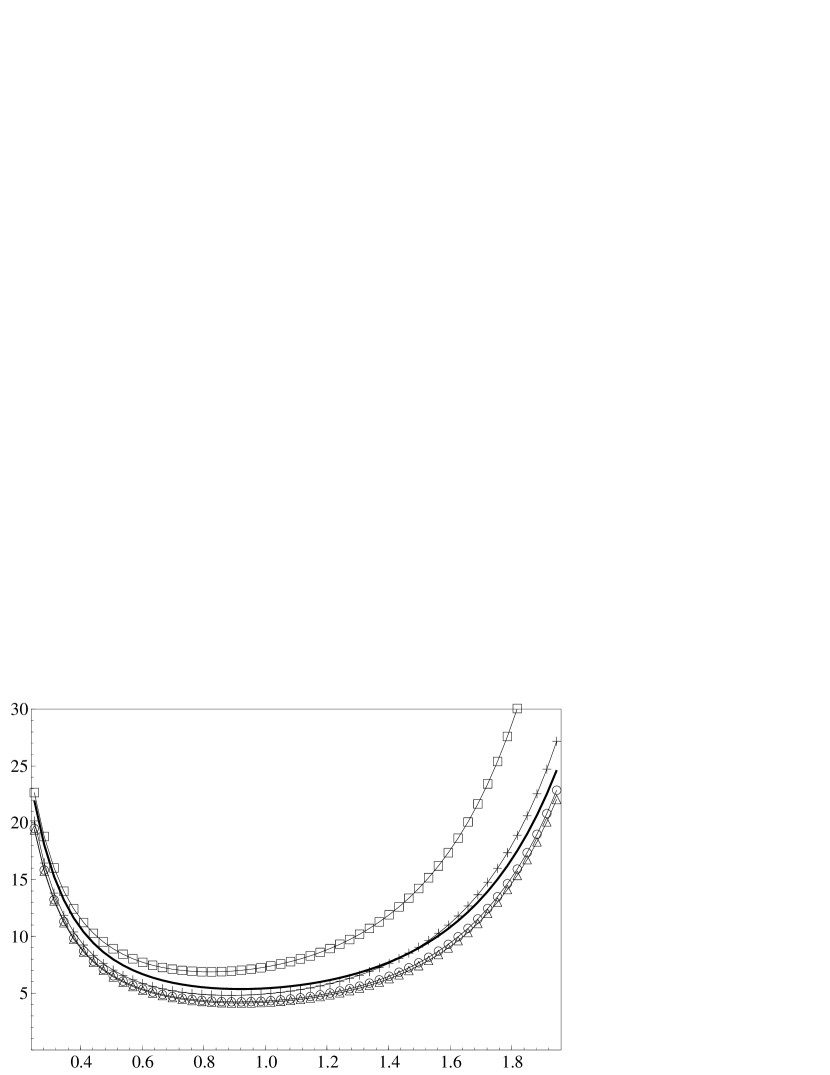

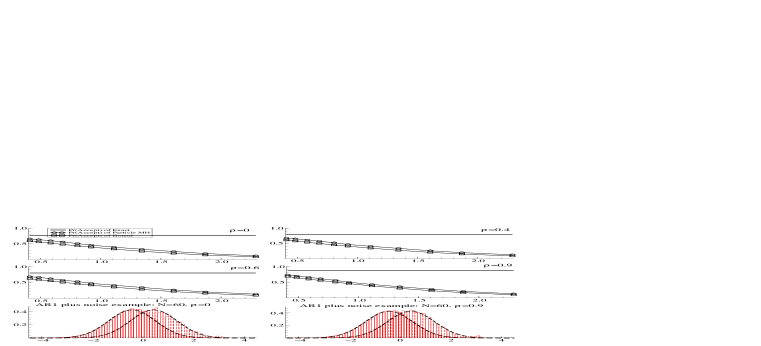

We now use these bounds to guide the choice of . The quantity we aim to minimize is the relative computing time for defined as because is usually approximately proportional to the number of samples used to estimate the likelihood and the computational cost at each iteration is typically proportional to , at least in the particle filter scenario described previously. We define similarly. As is intractable, we instead minimize the upper bounds , for . We similarly define the quantities and , which bound from below. Figure 1 plots these bounds against for different values of and .

Prior to discussing how these results guide the selection of , we outline some properties of the bounds. First, as the corresponding inefficiency increases, the upper bounds displayed in Fig. 1 become flatter as functions of , and the corresponding minimizing argument increases. This flattening effect suggests less sensitivity to the choice of for the pseudo-marginal algorithm. Second, for given , all the upper bounds are decreasing functions of the corresponding inefficiency, which suggests that the penalty from using the pseudo-marginal algorithm drops as the exact algorithm becomes more inefficient. Third, in the case discussed in Remark 2, where , so that , we obtain . Fourth, agrees with the lower bound as as indicated by Part 2 of Corollary 2. In this case, these two bounds, as well as , are sharp for . Fifth, is sharper than for , but requires a mild additional assumption.

Relative computing time against for different inefficiencies of the exact chain.

Relative computing time against for different inefficiencies of the exact jump chain.

As the likelihood is intractable, it is necessary to make a judgment on how to choose , because and are unknown and cannot be easily estimated. Consider two extreme scenarios. The first is the perfect proposal , so that by Corollary 3 and Remark 2, , which we denote by , is minimized at . The second scenario considers a very inefficient proposal corresponding to Part 4 of Corollary 2 so that , which is minimized at . If we choose over in scenario , then rises from to . Conversely, if we choose over in scenario , the relative computing time rises from to . This suggests that the penalty in choosing the wrong value is much more severe if we incorrectly assume we are in scenario than if we incorrectly assume we are in scenario . This is because as increases, is very flat relative to , as a function of . In practice, choosing slightly greater than appears sensible. For example, a value of leads to an increase in from the minimum value of to and an increase in from the minimum value of to . In Appendix 2, we compute lower and upper bounds for the minimizing argument of for various values of .

Some caution should be exercised in interpreting these results as the lower bounds apply to , but not in general to . Similarly, whilst and the lower bounds become exact for as , they only provide upper bounds for .

However, in an important class of problems is large, for instance when is a random walk proposal with small step size. In this case, we expect that as the step size gets smaller the acceptance probability of will tend towards unity and hence asymptotically . This suggests that, for small enough step size, .

The numerical results in this section are based on Assumption 2. However, the bounds on the relative inefficiences of and presented in Corollaries 1 and 2 can be calculated for any other noise distribution , subject to . These bounds can in turn be used to construct corresponding bounds on the relative computing times of and , provided that an appropriate penalization term is employed to account for the computational effort of obtaining the likelihood estimator.

3.6 Discussion

We now compare informally the bound of Part 4 of Corollary 2 to the results in Sherlock et al. (2013). These authors make Assumption 1, assume that the target factorises into independent and identically distributed components and that the proposal is an isotropic Gaussian random walk of jump size . In the Gaussian noise case, for where , their results and a standard calculation with their diffusion limit, suggest that as the relative inefficiency satisfies

| (28) |

where the expression for is given by equations (3.3) and (3.4) of Sherlock et al. (2013). We observe that converges to as . This is unsurprising. As , we conjecture that in this scenario the conditions of Part 4 of Corollary 2 apply, in particular that for any . Therefore, in this case, . As , we have informally that , so that it is reasonable to conjecture that . If one of these limits holds uniformly, then .

4 Application

4.1 Stochastic volatility model and pseudo-marginal algorithm

This section examines a multivariate partially observed diffusion model, which was introduced by Chernov et al. (2003), and discussed in Huang & Tauchen (2005). The regularly observed log price evolves according to,

and the leverage parameters corresponding to the correlations between the driving Brownian motions are corr and corr. The function s- is a spliced exponential function to ensure non-explosive growth, see Huang & Tauchen (2005). The two components for volatility allow for quite sudden changes in log price whilst retaining long memory in volatility. We note that the Brownian motion of the price process may be expressed as , where , and . Here is an independent Brownian motion. Suppose the log prices are observed at equally spaced times and for any which gives returns , for . The distribution of these returns conditional upon the volatility paths and the driving processes and is available in closed form as where

| (29) |

and s-. An Euler scheme is used to approximate the evolution of the volatilities and by placing a number, , of latent points between and . The volatility components are denoted by and . For notational convenience, the start and end points are set to and and similarly for . These latent points are evenly spaced in time by . The equation for the Euler evolution, starting at and , is

where and . Conditional upon these trajectories and the innovations, the distribution of the returns has a closed form so that where , and are the Euler approximations to the corresponding expression in (29).

We consider daily returns, , from the S&P 500 index. Bayesian inference is performed on the -dimensional parameter vector to which we assign a vague prior. We simulate from the posterior density using the pseudo-marginal algorithm where the likelihood is estimated using the bootstrap particle filter with particles. A multivariate Student-t random walk proposal on the parameter components transformed to the real line is used.

4.2 Empirical results for the error of the log-likelihood estimator

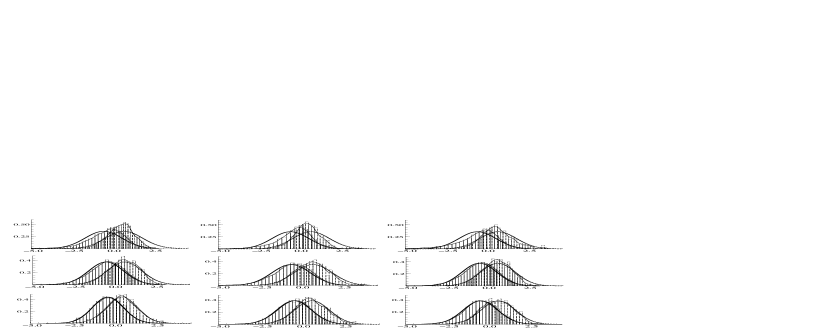

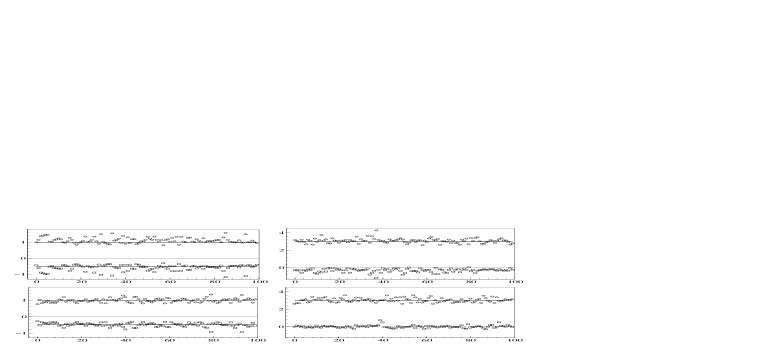

This section investigates empirically Assumptions 1 and 2 by examining the behaviour of for , 300 and 2700. Corresponding values of are selected in each case to ensure that the variance of evaluated at the posterior mean is approximately unity. We use in the Euler scheme.

The three plots on the left of Fig. 2 display the histograms corresponding to the density of for denoted , which is obtained by running particle filters at this value. As is unknown, it is estimated by averaging these estimates. The Metropolis–Hastings algorithm is then used to obtain the histograms corresponding to . We overlay on each histogram a kernel density estimate together with the corresponding assumed density, or , where is the sample variance of over the particle filters. For , there is a discrepancy between the assumed Gaussian densities and the true histograms representing and . In particular, whilst is well approximated over most of its support, it is slightly lighter tailed than the assumed Gaussian in the right tail and much heavier tailed in the left tail. This translates into a smaller discrepancy between and and a higher acceptance rate for the pseudo-marginal algorithm than the Gaussian assumption suggests. For and , the assumed Gaussian densities are very accurate.

We also examine when is distributed according to . We record samples from , for , 300 and 2700. For each of these samples, we run the particle filter times in order to estimate the true likelihood at these values. The resulting histograms, corresponding to the densities and , are displayed in the middle column of Fig. 2. We similarly examine the density of when is distributed according to the marginal proposal density in the stationary regime . Here is a multivariate Student-t random walk proposal, with step size proportional to . The right hand column of Fig. 2 shows the resulting histograms. In both scenarios, Assumptions 1 and 2 are problematic for as is not close to being Gaussian as is too small for the central limit theorem to provide a good approximation. Moreover, since is small, and are relatively diffuse. Consequently, is not close to marginalized over or . For and , the assumed densities and are close to the corresponding histograms and Assumptions 1 and 2 appear to capture reasonably well the salient features of the densities associated with . In particular, the approximation suggested by the central limit theorem becomes very good. Additionally, and are sufficiently concentrated to ensure that the variance of as a function of exhibits little variability.

4.3 Empirical results for the pseudo-marginal algorithm

We apply the pseudo-marginal algorithm with , and various values of . The standard deviation of is evaluated by Monte Carlo simulations, where is the posterior mean. For each value of , we compute the inefficiencies, denoted by IF, and the corresponding approximate relative computing times, denoted by RCT, of all parameter components. The quantity RCT is computed as divided by the inefficiency of when , the latter being an approximation of the inefficiency of . The results are very similar for all parameter components and so, for ease of presentation, Fig. 3 shows the average quantities over the components. For most parameters, the optimal value for is between and , corresponding to and . The results agree with the bound in Section 3.5. This can be partly explained because the inefficiencies associated with for are large, suggesting that the inefficiencies associated with are large.

As all the bounds in the paper are based on , it is useful to assess the discrepancy between and . One approach to explore this discrepancy is to examine the marginal acceptance probability under against as varies. Using the acceptance criterion (10) of , we obtain under Assumptions 1 and 2 that . If and are close in the sense of having similar marginal acceptance probabilities, then we expect to have a similar shape as its lower bound where is approximated using with . For this model, the two functions on either side of the inequality, displayed in Fig. 3, are similar.

Acknowledgements

The authors would like to thank the editor, the associate editor and the reviewers for their comments which helped to improve the paper significantly. Arnaud Doucet was partially supported by EPSRC and Robert Kohn was partially supported by an ARC Discovery grant.

Appendix 1

Proof of Lemma 2.

Proof of Theorem 1.

Without loss of generality, let . By Theorem 6 of Andrieu & Vihola (2012), and, by Lemma 2, , where by assumption. Hence, and Proposition 2 applied to yields that and

| (30) |

Since the assumptions of Lemma 3 are satisfied, we can substitute (30) into (19) to obtain

| (31) |

We now provide a spectral representation for . With ,

| (32) | ||||

and, as and are reversible, the following spectral representations, as in (12), hold

| (33) |

where we define , and to simplify notation. Using , we can rewrite (32) as

| (34) | ||||

where the second expression is finite since and

| (35) |

Rearranging (34), we obtain

| (36) |

with

| (37) |

By substituting (36) into (31), we obtain the result since

| (38) |

∎

Proof of Corollary 1.

Dividing (38) by , we obtain

| (39) |

where is the quantity in (36) and can be expressed in terms of , defined in (35), as

Lemma 3 ensures that the kernel is positive, implying that . Hence,

We can now bound from above by

| (40) | ||||

where we have used the identity . The last inequality is established by noting that and are non-negative. Substituting the expression into (39) establishes Part 1. To establish the inequality of Part 2, we note that if , then (40) is bounded from above by

∎

Proof of Corollary 2.

We establish the upper bound of Part 1 by first noting that (40) implies

with is the quantity in (36), given by (35) and . Upon substituting into (39), we obtain

and, after further manipulations,

as from Proposition 2.

To establish the upper bound of Part 2, we use that, in the right hand side of the equality of (39), the term defined in (37) and appearing in satisfies the inequality

| (41) |

where , by assumption. Therefore, upon substituting into (39), we obtain

as .

To establish the inequality of Part 3, we combine (36) and (39) to obtain

| (42) | ||||

The first inequality follows because the identity for given in (41) shows that when is positive. The second inequality follows from .

From (39), we have as the second and third terms on the left hand side of the inequality (42) are both positive. This establishes the inequality of Part 4. We examine the limit of as , again noting that . Using the inequality for given by (41) and the fact that by Lemma 3, we obtain the limiting form, as given by (27) for . ∎

Appendix 2

We exploit the two upper bounds and , together with the lower bound , in order to find an interval where the optimal value for lies. We consider how this interval varies as increases. To do this, we compute the interval where lies below the minimum of , and . Table 1 displays this interval together with the minimum of the two upper bounds and the minimum of the lower bound. It is straightforward to see that is contained in this interval and is contained in the corresponding interval in Table 1. It is apparent that the intervals tighten as increases. Similarly the endpoints of the interval containing both decrease whilst the lower endpoint of the interval containing increases.

| 1 | 10 | 25 | 100 | 1000 | |

|---|---|---|---|---|---|

| (3.201, 5.327) | (2.020, 2.256) | (1.773, 1.876) | (1.595, 1.625) | (1.518, 1.522) | |

| (0.548, 1.572) | (1.018, 1.598) | (1.205, 1.658) | (1.421, 1.730) | (1.607, 1.730) |

Supplementary Material

Appendix A Contents

This supplement provides some technical proofs and an additional example for the paper “Efficient implementation of Markov chain Monte Carlo when using an unbiased likelihood estimator”. Section B presents the proof of Proposition 2. Section C presents the proofs of Propositions 3 and 4 and Lemmas 1 and 3. Section D presents some auxiliary technical results. Section E illustrates the upper bound on the inefficiency of Part 4 of Corollary 2 and compares it to the results in Sherlock et al. (2013). Section F applies the pseudo-marginal algorithm to a linear Gaussian state-space model and presents additional simulation results for the stochastic volatility model discussed in the main paper. Section G explains how the bounds on the inefficiency introduced in Section 3.5 of the main paper are computed.

All code was implemented in the Ox language with pre-compiled C code for computationally intensive routines.

Appendix B Proof of Proposition 2

The proof of Proposition 2 relies on Lemmas 5 to 8, which are given below. Lemmas 5 to 7 establish that and whenever . To prove this result, we define the map that sends the functional to as a linear operator between two Hilbert spaces, and defined below. The space , respectively , corresponds to the set of functions having finite inefficiencies under , respectively under . We then exploit the structure of the Metropolis–Hastings type kernel to prove that this linear operator is bounded on a dense subspace , which allows us to extend the operator to . The proof is then completed by checking that the unique extension constructed this way is the one required. Lemma 8 is a general result on the central limit theorem for reversible and ergodic Markov chains which are not started in their stationary regime. The proof of Proposition 2 uses these preliminary results to establish the identity of interest.

Using the notation of Proposition 2, we write , for the norm and inner product of , with a similar notation for . By reversibility of and with respect to and respectively, it is easy to check that and are positive, self-adjoint operators on and respectively. By Theorem 13.11 in Rudin (1991), the inverses and are densely defined and self-adjoint. They are also positive, since for any , there exists a function such that , and thus

since is positive. Therefore, by Theorem 13.31 in Rudin (1991), there exists a unique, self-adjoint, positive operator such that . Finally, since is densely defined, so is . Similar considerations show the existence and uniqueness of the positive, self-adjoint operator , which is densely defined on .

We now introduce the inner product spaces and , where

Clearly the space , respectively , corresponds to the set of functions having finite inefficiencies under , respectively under .

Lemma 4.

Let and be ergodic. Then and are Hilbert spaces.

Proof.

Since and are ergodic, the only solutions in and , of , respectively , are almost surely constant with respect to and . If almost surely, then

where is the spectral measure of with respect to the function , and therefore must be an atom at 1, which is impossible as is ergodic; see the proof of Lemma 17 in Häggström & Rosenthal (2007) and Proposition 17.4.1 in Meyn & Tweedie (2009). Since and are injective in and respectively, and must also be injective on the corresponding spaces, because implies . In addition, as mentioned above, these operators are self-adjoint and thus their inverses, and , are densely defined and self-adjoint by Theorem 13.11 in Rudin (1991).

By Theorem 13.9 in Rudin (1991), and are closed operators on and respectively because they are self-adjoint. By Section 13.1 in Rudin (1991), a possibly unbounded operator on a Hilbert space is said to be closed if and only if its graph

is a closed subset of . Equivalently is closed if and implies . In particular, is in the domain of . It follows that and are Hilbert spaces by Proposition 1.4 in Schmüdgen (2012). ∎

Lemma 5.

The linear space

is dense in in the norm induced by .

Proof.

For , we have

where is the spectral measure associated with and . For , define

Then,

The integrand is bounded above by , since implies that , and thus, by dominated convergence, the integral vanishes as . Since is bounded, also vanishes. Therefore, in . In particular, is dense in . ∎

Lemma 6.

If , then and .

Proof.

For , there exists such that

Therefore, , since . Thus, we can define the multiplication operator by .

Let . Then,

because is self-adjoint. Similarly,

where with the finite norm of the operator . Recalling that , we obtain

It follows that is bounded as

Since is dense, given , there is a sequence such that , as . This, in particular, implies that is a Cauchy sequence in , that is

Since and are in , and, from the above calculation,

as . Therefore, forms a Cauchy sequence in ; in particular and are Cauchy in . Since is complete, we have and . Since is a closed operator, we can conclude that

and, in particular, .

To complete the proof, we need to show that . Recall that in implies that . We can then choose a subsequence such that -almost surely. Since is absolutely continuous with respect to , we also have -almost surely.

In addition, we know that in and thus in . Therefore, in . We can now choose a further subsequence such that -almost surely. Since also converges to -almost surely, and is a subsequence of , we conclude that -almost surely. ∎

Lemma 7.

Assume is -reversible and ergodic, and . Let be a Markov chain evolving according to . If , where is absolutely continuous with respect to then, as ,

Proof of Lemma 7.

Let be the associated spectral measure and define . Then,

as by dominated convergence, since by assumption. Hence, equation (4) in Wu & Woodroofe (2004) holds with , where . It is straightforward to check, with calculations similar to the above, that the solution to the approximate Poisson equation given in the proof of Theorem 1.3 in Kipnis & Varadhan (1986),

satisfies equation (5) in Wu & Woodroofe (2004), while equation (1.10) in Kipnis & Varadhan (1986) shows that converges in . Therefore, the conditions of Corollary 2 in Wu & Woodroofe (2004) are satisfied so the statement of the lemma follows from their equation (10); see their comments after this equation. ∎

Proof of Proposition 2.

Let be a Markov chain evolving according to and the associated jump chain representation evolving according to , as defined in Lemma 1. We denote by the law of a Markov chain with initial distribution and transition kernel . By Theorem 1.3 in Kipnis & Varadhan (1986), we have under

| (43) |

where is a square integrable martingale with respect to the natural filtration of , while we have the following convergence in probability

| (44) |

Define . The kernel is ergodic because is ergodic. Hence, almost surely,

| (45) |

The above limit also holds -almost surely, since is absolutely continuous with respect to . We first show that

| (46) |

Let be arbitrary and define the event

By (45), we have . The following inequality holds on the event ,

where is a square integrable martingale with stationary increments. Thus, for any ,

where . The third inequality follows from Doob’s maximal inequality. The last inequality follows because, for any square integrable martingale with stationary increments, holds. This bound is uniform in , and therefore

As is arbitrary,

for any , and therefore (46) holds. Now, by Proposition 1, . By the asymptotic negligibility (44) of and (46), we have by Slutsky’s theorem that

equivalently . Finally, note that for any ,

Therefore, using (43) and Slutsky’s theorem, when . However, this result also holds when , as established in Lemma 7. In particular, the asymptotic variance is the same. Moreover, is reversible and ergodic, while Lemma 6 guarantees that and . Hence, Proposition 1 applied to ensures that the asymptotic variance is also given by the integrated autocovariance time. Equating the two expressions, we obtain

where the equality in the second line follows from the expression of and , given in Lemma 1, and the properties of the geometric distribution. This yields the equality of Proposition 2, which can also be written as

as , implying that . ∎

Appendix C Proofs of other technical results in the main paper

Proof of Lemma 1.

As is -irreducible, it is also -irreducible as it is -invariant; see, for example, Tierney (1994), p. 1759. Hence, for any and with , there exists an such that . As is not concentrated on a single point by assumption, this implies that for any . The rest of the proposition follows directly from Lemma 1 in Douc & Robert (2011). ∎

Proof of Lemma 3.

Equations (17) and (18) and the expressions of their associated invariant distributions follow from a direct application of Lemma 1. The positivity of follows directly from Proposition 3, see Remark 1. We write . By applying Proposition 2 to , we obtain for any that , and

The identity follows easily as and .

To prove the geometric ergodicity of , we follow Meyn & Tweedie (2009, Chapter 15). Notice first that

and consider the set , where and . For any and ,

where

and is the probability measure concentrated on , given by

Hence, is a small set.

To complete the proof of geometric ergodicity of , we check that satisfies a geometric drift condition. Note that for any , and

| (47) |

We have , as established earlier, because by assumption. It follows that the first integral on the right hand side of (47) is bounded. To prove that the second integral is bounded, we use the fact that is a non-increasing function. We have

where , respectively , is the cumulative distribution function of , respectively , so its derivative with respect to is equal to

It follows that the second term on the right hand side of (47) is bounded by

Therefore, for any , there exists such that

for all . We now establish that

As is a non-increasing function, it follows that for

We now show that

The first term on the right hand side of (47) is bounded by

while we have already shown that the second term on right hand side of (47) is bounded.

Hence, we can conclude that, for any , there exists and such that

where .

The inequality now follows because is geometrically ergodic with drift function and . ∎

Proof of Proposition 3.

If for any , then is positive by definition, implying the positivity of as and

For a proposal of the form , Lemma 3.1 in Baxendale (2005) establishes that for any . For a -reversible proposal such that , we have for any ,

by a repeated application of Fubini’s theorem. ∎

Proof of Proposition 4.

Theorem 2.2 in Roberts & Tweedie (1996) establishes the ergodicity of . We extend their argument to prove the ergodicity of . For the ball centred at of radius , we define

which, by assumption, is such that . Then, we have for any and ,

| (48) |

which is strictly positive on . Hence, the -step density part of is strictly positive for all . This establishes the irreducibility of , and hence its ergodicity as it is -invariant. For , we have for any and ,

using calculations as in (48) and the fact that for any , as is irreducible. Finally, the ergodicity of follows, using similar arguments, from the ergodicity of . ∎

Appendix D Statements and proofs of auxiliary technical results

Proposition 5.

Define the relative computing time

where is the relative inefficiency. Using the same assumptions as in Theorem 1,

-

(i)

If , then is minimized at and , .

-

(ii)

If , increases to as

-

(iii)

and are decreasing functions of .

Proof of Proposition 5.

We consider minimizing with respect to . Then,

To obtain Part (i), we note that when . We define . Using Lemma 5 in Pitt et al. (2012), one can verify that is minimized at and that . The numerical values of Part (i) at can be found in Pitt et al. (2012). To obtain Part (ii), we note that

| (49) | ||||

so that if . For the limiting case of Part (ii),

which we can verify numerically is equal to at . For general values of ,

where for . Hence, increases with , which verifies Part (ii). Finally, to obtain Part (iii), it is straightforward to see that

so that and are decreasing functions of , holding constant. ∎

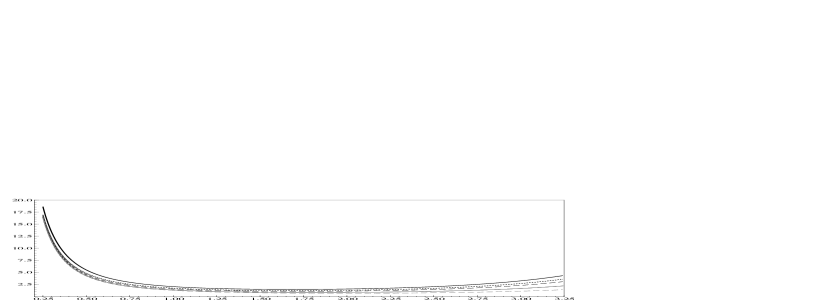

Appendix E Asymptotic upper bound

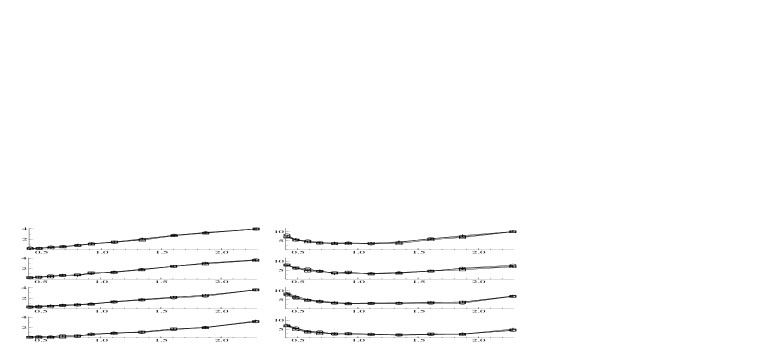

This section illustrates, in the Gaussian noise case, the lower bound on the inefficiency and the exact relative inefficiency obtained in Sherlock et al. (2013) and discussed in Section 3.6 of the main paper. Recall that as and note that as . Figure 4 displays the corresponding relative computing times and . They are very similar in shape as a function of , regardless of , and are also minimized at similar values: is minimized at and is minimized at , and , , , .

Appendix F Simulation results

This section applies the pseudo-marginal algorithm to a linear Gaussian state-space model and presents additional simulation results for the stochastic volatility model discussed in the main paper. The linear Gaussian state-space model we consider is a first order autoregression AR observed with noise. In this case, , and the state evolution is , where and are standard normal and independent. We take , so that the marginal variance of the state is . We consider a series of length , where is assumed known. The parameters of interest are therefore . The analysis is very similar to that of Section 4 of the main paper. However, for this state-space model, the likelihood can be calculated by using the Kalman filter. This facilitates the analysis of sections F.1 and F.2 in two ways. First, in the calculation of the log-likelihood error , the true likelihood term is known rather than estimated. Second, because the likelihood is known, we can directly examine the exact chain and estimate the inefficiency .

F.1 Empirical results for the error of the log-likelihood estimator

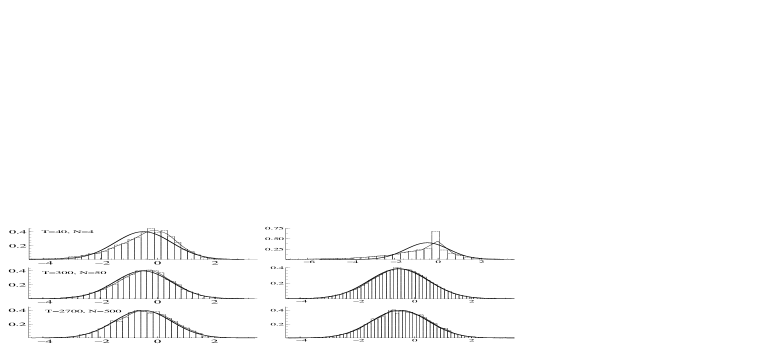

The analysis in this section mirrors that of Section 4.2 of the main paper. We investigate empirically Assumptions 1 and 2 by examining the behaviour of for , and . Corresponding values of are selected in each case to ensure that the variance of evaluated at the posterior mean is approximately unity. The three plots on the left of Fig. 5 display the histograms corresponding to the density of for , which is obtained by running particle filters at this value. We overlay on each histogram a kernel density estimate together with the corresponding assumed density, of Assumption 2, where is the sample variance of over the particle filters. For , there is a slight discrepancy between the assumed Gaussian densities and the true histograms representing . In particular, whilst is well approximated over most of its support, it is heavier tailed in the left tail. For and , the assumed Gaussian densities are very accurate.

We also examine when is distributed according to . We record samples from , for , and . For each of these samples, we run the particle filter times in order to estimate the true likelihood at these values. The resulting histograms, corresponding to the density are displayed on the right panel of Fig. 5. For and , the assumed densities are close to the corresponding histograms and Assumptions 1 and 2 again appear to capture reasonably well the salient features of the densities associated with .

It is important, in examining departures from Assumption 1, to consider the heterogeneity of the conditional density as varies over . In Fig. 6, the conditional moments associated with the density are estimated, based on running the particle filter independently times for each of values of from . We record the estimates of the mean, the variance and the third and fourth central moments at each value of , for and . There is a small degree of variability for around the values that we would expect which are and corresponding to where . This variability reduces as rises to . A small degree variability is expected as these are moments estimated from samples. This lack of heterogeneity explains why the values of , marginalized over , on the right hand side of Fig. 5, are close to for time series of moderate and large length. Figure 7 records a similar experiment for the stochastic volatility model and data considered in Section 4 of the main paper. There is rather more variability as the true value of the likelihood in this case is unknown and has to be estimated. However, the results are similar and the variability again reduces as rises to .

F.2 Empirical results for the pseudo-marginal algorithm

The pseudo-marginal algorithm is applied to data. The true likelihood of the data is computed by the Kalman filter as the model is a linear Gaussian state space model. This allows the exact Metropolis–Hastings scheme to be implemented so that the corresponding inefficiency can be easily estimated. We consider varying so that the standard deviation of the log-likelihood estimator varies. The grid of values that we consider for is , , , , , , , , , , , see Table 2. The value results in .

| IF | IF | IF | pr | |||||

| IF | IF | IF | CT | CT | CT | pr | ||

| IF | IF | IF | pr | |||||

| IF | IF | IF | CT | CT | CT | pr | ||

We transform each of the parameters to the real line so that , where both and are three dimensional vectors, and place a Gaussian prior on centred at zero with a large variance. We use the autoregressive Metropolis proposal

for both the pseudo-marginal algorithm and exact likelihood schemes, where is the mode of the log-likelihood obtained from the Kalman filter and the covariance is the negative inverse of the second derivative of the log-likelihood at the mode. Here denotes a standard multivariate t-distributed random variable with degrees of freedom. We set . We use this autoregressive proposal with the scalar autoregressive parameter chosen as one of , , , . We first apply this proposal, for the four values of , using the known likelihood in the Metropolis scheme and estimate the inefficiency for each of the parameters .

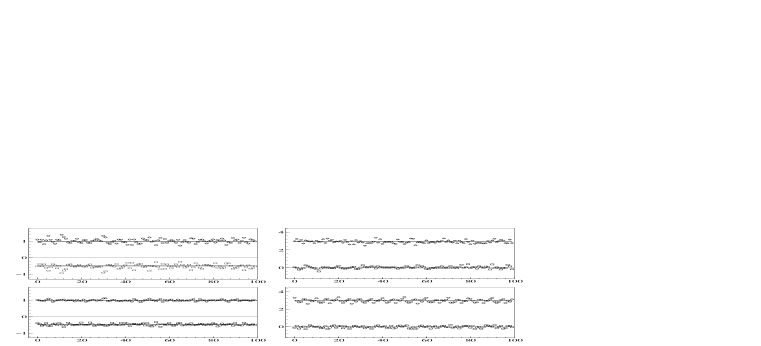

Figure 8 shows the acceptance probability for the pseudo-marginal algorithm against for the four values of the proposal parameter . The lower bound for the acceptance probabilities, as discussed at the end of Section 4.3 of the main paper, is also displayed and there is close correspondence in all cases. The histograms for the accepted and rejected values of , for when , are also displayed. The approximating asymptotic Gaussian densities, with , are superimposed. This figure shows that the approximating densities correspond very closely to the two histograms. It should be noted that these are the marginal values for over the draws from the posterior obtained by running the pseudo-marginal scheme, rather than being based upon a fixed value of the parameters.

Tables 2 and 3 show the pseudo-marginal algorithm results for and . For the independent Metropolis–Hastings proposal, it is clear from Table 2, that the computing time in minimised around or , depending on which parameter is examined, with the corresponding values of being and , supporting the findings that when an efficient proposal is used the optimal value of is close to unity. This is again supported by Fig. 9, for which the relative computing time ( is the top right plot) is shown against . We note that the relative inefficiencies and computing times are straightforward to calculate as the exact chain inefficiencies for the three parameters have been calculated and are given in the top row of Table 2. Table 3 shows the results for the more persistent proposal where . In this case, for all three parameters the optimal value of is around , at which , the corresponding graph of the relative computing time being given by the bottom right of Fig. 9. It is clear that again the findings are consistent with the discussion of 3.5 in the main paper. In particular, as increases, then should increase, and, from Fig. 9, it is clear that the optimal value of increases, the relative computing time decreases for any given . In addition, the relative computing time becomes more flat as a function of as increases.

Appendix G Numerical procedures

Under the Gaussian assumption, Corollary 3 specifies the function and the term can be accurately evaluated using numerical quadrature. This section explains how we numerically evaluate the terms and which appear in the bounds of Corollaries 1 and 2. The inefficiency is finite by Lemma 3, because is finite. The autocorrelations quickly descend to zero as a function of , for all . Hence, it is straightforward to estimate by the appropriate summation of the autocorrelations, and to tabulate it against for use in the bounds of Corollaries 1 and 2. The autocorrelation , for , is similarly tabulated.

From Lemma 3,

so the autocorrelation at lag is

with

| (50) |

The term can be computed by quadrature. The term (50) can be also accurately calculated by Monte Carlo integration, by simulating a large number of i.i.d. samples and then propagating each sample through the transition kernel times to obtain , yielding the estimate

References

- Andrieu et al. (2010) Andrieu, C., Doucet, A. & Holenstein, R. (2010). Particle Markov chain Monte Carlo methods. Journal of the Royal Statistical Society, Series B 72, 1–33.

- Andrieu & Vihola (2014) Andrieu, C. & Vihola, M. (2014). Establishing some order amongst exact approximations of MCMCs, arXiv:1404.6909.

- Andrieu & Vihola (2012) Andrieu, C. & Vihola, M. (2012). Convergence properties of pseudo-marginal Markov Chain Monte Carlo algorithms. Annals of Applied Probability, to appear.

- Andrieu & Roberts (2009) Andrieu, C. & Roberts, G. O. (2009). The pseudo-marginal approach for efficient Monte Carlo computations. The Annals of Statistics 37, 697–725.

- Baxendale (2005) Baxendale, P. (2005). Renewal theory and computable convergence rates for geometrically ergodic Markov chains. The Annals of Applied Probability 15, 700–738.

- Beaumont (2003) Beaumont, M. (2003a). Estimation of population growth or decline in genetically monitored populations. Genetics 164, 1139.

- Chernov et al. (2003) Chernov, M., Gallant, A. R., Ghysels, E. & Tauchen, G. (2003). Alternative models of stock price dynamics. Journal of Econometrics 116, 225–257.

- Douc & Robert (2011) Douc, R. & Robert, C. P. (2011). A vanilla Rao–Blackwellization of Metropolis–Hastings algorithms. The Annals of Statistics 39, 261–277.

- Geyer (1992) Geyer, C. J. (1992). Practical Markov chain Monte Carlo. Statistical Science 7, 473–483.

- Häggström & Rosenthal (2007) Häggström, O. & Rosenthal, J. S. (2007). On variance conditions for Markov chain central limit theorems. Electronic Communications in Probability 12, 454–64.

- Huang & Tauchen (2005) Huang, X. & Tauchen, G. (2005). The relative contribution of jumps to total price variation. Journal of Financial Econometrics 3, 456–499.

- Lin et al. (2000) Lin, L., Liu, K. F. & Sloan, J. (2000). A noisy Monte Carlo algorithm. Physical Review D 61, 074505.

- Peskun (1973) Peskun, P. H. (1973). Optimum Monte–Carlo sampling using Markov chains. Biometrika 60, 607–612.

- Pitt et al. (2012) Pitt, M. K., Silva, R., Giordani, P. & Kohn, R. (2012). On some properties of Markov chain Monte Carlo simulation methods based on the particle filter. Journal of Econometrics 171, 134–151.

- Roberts & Tweedie (1996) Roberts, G. & Tweedie, R. (1996). Geometric convergence and central limit theorems for multidimensional Hastings and Metropolis algorithms. Biometrika 83, 95–110.

- Rudolf & Ullrich (2013) Rudolf, D. & Ullrich, M. (2013). Positivity of hit-and-run and related algorithms. Electronic Communications in Probability 18, 1–8.

- Tierney (1994) Tierney, L. (1994). Markov chains for exploring posterior distributions (with discussion). The Annals of Statistics 21, 1701–62.

- Tierney (1998) Tierney, L. (1998). A note on Metropolis–Hastings kernels for general state spaces. The Annals of Applied Probability 8, 1–9.

- Kipnis & Varadhan (1986) Kipnis, C. & Varadhan, S. (1986). Central limit theorem for additive functionals of reversible Markov processes and applications to simple exclusions. Communications in Mathematical Physics 104, 1–19.

- Meyn & Tweedie (2009) Meyn, S. & Tweedie, R.L. (1991). Markov Chains and Stochastic Stability. Second edition. Cambridge University Press, Cambridge.

- Rudin (1991) Rudin, W. (1991). Functional Analysis. International series in pure and applied mathematics. McGraw-Hill, Inc., New York.

- Sherlock et al. (2013) Sherlock, C., Thiery, A., Roberts, G. & Rosenthal, J. (2013). On the efficiency of pseudo-marginal random walk Metropolis algorithms. ArXiv e-prints URL: http://arxiv.org/abs/1309.7209.

- Schmüdgen (2012) Schmüdgen, K. (2012). Unbounded Self-adjoint Operators on Hilbert Space. Graduate Text in Mathematics, Springer.

- Wu & Woodroofe (2004) Wu, W. & Woodroofe, M. (2004). Martingale approximations for sums of stationary processes. The Annals of Probability 32, 1674–1690.